FNSACC601 Prepare and Administer Tax Documentation for Legal Entities Final Assessment

VerifiedAdded on 2023/06/17

|12

|3068

|369

AI Summary

The article covers theory questions and practical activities related to FNSACC601 final assessment on tax documentation for legal entities. It includes topics such as tax legislation, managing conflicts of interest, supporting documentation, and practical activities. The practical activities include preparing statements, calculating net tax payable, and distribution schedules.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Assessment Instructions for the Candidate

Requirements:

Access to a computer loaded with Microsoft Word and Excel

Access to an email system

Calculator

Assessment Conditions:

Your assessment can be completed in the program of your choice such as

Microsoft Word or Excel.

It is recommended that on completion of this unit, participants should be able to

produce accurate work with not more than three re-submissions.

On completion

Upload your assessment document to the online platform.

Remember to name the document to include the following: Unit name and number -

assessment name and number - your name.

Assessment Outcomes

There are only two possible results of any assessment:

Competent

Not yet competent

Competent

An assessment of ‘Competent’ recognises that you have clearly demonstrated to your

assessor that you have current skills and knowledge as outlined in the units of competency

for which application was made.

Not Yet Competent

If an assessment of ‘Not Yet Competent’ is made, the assessor will give you specific feedback

as to the reasons for the result. This will also provide information about gaps found in the

assessment of competency. You may also discuss options to address the gaps in competency

with your assessor.

FNSACC601 - Prepare and Administer Tax

Documentation for Legal Entities

Final Assessment

Requirements:

Access to a computer loaded with Microsoft Word and Excel

Access to an email system

Calculator

Assessment Conditions:

Your assessment can be completed in the program of your choice such as

Microsoft Word or Excel.

It is recommended that on completion of this unit, participants should be able to

produce accurate work with not more than three re-submissions.

On completion

Upload your assessment document to the online platform.

Remember to name the document to include the following: Unit name and number -

assessment name and number - your name.

Assessment Outcomes

There are only two possible results of any assessment:

Competent

Not yet competent

Competent

An assessment of ‘Competent’ recognises that you have clearly demonstrated to your

assessor that you have current skills and knowledge as outlined in the units of competency

for which application was made.

Not Yet Competent

If an assessment of ‘Not Yet Competent’ is made, the assessor will give you specific feedback

as to the reasons for the result. This will also provide information about gaps found in the

assessment of competency. You may also discuss options to address the gaps in competency

with your assessor.

FNSACC601 - Prepare and Administer Tax

Documentation for Legal Entities

Final Assessment

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Prepare and Administer Tax Documentation for Legal Entities

Page 2 of 11

PART A – Theory Questions

(a) Explain how the following have a role in interpreting and applying tax legislation in

Australia.

Ensure you include both a description and the role they have in assisting to interpret the

legislation.

Public and private rulings and determination

Court and tribunal decisions

(b) Describe the three (3) methods specified by the TPB, for tax agents to manage conflicts

of interest

The public and private ruling has a crucial role in interpreting and applying tax

legislation. The public ruling is being defined as the binding interpretations relating to tax law

and this assist in interpretation of statement and guidelines. On the other side, the private

ruling is the one which only applies to the certain taxpayers only but after the application is

being provided by taxpayer for ruling. Both the public and private ruling is assistive in

interpreting the legislation as both these ruling involves the titles being used in the tax law.

For instance, TR in tax law interprets taxation ruling, LCR is law companion ruling, GSTR is GST

ruling and similar kind of rulings. Along with this the private ruling assist in interpreting the

fact that how a tax law is applied in respect to some specific scheme.

Court and tribunal are the regulatory bodies which provide justice and their final

judgment. This is essential for the reason that when any case is being handled by the case

then all the decision will be made by the related court and tribunal. Thus, it is very essential

for the court and tribunal to decide for the case to be solved in proper and justified manner.

The reason pertaining to the fact is that court and tribunal knows what needs to be done and

how the case will be solved. Thus, it plays an important role within the analysis and solving the

case of the people.

The first measure is to avoid that is the agent can try to avoid the situation and

conflict. This is the situation where the solution to the conflict of interest is not

controllable.

Along with this another method specified by the TPB for the management of conflict

Moreover, in addition to this disclosing is another way in which conflict can be

managed in proper and effective manner. This is particularly because when the

sufficient information is being provided then there will not be any situation of meeting

conflict.

Page 2 of 11

PART A – Theory Questions

(a) Explain how the following have a role in interpreting and applying tax legislation in

Australia.

Ensure you include both a description and the role they have in assisting to interpret the

legislation.

Public and private rulings and determination

Court and tribunal decisions

(b) Describe the three (3) methods specified by the TPB, for tax agents to manage conflicts

of interest

The public and private ruling has a crucial role in interpreting and applying tax

legislation. The public ruling is being defined as the binding interpretations relating to tax law

and this assist in interpretation of statement and guidelines. On the other side, the private

ruling is the one which only applies to the certain taxpayers only but after the application is

being provided by taxpayer for ruling. Both the public and private ruling is assistive in

interpreting the legislation as both these ruling involves the titles being used in the tax law.

For instance, TR in tax law interprets taxation ruling, LCR is law companion ruling, GSTR is GST

ruling and similar kind of rulings. Along with this the private ruling assist in interpreting the

fact that how a tax law is applied in respect to some specific scheme.

Court and tribunal are the regulatory bodies which provide justice and their final

judgment. This is essential for the reason that when any case is being handled by the case

then all the decision will be made by the related court and tribunal. Thus, it is very essential

for the court and tribunal to decide for the case to be solved in proper and justified manner.

The reason pertaining to the fact is that court and tribunal knows what needs to be done and

how the case will be solved. Thus, it plays an important role within the analysis and solving the

case of the people.

The first measure is to avoid that is the agent can try to avoid the situation and

conflict. This is the situation where the solution to the conflict of interest is not

controllable.

Along with this another method specified by the TPB for the management of conflict

Moreover, in addition to this disclosing is another way in which conflict can be

managed in proper and effective manner. This is particularly because when the

sufficient information is being provided then there will not be any situation of meeting

conflict.

Prepare and Administer Tax Documentation for Legal Entities

Page 3 of 11

(c) Indicate the supporting documentation the ATO might ask to be provided, to verify the

amounts included in the tax return for each of the following:

Assessable income

The support document which is necessary for the person to provide for the verification of

assessable income involves salary or wage slip including the employer name and address,

contact number and copies of original payment summary. In addition to this, it will also be

required for the person to present the original bank statement and original documents.

Deductions

For the deduction as well there are different support documents which need to be analyzed

and evaluated. This involves work related car expense which includes all the details of the

kilometer per car worked, per year income, copy of purchase or lease document for the

vehicles, car registration certificate and other related documents. Along with this, in case

there is any kind of travel expenses being undertaken by the person then its documents will

be required for the effective management of the work.

To establish a valid distribution has been made by a Family Trust, in particular:

The recipient is a beneficiary

Where and when the distribution decided/declared

When and how the distribution was settled (i.e. was it paid or otherwise

accounted for).

In case when recipient is beneficiary then in that case the net income of the trust will

be taxed depending on the fact that whether beneficiary is entitled to the income of trust or

not. In case the trust is having the derived capital gain or franked distribution then in that case

trustee has streamed the beneficiary

When the distribution is decided then the beneficiary will get the declared amount in

the intended manner.

Along with this the distribution or the settlement will take place in the intended

manner. This is necessary because of the reason that when the trustee has failed to provide

the final accounting then a petition can be found in order compels the trust to provide the

share.

To establish a complying SMSF has accounted for and correctly included all

contributions

(Note: it would not be less than a Tax Agent would require to prepare and lodge the

return)

This is also very essential for the person to comply with SMSF that is self- managed

super fund. This is particularly because of the reason that SMSF is the Australian

Page 3 of 11

(c) Indicate the supporting documentation the ATO might ask to be provided, to verify the

amounts included in the tax return for each of the following:

Assessable income

The support document which is necessary for the person to provide for the verification of

assessable income involves salary or wage slip including the employer name and address,

contact number and copies of original payment summary. In addition to this, it will also be

required for the person to present the original bank statement and original documents.

Deductions

For the deduction as well there are different support documents which need to be analyzed

and evaluated. This involves work related car expense which includes all the details of the

kilometer per car worked, per year income, copy of purchase or lease document for the

vehicles, car registration certificate and other related documents. Along with this, in case

there is any kind of travel expenses being undertaken by the person then its documents will

be required for the effective management of the work.

To establish a valid distribution has been made by a Family Trust, in particular:

The recipient is a beneficiary

Where and when the distribution decided/declared

When and how the distribution was settled (i.e. was it paid or otherwise

accounted for).

In case when recipient is beneficiary then in that case the net income of the trust will

be taxed depending on the fact that whether beneficiary is entitled to the income of trust or

not. In case the trust is having the derived capital gain or franked distribution then in that case

trustee has streamed the beneficiary

When the distribution is decided then the beneficiary will get the declared amount in

the intended manner.

Along with this the distribution or the settlement will take place in the intended

manner. This is necessary because of the reason that when the trustee has failed to provide

the final accounting then a petition can be found in order compels the trust to provide the

share.

To establish a complying SMSF has accounted for and correctly included all

contributions

(Note: it would not be less than a Tax Agent would require to prepare and lodge the

return)

This is also very essential for the person to comply with SMSF that is self- managed

super fund. This is particularly because of the reason that SMSF is the Australian

Prepare and Administer Tax Documentation for Legal Entities

Page 4 of 11

superannuation fund during the income year and not have been issued the SMSF with the

notice of non- compliance. There are various documents which need to be presented at the

time of taxation. All the document need to be managed and listed in proper manner as this

will outline all the details of the person in proper and effective manner.

Page 4 of 11

superannuation fund during the income year and not have been issued the SMSF with the

notice of non- compliance. There are various documents which need to be presented at the

time of taxation. All the document need to be managed and listed in proper manner as this

will outline all the details of the person in proper and effective manner.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Prepare and Administer Tax Documentation for Legal Entities

Page 5 of 11

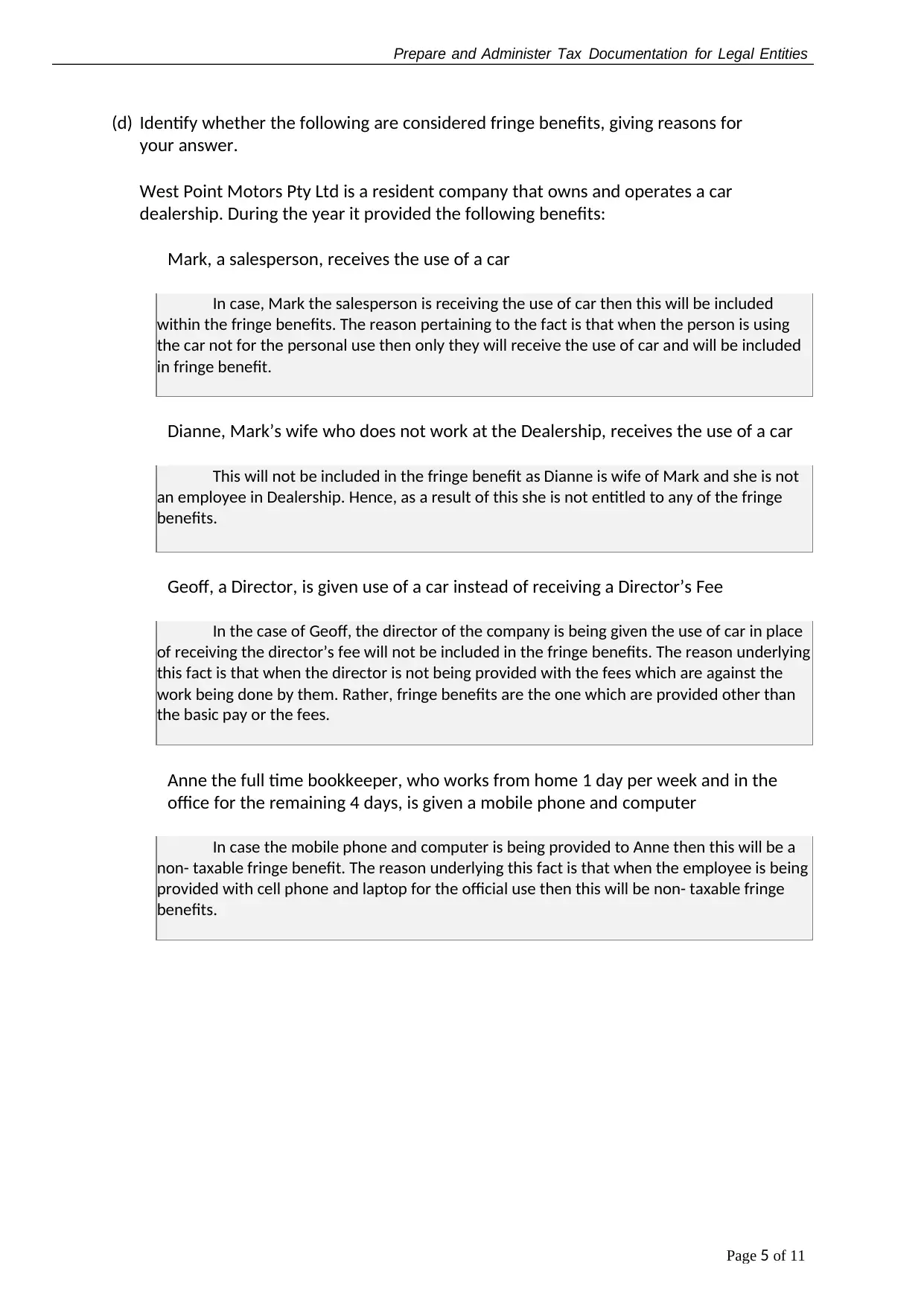

(d) Identify whether the following are considered fringe benefits, giving reasons for

your answer.

West Point Motors Pty Ltd is a resident company that owns and operates a car

dealership. During the year it provided the following benefits:

Mark, a salesperson, receives the use of a car

In case, Mark the salesperson is receiving the use of car then this will be included

within the fringe benefits. The reason pertaining to the fact is that when the person is using

the car not for the personal use then only they will receive the use of car and will be included

in fringe benefit.

Dianne, Mark’s wife who does not work at the Dealership, receives the use of a car

This will not be included in the fringe benefit as Dianne is wife of Mark and she is not

an employee in Dealership. Hence, as a result of this she is not entitled to any of the fringe

benefits.

Geoff, a Director, is given use of a car instead of receiving a Director’s Fee

In the case of Geoff, the director of the company is being given the use of car in place

of receiving the director’s fee will not be included in the fringe benefits. The reason underlying

this fact is that when the director is not being provided with the fees which are against the

work being done by them. Rather, fringe benefits are the one which are provided other than

the basic pay or the fees.

Anne the full time bookkeeper, who works from home 1 day per week and in the

office for the remaining 4 days, is given a mobile phone and computer

In case the mobile phone and computer is being provided to Anne then this will be a

non- taxable fringe benefit. The reason underlying this fact is that when the employee is being

provided with cell phone and laptop for the official use then this will be non- taxable fringe

benefits.

Page 5 of 11

(d) Identify whether the following are considered fringe benefits, giving reasons for

your answer.

West Point Motors Pty Ltd is a resident company that owns and operates a car

dealership. During the year it provided the following benefits:

Mark, a salesperson, receives the use of a car

In case, Mark the salesperson is receiving the use of car then this will be included

within the fringe benefits. The reason pertaining to the fact is that when the person is using

the car not for the personal use then only they will receive the use of car and will be included

in fringe benefit.

Dianne, Mark’s wife who does not work at the Dealership, receives the use of a car

This will not be included in the fringe benefit as Dianne is wife of Mark and she is not

an employee in Dealership. Hence, as a result of this she is not entitled to any of the fringe

benefits.

Geoff, a Director, is given use of a car instead of receiving a Director’s Fee

In the case of Geoff, the director of the company is being given the use of car in place

of receiving the director’s fee will not be included in the fringe benefits. The reason underlying

this fact is that when the director is not being provided with the fees which are against the

work being done by them. Rather, fringe benefits are the one which are provided other than

the basic pay or the fees.

Anne the full time bookkeeper, who works from home 1 day per week and in the

office for the remaining 4 days, is given a mobile phone and computer

In case the mobile phone and computer is being provided to Anne then this will be a

non- taxable fringe benefit. The reason underlying this fact is that when the employee is being

provided with cell phone and laptop for the official use then this will be non- taxable fringe

benefits.

Prepare and Administer Tax Documentation for Legal Entities

Page 6 of 11

PART B – Practical Activities

You are currently employed as a Tax Agent for a local Accounting Firm (Tax Agent number

12345678). Your clients include individuals (salary & wage earners and sole traders) as

well as companies, trusts and partnerships.

The policies and procedures of your firm require you to use the Microsoft Excel templates

provided to complete your calculations. The ATO website should be used to verify current

tax legislation and to seek advice and guidance.

All client communications should be via email. Client details required to complete the

Individual Tax Return are recorded on a new client details form.

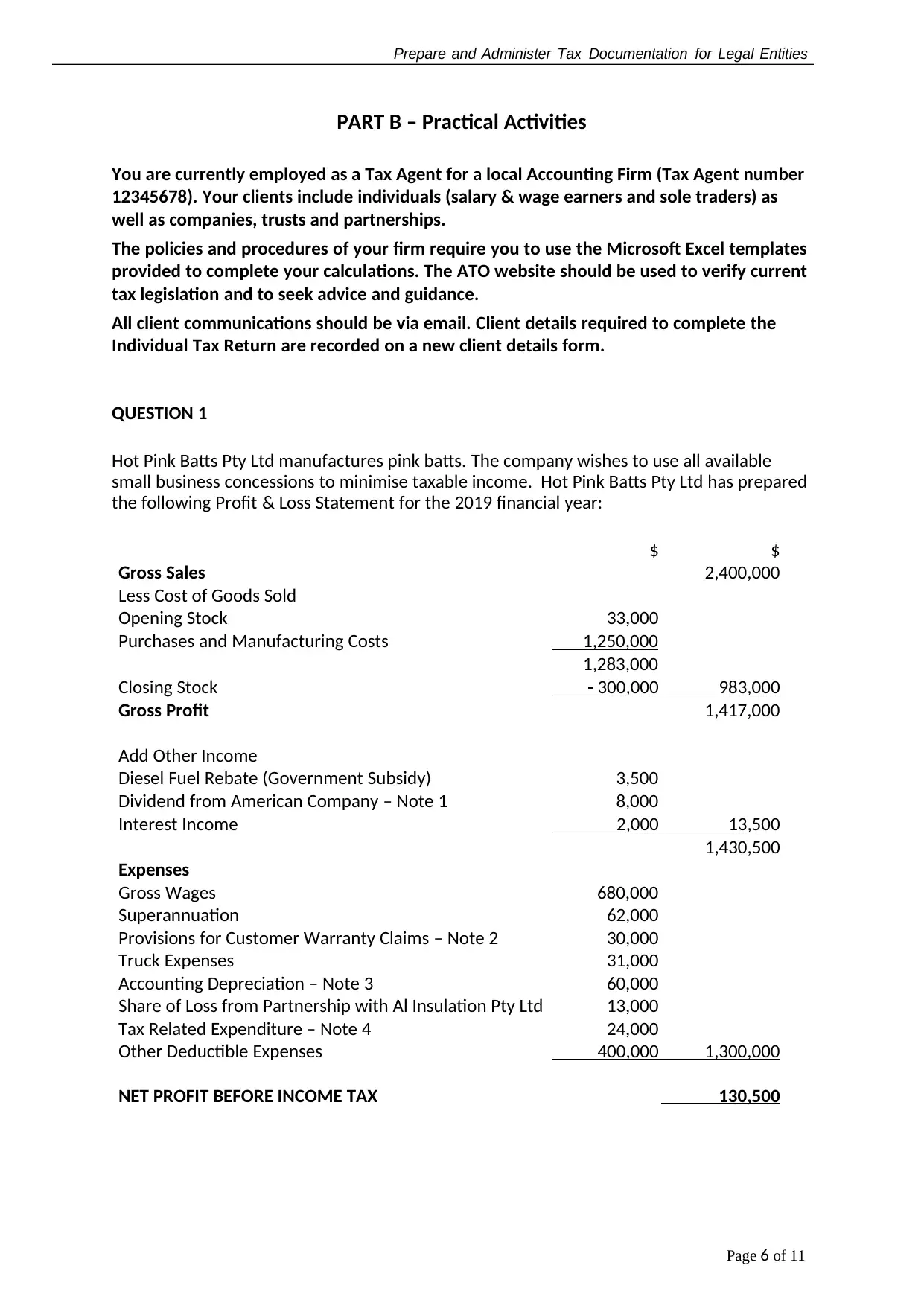

QUESTION 1

Hot Pink Batts Pty Ltd manufactures pink batts. The company wishes to use all available

small business concessions to minimise taxable income. Hot Pink Batts Pty Ltd has prepared

the following Profit & Loss Statement for the 2019 financial year:

Gross Sales

$ $

2,400,000

Less Cost of Goods Sold

Opening Stock 33,000

Purchases and Manufacturing Costs 1,250,000

1,283,000

Closing Stock - 300,000 983,000

Gross Profit 1,417,000

Add Other Income

Diesel Fuel Rebate (Government Subsidy) 3,500

Dividend from American Company – Note 1 8,000

Interest Income 2,000 13,500

Expenses

1,430,500

Gross Wages 680,000

Superannuation 62,000

Provisions for Customer Warranty Claims – Note 2 30,000

Truck Expenses 31,000

Accounting Depreciation – Note 3 60,000

Share of Loss from Partnership with Al Insulation Pty Ltd 13,000

Tax Related Expenditure – Note 4 24,000

Other Deductible Expenses 400,000 1,300,000

NET PROFIT BEFORE INCOME TAX 130,500

Page 6 of 11

PART B – Practical Activities

You are currently employed as a Tax Agent for a local Accounting Firm (Tax Agent number

12345678). Your clients include individuals (salary & wage earners and sole traders) as

well as companies, trusts and partnerships.

The policies and procedures of your firm require you to use the Microsoft Excel templates

provided to complete your calculations. The ATO website should be used to verify current

tax legislation and to seek advice and guidance.

All client communications should be via email. Client details required to complete the

Individual Tax Return are recorded on a new client details form.

QUESTION 1

Hot Pink Batts Pty Ltd manufactures pink batts. The company wishes to use all available

small business concessions to minimise taxable income. Hot Pink Batts Pty Ltd has prepared

the following Profit & Loss Statement for the 2019 financial year:

Gross Sales

$ $

2,400,000

Less Cost of Goods Sold

Opening Stock 33,000

Purchases and Manufacturing Costs 1,250,000

1,283,000

Closing Stock - 300,000 983,000

Gross Profit 1,417,000

Add Other Income

Diesel Fuel Rebate (Government Subsidy) 3,500

Dividend from American Company – Note 1 8,000

Interest Income 2,000 13,500

Expenses

1,430,500

Gross Wages 680,000

Superannuation 62,000

Provisions for Customer Warranty Claims – Note 2 30,000

Truck Expenses 31,000

Accounting Depreciation – Note 3 60,000

Share of Loss from Partnership with Al Insulation Pty Ltd 13,000

Tax Related Expenditure – Note 4 24,000

Other Deductible Expenses 400,000 1,300,000

NET PROFIT BEFORE INCOME TAX 130,500

Prepare and Administer Tax Documentation for Legal Entities

Page 7 of 11

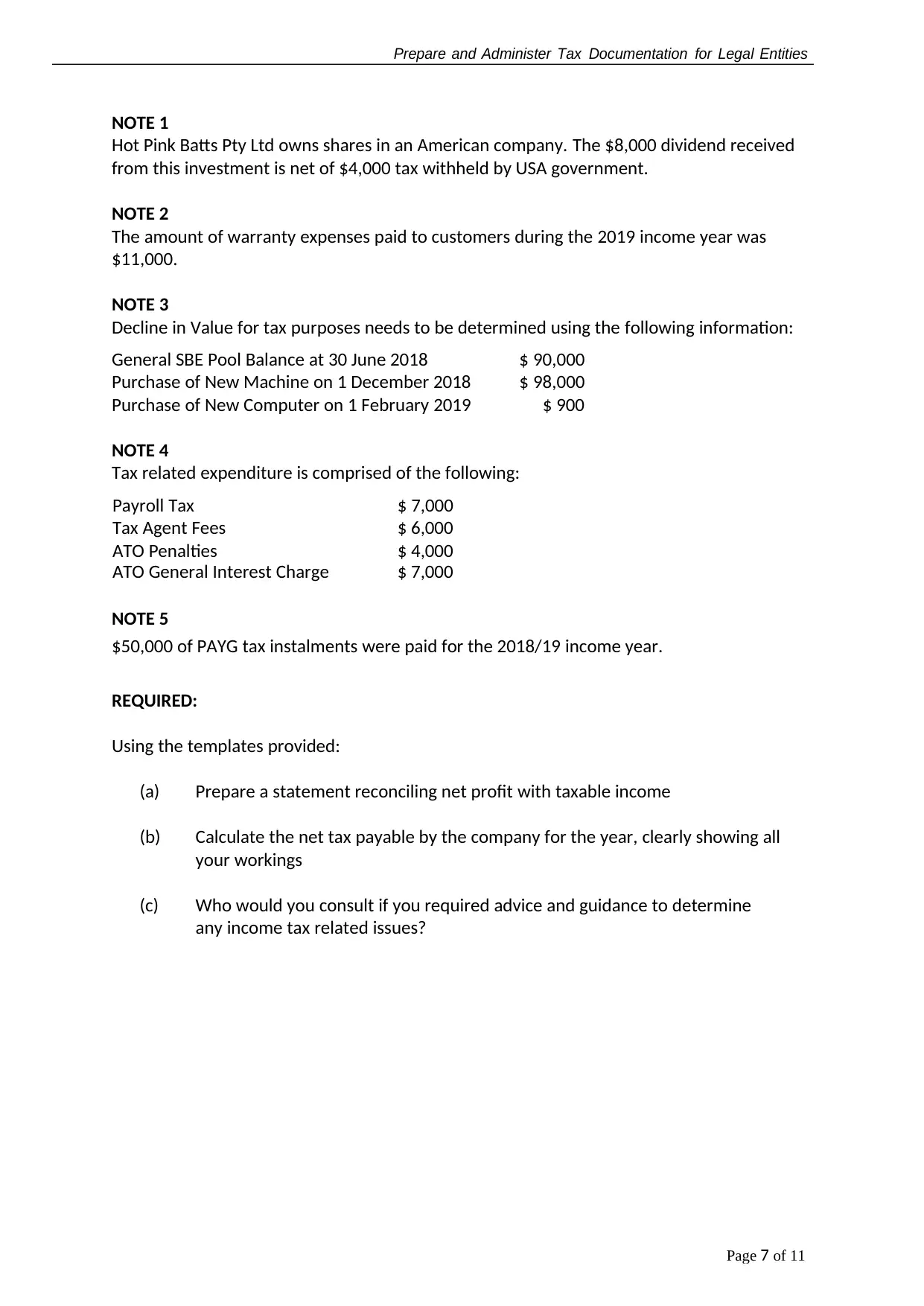

NOTE 1

Hot Pink Batts Pty Ltd owns shares in an American company. The $8,000 dividend received

from this investment is net of $4,000 tax withheld by USA government.

NOTE 2

The amount of warranty expenses paid to customers during the 2019 income year was

$11,000.

NOTE 3

Decline in Value for tax purposes needs to be determined using the following information:

General SBE Pool Balance at 30 June 2018 $ 90,000

Purchase of New Machine on 1 December 2018 $ 98,000

Purchase of New Computer on 1 February 2019 $ 900

NOTE 4

Tax related expenditure is comprised of the following:

Payroll Tax $ 7,000

Tax Agent Fees $ 6,000

ATO Penalties $ 4,000

ATO General Interest Charge $ 7,000

NOTE 5

$50,000 of PAYG tax instalments were paid for the 2018/19 income year.

REQUIRED:

Using the templates provided:

(a) Prepare a statement reconciling net profit with taxable income

(b) Calculate the net tax payable by the company for the year, clearly showing all

your workings

(c) Who would you consult if you required advice and guidance to determine

any income tax related issues?

Page 7 of 11

NOTE 1

Hot Pink Batts Pty Ltd owns shares in an American company. The $8,000 dividend received

from this investment is net of $4,000 tax withheld by USA government.

NOTE 2

The amount of warranty expenses paid to customers during the 2019 income year was

$11,000.

NOTE 3

Decline in Value for tax purposes needs to be determined using the following information:

General SBE Pool Balance at 30 June 2018 $ 90,000

Purchase of New Machine on 1 December 2018 $ 98,000

Purchase of New Computer on 1 February 2019 $ 900

NOTE 4

Tax related expenditure is comprised of the following:

Payroll Tax $ 7,000

Tax Agent Fees $ 6,000

ATO Penalties $ 4,000

ATO General Interest Charge $ 7,000

NOTE 5

$50,000 of PAYG tax instalments were paid for the 2018/19 income year.

REQUIRED:

Using the templates provided:

(a) Prepare a statement reconciling net profit with taxable income

(b) Calculate the net tax payable by the company for the year, clearly showing all

your workings

(c) Who would you consult if you required advice and guidance to determine

any income tax related issues?

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Prepare and Administer Tax Documentation for Legal Entities

Page 8 of 11

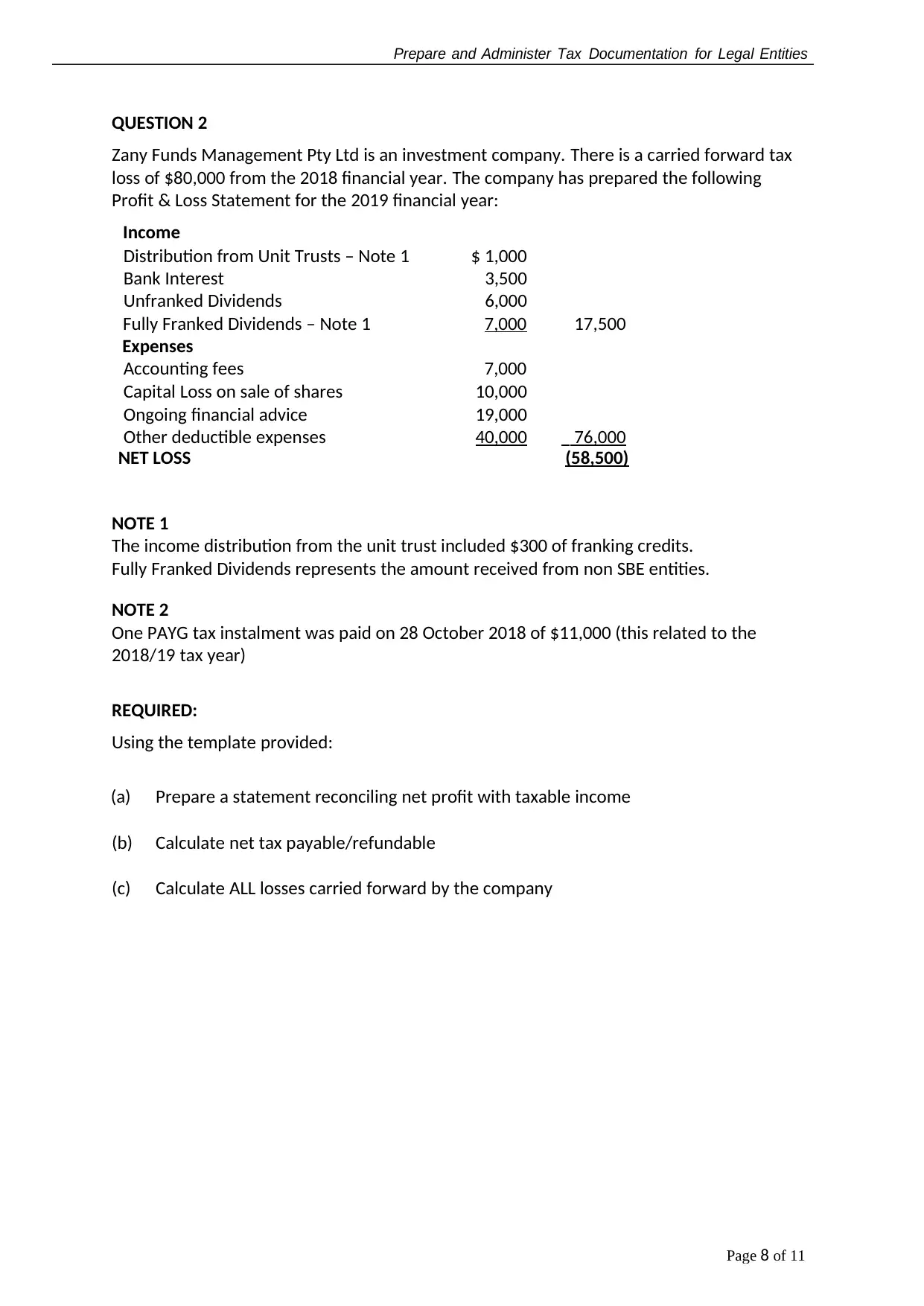

QUESTION 2

Zany Funds Management Pty Ltd is an investment company. There is a carried forward tax

loss of $80,000 from the 2018 financial year. The company has prepared the following

Profit & Loss Statement for the 2019 financial year:

Income

Distribution from Unit Trusts – Note 1 $ 1,000

Bank Interest 3,500

Unfranked Dividends 6,000

Fully Franked Dividends – Note 1

Expenses

Accounting fees

7,000

7,000

17,500

Capital Loss on sale of shares 10,000

Ongoing financial advice 19,000

Other deductible expenses 40,000 76,000

NET LOSS (58,500)

NOTE 1

The income distribution from the unit trust included $300 of franking credits.

Fully Franked Dividends represents the amount received from non SBE entities.

NOTE 2

One PAYG tax instalment was paid on 28 October 2018 of $11,000 (this related to the

2018/19 tax year)

REQUIRED:

Using the template provided:

(a) Prepare a statement reconciling net profit with taxable income

(b) Calculate net tax payable/refundable

(c) Calculate ALL losses carried forward by the company

Page 8 of 11

QUESTION 2

Zany Funds Management Pty Ltd is an investment company. There is a carried forward tax

loss of $80,000 from the 2018 financial year. The company has prepared the following

Profit & Loss Statement for the 2019 financial year:

Income

Distribution from Unit Trusts – Note 1 $ 1,000

Bank Interest 3,500

Unfranked Dividends 6,000

Fully Franked Dividends – Note 1

Expenses

Accounting fees

7,000

7,000

17,500

Capital Loss on sale of shares 10,000

Ongoing financial advice 19,000

Other deductible expenses 40,000 76,000

NET LOSS (58,500)

NOTE 1

The income distribution from the unit trust included $300 of franking credits.

Fully Franked Dividends represents the amount received from non SBE entities.

NOTE 2

One PAYG tax instalment was paid on 28 October 2018 of $11,000 (this related to the

2018/19 tax year)

REQUIRED:

Using the template provided:

(a) Prepare a statement reconciling net profit with taxable income

(b) Calculate net tax payable/refundable

(c) Calculate ALL losses carried forward by the company

Prepare and Administer Tax Documentation for Legal Entities

Page 9 of 11

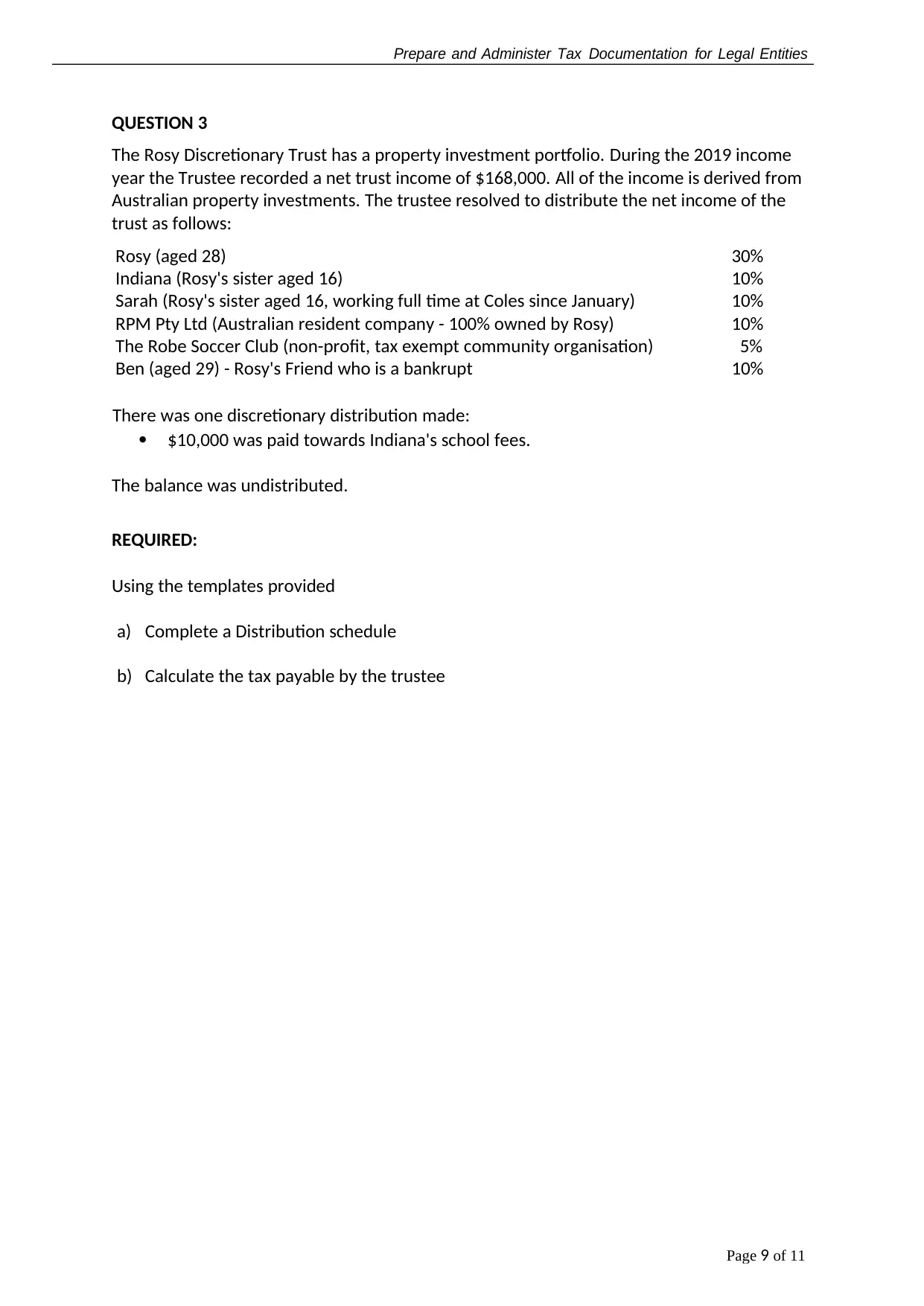

QUESTION 3

The Rosy Discretionary Trust has a property investment portfolio. During the 2019 income

year the Trustee recorded a net trust income of $168,000. All of the income is derived from

Australian property investments. The trustee resolved to distribute the net income of the

trust as follows:

Rosy (aged 28) 30%

Indiana (Rosy's sister aged 16) 10%

Sarah (Rosy's sister aged 16, working full time at Coles since January) 10%

RPM Pty Ltd (Australian resident company - 100% owned by Rosy) 10%

The Robe Soccer Club (non-profit, tax exempt community organisation) 5%

Ben (aged 29) - Rosy's Friend who is a bankrupt 10%

There was one discretionary distribution made:

$10,000 was paid towards Indiana's school fees.

The balance was undistributed.

REQUIRED:

Using the templates provided

a) Complete a Distribution schedule

b) Calculate the tax payable by the trustee

Page 9 of 11

QUESTION 3

The Rosy Discretionary Trust has a property investment portfolio. During the 2019 income

year the Trustee recorded a net trust income of $168,000. All of the income is derived from

Australian property investments. The trustee resolved to distribute the net income of the

trust as follows:

Rosy (aged 28) 30%

Indiana (Rosy's sister aged 16) 10%

Sarah (Rosy's sister aged 16, working full time at Coles since January) 10%

RPM Pty Ltd (Australian resident company - 100% owned by Rosy) 10%

The Robe Soccer Club (non-profit, tax exempt community organisation) 5%

Ben (aged 29) - Rosy's Friend who is a bankrupt 10%

There was one discretionary distribution made:

$10,000 was paid towards Indiana's school fees.

The balance was undistributed.

REQUIRED:

Using the templates provided

a) Complete a Distribution schedule

b) Calculate the tax payable by the trustee

Prepare and Administer Tax Documentation for Legal Entities

Page 10 of

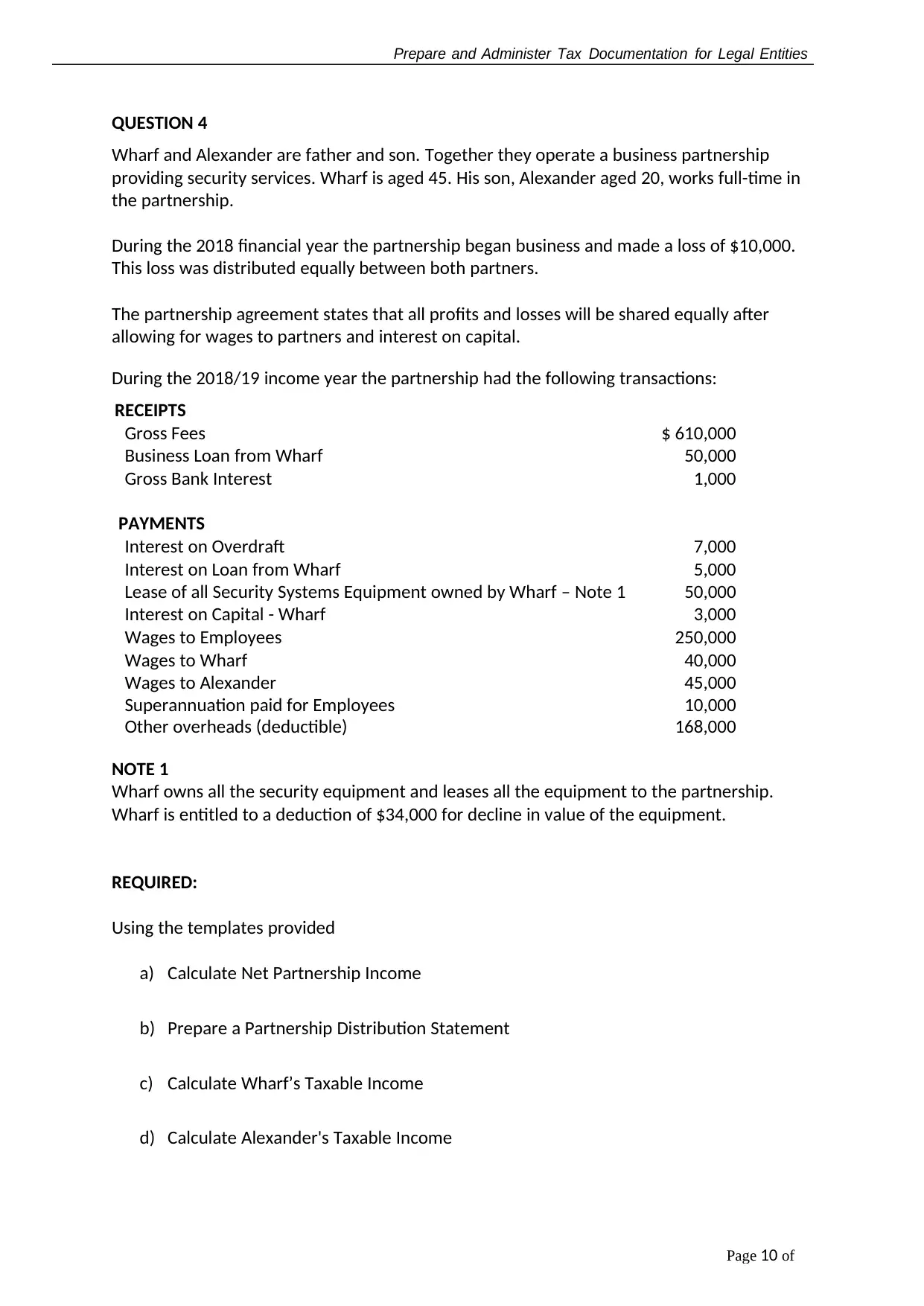

QUESTION 4

Wharf and Alexander are father and son. Together they operate a business partnership

providing security services. Wharf is aged 45. His son, Alexander aged 20, works full-time in

the partnership.

During the 2018 financial year the partnership began business and made a loss of $10,000.

This loss was distributed equally between both partners.

The partnership agreement states that all profits and losses will be shared equally after

allowing for wages to partners and interest on capital.

During the 2018/19 income year the partnership had the following transactions:

RECEIPTS

Gross Fees $ 610,000

Business Loan from Wharf 50,000

Gross Bank Interest 1,000

PAYMENTS

Interest on Overdraft 7,000

Interest on Loan from Wharf 5,000

Lease of all Security Systems Equipment owned by Wharf – Note 1 50,000

Interest on Capital - Wharf 3,000

Wages to Employees 250,000

Wages to Wharf 40,000

Wages to Alexander 45,000

Superannuation paid for Employees 10,000

Other overheads (deductible) 168,000

NOTE 1

Wharf owns all the security equipment and leases all the equipment to the partnership.

Wharf is entitled to a deduction of $34,000 for decline in value of the equipment.

REQUIRED:

Using the templates provided

a) Calculate Net Partnership Income

b) Prepare a Partnership Distribution Statement

c) Calculate Wharf’s Taxable Income

d) Calculate Alexander's Taxable Income

Page 10 of

QUESTION 4

Wharf and Alexander are father and son. Together they operate a business partnership

providing security services. Wharf is aged 45. His son, Alexander aged 20, works full-time in

the partnership.

During the 2018 financial year the partnership began business and made a loss of $10,000.

This loss was distributed equally between both partners.

The partnership agreement states that all profits and losses will be shared equally after

allowing for wages to partners and interest on capital.

During the 2018/19 income year the partnership had the following transactions:

RECEIPTS

Gross Fees $ 610,000

Business Loan from Wharf 50,000

Gross Bank Interest 1,000

PAYMENTS

Interest on Overdraft 7,000

Interest on Loan from Wharf 5,000

Lease of all Security Systems Equipment owned by Wharf – Note 1 50,000

Interest on Capital - Wharf 3,000

Wages to Employees 250,000

Wages to Wharf 40,000

Wages to Alexander 45,000

Superannuation paid for Employees 10,000

Other overheads (deductible) 168,000

NOTE 1

Wharf owns all the security equipment and leases all the equipment to the partnership.

Wharf is entitled to a deduction of $34,000 for decline in value of the equipment.

REQUIRED:

Using the templates provided

a) Calculate Net Partnership Income

b) Prepare a Partnership Distribution Statement

c) Calculate Wharf’s Taxable Income

d) Calculate Alexander's Taxable Income

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Prepare and Administer Tax Documentation for Legal Entities

Page 11 of 11

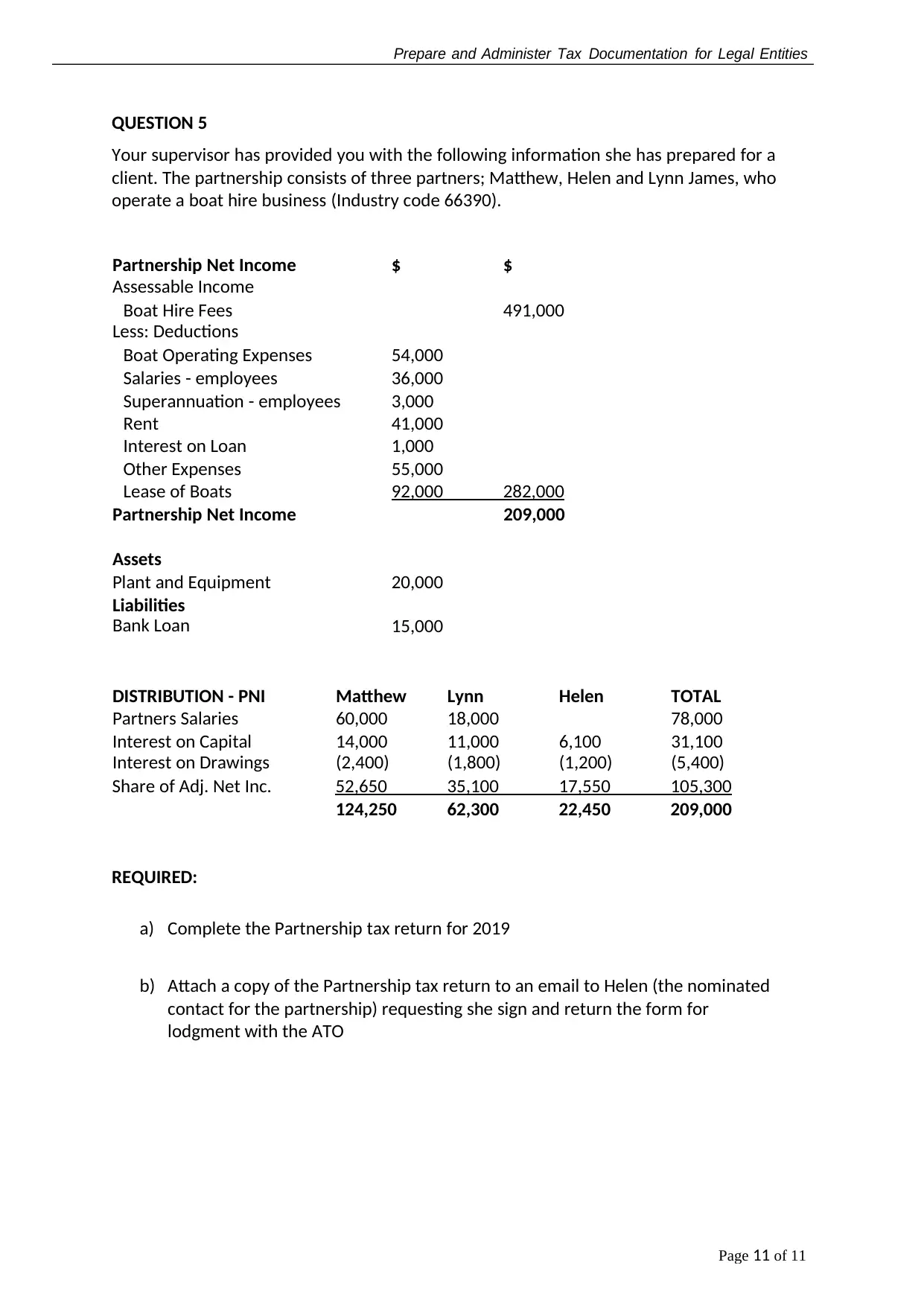

QUESTION 5

Your supervisor has provided you with the following information she has prepared for a

client. The partnership consists of three partners; Matthew, Helen and Lynn James, who

operate a boat hire business (Industry code 66390).

Partnership Net Income

Assessable Income

$ $

Boat Hire Fees 491,000

Less: Deductions

Boat Operating Expenses 54,000

Salaries - employees 36,000

Superannuation - employees 3,000

Rent 41,000

Interest on Loan 1,000

Other Expenses 55,000

Lease of Boats 92,000 282,000

Partnership Net Income 209,000

Assets

Plant and Equipment 20,000

Liabilities

Bank Loan 15,000

DISTRIBUTION - PNI Matthew Lynn Helen TOTAL

Partners Salaries 60,000 18,000 78,000

Interest on Capital 14,000 11,000 6,100 31,100

Interest on Drawings (2,400) (1,800) (1,200) (5,400)

Share of Adj. Net Inc. 52,650 35,100 17,550 105,300

124,250 62,300 22,450 209,000

REQUIRED:

a) Complete the Partnership tax return for 2019

b) Attach a copy of the Partnership tax return to an email to Helen (the nominated

contact for the partnership) requesting she sign and return the form for

lodgment with the ATO

Page 11 of 11

QUESTION 5

Your supervisor has provided you with the following information she has prepared for a

client. The partnership consists of three partners; Matthew, Helen and Lynn James, who

operate a boat hire business (Industry code 66390).

Partnership Net Income

Assessable Income

$ $

Boat Hire Fees 491,000

Less: Deductions

Boat Operating Expenses 54,000

Salaries - employees 36,000

Superannuation - employees 3,000

Rent 41,000

Interest on Loan 1,000

Other Expenses 55,000

Lease of Boats 92,000 282,000

Partnership Net Income 209,000

Assets

Plant and Equipment 20,000

Liabilities

Bank Loan 15,000

DISTRIBUTION - PNI Matthew Lynn Helen TOTAL

Partners Salaries 60,000 18,000 78,000

Interest on Capital 14,000 11,000 6,100 31,100

Interest on Drawings (2,400) (1,800) (1,200) (5,400)

Share of Adj. Net Inc. 52,650 35,100 17,550 105,300

124,250 62,300 22,450 209,000

REQUIRED:

a) Complete the Partnership tax return for 2019

b) Attach a copy of the Partnership tax return to an email to Helen (the nominated

contact for the partnership) requesting she sign and return the form for

lodgment with the ATO

Prepare and Administer Tax Documentation for Legal Entities

Page 12 of 11

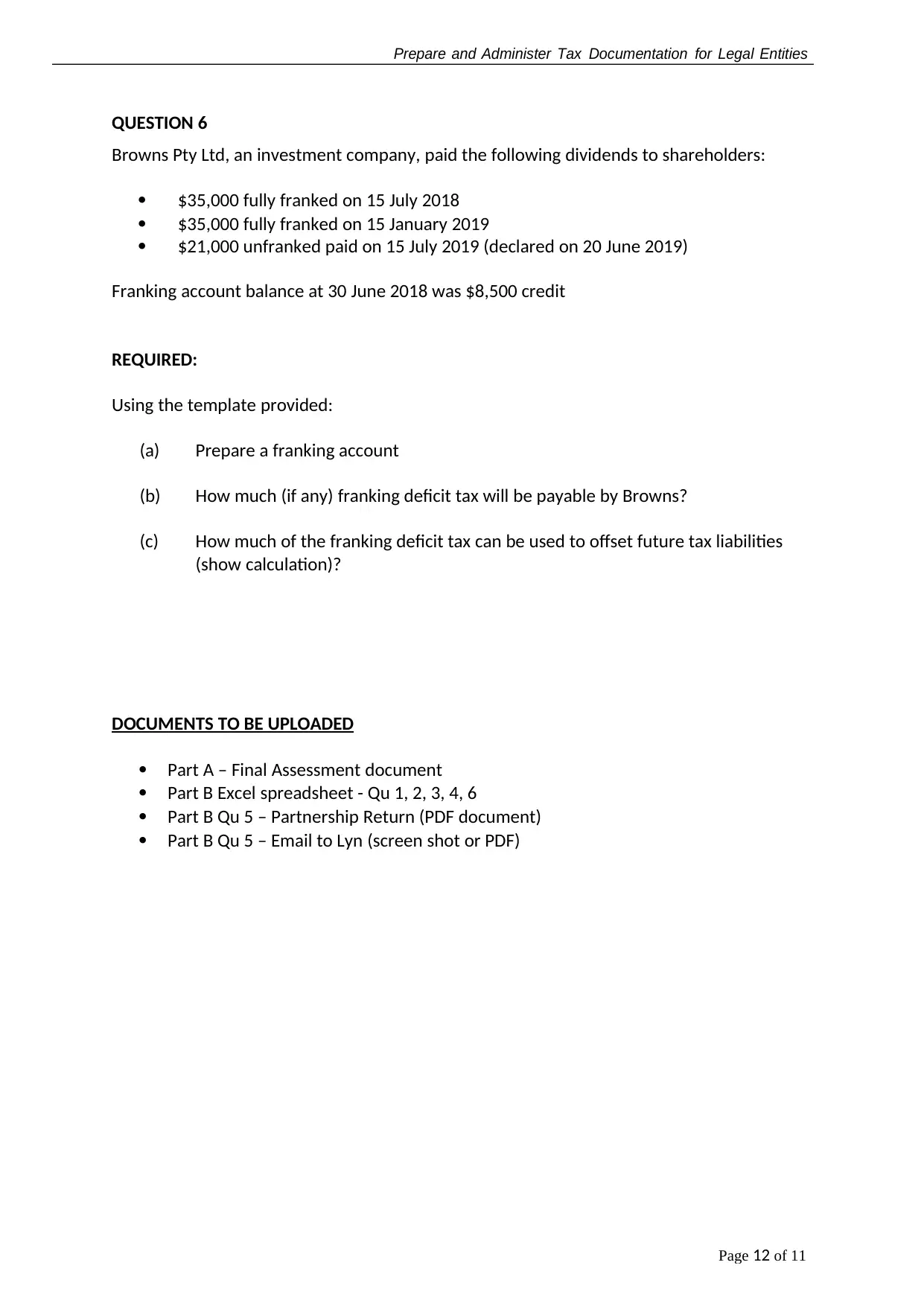

QUESTION 6

Browns Pty Ltd, an investment company, paid the following dividends to shareholders:

$35,000 fully franked on 15 July 2018

$35,000 fully franked on 15 January 2019

$21,000 unfranked paid on 15 July 2019 (declared on 20 June 2019)

Franking account balance at 30 June 2018 was $8,500 credit

REQUIRED:

Using the template provided:

(a) Prepare a franking account

(b) How much (if any) franking deficit tax will be payable by Browns?

(c) How much of the franking deficit tax can be used to offset future tax liabilities

(show calculation)?

DOCUMENTS TO BE UPLOADED

Part A – Final Assessment document

Part B Excel spreadsheet - Qu 1, 2, 3, 4, 6

Part B Qu 5 – Partnership Return (PDF document)

Part B Qu 5 – Email to Lyn (screen shot or PDF)

Page 12 of 11

QUESTION 6

Browns Pty Ltd, an investment company, paid the following dividends to shareholders:

$35,000 fully franked on 15 July 2018

$35,000 fully franked on 15 January 2019

$21,000 unfranked paid on 15 July 2019 (declared on 20 June 2019)

Franking account balance at 30 June 2018 was $8,500 credit

REQUIRED:

Using the template provided:

(a) Prepare a franking account

(b) How much (if any) franking deficit tax will be payable by Browns?

(c) How much of the franking deficit tax can be used to offset future tax liabilities

(show calculation)?

DOCUMENTS TO BE UPLOADED

Part A – Final Assessment document

Part B Excel spreadsheet - Qu 1, 2, 3, 4, 6

Part B Qu 5 – Partnership Return (PDF document)

Part B Qu 5 – Email to Lyn (screen shot or PDF)

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.