FNS40815 FNSCRD301 Assessment 1 Knowledge

VerifiedAdded on 2022/11/28

|8

|1506

|414

AI Summary

This document is Assessment 1 - Knowledge for FNS40815 Certificate IV in Finance & Mortgage Broking. It covers the understanding of different credit products and their application requirements. It also discusses the types of credit available in Australia, costs associated with credit, debt collectors, financial service provider's credit assessment policy, and the National Credit Code.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

FNS40815 Certificate IV in FINANCE & MORTGAGE

BROKING

FNSCRD301 Process applications for credit

Assessment 1 - Knowledge

FNS40815_ FNSCRD301 Assessment 1 Knowledge Document Owner: Released September 2024

Page 1 of 8

BROKING

FNSCRD301 Process applications for credit

Assessment 1 - Knowledge

FNS40815_ FNSCRD301 Assessment 1 Knowledge Document Owner: Released September 2024

Page 1 of 8

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

100654890662878334.docx

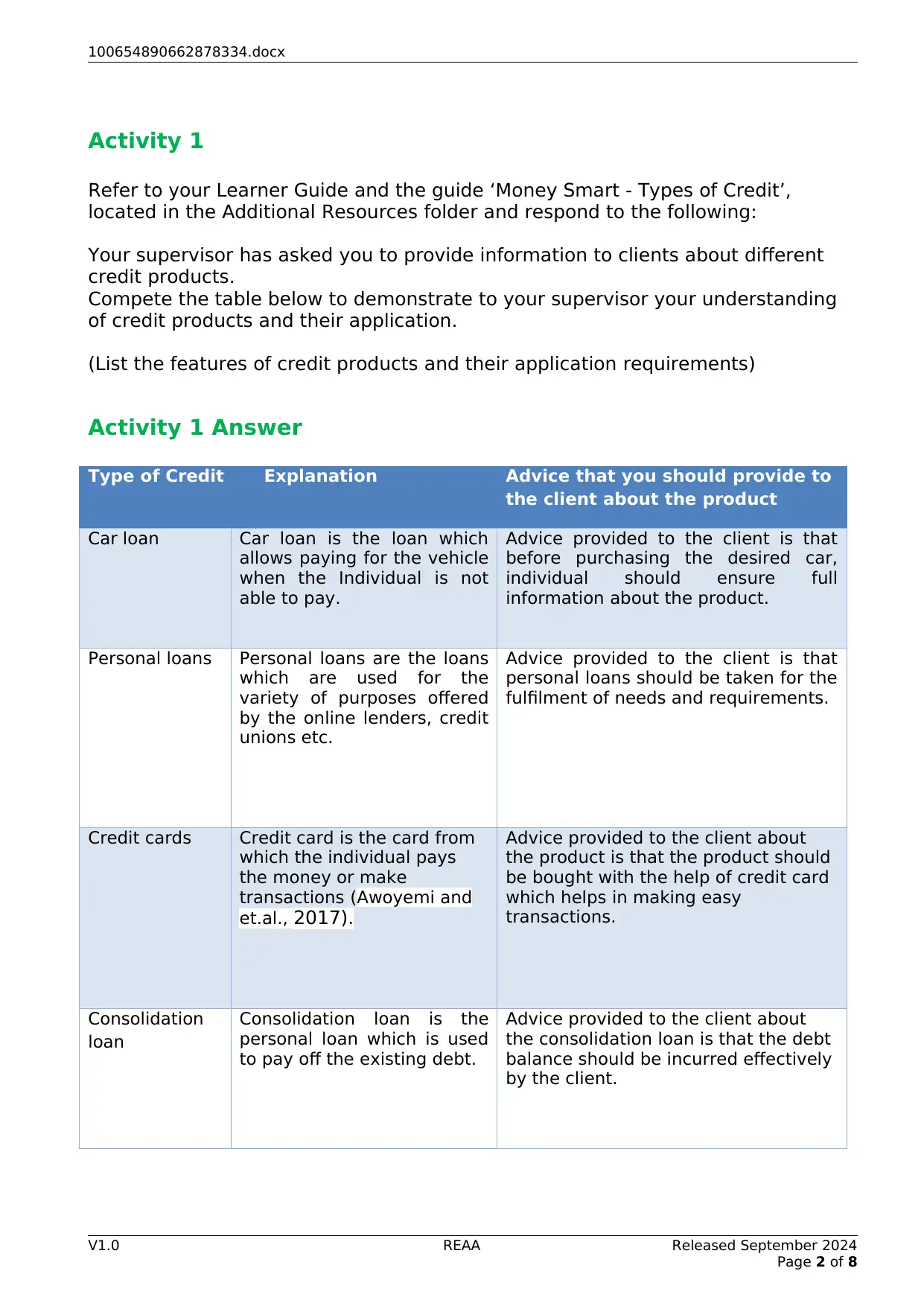

Activity 1

Refer to your Learner Guide and the guide ‘Money Smart - Types of Credit’,

located in the Additional Resources folder and respond to the following:

Your supervisor has asked you to provide information to clients about different

credit products.

Compete the table below to demonstrate to your supervisor your understanding

of credit products and their application.

(List the features of credit products and their application requirements)

Activity 1 Answer

Type of Credit Explanation Advice that you should provide to

the client about the product

Car loan Car loan is the loan which

allows paying for the vehicle

when the Individual is not

able to pay.

Advice provided to the client is that

before purchasing the desired car,

individual should ensure full

information about the product.

Personal loans Personal loans are the loans

which are used for the

variety of purposes offered

by the online lenders, credit

unions etc.

Advice provided to the client is that

personal loans should be taken for the

fulfilment of needs and requirements.

Credit cards Credit card is the card from

which the individual pays

the money or make

transactions (Awoyemi and

et.al., 2017).

Advice provided to the client about

the product is that the product should

be bought with the help of credit card

which helps in making easy

transactions.

Consolidation

loan

Consolidation loan is the

personal loan which is used

to pay off the existing debt.

Advice provided to the client about

the consolidation loan is that the debt

balance should be incurred effectively

by the client.

V1.0 REAA Released September 2024

Page 2 of 8

Activity 1

Refer to your Learner Guide and the guide ‘Money Smart - Types of Credit’,

located in the Additional Resources folder and respond to the following:

Your supervisor has asked you to provide information to clients about different

credit products.

Compete the table below to demonstrate to your supervisor your understanding

of credit products and their application.

(List the features of credit products and their application requirements)

Activity 1 Answer

Type of Credit Explanation Advice that you should provide to

the client about the product

Car loan Car loan is the loan which

allows paying for the vehicle

when the Individual is not

able to pay.

Advice provided to the client is that

before purchasing the desired car,

individual should ensure full

information about the product.

Personal loans Personal loans are the loans

which are used for the

variety of purposes offered

by the online lenders, credit

unions etc.

Advice provided to the client is that

personal loans should be taken for the

fulfilment of needs and requirements.

Credit cards Credit card is the card from

which the individual pays

the money or make

transactions (Awoyemi and

et.al., 2017).

Advice provided to the client about

the product is that the product should

be bought with the help of credit card

which helps in making easy

transactions.

Consolidation

loan

Consolidation loan is the

personal loan which is used

to pay off the existing debt.

Advice provided to the client about

the consolidation loan is that the debt

balance should be incurred effectively

by the client.

V1.0 REAA Released September 2024

Page 2 of 8

100654890662878334.docx

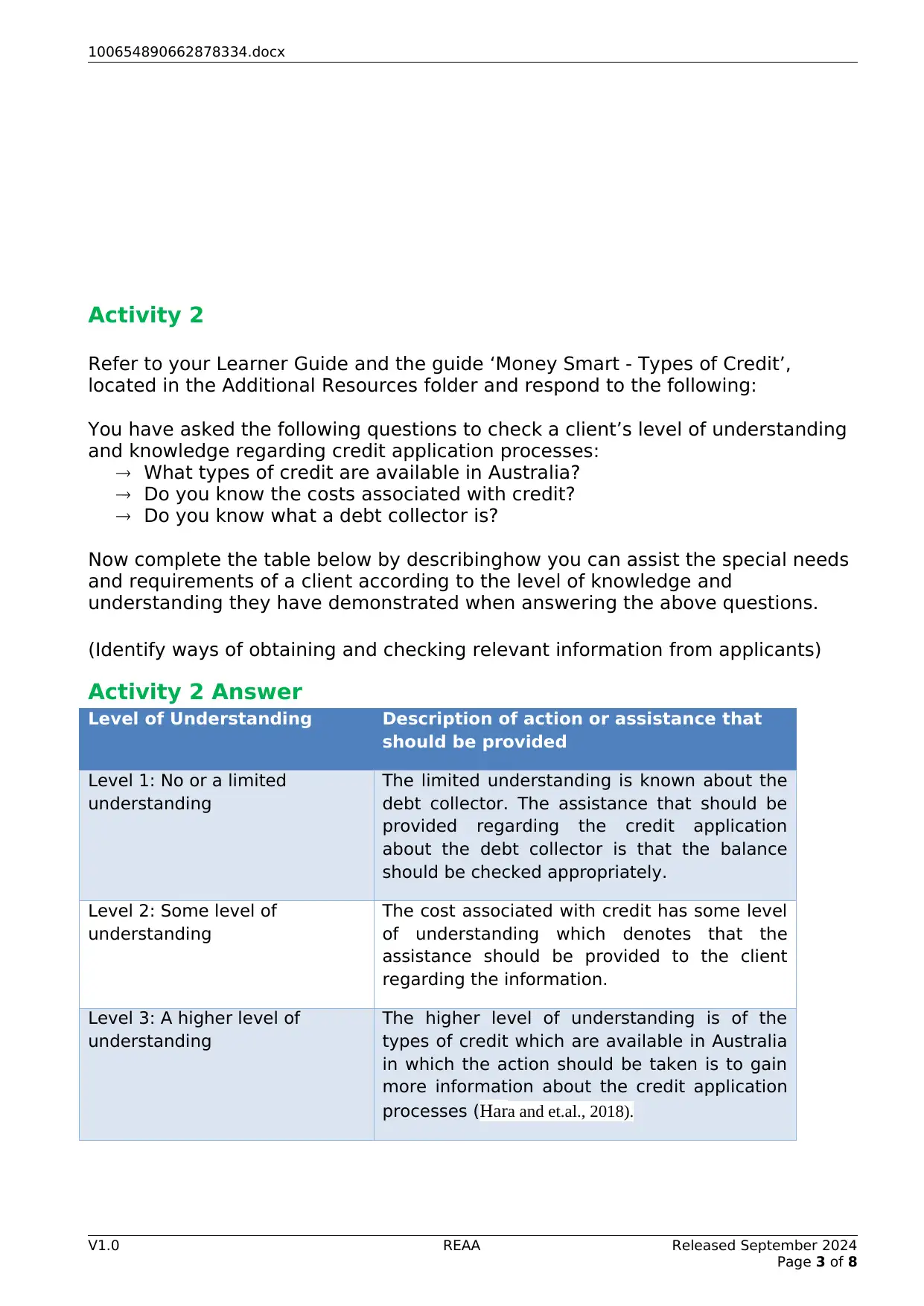

Activity 2

Refer to your Learner Guide and the guide ‘Money Smart - Types of Credit’,

located in the Additional Resources folder and respond to the following:

You have asked the following questions to check a client’s level of understanding

and knowledge regarding credit application processes:

What types of credit are available in Australia?

Do you know the costs associated with credit?

Do you know what a debt collector is?

Now complete the table below by describinghow you can assist the special needs

and requirements of a client according to the level of knowledge and

understanding they have demonstrated when answering the above questions.

(Identify ways of obtaining and checking relevant information from applicants)

Activity 2 Answer

Level of Understanding Description of action or assistance that

should be provided

Level 1: No or a limited

understanding

The limited understanding is known about the

debt collector. The assistance that should be

provided regarding the credit application

about the debt collector is that the balance

should be checked appropriately.

Level 2: Some level of

understanding

The cost associated with credit has some level

of understanding which denotes that the

assistance should be provided to the client

regarding the information.

Level 3: A higher level of

understanding

The higher level of understanding is of the

types of credit which are available in Australia

in which the action should be taken is to gain

more information about the credit application

processes (Hara and et.al., 2018).

V1.0 REAA Released September 2024

Page 3 of 8

Activity 2

Refer to your Learner Guide and the guide ‘Money Smart - Types of Credit’,

located in the Additional Resources folder and respond to the following:

You have asked the following questions to check a client’s level of understanding

and knowledge regarding credit application processes:

What types of credit are available in Australia?

Do you know the costs associated with credit?

Do you know what a debt collector is?

Now complete the table below by describinghow you can assist the special needs

and requirements of a client according to the level of knowledge and

understanding they have demonstrated when answering the above questions.

(Identify ways of obtaining and checking relevant information from applicants)

Activity 2 Answer

Level of Understanding Description of action or assistance that

should be provided

Level 1: No or a limited

understanding

The limited understanding is known about the

debt collector. The assistance that should be

provided regarding the credit application

about the debt collector is that the balance

should be checked appropriately.

Level 2: Some level of

understanding

The cost associated with credit has some level

of understanding which denotes that the

assistance should be provided to the client

regarding the information.

Level 3: A higher level of

understanding

The higher level of understanding is of the

types of credit which are available in Australia

in which the action should be taken is to gain

more information about the credit application

processes (Hara and et.al., 2018).

V1.0 REAA Released September 2024

Page 3 of 8

100654890662878334.docx

V1.0 REAA Released September 2024

Page 4 of 8

V1.0 REAA Released September 2024

Page 4 of 8

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

100654890662878334.docx

Activity 3

Explain the key features of a financial services provider’s credit assessment

policy based on the principles of responsible lending.

(Explain key features of organisational policy and procedures that relate to credit

assessments, security and customer service)

Activity 3 Answer

Financial service provider is the business offering financial advice or

intermediary advice and the representatives who work for providing the

services which are financial in terms and helps the clients to measure the most

effective ways of how to make the financial transactions to be made available

to the clients and the customers in the most effective way possible. The key

features of financial service provider’s credit assessment policy are the main

thing which the customers should be aware of (Rai and et.al., 2020). This makes the

most of the process of how the transactions are taken place and what are the

key features in which the transactions are done. Responsibly leading the way

through which the financial service provider’s credit assessment policy is

initiated is based on how the finance is being handled in the business and how

the credits are being managed by the customers.

V1.0 REAA Released September 2024

Page 5 of 8

Activity 3

Explain the key features of a financial services provider’s credit assessment

policy based on the principles of responsible lending.

(Explain key features of organisational policy and procedures that relate to credit

assessments, security and customer service)

Activity 3 Answer

Financial service provider is the business offering financial advice or

intermediary advice and the representatives who work for providing the

services which are financial in terms and helps the clients to measure the most

effective ways of how to make the financial transactions to be made available

to the clients and the customers in the most effective way possible. The key

features of financial service provider’s credit assessment policy are the main

thing which the customers should be aware of (Rai and et.al., 2020). This makes the

most of the process of how the transactions are taken place and what are the

key features in which the transactions are done. Responsibly leading the way

through which the financial service provider’s credit assessment policy is

initiated is based on how the finance is being handled in the business and how

the credits are being managed by the customers.

V1.0 REAA Released September 2024

Page 5 of 8

100654890662878334.docx

Activity 4

The purpose of the National Credit Code is to provide protection for consumers

who enter into credit contracts for personal purposes. How does the legislation

identify whether a loan is for personal purposes, as opposed to business

purposes?

(Explain the key purpose of relevant credit legislation, statutory requirements

and codes of practice, covering: consumer credit; personal property securities;

privacy)

Activity 4 Answer

National Credit Code is the process which regulates all consumers lending

which includes residential investment and the property by non corporate

borrowers. This is basically done for personal purposes and by making this

initiative the customers are aware of how and what are the financial

transactions which are being done in the process. This makes the national

credit code the most effective process for the transactions and for the purpose

of what is to be done regarding the credits which are made available to the

customers (Memorandum, 2019).This also helps in entering the credit contracts

and for personal loans which are made. The loan identifies whether it is of

personal purpose or for business purpose is that the customers identify what is

the source and what is the means of how the transaction is being done.

V1.0 REAA Released September 2024

Page 6 of 8

Activity 4

The purpose of the National Credit Code is to provide protection for consumers

who enter into credit contracts for personal purposes. How does the legislation

identify whether a loan is for personal purposes, as opposed to business

purposes?

(Explain the key purpose of relevant credit legislation, statutory requirements

and codes of practice, covering: consumer credit; personal property securities;

privacy)

Activity 4 Answer

National Credit Code is the process which regulates all consumers lending

which includes residential investment and the property by non corporate

borrowers. This is basically done for personal purposes and by making this

initiative the customers are aware of how and what are the financial

transactions which are being done in the process. This makes the national

credit code the most effective process for the transactions and for the purpose

of what is to be done regarding the credits which are made available to the

customers (Memorandum, 2019).This also helps in entering the credit contracts

and for personal loans which are made. The loan identifies whether it is of

personal purpose or for business purpose is that the customers identify what is

the source and what is the means of how the transaction is being done.

V1.0 REAA Released September 2024

Page 6 of 8

100654890662878334.docx

Activity 5

When taking out a business loan a lender will often want to secure the loan in the

form of an asset. This security is intended to minimise risk exposure in the event

the applicant is unable to repay the loan.

Describe the main types of ‘security’ that may be required to obtain a small

business loan.

(Explain types of security)

Activity 5 Answer

The types of security which may be required to obtain a small business loan

are – secured term loan, financing which is based on assets, invoice

discounting, letter of credit etc. These are the types of security loans which

are refereed for the purpose of how the small businesses incur the most of

the transactions which are done effectively on large basis. The security in

small business is essential part in the business which makes the most of the

work and this initiate and makes the profitable business earnings through

which the business is able to take the loans and then pay back with the

interest on small basis (Biira, 2021). This is the major source through which the

business will be initiating the major parts of how the security is to be

ensured to safeguard the business and to make it reach on the scales of

profits and losses.

V1.0 REAA Released September 2024

Page 7 of 8

Activity 5

When taking out a business loan a lender will often want to secure the loan in the

form of an asset. This security is intended to minimise risk exposure in the event

the applicant is unable to repay the loan.

Describe the main types of ‘security’ that may be required to obtain a small

business loan.

(Explain types of security)

Activity 5 Answer

The types of security which may be required to obtain a small business loan

are – secured term loan, financing which is based on assets, invoice

discounting, letter of credit etc. These are the types of security loans which

are refereed for the purpose of how the small businesses incur the most of

the transactions which are done effectively on large basis. The security in

small business is essential part in the business which makes the most of the

work and this initiate and makes the profitable business earnings through

which the business is able to take the loans and then pay back with the

interest on small basis (Biira, 2021). This is the major source through which the

business will be initiating the major parts of how the security is to be

ensured to safeguard the business and to make it reach on the scales of

profits and losses.

V1.0 REAA Released September 2024

Page 7 of 8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

100654890662878334.docx

REFERENCES

Books and Journals

Awoyemi, J.O. and et.al., 2017, October. Credit card fraud detection using machine learning

techniques: A comparative analysis. In 2017 International Conference on Computing

Networking and Informatics (ICCNI) (pp. 1-9). IEEE.

Hara and et.al., 2018. "Secured Transactions Law Reform in Japan: Japan Business Credit Project

Assessment of Interviews and Tentative Policy Proposals." Secured Transactions Law Reform

in Japan: Japan Business Credit Project Assessment of Interviews and Tentative Policy

Proposals (April 5, 2021). U of Penn, Inst for Law & Econ Research Paper 21-16 (2021).

Rai, R. and et.al., 2020, September. Institutionalizing Paradox: Contextual Ambidexterity in an

Oligopolistic Setting: The Case of a Financial Service Provider. In European Conference on

Innovation and Entrepreneurship (pp. 513-520). Academic Conferences International

Limited.

Memorandum, P.U.M.A., 3.7, 2019. CREDIT ENHANCEMENT. Commercial Law Aspects of

Residential Mortgage Securitisation in Australia.p.56.

Biira, F.J., 2021. Assessment of factors associated with access to credit “loans” For small and medium

business enterprises.

V1.0 REAA Released September 2024

Page 8 of 8

REFERENCES

Books and Journals

Awoyemi, J.O. and et.al., 2017, October. Credit card fraud detection using machine learning

techniques: A comparative analysis. In 2017 International Conference on Computing

Networking and Informatics (ICCNI) (pp. 1-9). IEEE.

Hara and et.al., 2018. "Secured Transactions Law Reform in Japan: Japan Business Credit Project

Assessment of Interviews and Tentative Policy Proposals." Secured Transactions Law Reform

in Japan: Japan Business Credit Project Assessment of Interviews and Tentative Policy

Proposals (April 5, 2021). U of Penn, Inst for Law & Econ Research Paper 21-16 (2021).

Rai, R. and et.al., 2020, September. Institutionalizing Paradox: Contextual Ambidexterity in an

Oligopolistic Setting: The Case of a Financial Service Provider. In European Conference on

Innovation and Entrepreneurship (pp. 513-520). Academic Conferences International

Limited.

Memorandum, P.U.M.A., 3.7, 2019. CREDIT ENHANCEMENT. Commercial Law Aspects of

Residential Mortgage Securitisation in Australia.p.56.

Biira, F.J., 2021. Assessment of factors associated with access to credit “loans” For small and medium

business enterprises.

V1.0 REAA Released September 2024

Page 8 of 8

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.