Assessment Workbook: FNSACC503 Manage budgets and forecasts

VerifiedAdded on 2023/06/03

|15

|4250

|387

AI Summary

This assessment workbook is for FNSACC503 Manage budgets and forecasts. It includes short answer questions, a cash receipts forecast, break even analysis, and strategies to mitigate financial risks. Learn how to prepare a budget, conduct discussions with stakeholders, and establish correct assumptions and parameters.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Assessment Workbook – FNSACC503 1 | P a g e Version 4.0

Assessment Workbook: FNSACC503

Manage budgets and forecasts

Assessment Workbook: FNSACC503

Manage budgets and forecasts

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Version control

Version No. Date Dept. Change

1.0 07/04/2015 Training Original

2.0 29/04/2016 Training Revised content

3.0 27/04/2016 Training Updated to include assessments

4.0 15/09/2016 Training Moodle updates and changed title from Assessment

Guide to Assessment Workbook

5.0 19/01/2018 Training Revised content

Copyright Statement

© Copyright National Training

Disclaimer

All rights reserved. No part of this publication may be reproduced or transmitted

in any form or by any means, electronic or mechanical, including photocopying,

scanning, recording, or any information storage retrieval system without

permission in writing from National Training. No patent liability is assumed with

respect to the use of information used herein.

While every effort has been taken in the preparation of this publication, the

publisher and authors assume no responsibility for errors or omissions. Neither is

any liability assumed for damages resulting from the use of information contained

herein.

Assessment Workbook – FNSACC503 2 | P a g e Version 4.0

Version No. Date Dept. Change

1.0 07/04/2015 Training Original

2.0 29/04/2016 Training Revised content

3.0 27/04/2016 Training Updated to include assessments

4.0 15/09/2016 Training Moodle updates and changed title from Assessment

Guide to Assessment Workbook

5.0 19/01/2018 Training Revised content

Copyright Statement

© Copyright National Training

Disclaimer

All rights reserved. No part of this publication may be reproduced or transmitted

in any form or by any means, electronic or mechanical, including photocopying,

scanning, recording, or any information storage retrieval system without

permission in writing from National Training. No patent liability is assumed with

respect to the use of information used herein.

While every effort has been taken in the preparation of this publication, the

publisher and authors assume no responsibility for errors or omissions. Neither is

any liability assumed for damages resulting from the use of information contained

herein.

Assessment Workbook – FNSACC503 2 | P a g e Version 4.0

Contents

How do I use this guide? 4

Introduction 5

Application 5

Elements and Performance Criteria 5

Pre-requisites 5

Appeals and reassessment 6

Plagiarism 6

Referencing Materials 6

Understanding your results 6

Results Legend 7

Assessment activity 7

Assessment 1 and 2 Instructions8

Assessment 1: Short Answer Questions 1 9

Question 1.....................................................................................................................................9

Question 2.....................................................................................................................................9

Question 3.....................................................................................................................................9

Question 4A.................................................................................................................................10

Question 4B.................................................................................................................................10

Question 5...................................................................................................................................10

Question 6...................................................................................................................................10

Question 7A.................................................................................................................................11

Question 7B.................................................................................................................................11

Question 8...................................................................................................................................11

Question 9...................................................................................................................................11

Question 10.................................................................................................................................12

Question 11.................................................................................................................................12

Question 12.................................................................................................................................12

Question 13.................................................................................................................................12

Question 14.................................................................................................................................13

Question 15.................................................................................................................................13

Assessment 2: Short Answer Questions 2 13

Question 1...................................................................................................................................13

Question 2...................................................................................................................................13

Question 3...................................................................................................................................13

Question 4...................................................................................................................................13

Question 5...................................................................................................................................14

Assessment Workbook – FNSACC503 3 | P a g e Version 4.0

How do I use this guide? 4

Introduction 5

Application 5

Elements and Performance Criteria 5

Pre-requisites 5

Appeals and reassessment 6

Plagiarism 6

Referencing Materials 6

Understanding your results 6

Results Legend 7

Assessment activity 7

Assessment 1 and 2 Instructions8

Assessment 1: Short Answer Questions 1 9

Question 1.....................................................................................................................................9

Question 2.....................................................................................................................................9

Question 3.....................................................................................................................................9

Question 4A.................................................................................................................................10

Question 4B.................................................................................................................................10

Question 5...................................................................................................................................10

Question 6...................................................................................................................................10

Question 7A.................................................................................................................................11

Question 7B.................................................................................................................................11

Question 8...................................................................................................................................11

Question 9...................................................................................................................................11

Question 10.................................................................................................................................12

Question 11.................................................................................................................................12

Question 12.................................................................................................................................12

Question 13.................................................................................................................................12

Question 14.................................................................................................................................13

Question 15.................................................................................................................................13

Assessment 2: Short Answer Questions 2 13

Question 1...................................................................................................................................13

Question 2...................................................................................................................................13

Question 3...................................................................................................................................13

Question 4...................................................................................................................................13

Question 5...................................................................................................................................14

Assessment Workbook – FNSACC503 3 | P a g e Version 4.0

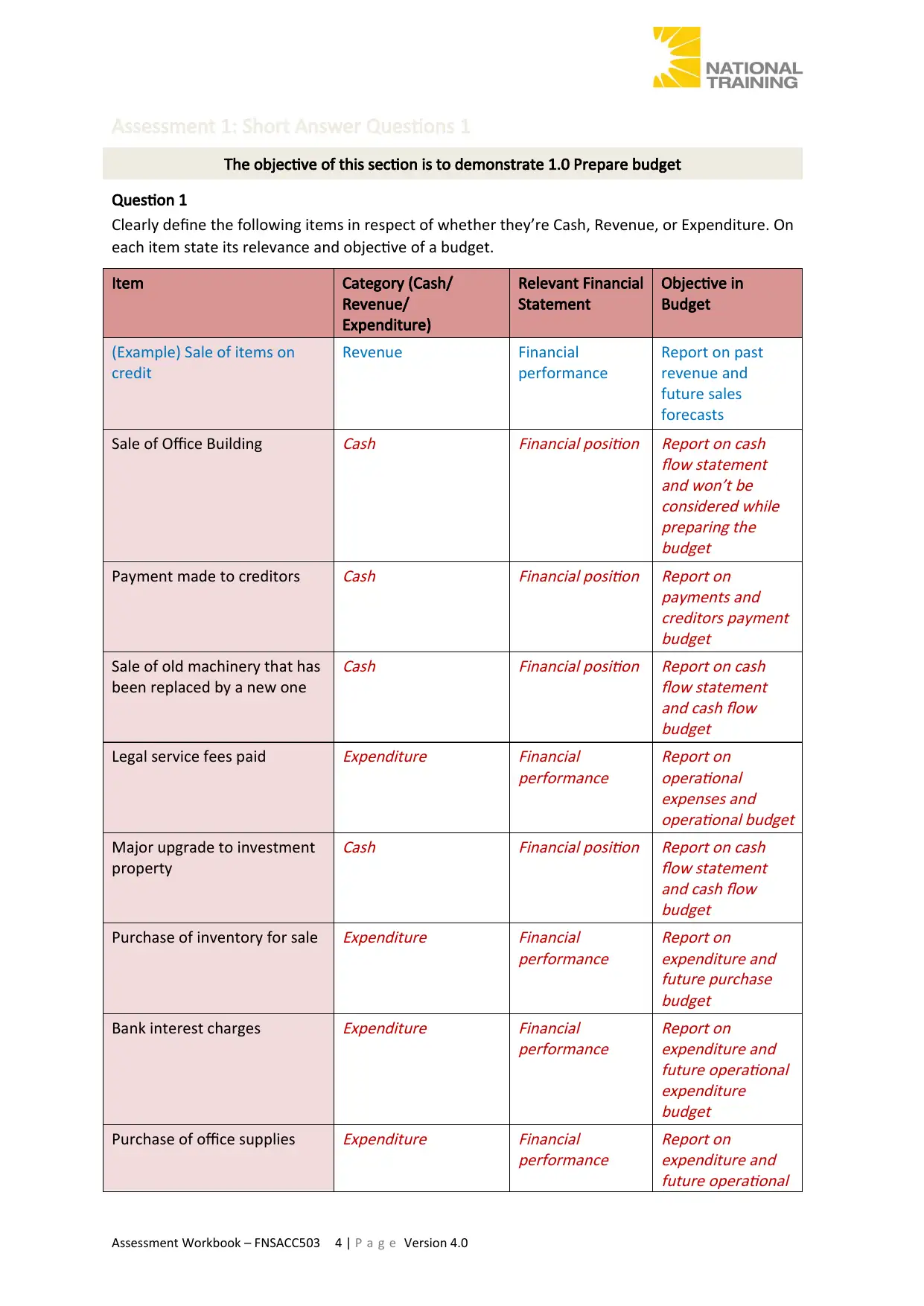

Assessment 1: Short Answer Questions 1

The objective of this section is to demonstrate 1.0 Prepare budget

Question 1

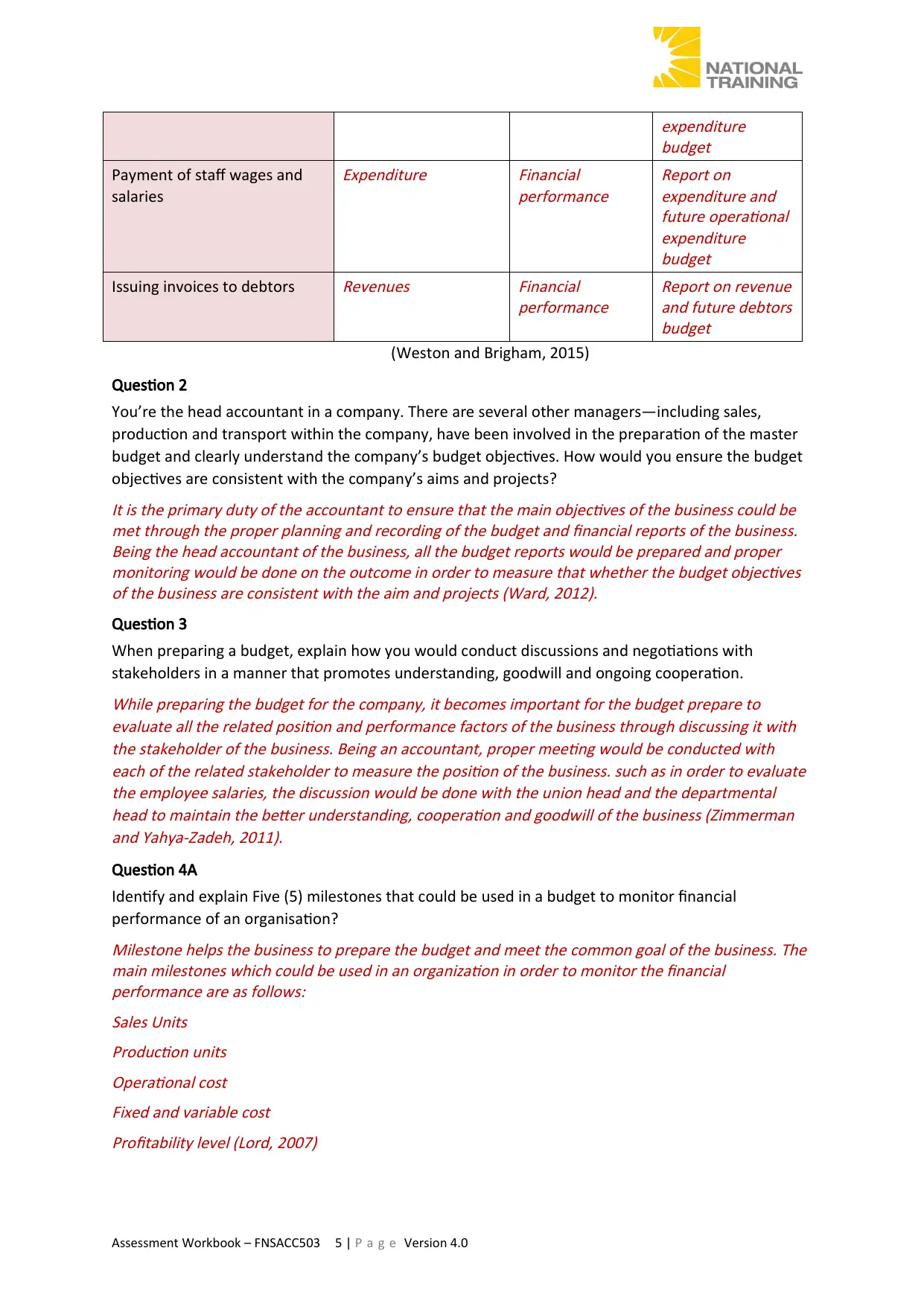

Clearly define the following items in respect of whether they’re Cash, Revenue, or Expenditure. On

each item state its relevance and objective of a budget.

Item Category (Cash/

Revenue/

Expenditure)

Relevant Financial

Statement

Objective in

Budget

(Example) Sale of items on

credit

Revenue Financial

performance

Report on past

revenue and

future sales

forecasts

Sale of Office Building

Cash

Financial position Report on cash

flow statement

and won’t be

considered while

preparing the

budget

Payment made to creditors

Cash

Financial position Report on

payments and

creditors payment

budget

Sale of old machinery that has

been replaced by a new one

Cash

Financial position Report on cash

flow statement

and cash flow

budget

Legal service fees paid

Expenditure

Financial

performance

Report on

operational

expenses and

operational budget

Major upgrade to investment

property

Cash

Financial position Report on cash

flow statement

and cash flow

budget

Purchase of inventory for sale

Expenditure

Financial

performance

Report on

expenditure and

future purchase

budget

Bank interest charges

Expenditure

Financial

performance

Report on

expenditure and

future operational

expenditure

budget

Purchase of office supplies

Expenditure

Financial

performance

Report on

expenditure and

future operational

Assessment Workbook – FNSACC503 4 | P a g e Version 4.0

The objective of this section is to demonstrate 1.0 Prepare budget

Question 1

Clearly define the following items in respect of whether they’re Cash, Revenue, or Expenditure. On

each item state its relevance and objective of a budget.

Item Category (Cash/

Revenue/

Expenditure)

Relevant Financial

Statement

Objective in

Budget

(Example) Sale of items on

credit

Revenue Financial

performance

Report on past

revenue and

future sales

forecasts

Sale of Office Building

Cash

Financial position Report on cash

flow statement

and won’t be

considered while

preparing the

budget

Payment made to creditors

Cash

Financial position Report on

payments and

creditors payment

budget

Sale of old machinery that has

been replaced by a new one

Cash

Financial position Report on cash

flow statement

and cash flow

budget

Legal service fees paid

Expenditure

Financial

performance

Report on

operational

expenses and

operational budget

Major upgrade to investment

property

Cash

Financial position Report on cash

flow statement

and cash flow

budget

Purchase of inventory for sale

Expenditure

Financial

performance

Report on

expenditure and

future purchase

budget

Bank interest charges

Expenditure

Financial

performance

Report on

expenditure and

future operational

expenditure

budget

Purchase of office supplies

Expenditure

Financial

performance

Report on

expenditure and

future operational

Assessment Workbook – FNSACC503 4 | P a g e Version 4.0

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

expenditure

budget

Payment of staff wages and

salaries

Expenditure

Financial

performance

Report on

expenditure and

future operational

expenditure

budget

Issuing invoices to debtors

Revenues

Financial

performance

Report on revenue

and future debtors

budget

(Weston and Brigham, 2015)

Question 2

You’re the head accountant in a company. There are several other managers—including sales,

production and transport within the company, have been involved in the preparation of the master

budget and clearly understand the company’s budget objectives. How would you ensure the budget

objectives are consistent with the company’s aims and projects?It is the primary duty of the accountant to ensure that the main objectives of the business could be

met through the proper planning and recording of the budget and financial reports of the business.

Being the head accountant of the business, all the budget reports would be prepared and proper

monitoring would be done on the outcome in order to measure that whether the budget objectives

of the business are consistent with the aim and projects (Ward, 2012).

Question 3

When preparing a budget, explain how you would conduct discussions and negotiations with

stakeholders in a manner that promotes understanding, goodwill and ongoing cooperation.While preparing the budget for the company, it becomes important for the budget prepare to

evaluate all the related position and performance factors of the business through discussing it with

the stakeholder of the business. Being an accountant, proper meeting would be conducted with

each of the related stakeholder to measure the position of the business. such as in order to evaluate

the employee salaries, the discussion would be done with the union head and the departmental

head to maintain the better understanding, cooperation and goodwill of the business (Zimmerman

and Yahya-Zadeh, 2011).

Question 4A

Identify and explain Five (5) milestones that could be used in a budget to monitor financial

performance of an organisation?Milestone helps the business to prepare the budget and meet the common goal of the business. The

main milestones which could be used in an organization in order to monitor the financial

performance are as follows:

Sales Units

Production units

Operational cost

Fixed and variable cost

Profitability level (Lord, 2007)

Assessment Workbook – FNSACC503 5 | P a g e Version 4.0

budget

Payment of staff wages and

salaries

Expenditure

Financial

performance

Report on

expenditure and

future operational

expenditure

budget

Issuing invoices to debtors

Revenues

Financial

performance

Report on revenue

and future debtors

budget

(Weston and Brigham, 2015)

Question 2

You’re the head accountant in a company. There are several other managers—including sales,

production and transport within the company, have been involved in the preparation of the master

budget and clearly understand the company’s budget objectives. How would you ensure the budget

objectives are consistent with the company’s aims and projects?It is the primary duty of the accountant to ensure that the main objectives of the business could be

met through the proper planning and recording of the budget and financial reports of the business.

Being the head accountant of the business, all the budget reports would be prepared and proper

monitoring would be done on the outcome in order to measure that whether the budget objectives

of the business are consistent with the aim and projects (Ward, 2012).

Question 3

When preparing a budget, explain how you would conduct discussions and negotiations with

stakeholders in a manner that promotes understanding, goodwill and ongoing cooperation.While preparing the budget for the company, it becomes important for the budget prepare to

evaluate all the related position and performance factors of the business through discussing it with

the stakeholder of the business. Being an accountant, proper meeting would be conducted with

each of the related stakeholder to measure the position of the business. such as in order to evaluate

the employee salaries, the discussion would be done with the union head and the departmental

head to maintain the better understanding, cooperation and goodwill of the business (Zimmerman

and Yahya-Zadeh, 2011).

Question 4A

Identify and explain Five (5) milestones that could be used in a budget to monitor financial

performance of an organisation?Milestone helps the business to prepare the budget and meet the common goal of the business. The

main milestones which could be used in an organization in order to monitor the financial

performance are as follows:

Sales Units

Production units

Operational cost

Fixed and variable cost

Profitability level (Lord, 2007)

Assessment Workbook – FNSACC503 5 | P a g e Version 4.0

Question 4B

List five (5) advantages of breaking down an annual budget into seasonal periods in accordance with

operating trends.Breakings down the annual budget into seasonal periods are quite important for the business. Some

of the advantage of it is as follows:

It becomes easier for the business to identify the performance in peak season and lean

seasons.

Sales growth of the business and changes in profitability position could be easily identified

through it.

Making the strategy and different policies at different time is easier through breaking down

the budgets.

The extra expenses of the business could be controlled.

Right uses and maximum uses of minimum resources could be done in an efficient way

(Madura, 2014).

The objective of this section is to demonstrate 2.0 Forecast estimates

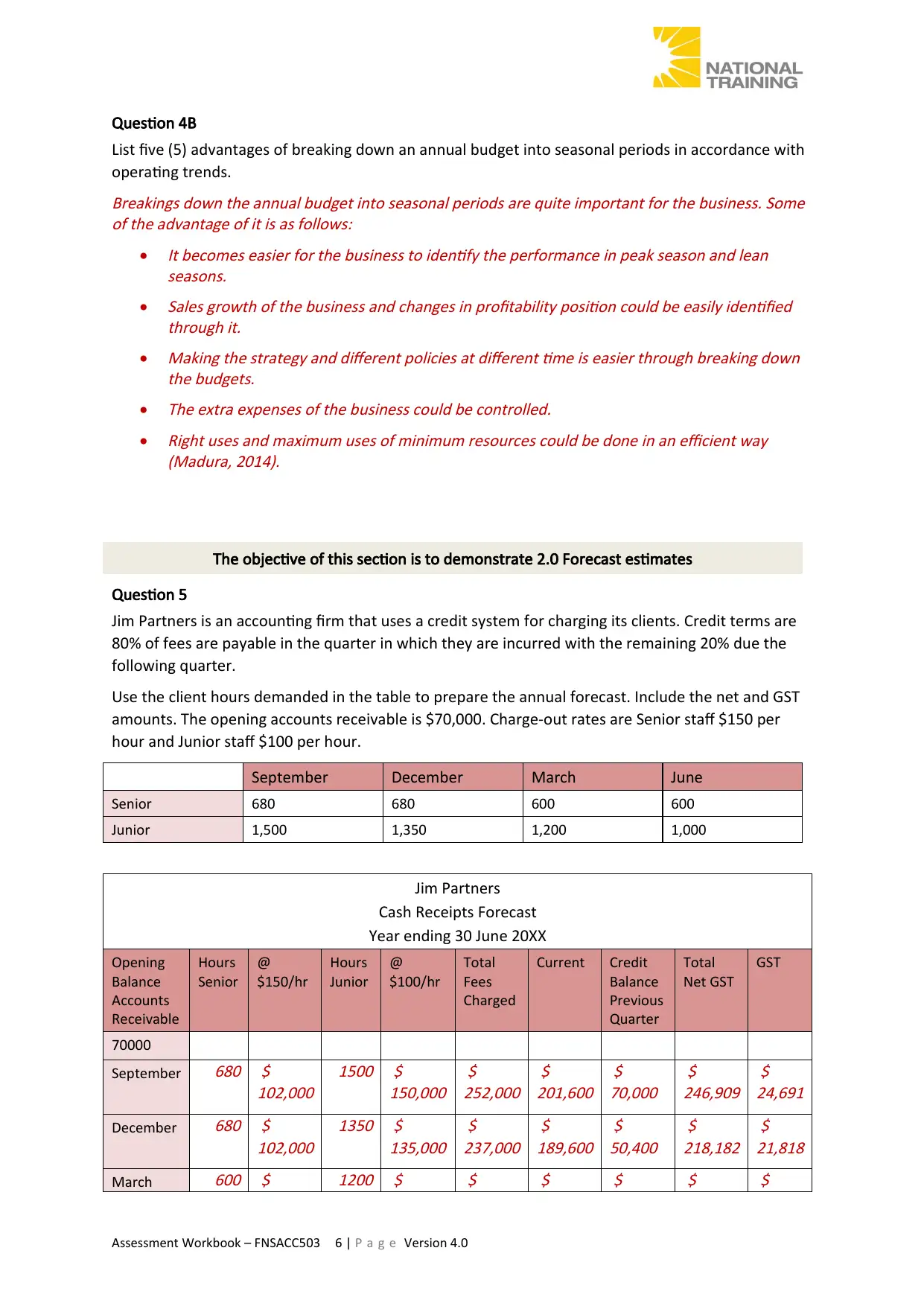

Question 5

Jim Partners is an accounting firm that uses a credit system for charging its clients. Credit terms are

80% of fees are payable in the quarter in which they are incurred with the remaining 20% due the

following quarter.

Use the client hours demanded in the table to prepare the annual forecast. Include the net and GST

amounts. The opening accounts receivable is $70,000. Charge-out rates are Senior staff $150 per

hour and Junior staff $100 per hour.

September December March June

Senior 680 680 600 600

Junior 1,500 1,350 1,200 1,000

Jim Partners

Cash Receipts Forecast

Year ending 30 June 20XX

Opening

Balance

Accounts

Receivable

Hours

Senior

@

$150/hr

Hours

Junior

@

$100/hr

Total

Fees

Charged

Current Credit

Balance

Previous

Quarter

Total

Net GST

GST

70000

September

680 $

102,000

1500 $

150,000

$

252,000

$

201,600

$

70,000

$

246,909

$

24,691

December

680 $

102,000

1350 $

135,000

$

237,000

$

189,600

$

50,400

$

218,182

$

21,818

March

600 $

1200 $ $ $ $ $ $

Assessment Workbook – FNSACC503 6 | P a g e Version 4.0

List five (5) advantages of breaking down an annual budget into seasonal periods in accordance with

operating trends.Breakings down the annual budget into seasonal periods are quite important for the business. Some

of the advantage of it is as follows:

It becomes easier for the business to identify the performance in peak season and lean

seasons.

Sales growth of the business and changes in profitability position could be easily identified

through it.

Making the strategy and different policies at different time is easier through breaking down

the budgets.

The extra expenses of the business could be controlled.

Right uses and maximum uses of minimum resources could be done in an efficient way

(Madura, 2014).

The objective of this section is to demonstrate 2.0 Forecast estimates

Question 5

Jim Partners is an accounting firm that uses a credit system for charging its clients. Credit terms are

80% of fees are payable in the quarter in which they are incurred with the remaining 20% due the

following quarter.

Use the client hours demanded in the table to prepare the annual forecast. Include the net and GST

amounts. The opening accounts receivable is $70,000. Charge-out rates are Senior staff $150 per

hour and Junior staff $100 per hour.

September December March June

Senior 680 680 600 600

Junior 1,500 1,350 1,200 1,000

Jim Partners

Cash Receipts Forecast

Year ending 30 June 20XX

Opening

Balance

Accounts

Receivable

Hours

Senior

@

$150/hr

Hours

Junior

@

$100/hr

Total

Fees

Charged

Current Credit

Balance

Previous

Quarter

Total

Net GST

GST

70000

September

680 $

102,000

1500 $

150,000

$

252,000

$

201,600

$

70,000

$

246,909

$

24,691

December

680 $

102,000

1350 $

135,000

$

237,000

$

189,600

$

50,400

$

218,182

$

21,818

March

600 $

1200 $ $ $ $ $ $

Assessment Workbook – FNSACC503 6 | P a g e Version 4.0

90,000

120,000 210,000 168,000 47,400 195,818 19,582

June

600 $

90,000

1000 $

100,000

$

190,000

$

152,000

$

42,000

$

176,364

$

17,636

Closing

2560 $

384,000

5050 $

505,000

$

889,000

$

711,200

$

38,000

$

681,091

$

68,109

Question 6

Identify the relevant information you could use to complete a budget. Explain how the information

would help you anticipate changes in circumstancesIt is important for the business to measure the quantitative and qualitative data both in order to

prepare the budget for the business and maintain the position of the business. Some of the

important and relevant information of the business are as follows:

Staff information

Economical changes

Order and supply document

Revenue forecasting

Technological development

Population trends

Industry changes

Cash requirement (Moles, Parrino and Kidwekk, 2011)

Question 7A

Why is it important to establish correct assumptions and parameters within a budget?It is important in a business to establish correct parameters and assumptions in order to maintain

the performance of the business and prepare better budgetary reports. On the basis of the correct

parameters and assumptions, it becomes simple for the business to evaluate the exact performance

of the business and the variances among the actual and expected behaviour becomes less which

helps the business to meet the common goal of the business. It also improved the accuracy and the

understanding of the stakeholders in the business.

Question 7B

Explain how you would review assumptions for accuracy, relevance and compliance with the

organisational policy and procedures.In order to review the accuracy, compliance and relevance of the business, it is important for the

business to measure the actual performance of the business with the expected performance. It

could also be measured through evaluation on the coordination among the department and the

employees of the business. Each of the accounts must be accurately evaluated in the business so

that the relevancy and the compliance of that item could be improved in the business. Faulty

estimations, timing differences and poor controls must be avoided in the business in order to

manage the overall performance of the business and maintain the accuracy, compliance and

relevance of the business (Lumby and Jones, 2007).

Assessment Workbook – FNSACC503 7 | P a g e Version 4.0

120,000 210,000 168,000 47,400 195,818 19,582

June

600 $

90,000

1000 $

100,000

$

190,000

$

152,000

$

42,000

$

176,364

$

17,636

Closing

2560 $

384,000

5050 $

505,000

$

889,000

$

711,200

$

38,000

$

681,091

$

68,109

Question 6

Identify the relevant information you could use to complete a budget. Explain how the information

would help you anticipate changes in circumstancesIt is important for the business to measure the quantitative and qualitative data both in order to

prepare the budget for the business and maintain the position of the business. Some of the

important and relevant information of the business are as follows:

Staff information

Economical changes

Order and supply document

Revenue forecasting

Technological development

Population trends

Industry changes

Cash requirement (Moles, Parrino and Kidwekk, 2011)

Question 7A

Why is it important to establish correct assumptions and parameters within a budget?It is important in a business to establish correct parameters and assumptions in order to maintain

the performance of the business and prepare better budgetary reports. On the basis of the correct

parameters and assumptions, it becomes simple for the business to evaluate the exact performance

of the business and the variances among the actual and expected behaviour becomes less which

helps the business to meet the common goal of the business. It also improved the accuracy and the

understanding of the stakeholders in the business.

Question 7B

Explain how you would review assumptions for accuracy, relevance and compliance with the

organisational policy and procedures.In order to review the accuracy, compliance and relevance of the business, it is important for the

business to measure the actual performance of the business with the expected performance. It

could also be measured through evaluation on the coordination among the department and the

employees of the business. Each of the accounts must be accurately evaluated in the business so

that the relevancy and the compliance of that item could be improved in the business. Faulty

estimations, timing differences and poor controls must be avoided in the business in order to

manage the overall performance of the business and maintain the accuracy, compliance and

relevance of the business (Lumby and Jones, 2007).

Assessment Workbook – FNSACC503 7 | P a g e Version 4.0

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Question 8

Identify financial risks and initiate protection strategies in accordance with organisational

procedures and policy

National Camper Trailers (NCT), is a private company that sells camping trailers has had high revenue

season over the Christmas holiday period. They decide to offer terms of credit to attract customers

in the slower mid-year period to help with cash inflows.

The terms are 50% payable on purchase with the balance payable within one month after purchase.

New credit customers have been assigned by several different sales staff.

a. What are some of the Financial Risks that National Camper Trailers NCT would face by using

this strategy? (List a minimum of three)Some of the financial risk which would be faced by NCT after applying this strategy is as follows:

Reduction in the cash flows of the business as the business has to wait for the customers to

pay the amount which would reduce the ability to purchase replacement products from the

suppliers.

Reduction in profit margin: Funding the credit sales could reduce the profit margin of the

business as the different provision for bad debts are prepared by the business while offering

the products on credit (Weston and Brigham, 2015).

Large debts: Unpaid debts in an organization could pose a risk to the business.

b. As an NCT management staff, identify some protection strategies you would initiate to

mitigate the risks in accordance with NCT’s organisational policies and procedures. (List a

minimum of five)Being the management staff of NCT, some strategy have been suggested to mitigate the risk of the

business which are as follows:

Perform a credit check

Keep records of credit

Provided a prompt response in written

Decide whether to offer credit or not

Evaluate the record of all the debtors before offering them the goods on credit (Krantz,

2016)

The objective of this section is to demonstrate 3.0 Document budget

Question 9

You have been provided with the following information from that National Camper Trailers. Present

a break even analysis in a line graph and indicate how my units need to be sold to break even. (you

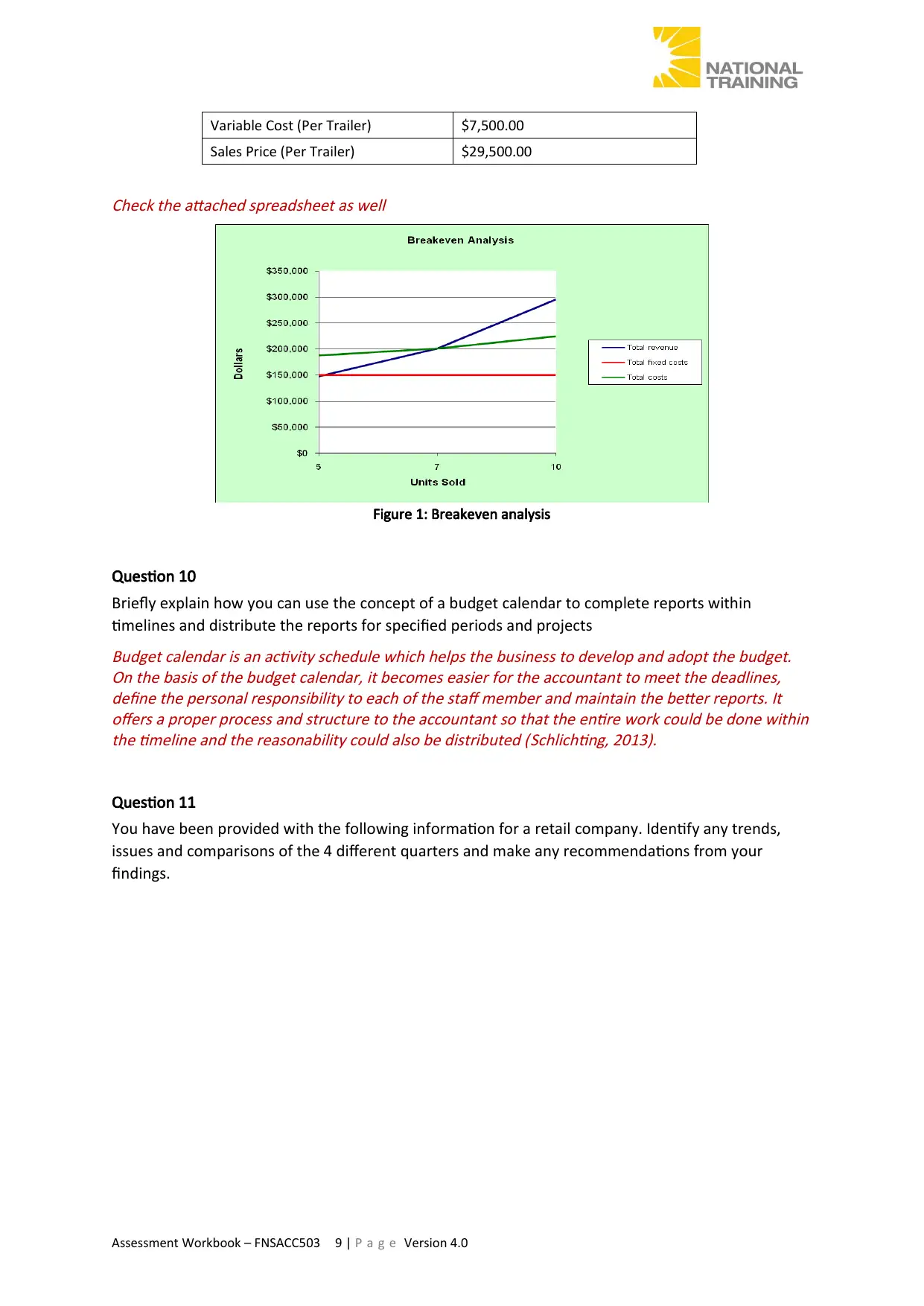

can perform the working on an excel spreadsheet and submit it as activity 9)

National Camper Trailers

Fixed Cost (Calendar Year) $150,000.00

Assessment Workbook – FNSACC503 8 | P a g e Version 4.0

Identify financial risks and initiate protection strategies in accordance with organisational

procedures and policy

National Camper Trailers (NCT), is a private company that sells camping trailers has had high revenue

season over the Christmas holiday period. They decide to offer terms of credit to attract customers

in the slower mid-year period to help with cash inflows.

The terms are 50% payable on purchase with the balance payable within one month after purchase.

New credit customers have been assigned by several different sales staff.

a. What are some of the Financial Risks that National Camper Trailers NCT would face by using

this strategy? (List a minimum of three)Some of the financial risk which would be faced by NCT after applying this strategy is as follows:

Reduction in the cash flows of the business as the business has to wait for the customers to

pay the amount which would reduce the ability to purchase replacement products from the

suppliers.

Reduction in profit margin: Funding the credit sales could reduce the profit margin of the

business as the different provision for bad debts are prepared by the business while offering

the products on credit (Weston and Brigham, 2015).

Large debts: Unpaid debts in an organization could pose a risk to the business.

b. As an NCT management staff, identify some protection strategies you would initiate to

mitigate the risks in accordance with NCT’s organisational policies and procedures. (List a

minimum of five)Being the management staff of NCT, some strategy have been suggested to mitigate the risk of the

business which are as follows:

Perform a credit check

Keep records of credit

Provided a prompt response in written

Decide whether to offer credit or not

Evaluate the record of all the debtors before offering them the goods on credit (Krantz,

2016)

The objective of this section is to demonstrate 3.0 Document budget

Question 9

You have been provided with the following information from that National Camper Trailers. Present

a break even analysis in a line graph and indicate how my units need to be sold to break even. (you

can perform the working on an excel spreadsheet and submit it as activity 9)

National Camper Trailers

Fixed Cost (Calendar Year) $150,000.00

Assessment Workbook – FNSACC503 8 | P a g e Version 4.0

Variable Cost (Per Trailer) $7,500.00

Sales Price (Per Trailer) $29,500.00

Check the attached spreadsheet as well

Figure 1: Breakeven analysis

Question 10

Briefly explain how you can use the concept of a budget calendar to complete reports within

timelines and distribute the reports for specified periods and projectsBudget calendar is an activity schedule which helps the business to develop and adopt the budget.

On the basis of the budget calendar, it becomes easier for the accountant to meet the deadlines,

define the personal responsibility to each of the staff member and maintain the better reports. It

offers a proper process and structure to the accountant so that the entire work could be done within

the timeline and the reasonability could also be distributed (Schlichting, 2013).

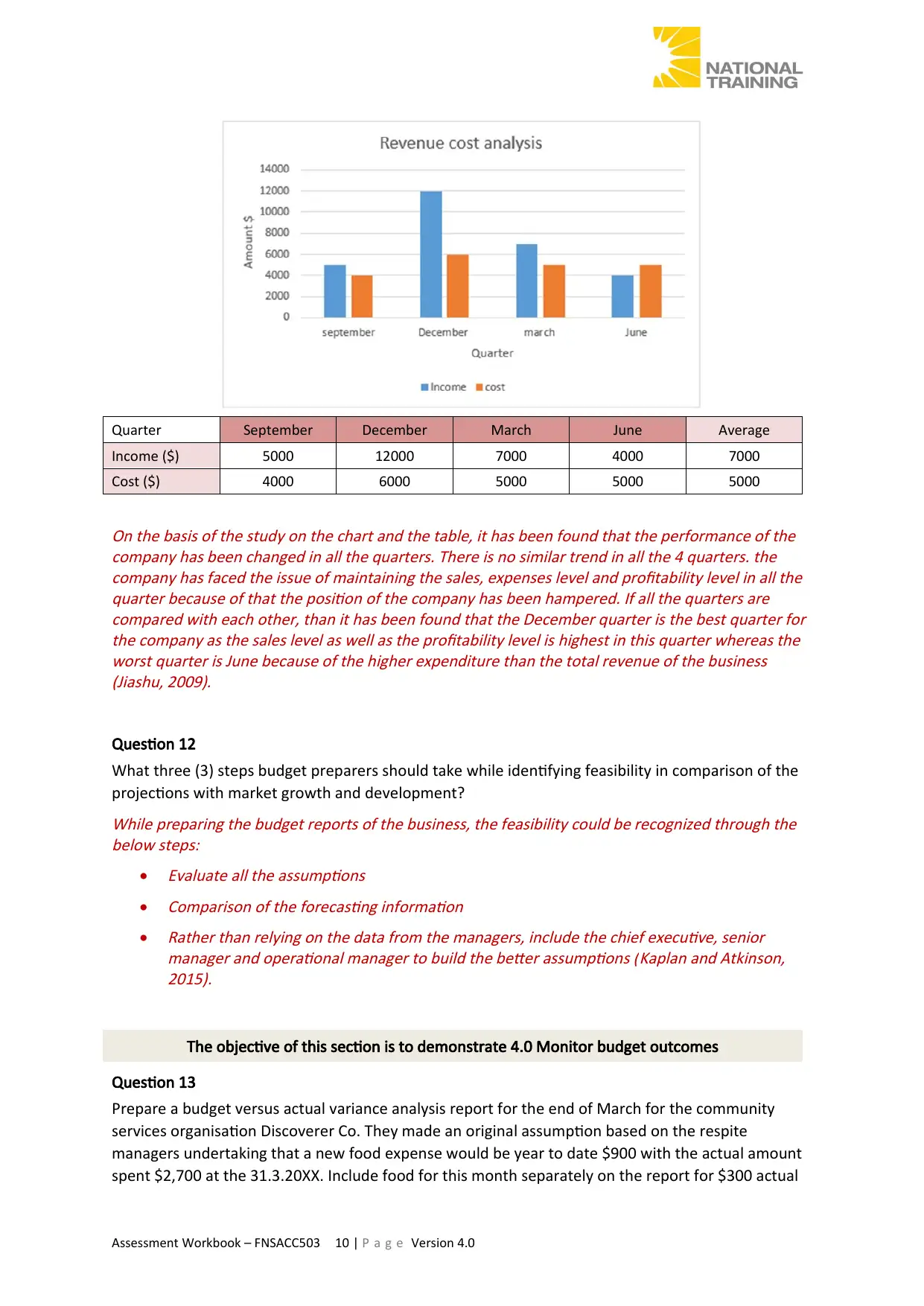

Question 11

You have been provided with the following information for a retail company. Identify any trends,

issues and comparisons of the 4 different quarters and make any recommendations from your

findings.

Assessment Workbook – FNSACC503 9 | P a g e Version 4.0

Sales Price (Per Trailer) $29,500.00

Check the attached spreadsheet as well

Figure 1: Breakeven analysis

Question 10

Briefly explain how you can use the concept of a budget calendar to complete reports within

timelines and distribute the reports for specified periods and projectsBudget calendar is an activity schedule which helps the business to develop and adopt the budget.

On the basis of the budget calendar, it becomes easier for the accountant to meet the deadlines,

define the personal responsibility to each of the staff member and maintain the better reports. It

offers a proper process and structure to the accountant so that the entire work could be done within

the timeline and the reasonability could also be distributed (Schlichting, 2013).

Question 11

You have been provided with the following information for a retail company. Identify any trends,

issues and comparisons of the 4 different quarters and make any recommendations from your

findings.

Assessment Workbook – FNSACC503 9 | P a g e Version 4.0

Quarter September December March June Average

Income ($) 5000 12000 7000 4000 7000

Cost ($) 4000 6000 5000 5000 5000

On the basis of the study on the chart and the table, it has been found that the performance of the

company has been changed in all the quarters. There is no similar trend in all the 4 quarters. the

company has faced the issue of maintaining the sales, expenses level and profitability level in all the

quarter because of that the position of the company has been hampered. If all the quarters are

compared with each other, than it has been found that the December quarter is the best quarter for

the company as the sales level as well as the profitability level is highest in this quarter whereas the

worst quarter is June because of the higher expenditure than the total revenue of the business

(Jiashu, 2009).

Question 12

What three (3) steps budget preparers should take while identifying feasibility in comparison of the

projections with market growth and development?While preparing the budget reports of the business, the feasibility could be recognized through the

below steps:

Evaluate all the assumptions

Comparison of the forecasting information

Rather than relying on the data from the managers, include the chief executive, senior

manager and operational manager to build the better assumptions (Kaplan and Atkinson,

2015).

The objective of this section is to demonstrate 4.0 Monitor budget outcomes

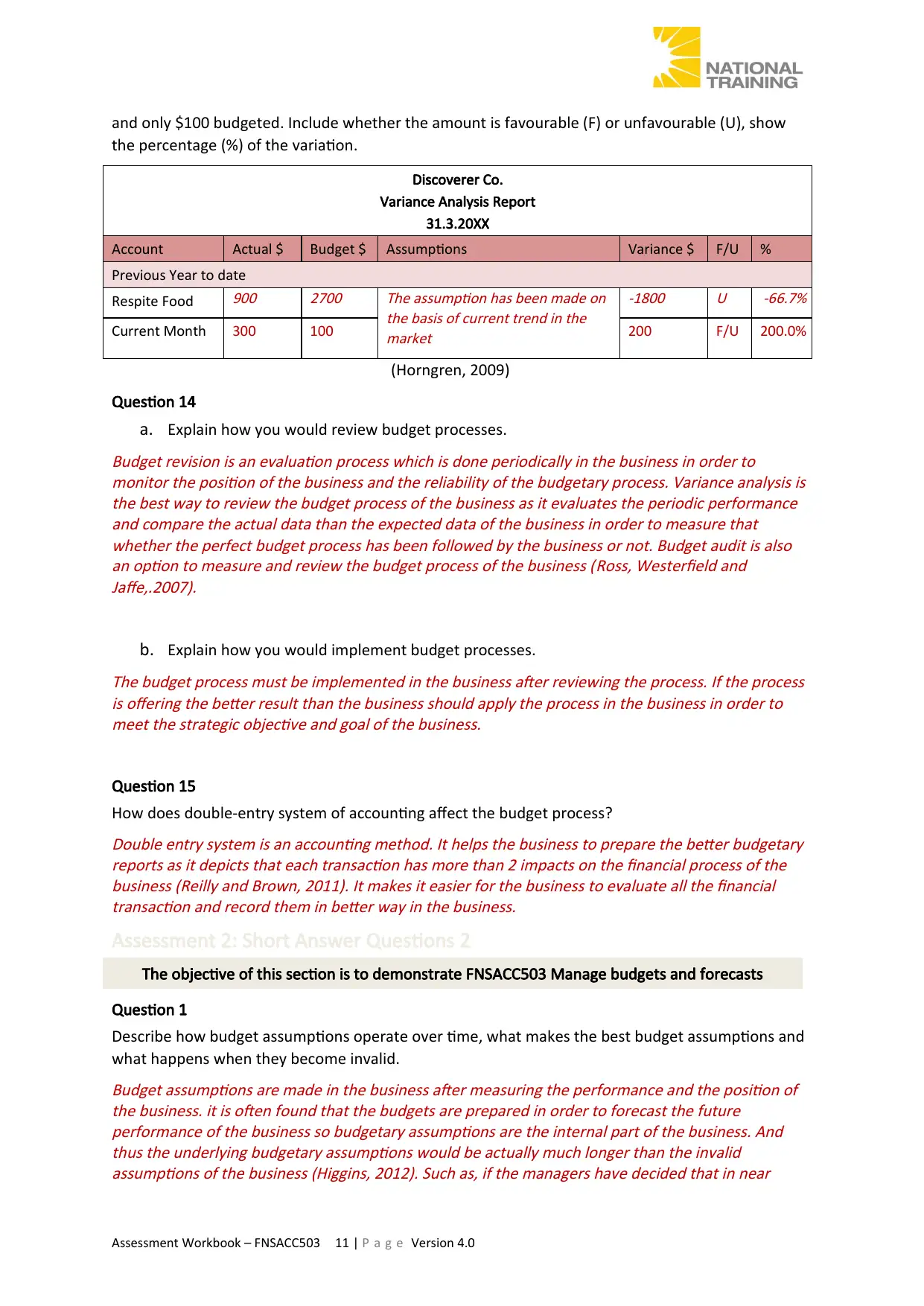

Question 13

Prepare a budget versus actual variance analysis report for the end of March for the community

services organisation Discoverer Co. They made an original assumption based on the respite

managers undertaking that a new food expense would be year to date $900 with the actual amount

spent $2,700 at the 31.3.20XX. Include food for this month separately on the report for $300 actual

Assessment Workbook – FNSACC503 10 | P a g e Version 4.0

Income ($) 5000 12000 7000 4000 7000

Cost ($) 4000 6000 5000 5000 5000

On the basis of the study on the chart and the table, it has been found that the performance of the

company has been changed in all the quarters. There is no similar trend in all the 4 quarters. the

company has faced the issue of maintaining the sales, expenses level and profitability level in all the

quarter because of that the position of the company has been hampered. If all the quarters are

compared with each other, than it has been found that the December quarter is the best quarter for

the company as the sales level as well as the profitability level is highest in this quarter whereas the

worst quarter is June because of the higher expenditure than the total revenue of the business

(Jiashu, 2009).

Question 12

What three (3) steps budget preparers should take while identifying feasibility in comparison of the

projections with market growth and development?While preparing the budget reports of the business, the feasibility could be recognized through the

below steps:

Evaluate all the assumptions

Comparison of the forecasting information

Rather than relying on the data from the managers, include the chief executive, senior

manager and operational manager to build the better assumptions (Kaplan and Atkinson,

2015).

The objective of this section is to demonstrate 4.0 Monitor budget outcomes

Question 13

Prepare a budget versus actual variance analysis report for the end of March for the community

services organisation Discoverer Co. They made an original assumption based on the respite

managers undertaking that a new food expense would be year to date $900 with the actual amount

spent $2,700 at the 31.3.20XX. Include food for this month separately on the report for $300 actual

Assessment Workbook – FNSACC503 10 | P a g e Version 4.0

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

and only $100 budgeted. Include whether the amount is favourable (F) or unfavourable (U), show

the percentage (%) of the variation.

Discoverer Co.

Variance Analysis Report

31.3.20XX

Account Actual $ Budget $ Assumptions Variance $ F/U %

Previous Year to date

Respite Food

900 2700 The assumption has been made on

the basis of current trend in the

market

-1800 U -66.7%

Current Month 300 100 200 F/U 200.0%

(Horngren, 2009)

Question 14

a. Explain how you would review budget processes.Budget revision is an evaluation process which is done periodically in the business in order to

monitor the position of the business and the reliability of the budgetary process. Variance analysis is

the best way to review the budget process of the business as it evaluates the periodic performance

and compare the actual data than the expected data of the business in order to measure that

whether the perfect budget process has been followed by the business or not. Budget audit is also

an option to measure and review the budget process of the business (Ross, Westerfield and

Jaffe,.2007).

b. Explain how you would implement budget processes.The budget process must be implemented in the business after reviewing the process. If the process

is offering the better result than the business should apply the process in the business in order to

meet the strategic objective and goal of the business.

Question 15

How does double-entry system of accounting affect the budget process?Double entry system is an accounting method. It helps the business to prepare the better budgetary

reports as it depicts that each transaction has more than 2 impacts on the financial process of the

business (Reilly and Brown, 2011). It makes it easier for the business to evaluate all the financial

transaction and record them in better way in the business.

Assessment 2: Short Answer Questions 2

The objective of this section is to demonstrate FNSACC503 Manage budgets and forecasts

Question 1

Describe how budget assumptions operate over time, what makes the best budget assumptions and

what happens when they become invalid.Budget assumptions are made in the business after measuring the performance and the position of

the business. it is often found that the budgets are prepared in order to forecast the future

performance of the business so budgetary assumptions are the internal part of the business. And

thus the underlying budgetary assumptions would be actually much longer than the invalid

assumptions of the business (Higgins, 2012). Such as, if the managers have decided that in near

Assessment Workbook – FNSACC503 11 | P a g e Version 4.0

the percentage (%) of the variation.

Discoverer Co.

Variance Analysis Report

31.3.20XX

Account Actual $ Budget $ Assumptions Variance $ F/U %

Previous Year to date

Respite Food

900 2700 The assumption has been made on

the basis of current trend in the

market

-1800 U -66.7%

Current Month 300 100 200 F/U 200.0%

(Horngren, 2009)

Question 14

a. Explain how you would review budget processes.Budget revision is an evaluation process which is done periodically in the business in order to

monitor the position of the business and the reliability of the budgetary process. Variance analysis is

the best way to review the budget process of the business as it evaluates the periodic performance

and compare the actual data than the expected data of the business in order to measure that

whether the perfect budget process has been followed by the business or not. Budget audit is also

an option to measure and review the budget process of the business (Ross, Westerfield and

Jaffe,.2007).

b. Explain how you would implement budget processes.The budget process must be implemented in the business after reviewing the process. If the process

is offering the better result than the business should apply the process in the business in order to

meet the strategic objective and goal of the business.

Question 15

How does double-entry system of accounting affect the budget process?Double entry system is an accounting method. It helps the business to prepare the better budgetary

reports as it depicts that each transaction has more than 2 impacts on the financial process of the

business (Reilly and Brown, 2011). It makes it easier for the business to evaluate all the financial

transaction and record them in better way in the business.

Assessment 2: Short Answer Questions 2

The objective of this section is to demonstrate FNSACC503 Manage budgets and forecasts

Question 1

Describe how budget assumptions operate over time, what makes the best budget assumptions and

what happens when they become invalid.Budget assumptions are made in the business after measuring the performance and the position of

the business. it is often found that the budgets are prepared in order to forecast the future

performance of the business so budgetary assumptions are the internal part of the business. And

thus the underlying budgetary assumptions would be actually much longer than the invalid

assumptions of the business (Higgins, 2012). Such as, if the managers have decided that in near

Assessment Workbook – FNSACC503 11 | P a g e Version 4.0

future the sales of the business would be improved by 5% and thus they have improved the cost of

the business by 5% as well than it is invalid because cost amount contains the fixed and variable

both cost. Wrong assumptions affect thee budgetary reports and the financial expectation level of

the business.

Question 2

Suppose several additional junior staff are employed in subsequent years after a new business is

established. The owner notices a large increase in the motor vehicle expense account. What changes

to assumptions or controls would you recommend?is several junior staff has been employed by the business in subsequent years after establishing the

new business and it has been noticed by the owner that the expenses account of the business has

been improved than it is recommended to the business to control over the motor vehicle and covey

to the staff that the motor vehicle of the business must not be used so often. it must be used by the

employees only in need (Gapenski, 2008).

Question 3

When researching information to complete the cash flow budget, what needs to be consideredWhile researching on the cash flow budget, below information must be considered by the business:

Forecast the income, expenditure and the net profit of the business

Current loan repayment

adjustment for non cash expenses of the business such as depreciation

Estimated payment of accounts payable and taxes

Anticipated collection of debtors amount (Barlow, 2006)

Question 4

How should budget assumptions be dealt with to guard against unethical assumptions?In order to guard against the unethical assumptions, a business should organize a committed which

evaluates the company’s responsibilities to its employees and the range of stakeholders. This

committee must make sure that no offensive and unethical practices must be done by the business

and its employees. The budgetary decision also involves the choices between earning extra money

and dealing with the consequences of the strategy and policy of the company. The committee must

ensure that no such activities could take place in the business (Hillier, Grinblatt and Titman, 2011).

Question 5

You have been asked by the owner of a new consultancy called Voyager to prepare the master

budget. The consultancy consists of the owner who charges out at $68 per hour and the junior staff

who are charged out at $42 per hour. The owner has advised you that the following hours are

forecast for each quarter.

The consultancy has a credit system of payments with 60% of payment received the quarter in which

they are earned and the remaining 40% earned the following month. The opening accounts

receivable is $13,200 incl GST. The GST is accounted for on an accrual basis.

Assessment Workbook – FNSACC503 12 | P a g e Version 4.0

the business by 5% as well than it is invalid because cost amount contains the fixed and variable

both cost. Wrong assumptions affect thee budgetary reports and the financial expectation level of

the business.

Question 2

Suppose several additional junior staff are employed in subsequent years after a new business is

established. The owner notices a large increase in the motor vehicle expense account. What changes

to assumptions or controls would you recommend?is several junior staff has been employed by the business in subsequent years after establishing the

new business and it has been noticed by the owner that the expenses account of the business has

been improved than it is recommended to the business to control over the motor vehicle and covey

to the staff that the motor vehicle of the business must not be used so often. it must be used by the

employees only in need (Gapenski, 2008).

Question 3

When researching information to complete the cash flow budget, what needs to be consideredWhile researching on the cash flow budget, below information must be considered by the business:

Forecast the income, expenditure and the net profit of the business

Current loan repayment

adjustment for non cash expenses of the business such as depreciation

Estimated payment of accounts payable and taxes

Anticipated collection of debtors amount (Barlow, 2006)

Question 4

How should budget assumptions be dealt with to guard against unethical assumptions?In order to guard against the unethical assumptions, a business should organize a committed which

evaluates the company’s responsibilities to its employees and the range of stakeholders. This

committee must make sure that no offensive and unethical practices must be done by the business

and its employees. The budgetary decision also involves the choices between earning extra money

and dealing with the consequences of the strategy and policy of the company. The committee must

ensure that no such activities could take place in the business (Hillier, Grinblatt and Titman, 2011).

Question 5

You have been asked by the owner of a new consultancy called Voyager to prepare the master

budget. The consultancy consists of the owner who charges out at $68 per hour and the junior staff

who are charged out at $42 per hour. The owner has advised you that the following hours are

forecast for each quarter.

The consultancy has a credit system of payments with 60% of payment received the quarter in which

they are earned and the remaining 40% earned the following month. The opening accounts

receivable is $13,200 incl GST. The GST is accounted for on an accrual basis.

Assessment Workbook – FNSACC503 12 | P a g e Version 4.0

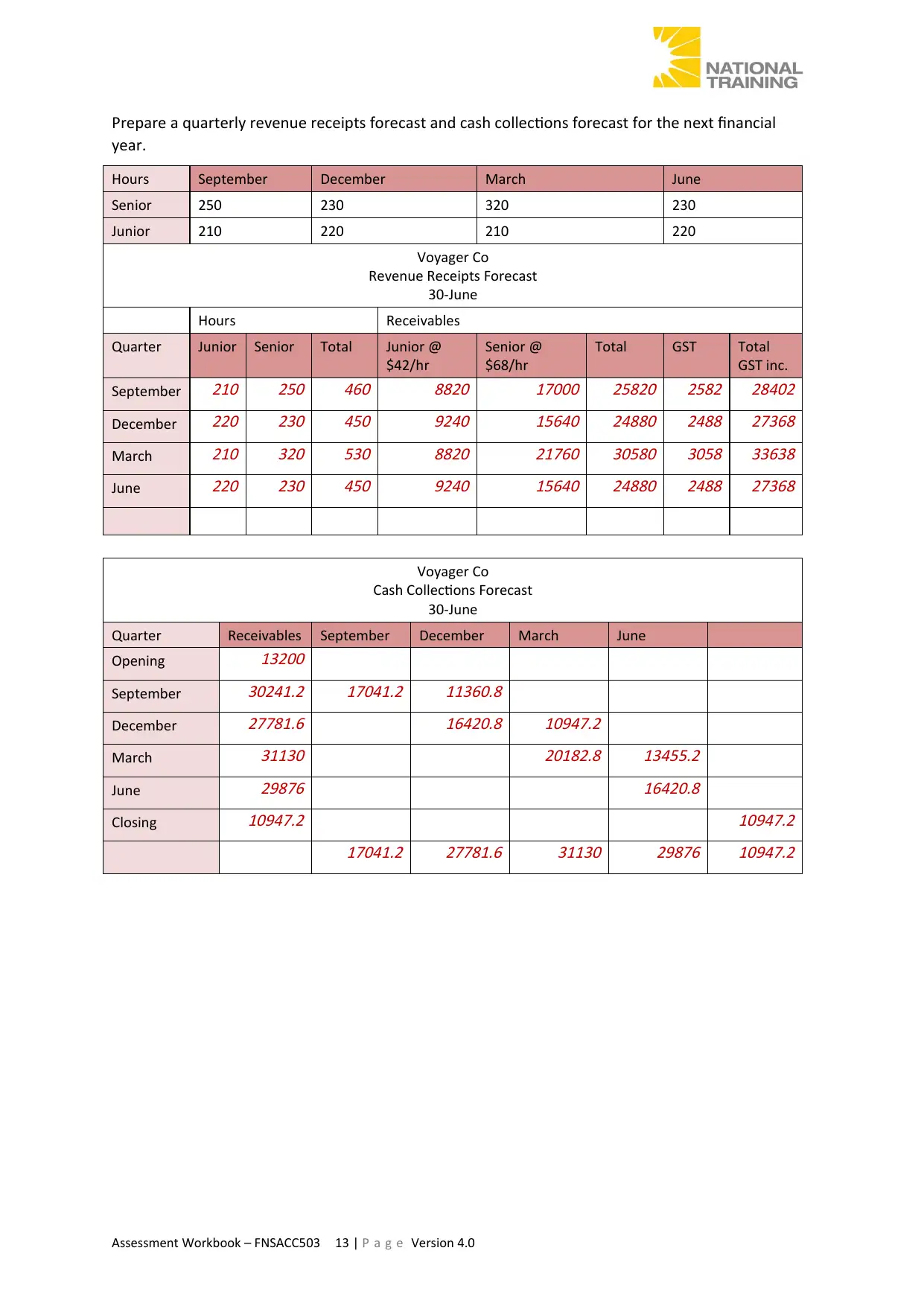

Prepare a quarterly revenue receipts forecast and cash collections forecast for the next financial

year.

Hours September December March June

Senior 250 230 320 230

Junior 210 220 210 220

Voyager Co

Revenue Receipts Forecast

30-June

Hours Receivables

Quarter Junior Senior Total Junior @

$42/hr

Senior @

$68/hr

Total GST Total

GST inc.

September

210 250 460 8820

17000 25820 2582 28402

December

220 230 450 9240

15640 24880 2488 27368

March

210 320 530 8820

21760 30580 3058 33638

June

220 230 450 9240

15640 24880 2488 27368

Voyager Co

Cash Collections Forecast

30-June

Quarter Receivables September December March June

Opening

13200

September

30241.2 17041.2 11360.8

December

27781.6

16420.8 10947.2

March

31130

20182.8 13455.2

June

29876

16420.8

Closing

10947.2

10947.2

17041.2 27781.6 31130 29876 10947.2

Assessment Workbook – FNSACC503 13 | P a g e Version 4.0

year.

Hours September December March June

Senior 250 230 320 230

Junior 210 220 210 220

Voyager Co

Revenue Receipts Forecast

30-June

Hours Receivables

Quarter Junior Senior Total Junior @

$42/hr

Senior @

$68/hr

Total GST Total

GST inc.

September

210 250 460 8820

17000 25820 2582 28402

December

220 230 450 9240

15640 24880 2488 27368

March

210 320 530 8820

21760 30580 3058 33638

June

220 230 450 9240

15640 24880 2488 27368

Voyager Co

Cash Collections Forecast

30-June

Quarter Receivables September December March June

Opening

13200

September

30241.2 17041.2 11360.8

December

27781.6

16420.8 10947.2

March

31130

20182.8 13455.2

June

29876

16420.8

Closing

10947.2

10947.2

17041.2 27781.6 31130 29876 10947.2

Assessment Workbook – FNSACC503 13 | P a g e Version 4.0

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

References:

Barlow.J.F.,2006. Excel models for business and operations management, 2nd edition, John Wiley

and sons ltd, England

Gapenski, L.C., 2008.

Healthcare finance: an introduction to accounting and financial management.

Health Administration Press.

Higgins, R. C., 2012.

Analysis for financial management. McGraw-Hill/Irwin.

Hillier, D., Grinblatt, M. and Titman, S., 2011.

Financial markets and corporate strategy. McGraw Hill.

Horngren, C.T., 2009.

Cost accounting: A managerial emphasis, 13/e. Pearson Education India.

Jiashu, G., 2009. Study on Fair Value Accounting——on the essential characteristics of financial

accounting [J].

Accounting Research,

5, p.003.

Kaplan, R.S. and Atkinson, A.A., 2015.

Advanced management accounting. PHI Learning.

Krantz, M. 2016.

Fundamental Analysis for Dummies. London: John Wiley and Sons.

Lord, B.R., 2007. Strategic management accounting.

Issues in Management Accounting,

3.

Lumby,S and Jones,C,.2007. Corporate finance theory and practice, 7th edition, Thomson, London

Madura, J. 2014.

Financial Markets and Institutions. Cengage Learning.

Moles, P. Parrino, R and Kidwekk, D,.2011. Corporate finance, European edition, John Wiley andsons,

United Kingdom

Reilly.F.K and Brown.K.C,.2011,Investment analysis and portfolio management,10th edition, South

western Cengage learning, India

Ross, S, A,. Westerfield, R, W,. and Jaffe, J,.2007, Corporate Finance, the McGraw-hill, India

Schlichting, T. 2013.

Fundamental Analysis, Behavioral Finance and Technical Analysis on the Stock

Market. GRIN Verlag.

Ward, K., 2012.

Strategic management accounting. Australia: Routledge.

Weaver, S.C., Weston, J.F. and Weaver, S., 2001.

Finance and accounting for nonfinancial managers.

New York: McGraw-Hill.

Weston, J.F. and Brigham, E.F., 2015.

Managerial finance. Hinsdale, IL: Dryden Press.

Zimmerman, J.L. and Yahya-Zadeh, M., 2011. Accounting for decision making and control.

Issues in

Accounting Education,

26(1), pp.258-259.

Assessment Workbook – FNSACC503 14 | P a g e Version 4.0

Barlow.J.F.,2006. Excel models for business and operations management, 2nd edition, John Wiley

and sons ltd, England

Gapenski, L.C., 2008.

Healthcare finance: an introduction to accounting and financial management.

Health Administration Press.

Higgins, R. C., 2012.

Analysis for financial management. McGraw-Hill/Irwin.

Hillier, D., Grinblatt, M. and Titman, S., 2011.

Financial markets and corporate strategy. McGraw Hill.

Horngren, C.T., 2009.

Cost accounting: A managerial emphasis, 13/e. Pearson Education India.

Jiashu, G., 2009. Study on Fair Value Accounting——on the essential characteristics of financial

accounting [J].

Accounting Research,

5, p.003.

Kaplan, R.S. and Atkinson, A.A., 2015.

Advanced management accounting. PHI Learning.

Krantz, M. 2016.

Fundamental Analysis for Dummies. London: John Wiley and Sons.

Lord, B.R., 2007. Strategic management accounting.

Issues in Management Accounting,

3.

Lumby,S and Jones,C,.2007. Corporate finance theory and practice, 7th edition, Thomson, London

Madura, J. 2014.

Financial Markets and Institutions. Cengage Learning.

Moles, P. Parrino, R and Kidwekk, D,.2011. Corporate finance, European edition, John Wiley andsons,

United Kingdom

Reilly.F.K and Brown.K.C,.2011,Investment analysis and portfolio management,10th edition, South

western Cengage learning, India

Ross, S, A,. Westerfield, R, W,. and Jaffe, J,.2007, Corporate Finance, the McGraw-hill, India

Schlichting, T. 2013.

Fundamental Analysis, Behavioral Finance and Technical Analysis on the Stock

Market. GRIN Verlag.

Ward, K., 2012.

Strategic management accounting. Australia: Routledge.

Weaver, S.C., Weston, J.F. and Weaver, S., 2001.

Finance and accounting for nonfinancial managers.

New York: McGraw-Hill.

Weston, J.F. and Brigham, E.F., 2015.

Managerial finance. Hinsdale, IL: Dryden Press.

Zimmerman, J.L. and Yahya-Zadeh, M., 2011. Accounting for decision making and control.

Issues in

Accounting Education,

26(1), pp.258-259.

Assessment Workbook – FNSACC503 14 | P a g e Version 4.0

Assessment Workbook – FNSACC503 15 | P a g e Version 4.0

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.