Monarch Institute FNS50215 Diploma of Accounting Module 2.3 Assignment

VerifiedAdded on 2023/03/30

|16

|2519

|270

Homework Assignment

AI Summary

This document presents a completed assignment for the FNS50215 Diploma of Accounting Module 2.3, focusing on providing management accounting information. The assignment includes solutions to short answer and worked answer questions. The questions cover topics such as calculating budgeted per-unit costs, preparing general journal entries to record transactions, and preparing job cost summaries and journal entries. Specifically, the assignment addresses prime costs, conversion costs, period costs, fixed and variable manufacturing costs, journal entries related to raw materials, labor, factory overhead, cost of goods sold, and job costing calculations. The student has provided detailed answers to these questions, including calculations and journal entries. The assignment is based on the material from the text “Provide Management Accounting Information” by Colin Davy & Danny Bruce.

FNS50215 Diploma of Accounting

Module 2.3Assignment

Instructions:

This assignment contains multiple Assessment Activities

Please complete the Declaration of Authenticity at the bottom of this page

Save this assignment (e.g. on your desktop)

To complete the assignment, read the instructions for each question carefully.

You may be required to refer to your learning materials or other sources to complete

this assessment.

You are required to type all your responses in the spaces provided

Once you have completed all parts of the assignment and saved it, login to the

Monarch Institute LMS to submit your assignment for grading

To submit your assignment click on the file ”SubmitDiploma of AccountingModule 2.3

Assignment” in the Module 2.3section of your course and upload your assignment file.

Please be sure to click “Continue” after clicking “submit”.This ensures your assessor receives

notification of your submission – very important!

Declaration of Understanding and Authenticity *

I have read and understood the assessment instructions provided to me in the Learning Management System.

I certify that the attached material is my original work. No other person’s work has been used without due

acknowledgement. I understand that the work submitted may be reproduced and/or communicated for the purpose

of detecting plagiarism.

Student Name*: Date:

* I understand that by typing my name or inserting a digital signature into this box that I agree and am bound by the

above student declaration.

Diploma of Accounting - Module 2.3 Assignment 180701 Page 1 of 16

Module 2.3Assignment

Instructions:

This assignment contains multiple Assessment Activities

Please complete the Declaration of Authenticity at the bottom of this page

Save this assignment (e.g. on your desktop)

To complete the assignment, read the instructions for each question carefully.

You may be required to refer to your learning materials or other sources to complete

this assessment.

You are required to type all your responses in the spaces provided

Once you have completed all parts of the assignment and saved it, login to the

Monarch Institute LMS to submit your assignment for grading

To submit your assignment click on the file ”SubmitDiploma of AccountingModule 2.3

Assignment” in the Module 2.3section of your course and upload your assignment file.

Please be sure to click “Continue” after clicking “submit”.This ensures your assessor receives

notification of your submission – very important!

Declaration of Understanding and Authenticity *

I have read and understood the assessment instructions provided to me in the Learning Management System.

I certify that the attached material is my original work. No other person’s work has been used without due

acknowledgement. I understand that the work submitted may be reproduced and/or communicated for the purpose

of detecting plagiarism.

Student Name*: Date:

* I understand that by typing my name or inserting a digital signature into this box that I agree and am bound by the

above student declaration.

Diploma of Accounting - Module 2.3 Assignment 180701 Page 1 of 16

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Units Covered: FNSACC507

Important assessment information

Aims of this assessment

This assessment focuses on providing management accounting information.

Marking and feedback

This assignment contains multiple Assessment Activities each containing specific instructions.

You are required to attempt all questions.

This particular assessment forms part of your overall assessment for the following unit(s) of

competency:

FNSACC507 Provide management accounting information

Grading for this assessment will be deemed “competent” or “not-yet-competent” in line with

specified educational standards under the Australian Qualifications Framework.

What does “competent” mean?

These answers contain relevant and accurate information in response to the question/s with

limited serious errors in fact or application. If incorrect information is contained in an answer, it

must be fundamentally outweighed by the accurate information provided. This will be assessed

against a marking guide provided to assessors for their determination.

What does “not-yet-competent” mean?

This occurs when an assessment does not meet the marking guide standards provided to

assessors. These answers either do not address the question specifically, or are wrong from a

legislative perspective, or are incorrectly applied. Answers that omit to provide a response to any

significant issue (where multiple issues must be addressed in a question) may also be deemed

not-yet-competent. Answers that have faulty reasoning, a poor standard of expression or include

plagiarism may also be deemed not-yet-competent. Please note, additional information regarding

Monarch’s plagiarism policy is contained in the Student Information Guide which can be found

here: http://www.monarch.edu.au/student-info/

Diploma of Accounting - Module 2.3 Assignment 180701 Page 2 of 16

Important assessment information

Aims of this assessment

This assessment focuses on providing management accounting information.

Marking and feedback

This assignment contains multiple Assessment Activities each containing specific instructions.

You are required to attempt all questions.

This particular assessment forms part of your overall assessment for the following unit(s) of

competency:

FNSACC507 Provide management accounting information

Grading for this assessment will be deemed “competent” or “not-yet-competent” in line with

specified educational standards under the Australian Qualifications Framework.

What does “competent” mean?

These answers contain relevant and accurate information in response to the question/s with

limited serious errors in fact or application. If incorrect information is contained in an answer, it

must be fundamentally outweighed by the accurate information provided. This will be assessed

against a marking guide provided to assessors for their determination.

What does “not-yet-competent” mean?

This occurs when an assessment does not meet the marking guide standards provided to

assessors. These answers either do not address the question specifically, or are wrong from a

legislative perspective, or are incorrectly applied. Answers that omit to provide a response to any

significant issue (where multiple issues must be addressed in a question) may also be deemed

not-yet-competent. Answers that have faulty reasoning, a poor standard of expression or include

plagiarism may also be deemed not-yet-competent. Please note, additional information regarding

Monarch’s plagiarism policy is contained in the Student Information Guide which can be found

here: http://www.monarch.edu.au/student-info/

Diploma of Accounting - Module 2.3 Assignment 180701 Page 2 of 16

Units Covered: FNSACC507

What happens if you are deemed not-yet-competent?

In the event you do not achieve competency by your assessor on this assessment, you will be

given one more opportunity to re-submit the assessment after consultation with your Trainer/

Assessor. You will know your assessment is deemed ‘not-yet-competent’ if your grade book in the

Monarch LMS says “NYC” after you have received an email from your assessor advising your

assessment has been graded.

Important: It is your responsibility to ensure your assessment resubmission addresses all areas

deemed unsatisfactory by your assessor. Please note, if you are still unsuccessful in meeting

competency after resubmitting your assessment, you will be required to repeat those units.

In the event that you have concerns about the assessment decision then you can refer to our

Complaints & Appeals process also contained within the Student Information Guide.

Expectations from your assessor when answering different types of assessment questions:

Knowledge based questions:

A knowledge based question requires you to clearly identify and cover the key subject matter

areas raised in the question in full as part of the response.

Performance based questions:

A performance based question requires you to clearly demonstrate your ability to complete

certain tasks, that is, to perform these tasks.

Good luck

Finally, good luck with your learning and assessments and remember your trainers are here to

assist you

Diploma of Accounting - Module 2.3 Assignment 180701 Page 3 of 16

What happens if you are deemed not-yet-competent?

In the event you do not achieve competency by your assessor on this assessment, you will be

given one more opportunity to re-submit the assessment after consultation with your Trainer/

Assessor. You will know your assessment is deemed ‘not-yet-competent’ if your grade book in the

Monarch LMS says “NYC” after you have received an email from your assessor advising your

assessment has been graded.

Important: It is your responsibility to ensure your assessment resubmission addresses all areas

deemed unsatisfactory by your assessor. Please note, if you are still unsuccessful in meeting

competency after resubmitting your assessment, you will be required to repeat those units.

In the event that you have concerns about the assessment decision then you can refer to our

Complaints & Appeals process also contained within the Student Information Guide.

Expectations from your assessor when answering different types of assessment questions:

Knowledge based questions:

A knowledge based question requires you to clearly identify and cover the key subject matter

areas raised in the question in full as part of the response.

Performance based questions:

A performance based question requires you to clearly demonstrate your ability to complete

certain tasks, that is, to perform these tasks.

Good luck

Finally, good luck with your learning and assessments and remember your trainers are here to

assist you

Diploma of Accounting - Module 2.3 Assignment 180701 Page 3 of 16

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Units Covered: FNSACC507

The following questions are based on the material in the text “Provide Management Accounting Information”

by Colin Davy & Danny Bruce, 7th edition (July, 2015) or 8th edition (January 2018).

Activity instructions to candidates

This is an open book assessment activity.

You are required to read this assessment and answer all questions that follow.

Please type your answers in the spaces provided.

Please ensure you have read “Important assessment information” at the front of this assessment

Estimated time for completion of this assessment activity: 2-3 hours

Diploma of Accounting - Module 2.3 Assignment 180701 Page 4 of 16

Assessment Activities

Short Answer and Worked Answer Questions

FNSACC507 Provide management accounting information

The following questions are based on the material in the text “Provide Management Accounting Information”

by Colin Davy & Danny Bruce, 7th edition (July, 2015) or 8th edition (January 2018).

Activity instructions to candidates

This is an open book assessment activity.

You are required to read this assessment and answer all questions that follow.

Please type your answers in the spaces provided.

Please ensure you have read “Important assessment information” at the front of this assessment

Estimated time for completion of this assessment activity: 2-3 hours

Diploma of Accounting - Module 2.3 Assignment 180701 Page 4 of 16

Assessment Activities

Short Answer and Worked Answer Questions

FNSACC507 Provide management accounting information

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Units Covered: FNSACC507

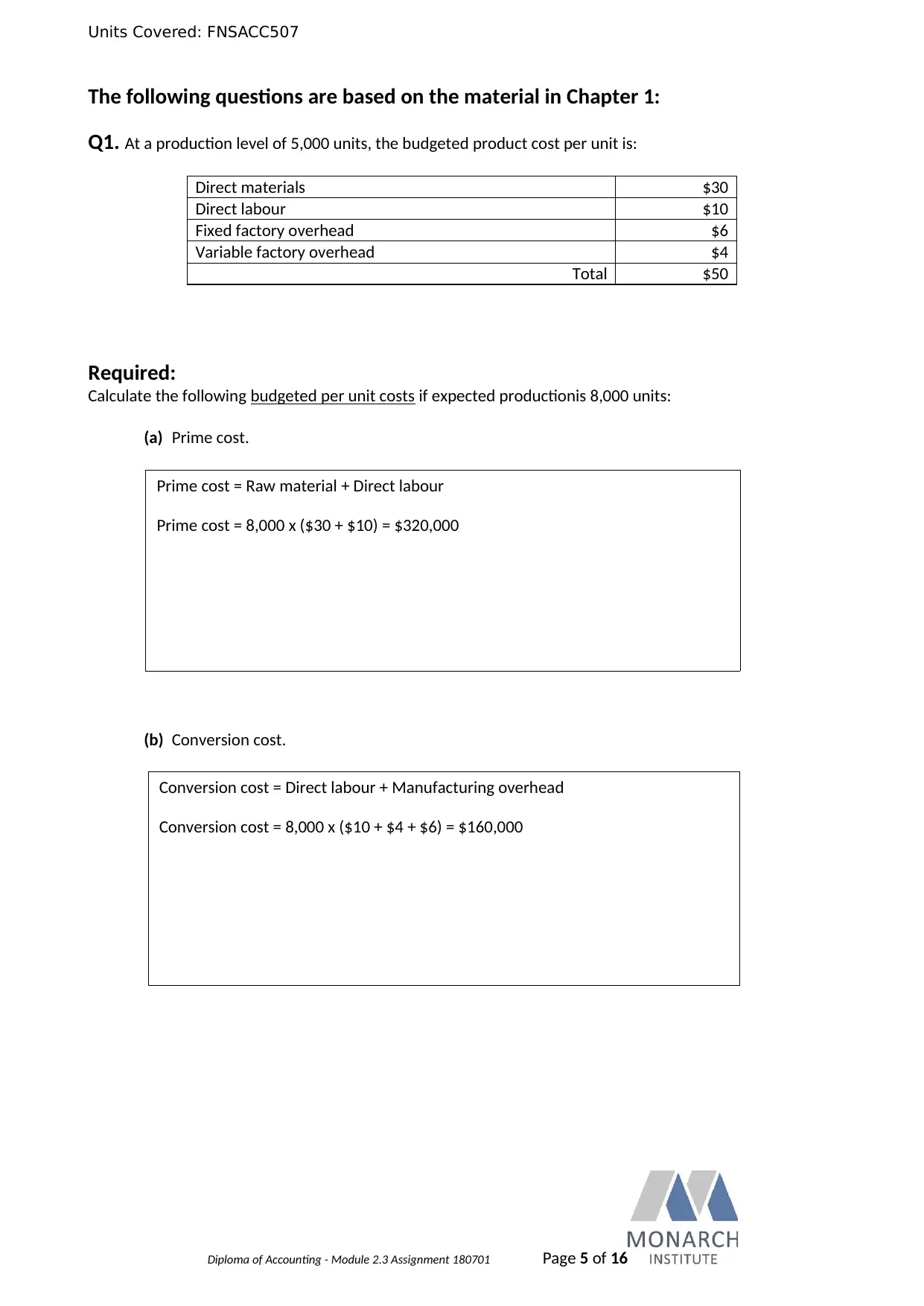

The following questions are based on the material in Chapter 1:

Q1. At a production level of 5,000 units, the budgeted product cost per unit is:

Direct materials $30

Direct labour $10

Fixed factory overhead $6

Variable factory overhead $4

Total $50

Required:

Calculate the following budgeted per unit costs if expected productionis 8,000 units:

(a) Prime cost.

(b) Conversion cost.

Diploma of Accounting - Module 2.3 Assignment 180701 Page 5 of 16

Conversion cost = Direct labour + Manufacturing overhead

Conversion cost = 8,000 x ($10 + $4 + $6) = $160,000

Prime cost = Raw material + Direct labour

Prime cost = 8,000 x ($30 + $10) = $320,000

The following questions are based on the material in Chapter 1:

Q1. At a production level of 5,000 units, the budgeted product cost per unit is:

Direct materials $30

Direct labour $10

Fixed factory overhead $6

Variable factory overhead $4

Total $50

Required:

Calculate the following budgeted per unit costs if expected productionis 8,000 units:

(a) Prime cost.

(b) Conversion cost.

Diploma of Accounting - Module 2.3 Assignment 180701 Page 5 of 16

Conversion cost = Direct labour + Manufacturing overhead

Conversion cost = 8,000 x ($10 + $4 + $6) = $160,000

Prime cost = Raw material + Direct labour

Prime cost = 8,000 x ($30 + $10) = $320,000

Units Covered: FNSACC507

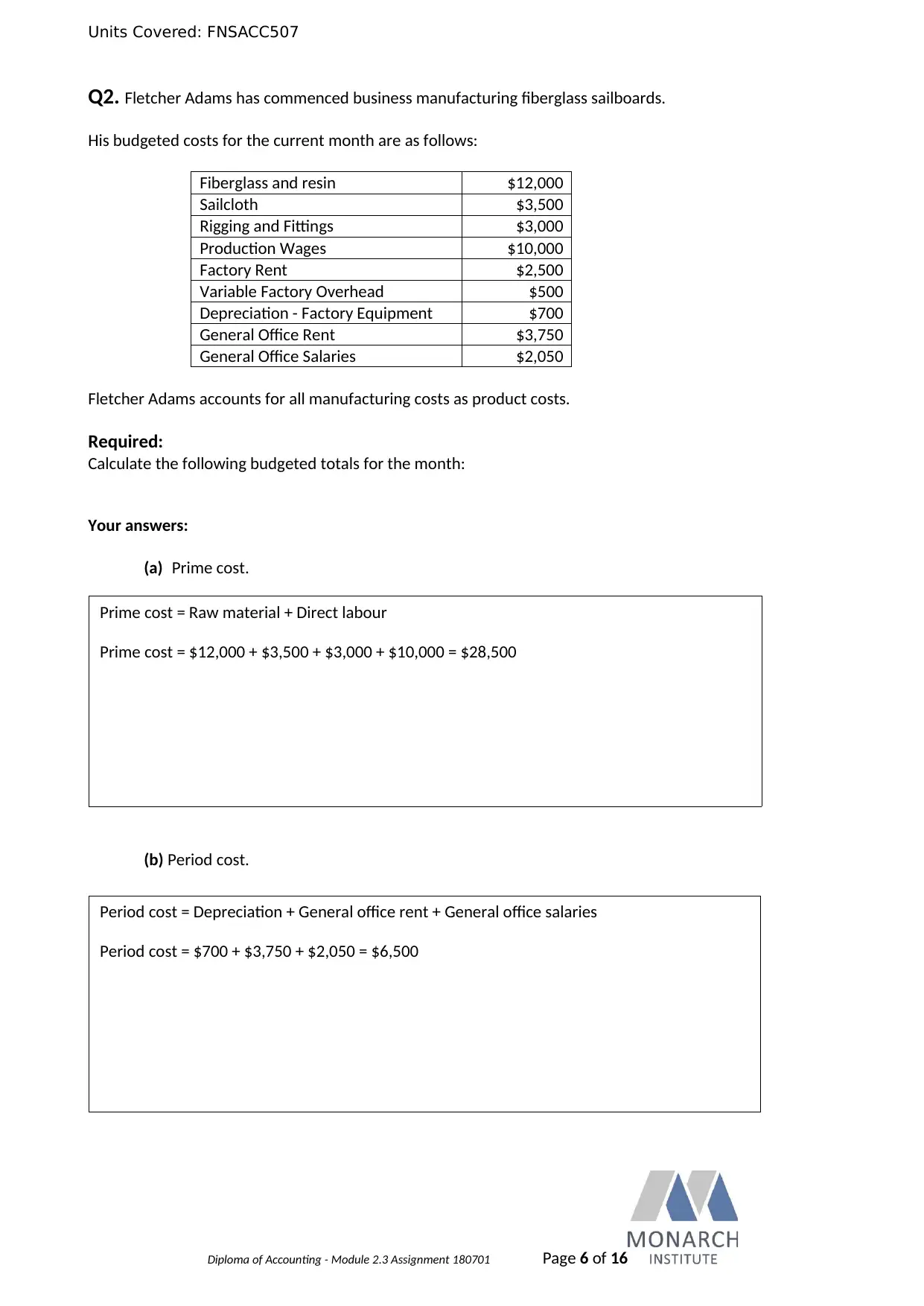

Q2. Fletcher Adams has commenced business manufacturing fiberglass sailboards.

His budgeted costs for the current month are as follows:

Fiberglass and resin $12,000

Sailcloth $3,500

Rigging and Fittings $3,000

Production Wages $10,000

Factory Rent $2,500

Variable Factory Overhead $500

Depreciation - Factory Equipment $700

General Office Rent $3,750

General Office Salaries $2,050

Fletcher Adams accounts for all manufacturing costs as product costs.

Required:

Calculate the following budgeted totals for the month:

Your answers:

(a) Prime cost.

(b) Period cost.

Diploma of Accounting - Module 2.3 Assignment 180701 Page 6 of 16

Prime cost = Raw material + Direct labour

Prime cost = $12,000 + $3,500 + $3,000 + $10,000 = $28,500

Period cost = Depreciation + General office rent + General office salaries

Period cost = $700 + $3,750 + $2,050 = $6,500

Q2. Fletcher Adams has commenced business manufacturing fiberglass sailboards.

His budgeted costs for the current month are as follows:

Fiberglass and resin $12,000

Sailcloth $3,500

Rigging and Fittings $3,000

Production Wages $10,000

Factory Rent $2,500

Variable Factory Overhead $500

Depreciation - Factory Equipment $700

General Office Rent $3,750

General Office Salaries $2,050

Fletcher Adams accounts for all manufacturing costs as product costs.

Required:

Calculate the following budgeted totals for the month:

Your answers:

(a) Prime cost.

(b) Period cost.

Diploma of Accounting - Module 2.3 Assignment 180701 Page 6 of 16

Prime cost = Raw material + Direct labour

Prime cost = $12,000 + $3,500 + $3,000 + $10,000 = $28,500

Period cost = Depreciation + General office rent + General office salaries

Period cost = $700 + $3,750 + $2,050 = $6,500

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Units Covered: FNSACC507

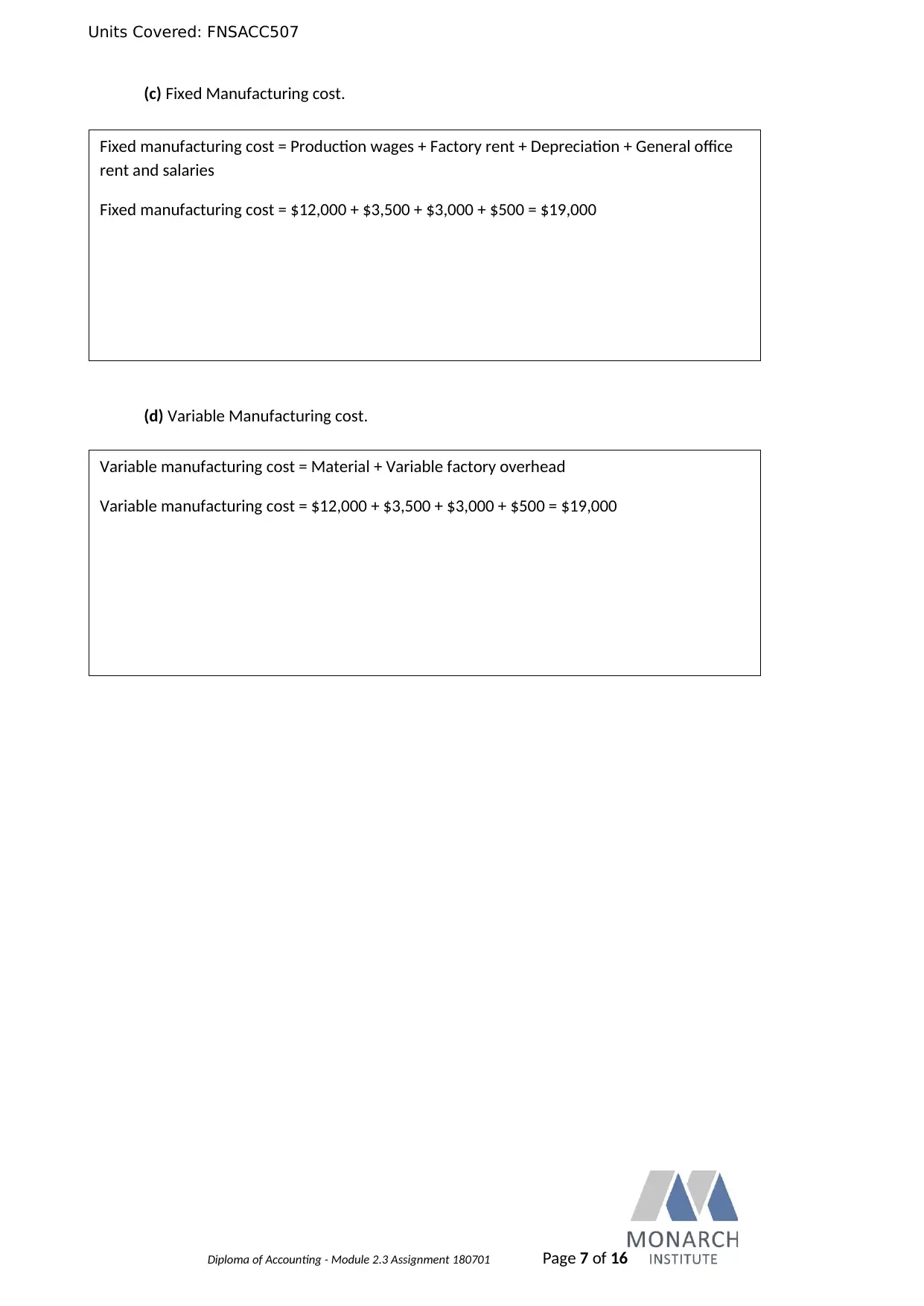

(c) Fixed Manufacturing cost.

(d) Variable Manufacturing cost.

Diploma of Accounting - Module 2.3 Assignment 180701 Page 7 of 16

Variable manufacturing cost = Material + Variable factory overhead

Variable manufacturing cost = $12,000 + $3,500 + $3,000 + $500 = $19,000

Fixed manufacturing cost = Production wages + Factory rent + Depreciation + General office

rent and salaries

Fixed manufacturing cost = $12,000 + $3,500 + $3,000 + $500 = $19,000

(c) Fixed Manufacturing cost.

(d) Variable Manufacturing cost.

Diploma of Accounting - Module 2.3 Assignment 180701 Page 7 of 16

Variable manufacturing cost = Material + Variable factory overhead

Variable manufacturing cost = $12,000 + $3,500 + $3,000 + $500 = $19,000

Fixed manufacturing cost = Production wages + Factory rent + Depreciation + General office

rent and salaries

Fixed manufacturing cost = $12,000 + $3,500 + $3,000 + $500 = $19,000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Units Covered: FNSACC507

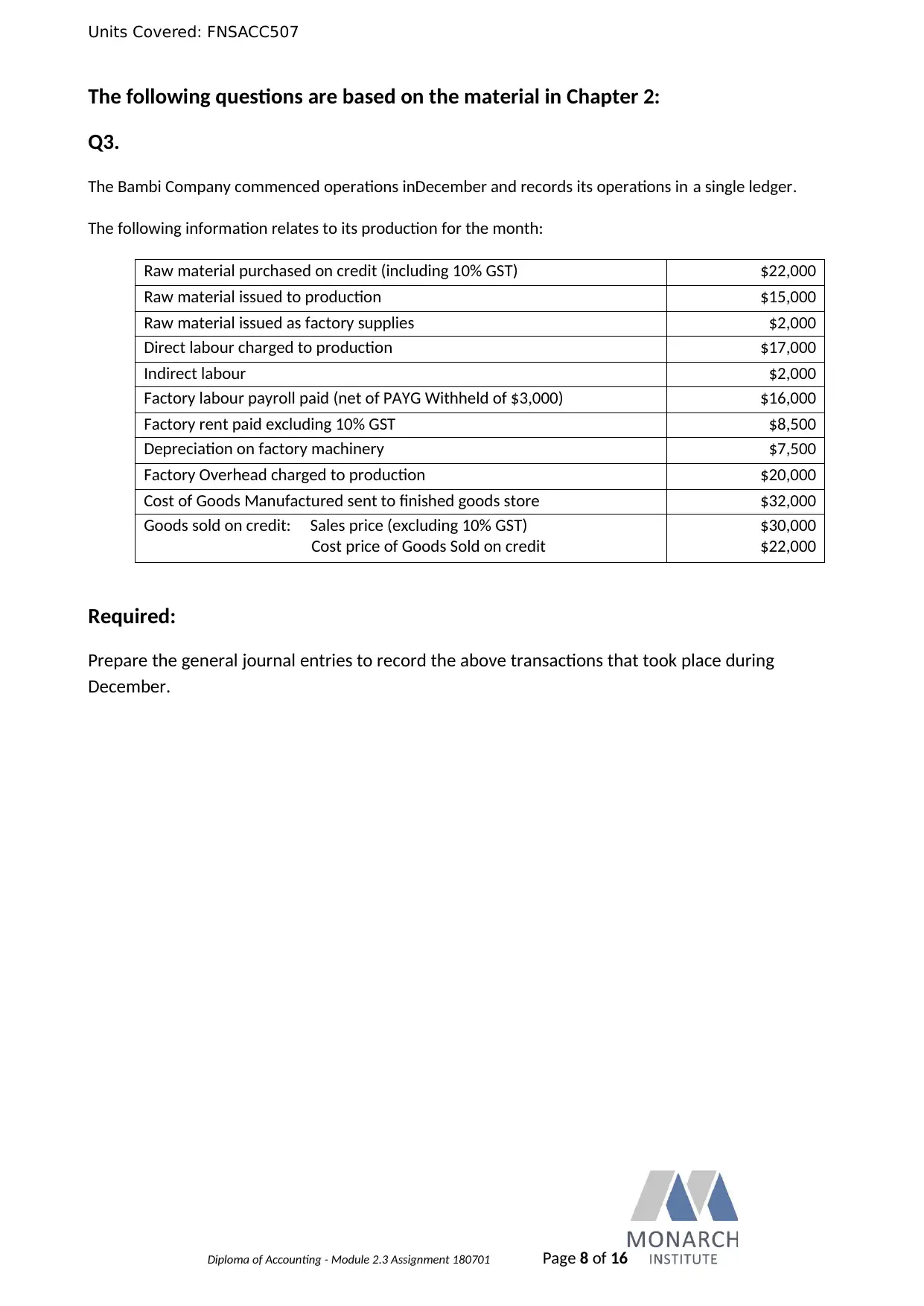

The following questions are based on the material in Chapter 2:

Q3.

The Bambi Company commenced operations inDecember and records its operations in a single ledger.

The following information relates to its production for the month:

Raw material purchased on credit (including 10% GST) $22,000

Raw material issued to production $15,000

Raw material issued as factory supplies $2,000

Direct labour charged to production $17,000

Indirect labour $2,000

Factory labour payroll paid (net of PAYG Withheld of $3,000) $16,000

Factory rent paid excluding 10% GST $8,500

Depreciation on factory machinery $7,500

Factory Overhead charged to production $20,000

Cost of Goods Manufactured sent to finished goods store $32,000

Goods sold on credit: Sales price (excluding 10% GST)

Cost price of Goods Sold on credit

$30,000

$22,000

Required:

Prepare the general journal entries to record the above transactions that took place during

December.

Diploma of Accounting - Module 2.3 Assignment 180701 Page 8 of 16

The following questions are based on the material in Chapter 2:

Q3.

The Bambi Company commenced operations inDecember and records its operations in a single ledger.

The following information relates to its production for the month:

Raw material purchased on credit (including 10% GST) $22,000

Raw material issued to production $15,000

Raw material issued as factory supplies $2,000

Direct labour charged to production $17,000

Indirect labour $2,000

Factory labour payroll paid (net of PAYG Withheld of $3,000) $16,000

Factory rent paid excluding 10% GST $8,500

Depreciation on factory machinery $7,500

Factory Overhead charged to production $20,000

Cost of Goods Manufactured sent to finished goods store $32,000

Goods sold on credit: Sales price (excluding 10% GST)

Cost price of Goods Sold on credit

$30,000

$22,000

Required:

Prepare the general journal entries to record the above transactions that took place during

December.

Diploma of Accounting - Module 2.3 Assignment 180701 Page 8 of 16

Units Covered: FNSACC507

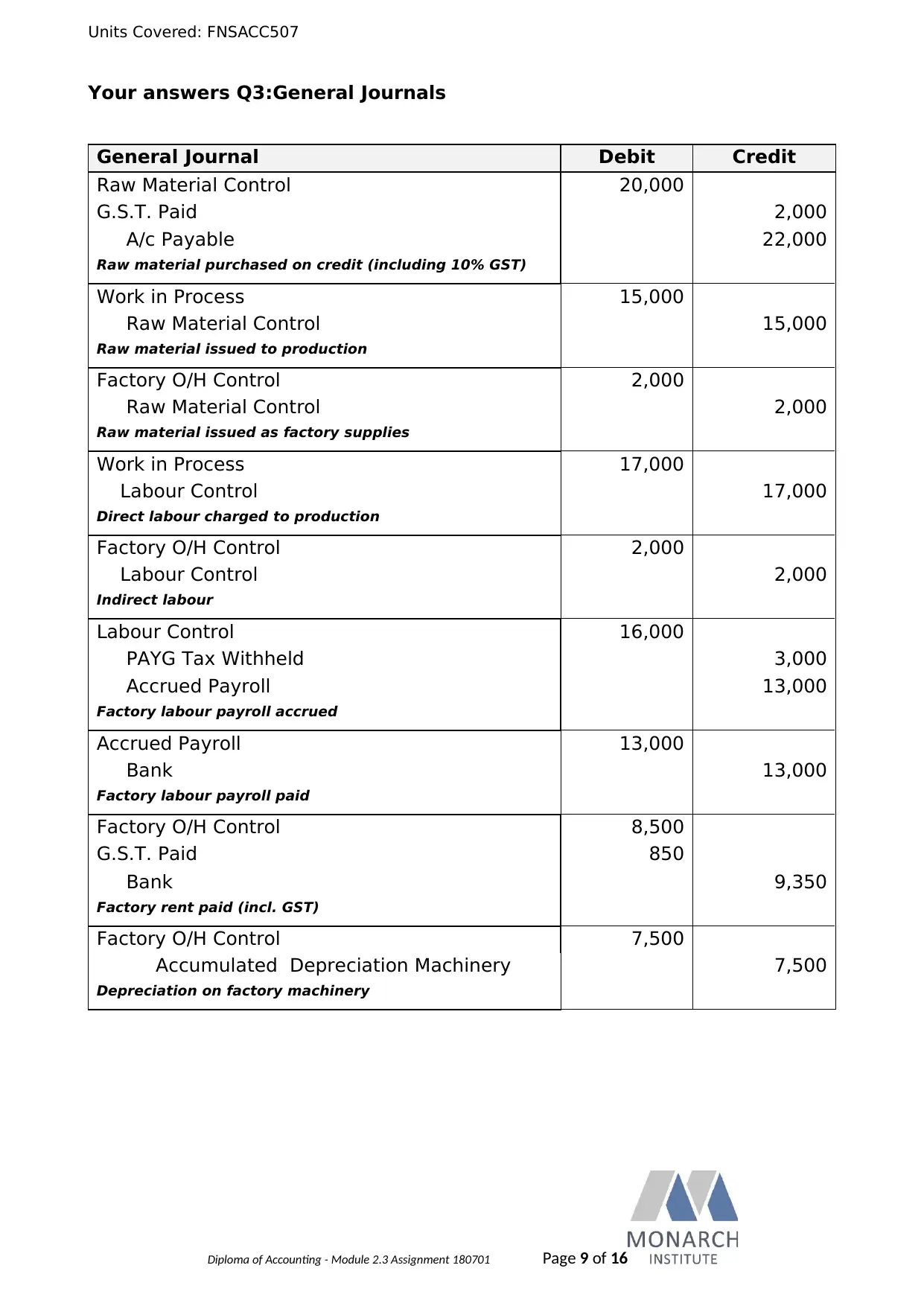

Your answers Q3:General Journals

General Journal Debit Credit

Raw Material Control 20,000

G.S.T. Paid 2,000

A/c Payable 22,000

Raw material purchased on credit (including 10% GST)

Work in Process 15,000

Raw Material Control 15,000

Raw material issued to production

Factory O/H Control 2,000

Raw Material Control 2,000

Raw material issued as factory supplies

Work in Process 17,000

Labour Control 17,000

Direct labour charged to production

Factory O/H Control 2,000

Labour Control 2,000

Indirect labour

Labour Control 16,000

PAYG Tax Withheld 3,000

Accrued Payroll 13,000

Factory labour payroll accrued

Accrued Payroll 13,000

Bank 13,000

Factory labour payroll paid

Factory O/H Control 8,500

G.S.T. Paid 850

Bank 9,350

Factory rent paid (incl. GST)

Factory O/H Control 7,500

Accumulated Depreciation Machinery 7,500

Depreciation on factory machinery

Diploma of Accounting - Module 2.3 Assignment 180701 Page 9 of 16

Your answers Q3:General Journals

General Journal Debit Credit

Raw Material Control 20,000

G.S.T. Paid 2,000

A/c Payable 22,000

Raw material purchased on credit (including 10% GST)

Work in Process 15,000

Raw Material Control 15,000

Raw material issued to production

Factory O/H Control 2,000

Raw Material Control 2,000

Raw material issued as factory supplies

Work in Process 17,000

Labour Control 17,000

Direct labour charged to production

Factory O/H Control 2,000

Labour Control 2,000

Indirect labour

Labour Control 16,000

PAYG Tax Withheld 3,000

Accrued Payroll 13,000

Factory labour payroll accrued

Accrued Payroll 13,000

Bank 13,000

Factory labour payroll paid

Factory O/H Control 8,500

G.S.T. Paid 850

Bank 9,350

Factory rent paid (incl. GST)

Factory O/H Control 7,500

Accumulated Depreciation Machinery 7,500

Depreciation on factory machinery

Diploma of Accounting - Module 2.3 Assignment 180701 Page 9 of 16

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Units Covered: FNSACC507

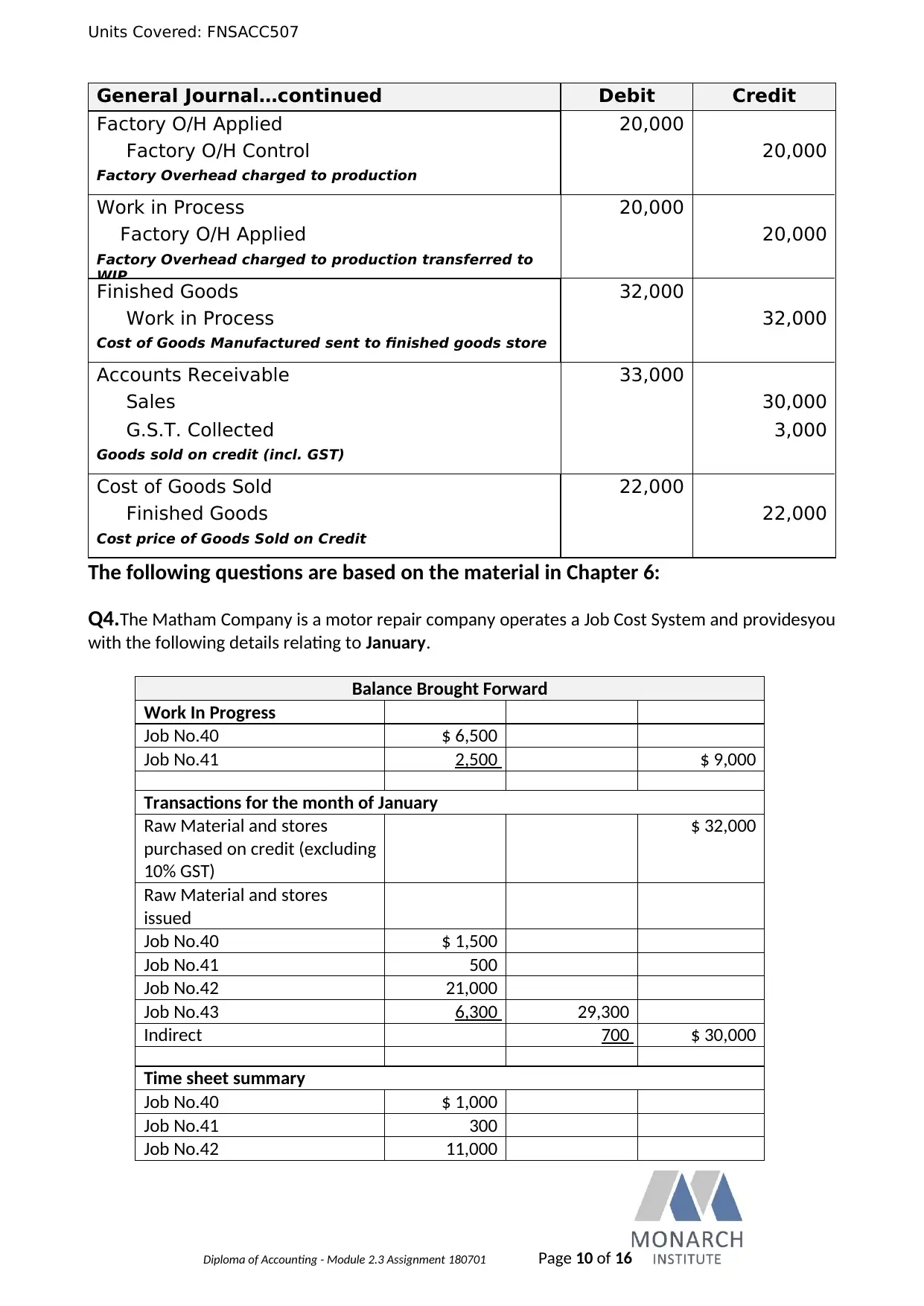

General Journal…continued Debit Credit

Factory O/H Applied 20,000

Factory O/H Control 20,000

Factory Overhead charged to production

Work in Process 20,000

Factory O/H Applied 20,000

Factory Overhead charged to production transferred to

WIP

Finished Goods 32,000

Work in Process 32,000

Cost of Goods Manufactured sent to finished goods store

Accounts Receivable 33,000

Sales 30,000

G.S.T. Collected 3,000

Goods sold on credit (incl. GST)

Cost of Goods Sold 22,000

Finished Goods 22,000

Cost price of Goods Sold on Credit

The following questions are based on the material in Chapter 6:

Q4.The Matham Company is a motor repair company operates a Job Cost System and providesyou

with the following details relating to January.

Balance Brought Forward

Work In Progress

Job No.40 $ 6,500

Job No.41 2,500 $ 9,000

Transactions for the month of January

Raw Material and stores

purchased on credit (excluding

10% GST)

$ 32,000

Raw Material and stores

issued

Job No.40 $ 1,500

Job No.41 500

Job No.42 21,000

Job No.43 6,300 29,300

Indirect 700 $ 30,000

Time sheet summary

Job No.40 $ 1,000

Job No.41 300

Job No.42 11,000

Diploma of Accounting - Module 2.3 Assignment 180701 Page 10 of 16

General Journal…continued Debit Credit

Factory O/H Applied 20,000

Factory O/H Control 20,000

Factory Overhead charged to production

Work in Process 20,000

Factory O/H Applied 20,000

Factory Overhead charged to production transferred to

WIP

Finished Goods 32,000

Work in Process 32,000

Cost of Goods Manufactured sent to finished goods store

Accounts Receivable 33,000

Sales 30,000

G.S.T. Collected 3,000

Goods sold on credit (incl. GST)

Cost of Goods Sold 22,000

Finished Goods 22,000

Cost price of Goods Sold on Credit

The following questions are based on the material in Chapter 6:

Q4.The Matham Company is a motor repair company operates a Job Cost System and providesyou

with the following details relating to January.

Balance Brought Forward

Work In Progress

Job No.40 $ 6,500

Job No.41 2,500 $ 9,000

Transactions for the month of January

Raw Material and stores

purchased on credit (excluding

10% GST)

$ 32,000

Raw Material and stores

issued

Job No.40 $ 1,500

Job No.41 500

Job No.42 21,000

Job No.43 6,300 29,300

Indirect 700 $ 30,000

Time sheet summary

Job No.40 $ 1,000

Job No.41 300

Job No.42 11,000

Diploma of Accounting - Module 2.3 Assignment 180701 Page 10 of 16

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Units Covered: FNSACC507

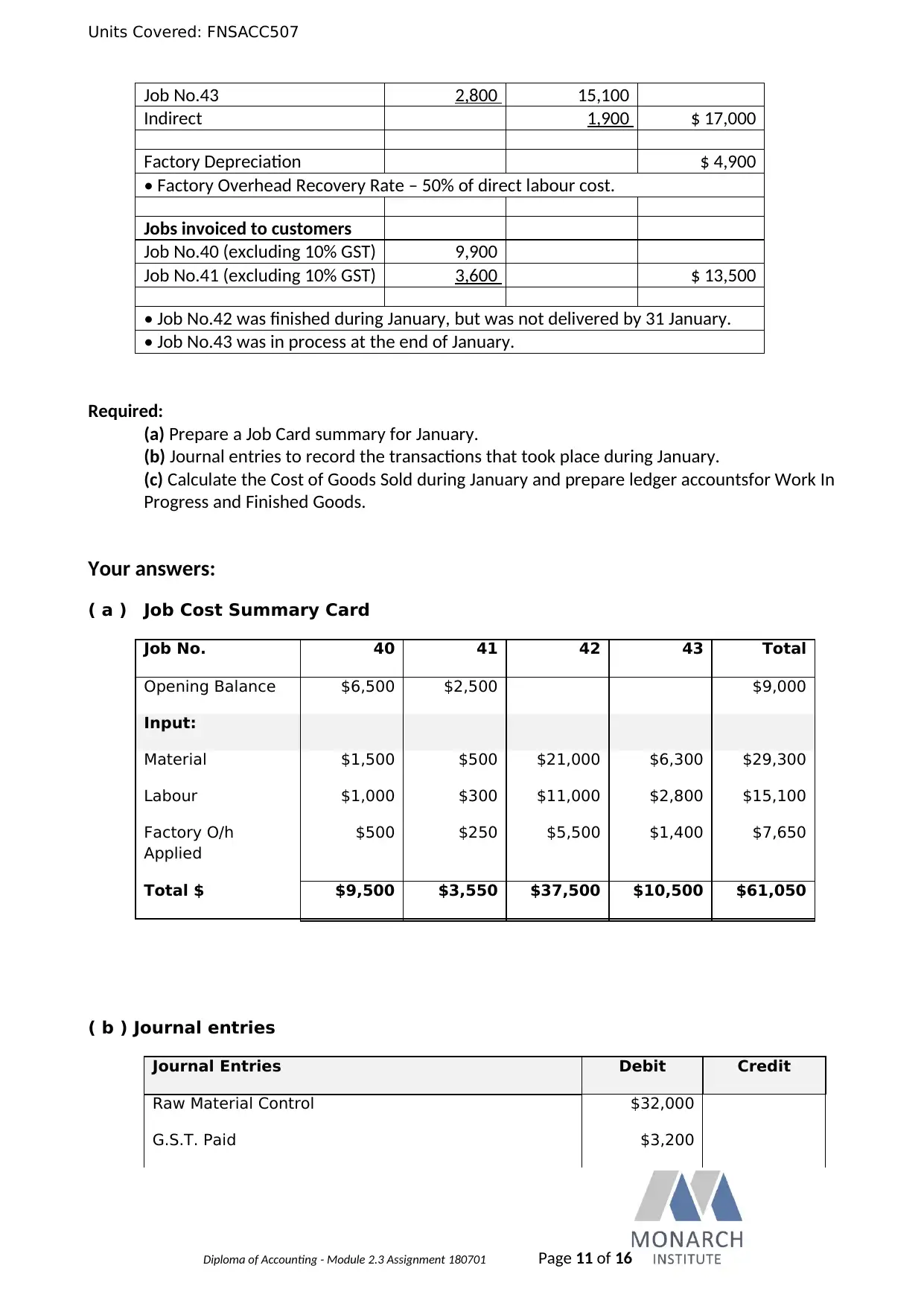

Job No.43 2,800 15,100

Indirect 1,900 $ 17,000

Factory Depreciation $ 4,900

• Factory Overhead Recovery Rate – 50% of direct labour cost.

Jobs invoiced to customers

Job No.40 (excluding 10% GST) 9,900

Job No.41 (excluding 10% GST) 3,600 $ 13,500

• Job No.42 was finished during January, but was not delivered by 31 January.

• Job No.43 was in process at the end of January.

Required:

(a) Prepare a Job Card summary for January.

(b) Journal entries to record the transactions that took place during January.

(c) Calculate the Cost of Goods Sold during January and prepare ledger accountsfor Work In

Progress and Finished Goods.

Your answers:

( a ) Job Cost Summary Card

Job No. 40 41 42 43 Total

Opening Balance $6,500 $2,500 $9,000

Input:

Material $1,500 $500 $21,000 $6,300 $29,300

Labour $1,000 $300 $11,000 $2,800 $15,100

Factory O/h

Applied

$500 $250 $5,500 $1,400 $7,650

Total $ $9,500 $3,550 $37,500 $10,500 $61,050

( b ) Journal entries

Journal Entries Debit Credit

Raw Material Control $32,000

G.S.T. Paid $3,200

Diploma of Accounting - Module 2.3 Assignment 180701 Page 11 of 16

Job No.43 2,800 15,100

Indirect 1,900 $ 17,000

Factory Depreciation $ 4,900

• Factory Overhead Recovery Rate – 50% of direct labour cost.

Jobs invoiced to customers

Job No.40 (excluding 10% GST) 9,900

Job No.41 (excluding 10% GST) 3,600 $ 13,500

• Job No.42 was finished during January, but was not delivered by 31 January.

• Job No.43 was in process at the end of January.

Required:

(a) Prepare a Job Card summary for January.

(b) Journal entries to record the transactions that took place during January.

(c) Calculate the Cost of Goods Sold during January and prepare ledger accountsfor Work In

Progress and Finished Goods.

Your answers:

( a ) Job Cost Summary Card

Job No. 40 41 42 43 Total

Opening Balance $6,500 $2,500 $9,000

Input:

Material $1,500 $500 $21,000 $6,300 $29,300

Labour $1,000 $300 $11,000 $2,800 $15,100

Factory O/h

Applied

$500 $250 $5,500 $1,400 $7,650

Total $ $9,500 $3,550 $37,500 $10,500 $61,050

( b ) Journal entries

Journal Entries Debit Credit

Raw Material Control $32,000

G.S.T. Paid $3,200

Diploma of Accounting - Module 2.3 Assignment 180701 Page 11 of 16

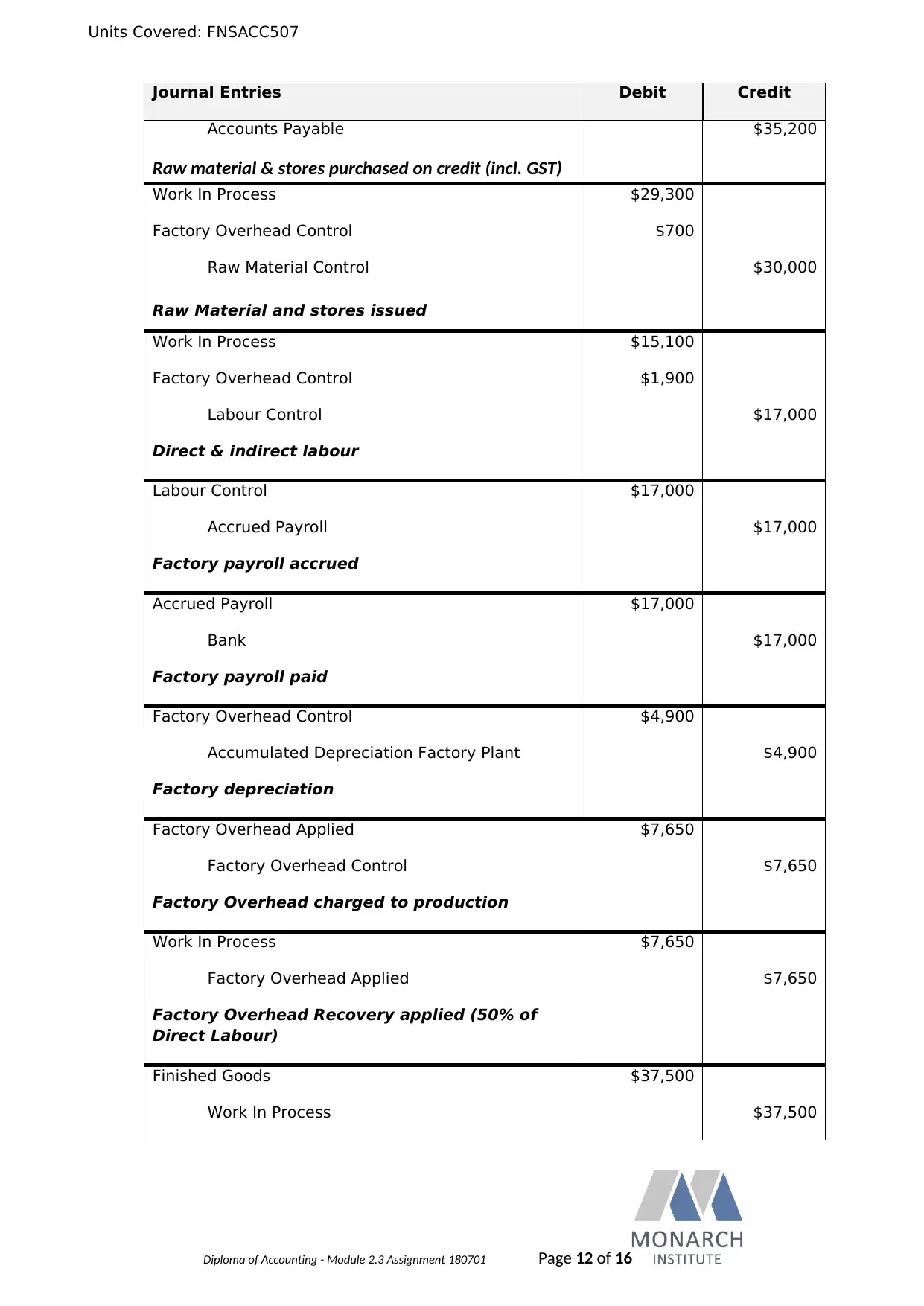

Units Covered: FNSACC507

Journal Entries Debit Credit

Accounts Payable $35,200

Raw material & stores purchased on credit (incl. GST)

Work In Process $29,300

Factory Overhead Control $700

Raw Material Control $30,000

Raw Material and stores issued

Work In Process $15,100

Factory Overhead Control $1,900

Labour Control $17,000

Direct & indirect labour

Labour Control $17,000

Accrued Payroll $17,000

Factory payroll accrued

Accrued Payroll $17,000

Bank $17,000

Factory payroll paid

Factory Overhead Control $4,900

Accumulated Depreciation Factory Plant $4,900

Factory depreciation

Factory Overhead Applied $7,650

Factory Overhead Control $7,650

Factory Overhead charged to production

Work In Process $7,650

Factory Overhead Applied $7,650

Factory Overhead Recovery applied (50% of

Direct Labour)

Finished Goods $37,500

Work In Process $37,500

Diploma of Accounting - Module 2.3 Assignment 180701 Page 12 of 16

Journal Entries Debit Credit

Accounts Payable $35,200

Raw material & stores purchased on credit (incl. GST)

Work In Process $29,300

Factory Overhead Control $700

Raw Material Control $30,000

Raw Material and stores issued

Work In Process $15,100

Factory Overhead Control $1,900

Labour Control $17,000

Direct & indirect labour

Labour Control $17,000

Accrued Payroll $17,000

Factory payroll accrued

Accrued Payroll $17,000

Bank $17,000

Factory payroll paid

Factory Overhead Control $4,900

Accumulated Depreciation Factory Plant $4,900

Factory depreciation

Factory Overhead Applied $7,650

Factory Overhead Control $7,650

Factory Overhead charged to production

Work In Process $7,650

Factory Overhead Applied $7,650

Factory Overhead Recovery applied (50% of

Direct Labour)

Finished Goods $37,500

Work In Process $37,500

Diploma of Accounting - Module 2.3 Assignment 180701 Page 12 of 16

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.