FNCE 300 Assignment on Finance

VerifiedAdded on 2022/09/01

|17

|3160

|15

AI Summary

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: FNCE300

FNCE 300

Name of the Student:

Name of the University:

Author’s Note

FNCE 300

Name of the Student:

Name of the University:

Author’s Note

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1FNCE 300

Table of Contents

Lesson 9: Valuation of Common Stocks.........................................................................................2

9.1 Dividend Discount Model......................................................................................................2

9.2 Valuation................................................................................................................................2

9.3 Equation Analysis..................................................................................................................4

9.4 Kirk’s Information Inc...........................................................................................................5

9.5 Invest Co. Inc.........................................................................................................................7

Lesson 10: Principles of Risk Management....................................................................................8

10.1 Computroids and Blazer Inc................................................................................................8

10.2 Bond Evaluation................................................................................................................12

10.3 Retail Business...................................................................................................................13

Lesson 11: Hedging, Insuring, and Diversifying...........................................................................13

11.1 Hedging..............................................................................................................................13

11.2 Annuity..............................................................................................................................14

11.3 Hedging..............................................................................................................................15

Table of Contents

Lesson 9: Valuation of Common Stocks.........................................................................................2

9.1 Dividend Discount Model......................................................................................................2

9.2 Valuation................................................................................................................................2

9.3 Equation Analysis..................................................................................................................4

9.4 Kirk’s Information Inc...........................................................................................................5

9.5 Invest Co. Inc.........................................................................................................................7

Lesson 10: Principles of Risk Management....................................................................................8

10.1 Computroids and Blazer Inc................................................................................................8

10.2 Bond Evaluation................................................................................................................12

10.3 Retail Business...................................................................................................................13

Lesson 11: Hedging, Insuring, and Diversifying...........................................................................13

11.1 Hedging..............................................................................................................................13

11.2 Annuity..............................................................................................................................14

11.3 Hedging..............................................................................................................................15

2FNCE 300

Lesson 9: Valuation of Common Stocks

9.1 Dividend Discount Model

a) Po: D1/(k-g).

1. Multiplication Effect in both the sides of the equation by (k-g) factor getting: Po(k-g)=D1.

2. Dividing both sides with Po thereby getting: (k-g) = D1/Po.

3. Now, if we add growth factor (g) in both sides: k= D1/Po+g

b) The two ways in which money can be earned from investment in shares is particularly with

the help of dividend yield and capital gain yield and the same can be well described with the help

of equation created or developed above whereby;

D1: Refers to the Dividend yield that the investors would be creating.

Po+g: Refers to the Capital Gain Yield that the company would be making.

On the other hand, the total return in the equation designed refers to the dividend and capital gain

made by the investors which can be well shown with D1+(Po+g).

9.2 Valuation

a) Price Po:

D1: 20

K: 0.15

g: 0.12

Po: D1/(K-g)

Lesson 9: Valuation of Common Stocks

9.1 Dividend Discount Model

a) Po: D1/(k-g).

1. Multiplication Effect in both the sides of the equation by (k-g) factor getting: Po(k-g)=D1.

2. Dividing both sides with Po thereby getting: (k-g) = D1/Po.

3. Now, if we add growth factor (g) in both sides: k= D1/Po+g

b) The two ways in which money can be earned from investment in shares is particularly with

the help of dividend yield and capital gain yield and the same can be well described with the help

of equation created or developed above whereby;

D1: Refers to the Dividend yield that the investors would be creating.

Po+g: Refers to the Capital Gain Yield that the company would be making.

On the other hand, the total return in the equation designed refers to the dividend and capital gain

made by the investors which can be well shown with D1+(Po+g).

9.2 Valuation

a) Price Po:

D1: 20

K: 0.15

g: 0.12

Po: D1/(K-g)

3FNCE 300

Po: 20/(0.15-0.12).

Po: 666.67

b) P5 can be well calculated with the help of back calculation as follows:

D6: 20

K: 0.15

g: retention rate*return on equity.

D5: D6/(1+g)

D5: 20/(1+0.12)

D5: 17.86

P5: (D6/(k-g))

P5: (20/(0.15-0.12))

P5: 666.67

c) i) The value of the share or price at Po can be well calculated from P5 as follows:

Po: P5/(1+k)^5

Po: 666.67/(1+0.15)^5

Po: 331.45

ii) The value of share or Price at P1 can be well calculated as follows:

P1: P5/(1+k)^4

Po: 20/(0.15-0.12).

Po: 666.67

b) P5 can be well calculated with the help of back calculation as follows:

D6: 20

K: 0.15

g: retention rate*return on equity.

D5: D6/(1+g)

D5: 20/(1+0.12)

D5: 17.86

P5: (D6/(k-g))

P5: (20/(0.15-0.12))

P5: 666.67

c) i) The value of the share or price at Po can be well calculated from P5 as follows:

Po: P5/(1+k)^5

Po: 666.67/(1+0.15)^5

Po: 331.45

ii) The value of share or Price at P1 can be well calculated as follows:

P1: P5/(1+k)^4

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4FNCE 300

P1: 666.67/(1+0.15)^4

P1: 381.17

iii) The value of share or Price at P2 can be well calculated as follows:

P2: P5/(1+k)^3

P2: 666.67/(1+0.15)^3

P2: 438.34

d) The relationship between P2 and P1 can be well derived because if no dividends are paid in

between two point of time period then the only factor that would be remaining will be the

discount factor.

9.3 Equation Analysis

It is important to note that if K: ROE then Price level is not related to r. The same can be well

analysed as follows:

Growth rate: retention rate*return on equity

ROE: Yn/En-1.

Now Since r = (Yn-Dn)/Yn

then D1= (1 – r) x Y1 and

P0 = D1 / (k – g) . P0 = [(1 – r) x Y1] / (k – g) > P0 = [(1 – r) x Y1] / (k – g),

but, since k = ROE = Y1 / E0

P0 = [(1 – r) x Y1] / (ROE– r x ROE)

P1: 666.67/(1+0.15)^4

P1: 381.17

iii) The value of share or Price at P2 can be well calculated as follows:

P2: P5/(1+k)^3

P2: 666.67/(1+0.15)^3

P2: 438.34

d) The relationship between P2 and P1 can be well derived because if no dividends are paid in

between two point of time period then the only factor that would be remaining will be the

discount factor.

9.3 Equation Analysis

It is important to note that if K: ROE then Price level is not related to r. The same can be well

analysed as follows:

Growth rate: retention rate*return on equity

ROE: Yn/En-1.

Now Since r = (Yn-Dn)/Yn

then D1= (1 – r) x Y1 and

P0 = D1 / (k – g) . P0 = [(1 – r) x Y1] / (k – g) > P0 = [(1 – r) x Y1] / (k – g),

but, since k = ROE = Y1 / E0

P0 = [(1 – r) x Y1] / (ROE– r x ROE)

5FNCE 300

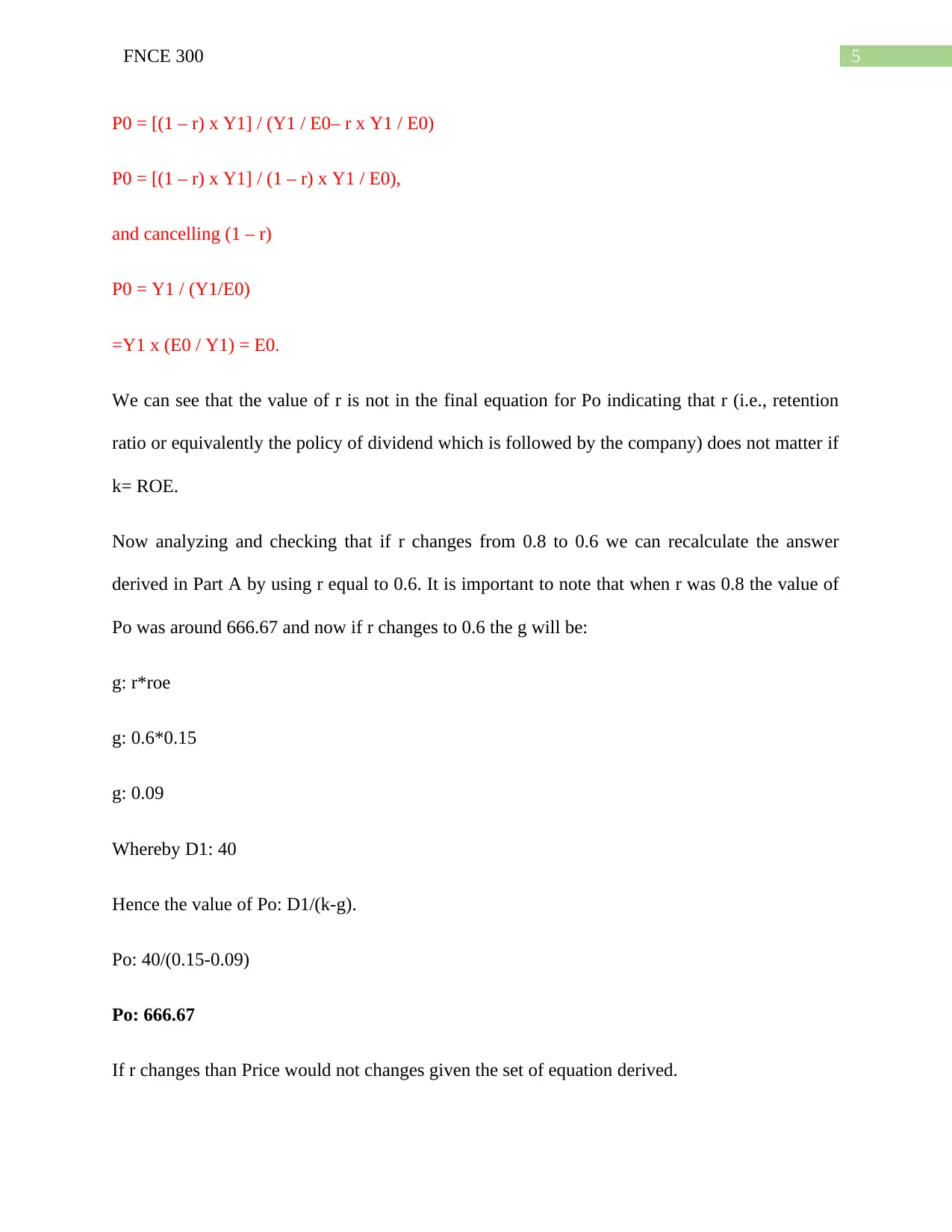

P0 = [(1 – r) x Y1] / (Y1 / E0– r x Y1 / E0)

P0 = [(1 – r) x Y1] / (1 – r) x Y1 / E0),

and cancelling (1 – r)

P0 = Y1 / (Y1/E0)

=Y1 x (E0 / Y1) = E0.

We can see that the value of r is not in the final equation for Po indicating that r (i.e., retention

ratio or equivalently the policy of dividend which is followed by the company) does not matter if

k= ROE.

Now analyzing and checking that if r changes from 0.8 to 0.6 we can recalculate the answer

derived in Part A by using r equal to 0.6. It is important to note that when r was 0.8 the value of

Po was around 666.67 and now if r changes to 0.6 the g will be:

g: r*roe

g: 0.6*0.15

g: 0.09

Whereby D1: 40

Hence the value of Po: D1/(k-g).

Po: 40/(0.15-0.09)

Po: 666.67

If r changes than Price would not changes given the set of equation derived.

P0 = [(1 – r) x Y1] / (Y1 / E0– r x Y1 / E0)

P0 = [(1 – r) x Y1] / (1 – r) x Y1 / E0),

and cancelling (1 – r)

P0 = Y1 / (Y1/E0)

=Y1 x (E0 / Y1) = E0.

We can see that the value of r is not in the final equation for Po indicating that r (i.e., retention

ratio or equivalently the policy of dividend which is followed by the company) does not matter if

k= ROE.

Now analyzing and checking that if r changes from 0.8 to 0.6 we can recalculate the answer

derived in Part A by using r equal to 0.6. It is important to note that when r was 0.8 the value of

Po was around 666.67 and now if r changes to 0.6 the g will be:

g: r*roe

g: 0.6*0.15

g: 0.09

Whereby D1: 40

Hence the value of Po: D1/(k-g).

Po: 40/(0.15-0.09)

Po: 666.67

If r changes than Price would not changes given the set of equation derived.

6FNCE 300

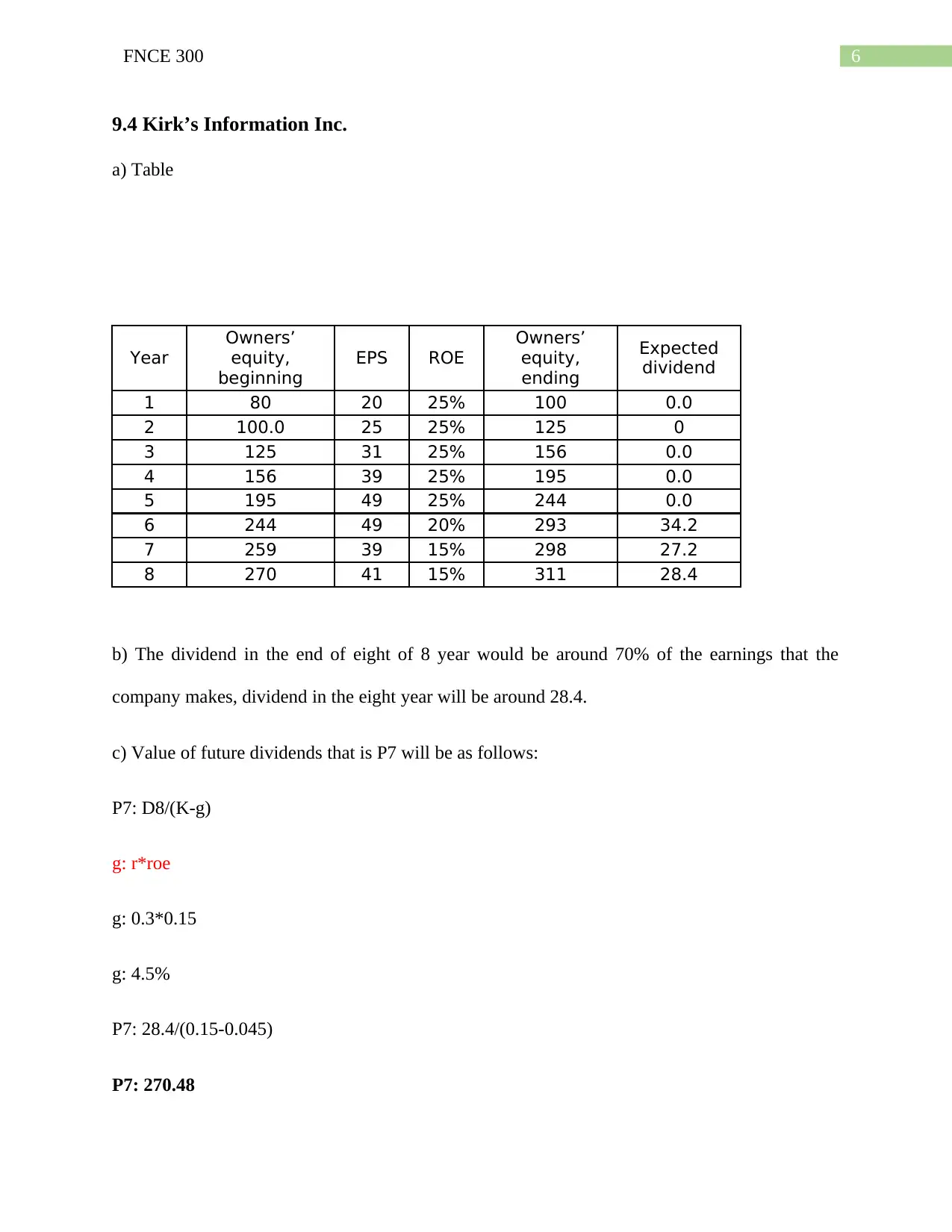

9.4 Kirk’s Information Inc.

a) Table

Year

Owners’

equity,

beginning

EPS ROE

Owners’

equity,

ending

Expected

dividend

1 80 20 25% 100 0.0

2 100.0 25 25% 125 0

3 125 31 25% 156 0.0

4 156 39 25% 195 0.0

5 195 49 25% 244 0.0

6 244 49 20% 293 34.2

7 259 39 15% 298 27.2

8 270 41 15% 311 28.4

b) The dividend in the end of eight of 8 year would be around 70% of the earnings that the

company makes, dividend in the eight year will be around 28.4.

c) Value of future dividends that is P7 will be as follows:

P7: D8/(K-g)

g: r*roe

g: 0.3*0.15

g: 4.5%

P7: 28.4/(0.15-0.045)

P7: 270.48

9.4 Kirk’s Information Inc.

a) Table

Year

Owners’

equity,

beginning

EPS ROE

Owners’

equity,

ending

Expected

dividend

1 80 20 25% 100 0.0

2 100.0 25 25% 125 0

3 125 31 25% 156 0.0

4 156 39 25% 195 0.0

5 195 49 25% 244 0.0

6 244 49 20% 293 34.2

7 259 39 15% 298 27.2

8 270 41 15% 311 28.4

b) The dividend in the end of eight of 8 year would be around 70% of the earnings that the

company makes, dividend in the eight year will be around 28.4.

c) Value of future dividends that is P7 will be as follows:

P7: D8/(K-g)

g: r*roe

g: 0.3*0.15

g: 4.5%

P7: 28.4/(0.15-0.045)

P7: 270.48

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7FNCE 300

d) The present value of P7 for a single assessment at the beginning of Year 1:

PO: P7/(1+k)^7

Po: 270.48/(1+0.15)^7

Po: 101.68

e) The value of share at time of considering all possible future dividends can be well calculated

as follows:

Po: D6/(1+k)^6+D7/(1+K)^7+D8/(k-g)

Po: 34.2/(1.15)^6+27.2/(1.15)^7+28.4/(0.15-0.045).

Po: 126.66

9.5 Invest Co. Inc.

a) If dividends are paid out then the same does not changes the value of the stock. It means that

dividend policy followed by the company does not affect the share price of the company.

b) In order to determine value per share we need to find the value of the firm which is as follows:

Value of Firm: Value of Equipment-Cash Balance

Value of Firm: 900,000-100,000

Value of Firm: 800,000

Value Per Share: Value of Firm/Outstanding Shares

Value Per Share: 800,000/100,000

Value Per Share: 8

d) The present value of P7 for a single assessment at the beginning of Year 1:

PO: P7/(1+k)^7

Po: 270.48/(1+0.15)^7

Po: 101.68

e) The value of share at time of considering all possible future dividends can be well calculated

as follows:

Po: D6/(1+k)^6+D7/(1+K)^7+D8/(k-g)

Po: 34.2/(1.15)^6+27.2/(1.15)^7+28.4/(0.15-0.045).

Po: 126.66

9.5 Invest Co. Inc.

a) If dividends are paid out then the same does not changes the value of the stock. It means that

dividend policy followed by the company does not affect the share price of the company.

b) In order to determine value per share we need to find the value of the firm which is as follows:

Value of Firm: Value of Equipment-Cash Balance

Value of Firm: 900,000-100,000

Value of Firm: 800,000

Value Per Share: Value of Firm/Outstanding Shares

Value Per Share: 800,000/100,000

Value Per Share: 8

8FNCE 300

Now, if we choose to sell the share for $10 when the actual value of per share is $8 the wealth

would be increasing $2 on a per share basis.

c) If we don’t choose to participate in the buyback program then the wealth or value remains

unchanged.

d) Stock Split does not affect the value of the shares. The total number of shares will just

multiply from 100,000 to 200,000 and the value of shares will be half and the value will remain

unchanged.

e) If dividends are paid then the same does not affect the wealth of shareholders.

f) If the stated amount of purchase that the company is considering that is $100,000 for buying

equipment which will be then used for earning a return equal to the firms discount rate, then the

actual value of the firm would be increasing to $900,000 from $800,000 and the overall wealth

would also increase by $1.

Lesson 10: Principles of Risk Management

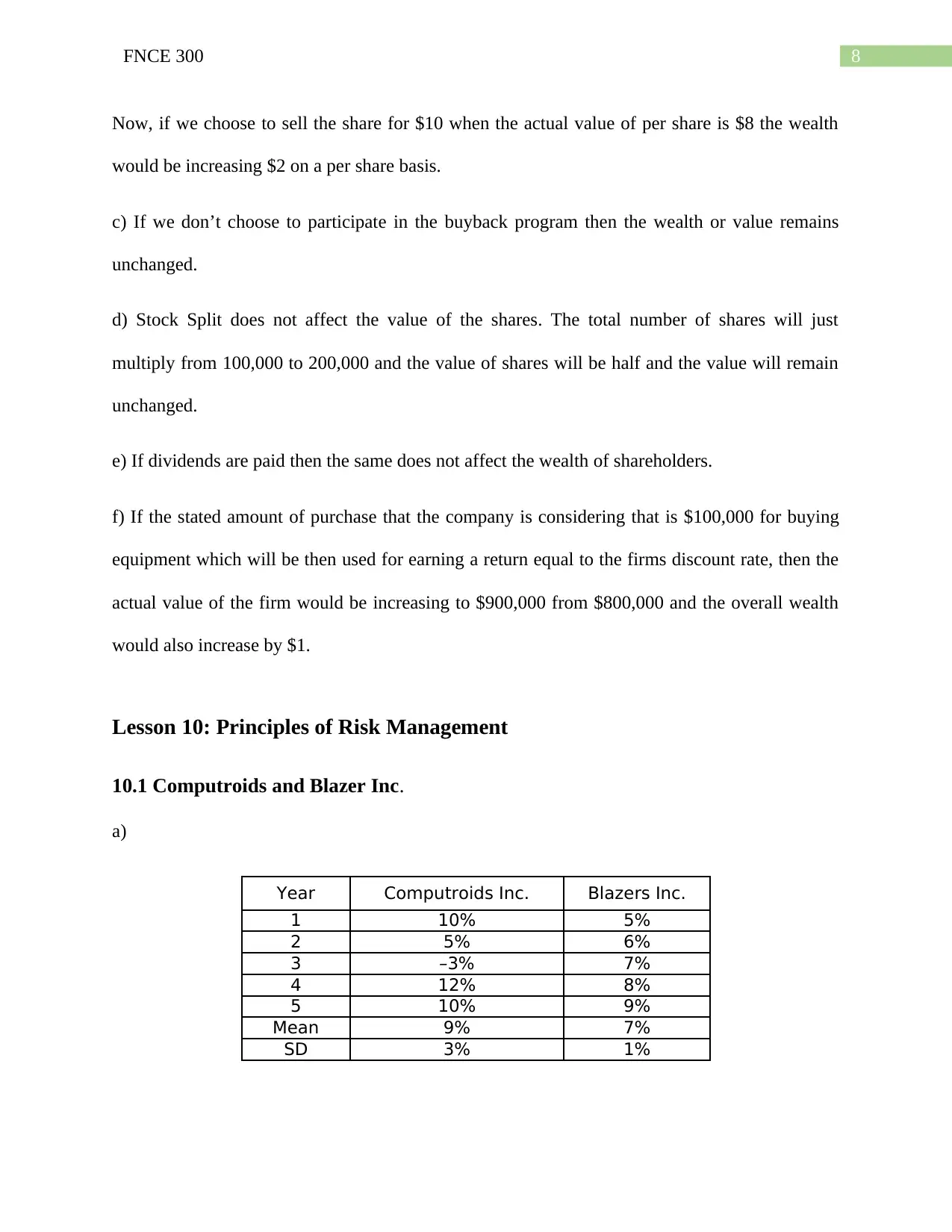

10.1 Computroids and Blazer Inc.

a)

Year Computroids Inc. Blazers Inc.

1 10% 5%

2 5% 6%

3 –3% 7%

4 12% 8%

5 10% 9%

Mean 9% 7%

SD 3% 1%

Now, if we choose to sell the share for $10 when the actual value of per share is $8 the wealth

would be increasing $2 on a per share basis.

c) If we don’t choose to participate in the buyback program then the wealth or value remains

unchanged.

d) Stock Split does not affect the value of the shares. The total number of shares will just

multiply from 100,000 to 200,000 and the value of shares will be half and the value will remain

unchanged.

e) If dividends are paid then the same does not affect the wealth of shareholders.

f) If the stated amount of purchase that the company is considering that is $100,000 for buying

equipment which will be then used for earning a return equal to the firms discount rate, then the

actual value of the firm would be increasing to $900,000 from $800,000 and the overall wealth

would also increase by $1.

Lesson 10: Principles of Risk Management

10.1 Computroids and Blazer Inc.

a)

Year Computroids Inc. Blazers Inc.

1 10% 5%

2 5% 6%

3 –3% 7%

4 12% 8%

5 10% 9%

Mean 9% 7%

SD 3% 1%

9FNCE 300

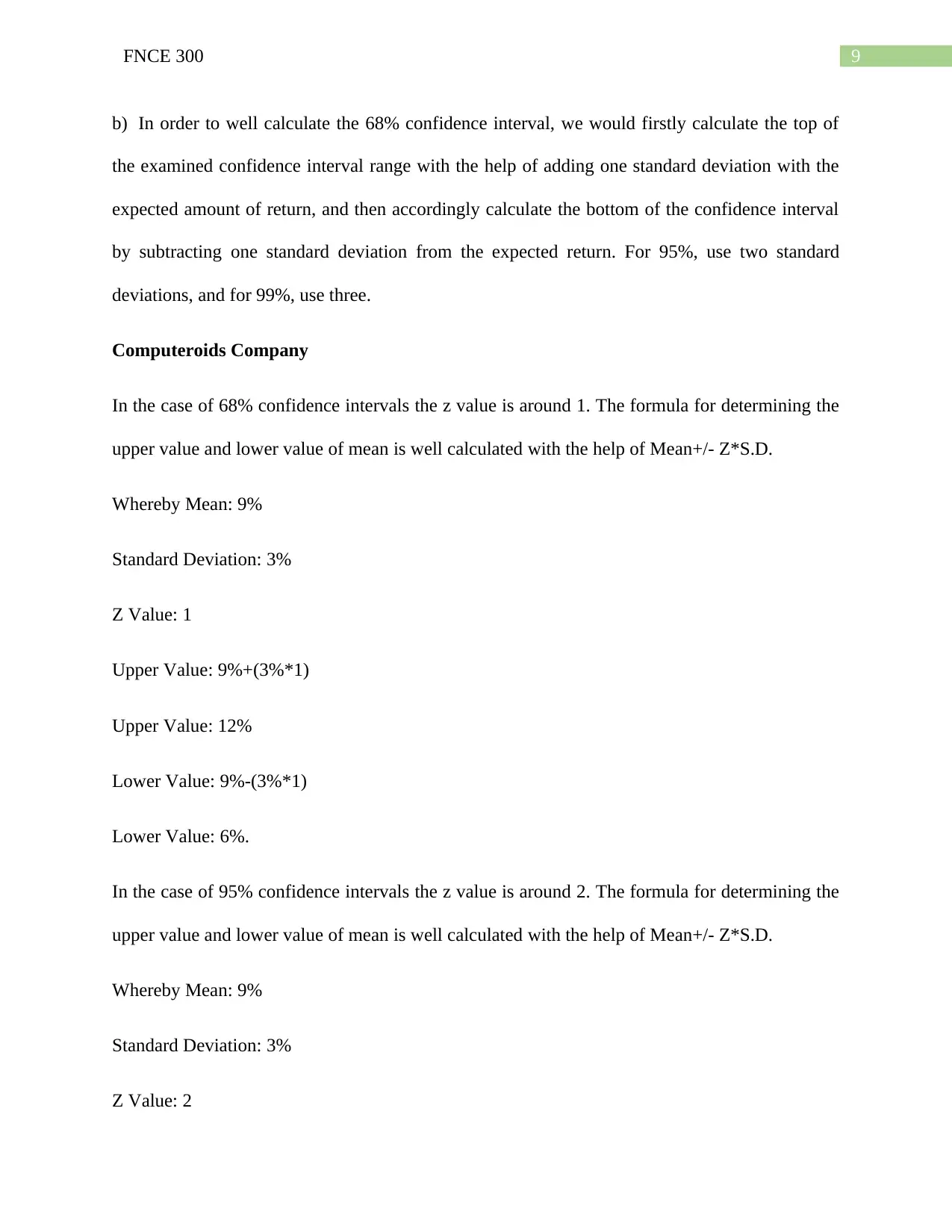

b) In order to well calculate the 68% confidence interval, we would firstly calculate the top of

the examined confidence interval range with the help of adding one standard deviation with the

expected amount of return, and then accordingly calculate the bottom of the confidence interval

by subtracting one standard deviation from the expected return. For 95%, use two standard

deviations, and for 99%, use three.

Computeroids Company

In the case of 68% confidence intervals the z value is around 1. The formula for determining the

upper value and lower value of mean is well calculated with the help of Mean+/- Z*S.D.

Whereby Mean: 9%

Standard Deviation: 3%

Z Value: 1

Upper Value: 9%+(3%*1)

Upper Value: 12%

Lower Value: 9%-(3%*1)

Lower Value: 6%.

In the case of 95% confidence intervals the z value is around 2. The formula for determining the

upper value and lower value of mean is well calculated with the help of Mean+/- Z*S.D.

Whereby Mean: 9%

Standard Deviation: 3%

Z Value: 2

b) In order to well calculate the 68% confidence interval, we would firstly calculate the top of

the examined confidence interval range with the help of adding one standard deviation with the

expected amount of return, and then accordingly calculate the bottom of the confidence interval

by subtracting one standard deviation from the expected return. For 95%, use two standard

deviations, and for 99%, use three.

Computeroids Company

In the case of 68% confidence intervals the z value is around 1. The formula for determining the

upper value and lower value of mean is well calculated with the help of Mean+/- Z*S.D.

Whereby Mean: 9%

Standard Deviation: 3%

Z Value: 1

Upper Value: 9%+(3%*1)

Upper Value: 12%

Lower Value: 9%-(3%*1)

Lower Value: 6%.

In the case of 95% confidence intervals the z value is around 2. The formula for determining the

upper value and lower value of mean is well calculated with the help of Mean+/- Z*S.D.

Whereby Mean: 9%

Standard Deviation: 3%

Z Value: 2

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10FNCE 300

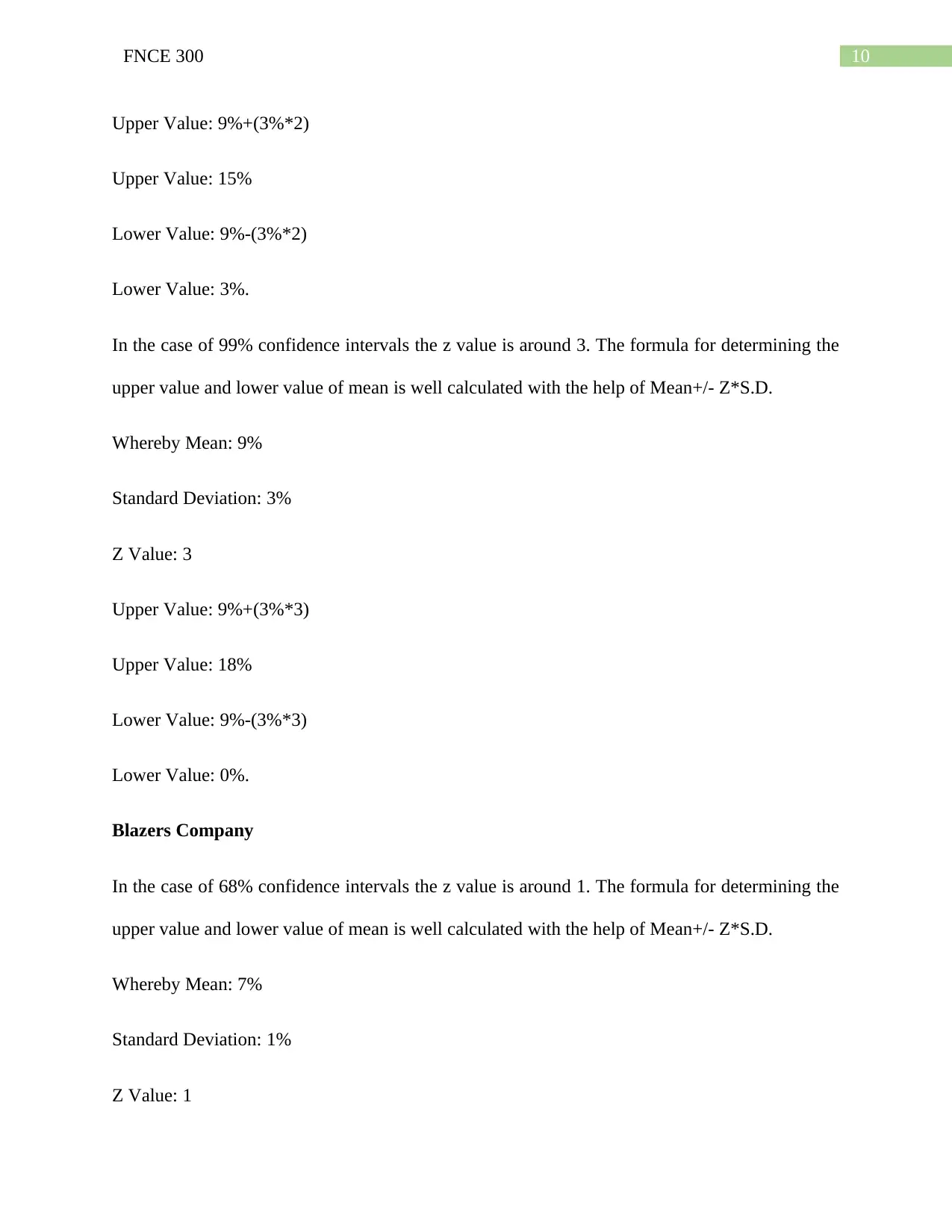

Upper Value: 9%+(3%*2)

Upper Value: 15%

Lower Value: 9%-(3%*2)

Lower Value: 3%.

In the case of 99% confidence intervals the z value is around 3. The formula for determining the

upper value and lower value of mean is well calculated with the help of Mean+/- Z*S.D.

Whereby Mean: 9%

Standard Deviation: 3%

Z Value: 3

Upper Value: 9%+(3%*3)

Upper Value: 18%

Lower Value: 9%-(3%*3)

Lower Value: 0%.

Blazers Company

In the case of 68% confidence intervals the z value is around 1. The formula for determining the

upper value and lower value of mean is well calculated with the help of Mean+/- Z*S.D.

Whereby Mean: 7%

Standard Deviation: 1%

Z Value: 1

Upper Value: 9%+(3%*2)

Upper Value: 15%

Lower Value: 9%-(3%*2)

Lower Value: 3%.

In the case of 99% confidence intervals the z value is around 3. The formula for determining the

upper value and lower value of mean is well calculated with the help of Mean+/- Z*S.D.

Whereby Mean: 9%

Standard Deviation: 3%

Z Value: 3

Upper Value: 9%+(3%*3)

Upper Value: 18%

Lower Value: 9%-(3%*3)

Lower Value: 0%.

Blazers Company

In the case of 68% confidence intervals the z value is around 1. The formula for determining the

upper value and lower value of mean is well calculated with the help of Mean+/- Z*S.D.

Whereby Mean: 7%

Standard Deviation: 1%

Z Value: 1

11FNCE 300

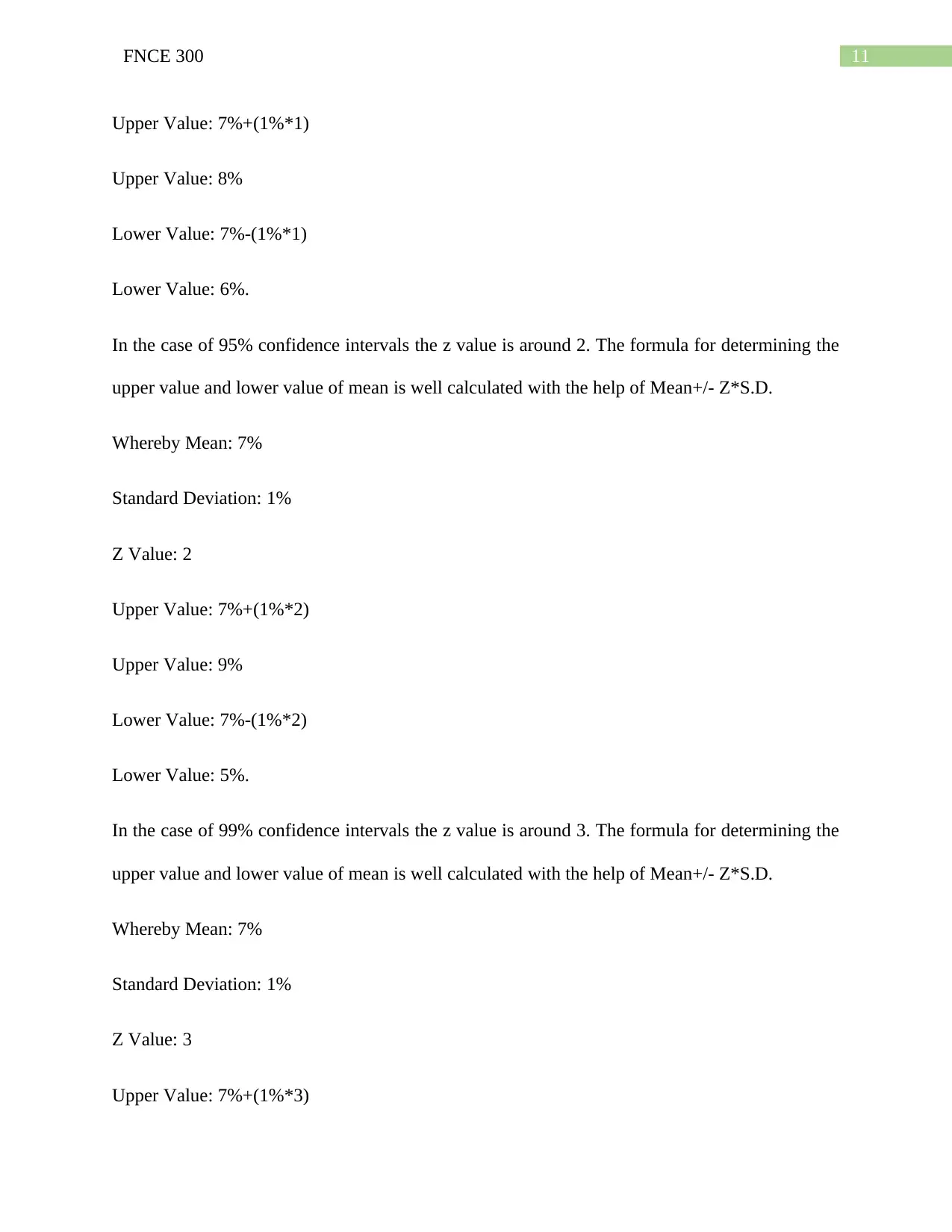

Upper Value: 7%+(1%*1)

Upper Value: 8%

Lower Value: 7%-(1%*1)

Lower Value: 6%.

In the case of 95% confidence intervals the z value is around 2. The formula for determining the

upper value and lower value of mean is well calculated with the help of Mean+/- Z*S.D.

Whereby Mean: 7%

Standard Deviation: 1%

Z Value: 2

Upper Value: 7%+(1%*2)

Upper Value: 9%

Lower Value: 7%-(1%*2)

Lower Value: 5%.

In the case of 99% confidence intervals the z value is around 3. The formula for determining the

upper value and lower value of mean is well calculated with the help of Mean+/- Z*S.D.

Whereby Mean: 7%

Standard Deviation: 1%

Z Value: 3

Upper Value: 7%+(1%*3)

Upper Value: 7%+(1%*1)

Upper Value: 8%

Lower Value: 7%-(1%*1)

Lower Value: 6%.

In the case of 95% confidence intervals the z value is around 2. The formula for determining the

upper value and lower value of mean is well calculated with the help of Mean+/- Z*S.D.

Whereby Mean: 7%

Standard Deviation: 1%

Z Value: 2

Upper Value: 7%+(1%*2)

Upper Value: 9%

Lower Value: 7%-(1%*2)

Lower Value: 5%.

In the case of 99% confidence intervals the z value is around 3. The formula for determining the

upper value and lower value of mean is well calculated with the help of Mean+/- Z*S.D.

Whereby Mean: 7%

Standard Deviation: 1%

Z Value: 3

Upper Value: 7%+(1%*3)

12FNCE 300

Upper Value: 10%

Lower Value: 7%-(1%*3)

Lower Value: 4%.

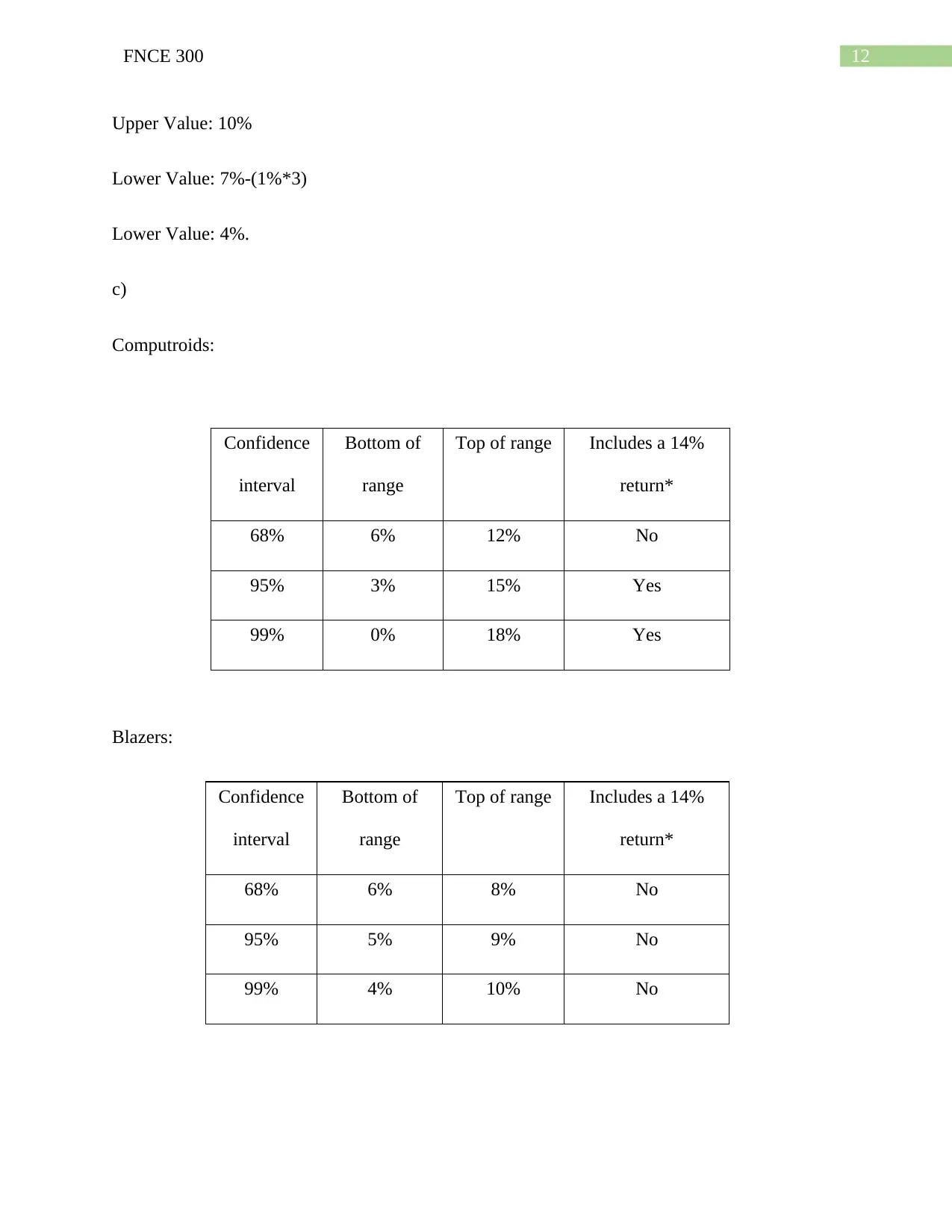

c)

Computroids:

Confidence

interval

Bottom of

range

Top of range Includes a 14%

return*

68% 6% 12% No

95% 3% 15% Yes

99% 0% 18% Yes

Blazers:

Confidence

interval

Bottom of

range

Top of range Includes a 14%

return*

68% 6% 8% No

95% 5% 9% No

99% 4% 10% No

Upper Value: 10%

Lower Value: 7%-(1%*3)

Lower Value: 4%.

c)

Computroids:

Confidence

interval

Bottom of

range

Top of range Includes a 14%

return*

68% 6% 12% No

95% 3% 15% Yes

99% 0% 18% Yes

Blazers:

Confidence

interval

Bottom of

range

Top of range Includes a 14%

return*

68% 6% 8% No

95% 5% 9% No

99% 4% 10% No

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

13FNCE 300

10.2 Bond Evaluation

a) If interest rate rises in that case the bond risk can be well reduced by buying bonds that mature

at different maturity dates. The risk can be hedged by using or with the initiation of interest rate

swaps and other financial derivatives instruments which mitigates or reduces the risk of interest

rate.

b) Interest rate and bond price have a negative correlation and if inflation rises it causes the

interest rate to increase which in turn decreases the price of the bonds. Treasury inflation

protection securities or inflation protected real yield securities can be well purchased by the

investors to reduce the risk in specifically related to inflation.

c) Market volatility in turn affects the bond systematic risk which can be well reduced with the

help of diversification among various courses of bonds like corporate and government bonds.

10.3 Retail Business

a) First Option: 10% of sales revenue will be preferable if the sales are volatile and if the market

demand in response to business is uncertain.

Second Option: Fixed Cost of $5,000 on the other hand would be preferable when the sales,

demand and profitability associated with the business is expected to be strong and consistent.

b) The incremental increase in the rental arrangement should be well discussed and the lock in

fixed or security amount that needs to be initially deposited should be well written down in the

lease contract. On the other hand, terms of renewal after five-years and exit policy before five-

years if possible and what conditions are there should be well discussed in the lease contract.

10.2 Bond Evaluation

a) If interest rate rises in that case the bond risk can be well reduced by buying bonds that mature

at different maturity dates. The risk can be hedged by using or with the initiation of interest rate

swaps and other financial derivatives instruments which mitigates or reduces the risk of interest

rate.

b) Interest rate and bond price have a negative correlation and if inflation rises it causes the

interest rate to increase which in turn decreases the price of the bonds. Treasury inflation

protection securities or inflation protected real yield securities can be well purchased by the

investors to reduce the risk in specifically related to inflation.

c) Market volatility in turn affects the bond systematic risk which can be well reduced with the

help of diversification among various courses of bonds like corporate and government bonds.

10.3 Retail Business

a) First Option: 10% of sales revenue will be preferable if the sales are volatile and if the market

demand in response to business is uncertain.

Second Option: Fixed Cost of $5,000 on the other hand would be preferable when the sales,

demand and profitability associated with the business is expected to be strong and consistent.

b) The incremental increase in the rental arrangement should be well discussed and the lock in

fixed or security amount that needs to be initially deposited should be well written down in the

lease contract. On the other hand, terms of renewal after five-years and exit policy before five-

years if possible and what conditions are there should be well discussed in the lease contract.

14FNCE 300

Lesson 11: Hedging, Insuring, and Diversifying

11.1 Hedging

a) The price variance can be well calculated with the help of the actual price and the upper range

of price level as follows:

Price Range: $3.00-$2.25: $0.75

Gallons of Water: 350 Gallons

Total Price Variance: 350*0.75: $262.5

b) Tom would be particularly affected with the price range difference of about $0.75 which is in

the case of lower side if the price falls from $2.25 to $1.50 and he is currently having a total of

100,000 gallons of oil. The price variance can affect Tom in particular if the price falls below the

specified levels such that it would be incurring a loss on an overall basis.

c) The non-contracting strategy that could be used in particular for the purpose of reducing the

risk can be well done with the help of purchasing the contracts that is in the form of the physical

storage that the company can well maintain.

d) Yes a financial contract or an agreement to buy the commodity (oil) at a fixed rate can be well

initiated with the Tom in order to reduce the risk exposure that is risk of rising price of oil. The

agreement would eliminate the risk of increasing price which in turn can affect the profitability

of the company.

e) Yes both the party can enter into an agreement to buy/sell the commodity at the fixed rate so

that the risk in the view perspective of increasing or decreasing prices can be well captured and

the nature of risk averse can be well removed.

Lesson 11: Hedging, Insuring, and Diversifying

11.1 Hedging

a) The price variance can be well calculated with the help of the actual price and the upper range

of price level as follows:

Price Range: $3.00-$2.25: $0.75

Gallons of Water: 350 Gallons

Total Price Variance: 350*0.75: $262.5

b) Tom would be particularly affected with the price range difference of about $0.75 which is in

the case of lower side if the price falls from $2.25 to $1.50 and he is currently having a total of

100,000 gallons of oil. The price variance can affect Tom in particular if the price falls below the

specified levels such that it would be incurring a loss on an overall basis.

c) The non-contracting strategy that could be used in particular for the purpose of reducing the

risk can be well done with the help of purchasing the contracts that is in the form of the physical

storage that the company can well maintain.

d) Yes a financial contract or an agreement to buy the commodity (oil) at a fixed rate can be well

initiated with the Tom in order to reduce the risk exposure that is risk of rising price of oil. The

agreement would eliminate the risk of increasing price which in turn can affect the profitability

of the company.

e) Yes both the party can enter into an agreement to buy/sell the commodity at the fixed rate so

that the risk in the view perspective of increasing or decreasing prices can be well captured and

the nature of risk averse can be well removed.

15FNCE 300

11.2 Annuity

a) The movement associated with the foreign currency can lead to appreciation or depreciation of

the currency which in turn could affect the overall value of the forex currency. In the given set of

example the foreign currency receivable is in Euro Currency and the home currency is in

Canadian Dollar. Now if the Euro Currency Depreciates then the same would be resulting in a

lower value or wealth in terms of Canadian Currency. If we use to get

1 Euro: 1.45 CAD

If Euro Depreciates the 1 Euro: 1.35 CAD

Thus previously what we could have received in CAD terms as of Euro 2,000 is around 2903.67

CAD now we would get around 2700 CAD. Thus, it is important to forecast and incorporate the

forex movements.

b) The currency followed in France is Euro and the currency in which the amount would be

receivable is also in Euro so it is important that since there is no other forex currency that is

related in particularly with this would not affect the forex currency value.

c) Derivatives contract in particular could be well used for the purpose of hedging the forex

currency that is related with the change in the value of analyzed currency. Since, the amount

would be receivable in Canadian Dollar and the home currency would be received in the Euro

Currency thus change in real value of Euro or Canadian Currency can affect the actual value in

Euro terms.

11.3 Hedging

Hedging Insuring Diversi-

11.2 Annuity

a) The movement associated with the foreign currency can lead to appreciation or depreciation of

the currency which in turn could affect the overall value of the forex currency. In the given set of

example the foreign currency receivable is in Euro Currency and the home currency is in

Canadian Dollar. Now if the Euro Currency Depreciates then the same would be resulting in a

lower value or wealth in terms of Canadian Currency. If we use to get

1 Euro: 1.45 CAD

If Euro Depreciates the 1 Euro: 1.35 CAD

Thus previously what we could have received in CAD terms as of Euro 2,000 is around 2903.67

CAD now we would get around 2700 CAD. Thus, it is important to forecast and incorporate the

forex movements.

b) The currency followed in France is Euro and the currency in which the amount would be

receivable is also in Euro so it is important that since there is no other forex currency that is

related in particularly with this would not affect the forex currency value.

c) Derivatives contract in particular could be well used for the purpose of hedging the forex

currency that is related with the change in the value of analyzed currency. Since, the amount

would be receivable in Canadian Dollar and the home currency would be received in the Euro

Currency thus change in real value of Euro or Canadian Currency can affect the actual value in

Euro terms.

11.3 Hedging

Hedging Insuring Diversi-

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

16FNCE 300

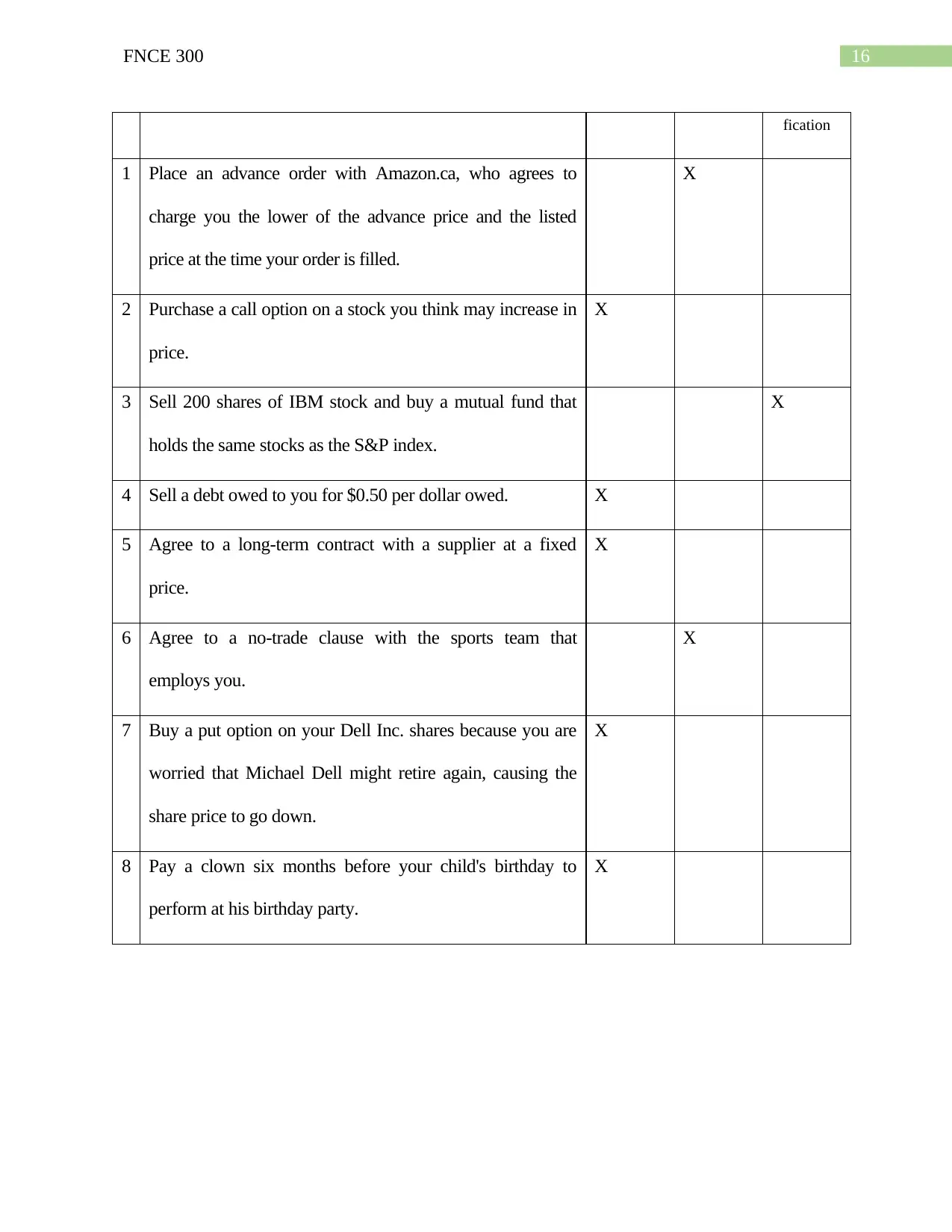

fication

1 Place an advance order with Amazon.ca, who agrees to

charge you the lower of the advance price and the listed

price at the time your order is filled.

X

2 Purchase a call option on a stock you think may increase in

price.

X

3 Sell 200 shares of IBM stock and buy a mutual fund that

holds the same stocks as the S&P index.

X

4 Sell a debt owed to you for $0.50 per dollar owed. X

5 Agree to a long-term contract with a supplier at a fixed

price.

X

6 Agree to a no-trade clause with the sports team that

employs you.

X

7 Buy a put option on your Dell Inc. shares because you are

worried that Michael Dell might retire again, causing the

share price to go down.

X

8 Pay a clown six months before your child's birthday to

perform at his birthday party.

X

fication

1 Place an advance order with Amazon.ca, who agrees to

charge you the lower of the advance price and the listed

price at the time your order is filled.

X

2 Purchase a call option on a stock you think may increase in

price.

X

3 Sell 200 shares of IBM stock and buy a mutual fund that

holds the same stocks as the S&P index.

X

4 Sell a debt owed to you for $0.50 per dollar owed. X

5 Agree to a long-term contract with a supplier at a fixed

price.

X

6 Agree to a no-trade clause with the sports team that

employs you.

X

7 Buy a put option on your Dell Inc. shares because you are

worried that Michael Dell might retire again, causing the

share price to go down.

X

8 Pay a clown six months before your child's birthday to

perform at his birthday party.

X

1 out of 17

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.