Self-Assessed Exercises: Superannuation and SMSF Workbook for Monarch

VerifiedAdded on 2020/03/02

|45

|4842

|475

Homework Assignment

AI Summary

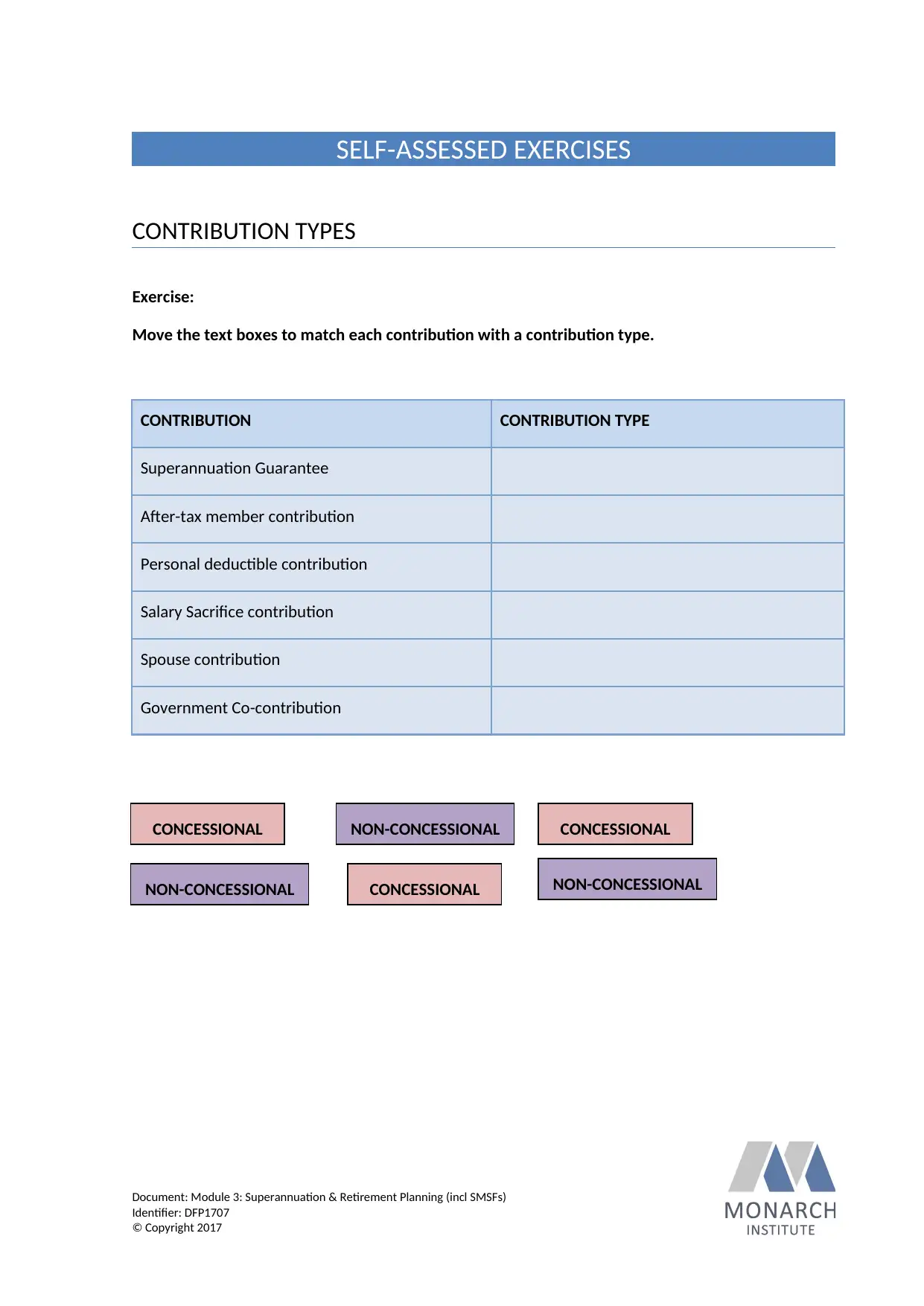

This workbook presents a series of self-assessed exercises designed to enhance understanding of key superannuation and SMSF concepts. It covers a range of topics including contribution types (Superannuation Guarantee, salary sacrifice, etc.), contribution caps, and eligibility criteria. Exercises involve matching contribution types, applying cap limits to various scenarios, determining eligibility to contribute, calculating superannuation guarantee and government co-contributions, and calculating tax rebates for spouse contributions. Furthermore, it delves into salary sacrifice calculations, earnings tax, franking credits, conditions of release, benefit components, and withdrawal tax implications. The workbook includes detailed calculations and scenarios to illustrate practical applications of superannuation rules and regulations, and also incorporates SMSF specific topics. The solution is provided for self-assessment.

1 out of 45

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.