Understanding Fiscal Administration: Importance, Reports, and Ratios

VerifiedAdded on 2023/06/08

|13

|2901

|473

AI Summary

This study explains the importance of fiscal administration, its obligations, and the role of a fiscal supervisor. It covers financial reports, including income statements, balance sheets, cash flow statements, and notes to accounts. The study also explains various ratios, such as liquidity, profitability, and efficiency ratios, and provides insights into the profitability, efficiency, and liquidity of a business. The study concludes with recommendations for improving the assets turnover ratio and enhancing the business's financial health.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Business

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Contents

Contents...........................................................................................................................................2

INTRODUCTION...........................................................................................................................1

SECTION 1.....................................................................................................................................1

SECTION 2.....................................................................................................................................2

SECTION 3:....................................................................................................................................4

SECTION: 4....................................................................................................................................5

CONCLUSION................................................................................................................................5

REFERENCES................................................................................................................................7

APPENDIX......................................................................................................................................8

Contents...........................................................................................................................................2

INTRODUCTION...........................................................................................................................1

SECTION 1.....................................................................................................................................1

SECTION 2.....................................................................................................................................2

SECTION 3:....................................................................................................................................4

SECTION: 4....................................................................................................................................5

CONCLUSION................................................................................................................................5

REFERENCES................................................................................................................................7

APPENDIX......................................................................................................................................8

INTRODUCTION

The prepared study's purpose is to clarify and describe fiscal administration and to

demonstrate for its necessity (Bouveret, 2018). To think about the obligations and tasks of a

fiscal supervisor. To analyze monetary accounts and clarify the function of ratios. The numerous

kinds of fiscal reports would be covered in detail, along with their uses in monetary planning. A

few instances would also be provided. The study's practical section would be shown together

with an income statement, balance sheet, and an analysis of the profitability, liquidity, and

efficiency of the company depending on the ratio findings. The recommended monetary

recommendations for enhancement would be accompanied by a conclusion.

SECTION 1

Our contemporary society is financially orientated and continually changing, therefore

financing is the foundation of commercial activities and offers accessibility to all the resources

needed by corporate firms. Making a gain requires funds, however this requirement only holds

true when there is good fiscal administration. Without funding, there could be no industry or

company. Finance management is a complicated procedure which engages with making the best

utilisation of a corporation's monetary funds. It involves giving a corporate investment decisions,

keeping up corporate ties with shareholders, bookkeeping, disclosing, budgetary control, and

handling costs and earnings. It also involves task evaluation, preparing, predicting, and inventory

control. Consequently, finance management in a firm encompasses everything which has to do

with cash or funds in general. Across a whole company' life span and in all aspects of its

operations, irrespective of its stage, this monetary mechanism is important (Eka, 2018).

Acquisitions, funding, and assets control are the 3 primary purposes of fiscal management,

and corporate purposes are reflected in such procedures. A finance supervisor should keep track

of financial statements, create projections, and consider the monetary implications. Prior to

investing any assets that may be accessible, it is essential to assess their potential and determine

how best to use them. The following phase is to acquire finance and determine where and how to

get funding for anticipated budgetary demands. The final step is to allocate funds in a corporate

entity in a way that will maximise their worth.

The prepared study's purpose is to clarify and describe fiscal administration and to

demonstrate for its necessity (Bouveret, 2018). To think about the obligations and tasks of a

fiscal supervisor. To analyze monetary accounts and clarify the function of ratios. The numerous

kinds of fiscal reports would be covered in detail, along with their uses in monetary planning. A

few instances would also be provided. The study's practical section would be shown together

with an income statement, balance sheet, and an analysis of the profitability, liquidity, and

efficiency of the company depending on the ratio findings. The recommended monetary

recommendations for enhancement would be accompanied by a conclusion.

SECTION 1

Our contemporary society is financially orientated and continually changing, therefore

financing is the foundation of commercial activities and offers accessibility to all the resources

needed by corporate firms. Making a gain requires funds, however this requirement only holds

true when there is good fiscal administration. Without funding, there could be no industry or

company. Finance management is a complicated procedure which engages with making the best

utilisation of a corporation's monetary funds. It involves giving a corporate investment decisions,

keeping up corporate ties with shareholders, bookkeeping, disclosing, budgetary control, and

handling costs and earnings. It also involves task evaluation, preparing, predicting, and inventory

control. Consequently, finance management in a firm encompasses everything which has to do

with cash or funds in general. Across a whole company' life span and in all aspects of its

operations, irrespective of its stage, this monetary mechanism is important (Eka, 2018).

Acquisitions, funding, and assets control are the 3 primary purposes of fiscal management,

and corporate purposes are reflected in such procedures. A finance supervisor should keep track

of financial statements, create projections, and consider the monetary implications. Prior to

investing any assets that may be accessible, it is essential to assess their potential and determine

how best to use them. The following phase is to acquire finance and determine where and how to

get funding for anticipated budgetary demands. The final step is to allocate funds in a corporate

entity in a way that will maximise their worth.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

SECTION 2

Every commercial firm typically prepares income accounts, which cover all fiscal activities

which have occurred over a certain duration of time. Yearly findings are most frequently

generated. They have 5 primary components; the initial 3 are, assets, liabilities, and equity,

reflect the monetary finance stance of a venture; the other 2, income and expenditure, display the

fiscal outcome of the company; and these 2 components are characterised in the "income

statement" or "statement of profit or loss."

Assets: It is a tool used by an organisation. It is dependent on the result of a previous

occurrence, is owned by someone, and anticipated to provide advantages in the coming.

As an illustration, the acquisition of a machinery which would be utilised to make goods

which would be marketed and bring in money in the near term is a historical occurrence.

Liabilities: It is the responsibility which resulted from historical actions and exists in the

current. It pertains to a company, and it would gain economically if the institution's funds

are used to pay this obligation. A mortgage from a banking institution is perhaps the most

typical type of obligation (Foyeke, Olusola and Aderemi, 2016).

Equities: It is the value that stays in assets after all business obligations have been

subtracted, hence it implies that Equity = Assets- Liabilities

Income: It is a result of financial gains realised within a certain accountancy term due to

enhanced holdings or decreased obligations that raise ownership. For instance, if a

product vendor lowers its pricing, the firm will obviously experience an improvement in

revenue.

Expenditure: It occurs from a decline in the economical advantage throughout the

course of an accountancy term due to diminished holdings or the influence of

obligations that lowers ownership. As an illustration, paying for power is an expenditure.

Income statement: It is a report whose goal is to provide monetary information for a

particular fiscal quarter. This statement details the revenue, costs, and profit or loss. A

customer should go for the income statement if they want to see how much revenue a

company makes.

Balance sheet: Assets, liabilities, and ownership are generated by the balance sheet,

which implies it provides information about the fiscal situation throughout a given year.

Obligations could be simply subtracted from overall assets to determine aggregate value.

Every commercial firm typically prepares income accounts, which cover all fiscal activities

which have occurred over a certain duration of time. Yearly findings are most frequently

generated. They have 5 primary components; the initial 3 are, assets, liabilities, and equity,

reflect the monetary finance stance of a venture; the other 2, income and expenditure, display the

fiscal outcome of the company; and these 2 components are characterised in the "income

statement" or "statement of profit or loss."

Assets: It is a tool used by an organisation. It is dependent on the result of a previous

occurrence, is owned by someone, and anticipated to provide advantages in the coming.

As an illustration, the acquisition of a machinery which would be utilised to make goods

which would be marketed and bring in money in the near term is a historical occurrence.

Liabilities: It is the responsibility which resulted from historical actions and exists in the

current. It pertains to a company, and it would gain economically if the institution's funds

are used to pay this obligation. A mortgage from a banking institution is perhaps the most

typical type of obligation (Foyeke, Olusola and Aderemi, 2016).

Equities: It is the value that stays in assets after all business obligations have been

subtracted, hence it implies that Equity = Assets- Liabilities

Income: It is a result of financial gains realised within a certain accountancy term due to

enhanced holdings or decreased obligations that raise ownership. For instance, if a

product vendor lowers its pricing, the firm will obviously experience an improvement in

revenue.

Expenditure: It occurs from a decline in the economical advantage throughout the

course of an accountancy term due to diminished holdings or the influence of

obligations that lowers ownership. As an illustration, paying for power is an expenditure.

Income statement: It is a report whose goal is to provide monetary information for a

particular fiscal quarter. This statement details the revenue, costs, and profit or loss. A

customer should go for the income statement if they want to see how much revenue a

company makes.

Balance sheet: Assets, liabilities, and ownership are generated by the balance sheet,

which implies it provides information about the fiscal situation throughout a given year.

Obligations could be simply subtracted from overall assets to determine aggregate value.

The variation between this and an income statement is that here, rather than an income

statement for a particular fiscal year, the accounts balances being presented (Ivanovich,

2020).

Understanding the stakeholders' contributions, the equity's flow, and its total at the

conclusion of the accounting year are the two main goals of the Statements of Shift in Equities.

Here, the shareholder equity, overall capital, retained earnings, and dividend payments are all

displayed.

Cash flow statement: It is a fiscal report whose purpose is to show the movements of

cash flows in an organisation over a predetermined temporal frame. Cash flows are broken down

into 3 categories: operating, investing, and financial activity. For instance, operating cash flows

demonstrate how much money a certain business operations generate.

Notes to accounts: Global Monetary Accounting Rules mandate that a note be included

with the monetary statements; nevertheless, most individuals fail to do so. In intended to

facilitate clients, such comments provide improved, clearer, and comprehensive details regarding

fiscal reports. This study goes into great depth about all the data which is lacking in the

preceding studies (Kwilinskyi, Shteingauz and Maslov, 2020).

Ratio analysis: It is mathematically defined as a number split by a fraction, expresses the

interrelationship among 2 things. The ratio is employed to assess a procedure' efficiency in fiscal

administration. The efficiency measurement is calculated by dividing the outcome by the inputs.

Such figures are extracted from the fiscal reports in order to provide a company with important

data. Liquidity ratios, profitability, efficiency, market value ratios, solvency, and other

subcategories are some of the major ratio types.

Liquidity ratios: It demonstrates a company's ability to pay both brief as well as longer

run obligations. It can be broken down into a few other liquidity ratios, including the

current, quick, and cash ratios. Assets which are projected to be turned into money during

the course of one fiscal term are referred to as current assets. A higher ratio indicates

great liquidity for the organisation. Since stocks are harder to turn into money, these are

not included in current assets in the calculation of quick ratio, which is different from the

current ratio. Just monetary assets or their substitutes are used in cash ratio calculations.

Shorter run obligations' liquidity is unhindered if the ratio is substantial.

statement for a particular fiscal year, the accounts balances being presented (Ivanovich,

2020).

Understanding the stakeholders' contributions, the equity's flow, and its total at the

conclusion of the accounting year are the two main goals of the Statements of Shift in Equities.

Here, the shareholder equity, overall capital, retained earnings, and dividend payments are all

displayed.

Cash flow statement: It is a fiscal report whose purpose is to show the movements of

cash flows in an organisation over a predetermined temporal frame. Cash flows are broken down

into 3 categories: operating, investing, and financial activity. For instance, operating cash flows

demonstrate how much money a certain business operations generate.

Notes to accounts: Global Monetary Accounting Rules mandate that a note be included

with the monetary statements; nevertheless, most individuals fail to do so. In intended to

facilitate clients, such comments provide improved, clearer, and comprehensive details regarding

fiscal reports. This study goes into great depth about all the data which is lacking in the

preceding studies (Kwilinskyi, Shteingauz and Maslov, 2020).

Ratio analysis: It is mathematically defined as a number split by a fraction, expresses the

interrelationship among 2 things. The ratio is employed to assess a procedure' efficiency in fiscal

administration. The efficiency measurement is calculated by dividing the outcome by the inputs.

Such figures are extracted from the fiscal reports in order to provide a company with important

data. Liquidity ratios, profitability, efficiency, market value ratios, solvency, and other

subcategories are some of the major ratio types.

Liquidity ratios: It demonstrates a company's ability to pay both brief as well as longer

run obligations. It can be broken down into a few other liquidity ratios, including the

current, quick, and cash ratios. Assets which are projected to be turned into money during

the course of one fiscal term are referred to as current assets. A higher ratio indicates

great liquidity for the organisation. Since stocks are harder to turn into money, these are

not included in current assets in the calculation of quick ratio, which is different from the

current ratio. Just monetary assets or their substitutes are used in cash ratio calculations.

Shorter run obligations' liquidity is unhindered if the ratio is substantial.

Efficiency ratios: They show how efficiently a business may utilize its holdings,

equipment, and personnel to boost sales. The ratio represents the return on investments

and is dependent on the expenses involved and income earned. Indications are important

since they show the present success of an organisation (Levy, Bouheni and Ammi, 2018).

To evaluate a company's standing on a corporate industry, such outcomes must be

evaluated to a rivalry. Businesses achieve profitability whenever companies understand

the effective use of assets. How frequently the products are traded during a specific

amount of time is reflected in the stock turnover ratio.

Profitability ratios: Every company's goal is to make revenue and then deposit a portion

of that earnings again into the company. A crucial element is for a firm to understand its

assets, where to use those, how and when to evaluate different factors, as well as how

much money this could generate from its operations. The various profitability ratios help

in this situation and they are as follows:

Among the most important measures of operating effectiveness is return on total assets. By

contrasting these with aggregate earnings, this ratio takes into account the resources which an

organisation employs to carry out its essential operations.

The return on equity ratio, which divides the total equity by the yearly net return of the

business, evaluates the returns on the owners' capital.

The return on invested capital metric demonstrates how an organisation distributes funds

from successful initiatives or acquisitions. The more a business performed, or the more

efficiently invested capital was used, the greater the ratio.

SECTION 3:

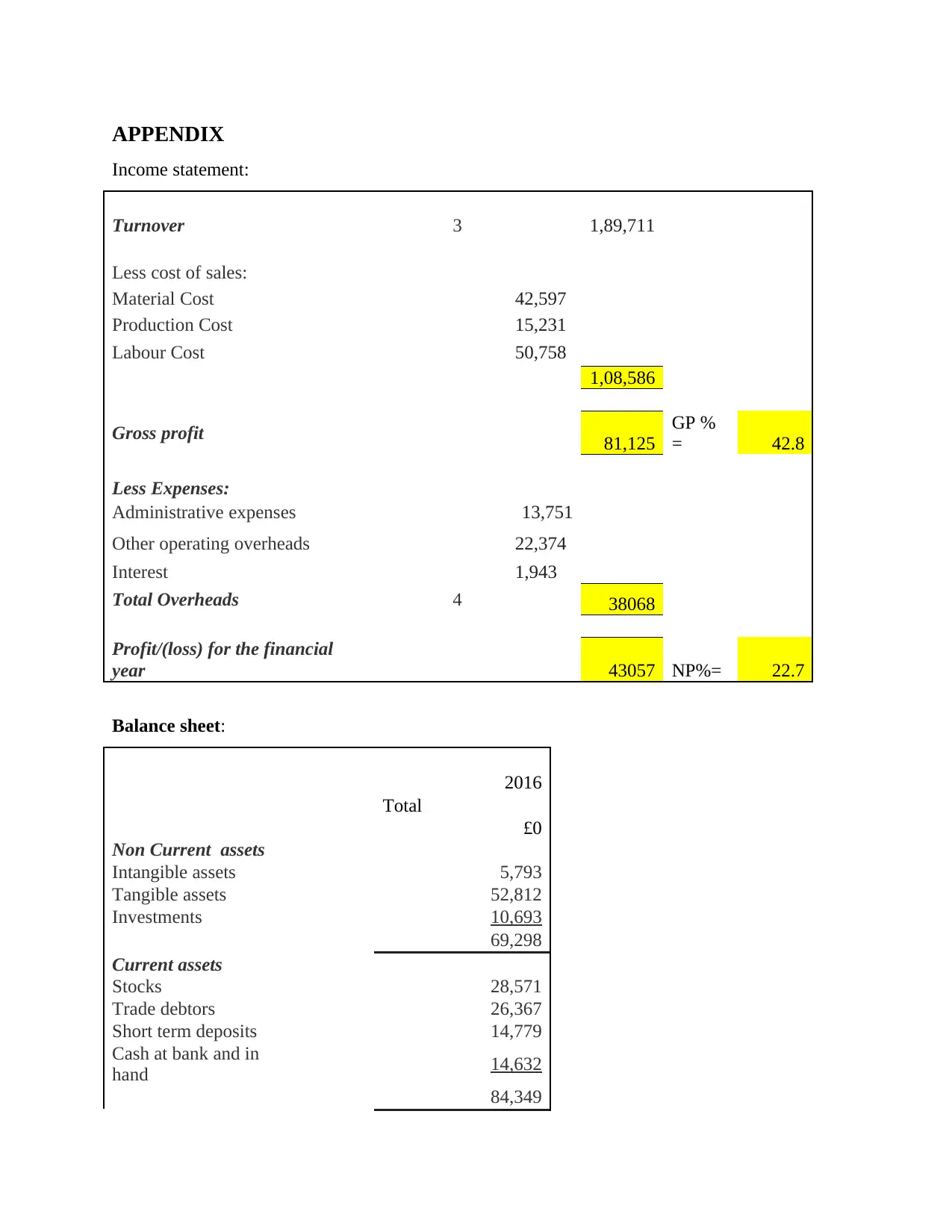

Income statement, Balance sheet, and the calculations are shown in Appendix

Summarize the business under study's profitability, efficiency, and liquidity: It is

possible to observe how much money was made over the course of 2 fiscal terms from the

statement that is included in the appendix. It is 18,987 in 2015, and it will grow by 127% in

2016. A company's fiscal health is shown if its revenues increase from the prior year. The

research also makes it very evident that the gross profit percent is 42.8 and the net profit percent

is 22.7. Such metrics provide insight into how well a company is growing and being handled.

The more a corporation grows, the greater the statistics. This statistics could be comparable to

those from prior years or with similar categories. Whenever the acid test ratio is 1, it indicates

equipment, and personnel to boost sales. The ratio represents the return on investments

and is dependent on the expenses involved and income earned. Indications are important

since they show the present success of an organisation (Levy, Bouheni and Ammi, 2018).

To evaluate a company's standing on a corporate industry, such outcomes must be

evaluated to a rivalry. Businesses achieve profitability whenever companies understand

the effective use of assets. How frequently the products are traded during a specific

amount of time is reflected in the stock turnover ratio.

Profitability ratios: Every company's goal is to make revenue and then deposit a portion

of that earnings again into the company. A crucial element is for a firm to understand its

assets, where to use those, how and when to evaluate different factors, as well as how

much money this could generate from its operations. The various profitability ratios help

in this situation and they are as follows:

Among the most important measures of operating effectiveness is return on total assets. By

contrasting these with aggregate earnings, this ratio takes into account the resources which an

organisation employs to carry out its essential operations.

The return on equity ratio, which divides the total equity by the yearly net return of the

business, evaluates the returns on the owners' capital.

The return on invested capital metric demonstrates how an organisation distributes funds

from successful initiatives or acquisitions. The more a business performed, or the more

efficiently invested capital was used, the greater the ratio.

SECTION 3:

Income statement, Balance sheet, and the calculations are shown in Appendix

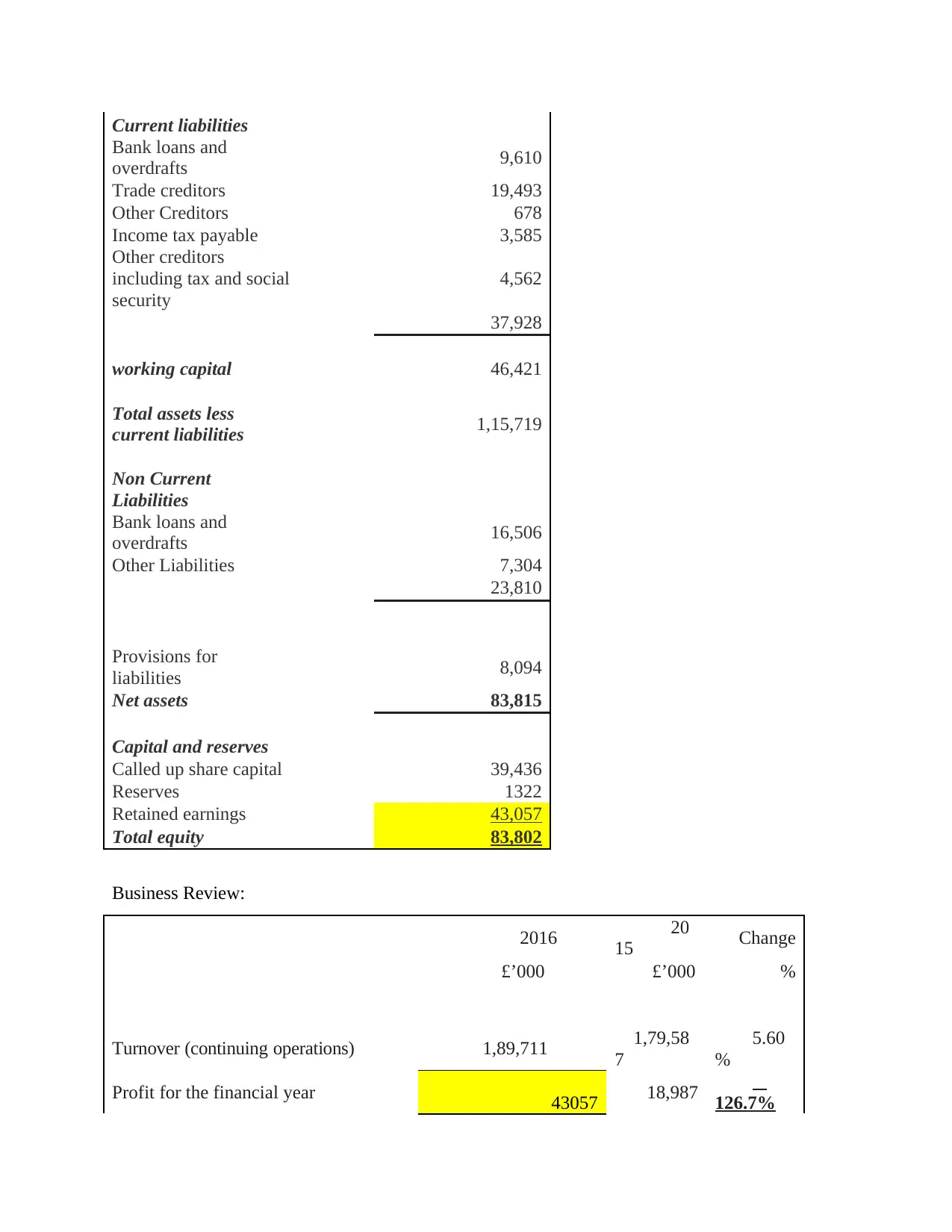

Summarize the business under study's profitability, efficiency, and liquidity: It is

possible to observe how much money was made over the course of 2 fiscal terms from the

statement that is included in the appendix. It is 18,987 in 2015, and it will grow by 127% in

2016. A company's fiscal health is shown if its revenues increase from the prior year. The

research also makes it very evident that the gross profit percent is 42.8 and the net profit percent

is 22.7. Such metrics provide insight into how well a company is growing and being handled.

The more a corporation grows, the greater the statistics. This statistics could be comparable to

those from prior years or with similar categories. Whenever the acid test ratio is 1, it indicates

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

that a business could repay all of its obligations in full. The acid test ratio for the undergoing

review of the business is 1.47, indicating that it has no trouble making debt payments. The

current ratio is more than 2, indicating indicates that the business will be able to repay its

obligations. It frequently pays twice as much toward its commitments as is necessary. The

current ratio for the business is 2.22. The sole outcome which is possibly not so favourable for

this organisation is its efficiency, as it has a ratio of 1.34. This outcome demonstrates how much

a company is ready to invest in new equipment and other assets in an attempt to boost sales.

Although the statistic is really favourable, there is still space for growth. The following

parameter measures stock turnover that currently stands at 2.34, making it the best of all the

indicators but still a potential area for improvement. In actuality, it demonstrates how many of a

firm's products or activities it could offer over a specific length of span.

SECTION: 4

The organisation does have to increase its assets turnover ratio since it is now only

approximately 1.6 that is a lower outcome and indicates ineffective financial and asset

administration. Manufacturing concerns can potentially be at blame for this (Sheedy, Griffin and

Barbour, 2017). A ratio around 3 must be their goal. This is quite significant since it affects

lenders and shareholders. This outcome typically indicates that there is an issue with

manufacturing or administration of a business. There are many opportunities for development.

The initial stage for this business is to concentrate on raising selling and earnings,

correspondingly, by enhancing its advertising approach and expanding the use of incentives and

price cuts while selling its products or operations. As a result, there would be quick selling and

less effort spent keeping inventory on hand. The next action which this business have to do is to

stop keeping the resources which are not being used. All resources should be thoroughly studied,

evaluated, and, if deemed superfluous, a choice should be taken regarding if to dissolve or trade

those. This company could rent additional assets if it requires those but lacks the funds to

purchase them. On the one side, this would significantly boost sales while having little of an

impact on expenses.

CONCLUSION

The significance of finance administration as well as the obligations of a fiscal supervisor

were discussed in this document. Finance reports and ratios were given and examined. Instances

review of the business is 1.47, indicating that it has no trouble making debt payments. The

current ratio is more than 2, indicating indicates that the business will be able to repay its

obligations. It frequently pays twice as much toward its commitments as is necessary. The

current ratio for the business is 2.22. The sole outcome which is possibly not so favourable for

this organisation is its efficiency, as it has a ratio of 1.34. This outcome demonstrates how much

a company is ready to invest in new equipment and other assets in an attempt to boost sales.

Although the statistic is really favourable, there is still space for growth. The following

parameter measures stock turnover that currently stands at 2.34, making it the best of all the

indicators but still a potential area for improvement. In actuality, it demonstrates how many of a

firm's products or activities it could offer over a specific length of span.

SECTION: 4

The organisation does have to increase its assets turnover ratio since it is now only

approximately 1.6 that is a lower outcome and indicates ineffective financial and asset

administration. Manufacturing concerns can potentially be at blame for this (Sheedy, Griffin and

Barbour, 2017). A ratio around 3 must be their goal. This is quite significant since it affects

lenders and shareholders. This outcome typically indicates that there is an issue with

manufacturing or administration of a business. There are many opportunities for development.

The initial stage for this business is to concentrate on raising selling and earnings,

correspondingly, by enhancing its advertising approach and expanding the use of incentives and

price cuts while selling its products or operations. As a result, there would be quick selling and

less effort spent keeping inventory on hand. The next action which this business have to do is to

stop keeping the resources which are not being used. All resources should be thoroughly studied,

evaluated, and, if deemed superfluous, a choice should be taken regarding if to dissolve or trade

those. This company could rent additional assets if it requires those but lacks the funds to

purchase them. On the one side, this would significantly boost sales while having little of an

impact on expenses.

CONCLUSION

The significance of finance administration as well as the obligations of a fiscal supervisor

were discussed in this document. Finance reports and ratios were given and examined. Instances

are provided as well as consideration of other categories. All evaluations have been finished, and

spreadsheets with the information have been provided. There were recommendations made for

the assessed firm's enhancements.

spreadsheets with the information have been provided. There were recommendations made for

the assessed firm's enhancements.

REFERENCES

Books and journals

Bouveret, A., 2018. Cyber risk for the financial sector: A framework for quantitative assessment.

International Monetary Fund.

Eka, H., 2018. Corporate finance and firm value in the Indonesian manufacturing

companies. BUSINESS STUDIES. 11(2). pp.113-127.

Foyeke, O.I., Olusola, F.S. and Aderemi, A.K., 2016. Financial structure and the profitability of

manufacturing companies in Nigeria.

Ivanovich, K.K., 2020. About some questions of classification of institutional conditions

determining the structure of doing business in Uzbekistan. South Asian Journal of

Marketing & Management Research. 10(5). pp.17-28.

Kwilinskyi, O., Shteingauz, D. and Maslov, V., 2020. Financial and credit instruments for

ensuring effective functioning of the residential real estate market.

Levy, A., Bouheni, F.B. and Ammi, C., 2018. Financial management: USGAAP and IFRS

Standards. John Wiley & Sons.

Sheedy, E.A., Griffin, B. and Barbour, J.P., 2017. A framework and measure for examining risk

climate in financial institutions. Journal of Business and Psychology. 32(1). pp.101-116.

Books and journals

Bouveret, A., 2018. Cyber risk for the financial sector: A framework for quantitative assessment.

International Monetary Fund.

Eka, H., 2018. Corporate finance and firm value in the Indonesian manufacturing

companies. BUSINESS STUDIES. 11(2). pp.113-127.

Foyeke, O.I., Olusola, F.S. and Aderemi, A.K., 2016. Financial structure and the profitability of

manufacturing companies in Nigeria.

Ivanovich, K.K., 2020. About some questions of classification of institutional conditions

determining the structure of doing business in Uzbekistan. South Asian Journal of

Marketing & Management Research. 10(5). pp.17-28.

Kwilinskyi, O., Shteingauz, D. and Maslov, V., 2020. Financial and credit instruments for

ensuring effective functioning of the residential real estate market.

Levy, A., Bouheni, F.B. and Ammi, C., 2018. Financial management: USGAAP and IFRS

Standards. John Wiley & Sons.

Sheedy, E.A., Griffin, B. and Barbour, J.P., 2017. A framework and measure for examining risk

climate in financial institutions. Journal of Business and Psychology. 32(1). pp.101-116.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

APPENDIX

Income statement:

Turnover 3 1,89,711

Less cost of sales:

Material Cost 42,597

Production Cost 15,231

Labour Cost 50,758

1,08,586

Gross profit 81,125

GP %

= 42.8

Less Expenses:

Administrative expenses 13,751

Other operating overheads 22,374

Interest 1,943

Total Overheads 4 38068

Profit/(loss) for the financial

year 43057 NP%= 22.7

Balance sheet:

2016

Total

£0

Non Current assets

Intangible assets 5,793

Tangible assets 52,812

Investments 10,693

69,298

Current assets

Stocks 28,571

Trade debtors 26,367

Short term deposits 14,779

Cash at bank and in

hand 14,632

84,349

Income statement:

Turnover 3 1,89,711

Less cost of sales:

Material Cost 42,597

Production Cost 15,231

Labour Cost 50,758

1,08,586

Gross profit 81,125

GP %

= 42.8

Less Expenses:

Administrative expenses 13,751

Other operating overheads 22,374

Interest 1,943

Total Overheads 4 38068

Profit/(loss) for the financial

year 43057 NP%= 22.7

Balance sheet:

2016

Total

£0

Non Current assets

Intangible assets 5,793

Tangible assets 52,812

Investments 10,693

69,298

Current assets

Stocks 28,571

Trade debtors 26,367

Short term deposits 14,779

Cash at bank and in

hand 14,632

84,349

Current liabilities

Bank loans and

overdrafts 9,610

Trade creditors 19,493

Other Creditors 678

Income tax payable 3,585

Other creditors

including tax and social

security

4,562

37,928

working capital 46,421

Total assets less

current liabilities 1,15,719

Non Current

Liabilities

Bank loans and

overdrafts 16,506

Other Liabilities 7,304

23,810

Provisions for

liabilities 8,094

Net assets 83,815

Capital and reserves

Called up share capital 39,436

Reserves 1322

Retained earnings 43,057

Total equity 83,802

Business Review:

2016 20

15 Change

£’000 £’000 %

Turnover (continuing operations) 1,89,711 1,79,58

7

5.60

%

Profit for the financial year 43057 18,987 126.7%

Bank loans and

overdrafts 9,610

Trade creditors 19,493

Other Creditors 678

Income tax payable 3,585

Other creditors

including tax and social

security

4,562

37,928

working capital 46,421

Total assets less

current liabilities 1,15,719

Non Current

Liabilities

Bank loans and

overdrafts 16,506

Other Liabilities 7,304

23,810

Provisions for

liabilities 8,094

Net assets 83,815

Capital and reserves

Called up share capital 39,436

Reserves 1322

Retained earnings 43,057

Total equity 83,802

Business Review:

2016 20

15 Change

£’000 £’000 %

Turnover (continuing operations) 1,89,711 1,79,58

7

5.60

%

Profit for the financial year 43057 18,987 126.7%

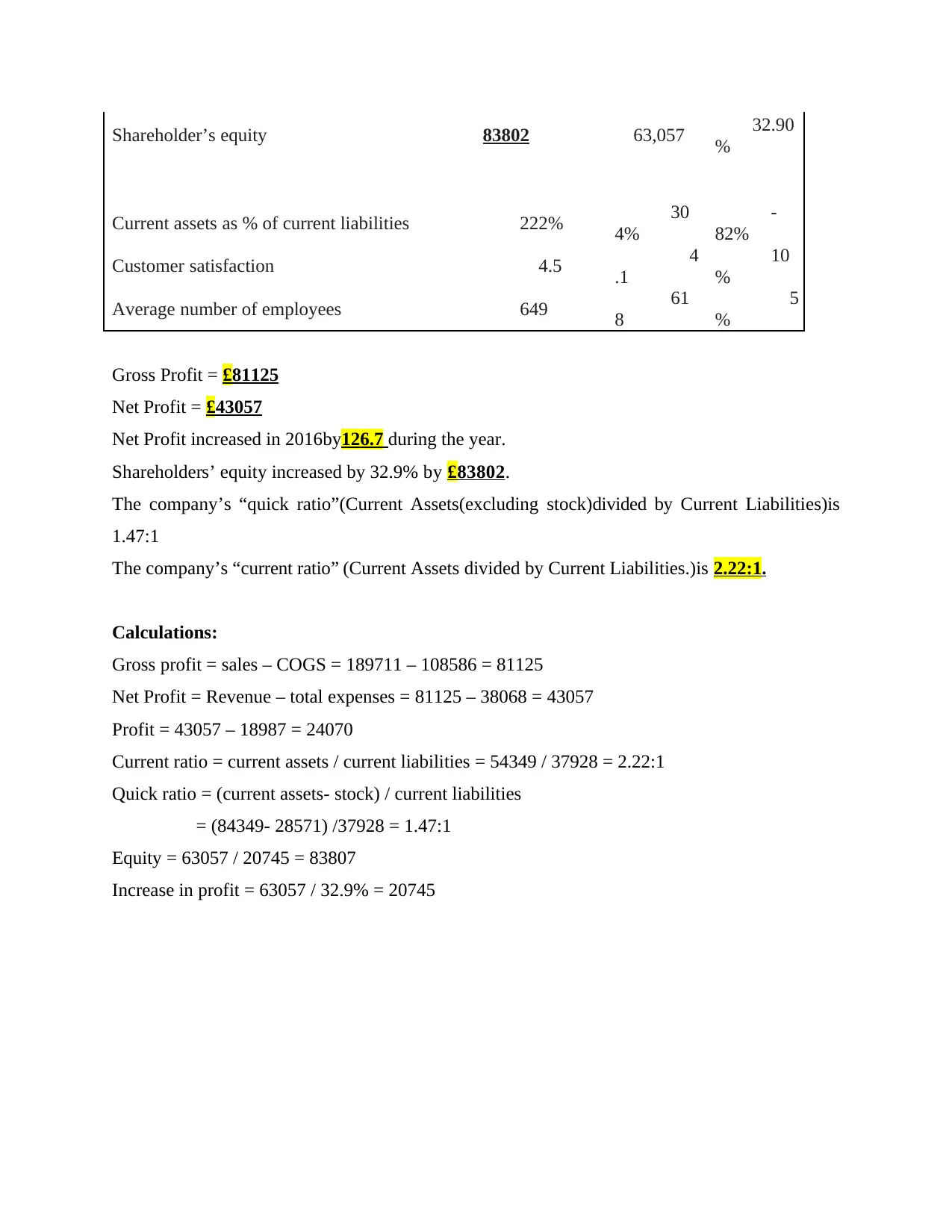

Shareholder’s equity 83802 63,057 32.90

%

Current assets as % of current liabilities 222% 30

4%

-

82%

Customer satisfaction 4.5 4

.1

10

%

Average number of employees 649 61

8

5

%

Gross Profit = £81125

Net Profit = £43057

Net Profit increased in 2016by126.7 during the year.

Shareholders’ equity increased by 32.9% by £83802.

The company’s “quick ratio”(Current Assets(excluding stock)divided by Current Liabilities)is

1.47:1

The company’s “current ratio” (Current Assets divided by Current Liabilities.)is 2.22:1.

Calculations:

Gross profit = sales – COGS = 189711 – 108586 = 81125

Net Profit = Revenue – total expenses = 81125 – 38068 = 43057

Profit = 43057 – 18987 = 24070

Current ratio = current assets / current liabilities = 54349 / 37928 = 2.22:1

Quick ratio = (current assets- stock) / current liabilities

= (84349- 28571) /37928 = 1.47:1

Equity = 63057 / 20745 = 83807

Increase in profit = 63057 / 32.9% = 20745

%

Current assets as % of current liabilities 222% 30

4%

-

82%

Customer satisfaction 4.5 4

.1

10

%

Average number of employees 649 61

8

5

%

Gross Profit = £81125

Net Profit = £43057

Net Profit increased in 2016by126.7 during the year.

Shareholders’ equity increased by 32.9% by £83802.

The company’s “quick ratio”(Current Assets(excluding stock)divided by Current Liabilities)is

1.47:1

The company’s “current ratio” (Current Assets divided by Current Liabilities.)is 2.22:1.

Calculations:

Gross profit = sales – COGS = 189711 – 108586 = 81125

Net Profit = Revenue – total expenses = 81125 – 38068 = 43057

Profit = 43057 – 18987 = 24070

Current ratio = current assets / current liabilities = 54349 / 37928 = 2.22:1

Quick ratio = (current assets- stock) / current liabilities

= (84349- 28571) /37928 = 1.47:1

Equity = 63057 / 20745 = 83807

Increase in profit = 63057 / 32.9% = 20745

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.