Tourism Business Analysis and Valuation

VerifiedAdded on 2020/02/24

|23

|6392

|95

AI Summary

This assignment delves into the analysis of a tourism business, encompassing various aspects such as direct and indirect carbon dioxide emissions, business model frameworks, profitability, and valuation techniques under International Financial Reporting Standards (IFRS). Students are expected to analyze relevant case studies and apply theoretical concepts to real-world examples within the tourism industry. The assignment emphasizes understanding the environmental impact, financial performance, and strategic value proposition of tourism businesses.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: BUSINESS VALUATION AND ANALYSIS

Business Valuation and Analysis

Name of the Student

Name of the University

Authors Note

Course ID

Business Valuation and Analysis

Name of the Student

Name of the University

Authors Note

Course ID

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1BUSINESS VALUATION AND ANALYSIS

Table of Contents

Introduction:...............................................................................................................................2

Macroeconomic Analysis:..........................................................................................................2

Industry analysis.........................................................................................................................6

Rivalry from existing competitors.............................................................................................7

Bargaining power of customers...............................................................................................10

Bargaining power of suppliers.................................................................................................10

Business Strategy Analysis:.....................................................................................................11

Growth in Network:.................................................................................................................12

Accounting Analysis................................................................................................................14

Recognition of the principal accounting policies.....................................................................14

Evaluating the accounting flexibility.......................................................................................15

Assessing the accounting strategy............................................................................................15

Assessing the quality of the disclosure....................................................................................16

Information distortion..............................................................................................................16

Undoing any accounting distortions.........................................................................................17

Conclusion:..............................................................................................................................18

Reference List:.........................................................................................................................19

Table of Contents

Introduction:...............................................................................................................................2

Macroeconomic Analysis:..........................................................................................................2

Industry analysis.........................................................................................................................6

Rivalry from existing competitors.............................................................................................7

Bargaining power of customers...............................................................................................10

Bargaining power of suppliers.................................................................................................10

Business Strategy Analysis:.....................................................................................................11

Growth in Network:.................................................................................................................12

Accounting Analysis................................................................................................................14

Recognition of the principal accounting policies.....................................................................14

Evaluating the accounting flexibility.......................................................................................15

Assessing the accounting strategy............................................................................................15

Assessing the quality of the disclosure....................................................................................16

Information distortion..............................................................................................................16

Undoing any accounting distortions.........................................................................................17

Conclusion:..............................................................................................................................18

Reference List:.........................................................................................................................19

2BUSINESS VALUATION AND ANALYSIS

Introduction:

In the age of globalization with the introduction of Science and Technology, every

organization operating within their economy assess their performance concerning the

industrial benchmark of the economy where the organizations operates (Kubasek, Brennan

and Browne 2016). The study is concerned with the evaluation of the financial statement for

Flight Centre Travel Group by taking in to the considerations the variable sources such as the yearly

report of the organization to gather information for assessment. The fiscal report of the Flight Centre

Travel Group will help in assessing the operations of the business. Flight Centre Travel Group has

been found to be one of the most renowned airline service within the geographical regions of

Australia. Flight Centre Travel Group is listed in the Australian stock exchange as one of the listed

companies and operating in the airline industry.

As evident from the report, the company has been generating profit for the last few years after

rising beyond the competition as the company was in the requirement of taking the business

performance to the new level (Kew and Stredwick 2017). The yearly report of the company

provides the information regarding the operations of the company. In addition to this, the use of

numerous analytical techniques has been implemented in the present study that comprises of

macroeconomic analysis, business strategy analysis, industry analysis and the accounting evaluation

for Flight Centre Travel Group. The study even analyses the extent of competition faced by the

company in the present travelling industry where theFlight Centre Travel Group operates.

Macroeconomic Analysis:

Flight centre travel group‘s economic environment

Economic environment relates to the external factors that influences the workplace

environment in the business. The economic objective of Flight centre travel group (FCTG) is

to contribute the destination nation they work and stay. Economic environment is categorized

into two parts such as – macro- environment and microenvironment. The success of this

Introduction:

In the age of globalization with the introduction of Science and Technology, every

organization operating within their economy assess their performance concerning the

industrial benchmark of the economy where the organizations operates (Kubasek, Brennan

and Browne 2016). The study is concerned with the evaluation of the financial statement for

Flight Centre Travel Group by taking in to the considerations the variable sources such as the yearly

report of the organization to gather information for assessment. The fiscal report of the Flight Centre

Travel Group will help in assessing the operations of the business. Flight Centre Travel Group has

been found to be one of the most renowned airline service within the geographical regions of

Australia. Flight Centre Travel Group is listed in the Australian stock exchange as one of the listed

companies and operating in the airline industry.

As evident from the report, the company has been generating profit for the last few years after

rising beyond the competition as the company was in the requirement of taking the business

performance to the new level (Kew and Stredwick 2017). The yearly report of the company

provides the information regarding the operations of the company. In addition to this, the use of

numerous analytical techniques has been implemented in the present study that comprises of

macroeconomic analysis, business strategy analysis, industry analysis and the accounting evaluation

for Flight Centre Travel Group. The study even analyses the extent of competition faced by the

company in the present travelling industry where theFlight Centre Travel Group operates.

Macroeconomic Analysis:

Flight centre travel group‘s economic environment

Economic environment relates to the external factors that influences the workplace

environment in the business. The economic objective of Flight centre travel group (FCTG) is

to contribute the destination nation they work and stay. Economic environment is categorized

into two parts such as – macro- environment and microenvironment. The success of this

3BUSINESS VALUATION AND ANALYSIS

organization is determined with the help of these two types of economic environment

(Woodford 2013). The management of the enterprise also ascertain that the benefits and

disadvantage of tourism are evenly shared in their travel agency business. In addition, the

economic environment of FCTG is also affected by the society’s economic health to which

their business is connected.

This enterprise is one of the major stakeholders in overall society where their business

operates and to the society where their customers like to travel. The management of the

organizations mainly operates on those key sectors that facilitates them in giving information

on the advisor’s economic liability and collecting resources in order to assists on the

knowledge of their customers. They focus on conducting package-reviewing process that

aspires in selecting their tour package that are beneficial for the Australian economy.

Analyzing how global economies affect the organizational performance over the years

Fluctuations in the global economies adversely affect the company’s growth over the

last few years. As the recession in US hits the global economy, it negatively influenced the

financial performance of many entities in the globe (Healy. and Palepu 2012) However,

FCTG also suffered from enormous loss during the year 2008-2009 owing to decrease in

number of both international and domestic tourist. The management of this firm strategized

to fire few employees in order to cover up huge loss during this phase. As a result, Australia’s

rate of unemployment increased above the target level , which is 5%. In additional,

uncertainties and changing economic condition of the less developed nation’s also influences

the travel agency business in Australia including FCTG. Moreover, changing visa policies of

the individual nations affects the performance of this organization as well as growth of

FCTG.

organization is determined with the help of these two types of economic environment

(Woodford 2013). The management of the enterprise also ascertain that the benefits and

disadvantage of tourism are evenly shared in their travel agency business. In addition, the

economic environment of FCTG is also affected by the society’s economic health to which

their business is connected.

This enterprise is one of the major stakeholders in overall society where their business

operates and to the society where their customers like to travel. The management of the

organizations mainly operates on those key sectors that facilitates them in giving information

on the advisor’s economic liability and collecting resources in order to assists on the

knowledge of their customers. They focus on conducting package-reviewing process that

aspires in selecting their tour package that are beneficial for the Australian economy.

Analyzing how global economies affect the organizational performance over the years

Fluctuations in the global economies adversely affect the company’s growth over the

last few years. As the recession in US hits the global economy, it negatively influenced the

financial performance of many entities in the globe (Healy. and Palepu 2012) However,

FCTG also suffered from enormous loss during the year 2008-2009 owing to decrease in

number of both international and domestic tourist. The management of this firm strategized

to fire few employees in order to cover up huge loss during this phase. As a result, Australia’s

rate of unemployment increased above the target level , which is 5%. In additional,

uncertainties and changing economic condition of the less developed nation’s also influences

the travel agency business in Australia including FCTG. Moreover, changing visa policies of

the individual nations affects the performance of this organization as well as growth of

FCTG.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4BUSINESS VALUATION AND ANALYSIS

Macroeconomic variables affecting the performance of FCTG

The macroeconomic variables assess the cyclical movements and inclination of the

respective economy (Trugman, 2016). These variables includes- GDP growth rate, inflation,

prices of crude oil, unemployment rate, exchange rates, interest rates, money supply etc.

Macroeconomic events and the economic health affects all the organizations of the economy.

In this study, four factors are considered for analyzing the impact of economic environment

of FCTG business that includes- GDP, Inflation, exchange rate, prices of crude oil.

The GDP of the economy is defined as the summation of its total consumption,

investment, government spending and net exports (Sekaran and Bougie, 2016). It is one of

the major factors that affect the business performance and determines the economic health of

the country. GDP growth rate refers to the economic trend of the nation over the years.

Owing to expansion of Australia’s GDP growth rate to 0.3% in 2017, the financial

performance of FCTG improved. This is because cyclical fluctuations in the respective

nation influence the credit demand. As recession hits Australian economy, the GDP growth

rate declined and hence this reduced the economy’s credit demand. However, this adversely

affected performance of FCTG in terms of revenue and profitability. after that phase the

credit demand again increased leading to rise in profit of the company.

Inflation rate is another macroeconomic factor that largely influences the purchasing

power and cost of business. High rate of inflation in the Australian economy during the

recession period (2008-2009) reduced the purchasing power of the customers and this led to

decline in aggregate demand in services (Goodwinet al. 2013). As a result, the business cost

of this travel agency increased and this decreased their profitability level. However, during

expansionary period, as the Australian recovered from huge financial crisis the inflation rate

Macroeconomic variables affecting the performance of FCTG

The macroeconomic variables assess the cyclical movements and inclination of the

respective economy (Trugman, 2016). These variables includes- GDP growth rate, inflation,

prices of crude oil, unemployment rate, exchange rates, interest rates, money supply etc.

Macroeconomic events and the economic health affects all the organizations of the economy.

In this study, four factors are considered for analyzing the impact of economic environment

of FCTG business that includes- GDP, Inflation, exchange rate, prices of crude oil.

The GDP of the economy is defined as the summation of its total consumption,

investment, government spending and net exports (Sekaran and Bougie, 2016). It is one of

the major factors that affect the business performance and determines the economic health of

the country. GDP growth rate refers to the economic trend of the nation over the years.

Owing to expansion of Australia’s GDP growth rate to 0.3% in 2017, the financial

performance of FCTG improved. This is because cyclical fluctuations in the respective

nation influence the credit demand. As recession hits Australian economy, the GDP growth

rate declined and hence this reduced the economy’s credit demand. However, this adversely

affected performance of FCTG in terms of revenue and profitability. after that phase the

credit demand again increased leading to rise in profit of the company.

Inflation rate is another macroeconomic factor that largely influences the purchasing

power and cost of business. High rate of inflation in the Australian economy during the

recession period (2008-2009) reduced the purchasing power of the customers and this led to

decline in aggregate demand in services (Goodwinet al. 2013). As a result, the business cost

of this travel agency increased and this decreased their profitability level. However, during

expansionary period, as the Australian recovered from huge financial crisis the inflation rate

5BUSINESS VALUATION AND ANALYSIS

fell and this raised the purchasing power in the economy. Hence, this increased the travel

demand of the customers leading to enhancement of financial performance of FCTG.

Volatility in Australia’s crude oil industry created huge risk to FCTG Company. As

rise in inflation rate of Australia increased prices of crude oil, FCTG ‘s input cost also

increased. This led to rise in airfares and hence the customers demand for travel

automatically reduced during 2008-2009. Though Australian economy has recovered from

recession phase, volatility in oil prices still exist in the economy. Hence, this factor often

influences their organizational performance.

Foreign exchange rate fluctuation affects the customers spending in travel destination.

In the current state, exchange rate depreciation raises the total demand for travel in the

economy (Frechtling 2013). However, as the Australians spend their money in travel; this

raised the profitability level of FCTG. Therefore, implementation of expansionary monetary

policy stabilizes this currency fluctuation and thus lowering the risk in foreign exchange.

Future forecast of FCTG ‘s financial performance

Recent statistic reflects that the Australian economy has been progressing over the

years. Therefore, if the GDP growth rates of this nation continuously increase, the credit

demand in the economy will increase at higher rate. In addition, implementation of

expansionary monetary policy will help keep the inflation rate low in the economy. As a

result, the prices of commodities and services automatically lower and this will increase their

purchasing power. Moreover, increase in consumers spending in travel will raise the revenue

of travel companies in Australia including FCTG. On the contrary, oil prices volatility in

Australia will always exist and this may create huge problems to this travel company (Borio

2014). In addition, changes in foreign exchange rate might influence their financial

performance of FCTG in future. Therefore, it is recommended that the management of FCTG

fell and this raised the purchasing power in the economy. Hence, this increased the travel

demand of the customers leading to enhancement of financial performance of FCTG.

Volatility in Australia’s crude oil industry created huge risk to FCTG Company. As

rise in inflation rate of Australia increased prices of crude oil, FCTG ‘s input cost also

increased. This led to rise in airfares and hence the customers demand for travel

automatically reduced during 2008-2009. Though Australian economy has recovered from

recession phase, volatility in oil prices still exist in the economy. Hence, this factor often

influences their organizational performance.

Foreign exchange rate fluctuation affects the customers spending in travel destination.

In the current state, exchange rate depreciation raises the total demand for travel in the

economy (Frechtling 2013). However, as the Australians spend their money in travel; this

raised the profitability level of FCTG. Therefore, implementation of expansionary monetary

policy stabilizes this currency fluctuation and thus lowering the risk in foreign exchange.

Future forecast of FCTG ‘s financial performance

Recent statistic reflects that the Australian economy has been progressing over the

years. Therefore, if the GDP growth rates of this nation continuously increase, the credit

demand in the economy will increase at higher rate. In addition, implementation of

expansionary monetary policy will help keep the inflation rate low in the economy. As a

result, the prices of commodities and services automatically lower and this will increase their

purchasing power. Moreover, increase in consumers spending in travel will raise the revenue

of travel companies in Australia including FCTG. On the contrary, oil prices volatility in

Australia will always exist and this may create huge problems to this travel company (Borio

2014). In addition, changes in foreign exchange rate might influence their financial

performance of FCTG in future. Therefore, it is recommended that the management of FCTG

6BUSINESS VALUATION AND ANALYSIS

must focus on these economic environmental factors before making their business strategies.

This will help the company to attain higher profitability and expand their business in the

future.

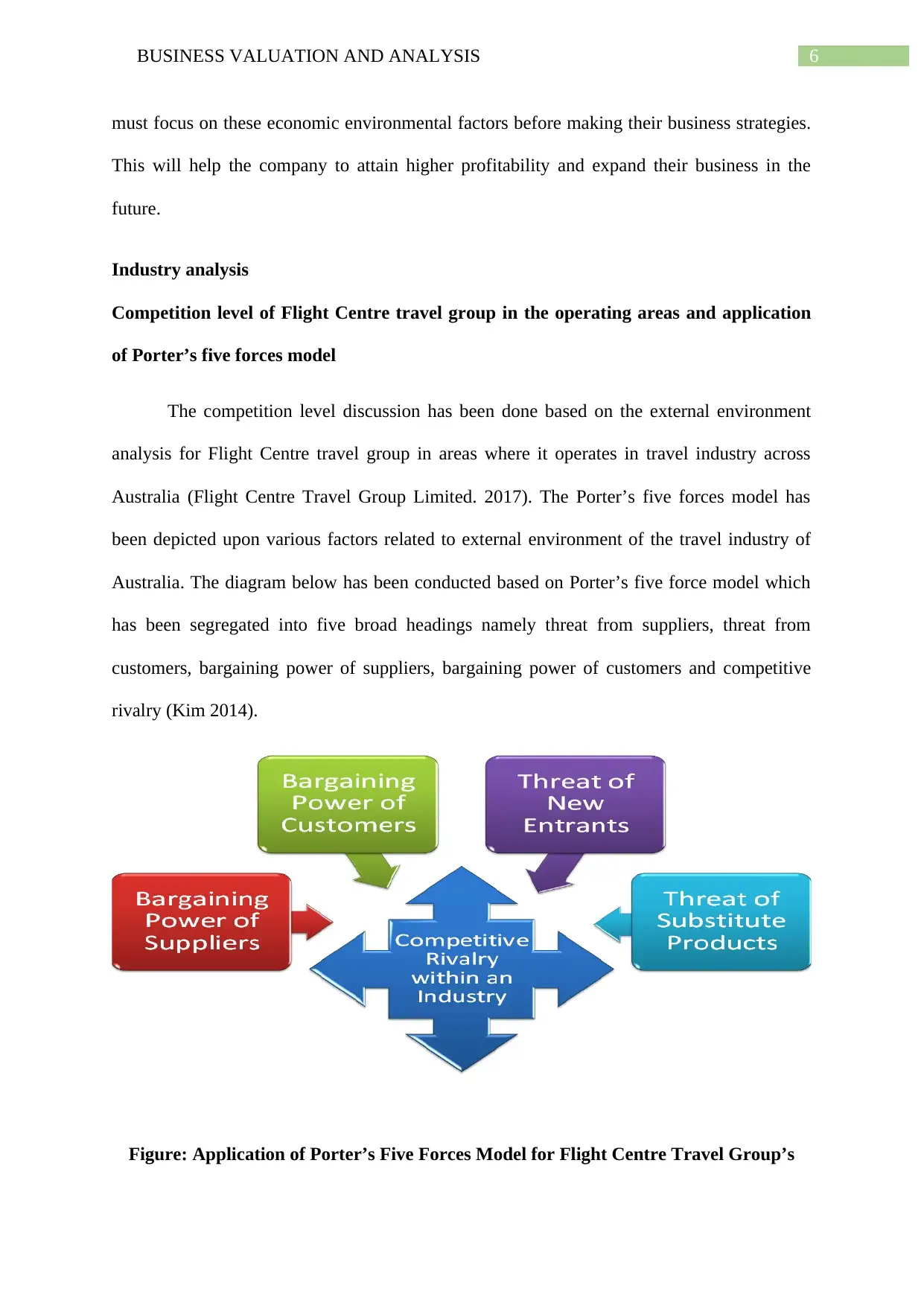

Industry analysis

Competition level of Flight Centre travel group in the operating areas and application

of Porter’s five forces model

The competition level discussion has been done based on the external environment

analysis for Flight Centre travel group in areas where it operates in travel industry across

Australia (Flight Centre Travel Group Limited. 2017). The Porter’s five forces model has

been depicted upon various factors related to external environment of the travel industry of

Australia. The diagram below has been conducted based on Porter’s five force model which

has been segregated into five broad headings namely threat from suppliers, threat from

customers, bargaining power of suppliers, bargaining power of customers and competitive

rivalry (Kim 2014).

Figure: Application of Porter’s Five Forces Model for Flight Centre Travel Group’s

must focus on these economic environmental factors before making their business strategies.

This will help the company to attain higher profitability and expand their business in the

future.

Industry analysis

Competition level of Flight Centre travel group in the operating areas and application

of Porter’s five forces model

The competition level discussion has been done based on the external environment

analysis for Flight Centre travel group in areas where it operates in travel industry across

Australia (Flight Centre Travel Group Limited. 2017). The Porter’s five forces model has

been depicted upon various factors related to external environment of the travel industry of

Australia. The diagram below has been conducted based on Porter’s five force model which

has been segregated into five broad headings namely threat from suppliers, threat from

customers, bargaining power of suppliers, bargaining power of customers and competitive

rivalry (Kim 2014).

Figure: Application of Porter’s Five Forces Model for Flight Centre Travel Group’s

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7BUSINESS VALUATION AND ANALYSIS

(Source: Flight Centre Travel Group Limited. 2017)

Rivalry from existing competitors

The criteria for rivalry from the existing firm have been identified with the lower

competition from the existing industry.

Lower risk from the rival firm- The travel industry of Australia has been depicted

with low amount of risk from the competitors due to lower cost incurred. The

competitors are able to maintain their inventory with the appropriate stock levels. The

main rationale for this is due to low storage cost which is having a positive impact on

the company’s dealing in travel business (Lloyd 2014).

Large Industry size- The travel industry of Australia seen to allow multiple firms for making

an effort and having higher market share of other firms. Henceforth, a large group of market

size is seen to create a positive impact on Flight Centre travel group. Due to the large nature

of industry, multiple opportunities have been presented to the company which belongs to

present and near future as well (Robinson et al. 2016).

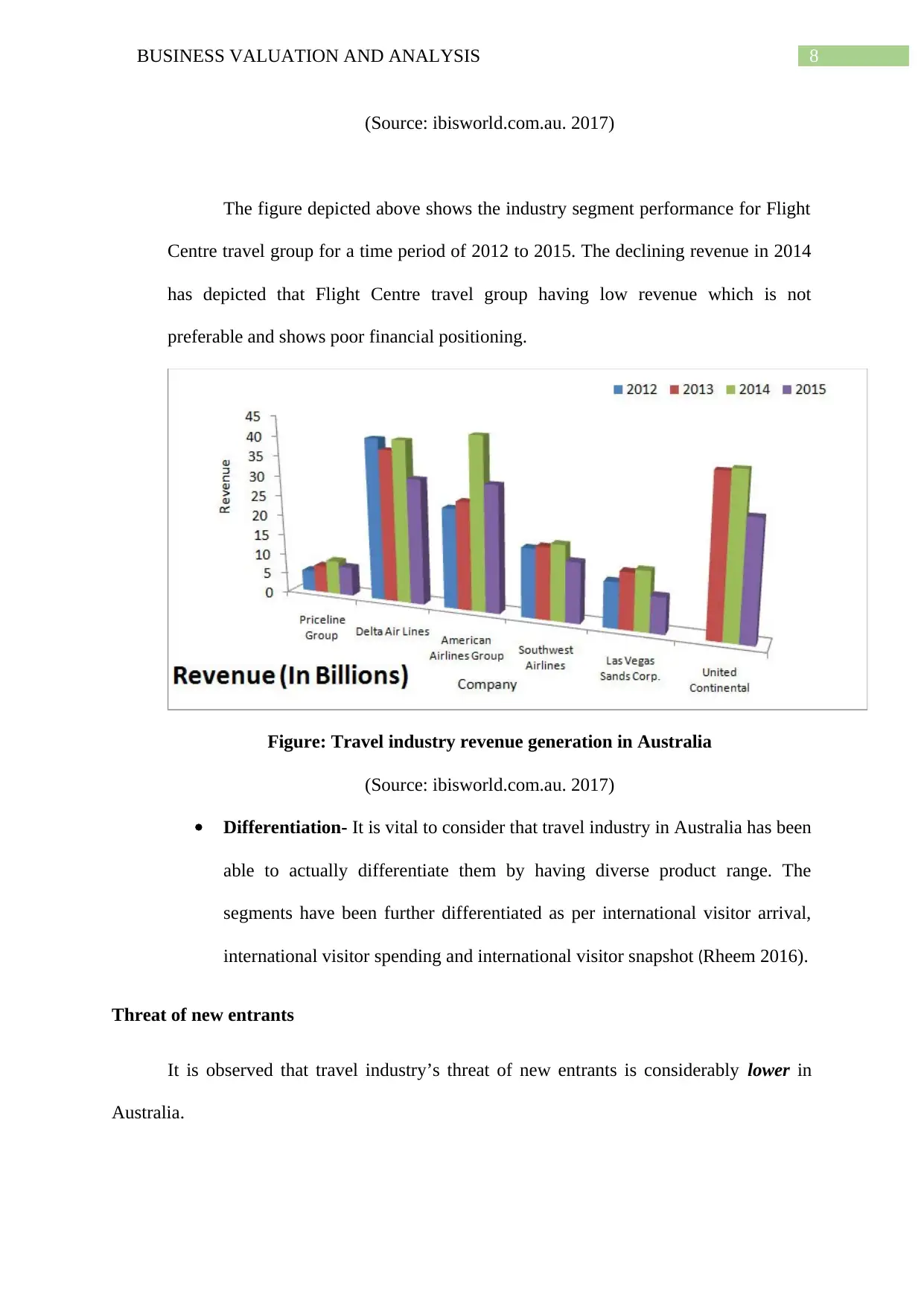

Figure: Segmental industry performance

(Source: Flight Centre Travel Group Limited. 2017)

Rivalry from existing competitors

The criteria for rivalry from the existing firm have been identified with the lower

competition from the existing industry.

Lower risk from the rival firm- The travel industry of Australia has been depicted

with low amount of risk from the competitors due to lower cost incurred. The

competitors are able to maintain their inventory with the appropriate stock levels. The

main rationale for this is due to low storage cost which is having a positive impact on

the company’s dealing in travel business (Lloyd 2014).

Large Industry size- The travel industry of Australia seen to allow multiple firms for making

an effort and having higher market share of other firms. Henceforth, a large group of market

size is seen to create a positive impact on Flight Centre travel group. Due to the large nature

of industry, multiple opportunities have been presented to the company which belongs to

present and near future as well (Robinson et al. 2016).

Figure: Segmental industry performance

8BUSINESS VALUATION AND ANALYSIS

(Source: ibisworld.com.au. 2017)

The figure depicted above shows the industry segment performance for Flight

Centre travel group for a time period of 2012 to 2015. The declining revenue in 2014

has depicted that Flight Centre travel group having low revenue which is not

preferable and shows poor financial positioning.

Figure: Travel industry revenue generation in Australia

(Source: ibisworld.com.au. 2017)

Differentiation- It is vital to consider that travel industry in Australia has been

able to actually differentiate them by having diverse product range. The

segments have been further differentiated as per international visitor arrival,

international visitor spending and international visitor snapshot (Rheem 2016).

Threat of new entrants

It is observed that travel industry’s threat of new entrants is considerably lower in

Australia.

(Source: ibisworld.com.au. 2017)

The figure depicted above shows the industry segment performance for Flight

Centre travel group for a time period of 2012 to 2015. The declining revenue in 2014

has depicted that Flight Centre travel group having low revenue which is not

preferable and shows poor financial positioning.

Figure: Travel industry revenue generation in Australia

(Source: ibisworld.com.au. 2017)

Differentiation- It is vital to consider that travel industry in Australia has been

able to actually differentiate them by having diverse product range. The

segments have been further differentiated as per international visitor arrival,

international visitor spending and international visitor snapshot (Rheem 2016).

Threat of new entrants

It is observed that travel industry’s threat of new entrants is considerably lower in

Australia.

9BUSINESS VALUATION AND ANALYSIS

Implementation of advanced technologies- To prevent the entry of Flight

Centre travel Group Company needs to implement advanced and innovative

technologies so that it can face your competition. The existing competition in

Australia needs to be first assessed and then addressed with use of those

advanced technologies.

Economies of scale- this conducive for the travel industry to have economies

of scale for lowering the cost. This is also required to produce the next best

unit of output at a reduced rate.

Higher cost of production- It is vital to know the underlying facts related to

new competitors trying to enter in the Australian travel industry. They will be

definitely having an access to increased cost of production which runs parallel

to the smaller economies of scale.

Skilled employees and human resources- Based on the analysis it has

considered that the travel industry has mostly searched for the employees who

are having low scale and do not have to pay higher remuneration towards their

work. In this way the profit margin is kept substantially low from the other

brand of companies. Henceforth, the changes are relevant to the macro

economy which largely influences the major challenges in a similar industry.

Threat of substitute products

The travel industry of Australia is on to face lower threats from substitute products.

Switching cost- the customers find the service quality to be low when they are having

a tendency to switch other brands. Flight Centre travel group needs to maintain its

quality and make the same as a barrier to the new entrants and various types of

substitute services.

Implementation of advanced technologies- To prevent the entry of Flight

Centre travel Group Company needs to implement advanced and innovative

technologies so that it can face your competition. The existing competition in

Australia needs to be first assessed and then addressed with use of those

advanced technologies.

Economies of scale- this conducive for the travel industry to have economies

of scale for lowering the cost. This is also required to produce the next best

unit of output at a reduced rate.

Higher cost of production- It is vital to know the underlying facts related to

new competitors trying to enter in the Australian travel industry. They will be

definitely having an access to increased cost of production which runs parallel

to the smaller economies of scale.

Skilled employees and human resources- Based on the analysis it has

considered that the travel industry has mostly searched for the employees who

are having low scale and do not have to pay higher remuneration towards their

work. In this way the profit margin is kept substantially low from the other

brand of companies. Henceforth, the changes are relevant to the macro

economy which largely influences the major challenges in a similar industry.

Threat of substitute products

The travel industry of Australia is on to face lower threats from substitute products.

Switching cost- the customers find the service quality to be low when they are having

a tendency to switch other brands. Flight Centre travel group needs to maintain its

quality and make the same as a barrier to the new entrants and various types of

substitute services.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10BUSINESS VALUATION AND ANALYSIS

Reduced quality of services- The Flight Centre travel group is seen to be having

multiple number of substitutes and responsible for delivering lower service quality.

However, the strategy is not applicable on the customers as they are more concerned

about the service quality factor than any other concern.

Bargaining power of customers

Based on the industry analysis in Australia the bargaining power is of customers is seen

to be medium. Some of the appropriate reason for justification has been enumerated

below as follows:

Large customer base- The travel company in Australia seen to be having a large

customer base where the customers medium bargaining power.

Price sensitive- the price sensitive nature of the customers for Flight Centre Travel

Group has been seen to be mainly less sensitive as it believes in delivering the best quality at

reasonable rates (Flight Centre Travel Group Limited. 2017). In addition to this, the

customers mostly look forward to alignment of the social status. In case a company is aware

that customers are only looking for quality, then the price increases automatically and this

needs to be taken into consideration (Lok, Asano and Rhodes 2014).

Bargaining power of suppliers

The bargaining power faced by Australian travel industry is designed to be high.

Some of the main reasons have been justified below as follows:

Intense competition- the travel company of Australia seen face a huge competition as

a suppliers provide the best price various types of other players in the market.

Diversified distribution channel-Based on the analysis that diversify distribution

channel has given rise to the high bargaining power from a single distributor and the

travel industry based in Australia. This has been particularly seen to be the area where

Reduced quality of services- The Flight Centre travel group is seen to be having

multiple number of substitutes and responsible for delivering lower service quality.

However, the strategy is not applicable on the customers as they are more concerned

about the service quality factor than any other concern.

Bargaining power of customers

Based on the industry analysis in Australia the bargaining power is of customers is seen

to be medium. Some of the appropriate reason for justification has been enumerated

below as follows:

Large customer base- The travel company in Australia seen to be having a large

customer base where the customers medium bargaining power.

Price sensitive- the price sensitive nature of the customers for Flight Centre Travel

Group has been seen to be mainly less sensitive as it believes in delivering the best quality at

reasonable rates (Flight Centre Travel Group Limited. 2017). In addition to this, the

customers mostly look forward to alignment of the social status. In case a company is aware

that customers are only looking for quality, then the price increases automatically and this

needs to be taken into consideration (Lok, Asano and Rhodes 2014).

Bargaining power of suppliers

The bargaining power faced by Australian travel industry is designed to be high.

Some of the main reasons have been justified below as follows:

Intense competition- the travel company of Australia seen face a huge competition as

a suppliers provide the best price various types of other players in the market.

Diversified distribution channel-Based on the analysis that diversify distribution

channel has given rise to the high bargaining power from a single distributor and the

travel industry based in Australia. This has been particularly seen to be the area where

11BUSINESS VALUATION AND ANALYSIS

volume is critical to the suppliers who are regularly providing services to Flight

Centre travel group.

Relies on high volume-It has been particularly noticed that the suppliers rely on high

volume which lead to higher bargaining power. Moreover, the producers are not seen

to be having the scope to cut down the negative profit (Robertson 2017).

Business Strategy Analysis:

Against the backyard of the noteworthy low airline, fares and lower confidence among the

customers there are some of the nations that have gone past the TTV for the financial year of 2016

(Wetherly and Otter 2014). Along with this, the business strategy of Flight Centre Travel Group has

been successful in attaining the revenue by around $350 million in the backdrop of profit for the third

successive year in the history of operations of the company. It is noteworthy to denote that the

business strategy of the business strategy of Flight Centre Travel Group has been successful in

producing GPB of $1 billion sales. The strategy of business has of Flight Centre Travel Group has

been designed in such a way that it provides the foundations of future growth by investing in the

innovating system that helps in introducing the advantage of higher cost with improved productivity

(Palepu, Healy and Peek 2013).

The business strategy of the Flight Centre Travel Group has been successful in improving the

streams of revenue together with the new and unique sort of goods and services for appealing its

customers (Wahlen, Baginski and Bradshaw 2014). It is worth mentioning that the business

strategy of Flight Centre Travel Group has been successful in improving the overseas network with

the help of rolling out the next generation stores and designs. The company has been successful in

developing the new innovative consumer cantered initiatives that consists of the flexibility of

workplace arrangement and programs that will help in increasing the ownership with the help of

digital capabilities.

The business strategy of Flight Centre Travel Group has been successful in expanding the

business level footprint particularly with the help of organic growth however, the company has also

volume is critical to the suppliers who are regularly providing services to Flight

Centre travel group.

Relies on high volume-It has been particularly noticed that the suppliers rely on high

volume which lead to higher bargaining power. Moreover, the producers are not seen

to be having the scope to cut down the negative profit (Robertson 2017).

Business Strategy Analysis:

Against the backyard of the noteworthy low airline, fares and lower confidence among the

customers there are some of the nations that have gone past the TTV for the financial year of 2016

(Wetherly and Otter 2014). Along with this, the business strategy of Flight Centre Travel Group has

been successful in attaining the revenue by around $350 million in the backdrop of profit for the third

successive year in the history of operations of the company. It is noteworthy to denote that the

business strategy of the business strategy of Flight Centre Travel Group has been successful in

producing GPB of $1 billion sales. The strategy of business has of Flight Centre Travel Group has

been designed in such a way that it provides the foundations of future growth by investing in the

innovating system that helps in introducing the advantage of higher cost with improved productivity

(Palepu, Healy and Peek 2013).

The business strategy of the Flight Centre Travel Group has been successful in improving the

streams of revenue together with the new and unique sort of goods and services for appealing its

customers (Wahlen, Baginski and Bradshaw 2014). It is worth mentioning that the business

strategy of Flight Centre Travel Group has been successful in improving the overseas network with

the help of rolling out the next generation stores and designs. The company has been successful in

developing the new innovative consumer cantered initiatives that consists of the flexibility of

workplace arrangement and programs that will help in increasing the ownership with the help of

digital capabilities.

The business strategy of Flight Centre Travel Group has been successful in expanding the

business level footprint particularly with the help of organic growth however, the company has also

12BUSINESS VALUATION AND ANALYSIS

gained success with the help of key market of Aisa, Europe and America (Jenkins and Williamson

2015). The acquirement of Netherlands is considered as one of the business milestone for the Flight

Central Travel Group because this has helped the company in entering in the markets of Europe that

comprise of the largest business travel market. On the other hand, the acquisition of Malaysia has

marked as the first international expansion in respect of the geographical territories for large number

of years. The business has been performing successfully ever since the company has acquired the

operations of the FLT with the objective of speedy growth in the noteworthy student and youth age

group in terms of both domestically and internationally.

Customer Centric Business approach:

A customer forms the important element for any kind of business. The business strategy

of Flight Centre Travel Group has been successful in holding its workforce in discharge of the

valuable service to achieve its business functions (Batkovsky, Batkovsky and Klochkov 2016).

Simultaneously, accordingly the business strategy of Flight Centre Travel Group represents that the

organization makes a huge investment by continuously investing in the areas of professional learning

and development by providing adequate amenities.

Growth in Network:

The business strategy of Flight Centre Travel Group has been successful in expanding the

network of the business with the help of strategic acquisition as this has helped in diversifying the

sales of the organization. The company has introduced the model of BYOjet that represents an online

business which specializes itself in the ultra-low cost airfares. It is worth mentioning that the

corporate travel of the Flight Centre Travel Group has become an integral part of the business because

they have become an international travel solution network (Hill, Jones and Schilling 2014). Along

with this, several brands have significantly attained the growth with the assistance of FX specialist

travel business and niche corporate brands have immensely contributed to the growth of the business.

Flight Centre Travel Group has also posted a successful solid sales and growth in attendance

at its network wide expo program and in several vital markets of Australia (Drnevich and Croson

gained success with the help of key market of Aisa, Europe and America (Jenkins and Williamson

2015). The acquirement of Netherlands is considered as one of the business milestone for the Flight

Central Travel Group because this has helped the company in entering in the markets of Europe that

comprise of the largest business travel market. On the other hand, the acquisition of Malaysia has

marked as the first international expansion in respect of the geographical territories for large number

of years. The business has been performing successfully ever since the company has acquired the

operations of the FLT with the objective of speedy growth in the noteworthy student and youth age

group in terms of both domestically and internationally.

Customer Centric Business approach:

A customer forms the important element for any kind of business. The business strategy

of Flight Centre Travel Group has been successful in holding its workforce in discharge of the

valuable service to achieve its business functions (Batkovsky, Batkovsky and Klochkov 2016).

Simultaneously, accordingly the business strategy of Flight Centre Travel Group represents that the

organization makes a huge investment by continuously investing in the areas of professional learning

and development by providing adequate amenities.

Growth in Network:

The business strategy of Flight Centre Travel Group has been successful in expanding the

network of the business with the help of strategic acquisition as this has helped in diversifying the

sales of the organization. The company has introduced the model of BYOjet that represents an online

business which specializes itself in the ultra-low cost airfares. It is worth mentioning that the

corporate travel of the Flight Centre Travel Group has become an integral part of the business because

they have become an international travel solution network (Hill, Jones and Schilling 2014). Along

with this, several brands have significantly attained the growth with the assistance of FX specialist

travel business and niche corporate brands have immensely contributed to the growth of the business.

Flight Centre Travel Group has also posted a successful solid sales and growth in attendance

at its network wide expo program and in several vital markets of Australia (Drnevich and Croson

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

13BUSINESS VALUATION AND ANALYSIS

2013). Despite the prevalence of trading climate Flight Centre Travel Group has been successful in

presenting a robust corporate performance which generally helps the company in transforming the

business structure with the help of international expansion. Furthermore, obtaining the presence of

continental Europe with the assistance of FCM Netherlands acquisition the company has been able to

recently grew in the international market after the launch of the leisure store in the Dawson Street of

Dublin.

The results obtained from the segmented growth in Mexico, TTV has helped the company in

modestly introducing the FX business in the markets of America, and presently the company has two

new outlets in Manhattan (Mishra and Zachary 2014). The segmented results have attained a

successful business strategy since the segment of South Africa have posted a positive growth and

profit from the higher sales. The annual reports of the company states that it has for the first time

topped the revenue growth. On the other hand, segments of New Zealand and Canada have

contributed for the very first time with a sum of $AU 1billion in TTV. The segment of Canada have

immensely contributed to the growth in profit by demonstrating the positive outcomes of corporate

level and closing down the loss making leisure in the late fiscal year of 2015.

Taking into the consideration the risk that is associated with the profit making structure of the

business is the increase in the cost of oil and gas segment that have created a noteworthy impact on

the performance of the business (Pettersson and Sorensen 2016). The is considered as the major

threat to the company’s performance as because the corporate demand of the travel has been

significantly impacted by the loss of some regional corporate accounts, investment in new and rising

businesses have provided lower sum of yield profits in India. In addition to this, the leisure liberty and

GOGO segments of the company have led to bottom line results and have been unsuccessful in

meeting the anticipations of the business (Wild and Staden 2013). This is considerably in the

decline of the $24.7 million with a write down of $12.0 million in USA segment and $12.7 million in

the other segment.

2013). Despite the prevalence of trading climate Flight Centre Travel Group has been successful in

presenting a robust corporate performance which generally helps the company in transforming the

business structure with the help of international expansion. Furthermore, obtaining the presence of

continental Europe with the assistance of FCM Netherlands acquisition the company has been able to

recently grew in the international market after the launch of the leisure store in the Dawson Street of

Dublin.

The results obtained from the segmented growth in Mexico, TTV has helped the company in

modestly introducing the FX business in the markets of America, and presently the company has two

new outlets in Manhattan (Mishra and Zachary 2014). The segmented results have attained a

successful business strategy since the segment of South Africa have posted a positive growth and

profit from the higher sales. The annual reports of the company states that it has for the first time

topped the revenue growth. On the other hand, segments of New Zealand and Canada have

contributed for the very first time with a sum of $AU 1billion in TTV. The segment of Canada have

immensely contributed to the growth in profit by demonstrating the positive outcomes of corporate

level and closing down the loss making leisure in the late fiscal year of 2015.

Taking into the consideration the risk that is associated with the profit making structure of the

business is the increase in the cost of oil and gas segment that have created a noteworthy impact on

the performance of the business (Pettersson and Sorensen 2016). The is considered as the major

threat to the company’s performance as because the corporate demand of the travel has been

significantly impacted by the loss of some regional corporate accounts, investment in new and rising

businesses have provided lower sum of yield profits in India. In addition to this, the leisure liberty and

GOGO segments of the company have led to bottom line results and have been unsuccessful in

meeting the anticipations of the business (Wild and Staden 2013). This is considerably in the

decline of the $24.7 million with a write down of $12.0 million in USA segment and $12.7 million in

the other segment.

14BUSINESS VALUATION AND ANALYSIS

To improve the business performance Flight Centre Travel Group has provided the customers

with the opportunity of booking through online to LCC airfares and ancillary products that have

ultimately helped in delivering the streams of revenue (Raubenheimer and Stammen 2013). Flight

Centre Travel Group is looking forward to expand the leisure of travel brands together with the

standalone branch to produce new streams of revenue. To improve the performance of the

organization, Flight Centre Travel Group has targeted to increase the sales of leisure as the mark of

business expansion by focussing on the package holidays for gaining growth in the markets of

Australia.

Accounting Analysis

There are six different stages in the model of accounting analysis and each one of

them are analysed briefly with respect to Flight Centre Travel Group. Each one of them are

discussed as follows:

Recognition of the principal accounting policies

With respect to the annual report of Flight Centre Travel Group, the financial

statement has been constructed in accordance with the Australian Accounting Standards and

the explanation disclosed by the Corporations Act 2001 and the Australian Accounting

Standards Board. The company has implemented AASB 9 from 1st January 2016 for

facilitating the hedge accounting process in their Flight Centre Global Product operations

(Flight Centre Travel Group Limited 2017). Furthermore, the company has even introduced

an innovative framework of impairment for their financial assets with an approach that is

three staged in nature. The model is inclusive of the 12 month anticipated credit losses,

lifetime predicted credit losses (impaired) and lifetime expected credit losses.

The company has even implemented the convention of historical cost, as amended

through the assessment of the FVOCI financial assets, financial instruments that are

derivative in nature and the contingent considerations. The company is associated with the

To improve the business performance Flight Centre Travel Group has provided the customers

with the opportunity of booking through online to LCC airfares and ancillary products that have

ultimately helped in delivering the streams of revenue (Raubenheimer and Stammen 2013). Flight

Centre Travel Group is looking forward to expand the leisure of travel brands together with the

standalone branch to produce new streams of revenue. To improve the performance of the

organization, Flight Centre Travel Group has targeted to increase the sales of leisure as the mark of

business expansion by focussing on the package holidays for gaining growth in the markets of

Australia.

Accounting Analysis

There are six different stages in the model of accounting analysis and each one of

them are analysed briefly with respect to Flight Centre Travel Group. Each one of them are

discussed as follows:

Recognition of the principal accounting policies

With respect to the annual report of Flight Centre Travel Group, the financial

statement has been constructed in accordance with the Australian Accounting Standards and

the explanation disclosed by the Corporations Act 2001 and the Australian Accounting

Standards Board. The company has implemented AASB 9 from 1st January 2016 for

facilitating the hedge accounting process in their Flight Centre Global Product operations

(Flight Centre Travel Group Limited 2017). Furthermore, the company has even introduced

an innovative framework of impairment for their financial assets with an approach that is

three staged in nature. The model is inclusive of the 12 month anticipated credit losses,

lifetime predicted credit losses (impaired) and lifetime expected credit losses.

The company has even implemented the convention of historical cost, as amended

through the assessment of the FVOCI financial assets, financial instruments that are

derivative in nature and the contingent considerations. The company is associated with the

15BUSINESS VALUATION AND ANALYSIS

rounding off the values to the nearest thousand dollars with respect to the Investments

Commission’s Instrument 2016/191 and the Australian Securities.

Evaluating the accounting flexibility

The flexibility of accounting can be assessed by taking assistance of the resulting data

content. In case of circumstances when the managers have the minimum amount of flexibility

is choosing the strategies of accounting and predictions related with their crucial factors for

success, the accounting information can be less knowledgeable and enlightening for obtaining

knowledge about the economies of the organization. Conversely, these are the selection of the

choices, which the company could have chosen from the list of alternatives that was available

to them. With respect to Flight Centre Travel Group, it has been noticed that the firm has

implemented stern and strict policies of accounting that is in line with the IFRS and the

AASB (Rhee and Yang 2015). The supervisors and the managers of the company does not

have the power to implement flexibility in choosing the accounting estimates and policies.

The higher level management of Flight Centre Travel Group has constructed the accounting

strategies and the associated estimates and it is the duty of the managers to abide by the rules

and norms (Van Nostrand, Sivaraman and Pinjari 2013). Therefore, it could be cited that the

accounting data of the company is increasingly knowledgeable and the author can obtain an

effective understanding of the aggregate economies of the organization.

Assessing the accounting strategy

As expressed by Gupta and Kumar (2013), when the management discovers flexibility

within accounting, they could make use of the same in order to interpret the economic

condition of the organization or to restrict the practical performance. One of the significant

requirements in scrutinising the strategies of accounting of the firm is the capability of the

firm to handle with the industrial regulations. An example can be cited, with the scenario that

rounding off the values to the nearest thousand dollars with respect to the Investments

Commission’s Instrument 2016/191 and the Australian Securities.

Evaluating the accounting flexibility

The flexibility of accounting can be assessed by taking assistance of the resulting data

content. In case of circumstances when the managers have the minimum amount of flexibility

is choosing the strategies of accounting and predictions related with their crucial factors for

success, the accounting information can be less knowledgeable and enlightening for obtaining

knowledge about the economies of the organization. Conversely, these are the selection of the

choices, which the company could have chosen from the list of alternatives that was available

to them. With respect to Flight Centre Travel Group, it has been noticed that the firm has

implemented stern and strict policies of accounting that is in line with the IFRS and the

AASB (Rhee and Yang 2015). The supervisors and the managers of the company does not

have the power to implement flexibility in choosing the accounting estimates and policies.

The higher level management of Flight Centre Travel Group has constructed the accounting

strategies and the associated estimates and it is the duty of the managers to abide by the rules

and norms (Van Nostrand, Sivaraman and Pinjari 2013). Therefore, it could be cited that the

accounting data of the company is increasingly knowledgeable and the author can obtain an

effective understanding of the aggregate economies of the organization.

Assessing the accounting strategy

As expressed by Gupta and Kumar (2013), when the management discovers flexibility

within accounting, they could make use of the same in order to interpret the economic

condition of the organization or to restrict the practical performance. One of the significant

requirements in scrutinising the strategies of accounting of the firm is the capability of the

firm to handle with the industrial regulations. An example can be cited, with the scenario that

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

16BUSINESS VALUATION AND ANALYSIS

Flight Centre Travel Group has won their appeal with respect to the competition that is

associated with the case of law test started against them by ACC associated to the charged

infringes of the Trade Practices Act 1974. The ACC has been asked to pay the legal expenses

of the firm for the initiation of the case and even for the succeeding appeal. The company was

paid a sum of $11,000,000 as a penalty, which has been declared in the financial report of the

firm. Furthermore, the administration does not adequate incentive facilities to influence the

employees and no transformations have been undertaken in the policies of accounting and the

anticipations in the current year.

Assessing the quality of the disclosure

The disclosure or the declaration quality of a firm can be analysed with the help of the

amount of declarations, Note 1 of the policies of accounting along with the sustaining

performance. The initial note with respect to Flight Centre Travel Group handles with the

origin of the construction of the financial reports with respect to IFRS and AASB. The

declarations are undertaken in accordance to the financial assets that are associated with

impairment and the consolidation principles (Tao and Huang 2014). These principles try to

consider the explained synopsis of the joint agreements, transformations in the rate of interest

of the ownership, subsidiaries, interpretation of the foreign currency and mutual agreements.

In addition, the company has framed the balance sheet statement, changes in the statement of

equity, income statement, which has aided in describing their present financial condition and

performance in the market of Australia (Duan et al. 2013).

Information distortion

This parameter lucidly explains that the researcher requires examining the several

items in a precise manner or obtaining extra data with respect to them. This considers the

audit reports that are unqualified, unexplained accounting transformations, unexplained

Flight Centre Travel Group has won their appeal with respect to the competition that is

associated with the case of law test started against them by ACC associated to the charged

infringes of the Trade Practices Act 1974. The ACC has been asked to pay the legal expenses

of the firm for the initiation of the case and even for the succeeding appeal. The company was

paid a sum of $11,000,000 as a penalty, which has been declared in the financial report of the

firm. Furthermore, the administration does not adequate incentive facilities to influence the

employees and no transformations have been undertaken in the policies of accounting and the

anticipations in the current year.

Assessing the quality of the disclosure

The disclosure or the declaration quality of a firm can be analysed with the help of the

amount of declarations, Note 1 of the policies of accounting along with the sustaining

performance. The initial note with respect to Flight Centre Travel Group handles with the

origin of the construction of the financial reports with respect to IFRS and AASB. The

declarations are undertaken in accordance to the financial assets that are associated with

impairment and the consolidation principles (Tao and Huang 2014). These principles try to

consider the explained synopsis of the joint agreements, transformations in the rate of interest

of the ownership, subsidiaries, interpretation of the foreign currency and mutual agreements.

In addition, the company has framed the balance sheet statement, changes in the statement of

equity, income statement, which has aided in describing their present financial condition and

performance in the market of Australia (Duan et al. 2013).

Information distortion

This parameter lucidly explains that the researcher requires examining the several

items in a precise manner or obtaining extra data with respect to them. This considers the

audit reports that are unqualified, unexplained accounting transformations, unexplained

17BUSINESS VALUATION AND ANALYSIS

transactions, rise in profits, associated transactions of the parties and unforeseen huge write-

offs (Meng et al. 2016). With respect to the auditor of the firm namely Ernst & Young, the

company has undertaken write-downs associated to the business, which have not reached the

projected anticipations. Conversely, according to the auditor report, no distinct

transformations in accounting have been undertaken in the 2016 accounting year and the

predictions have matched to the sustaining regulations and the standards in the country. There

have not been associated transactions shown in the annual report of Flight Centre Travel

Group, which explains that the company has no red flag potentials at the present scenario to

continue with their activities in the market of Australia.

Undoing any accounting distortions

As opined by McManus (2013), if there are any detected issues in the step shown

above, it is essential for the firm to restrict any distortion in the process of accounting.

Conversely, after the evaluation of the steps explained above with respect to Flight Centre

Travel Group, it can be described that no crucial distortions in accounting has been noticed in

the report of the auditors of Flight Centre Travel Group. The only issue discovered is the

writing down that is related with the activities of the business, as it has failed to reach the

expectations of the administration of the firm. In this scenario, there are two probable paths

of rectifying the specific distortion. This includes passing of journal entries or changing the

financial ratios that is based on the information gathered with the help of the financial reports

of the company. Conversely, it has to be kept in mind that journal entry passing cannot be

undertaken in case of impairment as it would have a undeviating effect over the ratios. In this

scenario, Flight Centre Travel Group can make use of any of the two choices that are

accessible to them by exploiting the financial report footnotes and the statement of cash flow

of the company.

transactions, rise in profits, associated transactions of the parties and unforeseen huge write-

offs (Meng et al. 2016). With respect to the auditor of the firm namely Ernst & Young, the

company has undertaken write-downs associated to the business, which have not reached the

projected anticipations. Conversely, according to the auditor report, no distinct

transformations in accounting have been undertaken in the 2016 accounting year and the

predictions have matched to the sustaining regulations and the standards in the country. There

have not been associated transactions shown in the annual report of Flight Centre Travel

Group, which explains that the company has no red flag potentials at the present scenario to

continue with their activities in the market of Australia.

Undoing any accounting distortions

As opined by McManus (2013), if there are any detected issues in the step shown

above, it is essential for the firm to restrict any distortion in the process of accounting.

Conversely, after the evaluation of the steps explained above with respect to Flight Centre

Travel Group, it can be described that no crucial distortions in accounting has been noticed in

the report of the auditors of Flight Centre Travel Group. The only issue discovered is the

writing down that is related with the activities of the business, as it has failed to reach the

expectations of the administration of the firm. In this scenario, there are two probable paths

of rectifying the specific distortion. This includes passing of journal entries or changing the

financial ratios that is based on the information gathered with the help of the financial reports

of the company. Conversely, it has to be kept in mind that journal entry passing cannot be

undertaken in case of impairment as it would have a undeviating effect over the ratios. In this

scenario, Flight Centre Travel Group can make use of any of the two choices that are

accessible to them by exploiting the financial report footnotes and the statement of cash flow

of the company.

18BUSINESS VALUATION AND ANALYSIS

Conclusion:

On arriving at the conclusion by analysing the numerous factors and information that has

been gathered from the sources of Flight Centre Travel Group the study concludes that the business

has been successful in expanding the network of its business. The company has been successful in

acclimatizing with the change in the consumer preferences by introducing innovative business

methods. This has helped the company to remain competitive in the consumer market by meeting the

expectations of the consumer in the economic downturn.

However, due the risk faced by the company the organization is required to transform the

patterns of consumer preferences in order to remain competitive in the business. On observing the

present trends of performance, it is understood that the company provides a recurring nature of returns

in respect of the competitive threats that is faced by the company. The company should implement the

innovating business techniques to overcome the major risk faced by the organization.

Conclusion:

On arriving at the conclusion by analysing the numerous factors and information that has

been gathered from the sources of Flight Centre Travel Group the study concludes that the business

has been successful in expanding the network of its business. The company has been successful in

acclimatizing with the change in the consumer preferences by introducing innovative business

methods. This has helped the company to remain competitive in the consumer market by meeting the

expectations of the consumer in the economic downturn.

However, due the risk faced by the company the organization is required to transform the

patterns of consumer preferences in order to remain competitive in the business. On observing the

present trends of performance, it is understood that the company provides a recurring nature of returns

in respect of the competitive threats that is faced by the company. The company should implement the

innovating business techniques to overcome the major risk faced by the organization.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

19BUSINESS VALUATION AND ANALYSIS

Reference List:

Batkovsky, A.M., Batkovsky, M.A. and Klochkov, V.V., 2016. Implementation Risks in

Investment Projects on Boosting High-Tech Business Production Capacity: Analysis and

Management. Journal of Applied Economic Sciences. Romania: European Research Centre

of Managerial Studies in Business Administration, 11(6), p.44.

Borio, C., 2014. The financial cycle and macroeconomics: What have we learnt?. Journal of

Banking & Finance, 45, pp.182-198.

Drnevich, P.L. and Croson, D.C., 2013. Information technology and business-level strategy:

Toward an integrated theoretical perspective. Mis Quarterly, 37(2).

Duan, W., Cao, Q., Yu, Y. and Levy, S., 2013, January. Mining online user-generated

content: using sentiment analysis technique to study hotel service quality. In System Sciences

(HICSS), 2013 46th Hawaii International Conference on (pp. 3119-3128). IEEE.

Flight Centre Travel Group Limited. 2017. Flight Centre Travel Group Limited. [online]

Available at: http://www.fctgl.com [Accessed 26 Aug. 2017].

Flight Centre Travel Group Limited. 2017. Flight Centre Travel Group Limited. [online]

Available at: http://www.fctgl.com [Accessed 26 Aug. 2017].

Frechtling, D., 2013. The Economic impact of tourism: Overview and examples of

macroeconomic analysis. UNWTO Statistics and TSA Issues Paper Series.

Goodwin, N., Nelson, J., Harris, J., Torras, M. and Roach, B., 2013. Macroeconomics in

context. ME Sharpe.

Gupta, V.K. and Kumar, P.V.V., 2013. Value-based accounting: A performance analysis of

Indian industry. IUP Journal of Accounting Research & Audit Practices, 12(1), p.7.

Reference List:

Batkovsky, A.M., Batkovsky, M.A. and Klochkov, V.V., 2016. Implementation Risks in

Investment Projects on Boosting High-Tech Business Production Capacity: Analysis and

Management. Journal of Applied Economic Sciences. Romania: European Research Centre

of Managerial Studies in Business Administration, 11(6), p.44.

Borio, C., 2014. The financial cycle and macroeconomics: What have we learnt?. Journal of

Banking & Finance, 45, pp.182-198.

Drnevich, P.L. and Croson, D.C., 2013. Information technology and business-level strategy:

Toward an integrated theoretical perspective. Mis Quarterly, 37(2).

Duan, W., Cao, Q., Yu, Y. and Levy, S., 2013, January. Mining online user-generated

content: using sentiment analysis technique to study hotel service quality. In System Sciences

(HICSS), 2013 46th Hawaii International Conference on (pp. 3119-3128). IEEE.

Flight Centre Travel Group Limited. 2017. Flight Centre Travel Group Limited. [online]

Available at: http://www.fctgl.com [Accessed 26 Aug. 2017].

Flight Centre Travel Group Limited. 2017. Flight Centre Travel Group Limited. [online]

Available at: http://www.fctgl.com [Accessed 26 Aug. 2017].

Frechtling, D., 2013. The Economic impact of tourism: Overview and examples of

macroeconomic analysis. UNWTO Statistics and TSA Issues Paper Series.

Goodwin, N., Nelson, J., Harris, J., Torras, M. and Roach, B., 2013. Macroeconomics in

context. ME Sharpe.

Gupta, V.K. and Kumar, P.V.V., 2013. Value-based accounting: A performance analysis of

Indian industry. IUP Journal of Accounting Research & Audit Practices, 12(1), p.7.

20BUSINESS VALUATION AND ANALYSIS

Healy, P.M. and Palepu, K.G., 2012. Business analysis valuation: Using financial statements.

Cengage Learning.

Hill, C.W., Jones, G.R. and Schilling, M.A., 2014. Strategic management: theory: an

integrated approach. Cengage Learning.

ibisworld.com.au.ezproxy.lib.uts.edu.au. 2017. Single Sign On | UTS Library. [online]

Available at: http://clients1.ibisworld.com.au.ezproxy.lib.uts.edu.au/reports/au/industry/

default.aspx?entid=541 [Accessed 26 Aug. 2017].

Jenkins, W. and Williamson, D., 2015. Strategic management and business analysis.

Routledge.

Kew, J., & Stredwick, J. (2017). Business environment: managing in a strategic context.

Kogan Page Publishers.

Kim, N., 2014. Employee turnover intention among newcomers in travel

industry. International Journal of Tourism Research, 16(1), pp.56-64.

Kubasek, N.K., Brennan, B.A. and Browne, M.N., 2016. The legal environment of business:

A critical thinking approach. Pearson.

Lloyd, D.W., 2014. Battlefield tourism: Pilgrimage and the commemoration of the Great

War in Britain, Australia and Canada, 1919-1939. A&C Black.

Lok, P., Asano, G. and Rhodes, J., 2014. The influence of online reviews on decision making:

implications to the travel industry.

McManus, L., 2013. Customer accounting and marketing performance measures in the hotel

industry: Evidence from Australia. International Journal of Hospitality Management, 33,

pp.140-152.

Healy, P.M. and Palepu, K.G., 2012. Business analysis valuation: Using financial statements.

Cengage Learning.

Hill, C.W., Jones, G.R. and Schilling, M.A., 2014. Strategic management: theory: an

integrated approach. Cengage Learning.

ibisworld.com.au.ezproxy.lib.uts.edu.au. 2017. Single Sign On | UTS Library. [online]

Available at: http://clients1.ibisworld.com.au.ezproxy.lib.uts.edu.au/reports/au/industry/

default.aspx?entid=541 [Accessed 26 Aug. 2017].

Jenkins, W. and Williamson, D., 2015. Strategic management and business analysis.

Routledge.

Kew, J., & Stredwick, J. (2017). Business environment: managing in a strategic context.

Kogan Page Publishers.

Kim, N., 2014. Employee turnover intention among newcomers in travel

industry. International Journal of Tourism Research, 16(1), pp.56-64.

Kubasek, N.K., Brennan, B.A. and Browne, M.N., 2016. The legal environment of business:

A critical thinking approach. Pearson.

Lloyd, D.W., 2014. Battlefield tourism: Pilgrimage and the commemoration of the Great

War in Britain, Australia and Canada, 1919-1939. A&C Black.

Lok, P., Asano, G. and Rhodes, J., 2014. The influence of online reviews on decision making:

implications to the travel industry.

McManus, L., 2013. Customer accounting and marketing performance measures in the hotel

industry: Evidence from Australia. International Journal of Hospitality Management, 33,

pp.140-152.

21BUSINESS VALUATION AND ANALYSIS

Meng, W., Xu, L., Hu, B., Zhou, J. and Wang, Z., 2016. Quantifying direct and indirect

carbon dioxide emissions of the Chinese tourism industry. Journal of Cleaner

Production, 126, pp.586-594.

Mishra, C.S. and Zachary, R.K., 2014. Business Model Theory. In The Theory of

Entrepreneurship (pp. 227-250). Palgrave Macmillan US.

Palepu, K.G., Healy, P.M. and Peek, E., 2013. Business analysis and valuation: IFRS edition.

Cengage Learning.

Palepu, K.G., Healy, P.M. and Peek, E., 2013. Business analysis and valuation: IFRS edition.

Cengage Learning.

Pettersson, K. and Sorensen, O., 2016. A short integrated presentation of valuation,

profitability and growth analysis. International Journal of Accounting and Finance, 6(1),

pp.43-61.

Raubenheimer, H. and Stammen-Hegener, C., 2013. Modern concepts of the theory of the

firm: managing enterprises of the new economy. Springer Science & Business Media.

Rhee, H.T. and Yang, S.B., 2015. How does hotel attribute importance vary among different

travelers? An exploratory case study based on a conjoint analysis. Electronic markets, 25(3),

pp.211-226.

Rheem, C., 2016. Outlook for Leisure Travel and Attractions.