Accounting Standards and Regulation: Impairment Test Analysis Report

VerifiedAdded on 2020/02/24

|9

|1895

|82

Report

AI Summary

This report provides an analysis of accounting standards and regulations, specifically focusing on the impairment test as per AASB 136, using Myer Holdings Ltd. as a case study. The report examines evidence of impairment, the process for determining impairment, and the required information. It explores asset turnover, asset flow, and asset base to determine any indication of impairment. The report also discusses the management's flexibility in impairment determination and the restructuring of Myer's Frankston department store. The report references ASIC guidelines and relevant accounting standards, providing a comprehensive overview of the topic.

Running head: ACCOUNTING STANDARDS AND REGULATION

Accounting standards and regulation

Name of the student

Name of the university

Author note

Accounting standards and regulation

Name of the student

Name of the university

Author note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1ACCOUNTING STANDARDS AND REGULATION

Executive summary

The main objective of this report is to focus on the determination of impairment test as per

AASB 136. The report will focus on the impairment evidence, process for the impairment,

required information for impairment and management’s flexibility for impairment with regard

to Myer Holdings Ltd. further, this report will focus on the restructuring of Myer’s Frankston

department store. Moreover, the report will carry out the tests with regard to asset turnover,

asset flow and asset base for determining whether there is any indication of impairment of any

of the stores.

Executive summary

The main objective of this report is to focus on the determination of impairment test as per

AASB 136. The report will focus on the impairment evidence, process for the impairment,

required information for impairment and management’s flexibility for impairment with regard

to Myer Holdings Ltd. further, this report will focus on the restructuring of Myer’s Frankston

department store. Moreover, the report will carry out the tests with regard to asset turnover,

asset flow and asset base for determining whether there is any indication of impairment of any

of the stores.

2ACCOUNTING STANDARDS AND REGULATION

Table of Contents

a. Evidence with regard to the impairment test.......................................................................4

b. Required process for determining the impairment..............................................................4

c. Required information for determining impairment test.......................................................6

d. Management’s flexibility for impairment determination....................................................7

Reference....................................................................................................................................8

Table of Contents

a. Evidence with regard to the impairment test.......................................................................4

b. Required process for determining the impairment..............................................................4

c. Required information for determining impairment test.......................................................6

d. Management’s flexibility for impairment determination....................................................7

Reference....................................................................................................................................8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3ACCOUNTING STANDARDS AND REGULATION

As per the ASIC Media Release 17 – 162, ASIC has kept on approaching

organizations to concentrate on giving data for clients of financial reports that is helpful and

significant. Declaring its concentration ranges for 30 June 2017 annual reports of listed

organizations and and different other public organization with numerous shareholders, ASIC

featured key zones to address. ASIC Commissioner John Price stated, 'As with past

announcing periods, chiefs and evaluators should concentrate on estimations of benefits and

bookkeeping strategy decisions. ASIC keeps on observing organizations utilize improbable

suppositions in testing the estimation of benefits or apply unseemly methodologies in regions,

for example, income acknowledgment.'

IAS 36 and AASB 136 on Impairment of assets ensure that an association's benefit is

not composed in the financial reports at the value which is as compared to the recoverable

sum. The recoverable sum for the asset is higher among the fair value of the asset less cost

associated with disposal and the value in use. Just special case to this is some intangible

resources and goodwill (Zhuang 2016). An association might survey at end of the each

accounting time frame that whether any sign exists there for the impairment of any asset and

if any sign is there, at that point the recoverable value of the asset should be measured. Each

organization is required to carry on the impairment test of its asset if there is any sign that the

asset can be impaired. Further, the test can be carried on for the cash generating unit (CGU)

where the asset does not make any income which is generally autonomous of those of

alternate resources. Different indications that may be used to recognize the fact that whether

the asset is going to be impaired or not are as follows –

Internal factors –

The asset is damaged physically or became obsolete

Company held the asset to be disposed in near future or part of the asset is getting

restructure or being idle for long time (Amiraslani, Iatridis and Pope, 2013)

Performance of the asset is not as per expectation

External factors –

Amount of net assets higher than the capitalization of the market.

Reduction in the value of the asset

Enhancement of the market’s interest rate

As per the ASIC Media Release 17 – 162, ASIC has kept on approaching

organizations to concentrate on giving data for clients of financial reports that is helpful and

significant. Declaring its concentration ranges for 30 June 2017 annual reports of listed

organizations and and different other public organization with numerous shareholders, ASIC

featured key zones to address. ASIC Commissioner John Price stated, 'As with past

announcing periods, chiefs and evaluators should concentrate on estimations of benefits and

bookkeeping strategy decisions. ASIC keeps on observing organizations utilize improbable

suppositions in testing the estimation of benefits or apply unseemly methodologies in regions,

for example, income acknowledgment.'

IAS 36 and AASB 136 on Impairment of assets ensure that an association's benefit is

not composed in the financial reports at the value which is as compared to the recoverable

sum. The recoverable sum for the asset is higher among the fair value of the asset less cost

associated with disposal and the value in use. Just special case to this is some intangible

resources and goodwill (Zhuang 2016). An association might survey at end of the each

accounting time frame that whether any sign exists there for the impairment of any asset and

if any sign is there, at that point the recoverable value of the asset should be measured. Each

organization is required to carry on the impairment test of its asset if there is any sign that the

asset can be impaired. Further, the test can be carried on for the cash generating unit (CGU)

where the asset does not make any income which is generally autonomous of those of

alternate resources. Different indications that may be used to recognize the fact that whether

the asset is going to be impaired or not are as follows –

Internal factors –

The asset is damaged physically or became obsolete

Company held the asset to be disposed in near future or part of the asset is getting

restructure or being idle for long time (Amiraslani, Iatridis and Pope, 2013)

Performance of the asset is not as per expectation

External factors –

Amount of net assets higher than the capitalization of the market.

Reduction in the value of the asset

Enhancement of the market’s interest rate

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4ACCOUNTING STANDARDS AND REGULATION

Unfavourable changes in the assets owing to the economies, technologies, markets and

laws.

a. Evidence with regard to the impairment test

Asset turnover – from the financial statement of Myer Holdings Ltd. it is recognized

that the ratio for the turnover of asset is for past years are ranged between 1.40 and

1.80. Thus, any significant movement for the asset turnover ratio has not been noticed

during the period under consideration. Thus, using this test, it can be stated that no

indication of impairment is there.

Asset base – looking at the asset base of the company, it is found that asset base of

Myer Holdings Ltd. has not experienced much changes and the asset base are almost

same for the past years. Therefore, if the asset base is used to determine the

impairment indication f the asset, there is clear indication that the asset will not be

impaired (Zhuang 2016).

Asset flow – from the given data for the flow of asset, it is identified that flow with

regard to all the assets are consistent or enhanced by little amount. Further, the

decreasing trend for any of the store, which can establish the requirement of

impairment test is not found. Therefore, though this tests also impairment indication

could not be established.

Though through the above strategies, impairment test could not be determined, some

indications are there with regard to the department store of the company in Frankston. It has

been identified that to compete with Amazon, company planned to alter their traditional white

and black colours of the stores with the signage of bright yellow and moreover, the staff of the

company will appear in the uniform which is different from the regular uniform of the

company (Malone, Tarca and Wee 2015). Further, the storage system of the company’s

product will be changed from the previous system that will enable to have more free space. As

per AASB 136, these things will be regarded as partial reconstruction that qualifies for the

determination of the test for impairment.

b. Required process for determining the impairment

For determining the test for impairment, Myer calculates the value in use s well as the

recoverable amount of the asset. The model use the forecasting of cash flow based on the

financial budget approved by the management of Myer and the approval is given for the

Unfavourable changes in the assets owing to the economies, technologies, markets and

laws.

a. Evidence with regard to the impairment test

Asset turnover – from the financial statement of Myer Holdings Ltd. it is recognized

that the ratio for the turnover of asset is for past years are ranged between 1.40 and

1.80. Thus, any significant movement for the asset turnover ratio has not been noticed

during the period under consideration. Thus, using this test, it can be stated that no

indication of impairment is there.

Asset base – looking at the asset base of the company, it is found that asset base of

Myer Holdings Ltd. has not experienced much changes and the asset base are almost

same for the past years. Therefore, if the asset base is used to determine the

impairment indication f the asset, there is clear indication that the asset will not be

impaired (Zhuang 2016).

Asset flow – from the given data for the flow of asset, it is identified that flow with

regard to all the assets are consistent or enhanced by little amount. Further, the

decreasing trend for any of the store, which can establish the requirement of

impairment test is not found. Therefore, though this tests also impairment indication

could not be established.

Though through the above strategies, impairment test could not be determined, some

indications are there with regard to the department store of the company in Frankston. It has

been identified that to compete with Amazon, company planned to alter their traditional white

and black colours of the stores with the signage of bright yellow and moreover, the staff of the

company will appear in the uniform which is different from the regular uniform of the

company (Malone, Tarca and Wee 2015). Further, the storage system of the company’s

product will be changed from the previous system that will enable to have more free space. As

per AASB 136, these things will be regarded as partial reconstruction that qualifies for the

determination of the test for impairment.

b. Required process for determining the impairment

For determining the test for impairment, Myer calculates the value in use s well as the

recoverable amount of the asset. The model use the forecasting of cash flow based on the

financial budget approved by the management of Myer and the approval is given for the

5ACCOUNTING STANDARDS AND REGULATION

period of five years. cash flow more than five years or beyond five years is extrapolated by

using the rate of terminal growth. Major assumptions with regard to the calculation are

mentioned below –

Pre-tax discount rate of 14.4%

Operational margin for gross profit at 39.5%

Terminal growth rate of 2.5%

The management decides the future cash flows from the asset’s carrying value or the

asset’s cash generating unit are as per the budget or it is significantly lower than the budget.

For this purpose, each store of the company is examined separately for determining the

existence of impairment (Gackstatter and Möller 2016). If through the test, it is found that

there is any indication of impairment for any of the store, the recoverable value for the unit is

measured and compared with the value-in-use.

period of five years. cash flow more than five years or beyond five years is extrapolated by

using the rate of terminal growth. Major assumptions with regard to the calculation are

mentioned below –

Pre-tax discount rate of 14.4%

Operational margin for gross profit at 39.5%

Terminal growth rate of 2.5%

The management decides the future cash flows from the asset’s carrying value or the

asset’s cash generating unit are as per the budget or it is significantly lower than the budget.

For this purpose, each store of the company is examined separately for determining the

existence of impairment (Gackstatter and Möller 2016). If through the test, it is found that

there is any indication of impairment for any of the store, the recoverable value for the unit is

measured and compared with the value-in-use.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6ACCOUNTING STANDARDS AND REGULATION

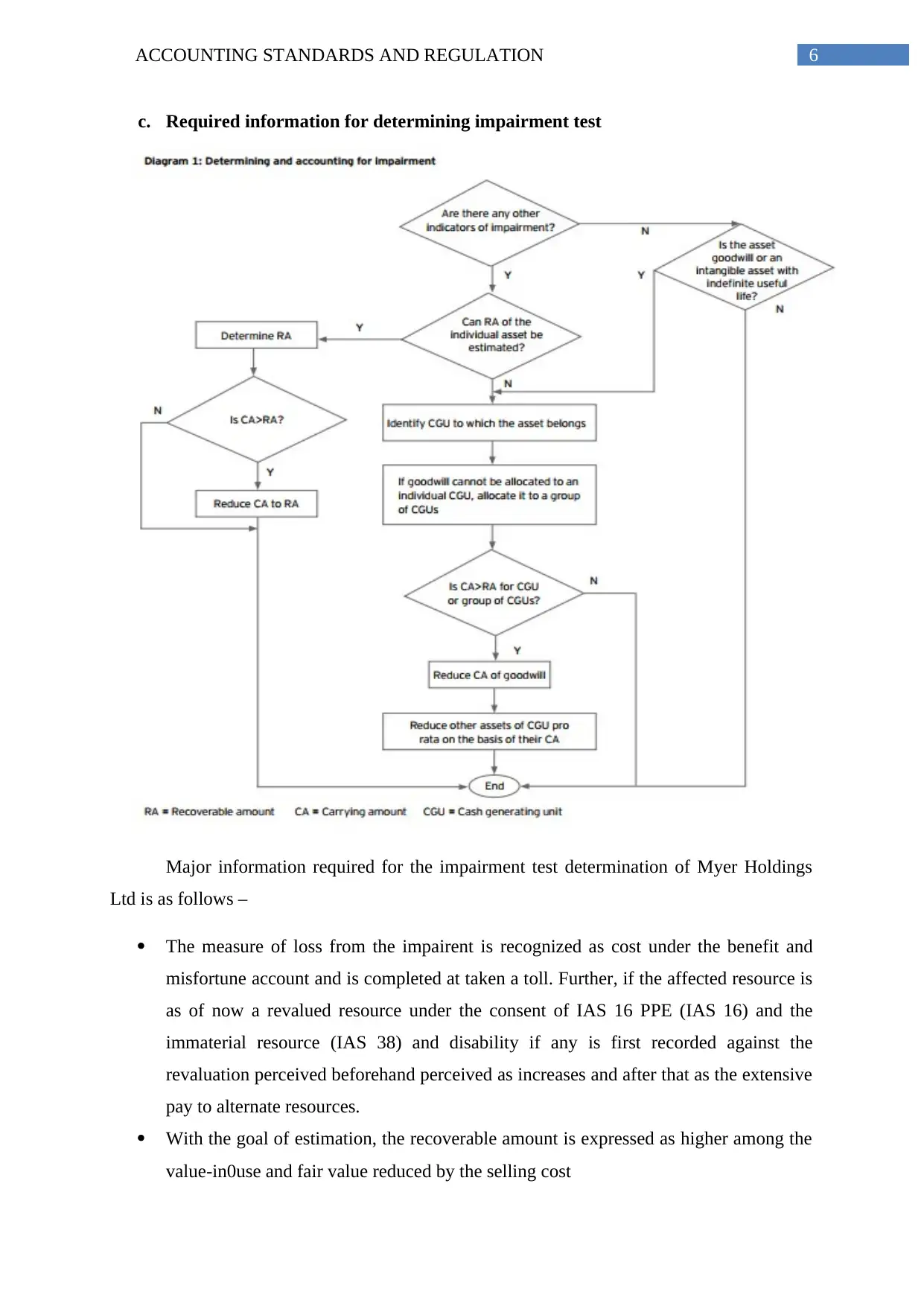

c. Required information for determining impairment test

Major information required for the impairment test determination of Myer Holdings

Ltd is as follows –

The measure of loss from the impairent is recognized as cost under the benefit and

misfortune account and is completed at taken a toll. Further, if the affected resource is

as of now a revalued resource under the consent of IAS 16 PPE (IAS 16) and the

immaterial resource (IAS 38) and disability if any is first recorded against the

revaluation perceived beforehand perceived as increases and after that as the extensive

pay to alternate resources.

With the goal of estimation, the recoverable amount is expressed as higher among the

value-in0use and fair value reduced by the selling cost

c. Required information for determining impairment test

Major information required for the impairment test determination of Myer Holdings

Ltd is as follows –

The measure of loss from the impairent is recognized as cost under the benefit and

misfortune account and is completed at taken a toll. Further, if the affected resource is

as of now a revalued resource under the consent of IAS 16 PPE (IAS 16) and the

immaterial resource (IAS 38) and disability if any is first recorded against the

revaluation perceived beforehand perceived as increases and after that as the extensive

pay to alternate resources.

With the goal of estimation, the recoverable amount is expressed as higher among the

value-in0use and fair value reduced by the selling cost

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7ACCOUNTING STANDARDS AND REGULATION

Loss from impairment that is perceived in the past period for the goodwill or any

advantage must be switched if any adjustment is there concerning the assessments that

were utilized for deciding the recoverable measure of the benefit (Linnenluecke et al.

2015).

Wide divulgences are required for whatever is left of hindrance and acknowledgment

of debilitation misfortune

d. Management’s flexibility for impairment determination

While ASIC does not anticipate that the directors will be specialists accounting they

should look for clarification and counsel supporting the bookkeeping medications picked and,

where proper, challenge the bookkeeping assessments and medicines connected in the

budgetary report. They ought to especially look for exhortation where a treatment does not

mirror their comprehension of the substance of a plan (Bond, Govendir and Wells 2016). Data

ought to be delivered on a convenient premise and be upheld by suitable examination and

documentation for the autonomous review. This will bolster the nature of money related data

in the market and empower reviewers to concentrate on their part in giving free affirmation on

the budgetary report.

It is perceived that the administration of Myer Holdings Ltd is very adaptable in

completing the tests for deciding the asset’s impairment. In addition, the administration

completes survey for the carrying value of the assets for each of the store of the organization

is attempted and distinguished whether sign of any impairment is exists (Kabir and Rahman

2016). According to the prerequisite of AASB 136, they guarantee to do the test for

impedance no less than one in every year Further, the administration decides different

certainties like assurance of the way that whether level without bounds money streams for the

impairment estimation of the advantages for the CGU of Myer. Thus, it is identified that the

company actively manage the test for determination of impairment annually in compliance

with AASB 136.

Loss from impairment that is perceived in the past period for the goodwill or any

advantage must be switched if any adjustment is there concerning the assessments that

were utilized for deciding the recoverable measure of the benefit (Linnenluecke et al.

2015).

Wide divulgences are required for whatever is left of hindrance and acknowledgment

of debilitation misfortune

d. Management’s flexibility for impairment determination

While ASIC does not anticipate that the directors will be specialists accounting they

should look for clarification and counsel supporting the bookkeeping medications picked and,

where proper, challenge the bookkeeping assessments and medicines connected in the

budgetary report. They ought to especially look for exhortation where a treatment does not

mirror their comprehension of the substance of a plan (Bond, Govendir and Wells 2016). Data

ought to be delivered on a convenient premise and be upheld by suitable examination and

documentation for the autonomous review. This will bolster the nature of money related data

in the market and empower reviewers to concentrate on their part in giving free affirmation on

the budgetary report.

It is perceived that the administration of Myer Holdings Ltd is very adaptable in

completing the tests for deciding the asset’s impairment. In addition, the administration

completes survey for the carrying value of the assets for each of the store of the organization

is attempted and distinguished whether sign of any impairment is exists (Kabir and Rahman

2016). According to the prerequisite of AASB 136, they guarantee to do the test for

impedance no less than one in every year Further, the administration decides different

certainties like assurance of the way that whether level without bounds money streams for the

impairment estimation of the advantages for the CGU of Myer. Thus, it is identified that the

company actively manage the test for determination of impairment annually in compliance

with AASB 136.

8ACCOUNTING STANDARDS AND REGULATION

Reference

Amiraslani, H., Iatridis, G.E. and Pope, P.F., 2013. Accounting for asset impairment: a test

for IFRS compliance across Europe. Centre for Financial Analysis and Reporting Research

(CeFARR).

Bond, D., Govendir, B. and Wells, P., 2016. An evaluation of asset impairment decisions by

Australian firms and whether this was impacted by AASB 136.

Gackstatter, T. and Möller, K., 2016. Triggering Events in Asset Impairment Accounting-a

Case Study in the Automotive Industry.

Kabir, H. and Rahman, A., 2016. The role of corporate governance in accounting discretion

under IFRS: Goodwill impairment in Australia. Journal of Contemporary Accounting &

Economics, 12(3), pp.290-308.

Linnenluecke, M.K., Birt, J., Lyon, J. and Sidhu, B.K., 2015. Planetary boundaries:

implications for asset impairment. Accounting & Finance, 55(4), pp.911-929.

Malone, L., Tarca, A. and Wee, M., 2015. Non-GAAP earnings disclosures and

IFRS. Accounting and Finance.

Rennekamp, K., Rupar, K.K. and Seybert, N., 2014. Impaired judgment: The effects of asset

impairment reversibility and cognitive dissonance on future investment. The Accounting

Review, 90(2), pp.739-759.

Zhuang, Z., 2016. Discussion of ‘An evaluation of asset impairments by Australian firms and

whether they were impacted by AASB 136’. Accounting & Finance, 56(1), pp.289-294.

Reference

Amiraslani, H., Iatridis, G.E. and Pope, P.F., 2013. Accounting for asset impairment: a test

for IFRS compliance across Europe. Centre for Financial Analysis and Reporting Research

(CeFARR).

Bond, D., Govendir, B. and Wells, P., 2016. An evaluation of asset impairment decisions by

Australian firms and whether this was impacted by AASB 136.

Gackstatter, T. and Möller, K., 2016. Triggering Events in Asset Impairment Accounting-a

Case Study in the Automotive Industry.

Kabir, H. and Rahman, A., 2016. The role of corporate governance in accounting discretion

under IFRS: Goodwill impairment in Australia. Journal of Contemporary Accounting &

Economics, 12(3), pp.290-308.

Linnenluecke, M.K., Birt, J., Lyon, J. and Sidhu, B.K., 2015. Planetary boundaries:

implications for asset impairment. Accounting & Finance, 55(4), pp.911-929.

Malone, L., Tarca, A. and Wee, M., 2015. Non-GAAP earnings disclosures and

IFRS. Accounting and Finance.

Rennekamp, K., Rupar, K.K. and Seybert, N., 2014. Impaired judgment: The effects of asset

impairment reversibility and cognitive dissonance on future investment. The Accounting

Review, 90(2), pp.739-759.

Zhuang, Z., 2016. Discussion of ‘An evaluation of asset impairments by Australian firms and

whether they were impacted by AASB 136’. Accounting & Finance, 56(1), pp.289-294.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.