Fixed Income and Credit Risk

VerifiedAdded on 2023/06/04

|40

|5316

|197

AI Summary

This document provides an in-depth discussion on the subject of bond interest structure, forwards rates and bonds spread with the objective of selecting two bonds issuer who shall have both the elements of corporates and two sovereign nations European Bank for Reconstruction and Development and Deutsche Bank AG.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: FIXED INCOME AND CREDIT RISK

Fixed Income and Credit Risk

Name of the Student:

Name of the University:

Authors Note:

Fixed Income and Credit Risk

Name of the Student:

Name of the University:

Authors Note:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1

FIXED INCOME AND CREDIT RISK

Contents

Introduction:....................................................................................................................................2

Part 1:...............................................................................................................................................2

Part 2:.............................................................................................................................................10

Part 3:.............................................................................................................................................21

Part 4:.............................................................................................................................................37

FIXED INCOME AND CREDIT RISK

Contents

Introduction:....................................................................................................................................2

Part 1:...............................................................................................................................................2

Part 2:.............................................................................................................................................10

Part 3:.............................................................................................................................................21

Part 4:.............................................................................................................................................37

2

FIXED INCOME AND CREDIT RISK

Introduction:

In order to provide in-depth discussion on the subject of bond interest structure, forwards

rates and bonds spread it is firstly essential to select two different bond issuers. The document

brief has asked to consider two bonds of sovereign nations or use two corporate bonds. However,

with the objective of selecting two bonds issuer who shall have both the elements of corporates

and two sovereign nations European Bank for Reconstruction and Development and Deutsche

Bank AG have been selected. Detailed discussion on the bonds issued by the two different

financial institutes from different countries have been made here with the objective of providing

necessary information to the readers on different elements of bonds.

Part 1:

Firstly let’s have the brief details about the bonds issued by European Bank for

Reconstruction and Development and Deutsche Bank AG. A clear understanding about the terms

and conditions of the bonds issued by the European Bank for Reconstruction and Development,

here in after to be referred to as EBRD only in this document and Deutsche Bank AG, here in

after to be referred to as Deutsche only in this document shall helpful in estimating the interest

structures, calculate forward rates and comment on the spread (Du, Tepper and Verdelhan,

2018).

The table below contains the information about the bonds issued by EBRD.

FIXED INCOME AND CREDIT RISK

Introduction:

In order to provide in-depth discussion on the subject of bond interest structure, forwards

rates and bonds spread it is firstly essential to select two different bond issuers. The document

brief has asked to consider two bonds of sovereign nations or use two corporate bonds. However,

with the objective of selecting two bonds issuer who shall have both the elements of corporates

and two sovereign nations European Bank for Reconstruction and Development and Deutsche

Bank AG have been selected. Detailed discussion on the bonds issued by the two different

financial institutes from different countries have been made here with the objective of providing

necessary information to the readers on different elements of bonds.

Part 1:

Firstly let’s have the brief details about the bonds issued by European Bank for

Reconstruction and Development and Deutsche Bank AG. A clear understanding about the terms

and conditions of the bonds issued by the European Bank for Reconstruction and Development,

here in after to be referred to as EBRD only in this document and Deutsche Bank AG, here in

after to be referred to as Deutsche only in this document shall helpful in estimating the interest

structures, calculate forward rates and comment on the spread (Du, Tepper and Verdelhan,

2018).

The table below contains the information about the bonds issued by EBRD.

3

FIXED INCOME AND CREDIT RISK

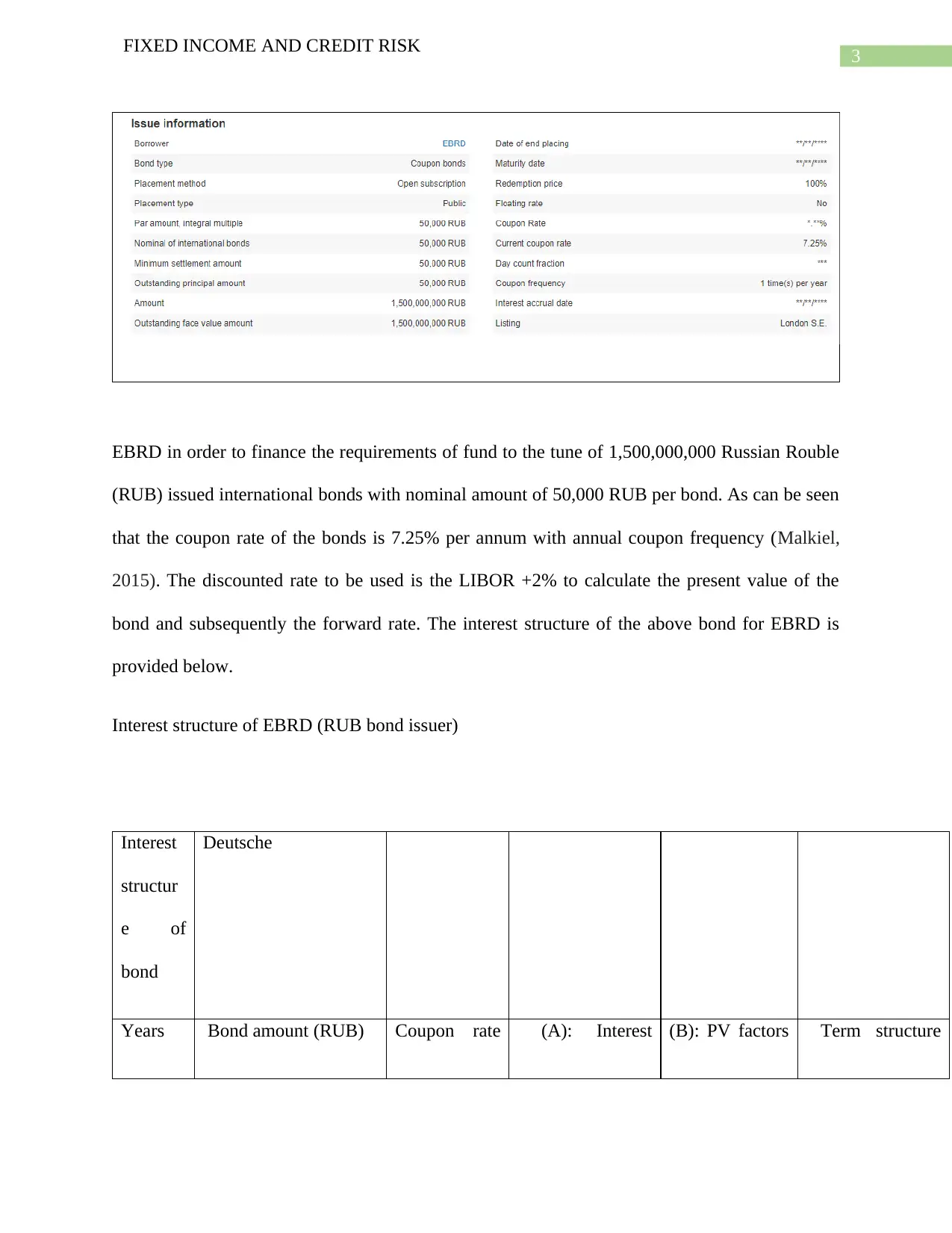

EBRD in order to finance the requirements of fund to the tune of 1,500,000,000 Russian Rouble

(RUB) issued international bonds with nominal amount of 50,000 RUB per bond. As can be seen

that the coupon rate of the bonds is 7.25% per annum with annual coupon frequency (Malkiel,

2015). The discounted rate to be used is the LIBOR +2% to calculate the present value of the

bond and subsequently the forward rate. The interest structure of the above bond for EBRD is

provided below.

Interest structure of EBRD (RUB bond issuer)

Interest

structur

e of

bond

Deutsche

Years Bond amount (RUB) Coupon rate (A): Interest (B): PV factors Term structure

FIXED INCOME AND CREDIT RISK

EBRD in order to finance the requirements of fund to the tune of 1,500,000,000 Russian Rouble

(RUB) issued international bonds with nominal amount of 50,000 RUB per bond. As can be seen

that the coupon rate of the bonds is 7.25% per annum with annual coupon frequency (Malkiel,

2015). The discounted rate to be used is the LIBOR +2% to calculate the present value of the

bond and subsequently the forward rate. The interest structure of the above bond for EBRD is

provided below.

Interest structure of EBRD (RUB bond issuer)

Interest

structur

e of

bond

Deutsche

Years Bond amount (RUB) Coupon rate (A): Interest (B): PV factors Term structure

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4

FIXED INCOME AND CREDIT RISK

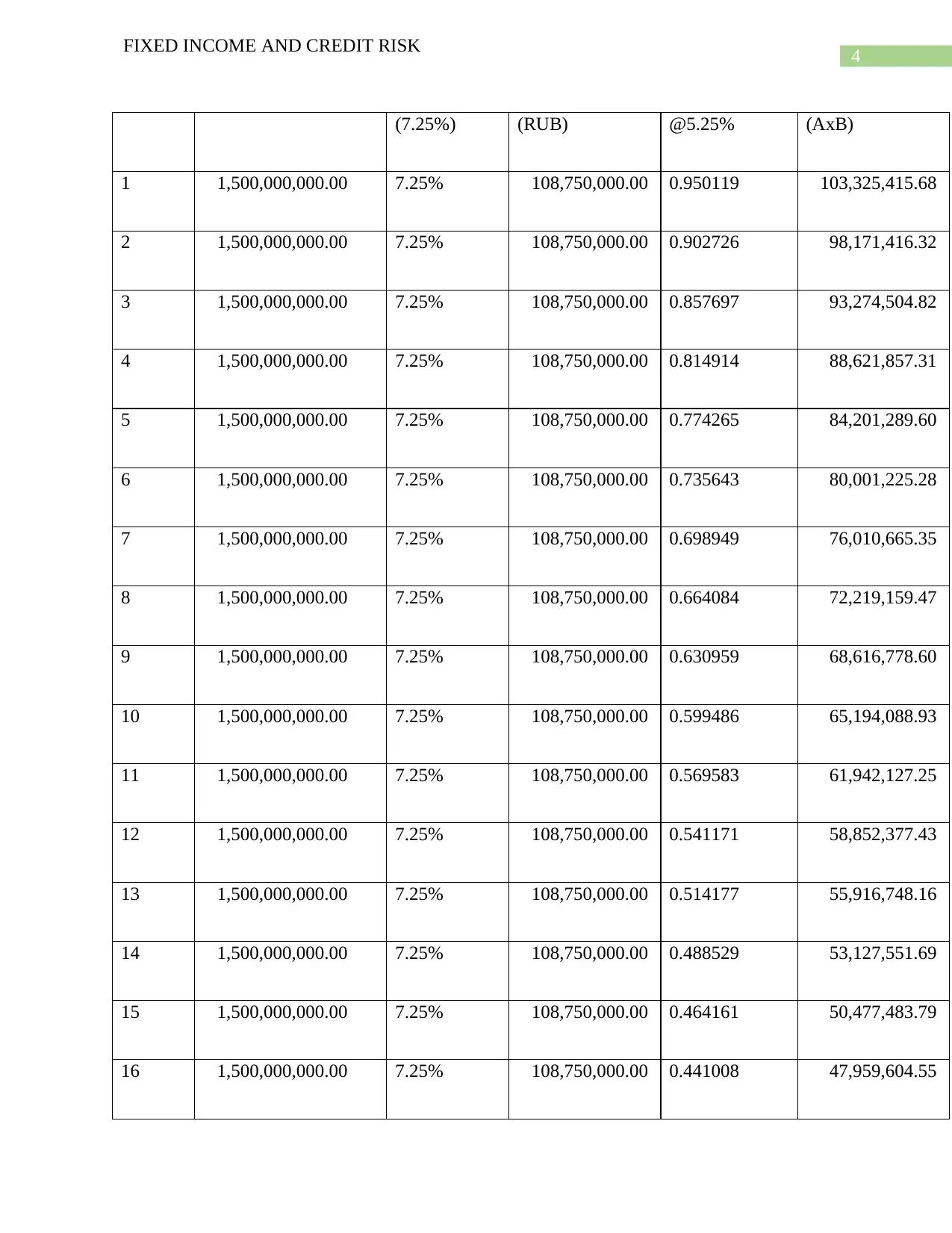

(7.25%) (RUB) @5.25% (AxB)

1 1,500,000,000.00 7.25% 108,750,000.00 0.950119 103,325,415.68

2 1,500,000,000.00 7.25% 108,750,000.00 0.902726 98,171,416.32

3 1,500,000,000.00 7.25% 108,750,000.00 0.857697 93,274,504.82

4 1,500,000,000.00 7.25% 108,750,000.00 0.814914 88,621,857.31

5 1,500,000,000.00 7.25% 108,750,000.00 0.774265 84,201,289.60

6 1,500,000,000.00 7.25% 108,750,000.00 0.735643 80,001,225.28

7 1,500,000,000.00 7.25% 108,750,000.00 0.698949 76,010,665.35

8 1,500,000,000.00 7.25% 108,750,000.00 0.664084 72,219,159.47

9 1,500,000,000.00 7.25% 108,750,000.00 0.630959 68,616,778.60

10 1,500,000,000.00 7.25% 108,750,000.00 0.599486 65,194,088.93

11 1,500,000,000.00 7.25% 108,750,000.00 0.569583 61,942,127.25

12 1,500,000,000.00 7.25% 108,750,000.00 0.541171 58,852,377.43

13 1,500,000,000.00 7.25% 108,750,000.00 0.514177 55,916,748.16

14 1,500,000,000.00 7.25% 108,750,000.00 0.488529 53,127,551.69

15 1,500,000,000.00 7.25% 108,750,000.00 0.464161 50,477,483.79

16 1,500,000,000.00 7.25% 108,750,000.00 0.441008 47,959,604.55

FIXED INCOME AND CREDIT RISK

(7.25%) (RUB) @5.25% (AxB)

1 1,500,000,000.00 7.25% 108,750,000.00 0.950119 103,325,415.68

2 1,500,000,000.00 7.25% 108,750,000.00 0.902726 98,171,416.32

3 1,500,000,000.00 7.25% 108,750,000.00 0.857697 93,274,504.82

4 1,500,000,000.00 7.25% 108,750,000.00 0.814914 88,621,857.31

5 1,500,000,000.00 7.25% 108,750,000.00 0.774265 84,201,289.60

6 1,500,000,000.00 7.25% 108,750,000.00 0.735643 80,001,225.28

7 1,500,000,000.00 7.25% 108,750,000.00 0.698949 76,010,665.35

8 1,500,000,000.00 7.25% 108,750,000.00 0.664084 72,219,159.47

9 1,500,000,000.00 7.25% 108,750,000.00 0.630959 68,616,778.60

10 1,500,000,000.00 7.25% 108,750,000.00 0.599486 65,194,088.93

11 1,500,000,000.00 7.25% 108,750,000.00 0.569583 61,942,127.25

12 1,500,000,000.00 7.25% 108,750,000.00 0.541171 58,852,377.43

13 1,500,000,000.00 7.25% 108,750,000.00 0.514177 55,916,748.16

14 1,500,000,000.00 7.25% 108,750,000.00 0.488529 53,127,551.69

15 1,500,000,000.00 7.25% 108,750,000.00 0.464161 50,477,483.79

16 1,500,000,000.00 7.25% 108,750,000.00 0.441008 47,959,604.55

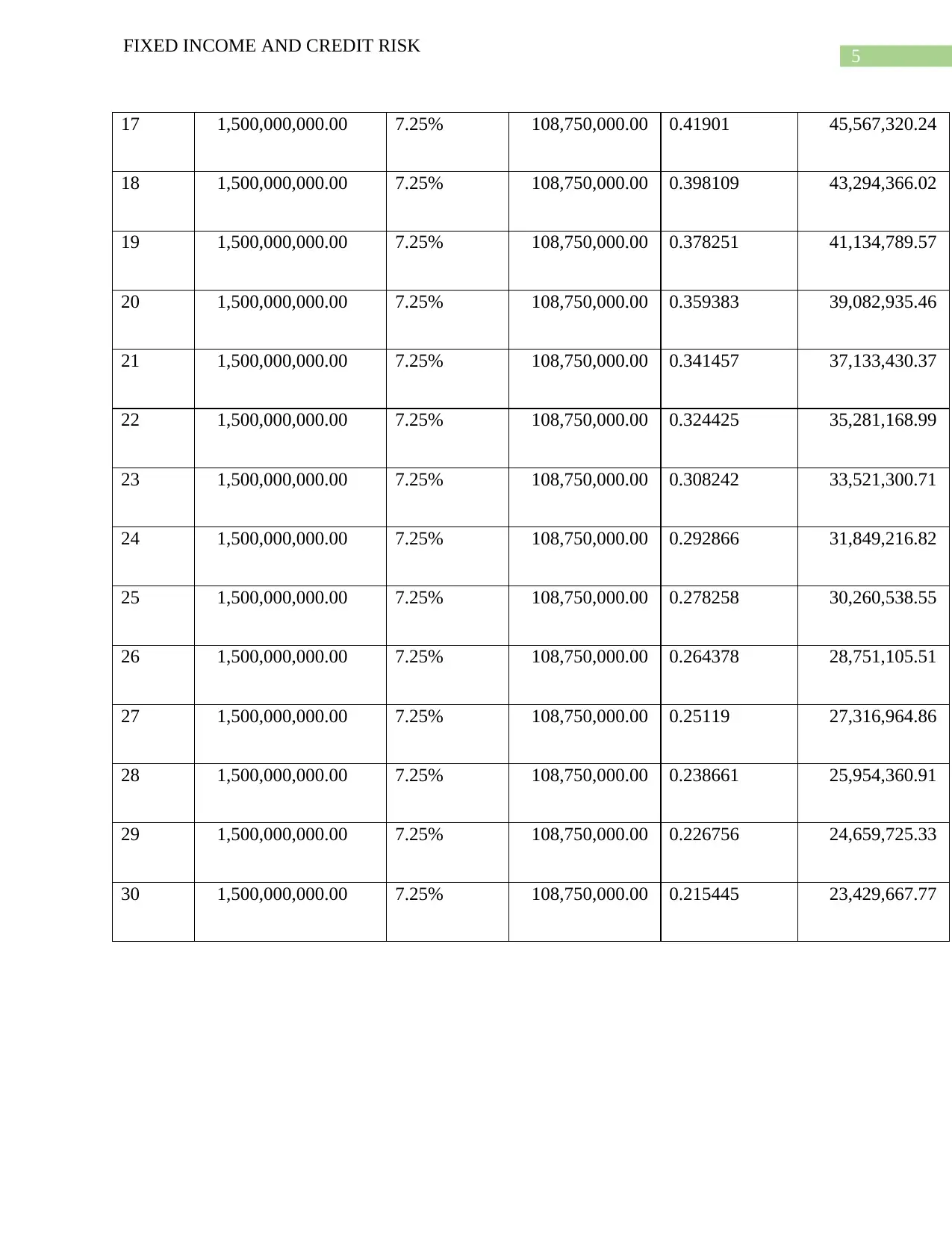

5

FIXED INCOME AND CREDIT RISK

17 1,500,000,000.00 7.25% 108,750,000.00 0.41901 45,567,320.24

18 1,500,000,000.00 7.25% 108,750,000.00 0.398109 43,294,366.02

19 1,500,000,000.00 7.25% 108,750,000.00 0.378251 41,134,789.57

20 1,500,000,000.00 7.25% 108,750,000.00 0.359383 39,082,935.46

21 1,500,000,000.00 7.25% 108,750,000.00 0.341457 37,133,430.37

22 1,500,000,000.00 7.25% 108,750,000.00 0.324425 35,281,168.99

23 1,500,000,000.00 7.25% 108,750,000.00 0.308242 33,521,300.71

24 1,500,000,000.00 7.25% 108,750,000.00 0.292866 31,849,216.82

25 1,500,000,000.00 7.25% 108,750,000.00 0.278258 30,260,538.55

26 1,500,000,000.00 7.25% 108,750,000.00 0.264378 28,751,105.51

27 1,500,000,000.00 7.25% 108,750,000.00 0.25119 27,316,964.86

28 1,500,000,000.00 7.25% 108,750,000.00 0.238661 25,954,360.91

29 1,500,000,000.00 7.25% 108,750,000.00 0.226756 24,659,725.33

30 1,500,000,000.00 7.25% 108,750,000.00 0.215445 23,429,667.77

FIXED INCOME AND CREDIT RISK

17 1,500,000,000.00 7.25% 108,750,000.00 0.41901 45,567,320.24

18 1,500,000,000.00 7.25% 108,750,000.00 0.398109 43,294,366.02

19 1,500,000,000.00 7.25% 108,750,000.00 0.378251 41,134,789.57

20 1,500,000,000.00 7.25% 108,750,000.00 0.359383 39,082,935.46

21 1,500,000,000.00 7.25% 108,750,000.00 0.341457 37,133,430.37

22 1,500,000,000.00 7.25% 108,750,000.00 0.324425 35,281,168.99

23 1,500,000,000.00 7.25% 108,750,000.00 0.308242 33,521,300.71

24 1,500,000,000.00 7.25% 108,750,000.00 0.292866 31,849,216.82

25 1,500,000,000.00 7.25% 108,750,000.00 0.278258 30,260,538.55

26 1,500,000,000.00 7.25% 108,750,000.00 0.264378 28,751,105.51

27 1,500,000,000.00 7.25% 108,750,000.00 0.25119 27,316,964.86

28 1,500,000,000.00 7.25% 108,750,000.00 0.238661 25,954,360.91

29 1,500,000,000.00 7.25% 108,750,000.00 0.226756 24,659,725.33

30 1,500,000,000.00 7.25% 108,750,000.00 0.215445 23,429,667.77

6

FIXED INCOME AND CREDIT RISK

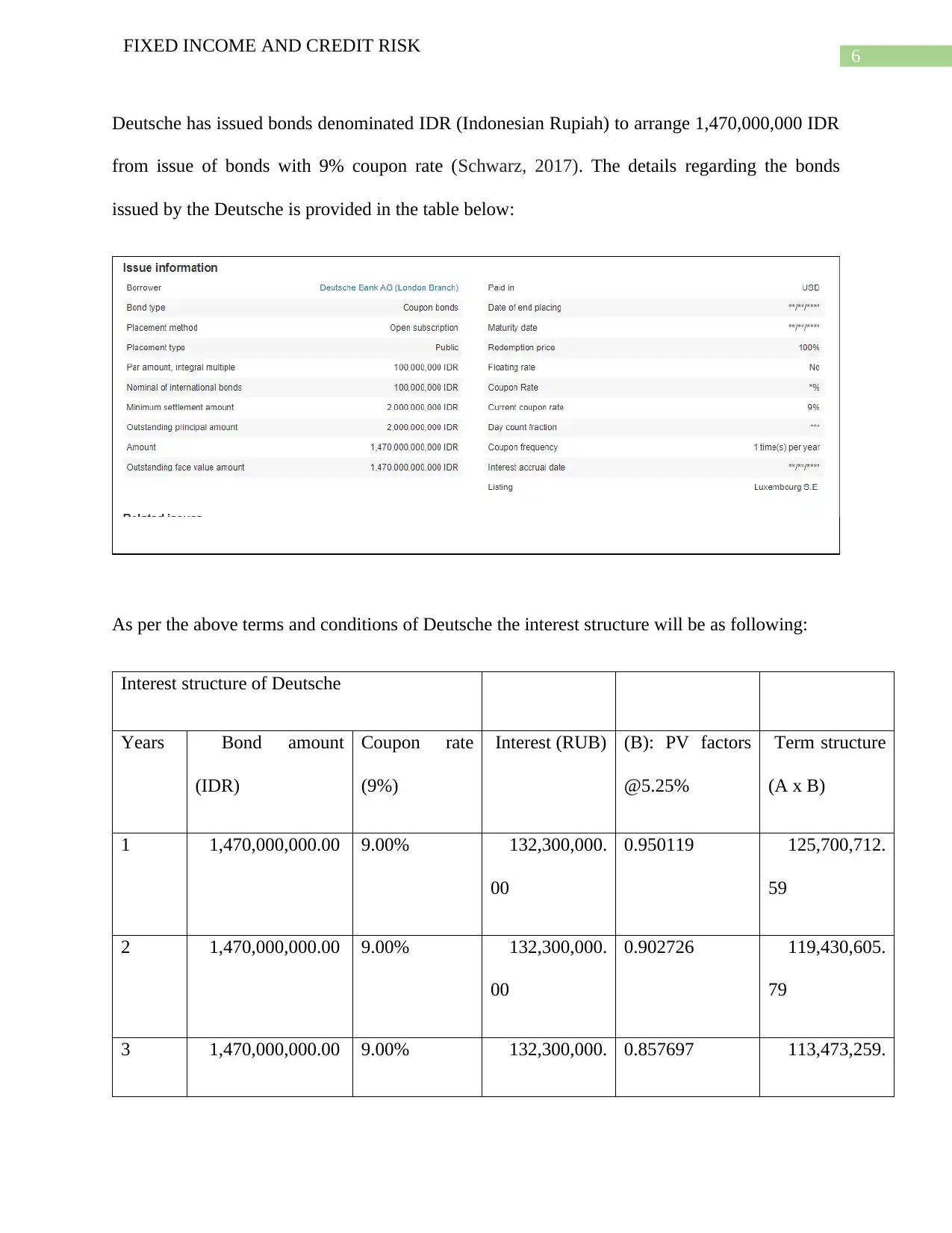

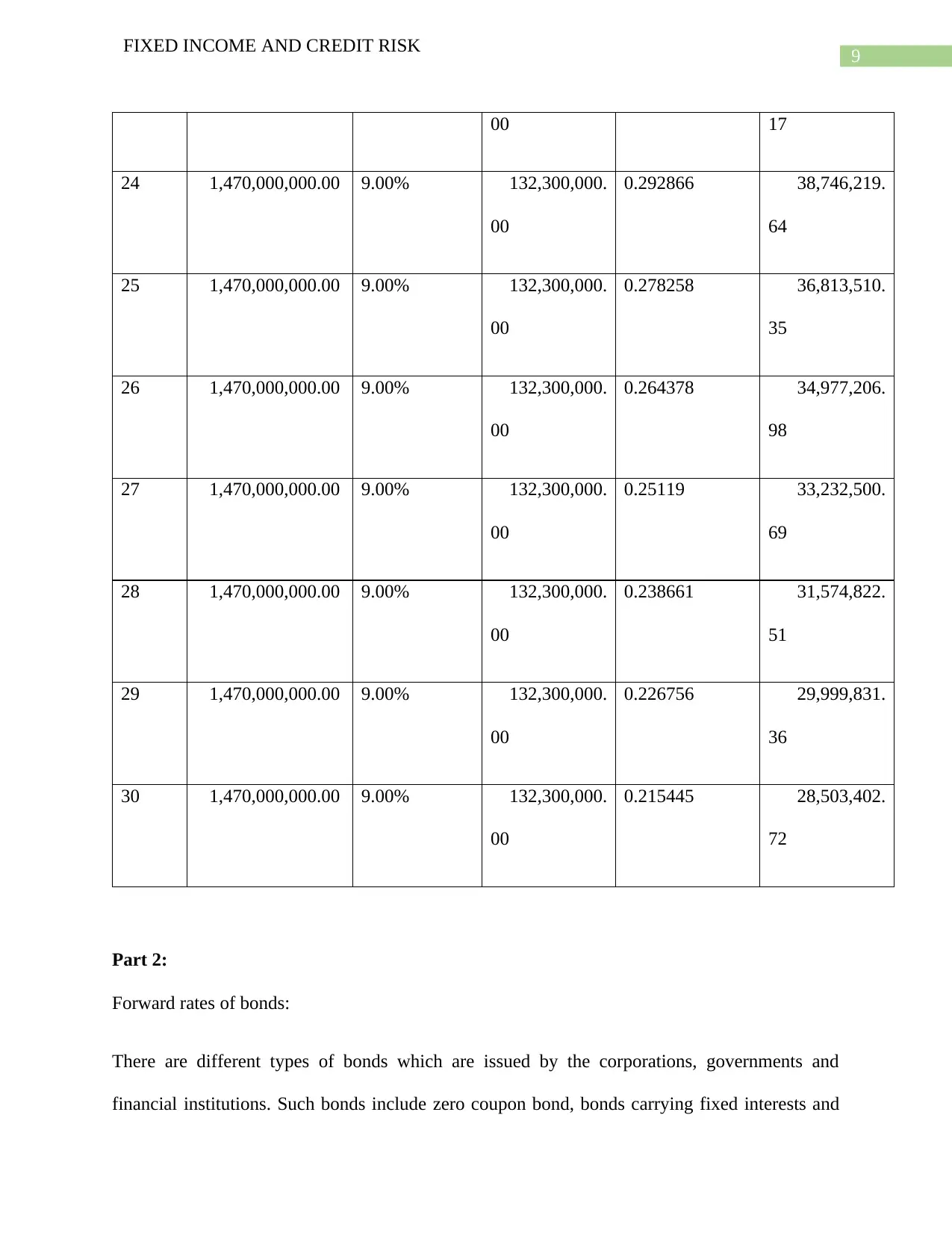

Deutsche has issued bonds denominated IDR (Indonesian Rupiah) to arrange 1,470,000,000 IDR

from issue of bonds with 9% coupon rate (Schwarz, 2017). The details regarding the bonds

issued by the Deutsche is provided in the table below:

As per the above terms and conditions of Deutsche the interest structure will be as following:

Interest structure of Deutsche

Years Bond amount

(IDR)

Coupon rate

(9%)

Interest (RUB) (B): PV factors

@5.25%

Term structure

(A x B)

1 1,470,000,000.00 9.00% 132,300,000.

00

0.950119 125,700,712.

59

2 1,470,000,000.00 9.00% 132,300,000.

00

0.902726 119,430,605.

79

3 1,470,000,000.00 9.00% 132,300,000. 0.857697 113,473,259.

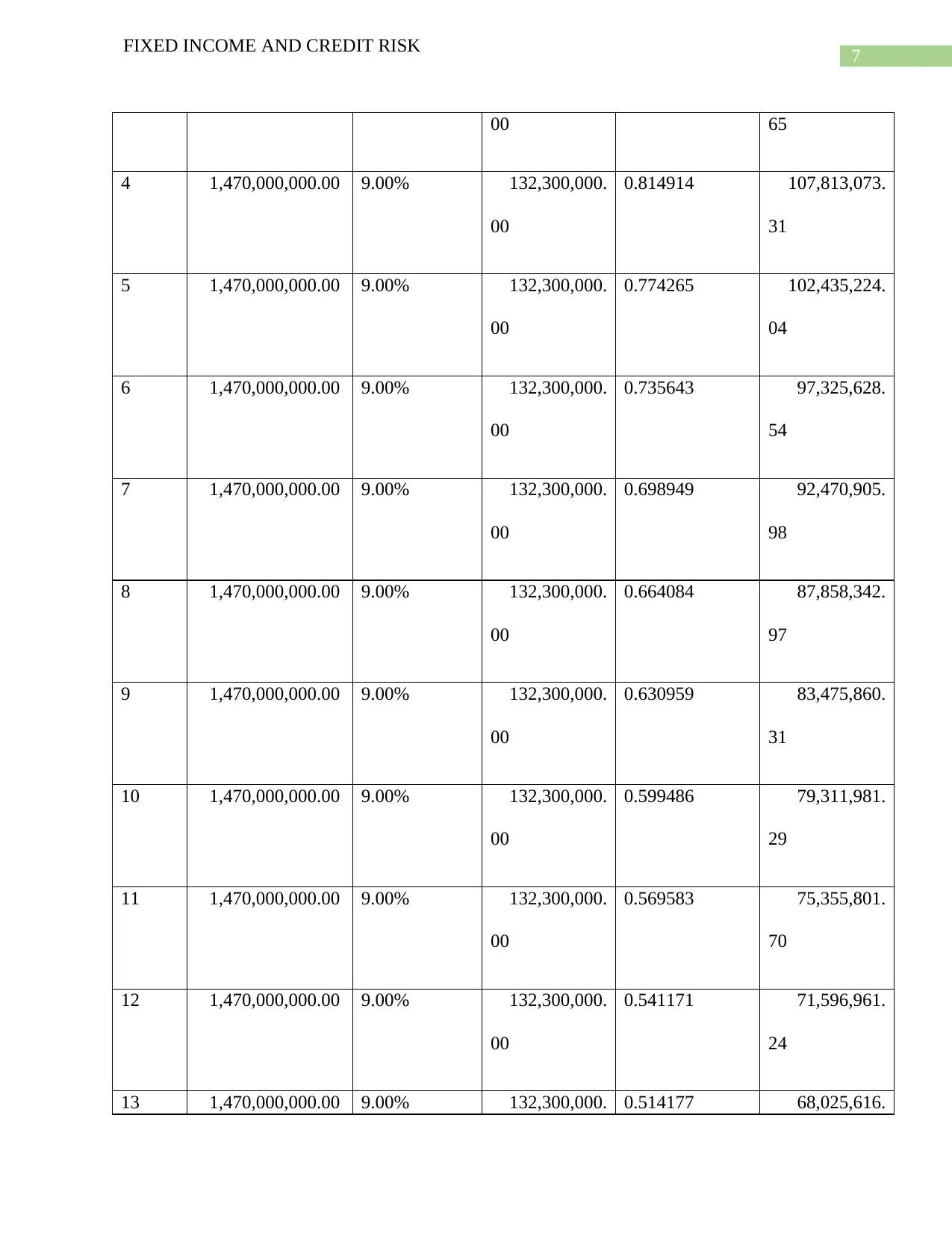

FIXED INCOME AND CREDIT RISK

Deutsche has issued bonds denominated IDR (Indonesian Rupiah) to arrange 1,470,000,000 IDR

from issue of bonds with 9% coupon rate (Schwarz, 2017). The details regarding the bonds

issued by the Deutsche is provided in the table below:

As per the above terms and conditions of Deutsche the interest structure will be as following:

Interest structure of Deutsche

Years Bond amount

(IDR)

Coupon rate

(9%)

Interest (RUB) (B): PV factors

@5.25%

Term structure

(A x B)

1 1,470,000,000.00 9.00% 132,300,000.

00

0.950119 125,700,712.

59

2 1,470,000,000.00 9.00% 132,300,000.

00

0.902726 119,430,605.

79

3 1,470,000,000.00 9.00% 132,300,000. 0.857697 113,473,259.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

FIXED INCOME AND CREDIT RISK

00 65

4 1,470,000,000.00 9.00% 132,300,000.

00

0.814914 107,813,073.

31

5 1,470,000,000.00 9.00% 132,300,000.

00

0.774265 102,435,224.

04

6 1,470,000,000.00 9.00% 132,300,000.

00

0.735643 97,325,628.

54

7 1,470,000,000.00 9.00% 132,300,000.

00

0.698949 92,470,905.

98

8 1,470,000,000.00 9.00% 132,300,000.

00

0.664084 87,858,342.

97

9 1,470,000,000.00 9.00% 132,300,000.

00

0.630959 83,475,860.

31

10 1,470,000,000.00 9.00% 132,300,000.

00

0.599486 79,311,981.

29

11 1,470,000,000.00 9.00% 132,300,000.

00

0.569583 75,355,801.

70

12 1,470,000,000.00 9.00% 132,300,000.

00

0.541171 71,596,961.

24

13 1,470,000,000.00 9.00% 132,300,000. 0.514177 68,025,616.

FIXED INCOME AND CREDIT RISK

00 65

4 1,470,000,000.00 9.00% 132,300,000.

00

0.814914 107,813,073.

31

5 1,470,000,000.00 9.00% 132,300,000.

00

0.774265 102,435,224.

04

6 1,470,000,000.00 9.00% 132,300,000.

00

0.735643 97,325,628.

54

7 1,470,000,000.00 9.00% 132,300,000.

00

0.698949 92,470,905.

98

8 1,470,000,000.00 9.00% 132,300,000.

00

0.664084 87,858,342.

97

9 1,470,000,000.00 9.00% 132,300,000.

00

0.630959 83,475,860.

31

10 1,470,000,000.00 9.00% 132,300,000.

00

0.599486 79,311,981.

29

11 1,470,000,000.00 9.00% 132,300,000.

00

0.569583 75,355,801.

70

12 1,470,000,000.00 9.00% 132,300,000.

00

0.541171 71,596,961.

24

13 1,470,000,000.00 9.00% 132,300,000. 0.514177 68,025,616.

8

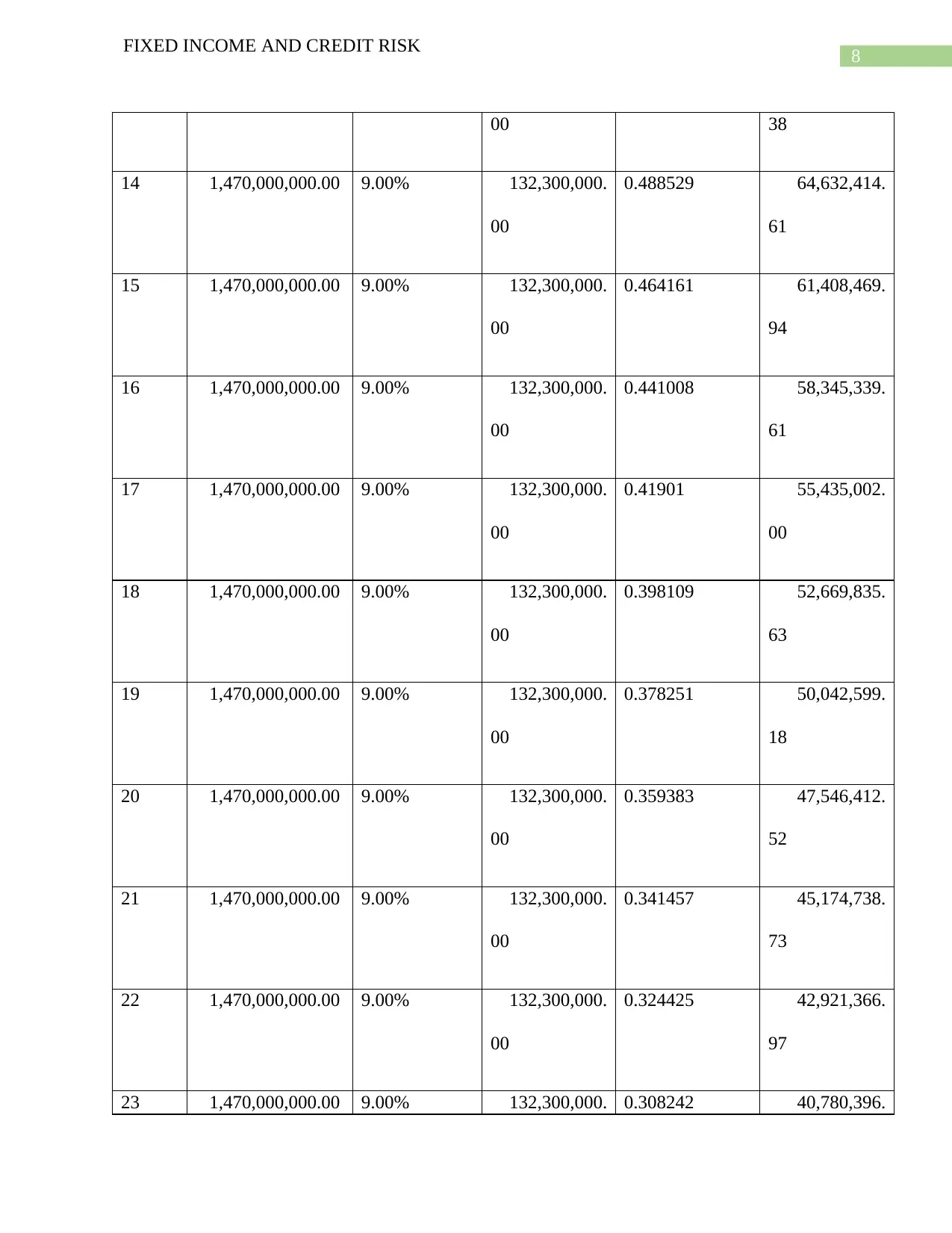

FIXED INCOME AND CREDIT RISK

00 38

14 1,470,000,000.00 9.00% 132,300,000.

00

0.488529 64,632,414.

61

15 1,470,000,000.00 9.00% 132,300,000.

00

0.464161 61,408,469.

94

16 1,470,000,000.00 9.00% 132,300,000.

00

0.441008 58,345,339.

61

17 1,470,000,000.00 9.00% 132,300,000.

00

0.41901 55,435,002.

00

18 1,470,000,000.00 9.00% 132,300,000.

00

0.398109 52,669,835.

63

19 1,470,000,000.00 9.00% 132,300,000.

00

0.378251 50,042,599.

18

20 1,470,000,000.00 9.00% 132,300,000.

00

0.359383 47,546,412.

52

21 1,470,000,000.00 9.00% 132,300,000.

00

0.341457 45,174,738.

73

22 1,470,000,000.00 9.00% 132,300,000.

00

0.324425 42,921,366.

97

23 1,470,000,000.00 9.00% 132,300,000. 0.308242 40,780,396.

FIXED INCOME AND CREDIT RISK

00 38

14 1,470,000,000.00 9.00% 132,300,000.

00

0.488529 64,632,414.

61

15 1,470,000,000.00 9.00% 132,300,000.

00

0.464161 61,408,469.

94

16 1,470,000,000.00 9.00% 132,300,000.

00

0.441008 58,345,339.

61

17 1,470,000,000.00 9.00% 132,300,000.

00

0.41901 55,435,002.

00

18 1,470,000,000.00 9.00% 132,300,000.

00

0.398109 52,669,835.

63

19 1,470,000,000.00 9.00% 132,300,000.

00

0.378251 50,042,599.

18

20 1,470,000,000.00 9.00% 132,300,000.

00

0.359383 47,546,412.

52

21 1,470,000,000.00 9.00% 132,300,000.

00

0.341457 45,174,738.

73

22 1,470,000,000.00 9.00% 132,300,000.

00

0.324425 42,921,366.

97

23 1,470,000,000.00 9.00% 132,300,000. 0.308242 40,780,396.

9

FIXED INCOME AND CREDIT RISK

00 17

24 1,470,000,000.00 9.00% 132,300,000.

00

0.292866 38,746,219.

64

25 1,470,000,000.00 9.00% 132,300,000.

00

0.278258 36,813,510.

35

26 1,470,000,000.00 9.00% 132,300,000.

00

0.264378 34,977,206.

98

27 1,470,000,000.00 9.00% 132,300,000.

00

0.25119 33,232,500.

69

28 1,470,000,000.00 9.00% 132,300,000.

00

0.238661 31,574,822.

51

29 1,470,000,000.00 9.00% 132,300,000.

00

0.226756 29,999,831.

36

30 1,470,000,000.00 9.00% 132,300,000.

00

0.215445 28,503,402.

72

Part 2:

Forward rates of bonds:

There are different types of bonds which are issued by the corporations, governments and

financial institutions. Such bonds include zero coupon bond, bonds carrying fixed interests and

FIXED INCOME AND CREDIT RISK

00 17

24 1,470,000,000.00 9.00% 132,300,000.

00

0.292866 38,746,219.

64

25 1,470,000,000.00 9.00% 132,300,000.

00

0.278258 36,813,510.

35

26 1,470,000,000.00 9.00% 132,300,000.

00

0.264378 34,977,206.

98

27 1,470,000,000.00 9.00% 132,300,000.

00

0.25119 33,232,500.

69

28 1,470,000,000.00 9.00% 132,300,000.

00

0.238661 31,574,822.

51

29 1,470,000,000.00 9.00% 132,300,000.

00

0.226756 29,999,831.

36

30 1,470,000,000.00 9.00% 132,300,000.

00

0.215445 28,503,402.

72

Part 2:

Forward rates of bonds:

There are different types of bonds which are issued by the corporations, governments and

financial institutions. Such bonds include zero coupon bond, bonds carrying fixed interests and

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10

FIXED INCOME AND CREDIT RISK

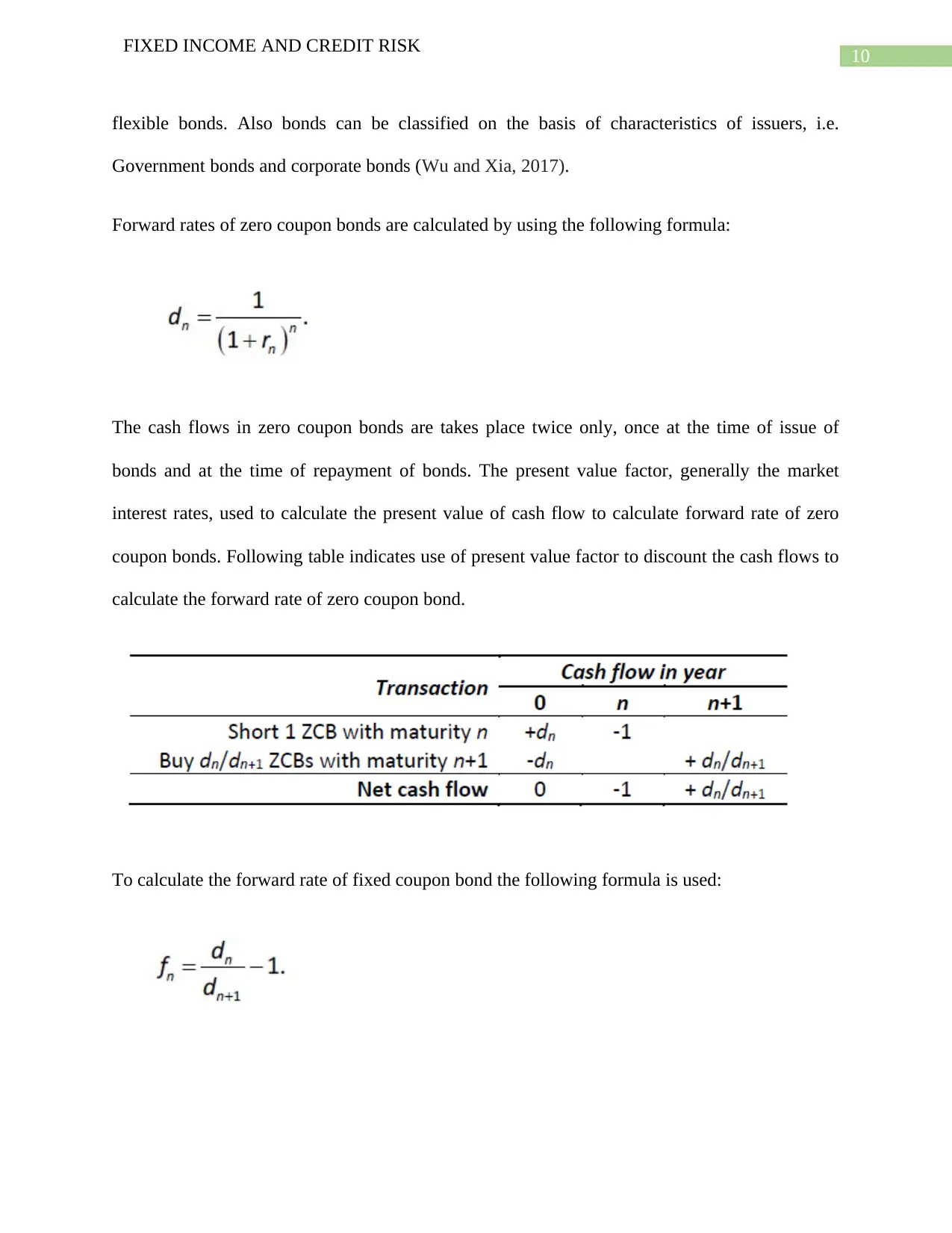

flexible bonds. Also bonds can be classified on the basis of characteristics of issuers, i.e.

Government bonds and corporate bonds (Wu and Xia, 2017).

Forward rates of zero coupon bonds are calculated by using the following formula:

The cash flows in zero coupon bonds are takes place twice only, once at the time of issue of

bonds and at the time of repayment of bonds. The present value factor, generally the market

interest rates, used to calculate the present value of cash flow to calculate forward rate of zero

coupon bonds. Following table indicates use of present value factor to discount the cash flows to

calculate the forward rate of zero coupon bond.

To calculate the forward rate of fixed coupon bond the following formula is used:

FIXED INCOME AND CREDIT RISK

flexible bonds. Also bonds can be classified on the basis of characteristics of issuers, i.e.

Government bonds and corporate bonds (Wu and Xia, 2017).

Forward rates of zero coupon bonds are calculated by using the following formula:

The cash flows in zero coupon bonds are takes place twice only, once at the time of issue of

bonds and at the time of repayment of bonds. The present value factor, generally the market

interest rates, used to calculate the present value of cash flow to calculate forward rate of zero

coupon bonds. Following table indicates use of present value factor to discount the cash flows to

calculate the forward rate of zero coupon bond.

To calculate the forward rate of fixed coupon bond the following formula is used:

11

FIXED INCOME AND CREDIT RISK

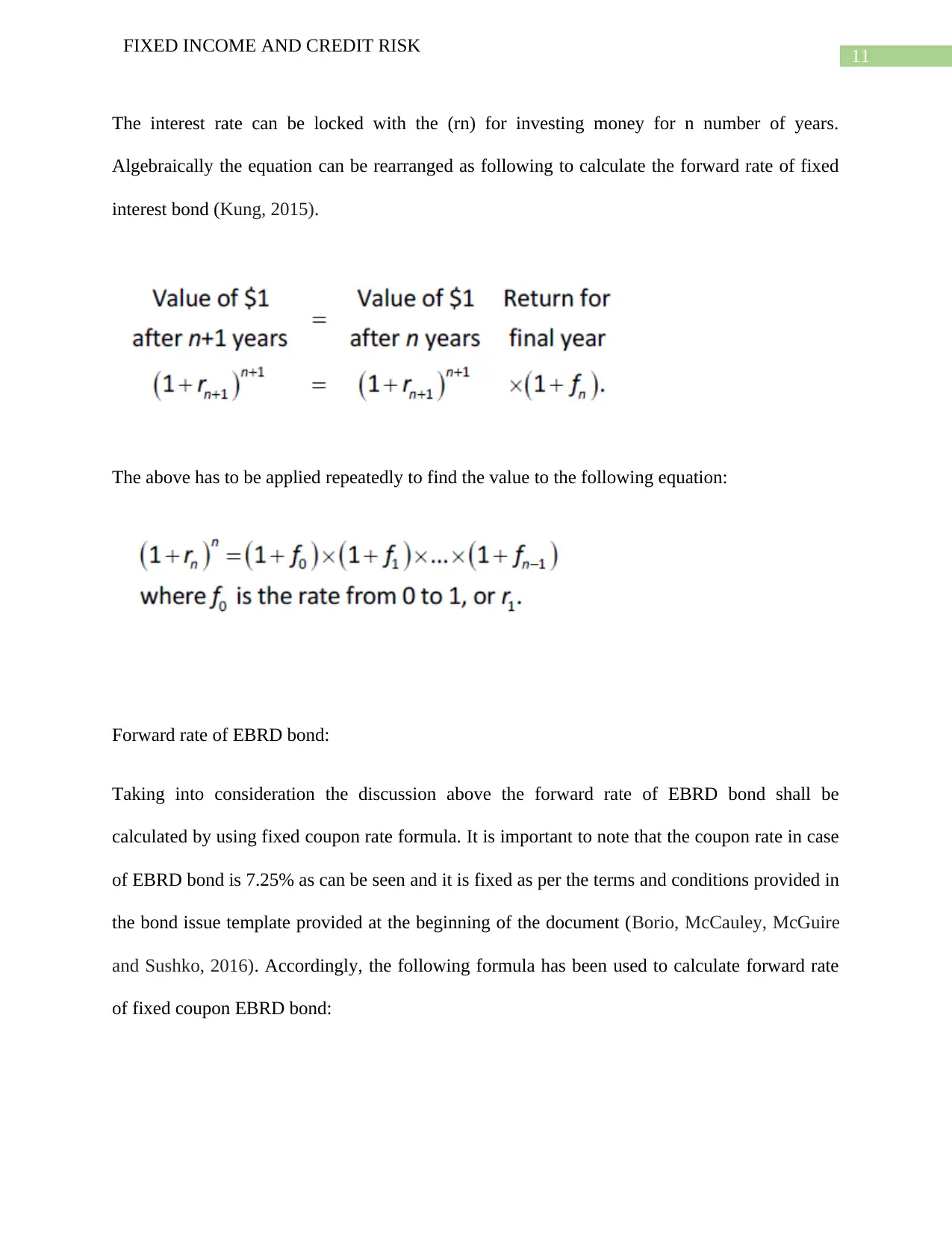

The interest rate can be locked with the (rn) for investing money for n number of years.

Algebraically the equation can be rearranged as following to calculate the forward rate of fixed

interest bond (Kung, 2015).

The above has to be applied repeatedly to find the value to the following equation:

Forward rate of EBRD bond:

Taking into consideration the discussion above the forward rate of EBRD bond shall be

calculated by using fixed coupon rate formula. It is important to note that the coupon rate in case

of EBRD bond is 7.25% as can be seen and it is fixed as per the terms and conditions provided in

the bond issue template provided at the beginning of the document (Borio, McCauley, McGuire

and Sushko, 2016). Accordingly, the following formula has been used to calculate forward rate

of fixed coupon EBRD bond:

FIXED INCOME AND CREDIT RISK

The interest rate can be locked with the (rn) for investing money for n number of years.

Algebraically the equation can be rearranged as following to calculate the forward rate of fixed

interest bond (Kung, 2015).

The above has to be applied repeatedly to find the value to the following equation:

Forward rate of EBRD bond:

Taking into consideration the discussion above the forward rate of EBRD bond shall be

calculated by using fixed coupon rate formula. It is important to note that the coupon rate in case

of EBRD bond is 7.25% as can be seen and it is fixed as per the terms and conditions provided in

the bond issue template provided at the beginning of the document (Borio, McCauley, McGuire

and Sushko, 2016). Accordingly, the following formula has been used to calculate forward rate

of fixed coupon EBRD bond:

12

FIXED INCOME AND CREDIT RISK

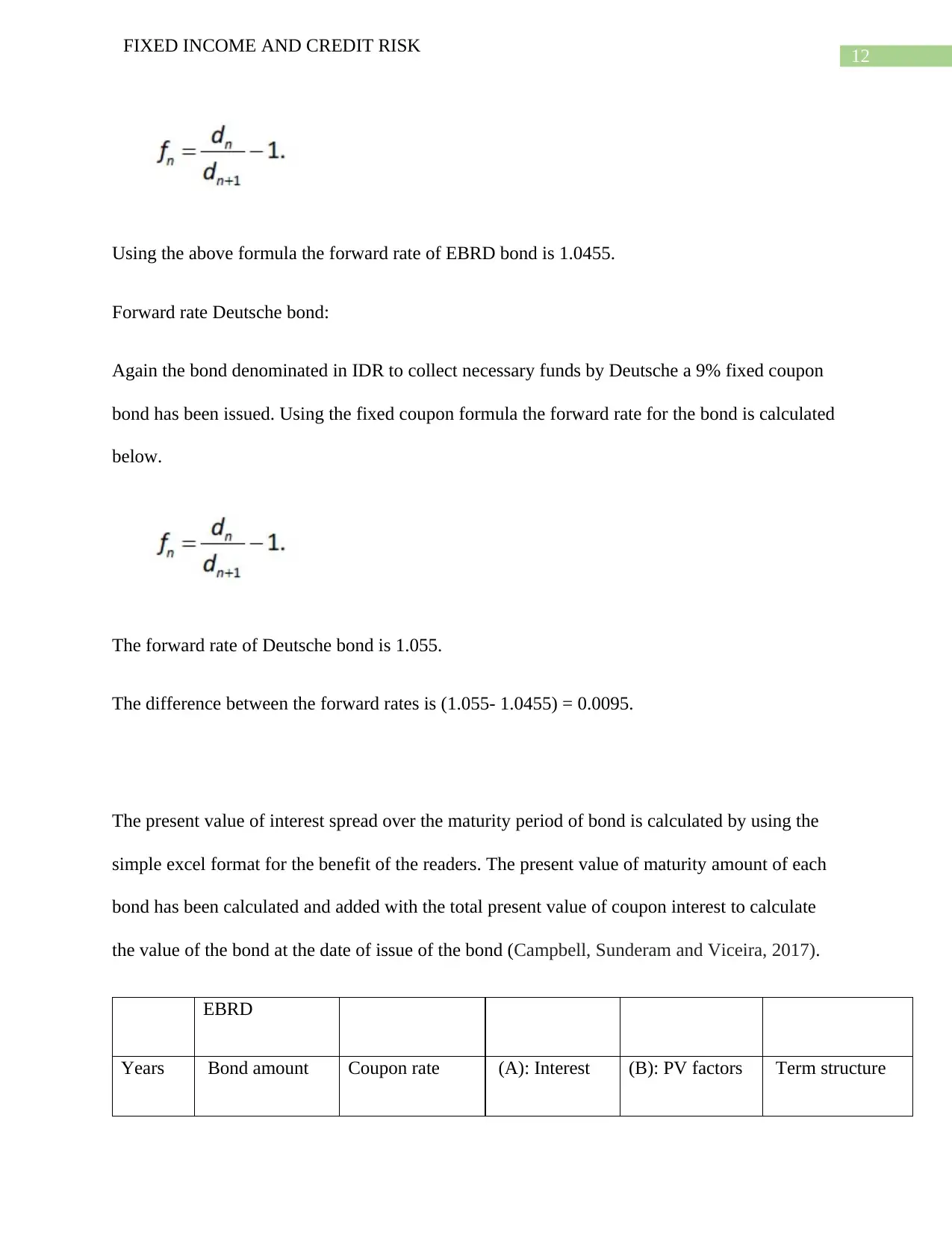

Using the above formula the forward rate of EBRD bond is 1.0455.

Forward rate Deutsche bond:

Again the bond denominated in IDR to collect necessary funds by Deutsche a 9% fixed coupon

bond has been issued. Using the fixed coupon formula the forward rate for the bond is calculated

below.

The forward rate of Deutsche bond is 1.055.

The difference between the forward rates is (1.055- 1.0455) = 0.0095.

The present value of interest spread over the maturity period of bond is calculated by using the

simple excel format for the benefit of the readers. The present value of maturity amount of each

bond has been calculated and added with the total present value of coupon interest to calculate

the value of the bond at the date of issue of the bond (Campbell, Sunderam and Viceira, 2017).

EBRD

Years Bond amount Coupon rate (A): Interest (B): PV factors Term structure

FIXED INCOME AND CREDIT RISK

Using the above formula the forward rate of EBRD bond is 1.0455.

Forward rate Deutsche bond:

Again the bond denominated in IDR to collect necessary funds by Deutsche a 9% fixed coupon

bond has been issued. Using the fixed coupon formula the forward rate for the bond is calculated

below.

The forward rate of Deutsche bond is 1.055.

The difference between the forward rates is (1.055- 1.0455) = 0.0095.

The present value of interest spread over the maturity period of bond is calculated by using the

simple excel format for the benefit of the readers. The present value of maturity amount of each

bond has been calculated and added with the total present value of coupon interest to calculate

the value of the bond at the date of issue of the bond (Campbell, Sunderam and Viceira, 2017).

EBRD

Years Bond amount Coupon rate (A): Interest (B): PV factors Term structure

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

13

FIXED INCOME AND CREDIT RISK

(RUB) (7.25%) (RUB) @5.25% (AxB)

1

50,000.00

7.25%

3,625.00

0.950119

3,444.18

2

50,000.00

7.25%

3,625.00

0.902726

3,272.38

3

50,000.00

7.25%

3,625.00

0.857697

3,109.15

4

50,000.00

7.25%

3,625.00

0.814914

2,954.06

5

50,000.00

7.25%

3,625.00

0.774265

2,806.71

6

50,000.00

7.25%

3,625.00

0.735643

2,666.71

7

50,000.00

7.25%

3,625.00

0.698949

2,533.69

8

50,000.00

7.25%

3,625.00

0.664084

2,407.31

9

50,000.00

7.25%

3,625.00

0.630959

2,287.23

10 7.25% 0.599486

FIXED INCOME AND CREDIT RISK

(RUB) (7.25%) (RUB) @5.25% (AxB)

1

50,000.00

7.25%

3,625.00

0.950119

3,444.18

2

50,000.00

7.25%

3,625.00

0.902726

3,272.38

3

50,000.00

7.25%

3,625.00

0.857697

3,109.15

4

50,000.00

7.25%

3,625.00

0.814914

2,954.06

5

50,000.00

7.25%

3,625.00

0.774265

2,806.71

6

50,000.00

7.25%

3,625.00

0.735643

2,666.71

7

50,000.00

7.25%

3,625.00

0.698949

2,533.69

8

50,000.00

7.25%

3,625.00

0.664084

2,407.31

9

50,000.00

7.25%

3,625.00

0.630959

2,287.23

10 7.25% 0.599486

14

FIXED INCOME AND CREDIT RISK

50,000.00 3,625.00 2,173.14

11

50,000.00

7.25%

3,625.00

0.569583

2,064.74

12

50,000.00

7.25%

3,625.00

0.541171

1,961.75

13

50,000.00

7.25%

3,625.00

0.514177

1,863.89

14

50,000.00

7.25%

3,625.00

0.488529

1,770.92

15

50,000.00

7.25%

3,625.00

0.464161

1,682.58

16

50,000.00

7.25%

3,625.00

0.441008

1,598.65

17

50,000.00

7.25%

3,625.00

0.41901

1,518.91

18

50,000.00

7.25%

3,625.00

0.398109

1,443.15

19

50,000.00

7.25%

3,625.00

0.378251

1,371.16

20 7.25% 0.359383

FIXED INCOME AND CREDIT RISK

50,000.00 3,625.00 2,173.14

11

50,000.00

7.25%

3,625.00

0.569583

2,064.74

12

50,000.00

7.25%

3,625.00

0.541171

1,961.75

13

50,000.00

7.25%

3,625.00

0.514177

1,863.89

14

50,000.00

7.25%

3,625.00

0.488529

1,770.92

15

50,000.00

7.25%

3,625.00

0.464161

1,682.58

16

50,000.00

7.25%

3,625.00

0.441008

1,598.65

17

50,000.00

7.25%

3,625.00

0.41901

1,518.91

18

50,000.00

7.25%

3,625.00

0.398109

1,443.15

19

50,000.00

7.25%

3,625.00

0.378251

1,371.16

20 7.25% 0.359383

15

FIXED INCOME AND CREDIT RISK

50,000.00 3,625.00 1,302.76

21

50,000.00

7.25%

3,625.00

0.341457

1,237.78

22

50,000.00

7.25%

3,625.00

0.324425

1,176.04

23

50,000.00

7.25%

3,625.00

0.308242

1,117.38

24

50,000.00

7.25%

3,625.00

0.292866

1,061.64

25

50,000.00

7.25%

3,625.00

0.278258

1,008.68

26

50,000.00

7.25%

3,625.00

0.264378

958.37

27

50,000.00

7.25%

3,625.00

0.25119

910.57

28

50,000.00

7.25%

3,625.00

0.238661

865.15

29

50,000.00

7.25%

3,625.00

0.226756

821.99

30 7.25% 0.215445

FIXED INCOME AND CREDIT RISK

50,000.00 3,625.00 1,302.76

21

50,000.00

7.25%

3,625.00

0.341457

1,237.78

22

50,000.00

7.25%

3,625.00

0.324425

1,176.04

23

50,000.00

7.25%

3,625.00

0.308242

1,117.38

24

50,000.00

7.25%

3,625.00

0.292866

1,061.64

25

50,000.00

7.25%

3,625.00

0.278258

1,008.68

26

50,000.00

7.25%

3,625.00

0.264378

958.37

27

50,000.00

7.25%

3,625.00

0.25119

910.57

28

50,000.00

7.25%

3,625.00

0.238661

865.15

29

50,000.00

7.25%

3,625.00

0.226756

821.99

30 7.25% 0.215445

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

16

FIXED INCOME AND CREDIT RISK

50,000.00 3,625.00 780.99

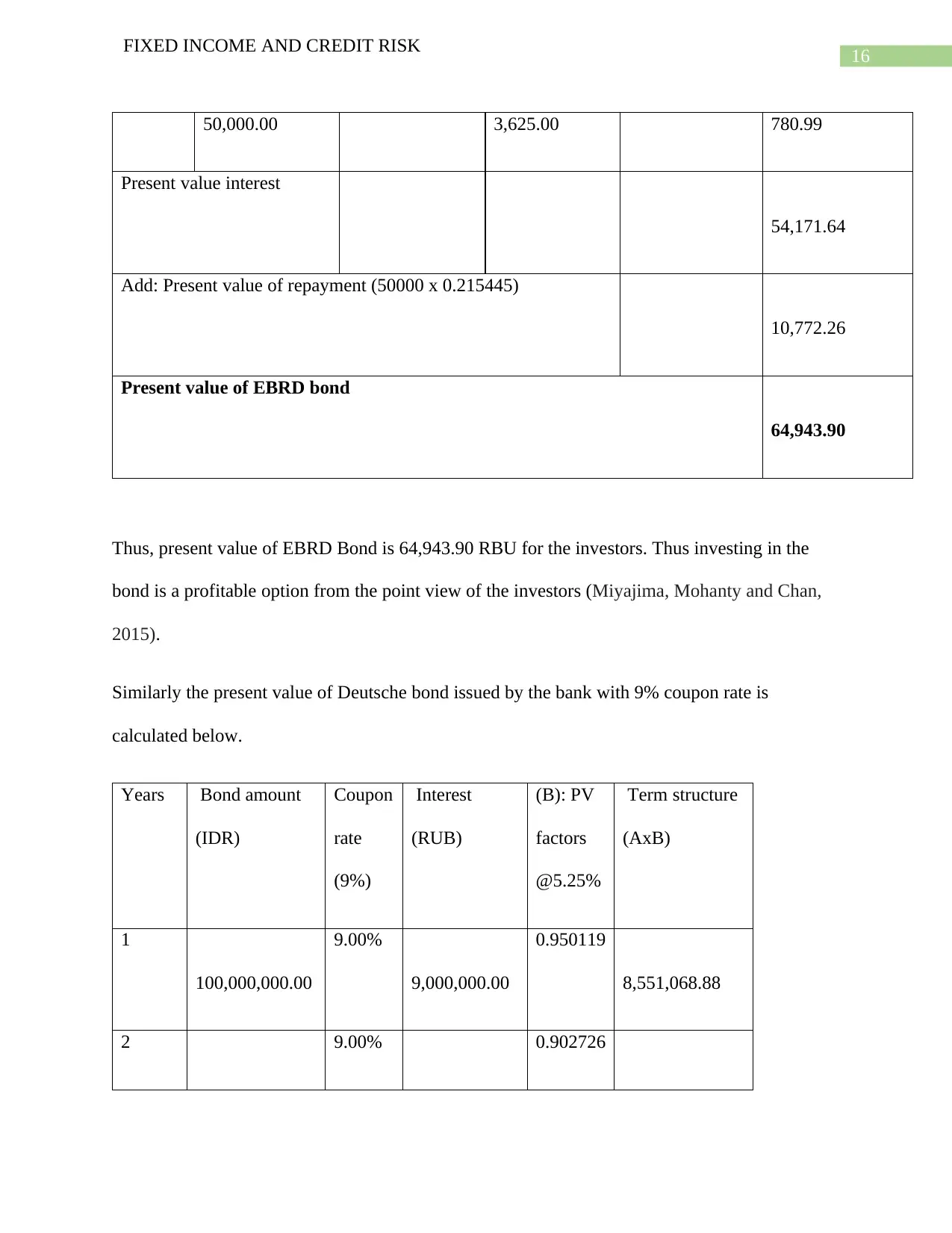

Present value interest

54,171.64

Add: Present value of repayment (50000 x 0.215445)

10,772.26

Present value of EBRD bond

64,943.90

Thus, present value of EBRD Bond is 64,943.90 RBU for the investors. Thus investing in the

bond is a profitable option from the point view of the investors (Miyajima, Mohanty and Chan,

2015).

Similarly the present value of Deutsche bond issued by the bank with 9% coupon rate is

calculated below.

Years Bond amount

(IDR)

Coupon

rate

(9%)

Interest

(RUB)

(B): PV

factors

@5.25%

Term structure

(AxB)

1

100,000,000.00

9.00%

9,000,000.00

0.950119

8,551,068.88

2 9.00% 0.902726

FIXED INCOME AND CREDIT RISK

50,000.00 3,625.00 780.99

Present value interest

54,171.64

Add: Present value of repayment (50000 x 0.215445)

10,772.26

Present value of EBRD bond

64,943.90

Thus, present value of EBRD Bond is 64,943.90 RBU for the investors. Thus investing in the

bond is a profitable option from the point view of the investors (Miyajima, Mohanty and Chan,

2015).

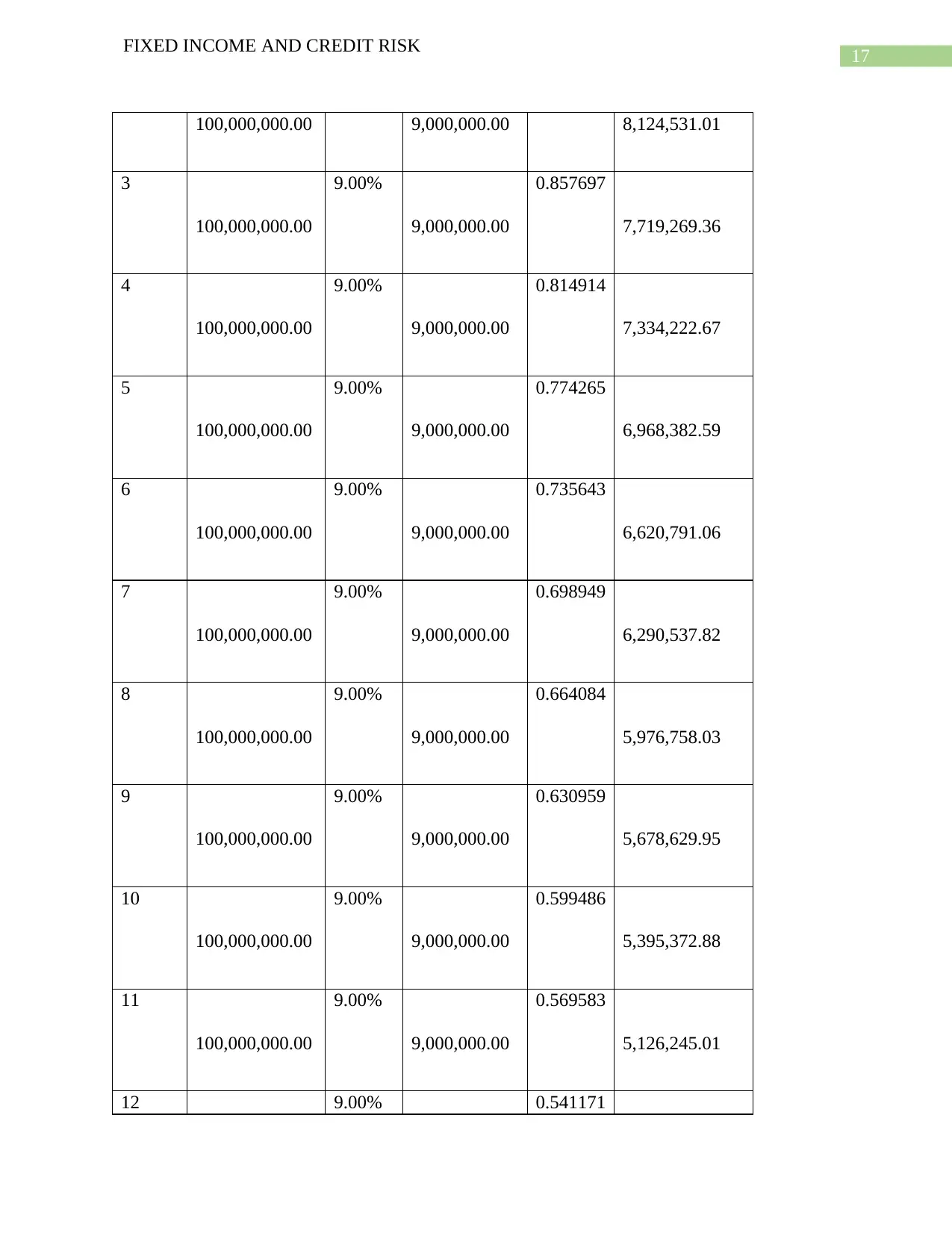

Similarly the present value of Deutsche bond issued by the bank with 9% coupon rate is

calculated below.

Years Bond amount

(IDR)

Coupon

rate

(9%)

Interest

(RUB)

(B): PV

factors

@5.25%

Term structure

(AxB)

1

100,000,000.00

9.00%

9,000,000.00

0.950119

8,551,068.88

2 9.00% 0.902726

17

FIXED INCOME AND CREDIT RISK

100,000,000.00 9,000,000.00 8,124,531.01

3

100,000,000.00

9.00%

9,000,000.00

0.857697

7,719,269.36

4

100,000,000.00

9.00%

9,000,000.00

0.814914

7,334,222.67

5

100,000,000.00

9.00%

9,000,000.00

0.774265

6,968,382.59

6

100,000,000.00

9.00%

9,000,000.00

0.735643

6,620,791.06

7

100,000,000.00

9.00%

9,000,000.00

0.698949

6,290,537.82

8

100,000,000.00

9.00%

9,000,000.00

0.664084

5,976,758.03

9

100,000,000.00

9.00%

9,000,000.00

0.630959

5,678,629.95

10

100,000,000.00

9.00%

9,000,000.00

0.599486

5,395,372.88

11

100,000,000.00

9.00%

9,000,000.00

0.569583

5,126,245.01

12 9.00% 0.541171

FIXED INCOME AND CREDIT RISK

100,000,000.00 9,000,000.00 8,124,531.01

3

100,000,000.00

9.00%

9,000,000.00

0.857697

7,719,269.36

4

100,000,000.00

9.00%

9,000,000.00

0.814914

7,334,222.67

5

100,000,000.00

9.00%

9,000,000.00

0.774265

6,968,382.59

6

100,000,000.00

9.00%

9,000,000.00

0.735643

6,620,791.06

7

100,000,000.00

9.00%

9,000,000.00

0.698949

6,290,537.82

8

100,000,000.00

9.00%

9,000,000.00

0.664084

5,976,758.03

9

100,000,000.00

9.00%

9,000,000.00

0.630959

5,678,629.95

10

100,000,000.00

9.00%

9,000,000.00

0.599486

5,395,372.88

11

100,000,000.00

9.00%

9,000,000.00

0.569583

5,126,245.01

12 9.00% 0.541171

18

FIXED INCOME AND CREDIT RISK

100,000,000.00 9,000,000.00 4,870,541.58

13

100,000,000.00

9.00%

9,000,000.00

0.514177

4,627,592.95

14

100,000,000.00

9.00%

9,000,000.00

0.488529

4,396,762.90

15

100,000,000.00

9.00%

9,000,000.00

0.464161

4,177,446.93

16

100,000,000.00

9.00%

9,000,000.00

0.441008

3,969,070.72

17

100,000,000.00

9.00%

9,000,000.00

0.41901

3,771,088.57

18

100,000,000.00

9.00%

9,000,000.00

0.398109

3,582,982.02

19

100,000,000.00

9.00%

9,000,000.00

0.378251

3,404,258.45

20

100,000,000.00

9.00%

9,000,000.00

0.359383

3,234,449.83

21

100,000,000.00

9.00%

9,000,000.00

0.341457

3,073,111.48

22 9.00% 0.324425

FIXED INCOME AND CREDIT RISK

100,000,000.00 9,000,000.00 4,870,541.58

13

100,000,000.00

9.00%

9,000,000.00

0.514177

4,627,592.95

14

100,000,000.00

9.00%

9,000,000.00

0.488529

4,396,762.90

15

100,000,000.00

9.00%

9,000,000.00

0.464161

4,177,446.93

16

100,000,000.00

9.00%

9,000,000.00

0.441008

3,969,070.72

17

100,000,000.00

9.00%

9,000,000.00

0.41901

3,771,088.57

18

100,000,000.00

9.00%

9,000,000.00

0.398109

3,582,982.02

19

100,000,000.00

9.00%

9,000,000.00

0.378251

3,404,258.45

20

100,000,000.00

9.00%

9,000,000.00

0.359383

3,234,449.83

21

100,000,000.00

9.00%

9,000,000.00

0.341457

3,073,111.48

22 9.00% 0.324425

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

19

FIXED INCOME AND CREDIT RISK

100,000,000.00 9,000,000.00 2,919,820.88

23

100,000,000.00

9.00%

9,000,000.00

0.308242

2,774,176.61

24

100,000,000.00

9.00%

9,000,000.00

0.292866

2,635,797.25

25

100,000,000.00

9.00%

9,000,000.00

0.278258

2,504,320.43

26

100,000,000.00

9.00%

9,000,000.00

0.264378

2,379,401.84

27

100,000,000.00

9.00%

9,000,000.00

0.25119

2,260,714.33

28

100,000,000.00

9.00%

9,000,000.00

0.238661

2,147,947.11

29

100,000,000.00

9.00%

9,000,000.00

0.226756

2,040,804.85

30

100,000,000.00

9.00%

9,000,000.00

0.215445

1,939,006.99

Present value total

interest 134,495,104.99

FIXED INCOME AND CREDIT RISK

100,000,000.00 9,000,000.00 2,919,820.88

23

100,000,000.00

9.00%

9,000,000.00

0.308242

2,774,176.61

24

100,000,000.00

9.00%

9,000,000.00

0.292866

2,635,797.25

25

100,000,000.00

9.00%

9,000,000.00

0.278258

2,504,320.43

26

100,000,000.00

9.00%

9,000,000.00

0.264378

2,379,401.84

27

100,000,000.00

9.00%

9,000,000.00

0.25119

2,260,714.33

28

100,000,000.00

9.00%

9,000,000.00

0.238661

2,147,947.11

29

100,000,000.00

9.00%

9,000,000.00

0.226756

2,040,804.85

30

100,000,000.00

9.00%

9,000,000.00

0.215445

1,939,006.99

Present value total

interest 134,495,104.99

20

FIXED INCOME AND CREDIT RISK

Add: Present value of principal(100,000,000 x

0.215445) 21,544,522.09

Present value of Deutsche Bond

156,039,627.08

As can be seen from the above that the investors by investing 100,000,000 IDR in Deutsche bond

expected to receive a present value of 156,039,627.08 IDR over the life time of the bond. Hence,

from the point of view of investors the proposal of investing in the bonds issued by Deutsche is a

profitable investment proposal (Hanson and Stein, 2015).

Part 3:

The spread is calculated to show the yield expected to be earned over the life time of a

bond. In this case the present value of bond from the point of view of investors, in both case,

show that the investors are expected to earn significant amount of return by investing in the bond

of EBRD and Deutsche. The method used here is relatively simple to find out the present value

of interest to be earned by the investors on the bond over the useful life of the bond (Rachel and

Smith, 2015). The coupon rate of bonds, i.e. 7.25% for EBRD RBU bond and 9% for Deutsche

IDR bond are fixed. Hence, there is no question fluctuation in the actual spread and yield of

bonds throughout the life time of the bond. Thus, there is no confusion regarding the periodic

coupon to be received from the bond (Du, Tepper and Verdelhan, 2018). However, in order to

calculate the present value of coupon as well as the principal to be rapid at the end of the

maturity period of the respective bonds it is important to use an appropriate rate of interest.

FIXED INCOME AND CREDIT RISK

Add: Present value of principal(100,000,000 x

0.215445) 21,544,522.09

Present value of Deutsche Bond

156,039,627.08

As can be seen from the above that the investors by investing 100,000,000 IDR in Deutsche bond

expected to receive a present value of 156,039,627.08 IDR over the life time of the bond. Hence,

from the point of view of investors the proposal of investing in the bonds issued by Deutsche is a

profitable investment proposal (Hanson and Stein, 2015).

Part 3:

The spread is calculated to show the yield expected to be earned over the life time of a

bond. In this case the present value of bond from the point of view of investors, in both case,

show that the investors are expected to earn significant amount of return by investing in the bond

of EBRD and Deutsche. The method used here is relatively simple to find out the present value

of interest to be earned by the investors on the bond over the useful life of the bond (Rachel and

Smith, 2015). The coupon rate of bonds, i.e. 7.25% for EBRD RBU bond and 9% for Deutsche

IDR bond are fixed. Hence, there is no question fluctuation in the actual spread and yield of

bonds throughout the life time of the bond. Thus, there is no confusion regarding the periodic

coupon to be received from the bond (Du, Tepper and Verdelhan, 2018). However, in order to

calculate the present value of coupon as well as the principal to be rapid at the end of the

maturity period of the respective bonds it is important to use an appropriate rate of interest.

21

FIXED INCOME AND CREDIT RISK

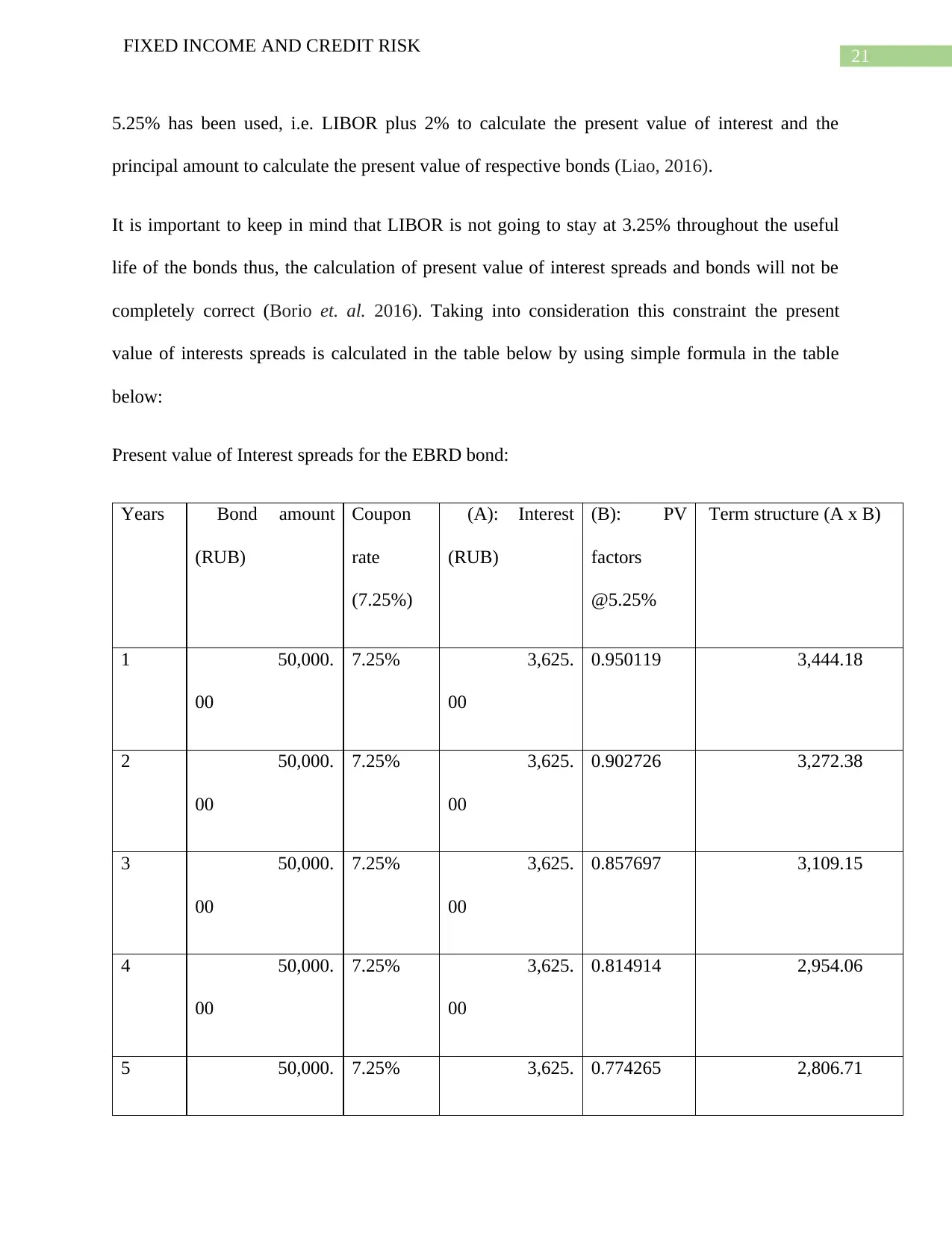

5.25% has been used, i.e. LIBOR plus 2% to calculate the present value of interest and the

principal amount to calculate the present value of respective bonds (Liao, 2016).

It is important to keep in mind that LIBOR is not going to stay at 3.25% throughout the useful

life of the bonds thus, the calculation of present value of interest spreads and bonds will not be

completely correct (Borio et. al. 2016). Taking into consideration this constraint the present

value of interests spreads is calculated in the table below by using simple formula in the table

below:

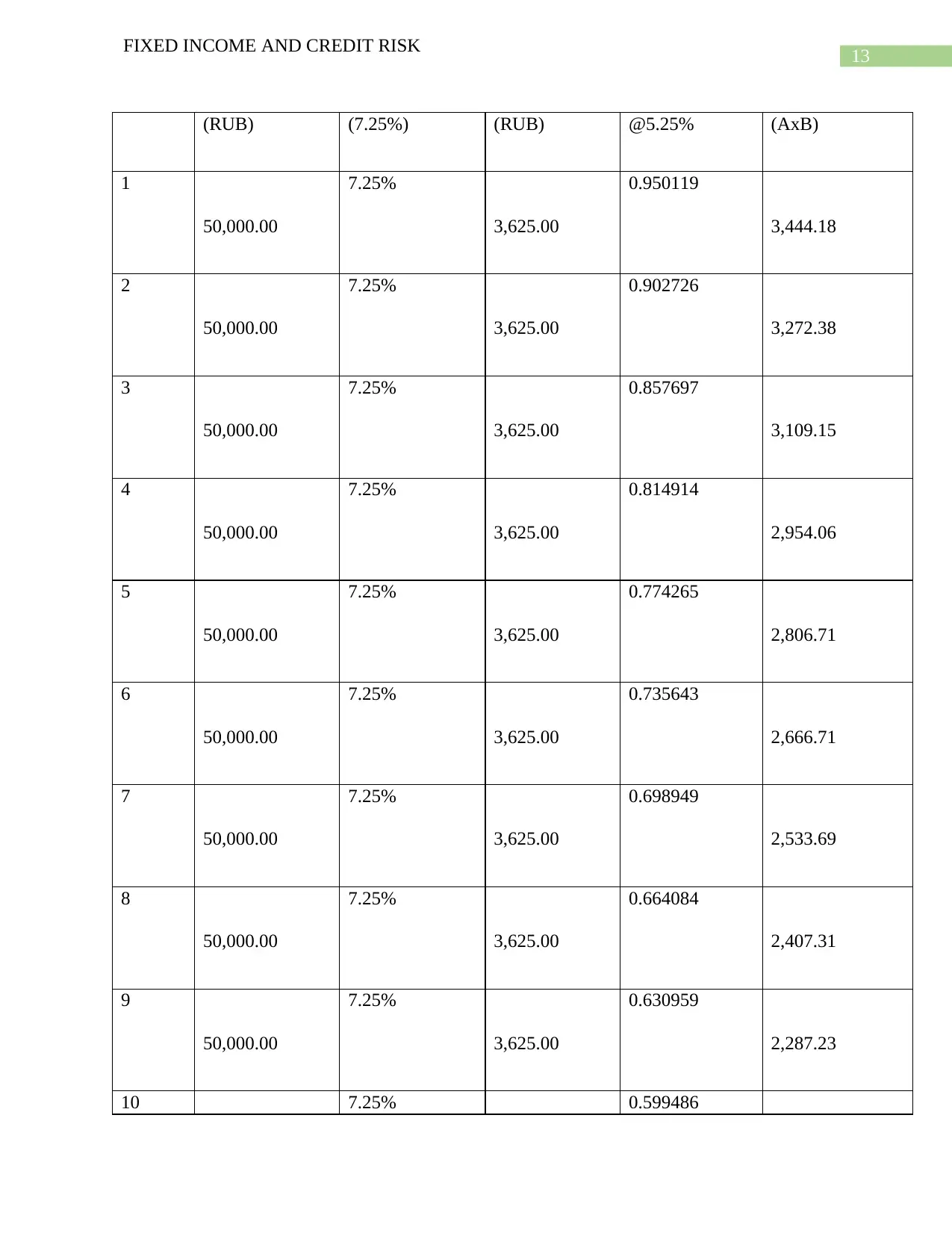

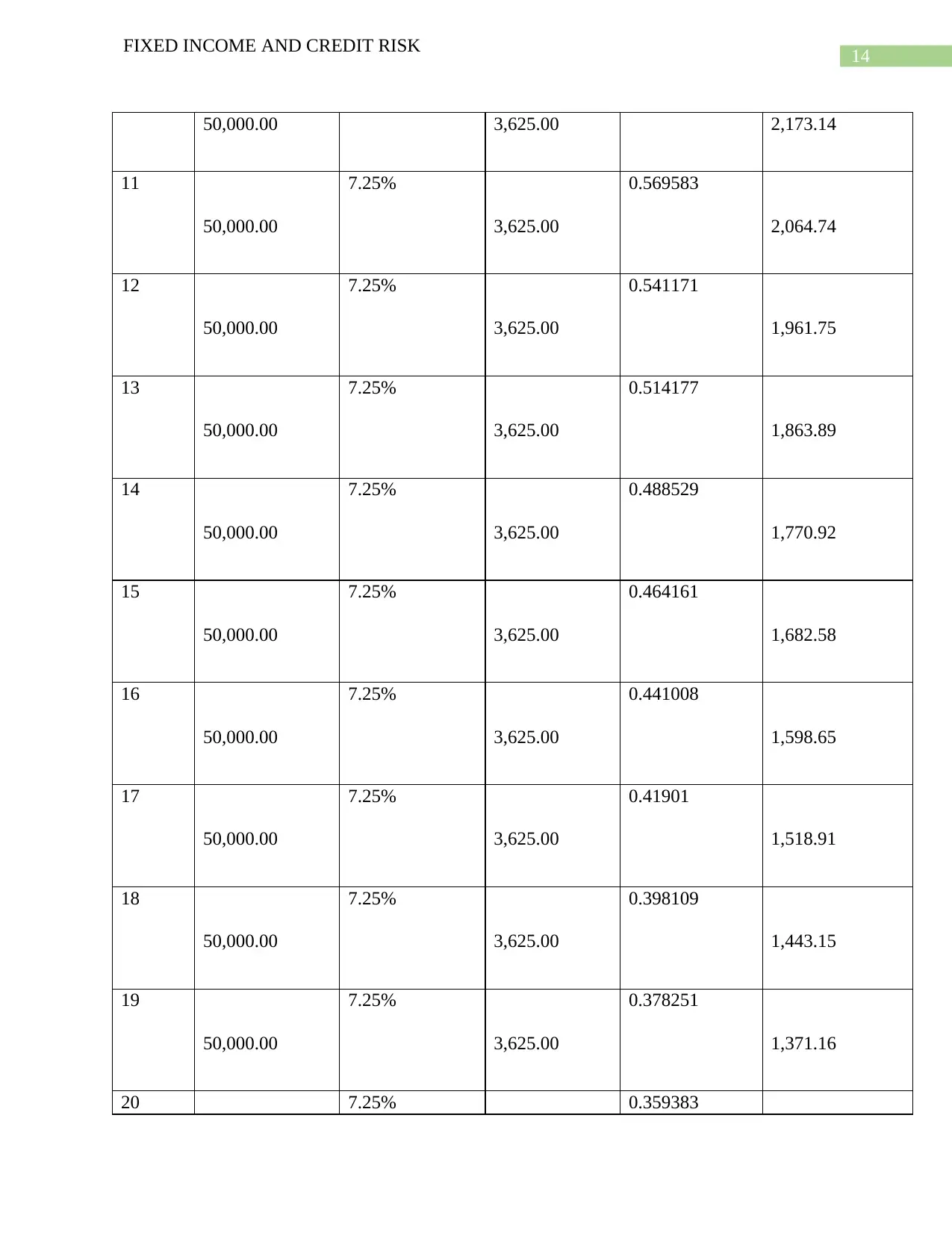

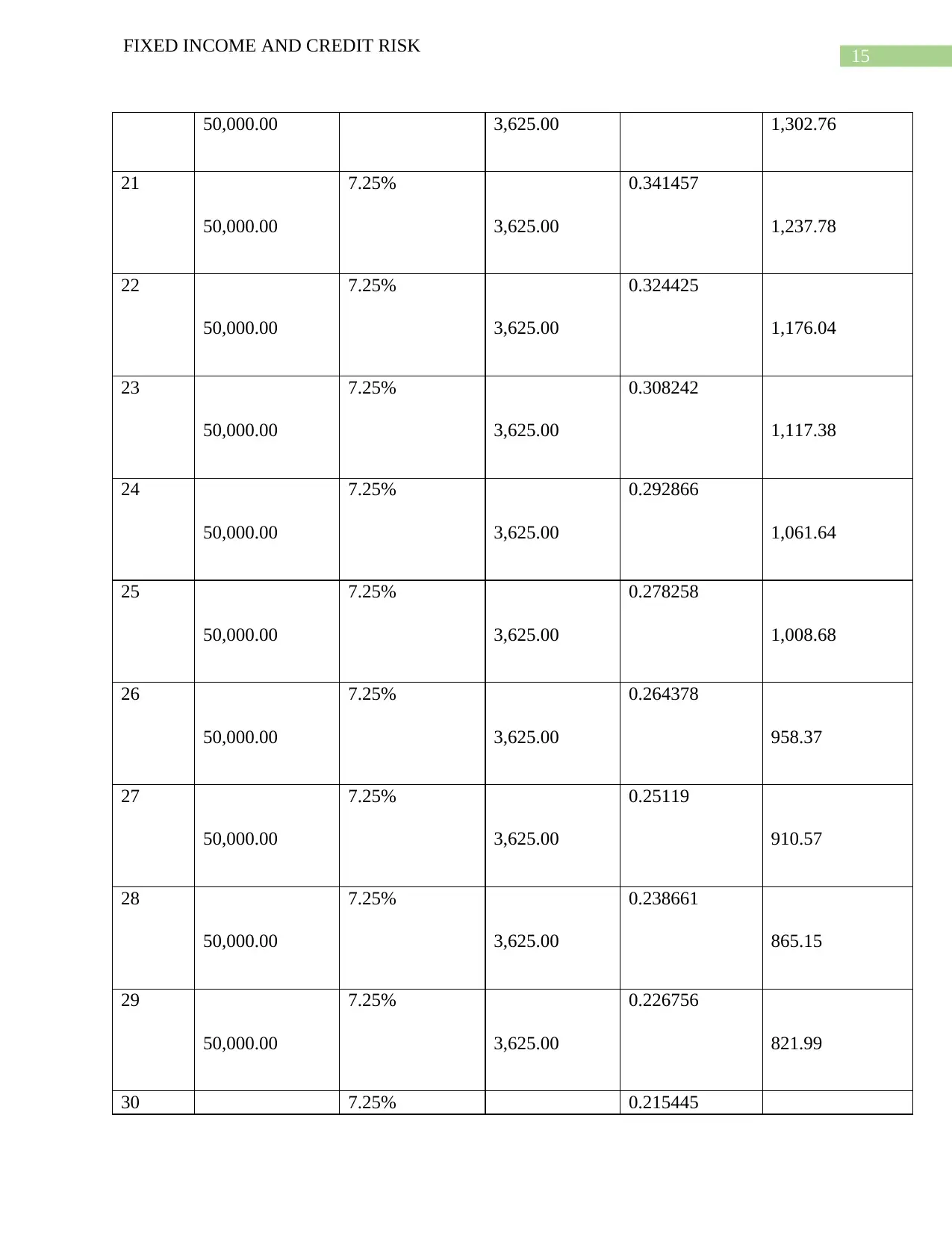

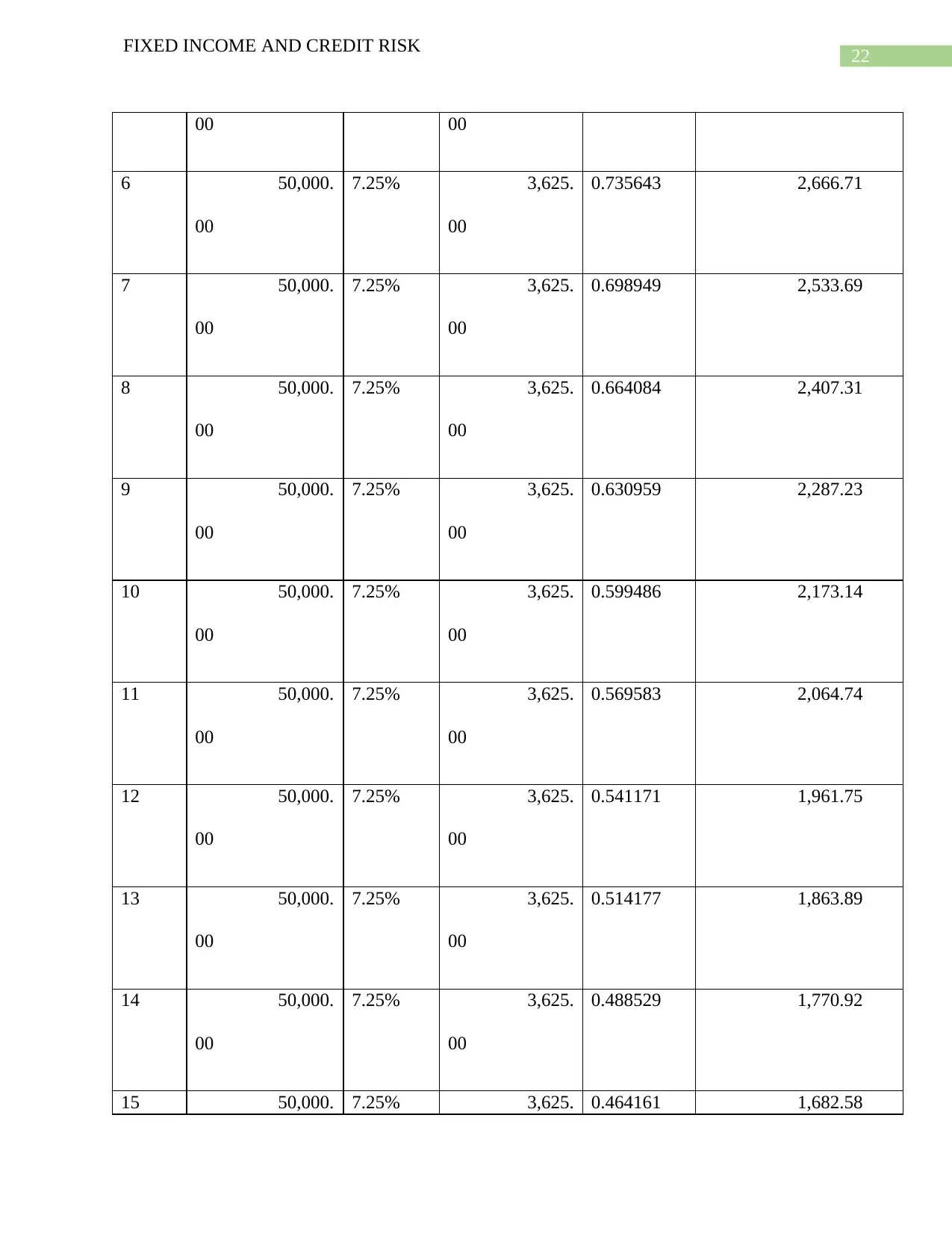

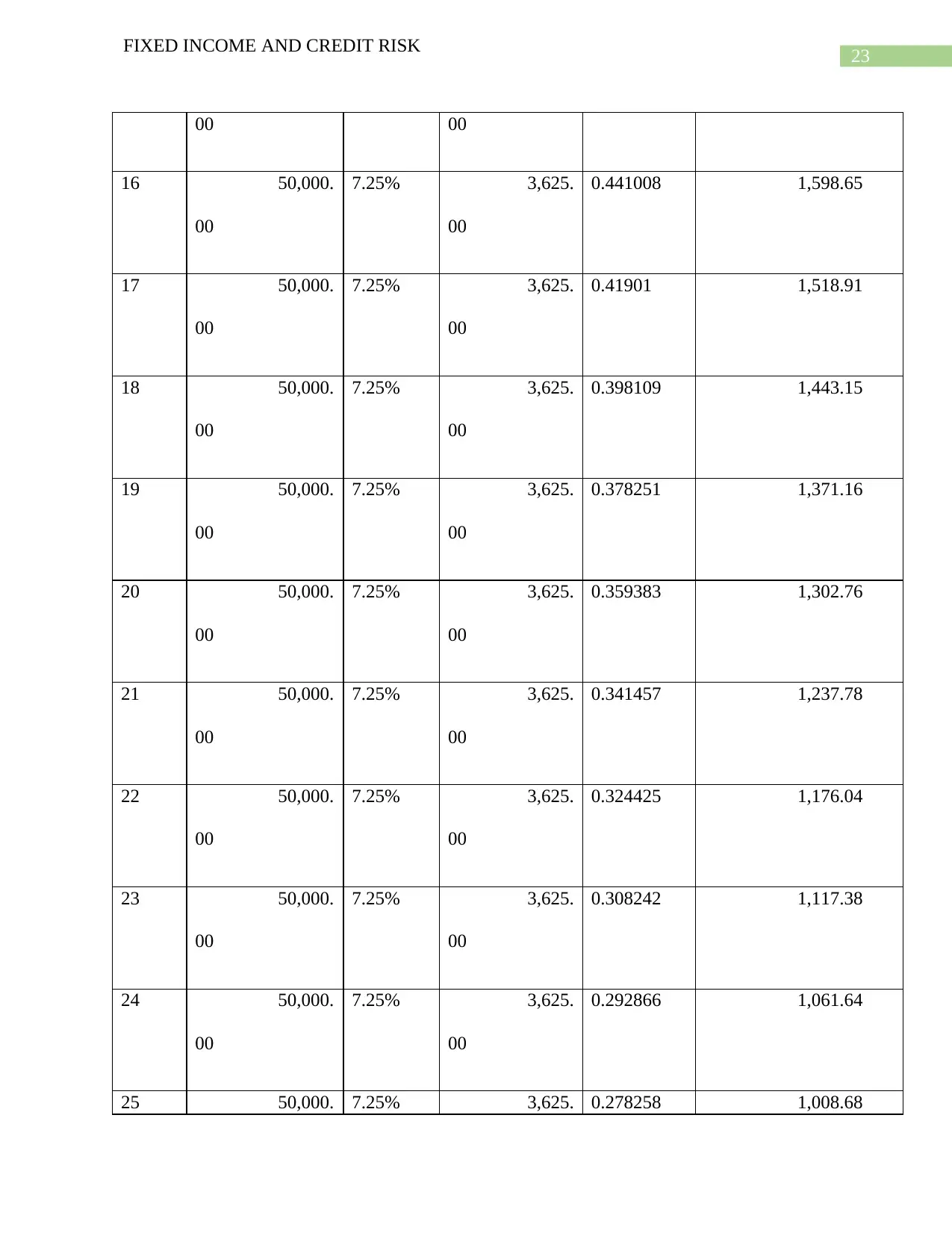

Present value of Interest spreads for the EBRD bond:

Years Bond amount

(RUB)

Coupon

rate

(7.25%)

(A): Interest

(RUB)

(B): PV

factors

@5.25%

Term structure (A x B)

1 50,000.

00

7.25% 3,625.

00

0.950119 3,444.18

2 50,000.

00

7.25% 3,625.

00

0.902726 3,272.38

3 50,000.

00

7.25% 3,625.

00

0.857697 3,109.15

4 50,000.

00

7.25% 3,625.

00

0.814914 2,954.06

5 50,000. 7.25% 3,625. 0.774265 2,806.71

FIXED INCOME AND CREDIT RISK

5.25% has been used, i.e. LIBOR plus 2% to calculate the present value of interest and the

principal amount to calculate the present value of respective bonds (Liao, 2016).

It is important to keep in mind that LIBOR is not going to stay at 3.25% throughout the useful

life of the bonds thus, the calculation of present value of interest spreads and bonds will not be

completely correct (Borio et. al. 2016). Taking into consideration this constraint the present

value of interests spreads is calculated in the table below by using simple formula in the table

below:

Present value of Interest spreads for the EBRD bond:

Years Bond amount

(RUB)

Coupon

rate

(7.25%)

(A): Interest

(RUB)

(B): PV

factors

@5.25%

Term structure (A x B)

1 50,000.

00

7.25% 3,625.

00

0.950119 3,444.18

2 50,000.

00

7.25% 3,625.

00

0.902726 3,272.38

3 50,000.

00

7.25% 3,625.

00

0.857697 3,109.15

4 50,000.

00

7.25% 3,625.

00

0.814914 2,954.06

5 50,000. 7.25% 3,625. 0.774265 2,806.71

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

22

FIXED INCOME AND CREDIT RISK

00 00

6 50,000.

00

7.25% 3,625.

00

0.735643 2,666.71

7 50,000.

00

7.25% 3,625.

00

0.698949 2,533.69

8 50,000.

00

7.25% 3,625.

00

0.664084 2,407.31

9 50,000.

00

7.25% 3,625.

00

0.630959 2,287.23

10 50,000.

00

7.25% 3,625.

00

0.599486 2,173.14

11 50,000.

00

7.25% 3,625.

00

0.569583 2,064.74

12 50,000.

00

7.25% 3,625.

00

0.541171 1,961.75

13 50,000.

00

7.25% 3,625.

00

0.514177 1,863.89

14 50,000.

00

7.25% 3,625.

00

0.488529 1,770.92

15 50,000. 7.25% 3,625. 0.464161 1,682.58

FIXED INCOME AND CREDIT RISK

00 00

6 50,000.

00

7.25% 3,625.

00

0.735643 2,666.71

7 50,000.

00

7.25% 3,625.

00

0.698949 2,533.69

8 50,000.

00

7.25% 3,625.

00

0.664084 2,407.31

9 50,000.

00

7.25% 3,625.

00

0.630959 2,287.23

10 50,000.

00

7.25% 3,625.

00

0.599486 2,173.14

11 50,000.

00

7.25% 3,625.

00

0.569583 2,064.74

12 50,000.

00

7.25% 3,625.

00

0.541171 1,961.75

13 50,000.

00

7.25% 3,625.

00

0.514177 1,863.89

14 50,000.

00

7.25% 3,625.

00

0.488529 1,770.92

15 50,000. 7.25% 3,625. 0.464161 1,682.58

23

FIXED INCOME AND CREDIT RISK

00 00

16 50,000.

00

7.25% 3,625.

00

0.441008 1,598.65

17 50,000.

00

7.25% 3,625.

00

0.41901 1,518.91

18 50,000.

00

7.25% 3,625.

00

0.398109 1,443.15

19 50,000.

00

7.25% 3,625.

00

0.378251 1,371.16

20 50,000.

00

7.25% 3,625.

00

0.359383 1,302.76

21 50,000.

00

7.25% 3,625.

00

0.341457 1,237.78

22 50,000.

00

7.25% 3,625.

00

0.324425 1,176.04

23 50,000.

00

7.25% 3,625.

00

0.308242 1,117.38

24 50,000.

00

7.25% 3,625.

00

0.292866 1,061.64

25 50,000. 7.25% 3,625. 0.278258 1,008.68

FIXED INCOME AND CREDIT RISK

00 00

16 50,000.

00

7.25% 3,625.

00

0.441008 1,598.65

17 50,000.

00

7.25% 3,625.

00

0.41901 1,518.91

18 50,000.

00

7.25% 3,625.

00

0.398109 1,443.15

19 50,000.

00

7.25% 3,625.

00

0.378251 1,371.16

20 50,000.

00

7.25% 3,625.

00

0.359383 1,302.76

21 50,000.

00

7.25% 3,625.

00

0.341457 1,237.78

22 50,000.

00

7.25% 3,625.

00

0.324425 1,176.04

23 50,000.

00

7.25% 3,625.

00

0.308242 1,117.38

24 50,000.

00

7.25% 3,625.

00

0.292866 1,061.64

25 50,000. 7.25% 3,625. 0.278258 1,008.68

24

FIXED INCOME AND CREDIT RISK

00 00

26 50,000.

00

7.25% 3,625.

00

0.264378 958.37

27 50,000.

00

7.25% 3,625.

00

0.25119 910.57

28 50,000.

00

7.25% 3,625.

00

0.238661 865.15

29 50,000.

00

7.25% 3,625.

00

0.226756 821.99

30 50,000.

00

7.25% 3,625.

00

0.215445 780.99

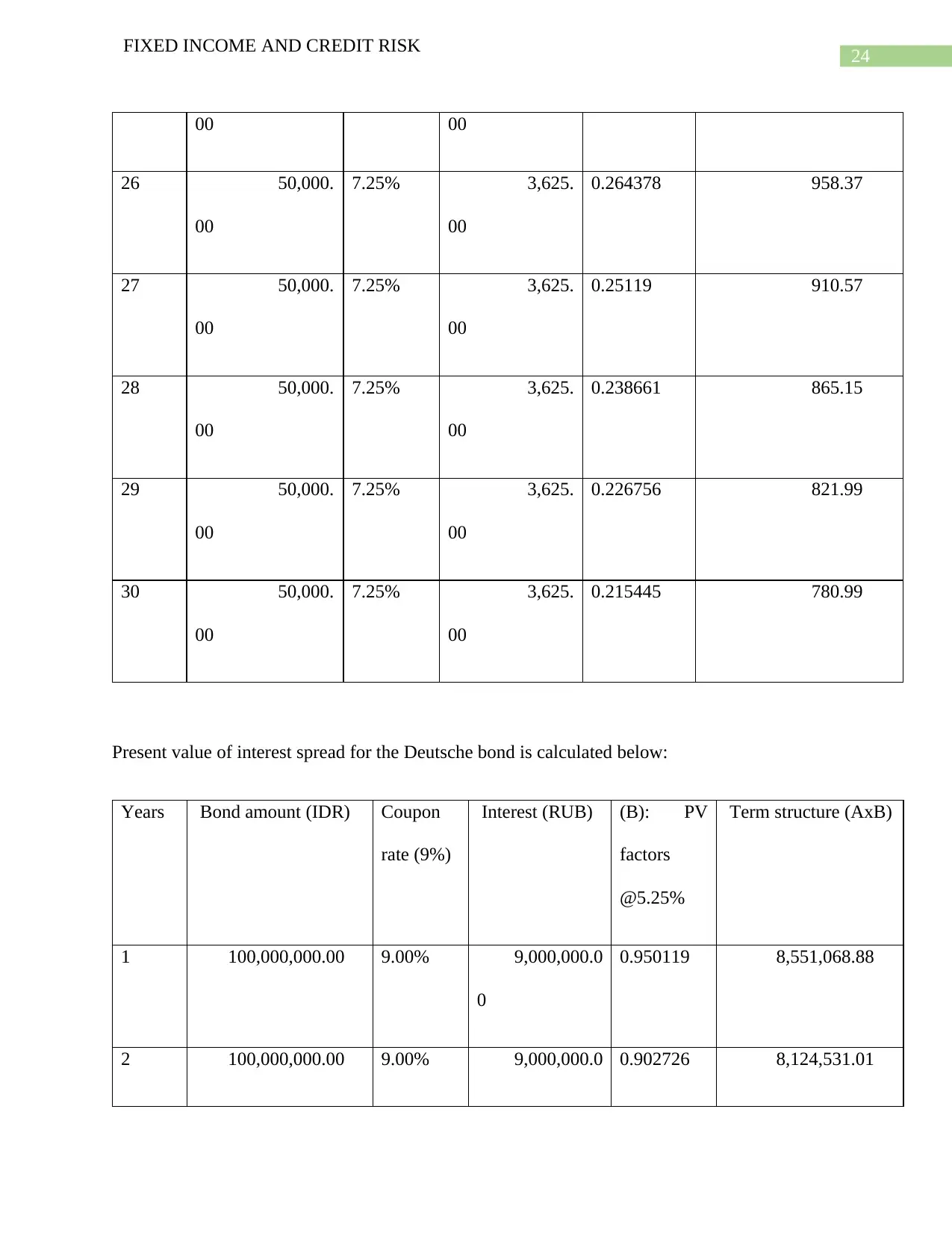

Present value of interest spread for the Deutsche bond is calculated below:

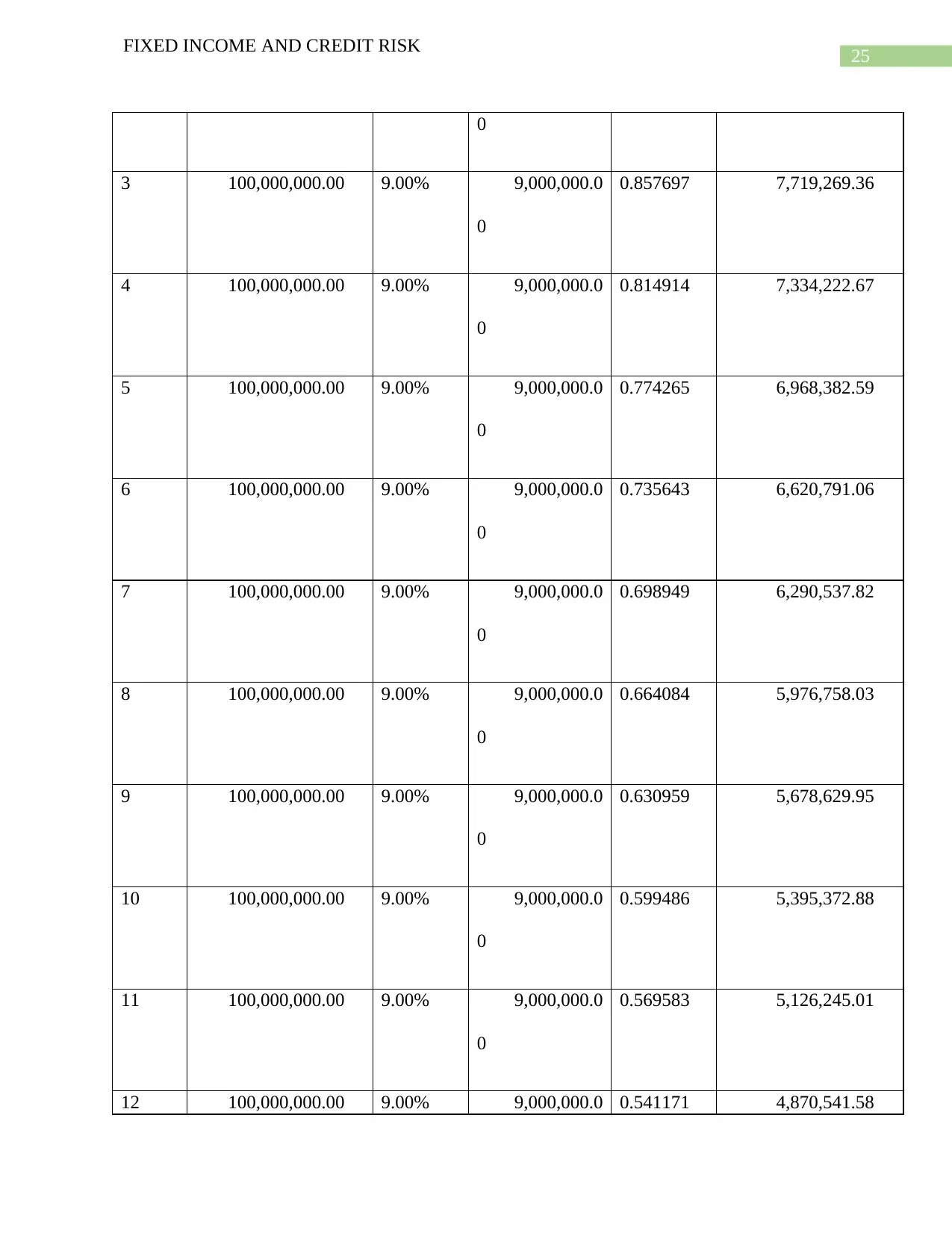

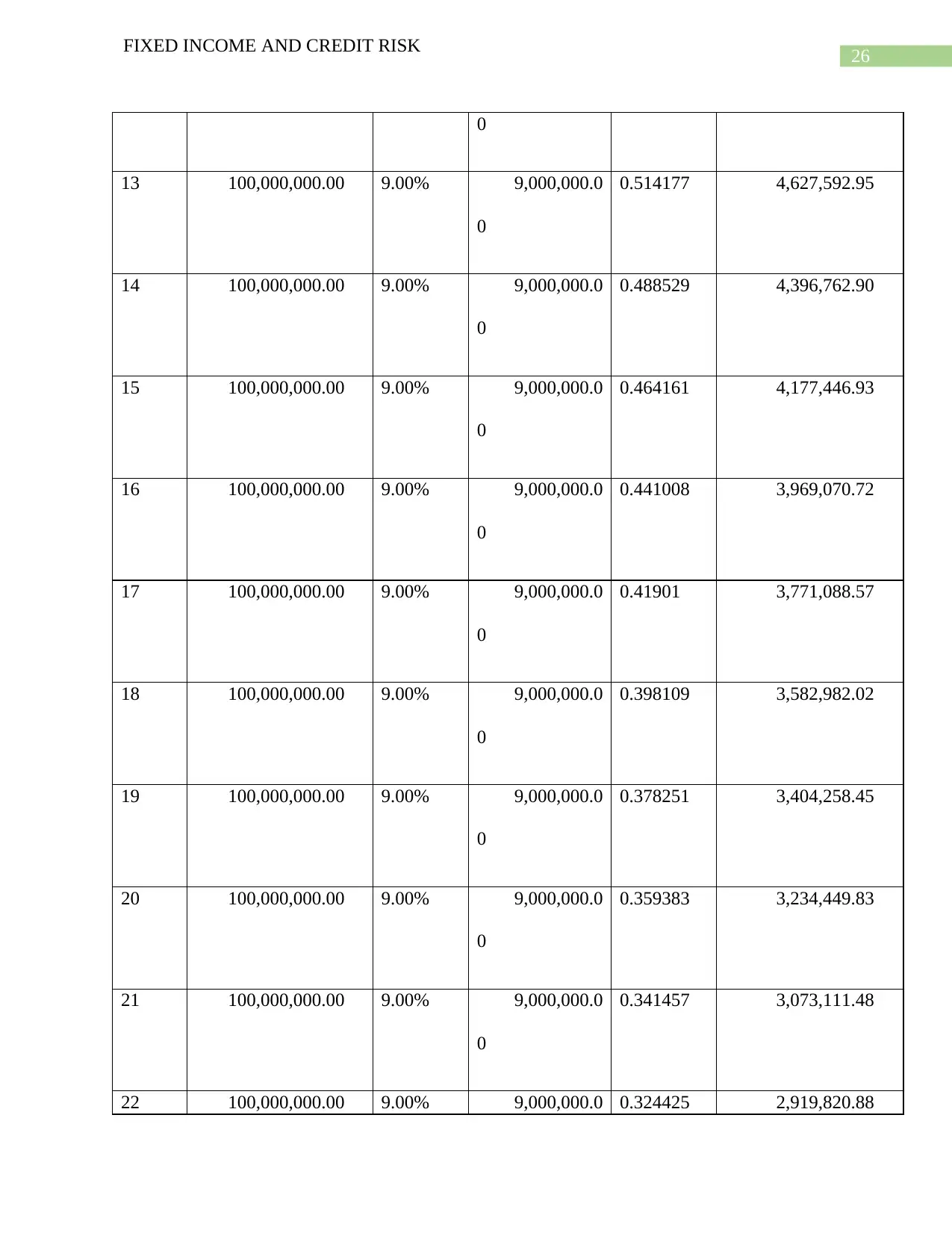

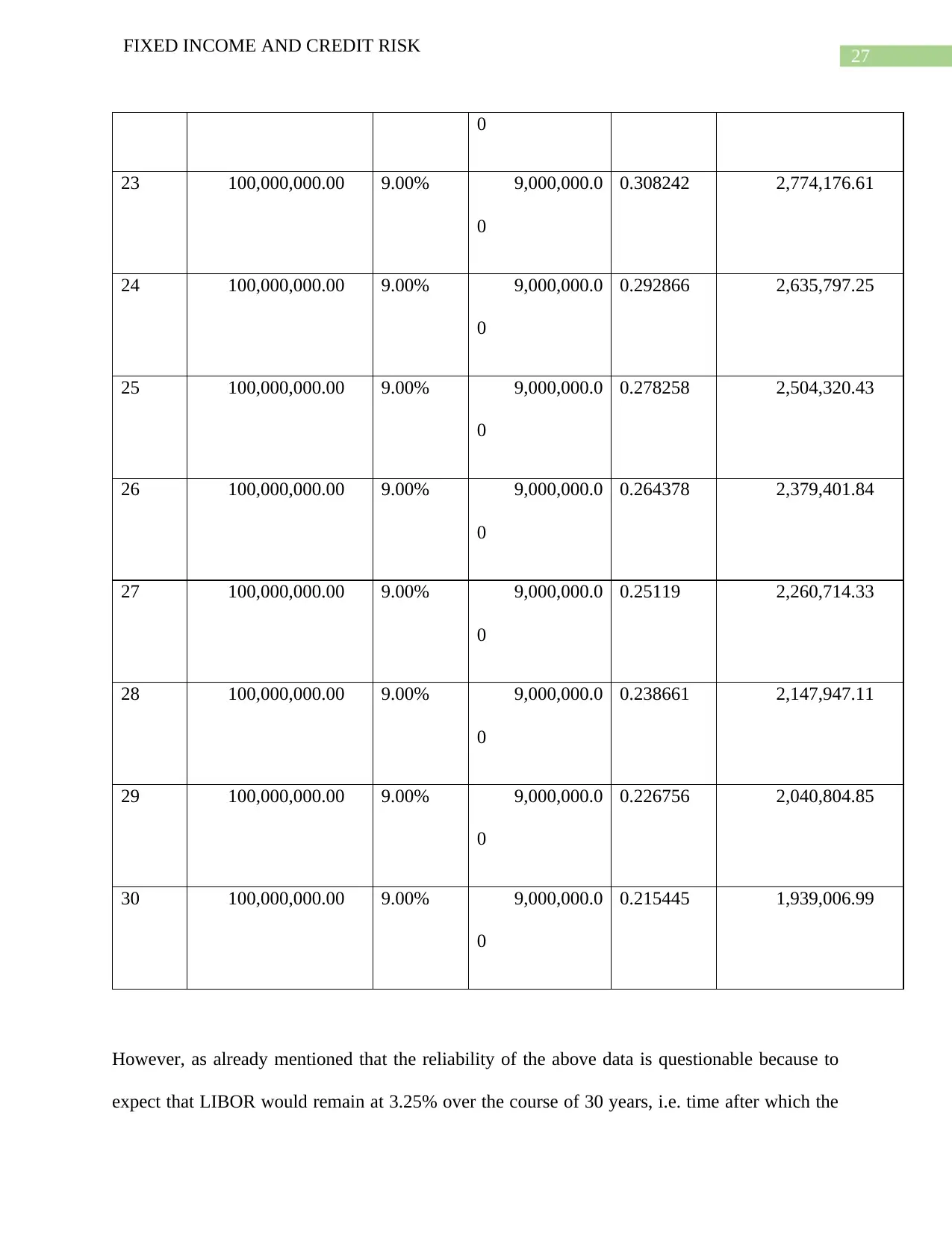

Years Bond amount (IDR) Coupon

rate (9%)

Interest (RUB) (B): PV

factors

@5.25%

Term structure (AxB)

1 100,000,000.00 9.00% 9,000,000.0

0

0.950119 8,551,068.88

2 100,000,000.00 9.00% 9,000,000.0 0.902726 8,124,531.01

FIXED INCOME AND CREDIT RISK

00 00

26 50,000.

00

7.25% 3,625.

00

0.264378 958.37

27 50,000.

00

7.25% 3,625.

00

0.25119 910.57

28 50,000.

00

7.25% 3,625.

00

0.238661 865.15

29 50,000.

00

7.25% 3,625.

00

0.226756 821.99

30 50,000.

00

7.25% 3,625.

00

0.215445 780.99

Present value of interest spread for the Deutsche bond is calculated below:

Years Bond amount (IDR) Coupon

rate (9%)

Interest (RUB) (B): PV

factors

@5.25%

Term structure (AxB)

1 100,000,000.00 9.00% 9,000,000.0

0

0.950119 8,551,068.88

2 100,000,000.00 9.00% 9,000,000.0 0.902726 8,124,531.01

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

25

FIXED INCOME AND CREDIT RISK

0

3 100,000,000.00 9.00% 9,000,000.0

0

0.857697 7,719,269.36

4 100,000,000.00 9.00% 9,000,000.0

0

0.814914 7,334,222.67

5 100,000,000.00 9.00% 9,000,000.0

0

0.774265 6,968,382.59

6 100,000,000.00 9.00% 9,000,000.0

0

0.735643 6,620,791.06

7 100,000,000.00 9.00% 9,000,000.0

0

0.698949 6,290,537.82

8 100,000,000.00 9.00% 9,000,000.0

0

0.664084 5,976,758.03

9 100,000,000.00 9.00% 9,000,000.0

0

0.630959 5,678,629.95

10 100,000,000.00 9.00% 9,000,000.0

0

0.599486 5,395,372.88

11 100,000,000.00 9.00% 9,000,000.0

0

0.569583 5,126,245.01

12 100,000,000.00 9.00% 9,000,000.0 0.541171 4,870,541.58

FIXED INCOME AND CREDIT RISK

0

3 100,000,000.00 9.00% 9,000,000.0

0

0.857697 7,719,269.36

4 100,000,000.00 9.00% 9,000,000.0

0

0.814914 7,334,222.67

5 100,000,000.00 9.00% 9,000,000.0

0

0.774265 6,968,382.59

6 100,000,000.00 9.00% 9,000,000.0

0

0.735643 6,620,791.06

7 100,000,000.00 9.00% 9,000,000.0

0

0.698949 6,290,537.82

8 100,000,000.00 9.00% 9,000,000.0

0

0.664084 5,976,758.03

9 100,000,000.00 9.00% 9,000,000.0

0

0.630959 5,678,629.95

10 100,000,000.00 9.00% 9,000,000.0

0

0.599486 5,395,372.88

11 100,000,000.00 9.00% 9,000,000.0

0

0.569583 5,126,245.01

12 100,000,000.00 9.00% 9,000,000.0 0.541171 4,870,541.58

26

FIXED INCOME AND CREDIT RISK

0

13 100,000,000.00 9.00% 9,000,000.0

0

0.514177 4,627,592.95

14 100,000,000.00 9.00% 9,000,000.0

0

0.488529 4,396,762.90

15 100,000,000.00 9.00% 9,000,000.0

0

0.464161 4,177,446.93

16 100,000,000.00 9.00% 9,000,000.0

0

0.441008 3,969,070.72

17 100,000,000.00 9.00% 9,000,000.0

0

0.41901 3,771,088.57

18 100,000,000.00 9.00% 9,000,000.0

0

0.398109 3,582,982.02

19 100,000,000.00 9.00% 9,000,000.0

0

0.378251 3,404,258.45

20 100,000,000.00 9.00% 9,000,000.0

0

0.359383 3,234,449.83

21 100,000,000.00 9.00% 9,000,000.0

0

0.341457 3,073,111.48

22 100,000,000.00 9.00% 9,000,000.0 0.324425 2,919,820.88

FIXED INCOME AND CREDIT RISK

0

13 100,000,000.00 9.00% 9,000,000.0

0

0.514177 4,627,592.95

14 100,000,000.00 9.00% 9,000,000.0

0

0.488529 4,396,762.90

15 100,000,000.00 9.00% 9,000,000.0

0

0.464161 4,177,446.93

16 100,000,000.00 9.00% 9,000,000.0

0

0.441008 3,969,070.72

17 100,000,000.00 9.00% 9,000,000.0

0

0.41901 3,771,088.57

18 100,000,000.00 9.00% 9,000,000.0

0

0.398109 3,582,982.02

19 100,000,000.00 9.00% 9,000,000.0

0

0.378251 3,404,258.45

20 100,000,000.00 9.00% 9,000,000.0

0

0.359383 3,234,449.83

21 100,000,000.00 9.00% 9,000,000.0

0

0.341457 3,073,111.48

22 100,000,000.00 9.00% 9,000,000.0 0.324425 2,919,820.88

27

FIXED INCOME AND CREDIT RISK

0

23 100,000,000.00 9.00% 9,000,000.0

0

0.308242 2,774,176.61

24 100,000,000.00 9.00% 9,000,000.0

0

0.292866 2,635,797.25

25 100,000,000.00 9.00% 9,000,000.0

0

0.278258 2,504,320.43

26 100,000,000.00 9.00% 9,000,000.0

0

0.264378 2,379,401.84

27 100,000,000.00 9.00% 9,000,000.0

0

0.25119 2,260,714.33

28 100,000,000.00 9.00% 9,000,000.0

0

0.238661 2,147,947.11

29 100,000,000.00 9.00% 9,000,000.0

0

0.226756 2,040,804.85

30 100,000,000.00 9.00% 9,000,000.0

0

0.215445 1,939,006.99

However, as already mentioned that the reliability of the above data is questionable because to

expect that LIBOR would remain at 3.25% over the course of 30 years, i.e. time after which the

FIXED INCOME AND CREDIT RISK

0

23 100,000,000.00 9.00% 9,000,000.0

0

0.308242 2,774,176.61

24 100,000,000.00 9.00% 9,000,000.0

0

0.292866 2,635,797.25

25 100,000,000.00 9.00% 9,000,000.0

0

0.278258 2,504,320.43

26 100,000,000.00 9.00% 9,000,000.0

0

0.264378 2,379,401.84

27 100,000,000.00 9.00% 9,000,000.0

0

0.25119 2,260,714.33

28 100,000,000.00 9.00% 9,000,000.0

0

0.238661 2,147,947.11

29 100,000,000.00 9.00% 9,000,000.0

0

0.226756 2,040,804.85

30 100,000,000.00 9.00% 9,000,000.0

0

0.215445 1,939,006.99

However, as already mentioned that the reliability of the above data is questionable because to

expect that LIBOR would remain at 3.25% over the course of 30 years, i.e. time after which the

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

28

FIXED INCOME AND CREDIT RISK

respective bonds shall be matured will be extremely naïve from financial view point. Thus, in

order to address the concern of the investors it would be beneficial to calculate the present value

of spreads by using different LIBOR rates. This will enable the investors to understand the

expected outcome of investing in the bond even if the market rate of interest changes in the

future (Ismailov and Rossi, 2018).

As already mentioned that the benefit of calculating the present value of spreads of bonds as well

as present value of bond is that the periodical coupon amount does not change. In this case the

annual interest on Deutsche and EBRD bond will remain at 9% and 7.25% of the nominal

amount of bond. Thus, to compensate the future uncertainty in market rate of interest little

adjustments to the LIBOR will be helpful in calculating the present value of spreads.

Accordingly, the present value of spread is calculated for both bonds by using different LIBOR

(Sushko et. al. 2017).

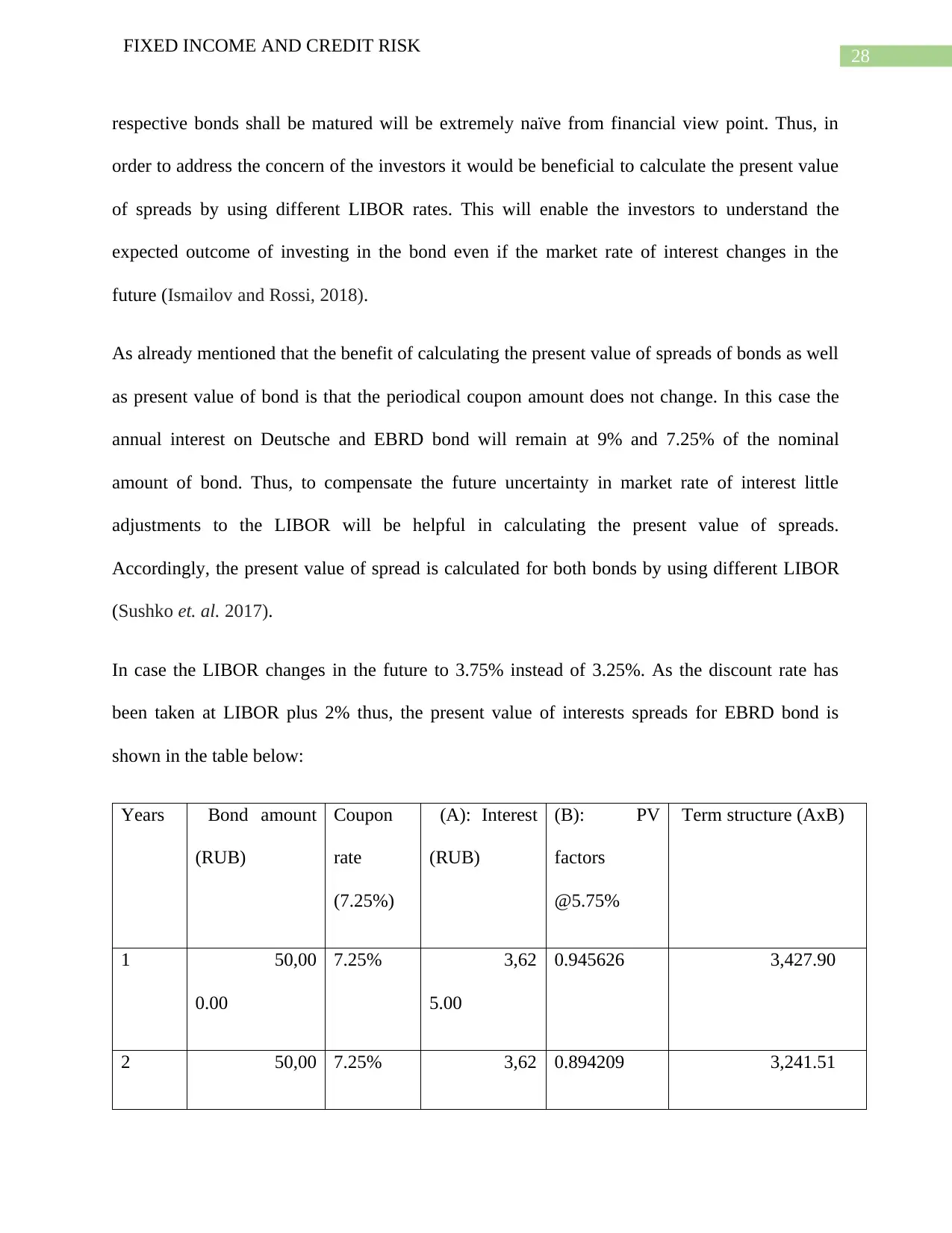

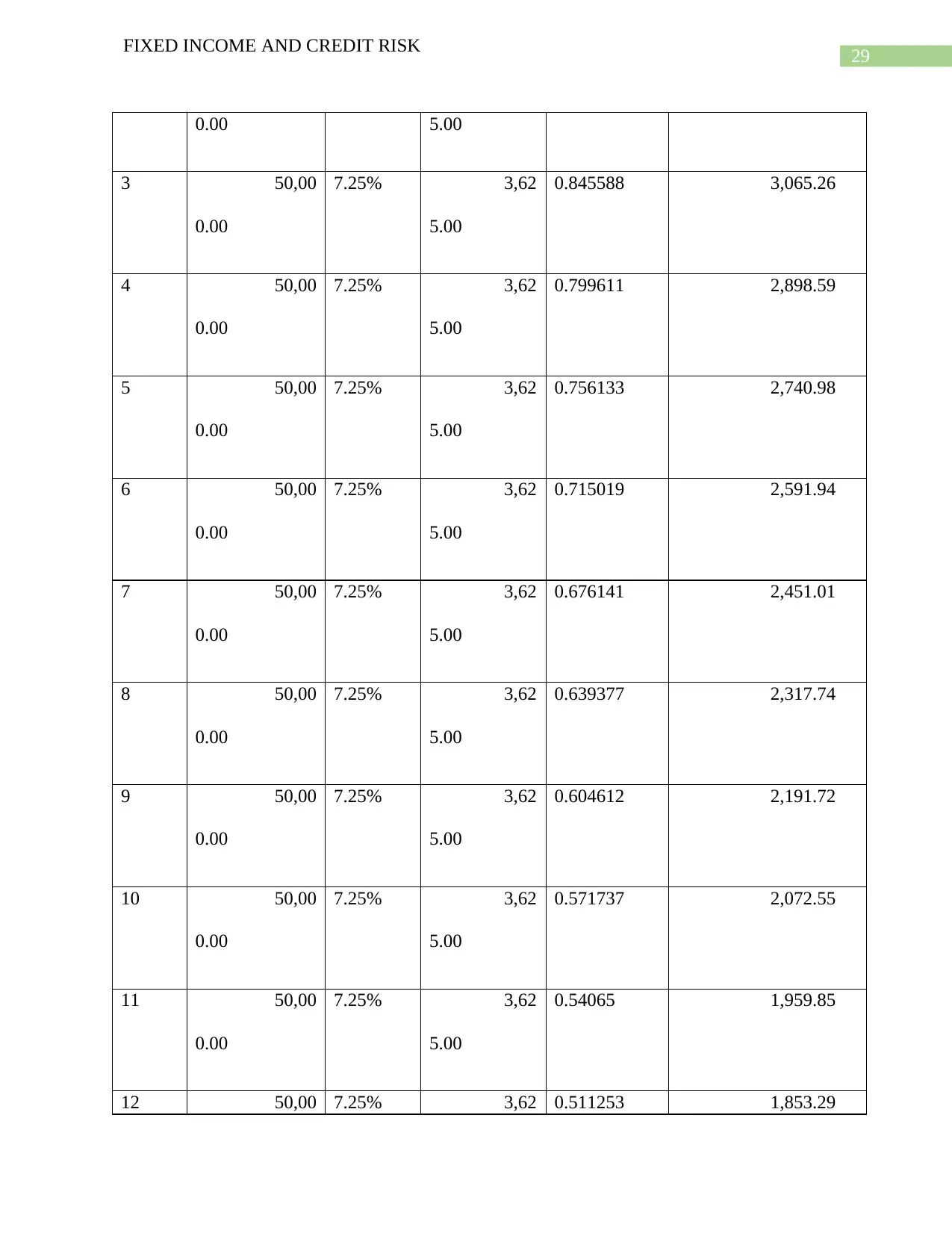

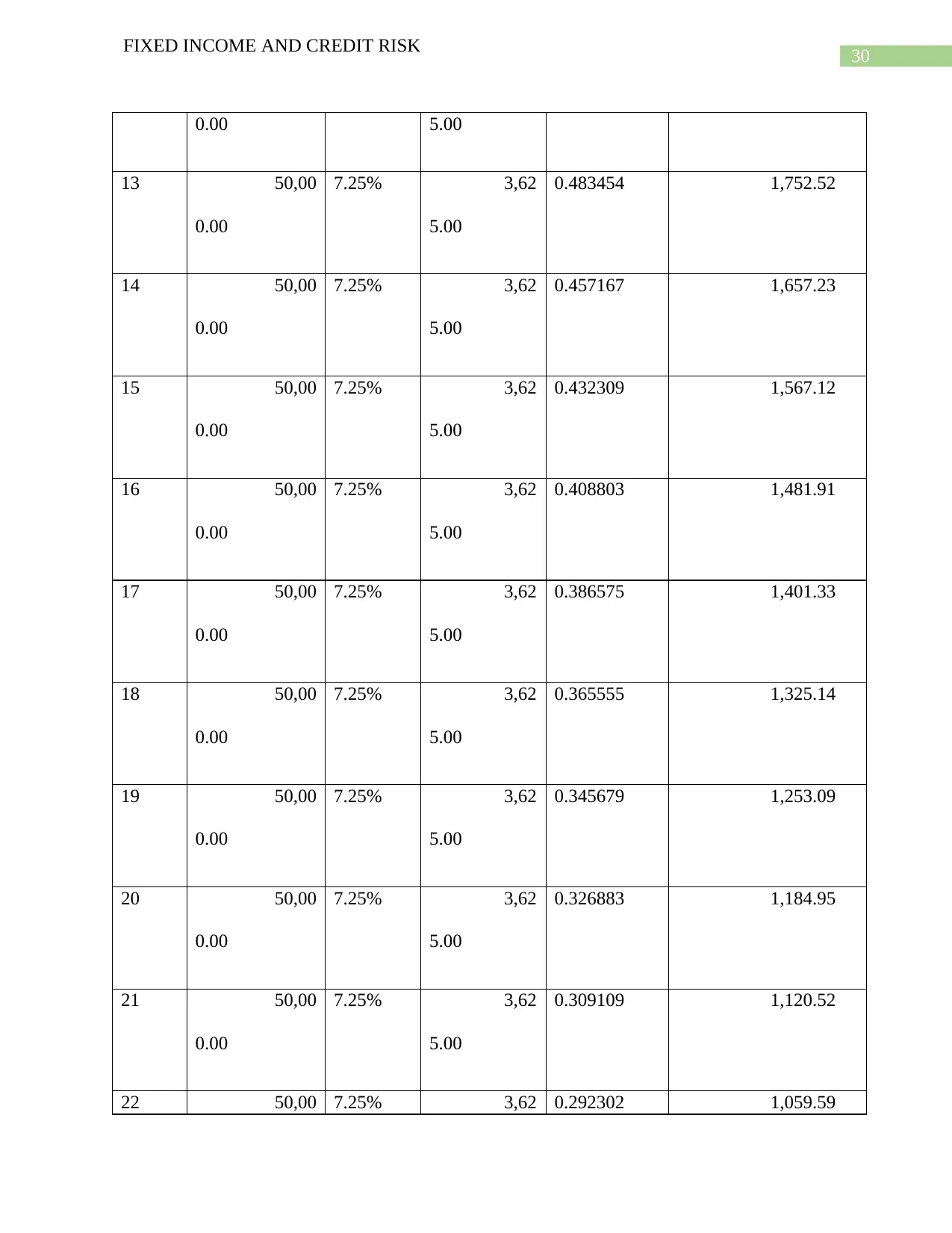

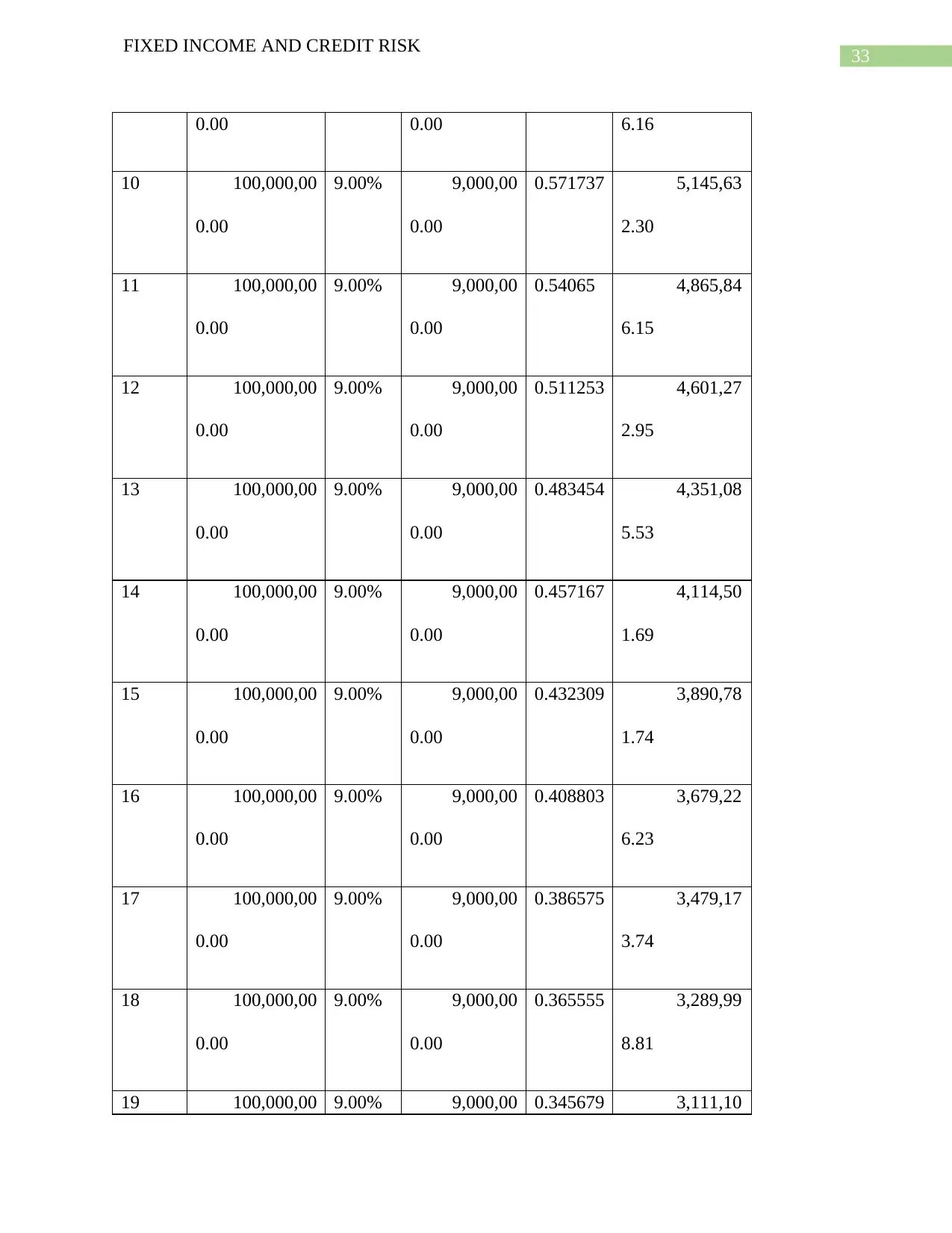

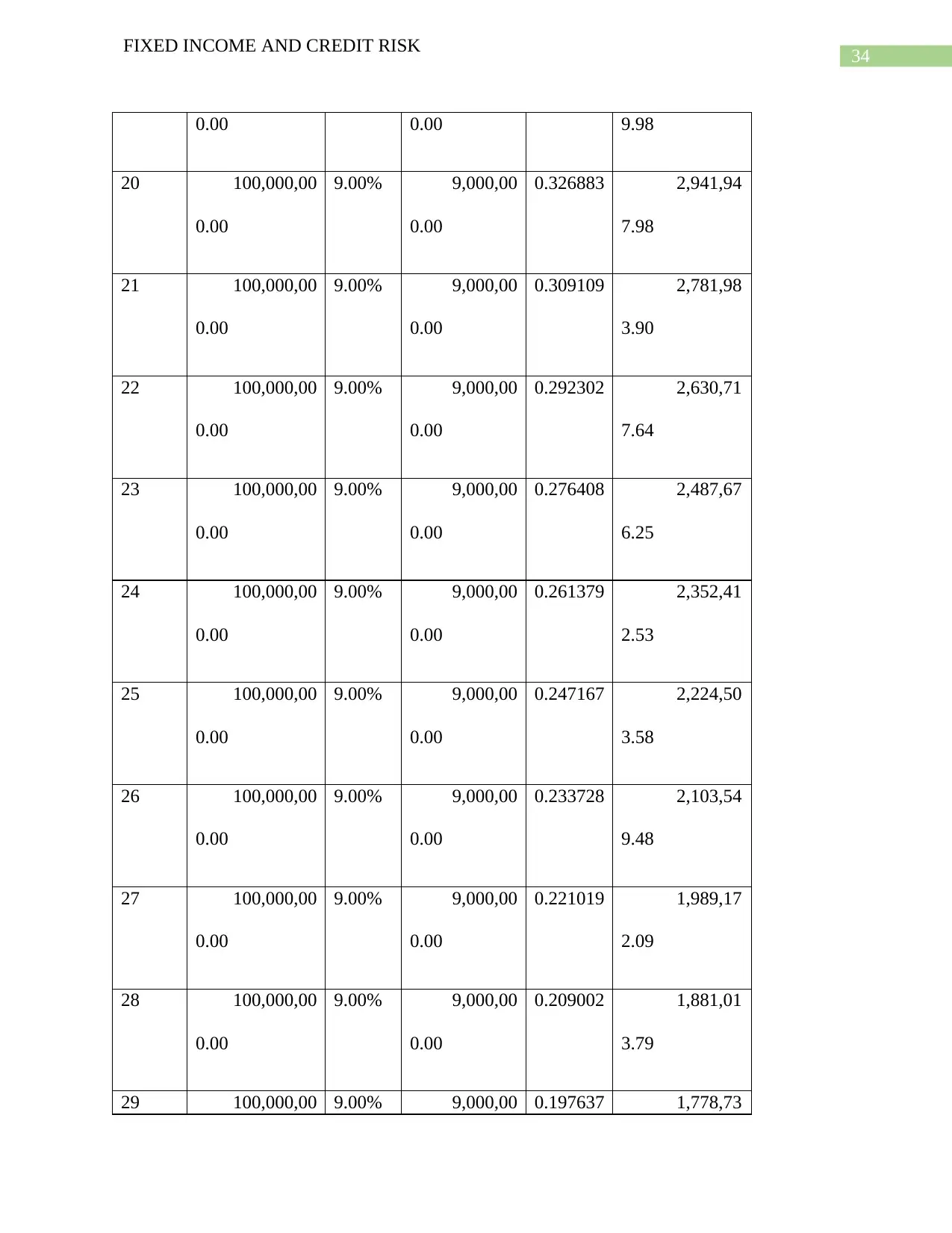

In case the LIBOR changes in the future to 3.75% instead of 3.25%. As the discount rate has

been taken at LIBOR plus 2% thus, the present value of interests spreads for EBRD bond is

shown in the table below:

Years Bond amount

(RUB)

Coupon

rate

(7.25%)

(A): Interest

(RUB)

(B): PV

factors

@5.75%

Term structure (AxB)

1 50,00

0.00

7.25% 3,62

5.00

0.945626 3,427.90

2 50,00 7.25% 3,62 0.894209 3,241.51

FIXED INCOME AND CREDIT RISK

respective bonds shall be matured will be extremely naïve from financial view point. Thus, in

order to address the concern of the investors it would be beneficial to calculate the present value

of spreads by using different LIBOR rates. This will enable the investors to understand the

expected outcome of investing in the bond even if the market rate of interest changes in the

future (Ismailov and Rossi, 2018).

As already mentioned that the benefit of calculating the present value of spreads of bonds as well

as present value of bond is that the periodical coupon amount does not change. In this case the

annual interest on Deutsche and EBRD bond will remain at 9% and 7.25% of the nominal

amount of bond. Thus, to compensate the future uncertainty in market rate of interest little

adjustments to the LIBOR will be helpful in calculating the present value of spreads.

Accordingly, the present value of spread is calculated for both bonds by using different LIBOR

(Sushko et. al. 2017).

In case the LIBOR changes in the future to 3.75% instead of 3.25%. As the discount rate has

been taken at LIBOR plus 2% thus, the present value of interests spreads for EBRD bond is

shown in the table below:

Years Bond amount

(RUB)

Coupon

rate

(7.25%)

(A): Interest

(RUB)

(B): PV

factors

@5.75%

Term structure (AxB)

1 50,00

0.00

7.25% 3,62

5.00

0.945626 3,427.90

2 50,00 7.25% 3,62 0.894209 3,241.51

29

FIXED INCOME AND CREDIT RISK

0.00 5.00

3 50,00

0.00

7.25% 3,62

5.00

0.845588 3,065.26

4 50,00

0.00

7.25% 3,62

5.00

0.799611 2,898.59

5 50,00

0.00

7.25% 3,62

5.00

0.756133 2,740.98

6 50,00

0.00

7.25% 3,62

5.00

0.715019 2,591.94

7 50,00

0.00

7.25% 3,62

5.00

0.676141 2,451.01

8 50,00

0.00

7.25% 3,62

5.00

0.639377 2,317.74

9 50,00

0.00

7.25% 3,62

5.00

0.604612 2,191.72

10 50,00

0.00

7.25% 3,62

5.00

0.571737 2,072.55

11 50,00

0.00

7.25% 3,62

5.00

0.54065 1,959.85

12 50,00 7.25% 3,62 0.511253 1,853.29

FIXED INCOME AND CREDIT RISK

0.00 5.00

3 50,00

0.00

7.25% 3,62

5.00

0.845588 3,065.26

4 50,00

0.00

7.25% 3,62

5.00

0.799611 2,898.59

5 50,00

0.00

7.25% 3,62

5.00

0.756133 2,740.98

6 50,00

0.00

7.25% 3,62

5.00

0.715019 2,591.94

7 50,00

0.00

7.25% 3,62

5.00

0.676141 2,451.01

8 50,00

0.00

7.25% 3,62

5.00

0.639377 2,317.74

9 50,00

0.00

7.25% 3,62

5.00

0.604612 2,191.72

10 50,00

0.00

7.25% 3,62

5.00

0.571737 2,072.55

11 50,00

0.00

7.25% 3,62

5.00

0.54065 1,959.85

12 50,00 7.25% 3,62 0.511253 1,853.29

30

FIXED INCOME AND CREDIT RISK

0.00 5.00

13 50,00

0.00

7.25% 3,62

5.00

0.483454 1,752.52

14 50,00

0.00

7.25% 3,62

5.00

0.457167 1,657.23

15 50,00

0.00

7.25% 3,62

5.00

0.432309 1,567.12

16 50,00

0.00

7.25% 3,62

5.00

0.408803 1,481.91

17 50,00

0.00

7.25% 3,62

5.00

0.386575 1,401.33

18 50,00

0.00

7.25% 3,62

5.00

0.365555 1,325.14

19 50,00

0.00

7.25% 3,62

5.00

0.345679 1,253.09

20 50,00

0.00

7.25% 3,62

5.00

0.326883 1,184.95

21 50,00

0.00

7.25% 3,62

5.00

0.309109 1,120.52

22 50,00 7.25% 3,62 0.292302 1,059.59

FIXED INCOME AND CREDIT RISK

0.00 5.00

13 50,00

0.00

7.25% 3,62

5.00

0.483454 1,752.52

14 50,00

0.00

7.25% 3,62

5.00

0.457167 1,657.23

15 50,00

0.00

7.25% 3,62

5.00

0.432309 1,567.12

16 50,00

0.00

7.25% 3,62

5.00

0.408803 1,481.91

17 50,00

0.00

7.25% 3,62

5.00

0.386575 1,401.33

18 50,00

0.00

7.25% 3,62

5.00

0.365555 1,325.14

19 50,00

0.00

7.25% 3,62

5.00

0.345679 1,253.09

20 50,00

0.00

7.25% 3,62

5.00

0.326883 1,184.95

21 50,00

0.00

7.25% 3,62

5.00

0.309109 1,120.52

22 50,00 7.25% 3,62 0.292302 1,059.59

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

31

FIXED INCOME AND CREDIT RISK

0.00 5.00

23 50,00

0.00

7.25% 3,62

5.00

0.276408 1,001.98

24 50,00

0.00

7.25% 3,62

5.00

0.261379 947.50

25 50,00

0.00

7.25% 3,62

5.00

0.247167 895.98

26 50,00

0.00

7.25% 3,62

5.00

0.233728 847.26

27 50,00

0.00

7.25% 3,62

5.00

0.221019 801.19

28 50,00

0.00

7.25% 3,62

5.00

0.209002 757.63

29 50,00

0.00

7.25% 3,62

5.00

0.197637 716.44

30 50,00

0.00

7.25% 3,62

5.00

0.186891 677.48

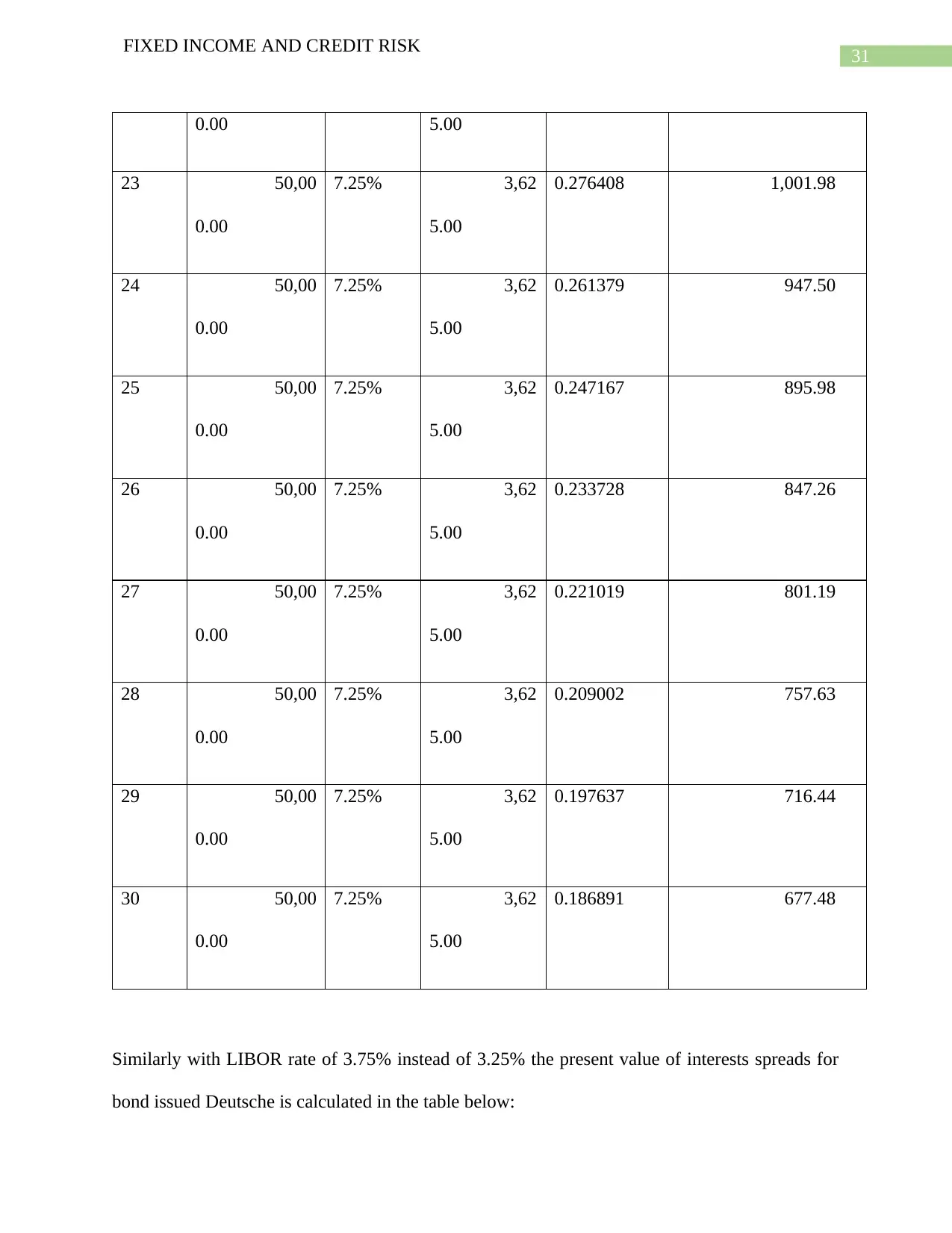

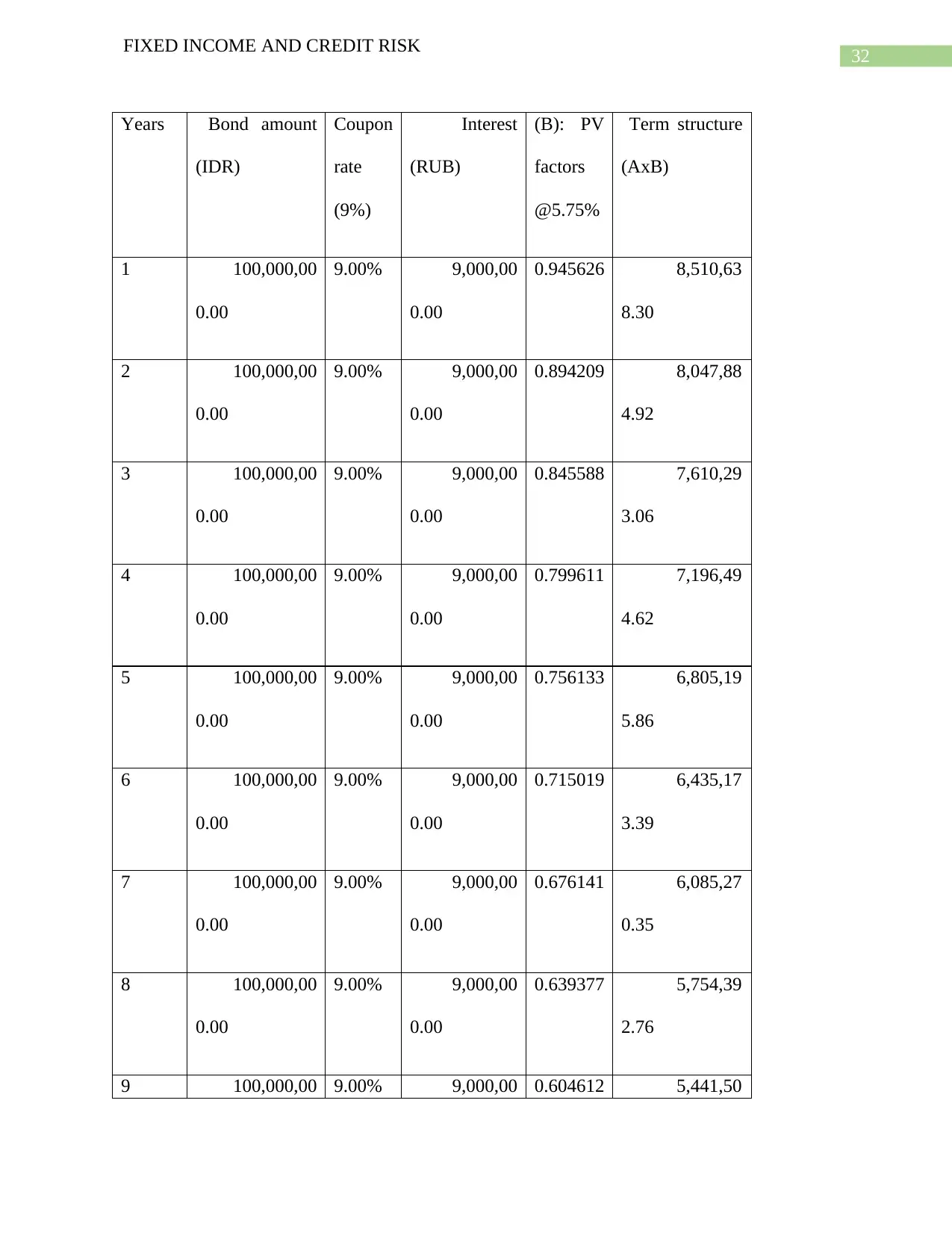

Similarly with LIBOR rate of 3.75% instead of 3.25% the present value of interests spreads for

bond issued Deutsche is calculated in the table below:

FIXED INCOME AND CREDIT RISK

0.00 5.00

23 50,00

0.00

7.25% 3,62

5.00

0.276408 1,001.98

24 50,00

0.00

7.25% 3,62

5.00

0.261379 947.50

25 50,00

0.00

7.25% 3,62

5.00

0.247167 895.98

26 50,00

0.00

7.25% 3,62

5.00

0.233728 847.26

27 50,00

0.00

7.25% 3,62

5.00

0.221019 801.19

28 50,00

0.00

7.25% 3,62

5.00

0.209002 757.63

29 50,00

0.00

7.25% 3,62

5.00

0.197637 716.44

30 50,00

0.00

7.25% 3,62

5.00

0.186891 677.48

Similarly with LIBOR rate of 3.75% instead of 3.25% the present value of interests spreads for

bond issued Deutsche is calculated in the table below:

32

FIXED INCOME AND CREDIT RISK

Years Bond amount

(IDR)

Coupon

rate

(9%)

Interest

(RUB)

(B): PV

factors

@5.75%

Term structure

(AxB)

1 100,000,00

0.00

9.00% 9,000,00

0.00

0.945626 8,510,63

8.30

2 100,000,00

0.00

9.00% 9,000,00

0.00

0.894209 8,047,88

4.92

3 100,000,00

0.00

9.00% 9,000,00

0.00

0.845588 7,610,29

3.06

4 100,000,00

0.00

9.00% 9,000,00

0.00

0.799611 7,196,49

4.62

5 100,000,00

0.00

9.00% 9,000,00

0.00

0.756133 6,805,19

5.86

6 100,000,00

0.00

9.00% 9,000,00

0.00

0.715019 6,435,17

3.39

7 100,000,00

0.00

9.00% 9,000,00

0.00

0.676141 6,085,27

0.35

8 100,000,00

0.00

9.00% 9,000,00

0.00

0.639377 5,754,39

2.76

9 100,000,00 9.00% 9,000,00 0.604612 5,441,50

FIXED INCOME AND CREDIT RISK

Years Bond amount

(IDR)

Coupon

rate

(9%)

Interest

(RUB)

(B): PV

factors

@5.75%

Term structure

(AxB)

1 100,000,00

0.00

9.00% 9,000,00

0.00

0.945626 8,510,63

8.30

2 100,000,00

0.00

9.00% 9,000,00

0.00

0.894209 8,047,88

4.92

3 100,000,00

0.00

9.00% 9,000,00

0.00

0.845588 7,610,29

3.06

4 100,000,00

0.00

9.00% 9,000,00

0.00

0.799611 7,196,49

4.62

5 100,000,00

0.00

9.00% 9,000,00

0.00

0.756133 6,805,19

5.86

6 100,000,00

0.00

9.00% 9,000,00

0.00

0.715019 6,435,17

3.39

7 100,000,00

0.00

9.00% 9,000,00

0.00

0.676141 6,085,27

0.35

8 100,000,00

0.00

9.00% 9,000,00

0.00

0.639377 5,754,39

2.76

9 100,000,00 9.00% 9,000,00 0.604612 5,441,50

33

FIXED INCOME AND CREDIT RISK

0.00 0.00 6.16

10 100,000,00

0.00

9.00% 9,000,00

0.00

0.571737 5,145,63

2.30

11 100,000,00

0.00

9.00% 9,000,00

0.00

0.54065 4,865,84

6.15

12 100,000,00

0.00

9.00% 9,000,00

0.00

0.511253 4,601,27

2.95

13 100,000,00

0.00

9.00% 9,000,00

0.00

0.483454 4,351,08

5.53

14 100,000,00

0.00

9.00% 9,000,00

0.00

0.457167 4,114,50

1.69

15 100,000,00

0.00

9.00% 9,000,00

0.00

0.432309 3,890,78

1.74

16 100,000,00

0.00

9.00% 9,000,00

0.00

0.408803 3,679,22

6.23

17 100,000,00

0.00

9.00% 9,000,00

0.00

0.386575 3,479,17

3.74

18 100,000,00

0.00

9.00% 9,000,00

0.00

0.365555 3,289,99

8.81

19 100,000,00 9.00% 9,000,00 0.345679 3,111,10

FIXED INCOME AND CREDIT RISK

0.00 0.00 6.16

10 100,000,00

0.00

9.00% 9,000,00

0.00

0.571737 5,145,63

2.30

11 100,000,00

0.00

9.00% 9,000,00

0.00

0.54065 4,865,84

6.15

12 100,000,00

0.00

9.00% 9,000,00

0.00

0.511253 4,601,27

2.95

13 100,000,00

0.00

9.00% 9,000,00

0.00

0.483454 4,351,08

5.53

14 100,000,00

0.00

9.00% 9,000,00

0.00

0.457167 4,114,50

1.69

15 100,000,00

0.00

9.00% 9,000,00

0.00

0.432309 3,890,78

1.74

16 100,000,00

0.00

9.00% 9,000,00

0.00

0.408803 3,679,22

6.23

17 100,000,00

0.00

9.00% 9,000,00

0.00

0.386575 3,479,17

3.74

18 100,000,00

0.00

9.00% 9,000,00

0.00

0.365555 3,289,99

8.81

19 100,000,00 9.00% 9,000,00 0.345679 3,111,10

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

34

FIXED INCOME AND CREDIT RISK

0.00 0.00 9.98

20 100,000,00

0.00

9.00% 9,000,00

0.00

0.326883 2,941,94

7.98

21 100,000,00

0.00

9.00% 9,000,00

0.00

0.309109 2,781,98

3.90

22 100,000,00

0.00

9.00% 9,000,00

0.00

0.292302 2,630,71

7.64

23 100,000,00

0.00

9.00% 9,000,00

0.00

0.276408 2,487,67

6.25

24 100,000,00

0.00

9.00% 9,000,00

0.00

0.261379 2,352,41

2.53

25 100,000,00

0.00

9.00% 9,000,00

0.00

0.247167 2,224,50

3.58

26 100,000,00

0.00

9.00% 9,000,00

0.00

0.233728 2,103,54

9.48

27 100,000,00

0.00

9.00% 9,000,00

0.00

0.221019 1,989,17

2.09

28 100,000,00

0.00

9.00% 9,000,00

0.00

0.209002 1,881,01

3.79

29 100,000,00 9.00% 9,000,00 0.197637 1,778,73

FIXED INCOME AND CREDIT RISK

0.00 0.00 9.98

20 100,000,00

0.00

9.00% 9,000,00

0.00

0.326883 2,941,94

7.98

21 100,000,00

0.00

9.00% 9,000,00

0.00

0.309109 2,781,98

3.90

22 100,000,00

0.00

9.00% 9,000,00

0.00

0.292302 2,630,71

7.64

23 100,000,00

0.00

9.00% 9,000,00

0.00

0.276408 2,487,67

6.25

24 100,000,00

0.00

9.00% 9,000,00

0.00

0.261379 2,352,41

2.53

25 100,000,00

0.00

9.00% 9,000,00

0.00

0.247167 2,224,50

3.58

26 100,000,00

0.00

9.00% 9,000,00

0.00

0.233728 2,103,54

9.48

27 100,000,00

0.00

9.00% 9,000,00

0.00

0.221019 1,989,17

2.09

28 100,000,00

0.00

9.00% 9,000,00

0.00

0.209002 1,881,01

3.79

29 100,000,00 9.00% 9,000,00 0.197637 1,778,73

35

FIXED INCOME AND CREDIT RISK

0.00 0.00 6.45

30 100,000,00

0.00

9.00% 9,000,00

0.00

0.186891 1,682,02

0.28

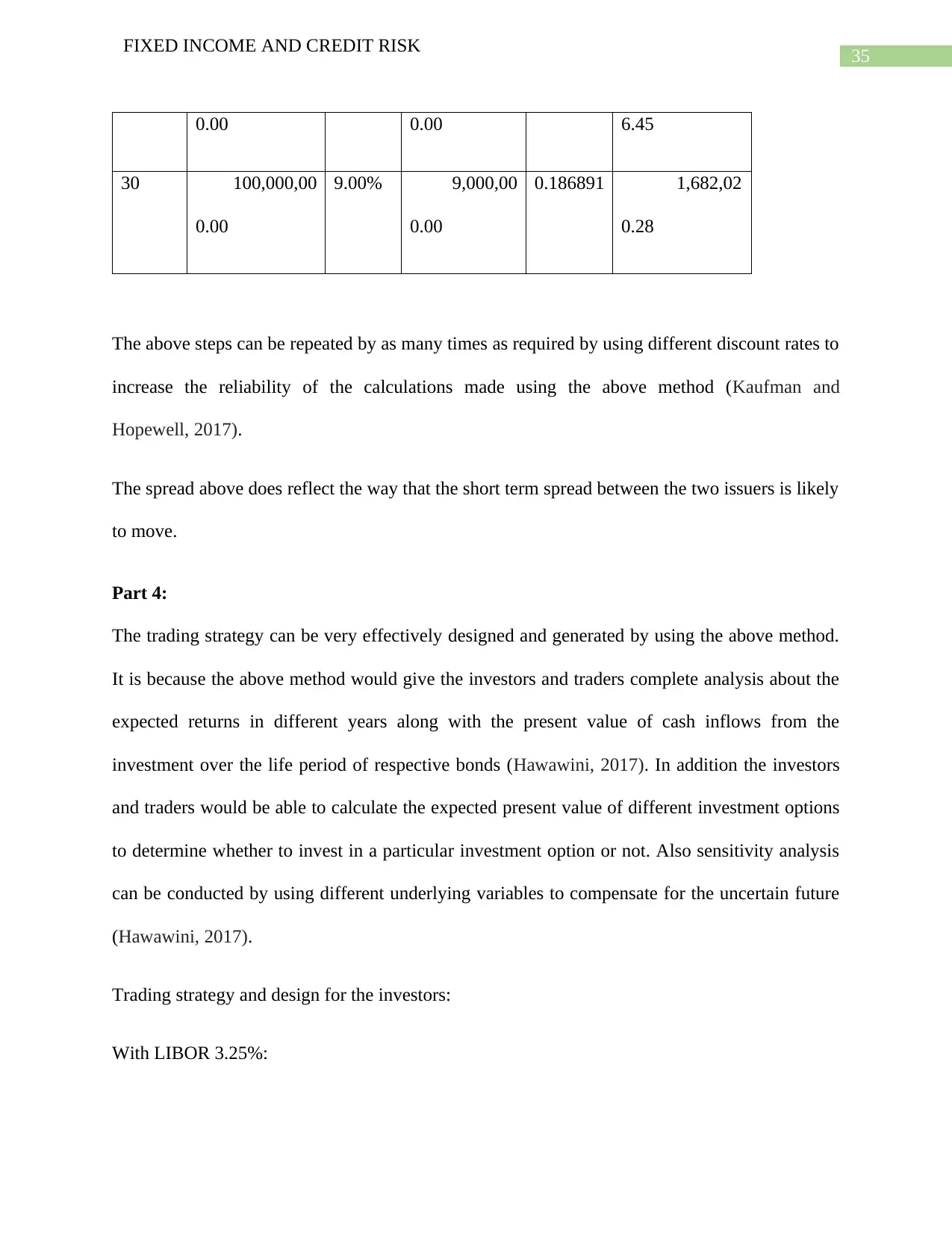

The above steps can be repeated by as many times as required by using different discount rates to

increase the reliability of the calculations made using the above method (Kaufman and

Hopewell, 2017).

The spread above does reflect the way that the short term spread between the two issuers is likely

to move.

Part 4:

The trading strategy can be very effectively designed and generated by using the above method.

It is because the above method would give the investors and traders complete analysis about the

expected returns in different years along with the present value of cash inflows from the

investment over the life period of respective bonds (Hawawini, 2017). In addition the investors

and traders would be able to calculate the expected present value of different investment options

to determine whether to invest in a particular investment option or not. Also sensitivity analysis

can be conducted by using different underlying variables to compensate for the uncertain future

(Hawawini, 2017).

Trading strategy and design for the investors:

With LIBOR 3.25%:

FIXED INCOME AND CREDIT RISK

0.00 0.00 6.45

30 100,000,00

0.00

9.00% 9,000,00

0.00

0.186891 1,682,02

0.28

The above steps can be repeated by as many times as required by using different discount rates to

increase the reliability of the calculations made using the above method (Kaufman and

Hopewell, 2017).

The spread above does reflect the way that the short term spread between the two issuers is likely

to move.

Part 4:

The trading strategy can be very effectively designed and generated by using the above method.

It is because the above method would give the investors and traders complete analysis about the

expected returns in different years along with the present value of cash inflows from the

investment over the life period of respective bonds (Hawawini, 2017). In addition the investors

and traders would be able to calculate the expected present value of different investment options

to determine whether to invest in a particular investment option or not. Also sensitivity analysis

can be conducted by using different underlying variables to compensate for the uncertain future

(Hawawini, 2017).

Trading strategy and design for the investors:

With LIBOR 3.25%:

36

FIXED INCOME AND CREDIT RISK

For EBRD bond:

The present value of EBRD bond is 64,943.90 RUB with nominal value of the bond is 50,000

RUB hence, investors should certainly invest in the bond in case the above circumstances persist

in the future (Schlarbaum, Racette and Boquist, 2017).

For Deutsche bond:

The present value of Deutsche bond is 156,039,627.08 with discount rate of 5.25% (LIBOR

3.25% + 2%) is significantly higher than the Nominal value of the bond hence, the option

provides significant opportunity to earn substantial return on the amount of investment in the

bond. Hence, the investor should invest in the bond (Schlarbaum, Racette and Boquist, 2017).

FIXED INCOME AND CREDIT RISK

For EBRD bond:

The present value of EBRD bond is 64,943.90 RUB with nominal value of the bond is 50,000

RUB hence, investors should certainly invest in the bond in case the above circumstances persist

in the future (Schlarbaum, Racette and Boquist, 2017).

For Deutsche bond:

The present value of Deutsche bond is 156,039,627.08 with discount rate of 5.25% (LIBOR

3.25% + 2%) is significantly higher than the Nominal value of the bond hence, the option

provides significant opportunity to earn substantial return on the amount of investment in the

bond. Hence, the investor should invest in the bond (Schlarbaum, Racette and Boquist, 2017).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

37

FIXED INCOME AND CREDIT RISK

References:

Borio, C.E., McCauley, R.N., McGuire, P. and Sushko, V., 2016. Covered interest parity lost:

understanding the cross-currency basis.

Borio, C.E., McCauley, R.N., McGuire, P. and Sushko, V., 2016. Covered interest parity lost:

understanding the cross-currency basis.

Campbell, J.Y., Sunderam, A. and Viceira, L.M., 2017. Inflation bets or deflation hedges? the

changing risks of nominal bonds. Critical Finance Review, 6(2), pp.263-301.

Du, W., Tepper, A. and Verdelhan, A., 2018. Deviations from covered interest rate parity. The

Journal of Finance, 73(3), pp.915-957.

Du, W., Tepper, A. and Verdelhan, A., 2018. Deviations from covered interest rate parity. The

Journal of Finance, 73(3), pp.915-957.

Hanson, S.G. and Stein, J.C., 2015. Monetary policy and long-term real rates. Journal of

Financial Economics, 115(3), pp.429-448. Hanson, S.G. and Stein, J.C., 2015. Monetary policy

and long-term real rates. Journal of Financial Economics, 115(3), pp.429-448.

Hawawini, G., 2017. Bond Duration and Immunization: Early Developments and Recent

Contributions. Routledge. Available at:

https://www.taylorfrancis.com/books/e/9781351381116/chapters/10.4324%2F9781315145976-1

[Accessed on 15 November 2018]

Hawawini, G., 2017. The Mathematics of Macaulay’s Duration. In Bond Duration and

Immunization (pp. 47-55). Routledge.

FIXED INCOME AND CREDIT RISK

References:

Borio, C.E., McCauley, R.N., McGuire, P. and Sushko, V., 2016. Covered interest parity lost:

understanding the cross-currency basis.

Borio, C.E., McCauley, R.N., McGuire, P. and Sushko, V., 2016. Covered interest parity lost:

understanding the cross-currency basis.

Campbell, J.Y., Sunderam, A. and Viceira, L.M., 2017. Inflation bets or deflation hedges? the

changing risks of nominal bonds. Critical Finance Review, 6(2), pp.263-301.

Du, W., Tepper, A. and Verdelhan, A., 2018. Deviations from covered interest rate parity. The

Journal of Finance, 73(3), pp.915-957.

Du, W., Tepper, A. and Verdelhan, A., 2018. Deviations from covered interest rate parity. The

Journal of Finance, 73(3), pp.915-957.

Hanson, S.G. and Stein, J.C., 2015. Monetary policy and long-term real rates. Journal of

Financial Economics, 115(3), pp.429-448. Hanson, S.G. and Stein, J.C., 2015. Monetary policy

and long-term real rates. Journal of Financial Economics, 115(3), pp.429-448.

Hawawini, G., 2017. Bond Duration and Immunization: Early Developments and Recent

Contributions. Routledge. Available at:

https://www.taylorfrancis.com/books/e/9781351381116/chapters/10.4324%2F9781315145976-1

[Accessed on 15 November 2018]

Hawawini, G., 2017. The Mathematics of Macaulay’s Duration. In Bond Duration and

Immunization (pp. 47-55). Routledge.

38

FIXED INCOME AND CREDIT RISK

Ismailov, A. and Rossi, B., 2018. Uncertainty and deviations from uncovered interest rate

parity. Journal of International Money and Finance, 88, pp.242-259.

Kaufman, G.G. and Hopewell, M.H., 2017. Bond price volatility and term to maturity: A

generalized respecification. In Bond Duration and Immunization (pp. 64-68). Routledge.

Available at:

https://www.taylorfrancis.com/books/e/9781351381116/chapters/10.4324%2F9781315145976-5

[Accessed on 15 November 2018]

Kung, H., 2015. Macroeconomic linkages between monetary policy and the term structure of

interest rates. Journal of Financial Economics, 115(1), pp.42-57.

Liao, G.Y., 2016. Credit migration and covered interest rate parity. Project on Behavioral

Finance and Financial Stability Working Paper Series,(2016-07).

Malkiel, B.G., 2015. Term structure of interest rates: expectations and behavior patterns.

Princeton University Press.

Miyajima, K., Mohanty, M.S. and Chan, T., 2015. Emerging market local currency bonds:

diversification and stability. Emerging Markets Review, 22, pp.126-139.

Rachel, L. and Smith, T., 2015. Secular drivers of the global real interest rate.

Schlarbaum, G.G., Racette, G.A. and Boquist, J.A., 2017. Duration and Risk Assessment for

Bonds and Common Stocks. In Bond Duration and Immunization (pp. 102-107). Routledge.

Available at: https://content.taylorfrancis.com/books/e/download?dac=C2017-0-55182-

X&isbn=9781315145976&doi=10.4324/9781315145976-8&format=pdf [Accessed on 15

November 2018]

FIXED INCOME AND CREDIT RISK

Ismailov, A. and Rossi, B., 2018. Uncertainty and deviations from uncovered interest rate

parity. Journal of International Money and Finance, 88, pp.242-259.

Kaufman, G.G. and Hopewell, M.H., 2017. Bond price volatility and term to maturity: A

generalized respecification. In Bond Duration and Immunization (pp. 64-68). Routledge.

Available at:

https://www.taylorfrancis.com/books/e/9781351381116/chapters/10.4324%2F9781315145976-5

[Accessed on 15 November 2018]

Kung, H., 2015. Macroeconomic linkages between monetary policy and the term structure of

interest rates. Journal of Financial Economics, 115(1), pp.42-57.

Liao, G.Y., 2016. Credit migration and covered interest rate parity. Project on Behavioral

Finance and Financial Stability Working Paper Series,(2016-07).

Malkiel, B.G., 2015. Term structure of interest rates: expectations and behavior patterns.

Princeton University Press.

Miyajima, K., Mohanty, M.S. and Chan, T., 2015. Emerging market local currency bonds:

diversification and stability. Emerging Markets Review, 22, pp.126-139.

Rachel, L. and Smith, T., 2015. Secular drivers of the global real interest rate.

Schlarbaum, G.G., Racette, G.A. and Boquist, J.A., 2017. Duration and Risk Assessment for

Bonds and Common Stocks. In Bond Duration and Immunization (pp. 102-107). Routledge.

Available at: https://content.taylorfrancis.com/books/e/download?dac=C2017-0-55182-

X&isbn=9781315145976&doi=10.4324/9781315145976-8&format=pdf [Accessed on 15

November 2018]

39

FIXED INCOME AND CREDIT RISK

Schwarz, K., 2017. Mind the gap: Disentangling credit and liquidity in risk spreads.