Comprehensive Valuation Report: Flight Centre Travel Group Limited

VerifiedAdded on 2023/05/31

|29

|6365

|232

Report

AI Summary

This report evaluates the financial performance of Flight Centre Travel Group Limited (FLT), an Australian public listed company, within the context of the Australian airline industry. It examines the company's share price performance, recent and overtime financial results, and current macroeconomic and microeconomic factors affecting its performance. A peer comparison with Helloworld Travel Limited, Webjet Limited, and Corporate Travel Management Ltd is conducted, alongside a Du Pont analysis to assess profitability. The report further includes a valuation analysis using the Capital Asset Pricing Model (CAPM) and Dividend Discount Model (DDM) to determine the intrinsic value of FLT shares and compares it to the market value, followed by a sensitivity and scenario analysis to provide a comprehensive overview of the company's financial standing and future prospects.

Running head: COMPANY VALUATION

Company Valuation

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Company Valuation

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1COMPANY VALUATION

Executive Summary:

The current report is prepared with the intent to evaluate the financial performance of a public

listed company in Australia. The organisation selected for meeting the purpose of this report is

Flight Centre Travel Group Limited (FLT). The airline industry of Australia has experienced a

steady growth over the past five years. However, the fuel prices have increased drastically over

the years after the global economic recession and as a result, the airfares have increased

considerably. By comparing with the major competitors of the organisation, it has been found out

that Helloworld Travel Limited is placed in a favourable position in the Australian aviation

industry followed by Webjet Limited and Flight Centre Travel Group Limited. The assessment

would also be showing valuation of the business for which computation of Beta and required rate

of return is also shown. The assessment also includes Dividend Discount Model analysis for the

purpose of computing the intrinsic value of the business and make comparison of the same with

the market value of the shares of Flight Centre Travel Group Limited (FLT).

Executive Summary:

The current report is prepared with the intent to evaluate the financial performance of a public

listed company in Australia. The organisation selected for meeting the purpose of this report is

Flight Centre Travel Group Limited (FLT). The airline industry of Australia has experienced a

steady growth over the past five years. However, the fuel prices have increased drastically over

the years after the global economic recession and as a result, the airfares have increased

considerably. By comparing with the major competitors of the organisation, it has been found out

that Helloworld Travel Limited is placed in a favourable position in the Australian aviation

industry followed by Webjet Limited and Flight Centre Travel Group Limited. The assessment

would also be showing valuation of the business for which computation of Beta and required rate

of return is also shown. The assessment also includes Dividend Discount Model analysis for the

purpose of computing the intrinsic value of the business and make comparison of the same with

the market value of the shares of Flight Centre Travel Group Limited (FLT).

2COMPANY VALUATION

Table of Contents

Part 1................................................................................................................................................3

1.0 Introduction:..........................................................................................................................3

2.0 Recent Financial Performance:..............................................................................................4

3.0 Overtime Financial Performance:..........................................................................................5

4.0 Current Issues:.......................................................................................................................6

4.1 Macroeconomic Factors:.......................................................................................................6

4.2 Microeconomic Factors:........................................................................................................7

5.0 Peer Comparison:...................................................................................................................8

6.1 Du Pont Analysis:................................................................................................................11

Part 2..............................................................................................................................................16

Valuation Analysis of CAPM Approach...................................................................................16

Dividend Discount Model..........................................................................................................18

Difference Between Intrinsic Value and Market Value............................................................20

Appropriateness of Dividend Discount Model..........................................................................21

Sensitivity and Scenario Analysis.............................................................................................22

References:....................................................................................................................................24

Table of Contents

Part 1................................................................................................................................................3

1.0 Introduction:..........................................................................................................................3

2.0 Recent Financial Performance:..............................................................................................4

3.0 Overtime Financial Performance:..........................................................................................5

4.0 Current Issues:.......................................................................................................................6

4.1 Macroeconomic Factors:.......................................................................................................6

4.2 Microeconomic Factors:........................................................................................................7

5.0 Peer Comparison:...................................................................................................................8

6.1 Du Pont Analysis:................................................................................................................11

Part 2..............................................................................................................................................16

Valuation Analysis of CAPM Approach...................................................................................16

Dividend Discount Model..........................................................................................................18

Difference Between Intrinsic Value and Market Value............................................................20

Appropriateness of Dividend Discount Model..........................................................................21

Sensitivity and Scenario Analysis.............................................................................................22

References:....................................................................................................................................24

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3COMPANY VALUATION

Part 1

1.0 Introduction:

The current report is prepared with the intent to evaluate the financial performance of a

public listed company in Australia. The organisation selected for meeting the purpose of this

report is Flight Centre Travel Group Limited (FLT), which is involved in providing retailing and

travel services for corporate, leisure and wholesale travel sectors in Australia, New Zealand,

Africa, USA, Asia and Europe (Flight Centre Travel Group, 2018). Therefore, for evaluating the

financial performance of the organisation, the analyses considered include share price analysis,

ratio analysis and stock price valuation using the dividend discount model.

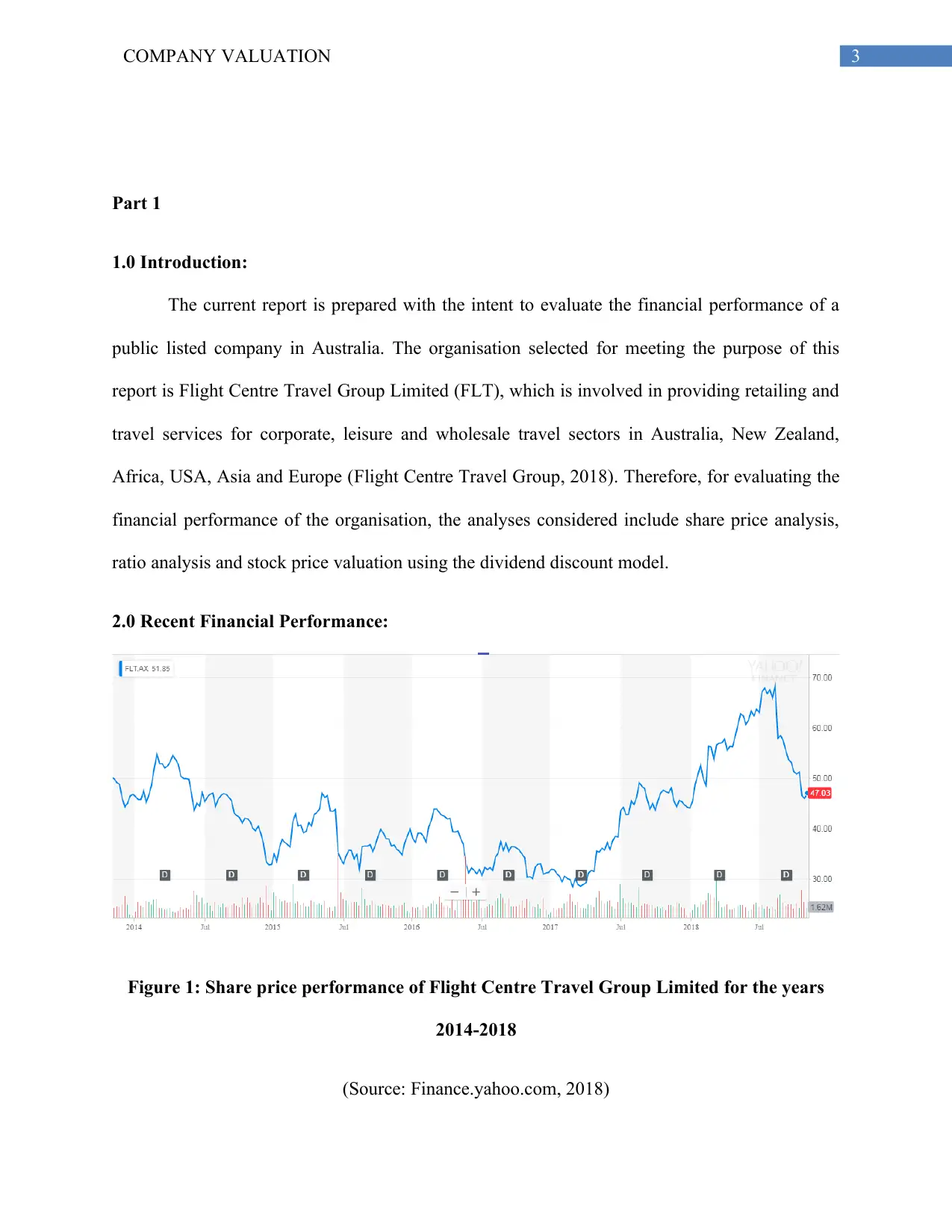

2.0 Recent Financial Performance:

Figure 1: Share price performance of Flight Centre Travel Group Limited for the years

2014-2018

(Source: Finance.yahoo.com, 2018)

Part 1

1.0 Introduction:

The current report is prepared with the intent to evaluate the financial performance of a

public listed company in Australia. The organisation selected for meeting the purpose of this

report is Flight Centre Travel Group Limited (FLT), which is involved in providing retailing and

travel services for corporate, leisure and wholesale travel sectors in Australia, New Zealand,

Africa, USA, Asia and Europe (Flight Centre Travel Group, 2018). Therefore, for evaluating the

financial performance of the organisation, the analyses considered include share price analysis,

ratio analysis and stock price valuation using the dividend discount model.

2.0 Recent Financial Performance:

Figure 1: Share price performance of Flight Centre Travel Group Limited for the years

2014-2018

(Source: Finance.yahoo.com, 2018)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4COMPANY VALUATION

From the above figure, it is evident that the share price of the organisation has started to

decline from 2014 until the first quarter of 2015 and fluctuating trend could be observed over the

years as well. From June to August in the year 2018, the insiders of the organisation have sold

more shares. The individual insiders own 29.84 million shares in the business, which constitute

of 29.52% of the overall number of outstanding shares (Howe, 2018). According to the earnings

expectations of the analysts, an increase of 30.67% is estimated over the next three years and

thus, this denotes a strong outlook for Flight Centre Travel Group Limited. However, this has not

been consistent with the signal that is sent by the company insiders with their net selling activity.

In case of line items, the organisation would experience restrained top-line growth level

over the upcoming year; however, a strong growth in earnings is expected to 10.88% as well.

This might due to sound cost minimisation initiatives that the organisation has undertaken for

driving greater earnings. However, this practice might not be feasible for the long-term and this

might prompt the insiders in reconsidering their shareholdings (Misund, Osmundsen &

Sikveland, 2015). In opposition, they might perceive that the stock has been overvalued by the

market in order to depict favourable selling environment. Moreover, it has been evaluated that

Flight Centre Travel Group Limited has acquired Unmapped, a technology-based organisation in

Canada, on 21st September 2018, due to which decline in stock price could be observed in the

third quarter of 2018.

From the above figure, it is evident that the share price of the organisation has started to

decline from 2014 until the first quarter of 2015 and fluctuating trend could be observed over the

years as well. From June to August in the year 2018, the insiders of the organisation have sold

more shares. The individual insiders own 29.84 million shares in the business, which constitute

of 29.52% of the overall number of outstanding shares (Howe, 2018). According to the earnings

expectations of the analysts, an increase of 30.67% is estimated over the next three years and

thus, this denotes a strong outlook for Flight Centre Travel Group Limited. However, this has not

been consistent with the signal that is sent by the company insiders with their net selling activity.

In case of line items, the organisation would experience restrained top-line growth level

over the upcoming year; however, a strong growth in earnings is expected to 10.88% as well.

This might due to sound cost minimisation initiatives that the organisation has undertaken for

driving greater earnings. However, this practice might not be feasible for the long-term and this

might prompt the insiders in reconsidering their shareholdings (Misund, Osmundsen &

Sikveland, 2015). In opposition, they might perceive that the stock has been overvalued by the

market in order to depict favourable selling environment. Moreover, it has been evaluated that

Flight Centre Travel Group Limited has acquired Unmapped, a technology-based organisation in

Canada, on 21st September 2018, due to which decline in stock price could be observed in the

third quarter of 2018.

5COMPANY VALUATION

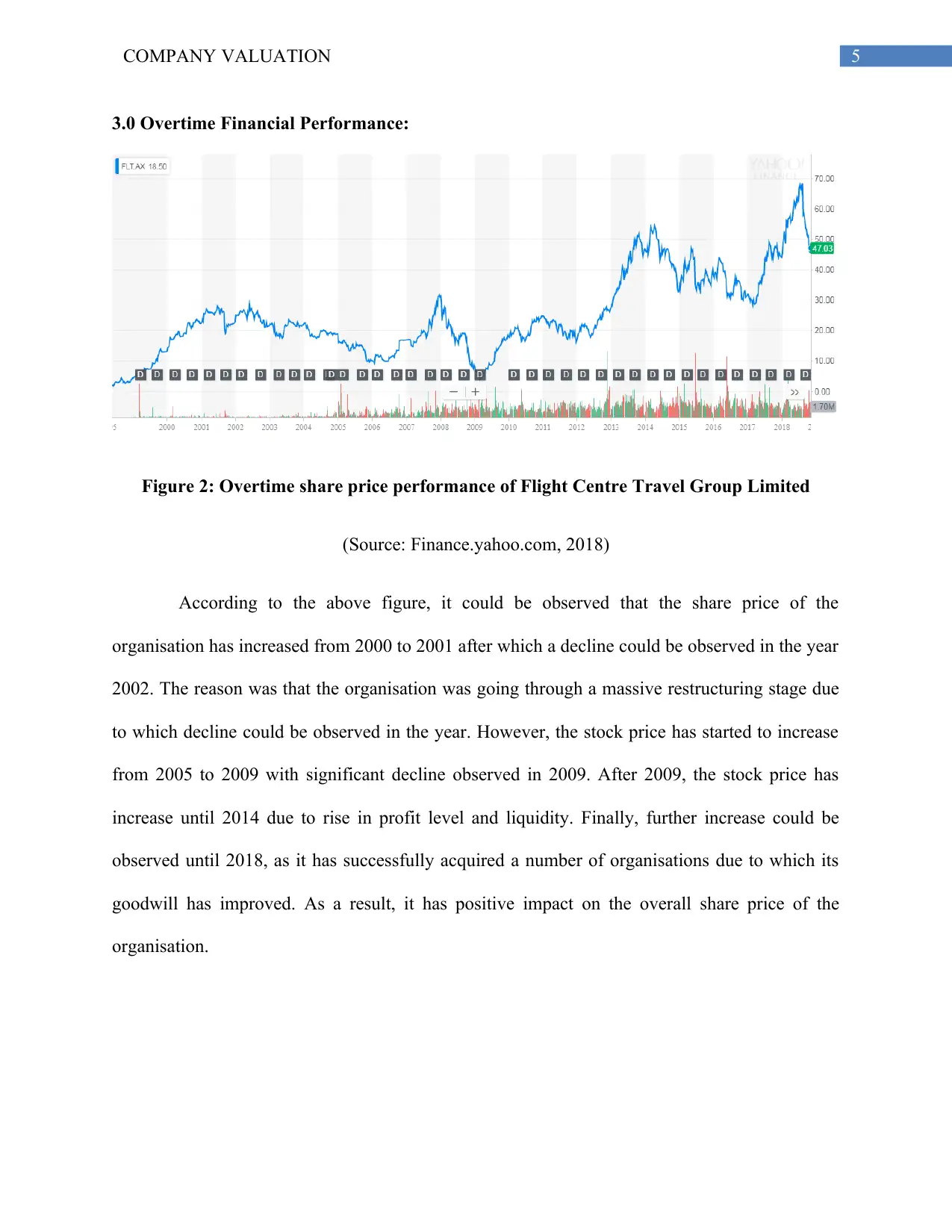

3.0 Overtime Financial Performance:

Figure 2: Overtime share price performance of Flight Centre Travel Group Limited

(Source: Finance.yahoo.com, 2018)

According to the above figure, it could be observed that the share price of the

organisation has increased from 2000 to 2001 after which a decline could be observed in the year

2002. The reason was that the organisation was going through a massive restructuring stage due

to which decline could be observed in the year. However, the stock price has started to increase

from 2005 to 2009 with significant decline observed in 2009. After 2009, the stock price has

increase until 2014 due to rise in profit level and liquidity. Finally, further increase could be

observed until 2018, as it has successfully acquired a number of organisations due to which its

goodwill has improved. As a result, it has positive impact on the overall share price of the

organisation.

3.0 Overtime Financial Performance:

Figure 2: Overtime share price performance of Flight Centre Travel Group Limited

(Source: Finance.yahoo.com, 2018)

According to the above figure, it could be observed that the share price of the

organisation has increased from 2000 to 2001 after which a decline could be observed in the year

2002. The reason was that the organisation was going through a massive restructuring stage due

to which decline could be observed in the year. However, the stock price has started to increase

from 2005 to 2009 with significant decline observed in 2009. After 2009, the stock price has

increase until 2014 due to rise in profit level and liquidity. Finally, further increase could be

observed until 2018, as it has successfully acquired a number of organisations due to which its

goodwill has improved. As a result, it has positive impact on the overall share price of the

organisation.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6COMPANY VALUATION

4.0 Current Issues:

4.1 Macroeconomic Factors:

There are certain macroeconomic factors that have direct impact on the financial

performance of Flight Centre Travel Group Limited and they are demonstrated briefly as

follows:

Individual income:

The social trends and conditions as inherent with respect to the airline sector have impact

on the performance of the organisation greatly. An evaluation of the Australian airline sector

indicates that the social trends have affected the same. This suggests that there has been greater

level of acceptance of low cost air travelling services within the customers (Brigham et al.,

2016). This is mainly due to the fact that there has been reduction in the purchasing power of the

consumers towards leisure services because of fall in income level. This has affected the airlines

like Flight Centre Travel Group Limited providing premium class air travelling services.

Growth of the industry:

The airline industry of Australia has experienced a steady growth over the past five years.

However, the fuel prices have increased drastically over the years after the global economic

recession and as a result, the airfares have increased considerably. The low income, increased

levels of unemployment and unavoidable disasters such as ash cloud have minimised the overall

air travel demand in Australia.

Government regulation:

4.0 Current Issues:

4.1 Macroeconomic Factors:

There are certain macroeconomic factors that have direct impact on the financial

performance of Flight Centre Travel Group Limited and they are demonstrated briefly as

follows:

Individual income:

The social trends and conditions as inherent with respect to the airline sector have impact

on the performance of the organisation greatly. An evaluation of the Australian airline sector

indicates that the social trends have affected the same. This suggests that there has been greater

level of acceptance of low cost air travelling services within the customers (Brigham et al.,

2016). This is mainly due to the fact that there has been reduction in the purchasing power of the

consumers towards leisure services because of fall in income level. This has affected the airlines

like Flight Centre Travel Group Limited providing premium class air travelling services.

Growth of the industry:

The airline industry of Australia has experienced a steady growth over the past five years.

However, the fuel prices have increased drastically over the years after the global economic

recession and as a result, the airfares have increased considerably. The low income, increased

levels of unemployment and unavoidable disasters such as ash cloud have minimised the overall

air travel demand in Australia.

Government regulation:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7COMPANY VALUATION

The Australian airline industry has been deregulated and this deregulation has eliminated

the barriers for the new organisations to tap into the airline market of the nation (Collewaert &

Manigart, 2016). This has direct effect on organisations like Flight Centre Travel Group Limited,

as they are old market players and they would be affected significantly by this regulation. The

preference of the travellers keeps on varying over the years from one airline to another; however,

with the value of money, the selection of individuals for travelling through air has risen.

4.2 Microeconomic Factors:

There are certain microeconomic factors those are deemed to impact the financial

performance of Flight Centre Travel Group and these are explained under:

Operation

The current business operations of Flight Centre Travel Group are focussed on

positioning itself as leader in air travel business through expanding its online presence through

rolling out flagship stores. The company’s Australian operations is observed to improve and

attain increased profits. Moreover, majority of its operations is carried out offline with physical

stores to attain 95% sales in the current year along with that its online operations will contribute

to 5% growth in its sales (Penman, 2015).

Level of Debt

The level of debt for Flight Centre Travel Group is observed to be 35.50 M for the year

2018. Moreover, the debt-to-equity ratio of the company is 6.89% for the year which indicates it

is likely to face low risk related with debt (Schmidlin, 2014). Moreover, the debt levels are

sustainable through measuring interest payments against earnings of the company.

Directions, Goals

The Australian airline industry has been deregulated and this deregulation has eliminated

the barriers for the new organisations to tap into the airline market of the nation (Collewaert &

Manigart, 2016). This has direct effect on organisations like Flight Centre Travel Group Limited,

as they are old market players and they would be affected significantly by this regulation. The

preference of the travellers keeps on varying over the years from one airline to another; however,

with the value of money, the selection of individuals for travelling through air has risen.

4.2 Microeconomic Factors:

There are certain microeconomic factors those are deemed to impact the financial

performance of Flight Centre Travel Group and these are explained under:

Operation

The current business operations of Flight Centre Travel Group are focussed on

positioning itself as leader in air travel business through expanding its online presence through

rolling out flagship stores. The company’s Australian operations is observed to improve and

attain increased profits. Moreover, majority of its operations is carried out offline with physical

stores to attain 95% sales in the current year along with that its online operations will contribute

to 5% growth in its sales (Penman, 2015).

Level of Debt

The level of debt for Flight Centre Travel Group is observed to be 35.50 M for the year

2018. Moreover, the debt-to-equity ratio of the company is 6.89% for the year which indicates it

is likely to face low risk related with debt (Schmidlin, 2014). Moreover, the debt levels are

sustainable through measuring interest payments against earnings of the company.

Directions, Goals

8COMPANY VALUATION

Flight Centre Travel Group is focussed on setting goals to bring in charge through

aggressively increasing its online presence. The company has set directions to maintain its

growth by developing plans to boost online along with call centre sales along with developing a

network of independent home-based contractor travel agents all through Australia (Rojo-

Ramírez, 2014).

Competition

The major competitors for the company are observed to be Hello world Travel Ltd,

Webjet Ltd and Corporate Travel Management Ltd. Flight Centre Travel Group is not able to

increase its ticket prices for the strong competition faced by it in the travel industry. Its

competitors are observed to offer cheap priced tickets in comparison to this airline company.

5.0 Peer Comparison:

Helloworld Travel Ltd

From analysing the share price trend of Helloworld Travel Ltd it has been observed that

the share prices of the company are observed to increase from the year 2014 to the year 2018.

Such increase in the company’s share price is because of its highly competitive rebranding

marketing initiatives that evidences its strong financial performance. The new branding was

successfully rolled out across the network all through its business locations. Moreover, an

increase in the company’s share price is observed because of its increase in cruise, corporate

along with air business along with improved contracting outcomes were important factors in

increasing its turnover result for the year. The acquisition decision of the company for Magellan

Travel Group has been successful in attaing 10.3% over the recent months (Helloworld Travel

Limited., 2018).

Flight Centre Travel Group is focussed on setting goals to bring in charge through

aggressively increasing its online presence. The company has set directions to maintain its

growth by developing plans to boost online along with call centre sales along with developing a

network of independent home-based contractor travel agents all through Australia (Rojo-

Ramírez, 2014).

Competition

The major competitors for the company are observed to be Hello world Travel Ltd,

Webjet Ltd and Corporate Travel Management Ltd. Flight Centre Travel Group is not able to

increase its ticket prices for the strong competition faced by it in the travel industry. Its

competitors are observed to offer cheap priced tickets in comparison to this airline company.

5.0 Peer Comparison:

Helloworld Travel Ltd

From analysing the share price trend of Helloworld Travel Ltd it has been observed that

the share prices of the company are observed to increase from the year 2014 to the year 2018.

Such increase in the company’s share price is because of its highly competitive rebranding

marketing initiatives that evidences its strong financial performance. The new branding was

successfully rolled out across the network all through its business locations. Moreover, an

increase in the company’s share price is observed because of its increase in cruise, corporate

along with air business along with improved contracting outcomes were important factors in

increasing its turnover result for the year. The acquisition decision of the company for Magellan

Travel Group has been successful in attaing 10.3% over the recent months (Helloworld Travel

Limited., 2018).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9COMPANY VALUATION

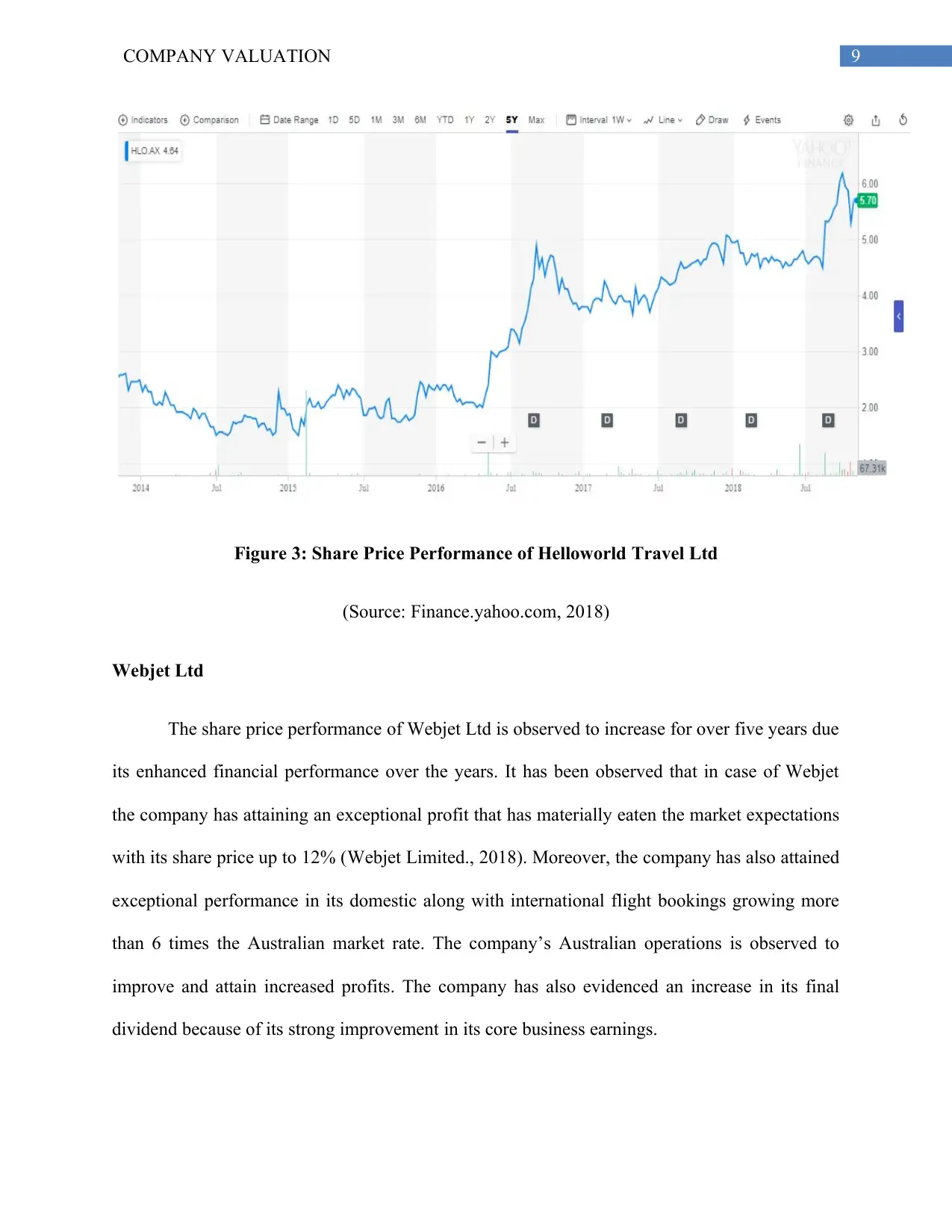

Figure 3: Share Price Performance of Helloworld Travel Ltd

(Source: Finance.yahoo.com, 2018)

Webjet Ltd

The share price performance of Webjet Ltd is observed to increase for over five years due

its enhanced financial performance over the years. It has been observed that in case of Webjet

the company has attaining an exceptional profit that has materially eaten the market expectations

with its share price up to 12% (Webjet Limited., 2018). Moreover, the company has also attained

exceptional performance in its domestic along with international flight bookings growing more

than 6 times the Australian market rate. The company’s Australian operations is observed to

improve and attain increased profits. The company has also evidenced an increase in its final

dividend because of its strong improvement in its core business earnings.

Figure 3: Share Price Performance of Helloworld Travel Ltd

(Source: Finance.yahoo.com, 2018)

Webjet Ltd

The share price performance of Webjet Ltd is observed to increase for over five years due

its enhanced financial performance over the years. It has been observed that in case of Webjet

the company has attaining an exceptional profit that has materially eaten the market expectations

with its share price up to 12% (Webjet Limited., 2018). Moreover, the company has also attained

exceptional performance in its domestic along with international flight bookings growing more

than 6 times the Australian market rate. The company’s Australian operations is observed to

improve and attain increased profits. The company has also evidenced an increase in its final

dividend because of its strong improvement in its core business earnings.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10COMPANY VALUATION

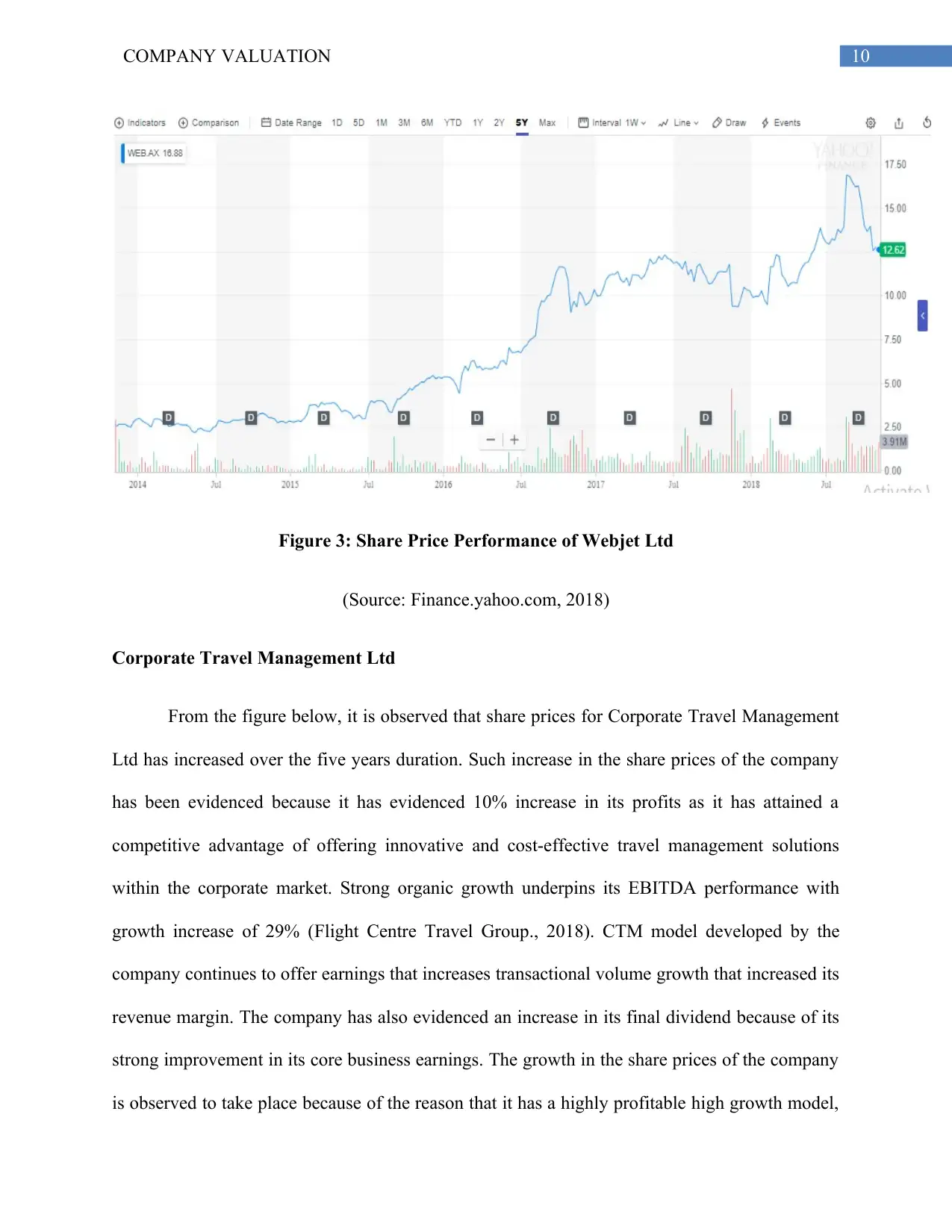

Figure 3: Share Price Performance of Webjet Ltd

(Source: Finance.yahoo.com, 2018)

Corporate Travel Management Ltd

From the figure below, it is observed that share prices for Corporate Travel Management

Ltd has increased over the five years duration. Such increase in the share prices of the company

has been evidenced because it has evidenced 10% increase in its profits as it has attained a

competitive advantage of offering innovative and cost-effective travel management solutions

within the corporate market. Strong organic growth underpins its EBITDA performance with

growth increase of 29% (Flight Centre Travel Group., 2018). CTM model developed by the

company continues to offer earnings that increases transactional volume growth that increased its

revenue margin. The company has also evidenced an increase in its final dividend because of its

strong improvement in its core business earnings. The growth in the share prices of the company

is observed to take place because of the reason that it has a highly profitable high growth model,

Figure 3: Share Price Performance of Webjet Ltd

(Source: Finance.yahoo.com, 2018)

Corporate Travel Management Ltd

From the figure below, it is observed that share prices for Corporate Travel Management

Ltd has increased over the five years duration. Such increase in the share prices of the company

has been evidenced because it has evidenced 10% increase in its profits as it has attained a

competitive advantage of offering innovative and cost-effective travel management solutions

within the corporate market. Strong organic growth underpins its EBITDA performance with

growth increase of 29% (Flight Centre Travel Group., 2018). CTM model developed by the

company continues to offer earnings that increases transactional volume growth that increased its

revenue margin. The company has also evidenced an increase in its final dividend because of its

strong improvement in its core business earnings. The growth in the share prices of the company

is observed to take place because of the reason that it has a highly profitable high growth model,

11COMPANY VALUATION

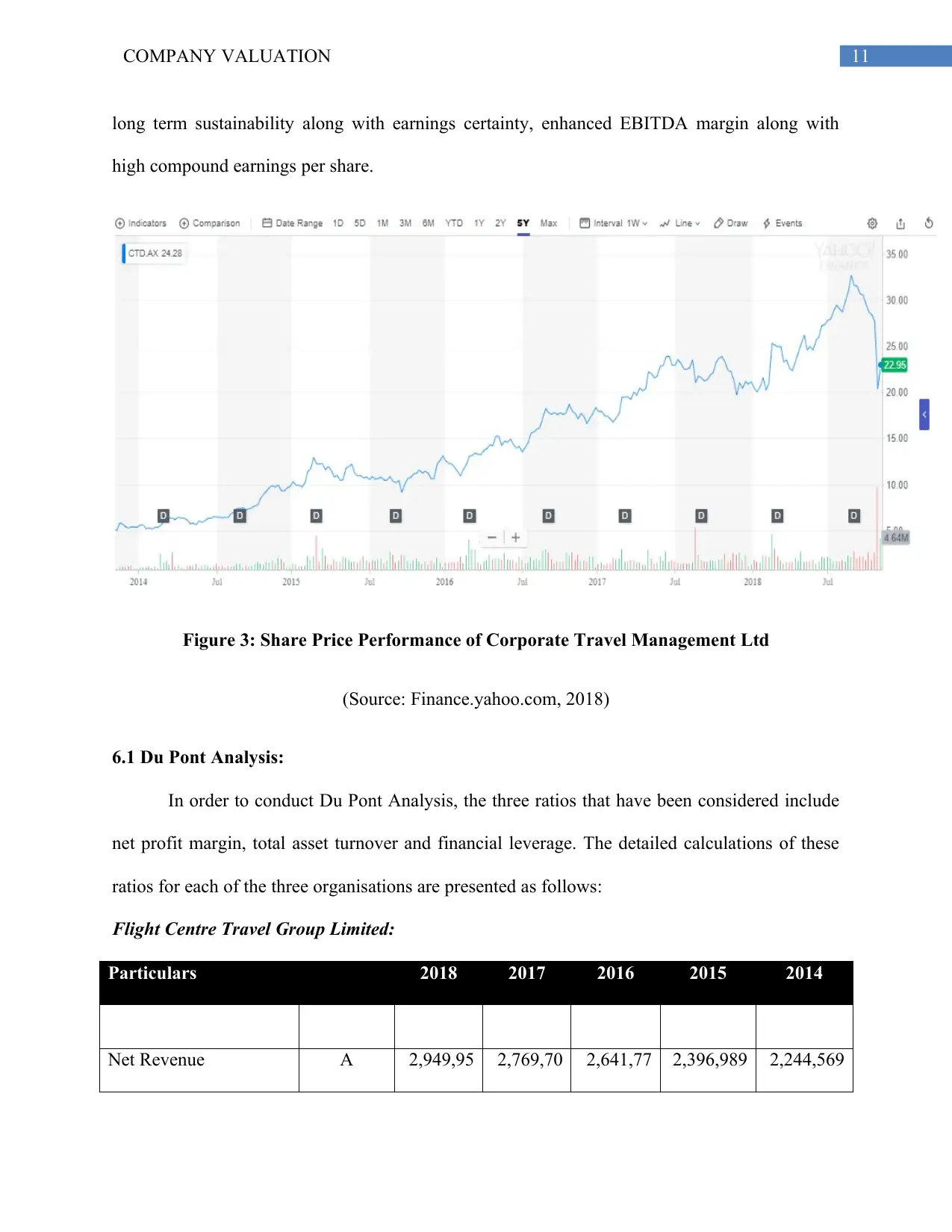

long term sustainability along with earnings certainty, enhanced EBITDA margin along with

high compound earnings per share.

Figure 3: Share Price Performance of Corporate Travel Management Ltd

(Source: Finance.yahoo.com, 2018)

6.1 Du Pont Analysis:

In order to conduct Du Pont Analysis, the three ratios that have been considered include

net profit margin, total asset turnover and financial leverage. The detailed calculations of these

ratios for each of the three organisations are presented as follows:

Flight Centre Travel Group Limited:

Particulars 2018 2017 2016 2015 2014

Net Revenue A 2,949,95 2,769,70 2,641,77 2,396,989 2,244,569

long term sustainability along with earnings certainty, enhanced EBITDA margin along with

high compound earnings per share.

Figure 3: Share Price Performance of Corporate Travel Management Ltd

(Source: Finance.yahoo.com, 2018)

6.1 Du Pont Analysis:

In order to conduct Du Pont Analysis, the three ratios that have been considered include

net profit margin, total asset turnover and financial leverage. The detailed calculations of these

ratios for each of the three organisations are presented as follows:

Flight Centre Travel Group Limited:

Particulars 2018 2017 2016 2015 2014

Net Revenue A 2,949,95 2,769,70 2,641,77 2,396,989 2,244,569

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 29

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.