HI6026 Audit, Assurance, and Compliance: A Detailed Report

VerifiedAdded on 2023/06/07

|15

|3603

|483

Report

AI Summary

This report provides an analysis of the audit report for Flight Centre Travel Group Limited, focusing on key aspects such as auditor independence, non-audit services, remuneration of the auditor, and the role of the audit committee. The report highlights the auditor's clean opinion, key audit matters including impairment testing and business acquisitions, and the differences in responsibilities between the directors and auditors. The analysis also covers material subsequent events and concludes that the audit report reflects a true and fair view of the company's financial statements in compliance with relevant regulations. Desklib offers a wide range of solved assignments and study resources for students.

HI6026 Audit,

Assurance and

Compliance

Assurance and

Compliance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

EXECUTIVE SUMMARY

Audit and assurance program is very much needed in this complex economic

condition. The report is made on the audit report of company named Flight Centre Travel

Group Limited. The auditors of the company are Ernst & Young. The auditors have issued a

clean report. The various components of the report are highlighted in the coming sections that

represent the efficiency with which the auditor has performed his duties. Explicit and clear

declarations have also been presented in the annual report. These auditors are indulged in

identify the true and fair view of the assets and liabilities shown in the books of account of

company.

Audit and assurance program is very much needed in this complex economic

condition. The report is made on the audit report of company named Flight Centre Travel

Group Limited. The auditors of the company are Ernst & Young. The auditors have issued a

clean report. The various components of the report are highlighted in the coming sections that

represent the efficiency with which the auditor has performed his duties. Explicit and clear

declarations have also been presented in the annual report. These auditors are indulged in

identify the true and fair view of the assets and liabilities shown in the books of account of

company.

Table of Contents

EXECUTIVE SUMMARY........................................................................................................2

INTRODUCTION......................................................................................................................5

CONTENTS...............................................................................................................................5

INDEPENDENCE OF THE AUDITORS AND NON-AUDIT SERVICES.........................5

REMUNERATION OF AUDITOR.......................................................................................6

AUDIT COMMITTEE AND AUDIT CHARTER................................................................8

STRUCTURE.....................................................................................................................8

FUNCTION AND RESPONSIBILITIES..........................................................................8

INDEPENDENT AUDITOR’S REPORT TO STAKEHOLDERS.......................................9

OPINION............................................................................................................................9

KEY AUDIT MATTERS...................................................................................................9

DIFFERENCE OF RESPONSIBILITY...............................................................................10

DIRECTOR’S RESPONSIBILITY..................................................................................10

AUDITOR’S RESPONSIBILITY....................................................................................11

MATERIAL SUBSEQUENT EVENTS..............................................................................11

CONCLUSION........................................................................................................................11

REFERENCES.........................................................................................................................12

EXECUTIVE SUMMARY........................................................................................................2

INTRODUCTION......................................................................................................................5

CONTENTS...............................................................................................................................5

INDEPENDENCE OF THE AUDITORS AND NON-AUDIT SERVICES.........................5

REMUNERATION OF AUDITOR.......................................................................................6

AUDIT COMMITTEE AND AUDIT CHARTER................................................................8

STRUCTURE.....................................................................................................................8

FUNCTION AND RESPONSIBILITIES..........................................................................8

INDEPENDENT AUDITOR’S REPORT TO STAKEHOLDERS.......................................9

OPINION............................................................................................................................9

KEY AUDIT MATTERS...................................................................................................9

DIFFERENCE OF RESPONSIBILITY...............................................................................10

DIRECTOR’S RESPONSIBILITY..................................................................................10

AUDITOR’S RESPONSIBILITY....................................................................................11

MATERIAL SUBSEQUENT EVENTS..............................................................................11

CONCLUSION........................................................................................................................11

REFERENCES.........................................................................................................................12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTRODUCTION

For any successful organisation it is nowadays important to maintain transparency regarding

everything that happens in the entity. All information is required to be transmitted to the

stakeholders through the annual reports. One such information is of the audit function. The

annual report needs to contain every detail regarding the auditors. The contents must include

in clearly stated words the declaration that the auditor gives about his independence, the

remuneration paid to the auditors, any kind of non-audit services if provided by him to the

entity, the formation of any audit committee along with the audit charter, the kind of opinion

that the auditor have expressed, and the key audit matters highlighted by him in the audit

report. All information needs to be expressly included with the management affirmation to

the same. This report will reflects the independence of the auditors and non-audit services,

auditing functioning, responsibilities and material details to bifurcate the key audit matters

and auditor responsibilities of Flight Centre Travel Group Limited. The key auditor matters

have highlighted the audit functions and undertaken audit activities of the auditors (Flight

Centre Travel Group Limited, 2018).

CONTENTS

INDEPENDENCE OF THE AUDITORS AND NON-AUDIT SERVICES

The auditors have expressly provided their independence declaration to the Flight Centre

Travel Group Limited’s management. It clearly states that the auditors have no intention and

have tried not to contravene the regulations laid on them by the Corporations Act 2001 and

the applicable codes of professional conduct as far as their independence is considered. This

declaration is given in their utmost belief and knowledge (Tepalagul, and Lin, 2015). The

auditor’s key functions have reflected the key compliance program which has been given in

the audit report of company. It is analyzed that audit committee appointed in Flight Centre

Travel Group Limited is done to evaluate and analysis the true and fair view of the assets and

libiliteis recorded in the books of accounts (Worth, 2009).

Further, it is mentioned explicitly in the annual report that the Flight Centre Travel Group

Limited has tried to exploit fully the potential that the auditors have. This is done by getting

professional aid from the auditors on certain non-audit matters also. For the concern of

auditor independence, it is believed to the satisfaction of the audit and risk committee that the

For any successful organisation it is nowadays important to maintain transparency regarding

everything that happens in the entity. All information is required to be transmitted to the

stakeholders through the annual reports. One such information is of the audit function. The

annual report needs to contain every detail regarding the auditors. The contents must include

in clearly stated words the declaration that the auditor gives about his independence, the

remuneration paid to the auditors, any kind of non-audit services if provided by him to the

entity, the formation of any audit committee along with the audit charter, the kind of opinion

that the auditor have expressed, and the key audit matters highlighted by him in the audit

report. All information needs to be expressly included with the management affirmation to

the same. This report will reflects the independence of the auditors and non-audit services,

auditing functioning, responsibilities and material details to bifurcate the key audit matters

and auditor responsibilities of Flight Centre Travel Group Limited. The key auditor matters

have highlighted the audit functions and undertaken audit activities of the auditors (Flight

Centre Travel Group Limited, 2018).

CONTENTS

INDEPENDENCE OF THE AUDITORS AND NON-AUDIT SERVICES

The auditors have expressly provided their independence declaration to the Flight Centre

Travel Group Limited’s management. It clearly states that the auditors have no intention and

have tried not to contravene the regulations laid on them by the Corporations Act 2001 and

the applicable codes of professional conduct as far as their independence is considered. This

declaration is given in their utmost belief and knowledge (Tepalagul, and Lin, 2015). The

auditor’s key functions have reflected the key compliance program which has been given in

the audit report of company. It is analyzed that audit committee appointed in Flight Centre

Travel Group Limited is done to evaluate and analysis the true and fair view of the assets and

libiliteis recorded in the books of accounts (Worth, 2009).

Further, it is mentioned explicitly in the annual report that the Flight Centre Travel Group

Limited has tried to exploit fully the potential that the auditors have. This is done by getting

professional aid from the auditors on certain non-audit matters also. For the concern of

auditor independence, it is believed to the satisfaction of the audit and risk committee that the

provision of such services had not left any impact on the independence of the auditor (Wu,

Hsu, and Haslam, 2016). The tax compliance program and audit functions are undertaken to

analysis how well auditors have performed to explicit the fairness of the recorded details. The

non-audit services are provided in compliance with the principles that the APES 110 Code of

Ethics for Professional Accountants have set in relation to auditor’s independence. However,

the list of non-audit services provided is set out below (O'Donnell, Arnold, and Sutton, 2010).

Tax compliance, and

Other services (Bell, Causholli, and Knechel, 2015).

Nature of the non-audit services

These non-audit services provide by the auditors are of revenue nature.

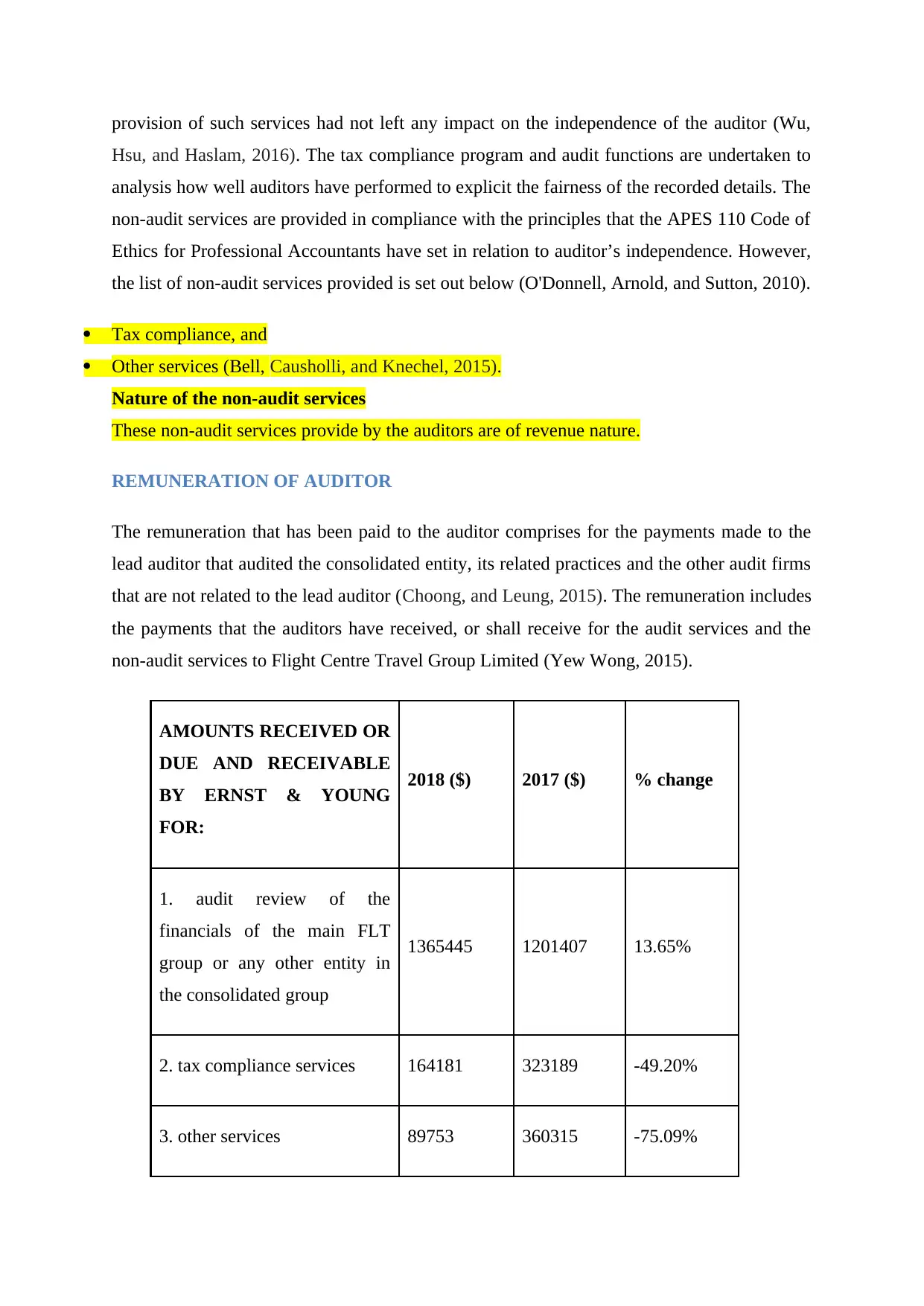

REMUNERATION OF AUDITOR

The remuneration that has been paid to the auditor comprises for the payments made to the

lead auditor that audited the consolidated entity, its related practices and the other audit firms

that are not related to the lead auditor (Choong, and Leung, 2015). The remuneration includes

the payments that the auditors have received, or shall receive for the audit services and the

non-audit services to Flight Centre Travel Group Limited (Yew Wong, 2015).

AMOUNTS RECEIVED OR

DUE AND RECEIVABLE

BY ERNST & YOUNG

FOR:

2018 ($) 2017 ($) % change

1. audit review of the

financials of the main FLT

group or any other entity in

the consolidated group

1365445 1201407 13.65%

2. tax compliance services 164181 323189 -49.20%

3. other services 89753 360315 -75.09%

Hsu, and Haslam, 2016). The tax compliance program and audit functions are undertaken to

analysis how well auditors have performed to explicit the fairness of the recorded details. The

non-audit services are provided in compliance with the principles that the APES 110 Code of

Ethics for Professional Accountants have set in relation to auditor’s independence. However,

the list of non-audit services provided is set out below (O'Donnell, Arnold, and Sutton, 2010).

Tax compliance, and

Other services (Bell, Causholli, and Knechel, 2015).

Nature of the non-audit services

These non-audit services provide by the auditors are of revenue nature.

REMUNERATION OF AUDITOR

The remuneration that has been paid to the auditor comprises for the payments made to the

lead auditor that audited the consolidated entity, its related practices and the other audit firms

that are not related to the lead auditor (Choong, and Leung, 2015). The remuneration includes

the payments that the auditors have received, or shall receive for the audit services and the

non-audit services to Flight Centre Travel Group Limited (Yew Wong, 2015).

AMOUNTS RECEIVED OR

DUE AND RECEIVABLE

BY ERNST & YOUNG

FOR:

2018 ($) 2017 ($) % change

1. audit review of the

financials of the main FLT

group or any other entity in

the consolidated group

1365445 1201407 13.65%

2. tax compliance services 164181 323189 -49.20%

3. other services 89753 360315 -75.09%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Total 1619379 1884911 -14.09%

AMOUNTS RECEIVED OR

DUE AND RECEIVABLE

BY RELATED

PRACTICES OF ERNST &

YOUNG FOR:

2018 ($) 2017 ($) % change

1. audit review of the

financials of the main FLT

group or any other entity in

the consolidated group (Flight

Centre Travel Group Limited,

2018).

1386642 1459041 -4.96%

2. tax compliance services 195187 226128 -13.68%

3. Special audit by regulators 39147 20050 95.25%

4. other services 66035 20308 225.17%

Total 1687011 1725527 -2.23%

AMOUNTS RECEIVED OR

DUE AND RECEIVABLE

BY NON LEAD AUDIT

FIRMS

2018 ($) 2017 ($) % change

AMOUNTS RECEIVED OR

DUE AND RECEIVABLE

BY RELATED

PRACTICES OF ERNST &

YOUNG FOR:

2018 ($) 2017 ($) % change

1. audit review of the

financials of the main FLT

group or any other entity in

the consolidated group (Flight

Centre Travel Group Limited,

2018).

1386642 1459041 -4.96%

2. tax compliance services 195187 226128 -13.68%

3. Special audit by regulators 39147 20050 95.25%

4. other services 66035 20308 225.17%

Total 1687011 1725527 -2.23%

AMOUNTS RECEIVED OR

DUE AND RECEIVABLE

BY NON LEAD AUDIT

FIRMS

2018 ($) 2017 ($) % change

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

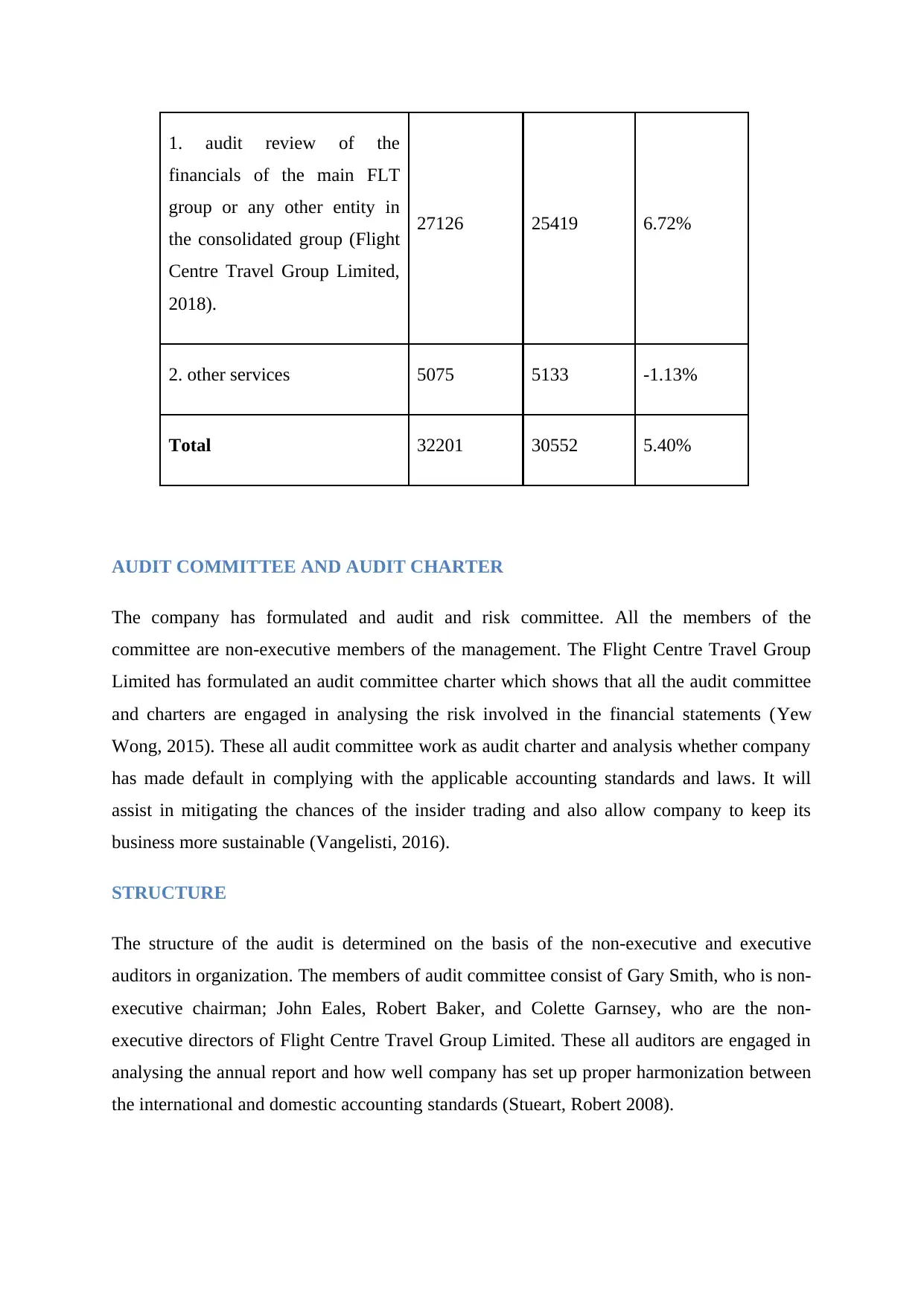

1. audit review of the

financials of the main FLT

group or any other entity in

the consolidated group (Flight

Centre Travel Group Limited,

2018).

27126 25419 6.72%

2. other services 5075 5133 -1.13%

Total 32201 30552 5.40%

AUDIT COMMITTEE AND AUDIT CHARTER

The company has formulated and audit and risk committee. All the members of the

committee are non-executive members of the management. The Flight Centre Travel Group

Limited has formulated an audit committee charter which shows that all the audit committee

and charters are engaged in analysing the risk involved in the financial statements (Yew

Wong, 2015). These all audit committee work as audit charter and analysis whether company

has made default in complying with the applicable accounting standards and laws. It will

assist in mitigating the chances of the insider trading and also allow company to keep its

business more sustainable (Vangelisti, 2016).

STRUCTURE

The structure of the audit is determined on the basis of the non-executive and executive

auditors in organization. The members of audit committee consist of Gary Smith, who is non-

executive chairman; John Eales, Robert Baker, and Colette Garnsey, who are the non-

executive directors of Flight Centre Travel Group Limited. These all auditors are engaged in

analysing the annual report and how well company has set up proper harmonization between

the international and domestic accounting standards (Stueart, Robert 2008).

financials of the main FLT

group or any other entity in

the consolidated group (Flight

Centre Travel Group Limited,

2018).

27126 25419 6.72%

2. other services 5075 5133 -1.13%

Total 32201 30552 5.40%

AUDIT COMMITTEE AND AUDIT CHARTER

The company has formulated and audit and risk committee. All the members of the

committee are non-executive members of the management. The Flight Centre Travel Group

Limited has formulated an audit committee charter which shows that all the audit committee

and charters are engaged in analysing the risk involved in the financial statements (Yew

Wong, 2015). These all audit committee work as audit charter and analysis whether company

has made default in complying with the applicable accounting standards and laws. It will

assist in mitigating the chances of the insider trading and also allow company to keep its

business more sustainable (Vangelisti, 2016).

STRUCTURE

The structure of the audit is determined on the basis of the non-executive and executive

auditors in organization. The members of audit committee consist of Gary Smith, who is non-

executive chairman; John Eales, Robert Baker, and Colette Garnsey, who are the non-

executive directors of Flight Centre Travel Group Limited. These all auditors are engaged in

analysing the annual report and how well company has set up proper harmonization between

the international and domestic accounting standards (Stueart, Robert 2008).

FUNCTION AND RESPONSIBILITIES

To review and provide recommendations in order to make the corporate reporting of the

entity acceptable by the applicable framework.

To analysis whether the directors and key managerial persons are providing proper

managerial representation letters in its books of accounts.

To recommend, appoint and remove the independent auditors from the undertaken work and

audit program (Bradbury, 2017).

To analysis the fairness of booked assets and liabilities

To identify and evaluate the carrying value of the values.

To review the financial statements of the entity to gather an understanding of whether the

requirement of compliance with the true and fair view is reflected in them (He, et. al 2017).

Reviewing the appropriateness of the various accounting judgements, estimates and policies

used by the entity in preparation of the financial statements (He, Pittman, Rui, and Wu,

(2017).

To recommend and decide on the appointment, remuneration, and removal of the external

and independent auditor (Flight Centre Travel Group Limited, 2018).

To manage the internal audit function by deciding the head of the same and assessing his

capabilities to lead the internal audit team.

To look into the efficiency with which the appraisal of the financial statements is being

carried out by the external auditor.

To bring into knowledge of the entity the relevant updates brought in the financial reporting

requirements and help in complying with the recent and important changes taken place in the

field of it.

To assess whether the external auditors are complying with the requirement of the

independence expected out of them and the ways in which they are dealing with the provision

of non-audit services (Novitaningrum, and Amboningtyas, 2017).

To act as fiduciary person for the stakeholders so that they could give transprent details of the

financial statement of company.

Auditors are also providing non-audit services such as insurance coverage details,

computation and analysis of the accounts and assisting accountants to comply with the

international and domestic financial reporting standards.

To review and provide recommendations in order to make the corporate reporting of the

entity acceptable by the applicable framework.

To analysis whether the directors and key managerial persons are providing proper

managerial representation letters in its books of accounts.

To recommend, appoint and remove the independent auditors from the undertaken work and

audit program (Bradbury, 2017).

To analysis the fairness of booked assets and liabilities

To identify and evaluate the carrying value of the values.

To review the financial statements of the entity to gather an understanding of whether the

requirement of compliance with the true and fair view is reflected in them (He, et. al 2017).

Reviewing the appropriateness of the various accounting judgements, estimates and policies

used by the entity in preparation of the financial statements (He, Pittman, Rui, and Wu,

(2017).

To recommend and decide on the appointment, remuneration, and removal of the external

and independent auditor (Flight Centre Travel Group Limited, 2018).

To manage the internal audit function by deciding the head of the same and assessing his

capabilities to lead the internal audit team.

To look into the efficiency with which the appraisal of the financial statements is being

carried out by the external auditor.

To bring into knowledge of the entity the relevant updates brought in the financial reporting

requirements and help in complying with the recent and important changes taken place in the

field of it.

To assess whether the external auditors are complying with the requirement of the

independence expected out of them and the ways in which they are dealing with the provision

of non-audit services (Novitaningrum, and Amboningtyas, 2017).

To act as fiduciary person for the stakeholders so that they could give transprent details of the

financial statement of company.

Auditors are also providing non-audit services such as insurance coverage details,

computation and analysis of the accounts and assisting accountants to comply with the

international and domestic financial reporting standards.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INDEPENDENT AUDITOR’S REPORT TO STAKEHOLDERS

OPINION

The auditors of the entity have expressed an unmodified opinion or a clean opinion on the

financial statements of Flight Centre Travel Group Limited. In their opinion and according to

the audit procedures performed by them, the financial statements are made in compliance

with the provisions of the Corporations Act 2001. The regulations provided by the Australian

Accounting Standards and the Corporations Regulations 2001 are also being followed. There

are no visible material misstatements that came to the knowledge of the auditor from the

procedures that he has performed. Further, the auditors have stated that they have completely

embraced the independence requirement expected out of them throughout the audit.

Moreover, they have mentioned in the audit report itself that the ethical requirements laid by

the APES 110 Code of Ethics for Professional Accountants have also been complied with.

The auditor’s opinion reflects that Flight Centre Travel Group Limited has complied all the

applicable rules and made complete disclosure in its financial statement (Flight Centre Travel

Group Limited, 2018). It is further analysed that non-qualified audit report given by auditors

helps stakeholders to determine that all the information shown by the Flight Centre Travel

Group Limited in its financial report reflects eh true and fair view of the assets and liabilities.

This audit opinion given by the auditors is very much required for the stakeholders to take

their financial investment decision. It will assist in boosting their confidence on the annual

report and financial statements shared by the auditors (Flight Centre Travel Group Limited,

2018).

KEY AUDIT MATTERS

The key audit matters do not cast any modification on the financial statements of the entity.

They are just the areas which concern the auditors as professionals and they wish to further

inform the stakeholders regarding the same (Cordoş, and Fülöp, 2015). From the annual

report of the entity, the following key audit matters can be identified which helps in analysing

the key performance of the auditors and fairness of the financial statement shared by the

company.

IMPAIRMENT TESTING OF GOODWILL AND OTHER INTANGIBLE ASSETS

OPINION

The auditors of the entity have expressed an unmodified opinion or a clean opinion on the

financial statements of Flight Centre Travel Group Limited. In their opinion and according to

the audit procedures performed by them, the financial statements are made in compliance

with the provisions of the Corporations Act 2001. The regulations provided by the Australian

Accounting Standards and the Corporations Regulations 2001 are also being followed. There

are no visible material misstatements that came to the knowledge of the auditor from the

procedures that he has performed. Further, the auditors have stated that they have completely

embraced the independence requirement expected out of them throughout the audit.

Moreover, they have mentioned in the audit report itself that the ethical requirements laid by

the APES 110 Code of Ethics for Professional Accountants have also been complied with.

The auditor’s opinion reflects that Flight Centre Travel Group Limited has complied all the

applicable rules and made complete disclosure in its financial statement (Flight Centre Travel

Group Limited, 2018). It is further analysed that non-qualified audit report given by auditors

helps stakeholders to determine that all the information shown by the Flight Centre Travel

Group Limited in its financial report reflects eh true and fair view of the assets and liabilities.

This audit opinion given by the auditors is very much required for the stakeholders to take

their financial investment decision. It will assist in boosting their confidence on the annual

report and financial statements shared by the auditors (Flight Centre Travel Group Limited,

2018).

KEY AUDIT MATTERS

The key audit matters do not cast any modification on the financial statements of the entity.

They are just the areas which concern the auditors as professionals and they wish to further

inform the stakeholders regarding the same (Cordoş, and Fülöp, 2015). From the annual

report of the entity, the following key audit matters can be identified which helps in analysing

the key performance of the auditors and fairness of the financial statement shared by the

company.

IMPAIRMENT TESTING OF GOODWILL AND OTHER INTANGIBLE ASSETS

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

This is a key audit matter in the judgement of auditor because of the huge balance of the

impairment amount in relation to the total assets. Further lot estimation is also involved in the

same

AUDIT PROCEDURE: The requirements of AASB 136, Impairment of Assets are

considered. Valuation specialist is being called to determine the accuracy of the valuation and

the cash flow statement is also assessed to determine the level of accuracy with which the

forecasts and the assumptions are being made.

o The audit procedure followed can be brought in the category of the test of control.

BUSINESS ACQUISITIONS

The huge number of the business acquisitions and the combinations entered into by the entity

has made this a key audit matter (Flight Centre Travel Group Limited, 2018).

AUDIT PROCEDURE: the audit procedure included the assessment of the procedure that the

entity has followed along with the compliance of the applicable accounting standard. The

adequacy of valuation is also checked (Flight Centre Travel Group Limited, 2018).

o This audit procedure can be called as the test of control.

o The test control has been undertaken to determine the fair value of the recorded assets and

liabilities in the books of accounts.

o The impairment test is also assessed by the auditors to help accountant to determine the true

and fair view of the assets and liabilities in the books of accounts (Flight Centre Travel Group

Limited, 2018).

RECOVERABILTIY OF OVERRIDE RECEIVABLE

Certain factors related to this account that are beyond the control of the Flight Centre Travel

Group Limited have made it a matter of key concern.

AUDIT PROCEDURE: This included verification of the receipts in this account, sampling

technique to examine certain override contracts, and observation of the calculation

methodology of override receivable amounts.

o These audit procedures fall under the purview of test of control and substantive test of details.

However, impairment test and assertion test have been implemented by organization to

determine the carrying value of its recorded assets in the books of accounts.

impairment amount in relation to the total assets. Further lot estimation is also involved in the

same

AUDIT PROCEDURE: The requirements of AASB 136, Impairment of Assets are

considered. Valuation specialist is being called to determine the accuracy of the valuation and

the cash flow statement is also assessed to determine the level of accuracy with which the

forecasts and the assumptions are being made.

o The audit procedure followed can be brought in the category of the test of control.

BUSINESS ACQUISITIONS

The huge number of the business acquisitions and the combinations entered into by the entity

has made this a key audit matter (Flight Centre Travel Group Limited, 2018).

AUDIT PROCEDURE: the audit procedure included the assessment of the procedure that the

entity has followed along with the compliance of the applicable accounting standard. The

adequacy of valuation is also checked (Flight Centre Travel Group Limited, 2018).

o This audit procedure can be called as the test of control.

o The test control has been undertaken to determine the fair value of the recorded assets and

liabilities in the books of accounts.

o The impairment test is also assessed by the auditors to help accountant to determine the true

and fair view of the assets and liabilities in the books of accounts (Flight Centre Travel Group

Limited, 2018).

RECOVERABILTIY OF OVERRIDE RECEIVABLE

Certain factors related to this account that are beyond the control of the Flight Centre Travel

Group Limited have made it a matter of key concern.

AUDIT PROCEDURE: This included verification of the receipts in this account, sampling

technique to examine certain override contracts, and observation of the calculation

methodology of override receivable amounts.

o These audit procedures fall under the purview of test of control and substantive test of details.

However, impairment test and assertion test have been implemented by organization to

determine the carrying value of its recorded assets in the books of accounts.

DIFFERENCE OF RESPONSIBILITY BETWEEN THE DIRECTORS AND

AUDITORS

DIRECTOR’S RESPONSIBILITY

The preparation of the financial statements and following the requirements of the

corporation’s act 2001 and the accounting standards in such preparation is the duty of the

directors. Further they are the responsible party for assessing the ability of the consolidated

group as a going concern (Shaukat, Qiu, and Trojanowski , 2016). The director’s

responsibilities show the extent to which they will be liable if in case company fails to

comply with the applicable laws and accounting standards (Mock, Ragothaman, and

Srivastava, 2018).

AUDITOR’S RESPONSIBILITY

The auditor’s responsibility is limited to do an appraisal of the financials prepared by the

entity and the internal controls existing in the entity to provide a reasonable assurance on the

same. The assurance relates to the presentation of financials in accordance with the applicable

standards and regulations. Nonetheless, if in case they will to identify the discrepancies and

issues in the financial statement shared with them then they will be held liable for the same.

Until and unless, auditors are given management representation letter with then only they will

have to analysis financial details by documenting and doing the personal visit with the

company. It will assists in confirming the right value of the recorded assets and liabilities in

the books of accounts of company. it includes any kind of non-audit services if provided by

auditors to the entity, the formation of any audit committee along with the audit charter, the

kind of opinion that the auditor have expressed, and the key audit matters highlighted by him

in the audit report (Flight Centre Travel Group Limited, 2018).

MATERIAL SUBSEQUENT EVENTS

The material subsequent events include the dividend declaration and the acquisitions made

subsequent to year end. They have been treated as per the regulations and comply well with

the requirements (Knechel, and Salterio, 2016). It has also increased the transparency of the

details recorded in the books of account of Flight Centre Travel Group Limited. The main

material details reflects how well company has complied with the applicable rules and

AUDITORS

DIRECTOR’S RESPONSIBILITY

The preparation of the financial statements and following the requirements of the

corporation’s act 2001 and the accounting standards in such preparation is the duty of the

directors. Further they are the responsible party for assessing the ability of the consolidated

group as a going concern (Shaukat, Qiu, and Trojanowski , 2016). The director’s

responsibilities show the extent to which they will be liable if in case company fails to

comply with the applicable laws and accounting standards (Mock, Ragothaman, and

Srivastava, 2018).

AUDITOR’S RESPONSIBILITY

The auditor’s responsibility is limited to do an appraisal of the financials prepared by the

entity and the internal controls existing in the entity to provide a reasonable assurance on the

same. The assurance relates to the presentation of financials in accordance with the applicable

standards and regulations. Nonetheless, if in case they will to identify the discrepancies and

issues in the financial statement shared with them then they will be held liable for the same.

Until and unless, auditors are given management representation letter with then only they will

have to analysis financial details by documenting and doing the personal visit with the

company. It will assists in confirming the right value of the recorded assets and liabilities in

the books of accounts of company. it includes any kind of non-audit services if provided by

auditors to the entity, the formation of any audit committee along with the audit charter, the

kind of opinion that the auditor have expressed, and the key audit matters highlighted by him

in the audit report (Flight Centre Travel Group Limited, 2018).

MATERIAL SUBSEQUENT EVENTS

The material subsequent events include the dividend declaration and the acquisitions made

subsequent to year end. They have been treated as per the regulations and comply well with

the requirements (Knechel, and Salterio, 2016). It has also increased the transparency of the

details recorded in the books of account of Flight Centre Travel Group Limited. The main

material details reflects how well company has complied with the applicable rules and

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.