First Home Owner Loan: Product, Application, and Servicing Analysis

VerifiedAdded on 2020/07/23

|56

|12872

|30

Homework Assignment

AI Summary

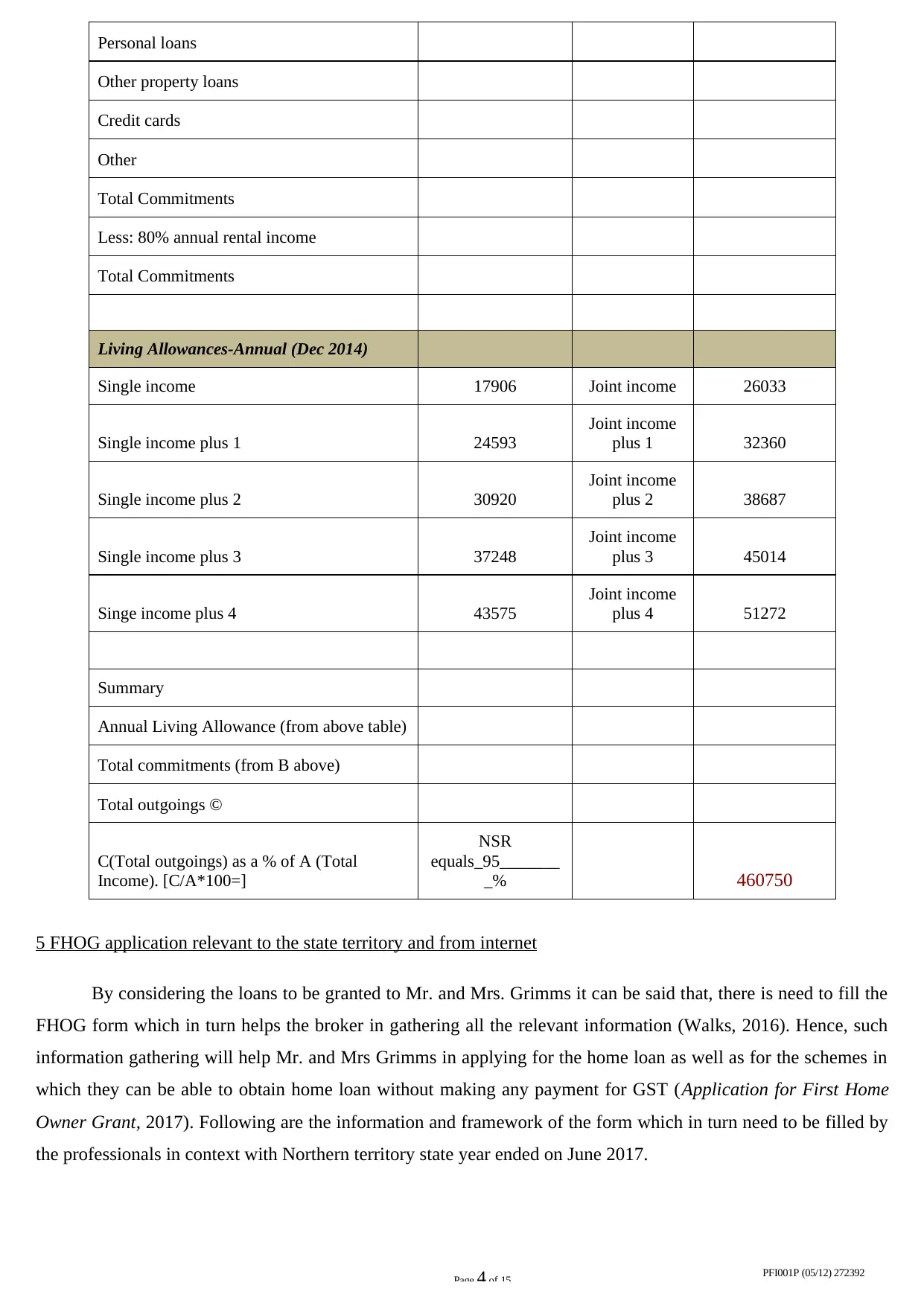

This report provides a comprehensive analysis of a first home owner loan, focusing on the case of Mr. and Mrs. Grimms. It begins with a product recommendation for a First Home Owner Grant (FHOG) to minimize interest payments and tax obligations. The report then outlines the supporting documents required for a loan application, including identity proof, income verification (payslips, group certificates, employer letters, and income from other sources), and asset and liability documentation. A detailed loan costing sheet is presented, estimating various expenses such as application costs, stamp duty, and solicitor fees. The report also includes a loan servicing calculation (NSR) to assess the borrowers' ability to repay the loan. Finally, it incorporates the FHOG application form relevant to the Northern Territory, along with a loan application form and checklist, offering a complete overview of the home loan process. The report emphasizes the importance of accurate documentation and financial planning for first-time homebuyers.

1 out of 56

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.