Assessment Summary Sheet for FNSACC301

VerifiedAdded on 2023/06/10

|21

|4759

|388

AI Summary

This assessment tool is for FNSACC301 - Process Financial Transactions and Extract Interim Reports. It includes a cover sheet, assessment/evidence gathering conditions, resources required, instructions for students, procedures and specifications of the assessment, and assessment 2 which includes case analysis, posting to general journal, and short answer questions.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Assessment Summary Sheet

This form is to be completed by the assessor and used a final record of student competency.

All student submissions including any associated checklists (outlined below) are to be attached to this cover sheet

before placing on the students file.

Student results are not to be entered onto the Student Database unless all relevant paperwork is completed and

attached to this form.

Student Name:

Student ID No:

Final Completion Date:

Unit Code: FNSACC301

Unit Title: Process Financial Transactions and Extract Interim Reports

Please attach the following documentation to this form Result

Assessment Week 1 Research, analysis and short questions S / NYS / DNS

Assessment Week 2 Case Analysis and written response S / NYS / DNS

Final Assessment Result for this unit C / NYC

Feedback is given to the student on each Assessment task Yes / No

Feedback is given to the student on final outcome of the unit Yes / No

Student Declaration I have been assessed in a fair and

flexible manner. I understand that the Elite Education

Vocation Institute’s Student Assessment, Reassessment

and Repeating Units of Competency Guidelines apply to

these assessment tasks.

Assessor Declaration: I declare that I have conducted a

fair, valid, reliable and flexible assessment with this student,

and I have provided appropriate feedback.

Name: Name:

Signature: Signature:

Date: Date:

V2017.T4. 1.0

FNS50215 Diploma of Accounting/ FNSACC301/ 2017/ T4/ Assessment Tool Page 1 of 21

This form is to be completed by the assessor and used a final record of student competency.

All student submissions including any associated checklists (outlined below) are to be attached to this cover sheet

before placing on the students file.

Student results are not to be entered onto the Student Database unless all relevant paperwork is completed and

attached to this form.

Student Name:

Student ID No:

Final Completion Date:

Unit Code: FNSACC301

Unit Title: Process Financial Transactions and Extract Interim Reports

Please attach the following documentation to this form Result

Assessment Week 1 Research, analysis and short questions S / NYS / DNS

Assessment Week 2 Case Analysis and written response S / NYS / DNS

Final Assessment Result for this unit C / NYC

Feedback is given to the student on each Assessment task Yes / No

Feedback is given to the student on final outcome of the unit Yes / No

Student Declaration I have been assessed in a fair and

flexible manner. I understand that the Elite Education

Vocation Institute’s Student Assessment, Reassessment

and Repeating Units of Competency Guidelines apply to

these assessment tasks.

Assessor Declaration: I declare that I have conducted a

fair, valid, reliable and flexible assessment with this student,

and I have provided appropriate feedback.

Name: Name:

Signature: Signature:

Date: Date:

V2017.T4. 1.0

FNS50215 Diploma of Accounting/ FNSACC301/ 2017/ T4/ Assessment Tool Page 1 of 21

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Assessment Cover Sheet

Assessment Week Two Details

Term and Year Term 4 2017

Assessment Type Case Analysis and written response

Due Date Class Room

Student Name:

Student ID No:

Date:

Qualification : FNS50215 Diploma of Accounting

Unit Code: FNSACC301

Unit Title: Process Financial Transactions and Extract Interim Reports

Assessor’s Name Ada DU

Student Declaration: I declare that this work has been

completed by me honestly and with integrity. I understand

that the Elite Education Vocation Institute’s Student

Assessment, Reassessment and Repeating Units of

Competency Guidelines apply to these assessment tasks.

Assessor Declaration: I declare that I have conducted a

fair, valid, reliable and flexible assessment with this student,

and I have provided appropriate feedback.

Name: Name:

Signature: Signature:

Date: Date:

Student was absent from the feedback session.

V2017.T4. 1.0

FNS50215 Diploma of Accounting/ FNSACC301/ 2017/ T4/ Assessment Tool Page 2 of 21

Assessment Week Two Details

Term and Year Term 4 2017

Assessment Type Case Analysis and written response

Due Date Class Room

Student Name:

Student ID No:

Date:

Qualification : FNS50215 Diploma of Accounting

Unit Code: FNSACC301

Unit Title: Process Financial Transactions and Extract Interim Reports

Assessor’s Name Ada DU

Student Declaration: I declare that this work has been

completed by me honestly and with integrity. I understand

that the Elite Education Vocation Institute’s Student

Assessment, Reassessment and Repeating Units of

Competency Guidelines apply to these assessment tasks.

Assessor Declaration: I declare that I have conducted a

fair, valid, reliable and flexible assessment with this student,

and I have provided appropriate feedback.

Name: Name:

Signature: Signature:

Date: Date:

Student was absent from the feedback session.

V2017.T4. 1.0

FNS50215 Diploma of Accounting/ FNSACC301/ 2017/ T4/ Assessment Tool Page 2 of 21

Assessment/evidence gathering conditions

Each assessment component is recorded as either Satisfactory (S) or Not Yet Satisfactory (NYS). A student can only

achieve competence when all assessment components listed under procedures and specifications of the assessment

section are Satisfactory. Your trainer will give you feedback after the completion of each assessment. A student who is

assessed as NYS is eligible for re-assessment. Should the student fail to submit the assessment, a result outcome of Did

Not Submit (DNS) will be recorded.

Principles of Assessment

Based on Clauses 1.8 – 1.12 from the Australian Standards Quality Assurance’s (ASQA) Standards for Registered Training

Organizations (RTO) 2015, the learner would be assessed based on the following principles:

Fairness - (1) the individual learner’s needs are considered in the assessment process, (2) where appropriate, reasonable

adjustments are applied by the RTO to take into account the individual leaner’s needs and, (3) the RTO informs

the leaner about the assessment process, and provides the learner with the opportunity to challenge the result

of the assessment and be reassessed if necessary.

Flexibility – assessment is flexible to the individual learner by; (1) reflecting the learner’s needs, (2) assessing competencies

held by the learner no matter how or where they have been acquired and, (3) the unit of competency and

associated assessment requirements, and the individual.

Validity – (1) requires that assessment against the unit/s of competency and the associated assessment requirements

covers the broad range of skills and knowledge, (2) assessment of knowledge and skills is integrated with their

practical application, (3) assessment to be based on evidence that demonstrates tat a leaner could

demonstrate these skills and knowledge in other similar situations and, (4) judgement of competence is based

on evidence of learner performance that is aligned to the unit/s of competency and associated assessment

requirements.

Reliability – evidence presented for assessment is consistently interpreted and assessment results are comparable

irrespective of the assessor conducting the assessment

Rules of Evidence

Validity – the assessor is assured that the learner has the skills, knowledge and attributes, as described in the module

of unit of competency and associated assessment requirements.

Sufficiency – the assessor is assured that the quality, quantity and relevance of the assessment evidence enables a

judgement to be made of a learner’s competency.

Authenticity – the assessor is assured that the evidence presented for assessment is the learner’s own work. This would

mean that any form of plagiarism or copying of other’s work may not be permitted and would be deemed

strictly as a ‘Not Yet Competent’ grading.

Currency – the assessor is assured that the assessment evidence demonstrates current competency. This requires the

assessment evidence to be from the present or the very recent past.

V2017.T4. 1.0

FNS50215 Diploma of Accounting/ FNSACC301/ 2017/ T4/ Assessment Tool Page 3 of 21

Each assessment component is recorded as either Satisfactory (S) or Not Yet Satisfactory (NYS). A student can only

achieve competence when all assessment components listed under procedures and specifications of the assessment

section are Satisfactory. Your trainer will give you feedback after the completion of each assessment. A student who is

assessed as NYS is eligible for re-assessment. Should the student fail to submit the assessment, a result outcome of Did

Not Submit (DNS) will be recorded.

Principles of Assessment

Based on Clauses 1.8 – 1.12 from the Australian Standards Quality Assurance’s (ASQA) Standards for Registered Training

Organizations (RTO) 2015, the learner would be assessed based on the following principles:

Fairness - (1) the individual learner’s needs are considered in the assessment process, (2) where appropriate, reasonable

adjustments are applied by the RTO to take into account the individual leaner’s needs and, (3) the RTO informs

the leaner about the assessment process, and provides the learner with the opportunity to challenge the result

of the assessment and be reassessed if necessary.

Flexibility – assessment is flexible to the individual learner by; (1) reflecting the learner’s needs, (2) assessing competencies

held by the learner no matter how or where they have been acquired and, (3) the unit of competency and

associated assessment requirements, and the individual.

Validity – (1) requires that assessment against the unit/s of competency and the associated assessment requirements

covers the broad range of skills and knowledge, (2) assessment of knowledge and skills is integrated with their

practical application, (3) assessment to be based on evidence that demonstrates tat a leaner could

demonstrate these skills and knowledge in other similar situations and, (4) judgement of competence is based

on evidence of learner performance that is aligned to the unit/s of competency and associated assessment

requirements.

Reliability – evidence presented for assessment is consistently interpreted and assessment results are comparable

irrespective of the assessor conducting the assessment

Rules of Evidence

Validity – the assessor is assured that the learner has the skills, knowledge and attributes, as described in the module

of unit of competency and associated assessment requirements.

Sufficiency – the assessor is assured that the quality, quantity and relevance of the assessment evidence enables a

judgement to be made of a learner’s competency.

Authenticity – the assessor is assured that the evidence presented for assessment is the learner’s own work. This would

mean that any form of plagiarism or copying of other’s work may not be permitted and would be deemed

strictly as a ‘Not Yet Competent’ grading.

Currency – the assessor is assured that the assessment evidence demonstrates current competency. This requires the

assessment evidence to be from the present or the very recent past.

V2017.T4. 1.0

FNS50215 Diploma of Accounting/ FNSACC301/ 2017/ T4/ Assessment Tool Page 3 of 21

Resources required for this Assessment

All documents must be created using Microsoft Office suites i.e., MS Word, Excel, PowerPoint

Upon completion, submit the assessment via the student learning management system to your trainer along with the

completed assessment coversheet.

Refer the notes on eLearning to answer the tasks

Any additional material will be provided by Trainer

Instructions for Students

Please read the following instructions carefully

This assessment is to be completed according to the instructions given by your assessor.

Students are allowed to take this assessment home.

Feedback on each task will be provided to enable you to determine how your work could be improved. You will be

provided with feedback on your work within 2 weeks of the assessment due date.

Should you not answer the questions correctly, you will be given feedback on the results and your gaps in knowledge.

You will be given another opportunity to demonstrate your knowledge and skills to be deemed competent for this unit

of competency.

If you are not sure about any aspect of this assessment, please ask for clarification from your assessor.

Please refer to the College re-assessment and re-enrolment policy for more information.

Procedures and Specifications of the Assessment

To complete the unit requirements safely and effectively, the individual must:

Define international marketing

Identify international trade patterns

Explain international trade policies and agreements

Identify legislative requirements

V2017.T4. 1.0

FNS50215 Diploma of Accounting/ FNSACC301/ 2017/ T4/ Assessment Tool Page 4 of 21

All documents must be created using Microsoft Office suites i.e., MS Word, Excel, PowerPoint

Upon completion, submit the assessment via the student learning management system to your trainer along with the

completed assessment coversheet.

Refer the notes on eLearning to answer the tasks

Any additional material will be provided by Trainer

Instructions for Students

Please read the following instructions carefully

This assessment is to be completed according to the instructions given by your assessor.

Students are allowed to take this assessment home.

Feedback on each task will be provided to enable you to determine how your work could be improved. You will be

provided with feedback on your work within 2 weeks of the assessment due date.

Should you not answer the questions correctly, you will be given feedback on the results and your gaps in knowledge.

You will be given another opportunity to demonstrate your knowledge and skills to be deemed competent for this unit

of competency.

If you are not sure about any aspect of this assessment, please ask for clarification from your assessor.

Please refer to the College re-assessment and re-enrolment policy for more information.

Procedures and Specifications of the Assessment

To complete the unit requirements safely and effectively, the individual must:

Define international marketing

Identify international trade patterns

Explain international trade policies and agreements

Identify legislative requirements

V2017.T4. 1.0

FNS50215 Diploma of Accounting/ FNSACC301/ 2017/ T4/ Assessment Tool Page 4 of 21

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

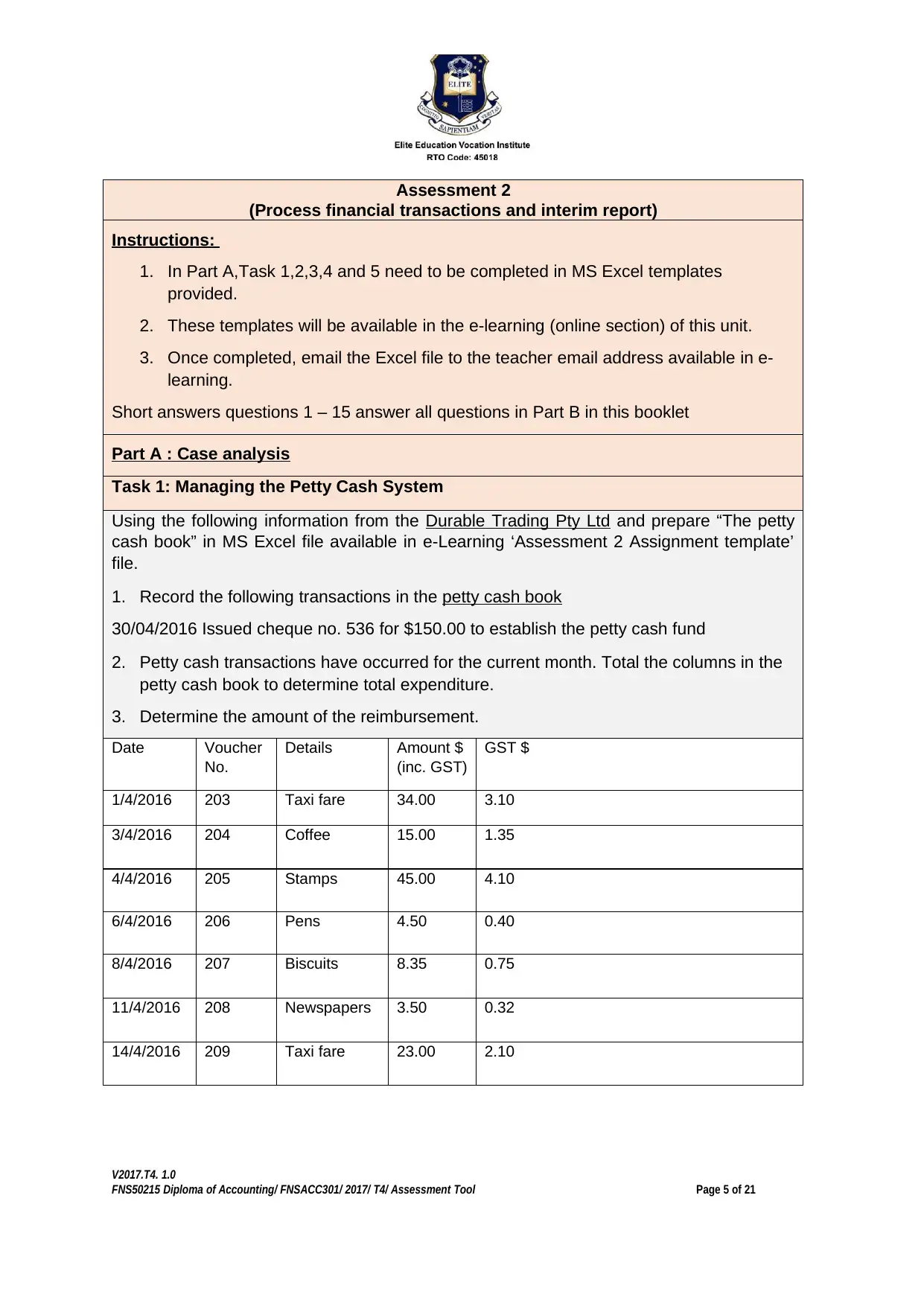

Assessment 2

(Process financial transactions and interim report)

Instructions:

1. In Part A,Task 1,2,3,4 and 5 need to be completed in MS Excel templates

provided.

2. These templates will be available in the e-learning (online section) of this unit.

3. Once completed, email the Excel file to the teacher email address available in e-

learning.

Short answers questions 1 – 15 answer all questions in Part B in this booklet

Part A : Case analysis

Task 1: Managing the Petty Cash System

Using the following information from the Durable Trading Pty Ltd and prepare “The petty

cash book” in MS Excel file available in e-Learning ‘Assessment 2 Assignment template’

file.

1. Record the following transactions in the petty cash book

30/04/2016 Issued cheque no. 536 for $150.00 to establish the petty cash fund

2. Petty cash transactions have occurred for the current month. Total the columns in the

petty cash book to determine total expenditure.

3. Determine the amount of the reimbursement.

Date Voucher

No.

Details Amount $

(inc. GST)

GST $

1/4/2016 203 Taxi fare 34.00 3.10

3/4/2016 204 Coffee 15.00 1.35

4/4/2016 205 Stamps 45.00 4.10

6/4/2016 206 Pens 4.50 0.40

8/4/2016 207 Biscuits 8.35 0.75

11/4/2016 208 Newspapers 3.50 0.32

14/4/2016 209 Taxi fare 23.00 2.10

V2017.T4. 1.0

FNS50215 Diploma of Accounting/ FNSACC301/ 2017/ T4/ Assessment Tool Page 5 of 21

(Process financial transactions and interim report)

Instructions:

1. In Part A,Task 1,2,3,4 and 5 need to be completed in MS Excel templates

provided.

2. These templates will be available in the e-learning (online section) of this unit.

3. Once completed, email the Excel file to the teacher email address available in e-

learning.

Short answers questions 1 – 15 answer all questions in Part B in this booklet

Part A : Case analysis

Task 1: Managing the Petty Cash System

Using the following information from the Durable Trading Pty Ltd and prepare “The petty

cash book” in MS Excel file available in e-Learning ‘Assessment 2 Assignment template’

file.

1. Record the following transactions in the petty cash book

30/04/2016 Issued cheque no. 536 for $150.00 to establish the petty cash fund

2. Petty cash transactions have occurred for the current month. Total the columns in the

petty cash book to determine total expenditure.

3. Determine the amount of the reimbursement.

Date Voucher

No.

Details Amount $

(inc. GST)

GST $

1/4/2016 203 Taxi fare 34.00 3.10

3/4/2016 204 Coffee 15.00 1.35

4/4/2016 205 Stamps 45.00 4.10

6/4/2016 206 Pens 4.50 0.40

8/4/2016 207 Biscuits 8.35 0.75

11/4/2016 208 Newspapers 3.50 0.32

14/4/2016 209 Taxi fare 23.00 2.10

V2017.T4. 1.0

FNS50215 Diploma of Accounting/ FNSACC301/ 2017/ T4/ Assessment Tool Page 5 of 21

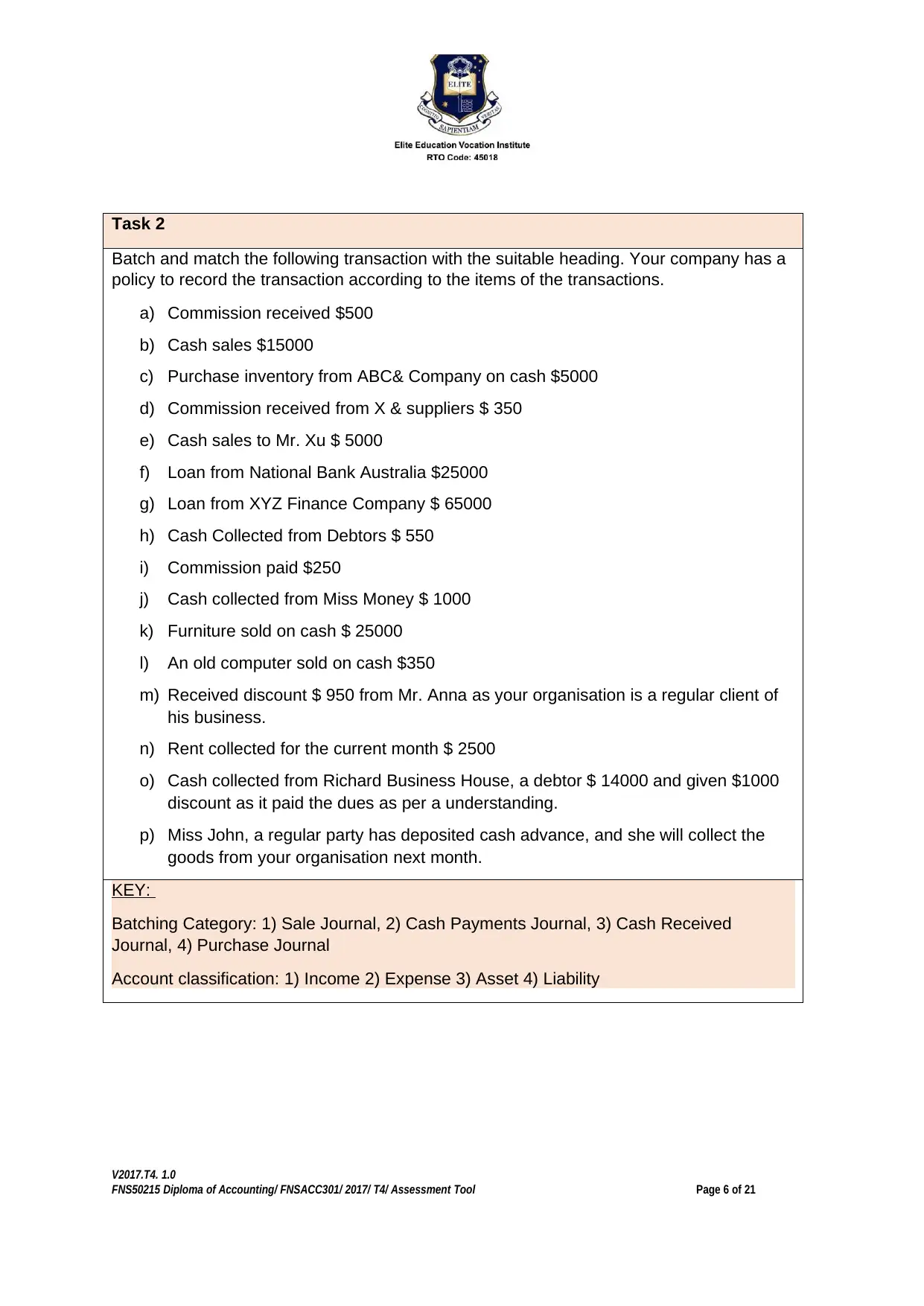

Task 2

Batch and match the following transaction with the suitable heading. Your company has a

policy to record the transaction according to the items of the transactions.

a) Commission received $500

b) Cash sales $15000

c) Purchase inventory from ABC& Company on cash $5000

d) Commission received from X & suppliers $ 350

e) Cash sales to Mr. Xu $ 5000

f) Loan from National Bank Australia $25000

g) Loan from XYZ Finance Company $ 65000

h) Cash Collected from Debtors $ 550

i) Commission paid $250

j) Cash collected from Miss Money $ 1000

k) Furniture sold on cash $ 25000

l) An old computer sold on cash $350

m) Received discount $ 950 from Mr. Anna as your organisation is a regular client of

his business.

n) Rent collected for the current month $ 2500

o) Cash collected from Richard Business House, a debtor $ 14000 and given $1000

discount as it paid the dues as per a understanding.

p) Miss John, a regular party has deposited cash advance, and she will collect the

goods from your organisation next month.

KEY:

Batching Category: 1) Sale Journal, 2) Cash Payments Journal, 3) Cash Received

Journal, 4) Purchase Journal

Account classification: 1) Income 2) Expense 3) Asset 4) Liability

V2017.T4. 1.0

FNS50215 Diploma of Accounting/ FNSACC301/ 2017/ T4/ Assessment Tool Page 6 of 21

Batch and match the following transaction with the suitable heading. Your company has a

policy to record the transaction according to the items of the transactions.

a) Commission received $500

b) Cash sales $15000

c) Purchase inventory from ABC& Company on cash $5000

d) Commission received from X & suppliers $ 350

e) Cash sales to Mr. Xu $ 5000

f) Loan from National Bank Australia $25000

g) Loan from XYZ Finance Company $ 65000

h) Cash Collected from Debtors $ 550

i) Commission paid $250

j) Cash collected from Miss Money $ 1000

k) Furniture sold on cash $ 25000

l) An old computer sold on cash $350

m) Received discount $ 950 from Mr. Anna as your organisation is a regular client of

his business.

n) Rent collected for the current month $ 2500

o) Cash collected from Richard Business House, a debtor $ 14000 and given $1000

discount as it paid the dues as per a understanding.

p) Miss John, a regular party has deposited cash advance, and she will collect the

goods from your organisation next month.

KEY:

Batching Category: 1) Sale Journal, 2) Cash Payments Journal, 3) Cash Received

Journal, 4) Purchase Journal

Account classification: 1) Income 2) Expense 3) Asset 4) Liability

V2017.T4. 1.0

FNS50215 Diploma of Accounting/ FNSACC301/ 2017/ T4/ Assessment Tool Page 6 of 21

Account classification

a) …………………………..

b) …………………………..

c) …………………………..

d) …………………………..

e) …………………………..

f) …………………………..

g) …………………………..

h) …………………………..

i) ………………………..

j) …………………………..

k) …………………………..

l) …………………………..

m) …………………………..

n) …………………………..

o) …………………………..

p) …………………………..

Batching Category

Batching Category

a) …………………………..

b) …………………………..

c) …………………………..

d) …………………………..

e) …………………………..

f) …………………………..

g) …………………………..

h) …………………………..

i) …………………………..

j) …………………………..

k) …………………………..

l) …………………………..

m) …………………………..

n) …………………………..

o) …………………………..

p) …………………………..

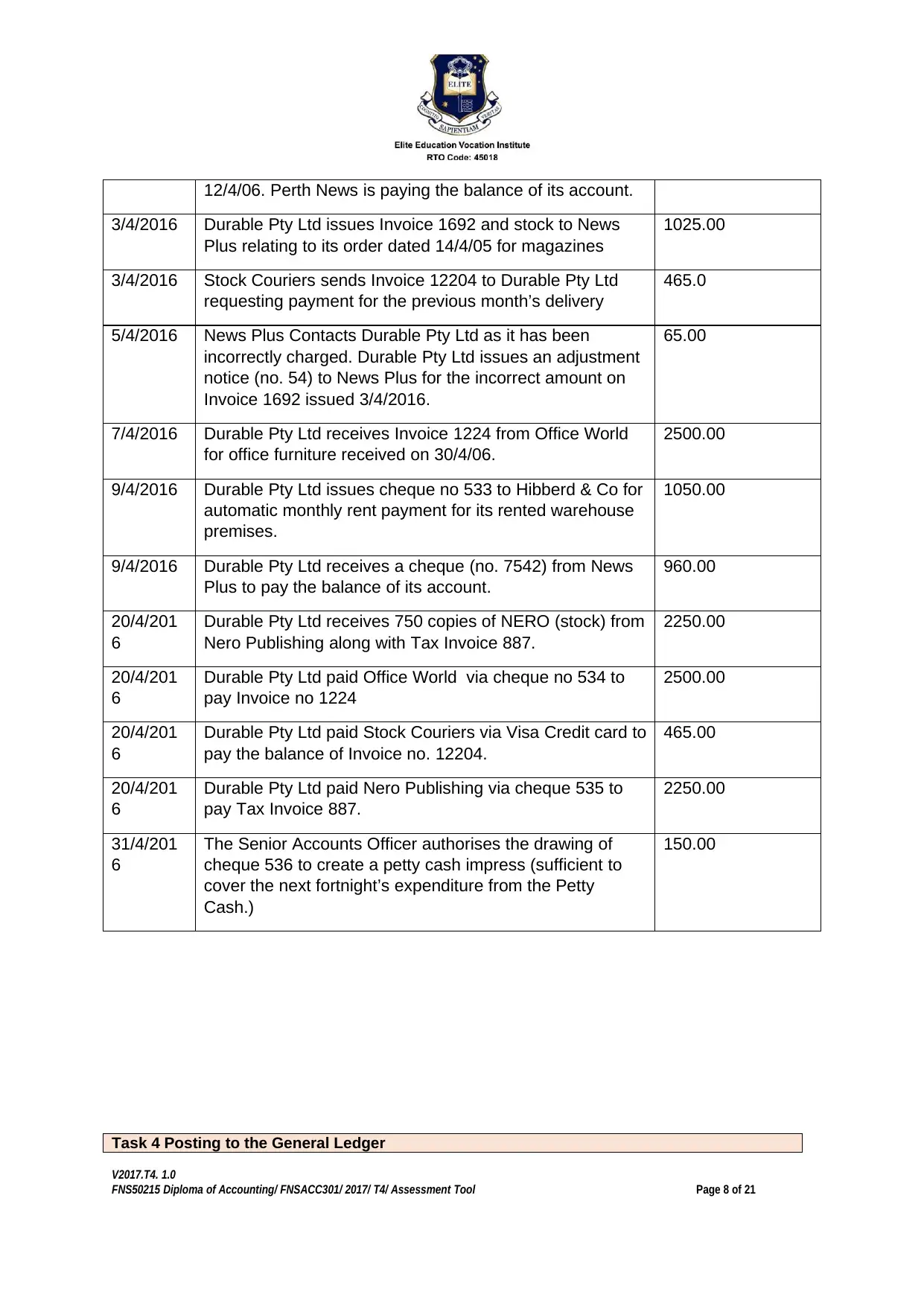

Task 3: Posting to General Journal

To complete this assignment, you will need to enter the following transactions and

communicate your manager (Trainer) for approval on these journals for April 2016 into

General journal.

Process the journal entries for the following transactions in the Journal worksheet provided.

[Hint] Total debits and credits are $14,330.00

Date Details Amount (inc.GST

where applicable)

2/4/2016 Durable Pty Ltd receives a cheque (no 683) from Perth

News. The cheque is attached to a remittance advice that

refers to invoice 1638 issued by Durable Pty Ltd in

650.00

V2017.T4. 1.0

FNS50215 Diploma of Accounting/ FNSACC301/ 2017/ T4/ Assessment Tool Page 7 of 21

a) …………………………..

b) …………………………..

c) …………………………..

d) …………………………..

e) …………………………..

f) …………………………..

g) …………………………..

h) …………………………..

i) ………………………..

j) …………………………..

k) …………………………..

l) …………………………..

m) …………………………..

n) …………………………..

o) …………………………..

p) …………………………..

Batching Category

Batching Category

a) …………………………..

b) …………………………..

c) …………………………..

d) …………………………..

e) …………………………..

f) …………………………..

g) …………………………..

h) …………………………..

i) …………………………..

j) …………………………..

k) …………………………..

l) …………………………..

m) …………………………..

n) …………………………..

o) …………………………..

p) …………………………..

Task 3: Posting to General Journal

To complete this assignment, you will need to enter the following transactions and

communicate your manager (Trainer) for approval on these journals for April 2016 into

General journal.

Process the journal entries for the following transactions in the Journal worksheet provided.

[Hint] Total debits and credits are $14,330.00

Date Details Amount (inc.GST

where applicable)

2/4/2016 Durable Pty Ltd receives a cheque (no 683) from Perth

News. The cheque is attached to a remittance advice that

refers to invoice 1638 issued by Durable Pty Ltd in

650.00

V2017.T4. 1.0

FNS50215 Diploma of Accounting/ FNSACC301/ 2017/ T4/ Assessment Tool Page 7 of 21

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

12/4/06. Perth News is paying the balance of its account.

3/4/2016 Durable Pty Ltd issues Invoice 1692 and stock to News

Plus relating to its order dated 14/4/05 for magazines

1025.00

3/4/2016 Stock Couriers sends Invoice 12204 to Durable Pty Ltd

requesting payment for the previous month’s delivery

465.0

5/4/2016 News Plus Contacts Durable Pty Ltd as it has been

incorrectly charged. Durable Pty Ltd issues an adjustment

notice (no. 54) to News Plus for the incorrect amount on

Invoice 1692 issued 3/4/2016.

65.00

7/4/2016 Durable Pty Ltd receives Invoice 1224 from Office World

for office furniture received on 30/4/06.

2500.00

9/4/2016 Durable Pty Ltd issues cheque no 533 to Hibberd & Co for

automatic monthly rent payment for its rented warehouse

premises.

1050.00

9/4/2016 Durable Pty Ltd receives a cheque (no. 7542) from News

Plus to pay the balance of its account.

960.00

20/4/201

6

Durable Pty Ltd receives 750 copies of NERO (stock) from

Nero Publishing along with Tax Invoice 887.

2250.00

20/4/201

6

Durable Pty Ltd paid Office World via cheque no 534 to

pay Invoice no 1224

2500.00

20/4/201

6

Durable Pty Ltd paid Stock Couriers via Visa Credit card to

pay the balance of Invoice no. 12204.

465.00

20/4/201

6

Durable Pty Ltd paid Nero Publishing via cheque 535 to

pay Tax Invoice 887.

2250.00

31/4/201

6

The Senior Accounts Officer authorises the drawing of

cheque 536 to create a petty cash impress (sufficient to

cover the next fortnight’s expenditure from the Petty

Cash.)

150.00

Task 4 Posting to the General Ledger

V2017.T4. 1.0

FNS50215 Diploma of Accounting/ FNSACC301/ 2017/ T4/ Assessment Tool Page 8 of 21

3/4/2016 Durable Pty Ltd issues Invoice 1692 and stock to News

Plus relating to its order dated 14/4/05 for magazines

1025.00

3/4/2016 Stock Couriers sends Invoice 12204 to Durable Pty Ltd

requesting payment for the previous month’s delivery

465.0

5/4/2016 News Plus Contacts Durable Pty Ltd as it has been

incorrectly charged. Durable Pty Ltd issues an adjustment

notice (no. 54) to News Plus for the incorrect amount on

Invoice 1692 issued 3/4/2016.

65.00

7/4/2016 Durable Pty Ltd receives Invoice 1224 from Office World

for office furniture received on 30/4/06.

2500.00

9/4/2016 Durable Pty Ltd issues cheque no 533 to Hibberd & Co for

automatic monthly rent payment for its rented warehouse

premises.

1050.00

9/4/2016 Durable Pty Ltd receives a cheque (no. 7542) from News

Plus to pay the balance of its account.

960.00

20/4/201

6

Durable Pty Ltd receives 750 copies of NERO (stock) from

Nero Publishing along with Tax Invoice 887.

2250.00

20/4/201

6

Durable Pty Ltd paid Office World via cheque no 534 to

pay Invoice no 1224

2500.00

20/4/201

6

Durable Pty Ltd paid Stock Couriers via Visa Credit card to

pay the balance of Invoice no. 12204.

465.00

20/4/201

6

Durable Pty Ltd paid Nero Publishing via cheque 535 to

pay Tax Invoice 887.

2250.00

31/4/201

6

The Senior Accounts Officer authorises the drawing of

cheque 536 to create a petty cash impress (sufficient to

cover the next fortnight’s expenditure from the Petty

Cash.)

150.00

Task 4 Posting to the General Ledger

V2017.T4. 1.0

FNS50215 Diploma of Accounting/ FNSACC301/ 2017/ T4/ Assessment Tool Page 8 of 21

At the end of each month, you are required to post the journal entries to the general

ledger. Complete the following tasks for Durable Pty Ltd:

1. Post the journal entries to the general ledger accounts in the Ledger worksheet.

2. Total each of the account balances in the General ledger?

Task 5 Prepare a Trial Balance

Prepare a Trial balance in the Trial Balance worksheet for all active general ledger

accounts for the month ending 30th April 2016 for Durable Pty Ltd. (Hint: Total

V2017.T4. 1.0

FNS50215 Diploma of Accounting/ FNSACC301/ 2017/ T4/ Assessment Tool Page 9 of 21

ledger. Complete the following tasks for Durable Pty Ltd:

1. Post the journal entries to the general ledger accounts in the Ledger worksheet.

2. Total each of the account balances in the General ledger?

Task 5 Prepare a Trial Balance

Prepare a Trial balance in the Trial Balance worksheet for all active general ledger

accounts for the month ending 30th April 2016 for Durable Pty Ltd. (Hint: Total

V2017.T4. 1.0

FNS50215 Diploma of Accounting/ FNSACC301/ 2017/ T4/ Assessment Tool Page 9 of 21

debits and credits are $6474.10)

Assessment 2 Part B Short answers-Written response

Q1. When a staff member presents you with a petty cash voucher, what supporting

documentation must be attached? Who is required to approve their petty cash claim?

V2017.T4. 1.0

FNS50215 Diploma of Accounting/ FNSACC301/ 2017/ T4/ Assessment Tool Page 10 of 21

Assessment 2 Part B Short answers-Written response

Q1. When a staff member presents you with a petty cash voucher, what supporting

documentation must be attached? Who is required to approve their petty cash claim?

V2017.T4. 1.0

FNS50215 Diploma of Accounting/ FNSACC301/ 2017/ T4/ Assessment Tool Page 10 of 21

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

The petty cash voucher must be supported by an original receipt document for

every cash disbursement transaction from the fund kept for petty expenses. Two

documents are required for the petty cash transactions. One is issued from the

custodian and other is issued by the payee. The custodian of petty cash fund is

required to approve the petty cash claim.

Q2. A colleague has had a busy day. Even though it is against organisational policy the

colleague has decided to leave the banking until the next day and leaves the money in the

cash register overnight. The next morning, when the colleague checks the takings, $100 is

missing.

Describe two actions the colleague should have taken to help ensure the money was not

‘at risk’

He must have kept the money into some lockers so that it could not be lost or

misplaced.

Further, he should have submitted the cash into bank account to avoid any loss.

Q3. a) Under GST legislation, what details must be included on a TAX Invoice received

from a creditor before you can process it?

b) If the supplier has not provided their ABN, what procedures must Accounts Payable

follow?

V2017.T4. 1.0

FNS50215 Diploma of Accounting/ FNSACC301/ 2017/ T4/ Assessment Tool Page 11 of 21

every cash disbursement transaction from the fund kept for petty expenses. Two

documents are required for the petty cash transactions. One is issued from the

custodian and other is issued by the payee. The custodian of petty cash fund is

required to approve the petty cash claim.

Q2. A colleague has had a busy day. Even though it is against organisational policy the

colleague has decided to leave the banking until the next day and leaves the money in the

cash register overnight. The next morning, when the colleague checks the takings, $100 is

missing.

Describe two actions the colleague should have taken to help ensure the money was not

‘at risk’

He must have kept the money into some lockers so that it could not be lost or

misplaced.

Further, he should have submitted the cash into bank account to avoid any loss.

Q3. a) Under GST legislation, what details must be included on a TAX Invoice received

from a creditor before you can process it?

b) If the supplier has not provided their ABN, what procedures must Accounts Payable

follow?

V2017.T4. 1.0

FNS50215 Diploma of Accounting/ FNSACC301/ 2017/ T4/ Assessment Tool Page 11 of 21

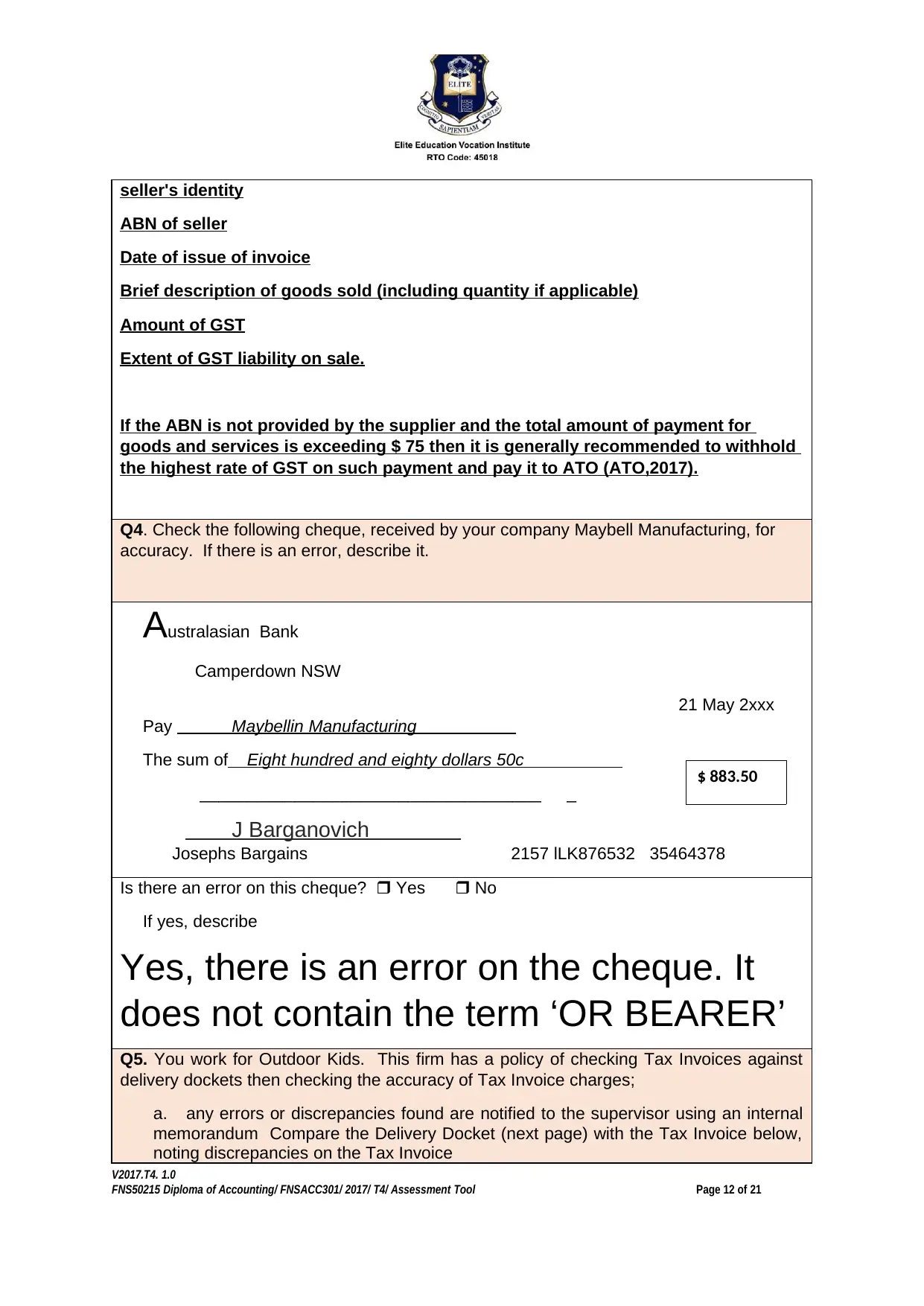

seller's identity

ABN of seller

Date of issue of invoice

Brief description of goods sold (including quantity if applicable)

Amount of GST

Extent of GST liability on sale.

If the ABN is not provided by the supplier and the total amount of payment for

goods and services is exceeding $ 75 then it is generally recommended to withhold

the highest rate of GST on such payment and pay it to ATO (ATO,2017).

Q4. Check the following cheque, received by your company Maybell Manufacturing, for

accuracy. If there is an error, describe it.

Australasian Bank

Camperdown NSW

21 May 2xxx

Pay Maybellin Manufacturing

The sum of Eight hundred and eighty dollars 50c

____________________________________ _

J Barganovich

Josephs Bargains 2157 lLK876532 35464378

Is there an error on this cheque? Yes No

If yes, describe

Yes, there is an error on the cheque. It

does not contain the term ‘OR BEARER’

Q5. You work for Outdoor Kids. This firm has a policy of checking Tax Invoices against

delivery dockets then checking the accuracy of Tax Invoice charges;

a. any errors or discrepancies found are notified to the supervisor using an internal

memorandum Compare the Delivery Docket (next page) with the Tax Invoice below,

noting discrepancies on the Tax Invoice

V2017.T4. 1.0

FNS50215 Diploma of Accounting/ FNSACC301/ 2017/ T4/ Assessment Tool Page 12 of 21

$ 883.50

ABN of seller

Date of issue of invoice

Brief description of goods sold (including quantity if applicable)

Amount of GST

Extent of GST liability on sale.

If the ABN is not provided by the supplier and the total amount of payment for

goods and services is exceeding $ 75 then it is generally recommended to withhold

the highest rate of GST on such payment and pay it to ATO (ATO,2017).

Q4. Check the following cheque, received by your company Maybell Manufacturing, for

accuracy. If there is an error, describe it.

Australasian Bank

Camperdown NSW

21 May 2xxx

Pay Maybellin Manufacturing

The sum of Eight hundred and eighty dollars 50c

____________________________________ _

J Barganovich

Josephs Bargains 2157 lLK876532 35464378

Is there an error on this cheque? Yes No

If yes, describe

Yes, there is an error on the cheque. It

does not contain the term ‘OR BEARER’

Q5. You work for Outdoor Kids. This firm has a policy of checking Tax Invoices against

delivery dockets then checking the accuracy of Tax Invoice charges;

a. any errors or discrepancies found are notified to the supervisor using an internal

memorandum Compare the Delivery Docket (next page) with the Tax Invoice below,

noting discrepancies on the Tax Invoice

V2017.T4. 1.0

FNS50215 Diploma of Accounting/ FNSACC301/ 2017/ T4/ Assessment Tool Page 12 of 21

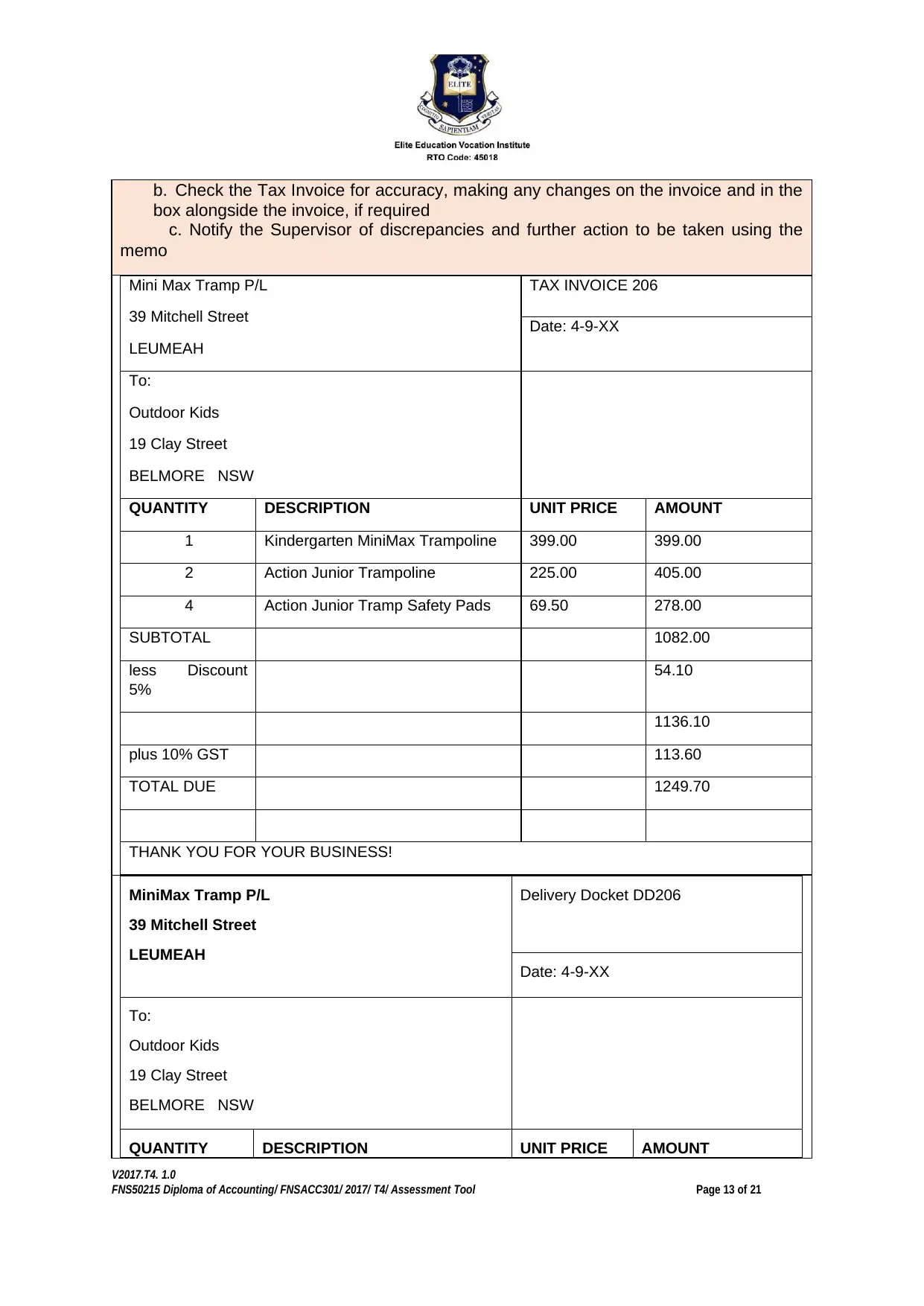

$ 883.50

b. Check the Tax Invoice for accuracy, making any changes on the invoice and in the

box alongside the invoice, if required

c. Notify the Supervisor of discrepancies and further action to be taken using the

memo

Mini Max Tramp P/L

39 Mitchell Street

LEUMEAH

TAX INVOICE 206

Date: 4-9-XX

To:

Outdoor Kids

19 Clay Street

BELMORE NSW

QUANTITY DESCRIPTION UNIT PRICE AMOUNT

1 Kindergarten MiniMax Trampoline 399.00 399.00

2 Action Junior Trampoline 225.00 405.00

4 Action Junior Tramp Safety Pads 69.50 278.00

SUBTOTAL 1082.00

less Discount

5%

54.10

1136.10

plus 10% GST 113.60

TOTAL DUE 1249.70

THANK YOU FOR YOUR BUSINESS!

MiniMax Tramp P/L

39 Mitchell Street

LEUMEAH

Delivery Docket DD206

Date: 4-9-XX

To:

Outdoor Kids

19 Clay Street

BELMORE NSW

QUANTITY DESCRIPTION UNIT PRICE AMOUNT

V2017.T4. 1.0

FNS50215 Diploma of Accounting/ FNSACC301/ 2017/ T4/ Assessment Tool Page 13 of 21

box alongside the invoice, if required

c. Notify the Supervisor of discrepancies and further action to be taken using the

memo

Mini Max Tramp P/L

39 Mitchell Street

LEUMEAH

TAX INVOICE 206

Date: 4-9-XX

To:

Outdoor Kids

19 Clay Street

BELMORE NSW

QUANTITY DESCRIPTION UNIT PRICE AMOUNT

1 Kindergarten MiniMax Trampoline 399.00 399.00

2 Action Junior Trampoline 225.00 405.00

4 Action Junior Tramp Safety Pads 69.50 278.00

SUBTOTAL 1082.00

less Discount

5%

54.10

1136.10

plus 10% GST 113.60

TOTAL DUE 1249.70

THANK YOU FOR YOUR BUSINESS!

MiniMax Tramp P/L

39 Mitchell Street

LEUMEAH

Delivery Docket DD206

Date: 4-9-XX

To:

Outdoor Kids

19 Clay Street

BELMORE NSW

QUANTITY DESCRIPTION UNIT PRICE AMOUNT

V2017.T4. 1.0

FNS50215 Diploma of Accounting/ FNSACC301/ 2017/ T4/ Assessment Tool Page 13 of 21

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

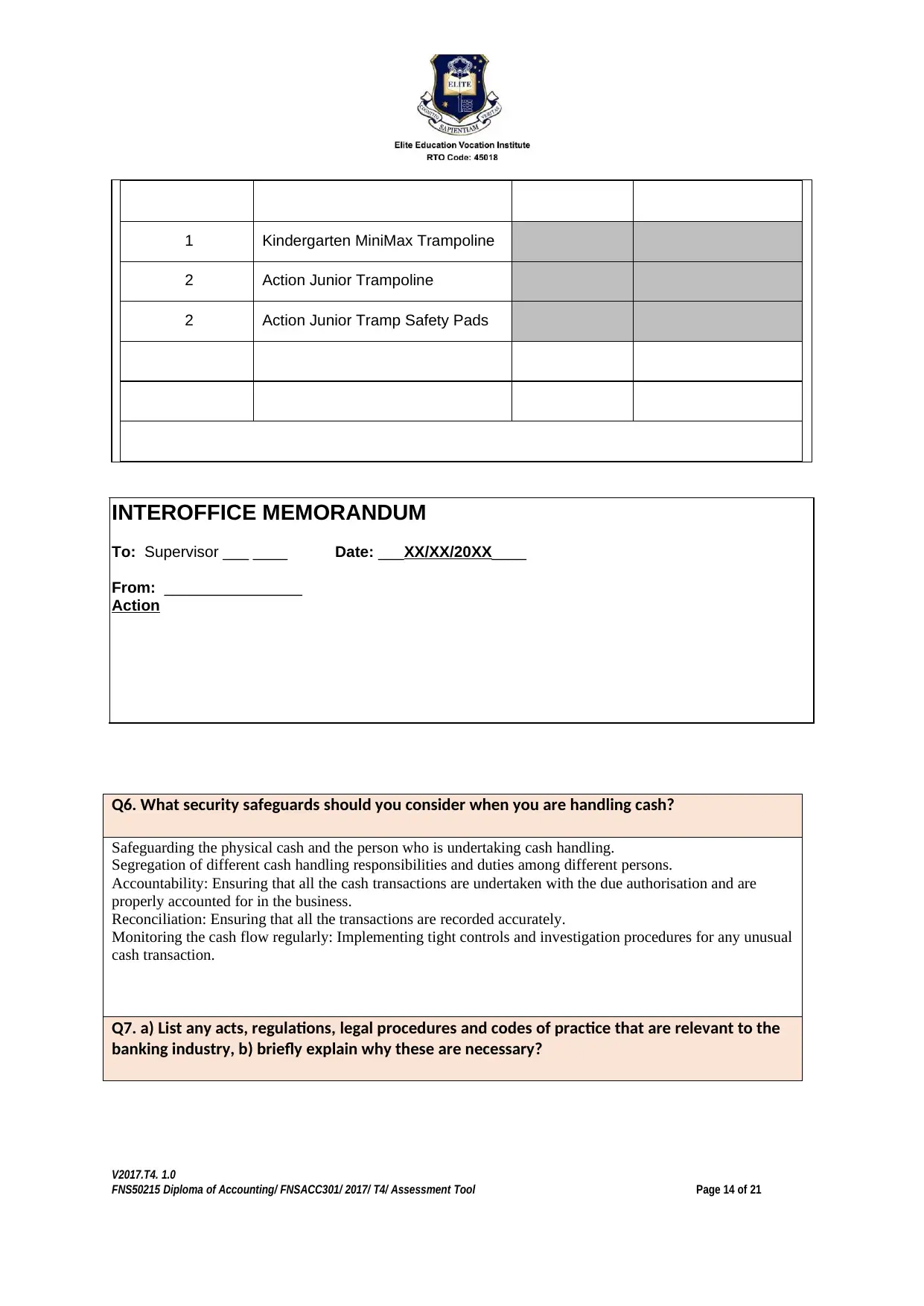

1 Kindergarten MiniMax Trampoline

2 Action Junior Trampoline

2 Action Junior Tramp Safety Pads

INTEROFFICE MEMORANDUM

To: Supervisor ___ ____ Date: ___XX/XX/20XX____

From: ________________

Action

Q6. What security safeguards should you consider when you are handling cash?

Safeguarding the physical cash and the person who is undertaking cash handling.

Segregation of different cash handling responsibilities and duties among different persons.

Accountability: Ensuring that all the cash transactions are undertaken with the due authorisation and are

properly accounted for in the business.

Reconciliation: Ensuring that all the transactions are recorded accurately.

Monitoring the cash flow regularly: Implementing tight controls and investigation procedures for any unusual

cash transaction.

Q7. a) List any acts, regulations, legal procedures and codes of practice that are relevant to the

banking industry, b) briefly explain why these are necessary?

V2017.T4. 1.0

FNS50215 Diploma of Accounting/ FNSACC301/ 2017/ T4/ Assessment Tool Page 14 of 21

2 Action Junior Trampoline

2 Action Junior Tramp Safety Pads

INTEROFFICE MEMORANDUM

To: Supervisor ___ ____ Date: ___XX/XX/20XX____

From: ________________

Action

Q6. What security safeguards should you consider when you are handling cash?

Safeguarding the physical cash and the person who is undertaking cash handling.

Segregation of different cash handling responsibilities and duties among different persons.

Accountability: Ensuring that all the cash transactions are undertaken with the due authorisation and are

properly accounted for in the business.

Reconciliation: Ensuring that all the transactions are recorded accurately.

Monitoring the cash flow regularly: Implementing tight controls and investigation procedures for any unusual

cash transaction.

Q7. a) List any acts, regulations, legal procedures and codes of practice that are relevant to the

banking industry, b) briefly explain why these are necessary?

V2017.T4. 1.0

FNS50215 Diploma of Accounting/ FNSACC301/ 2017/ T4/ Assessment Tool Page 14 of 21

Banking Act, 1959

Reserve Bank Act, 1959

Australian Prudential Regulation Authority Act, 1998

Bills of Exchange Act, 1909

Cheques Act, 1986

Financial Transaction Report Act, 1988

Anti-Money Laundering and Counter –Terrorism Financing Act, 2006

Australian Securities and Investment Commission Act, 2001

Financial Transactions Reports Act, 1988

Code of practice:

Code of Conduct (ASIC)

ePayment and financial services sector

Q8. Explain the relationship between a “batch total” for banking purposes and “receipts

issued”.

When some cash is deposited in bank it might cover various checks in addition to the cash. The word batch is

usually printed on the receipt issued by bank for the deposit made. The receipt only includes the total amount

of cash deposited instead of showing individual amount of each of the item deposited. The transaction of

deposit is generally processed at the night once the bank gets closed for the day. When a deposit transaction

includes multiple checks, all the checks are grouped together to be processed as the batch transaction.

Q9. Describe the banking facilities you should use when performing the business banking

procedure

V2017.T4. 1.0

FNS50215 Diploma of Accounting/ FNSACC301/ 2017/ T4/ Assessment Tool Page 15 of 21

Reserve Bank Act, 1959

Australian Prudential Regulation Authority Act, 1998

Bills of Exchange Act, 1909

Cheques Act, 1986

Financial Transaction Report Act, 1988

Anti-Money Laundering and Counter –Terrorism Financing Act, 2006

Australian Securities and Investment Commission Act, 2001

Financial Transactions Reports Act, 1988

Code of practice:

Code of Conduct (ASIC)

ePayment and financial services sector

Q8. Explain the relationship between a “batch total” for banking purposes and “receipts

issued”.

When some cash is deposited in bank it might cover various checks in addition to the cash. The word batch is

usually printed on the receipt issued by bank for the deposit made. The receipt only includes the total amount

of cash deposited instead of showing individual amount of each of the item deposited. The transaction of

deposit is generally processed at the night once the bank gets closed for the day. When a deposit transaction

includes multiple checks, all the checks are grouped together to be processed as the batch transaction.

Q9. Describe the banking facilities you should use when performing the business banking

procedure

V2017.T4. 1.0

FNS50215 Diploma of Accounting/ FNSACC301/ 2017/ T4/ Assessment Tool Page 15 of 21

The locker facility

Cash Deposit or Lending functions

ATM facilities

Processing and issuance of Debit cards and credit cards.

Net banking facilities.

Q10. Explain the banking procedures that would be followed when customers pay by credit card

or debit card

1)Payment authentication

At this point the merchant bank captures the customer account information and then transfers it to the

acquirer.

2)Transaction submission:

At this stage merchant acquirer asks form the master-card to obtain the authorization of issuing bank of

customer.

3)Authorization request:

The mastercard submits the concerned transaction to issuer for the authorization.

4)Authorization response:

The transaction is authorized by the issuing bank and response is sent back to the merchant.

5)Merchant payment

The issuing bank sends the payment to the acquirer of merchant who finally deposits the payment amount to

the merchant account.

Q11. What items and documentation must be taken to the bank when banking the day’s takings?

V2017.T4. 1.0

FNS50215 Diploma of Accounting/ FNSACC301/ 2017/ T4/ Assessment Tool Page 16 of 21

Cash Deposit or Lending functions

ATM facilities

Processing and issuance of Debit cards and credit cards.

Net banking facilities.

Q10. Explain the banking procedures that would be followed when customers pay by credit card

or debit card

1)Payment authentication

At this point the merchant bank captures the customer account information and then transfers it to the

acquirer.

2)Transaction submission:

At this stage merchant acquirer asks form the master-card to obtain the authorization of issuing bank of

customer.

3)Authorization request:

The mastercard submits the concerned transaction to issuer for the authorization.

4)Authorization response:

The transaction is authorized by the issuing bank and response is sent back to the merchant.

5)Merchant payment

The issuing bank sends the payment to the acquirer of merchant who finally deposits the payment amount to

the merchant account.

Q11. What items and documentation must be taken to the bank when banking the day’s takings?

V2017.T4. 1.0

FNS50215 Diploma of Accounting/ FNSACC301/ 2017/ T4/ Assessment Tool Page 16 of 21

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Receipts of day’s takings.

Deposit forms

Cheques

Bank Book

Documents of Identity.

Q12. What procedure should be followed by the person who performed the daily banking, after

the deposit has been made at the bank?

After depositing the cash in bank, the depositor must check the message alert on the registered e-mail ID or

the contact number to ensure that the amount is deposited correctly in the account.

Further, the deposit slip or acknowledgement document must be collected personally from the bank where the

amount is deposited or if the amount is deposited on the online platform , the deposit slip must be

downloaded from the portal.

Record the cash deposition transaction in the cash journal maintained by the firm.

Make the respective journal entry in the journal leger manually if the books of accounts are maintained

manually and if the records are maintained using the accounting software, the relevant entry for the

transaction of cash deposition must be made through such software.

Tally the bank statement must be tallied with the cash book of the business.

Q13. What steps would you take if you found a discrepancy between the bank deposit form signed by the

bank and the cash records maintained by the business?

V2017.T4. 1.0

FNS50215 Diploma of Accounting/ FNSACC301/ 2017/ T4/ Assessment Tool Page 17 of 21

Deposit forms

Cheques

Bank Book

Documents of Identity.

Q12. What procedure should be followed by the person who performed the daily banking, after

the deposit has been made at the bank?

After depositing the cash in bank, the depositor must check the message alert on the registered e-mail ID or

the contact number to ensure that the amount is deposited correctly in the account.

Further, the deposit slip or acknowledgement document must be collected personally from the bank where the

amount is deposited or if the amount is deposited on the online platform , the deposit slip must be

downloaded from the portal.

Record the cash deposition transaction in the cash journal maintained by the firm.

Make the respective journal entry in the journal leger manually if the books of accounts are maintained

manually and if the records are maintained using the accounting software, the relevant entry for the

transaction of cash deposition must be made through such software.

Tally the bank statement must be tallied with the cash book of the business.

Q13. What steps would you take if you found a discrepancy between the bank deposit form signed by the

bank and the cash records maintained by the business?

V2017.T4. 1.0

FNS50215 Diploma of Accounting/ FNSACC301/ 2017/ T4/ Assessment Tool Page 17 of 21

Comparison of both the documents i.e. bank deposit form and cash record of the business must be made.

This comparison will enable the cashier of the business to ensure that all the cash deposit transactions have

been properly recorded in the cash book.

The transactions of bank deposits must be verified using the deposit slips issued by the bank each time when

the cash was deposited in the bank.

The dates at which bank has issued the deposit slip must be matched with the dates of deposition of cash to

the bank.

Preparation of bank reconciliation statements must be followed in the circumstances when there is any

discrepancy found in the cash and bank records.

Q14. Provide at least three reasons why it is important to check financial documents before

they are processed?

To ensure the accuracy of the information and data provided in the financial documents.

To nullify the impact of errors and omissions of the financial documents.

To ensure that all the terms of documents are agreeable to the signing parties before the

financial document is processed.

Assessment Two Feedback Evaluation

V2017.T4. 1.0

FNS50215 Diploma of Accounting/ FNSACC301/ 2017/ T4/ Assessment Tool Page 18 of 21

This comparison will enable the cashier of the business to ensure that all the cash deposit transactions have

been properly recorded in the cash book.

The transactions of bank deposits must be verified using the deposit slips issued by the bank each time when

the cash was deposited in the bank.

The dates at which bank has issued the deposit slip must be matched with the dates of deposition of cash to

the bank.

Preparation of bank reconciliation statements must be followed in the circumstances when there is any

discrepancy found in the cash and bank records.

Q14. Provide at least three reasons why it is important to check financial documents before

they are processed?

To ensure the accuracy of the information and data provided in the financial documents.

To nullify the impact of errors and omissions of the financial documents.

To ensure that all the terms of documents are agreeable to the signing parties before the

financial document is processed.

Assessment Two Feedback Evaluation

V2017.T4. 1.0

FNS50215 Diploma of Accounting/ FNSACC301/ 2017/ T4/ Assessment Tool Page 18 of 21

Student’s name:

Trainer/ Assessor’s name: Date:

Unit name: FNSACC301 Process financial transactions and extract interim reports

Assessment Submission Checklist to be completed by the Trainer/Assessor

Did the student complete and provide evidence for the following: Yes No

1. Provide a discussion on the short questions?

2. Provide an analysis for petty cash?

3. Understanding how to post to general ledgers?

4. Provide an evidence to do bank reconciliation?

5. Submit within agreed timeframe?

6. Extract and check trial balance and or prepare other required reports?

Has the learner proven they can: Yes No

V2017.T4. 1.0

FNS50215 Diploma of Accounting/ FNSACC301/ 2017/ T4/ Assessment Tool Page 19 of 21

Trainer/ Assessor’s name: Date:

Unit name: FNSACC301 Process financial transactions and extract interim reports

Assessment Submission Checklist to be completed by the Trainer/Assessor

Did the student complete and provide evidence for the following: Yes No

1. Provide a discussion on the short questions?

2. Provide an analysis for petty cash?

3. Understanding how to post to general ledgers?

4. Provide an evidence to do bank reconciliation?

5. Submit within agreed timeframe?

6. Extract and check trial balance and or prepare other required reports?

Has the learner proven they can: Yes No

V2017.T4. 1.0

FNS50215 Diploma of Accounting/ FNSACC301/ 2017/ T4/ Assessment Tool Page 19 of 21

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1.1 Identify, check and record information from documents

1.2 Examine supporting documentation to establish accuracy and completeness and to ensure

authorisation by appropriate personnel

1.3. Find and correct any errors

2.1 Enter accurately and balance deposits and withdrawals according to organisational procedures

2.2 Check cheques and card vouchers for validity before processing

2.3 Reconcile banking documentation with organisation’s financial records

2.4 Check, process and record petty cash claims and vouchers, and balance petty cash book according

to organisational procedures

3.1 Prepare invoices in accordance with organisational procedures

3.2 Check invoices against source documents for accuracy and correct any errors

3.3 File all invoices and related documents for auditing purposes

4.1 Prepare journals accurately and completely, and batch items within organisational timelines

4.2 Match batch items precisely to initial receipt records

4.3 Ensure journals are authorised by appropriate person and process in accordance with organisational

policy and procedures

5.1 Post journals accurately to ledger in accordance with organisational input standards, with

transactions correctly allocated to system and accounts

6.1 Enter data accurately into system in accordance with organisational input standards and correctly

allocate transactions to system and accounts

6.2 Update related systems to maintain integrity of relationships between financial systems

7.1 Select deposit facility appropriate to banking method to be used

7.2 Balance batch with deposit facility without error

V2017.T4. 1.0

FNS50215 Diploma of Accounting/ FNSACC301/ 2017/ T4/ Assessment Tool Page 20 of 21

1.2 Examine supporting documentation to establish accuracy and completeness and to ensure

authorisation by appropriate personnel

1.3. Find and correct any errors

2.1 Enter accurately and balance deposits and withdrawals according to organisational procedures

2.2 Check cheques and card vouchers for validity before processing

2.3 Reconcile banking documentation with organisation’s financial records

2.4 Check, process and record petty cash claims and vouchers, and balance petty cash book according

to organisational procedures

3.1 Prepare invoices in accordance with organisational procedures

3.2 Check invoices against source documents for accuracy and correct any errors

3.3 File all invoices and related documents for auditing purposes

4.1 Prepare journals accurately and completely, and batch items within organisational timelines

4.2 Match batch items precisely to initial receipt records

4.3 Ensure journals are authorised by appropriate person and process in accordance with organisational

policy and procedures

5.1 Post journals accurately to ledger in accordance with organisational input standards, with

transactions correctly allocated to system and accounts

6.1 Enter data accurately into system in accordance with organisational input standards and correctly

allocate transactions to system and accounts

6.2 Update related systems to maintain integrity of relationships between financial systems

7.1 Select deposit facility appropriate to banking method to be used

7.2 Balance batch with deposit facility without error

V2017.T4. 1.0

FNS50215 Diploma of Accounting/ FNSACC301/ 2017/ T4/ Assessment Tool Page 20 of 21

7.3 Take security and safety precautions appropriate to method of banking, in accordance with

organisational policy and industry and legislative requirements

7.4 Obtain and file proof of lodgement so that it is easily accessible and traceable

8.2 Complete cash and credit journals and post to general ledger

8.3 Extract and check trial balance and prepare other required reports

Assessment outcome Satisfactory Not Yet Satisfactory Re-assessment required

Student Signature

The result of my performance in this unit has been discussed and explained to me.

____________________________ Date: ______________

Student signature

Trainer/ Assessor’s

Signature

Trainer/ Assessor’s declaration:

I hereby certify that the above student has been assessed by myself and all assessments are carried out as

required by the Principles of Assessments (Clause 1.8 of the Standards for RTO 2015).

____________________________ Date: ______________

Assessor signature

V2017.T4. 1.0

FNS50215 Diploma of Accounting/ FNSACC301/ 2017/ T4/ Assessment Tool Page 21 of 21

organisational policy and industry and legislative requirements

7.4 Obtain and file proof of lodgement so that it is easily accessible and traceable

8.2 Complete cash and credit journals and post to general ledger

8.3 Extract and check trial balance and prepare other required reports

Assessment outcome Satisfactory Not Yet Satisfactory Re-assessment required

Student Signature

The result of my performance in this unit has been discussed and explained to me.

____________________________ Date: ______________

Student signature

Trainer/ Assessor’s

Signature

Trainer/ Assessor’s declaration:

I hereby certify that the above student has been assessed by myself and all assessments are carried out as

required by the Principles of Assessments (Clause 1.8 of the Standards for RTO 2015).

____________________________ Date: ______________

Assessor signature

V2017.T4. 1.0

FNS50215 Diploma of Accounting/ FNSACC301/ 2017/ T4/ Assessment Tool Page 21 of 21

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.