Quantitative Analysis and Forecasting of ANZ Stock Returns (2020-2022)

VerifiedAdded on 2023/06/04

|12

|2960

|362

Report

AI Summary

This report presents a forecasting and quantitative analysis of ANZ (Australia & New Zealand Banking Group) stock returns. The analysis utilizes weekly stock price data from October 2020 to October 2022. The report begins with a graphical presentation of weekly returns, demonstrating their random nature without discernible trends or seasonality. Descriptive statistics, including mean, median, standard deviation, and range, are calculated and discussed, revealing a mean return of 0.0034, a standard deviation of 0.033, and a total return of 35.81% over the two-year period. A regression analysis is then conducted to test the predictive power of past returns on future returns. The regression results indicate a poor predictive power of lagged returns, with a p-value of 0.963, an adjusted R-squared of -0.009, and a slope of 0.0046. The report concludes that past returns have minimal influence on future returns, suggesting that other factors significantly impact ANZ stock performance.

FORECASTING AND

QUANTITATIVE

ANALYSIS

QUANTITATIVE

ANALYSIS

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

MAIN BODY..................................................................................................................................4

Presentation of data graphically and discussion of results..........................................................4

Calculation & presentation of descriptive statistics for the stock returns of ANZ......................5

Regression analysis to test the predictive power of past returns on future returns......................6

Summarizing the results, providing conclusions and making recommendations........................7

REFERENCES................................................................................................................................9

Books and Journals......................................................................................................................9

INTRODUCTION...........................................................................................................................3

MAIN BODY..................................................................................................................................4

Presentation of data graphically and discussion of results..........................................................4

Calculation & presentation of descriptive statistics for the stock returns of ANZ......................5

Regression analysis to test the predictive power of past returns on future returns......................6

Summarizing the results, providing conclusions and making recommendations........................7

REFERENCES................................................................................................................................9

Books and Journals......................................................................................................................9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Forecasting and quantitative analysis with regards to stocks involve statistical analysis to

determine the future returns by holding the stock in alignment with the past or lagged returns

derived through the stock. This report would be based on the forecasting & quantitative analysis

of one such Australian listed stock that is, ANZ which is one of the stock forming part of ASX

200 index. ANZ or the Australia & New Zealand Banking Group limited is a multinational

financial services & banking company of Australia headquartered in Melbourne, Victoria. This

bank has obtained second largest & fourth largest place in Australia on the basis of assets held

and market capitalization. The current corporate entity of the bank was set up in 1970 on 1st

October with the merger between ANZ and ES&A bank which was considered as the largest

merger of the Australian history (Ghosal and et. al. 2020).

ANZ is a public limited bank and accordingly traded as ASX: ANZ and NZX: ANZ along with

being one of the component of ASX 200 Index. It served the population across the globe through

range of financial & banking services such as consumer banking, corporate banking, private

banking, investment management & banking, credit cards, private equity, mortgages and global

wealth management (Gunst and Mason, 2018). With 51000 employee base, this bank is serving

approximately 9 million customers across the globe where six million are belonging from

Australia itself who are served through 570 or more branches of the bank.

In this report, the weekly stock returns of ANZ would be calculated and presented

graphically. Further, the calculation, presentation and discussion will be done of description

results obtained for the weekly stock returns of ANZ for past two years. Next, the regression

model will be used to determine the predictive power of past returns on future returns along with

explaining correlation, slope and p value of the series. At last the summary will be presented for

the results and accordingly, recommendations will be made for the improvement in analysis.

The time interval chosen for the forecasting & quantitative analysis performed here is weekly

data where the opening stock prices of ANZ will be taken into account to indicate how returns

have changed every week during the last two years. Daily data if taken for six months would

give a short picture of ANZ stock performance while the monthly data of ANZ stock prices for 5

or more years makes the analysis time consuming (Valaskova, Kliestik and Kovacova, 2018).

Forecasting and quantitative analysis with regards to stocks involve statistical analysis to

determine the future returns by holding the stock in alignment with the past or lagged returns

derived through the stock. This report would be based on the forecasting & quantitative analysis

of one such Australian listed stock that is, ANZ which is one of the stock forming part of ASX

200 index. ANZ or the Australia & New Zealand Banking Group limited is a multinational

financial services & banking company of Australia headquartered in Melbourne, Victoria. This

bank has obtained second largest & fourth largest place in Australia on the basis of assets held

and market capitalization. The current corporate entity of the bank was set up in 1970 on 1st

October with the merger between ANZ and ES&A bank which was considered as the largest

merger of the Australian history (Ghosal and et. al. 2020).

ANZ is a public limited bank and accordingly traded as ASX: ANZ and NZX: ANZ along with

being one of the component of ASX 200 Index. It served the population across the globe through

range of financial & banking services such as consumer banking, corporate banking, private

banking, investment management & banking, credit cards, private equity, mortgages and global

wealth management (Gunst and Mason, 2018). With 51000 employee base, this bank is serving

approximately 9 million customers across the globe where six million are belonging from

Australia itself who are served through 570 or more branches of the bank.

In this report, the weekly stock returns of ANZ would be calculated and presented

graphically. Further, the calculation, presentation and discussion will be done of description

results obtained for the weekly stock returns of ANZ for past two years. Next, the regression

model will be used to determine the predictive power of past returns on future returns along with

explaining correlation, slope and p value of the series. At last the summary will be presented for

the results and accordingly, recommendations will be made for the improvement in analysis.

The time interval chosen for the forecasting & quantitative analysis performed here is weekly

data where the opening stock prices of ANZ will be taken into account to indicate how returns

have changed every week during the last two years. Daily data if taken for six months would

give a short picture of ANZ stock performance while the monthly data of ANZ stock prices for 5

or more years makes the analysis time consuming (Valaskova, Kliestik and Kovacova, 2018).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Accordingly, weekly stock price data will be taken to capture the market volatility in a better

way. Further, the time period of 2 years will be taken beginning from 1st October 2020 to 1st

October 2022 which is considered to be not so short as well as long period for the purpose of

analysis & forecasting and thus, makes the process simple.

MAIN BODY

Presentation of data graphically and discussion of results

0 2 4 6 8 10 12

0

2

4

6

8

10

12

Weekly returns of ANZ from 2020 - 2022

The above graph shows the weekly returns derived from holding the stock of ANZ from 2020 to

2022 and accordingly, it can be seen that the returns are showing randomness in its movement

where the returns are not following any kind of trend or pattern. This is because of the returns

calculated on the opening price of ANZ stock having taken the random values and accordingly

moving upward or downward randomly without following any trend.

Accordingly, there is no requirement of transforming or decomposing the data pertaining

to weekly stock returns of ANZ for making it well-organized and predictable. It is needed for

build a model as well as making predictions. Decomposed data are free from any kind of

seasonality or trend where the seasonality factor and trend factor are eliminated from the time

series data (Farzaneh and et. al. 2020). As the data of weekly stock returns have already taken

random values and no trend or seasonality is present here, there is no need for further

transformation or decomposition or adjustment to be done in the company’s stock returns data.

Overall, decomposition of time series data is done only when the factor of trend or seasonality is

way. Further, the time period of 2 years will be taken beginning from 1st October 2020 to 1st

October 2022 which is considered to be not so short as well as long period for the purpose of

analysis & forecasting and thus, makes the process simple.

MAIN BODY

Presentation of data graphically and discussion of results

0 2 4 6 8 10 12

0

2

4

6

8

10

12

Weekly returns of ANZ from 2020 - 2022

The above graph shows the weekly returns derived from holding the stock of ANZ from 2020 to

2022 and accordingly, it can be seen that the returns are showing randomness in its movement

where the returns are not following any kind of trend or pattern. This is because of the returns

calculated on the opening price of ANZ stock having taken the random values and accordingly

moving upward or downward randomly without following any trend.

Accordingly, there is no requirement of transforming or decomposing the data pertaining

to weekly stock returns of ANZ for making it well-organized and predictable. It is needed for

build a model as well as making predictions. Decomposed data are free from any kind of

seasonality or trend where the seasonality factor and trend factor are eliminated from the time

series data (Farzaneh and et. al. 2020). As the data of weekly stock returns have already taken

random values and no trend or seasonality is present here, there is no need for further

transformation or decomposition or adjustment to be done in the company’s stock returns data.

Overall, decomposition of time series data is done only when the factor of trend or seasonality is

present in the data which makes it necessary to adjust the data for trends or seasonality in order

to make qualitative predictions.

White noise in time series data like the weekly data of stock returns of ANZ involves the

variable taking place independently along with its distribution being identical giving the value of

mean equivalent to zero (Requioma, et. al. 2020). Therefore, as in the given case, it has been

already discussed that weekly stock returns are randomly distributed throughout the two - year

time period in the past along with the mean value being equivalent to zero, this time series of

weekly stock returns looks like white noise.

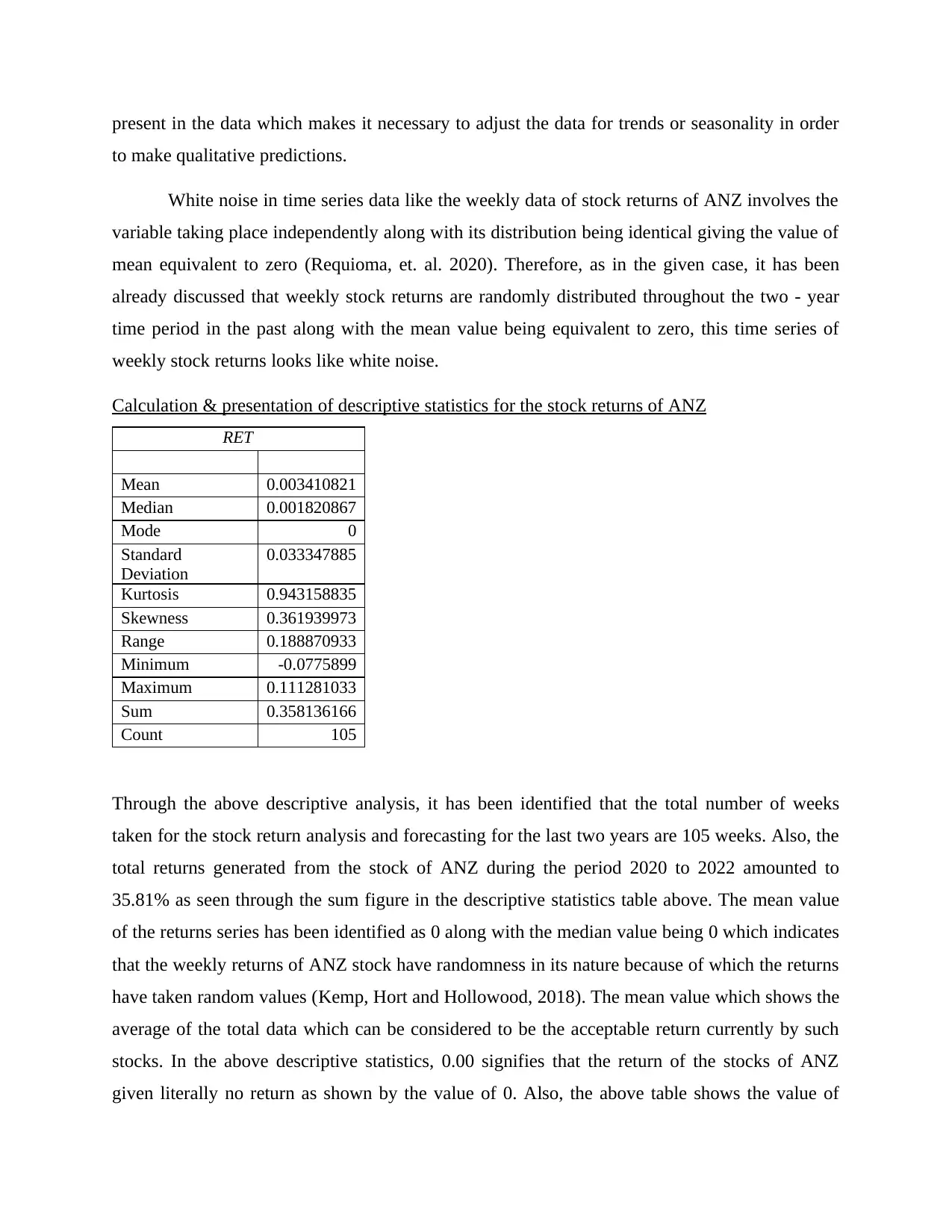

Calculation & presentation of descriptive statistics for the stock returns of ANZ

RET

Mean 0.003410821

Median 0.001820867

Mode 0

Standard

Deviation

0.033347885

Kurtosis 0.943158835

Skewness 0.361939973

Range 0.188870933

Minimum -0.0775899

Maximum 0.111281033

Sum 0.358136166

Count 105

Through the above descriptive analysis, it has been identified that the total number of weeks

taken for the stock return analysis and forecasting for the last two years are 105 weeks. Also, the

total returns generated from the stock of ANZ during the period 2020 to 2022 amounted to

35.81% as seen through the sum figure in the descriptive statistics table above. The mean value

of the returns series has been identified as 0 along with the median value being 0 which indicates

that the weekly returns of ANZ stock have randomness in its nature because of which the returns

have taken random values (Kemp, Hort and Hollowood, 2018). The mean value which shows the

average of the total data which can be considered to be the acceptable return currently by such

stocks. In the above descriptive statistics, 0.00 signifies that the return of the stocks of ANZ

given literally no return as shown by the value of 0. Also, the above table shows the value of

to make qualitative predictions.

White noise in time series data like the weekly data of stock returns of ANZ involves the

variable taking place independently along with its distribution being identical giving the value of

mean equivalent to zero (Requioma, et. al. 2020). Therefore, as in the given case, it has been

already discussed that weekly stock returns are randomly distributed throughout the two - year

time period in the past along with the mean value being equivalent to zero, this time series of

weekly stock returns looks like white noise.

Calculation & presentation of descriptive statistics for the stock returns of ANZ

RET

Mean 0.003410821

Median 0.001820867

Mode 0

Standard

Deviation

0.033347885

Kurtosis 0.943158835

Skewness 0.361939973

Range 0.188870933

Minimum -0.0775899

Maximum 0.111281033

Sum 0.358136166

Count 105

Through the above descriptive analysis, it has been identified that the total number of weeks

taken for the stock return analysis and forecasting for the last two years are 105 weeks. Also, the

total returns generated from the stock of ANZ during the period 2020 to 2022 amounted to

35.81% as seen through the sum figure in the descriptive statistics table above. The mean value

of the returns series has been identified as 0 along with the median value being 0 which indicates

that the weekly returns of ANZ stock have randomness in its nature because of which the returns

have taken random values (Kemp, Hort and Hollowood, 2018). The mean value which shows the

average of the total data which can be considered to be the acceptable return currently by such

stocks. In the above descriptive statistics, 0.00 signifies that the return of the stocks of ANZ

given literally no return as shown by the value of 0. Also, the above table shows the value of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

median which shows the middle value from the list of the total data being analyzed and studied

for such descriptive statistics under consideration. It shall be noted that such list of data needs to

be in ascending order in order to be able to calculate median from such data (Mishra and et.al.,

2019). The value of median of such data of stock returns of ANZ is 0.00 which again signifies no

relevant significance as the mean was also 0.00 and the middle value is also 0.00. although the

mean and median is 0.00 but it is clear that maximum value of such returns is 0.11 and minimum

value is -0.077 which shows that the return ranges from -0.077 to 0.11 thus, rendering the range

of 0.1888 of the returns generated form the stock of ANZ during the period of 2020 to 2022.

The standard deviation in any descriptive statistics is the measure of dispersion of the data from

the mean of such a data. Lower standard deviation denotes that the current data is clustered

around the mean of such data and higher standard deviation shows that the data is more spread

from such mean. Therefore, in the given data set of returns generated form the stock of ANZ

during the period of 2020 to 2022, the value of standard deviation comes to 0.033 i.e., 3.33%.

Such a value of standard deviation shows that there is lower level of standard deviation. This

means that the data related to the returns of the stock of ANZ from 2020 to 2022 is not spread

and is clustered around the mean value which is 0.003 (Kaur, Stoltzfus and Yellapu, 2018).

Theoretically, this shows that the data values are not very far differentiated from the mean of the

data set and the mean value is a reliable source of information regarding the returns of the stock

of ANZ. This data set includes total of 105 individual returns of ANZ relating to the different

time periods which are being assessed for its movement and direction of movement through the

analysis of descriptive statistics.

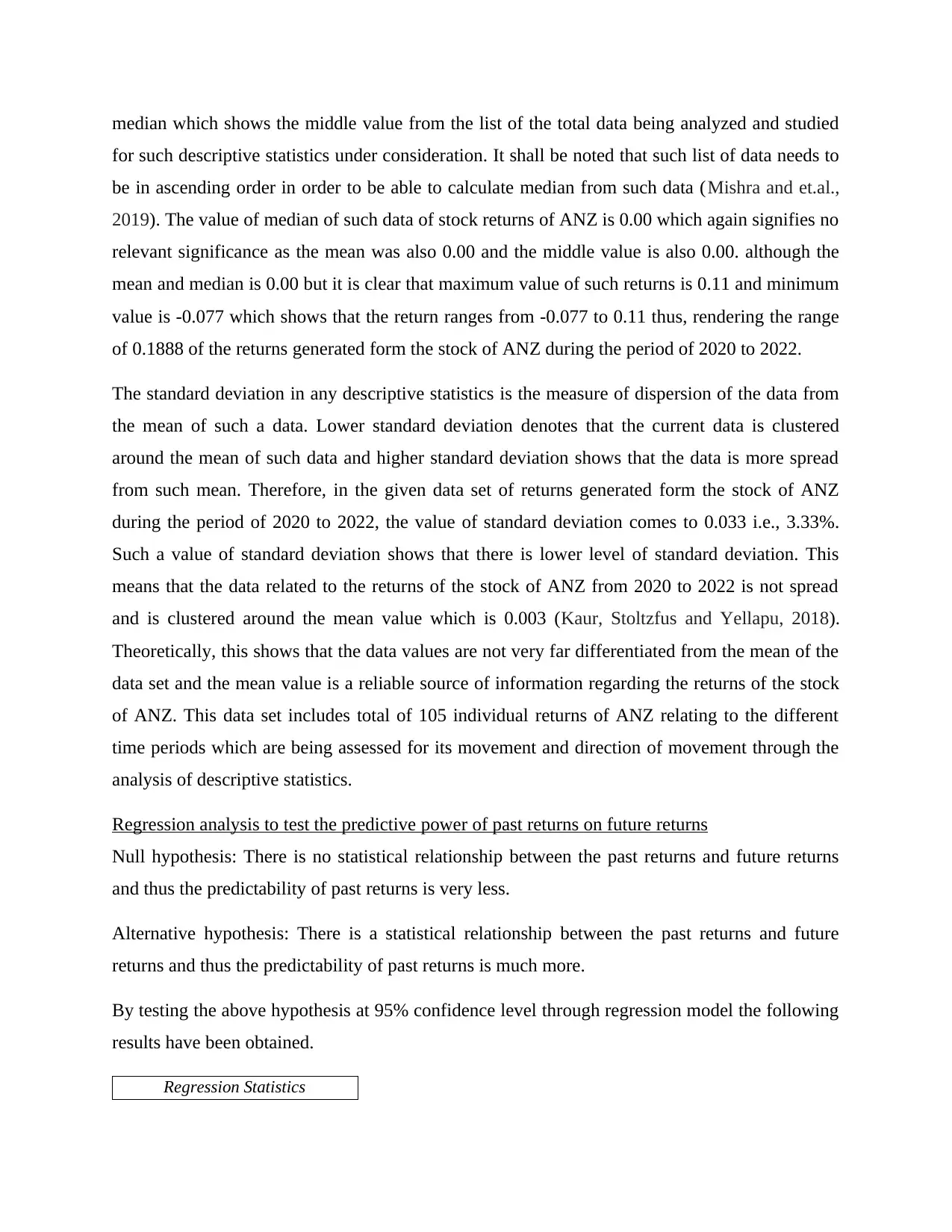

Regression analysis to test the predictive power of past returns on future returns

Null hypothesis: There is no statistical relationship between the past returns and future returns

and thus the predictability of past returns is very less.

Alternative hypothesis: There is a statistical relationship between the past returns and future

returns and thus the predictability of past returns is much more.

By testing the above hypothesis at 95% confidence level through regression model the following

results have been obtained.

Regression Statistics

for such descriptive statistics under consideration. It shall be noted that such list of data needs to

be in ascending order in order to be able to calculate median from such data (Mishra and et.al.,

2019). The value of median of such data of stock returns of ANZ is 0.00 which again signifies no

relevant significance as the mean was also 0.00 and the middle value is also 0.00. although the

mean and median is 0.00 but it is clear that maximum value of such returns is 0.11 and minimum

value is -0.077 which shows that the return ranges from -0.077 to 0.11 thus, rendering the range

of 0.1888 of the returns generated form the stock of ANZ during the period of 2020 to 2022.

The standard deviation in any descriptive statistics is the measure of dispersion of the data from

the mean of such a data. Lower standard deviation denotes that the current data is clustered

around the mean of such data and higher standard deviation shows that the data is more spread

from such mean. Therefore, in the given data set of returns generated form the stock of ANZ

during the period of 2020 to 2022, the value of standard deviation comes to 0.033 i.e., 3.33%.

Such a value of standard deviation shows that there is lower level of standard deviation. This

means that the data related to the returns of the stock of ANZ from 2020 to 2022 is not spread

and is clustered around the mean value which is 0.003 (Kaur, Stoltzfus and Yellapu, 2018).

Theoretically, this shows that the data values are not very far differentiated from the mean of the

data set and the mean value is a reliable source of information regarding the returns of the stock

of ANZ. This data set includes total of 105 individual returns of ANZ relating to the different

time periods which are being assessed for its movement and direction of movement through the

analysis of descriptive statistics.

Regression analysis to test the predictive power of past returns on future returns

Null hypothesis: There is no statistical relationship between the past returns and future returns

and thus the predictability of past returns is very less.

Alternative hypothesis: There is a statistical relationship between the past returns and future

returns and thus the predictability of past returns is much more.

By testing the above hypothesis at 95% confidence level through regression model the following

results have been obtained.

Regression Statistics

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Multiple R 0.00455187

8

R Square 2.07196E-

05

Adjusted R

Square

-0.009783

Standard Error 0.03367117

9

Observations 104

ANOVA

df SS MS F Significance

F

Regression 1 2.4E-06 2.4E-06 0.002113 0.963422

Residual 102 0.115642 0.001134

Total 103 0.115645

Coefficie

nts

Standard

Error

t Stat P-

value

Lower

95%

Upper

95%

Lower

95.0%

Upper

95.0%

Interce

pt

0.003428

56

0.003318 1.0333

42

0.3038

88

-0.00315 0.01001 -0.00315 0.01001

Retlag 0.004553

998

0.09906 0.0459

72

0.9634

22

-0.19193 0.20103

9

-0.19193 0.201039

Regression equation obtained on the basis of above analysis is as follows:

Y = a + bx

Y = future returns or the weekly returns of ANZ stocks

a = intercept of the regression line where the x axis and y axis intersect each other = 0.003

b = slope of the regression line = 0.0046

x = value of RETLAG (returns of the last week)

Accordingly, the regression equation for the stock returns of ANZ would be as follows:

Ret = 0.003 + 0.0046(Retlag)

Number of observation 105

Adjusted r square -0.009783

8

R Square 2.07196E-

05

Adjusted R

Square

-0.009783

Standard Error 0.03367117

9

Observations 104

ANOVA

df SS MS F Significance

F

Regression 1 2.4E-06 2.4E-06 0.002113 0.963422

Residual 102 0.115642 0.001134

Total 103 0.115645

Coefficie

nts

Standard

Error

t Stat P-

value

Lower

95%

Upper

95%

Lower

95.0%

Upper

95.0%

Interce

pt

0.003428

56

0.003318 1.0333

42

0.3038

88

-0.00315 0.01001 -0.00315 0.01001

Retlag 0.004553

998

0.09906 0.0459

72

0.9634

22

-0.19193 0.20103

9

-0.19193 0.201039

Regression equation obtained on the basis of above analysis is as follows:

Y = a + bx

Y = future returns or the weekly returns of ANZ stocks

a = intercept of the regression line where the x axis and y axis intersect each other = 0.003

b = slope of the regression line = 0.0046

x = value of RETLAG (returns of the last week)

Accordingly, the regression equation for the stock returns of ANZ would be as follows:

Ret = 0.003 + 0.0046(Retlag)

Number of observation 105

Adjusted r square -0.009783

Value of the slope 0.0046

P value of the slope 0.963422

Through the above regression analysis results, it can be seen that the predictive power of

lagged returns is very poor because the p value obtained through the regression model is 0.963

which is greater than the significance value of 0.05 and thus the null hypothesis must be accepted

which states that the predictive power of lagged returns on future returns from ANZ stock is less

because of no statistical relationship existing between the predictor variable and response

variable which include Retlag and Ret respectively. Further, the value of slope has come out as

0.0046 which indicates that a one unit change in predictor variable that is, Retlag or past returns

would result in 0.0046 change in the response variable that is, Ret or future weekly returns from

ANZ stocks. This shows that the predictability of the independent variable or x variable which is

Retlag showing the past returns of the ANZ stock is very less in determining the current or future

weekly returns that would be obtained through holding the stocks of ANZ (Bhatnagar, and et. al.

2021). Also, the value of adjusted r square has obtained which indicates the changes that is

taking place in dependent variable with the changes taking place in independent variable. This

value comes as -0.0097 where the value is negative and this means the Retlag are not capable of

determining or forecasting the future returns of Ret. At last the number of observations with

reference to the weekly stock returns of ANZ includes 105 weeks which are relevant to the past

two years that is, from October 2020 to October 2022.

Summarizing the results, providing conclusions and making recommendations

Through the above report, it has been determined that the weekly returns of ANZ stock is

showing decreasing patterns however, no constant trend or seasonality found in the time series

data. As the prices of stock of ANZ is taking random value, the mean value of the weekly returns

comes as 0 and thus, the data can be said to be looking like white noise (Brook and Arnold,

2018). Further, the lagged or past returns of the stock are found to be less powerful in predicting

the future stock returns of ANZ because of the acceptance of null hypothesis, negative adjusted r

value and the value of slope found to be very low or equivalent to zero. The following

recommendations could be made for the improvement of the analysis:

P value of the slope 0.963422

Through the above regression analysis results, it can be seen that the predictive power of

lagged returns is very poor because the p value obtained through the regression model is 0.963

which is greater than the significance value of 0.05 and thus the null hypothesis must be accepted

which states that the predictive power of lagged returns on future returns from ANZ stock is less

because of no statistical relationship existing between the predictor variable and response

variable which include Retlag and Ret respectively. Further, the value of slope has come out as

0.0046 which indicates that a one unit change in predictor variable that is, Retlag or past returns

would result in 0.0046 change in the response variable that is, Ret or future weekly returns from

ANZ stocks. This shows that the predictability of the independent variable or x variable which is

Retlag showing the past returns of the ANZ stock is very less in determining the current or future

weekly returns that would be obtained through holding the stocks of ANZ (Bhatnagar, and et. al.

2021). Also, the value of adjusted r square has obtained which indicates the changes that is

taking place in dependent variable with the changes taking place in independent variable. This

value comes as -0.0097 where the value is negative and this means the Retlag are not capable of

determining or forecasting the future returns of Ret. At last the number of observations with

reference to the weekly stock returns of ANZ includes 105 weeks which are relevant to the past

two years that is, from October 2020 to October 2022.

Summarizing the results, providing conclusions and making recommendations

Through the above report, it has been determined that the weekly returns of ANZ stock is

showing decreasing patterns however, no constant trend or seasonality found in the time series

data. As the prices of stock of ANZ is taking random value, the mean value of the weekly returns

comes as 0 and thus, the data can be said to be looking like white noise (Brook and Arnold,

2018). Further, the lagged or past returns of the stock are found to be less powerful in predicting

the future stock returns of ANZ because of the acceptance of null hypothesis, negative adjusted r

value and the value of slope found to be very low or equivalent to zero. The following

recommendations could be made for the improvement of the analysis:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The Retlag must be replace with some variables like the market risk (beta), market size

(market capitalization), profitability of the company or the book value of stock. This is

because these factors are better representative as well as highly affecting the stock prices

of the company. Thus, making predictions for future stock returns much simpler & easy.

The analysis could be improved by taking the data for greater term like five years which

can be both weekly or monthly to indicate how ANZ stock is providing returns on year

on year basis (Desboulets, 2018).

It is also recommended to include the time series data for the ASX index 200 of which

ANZ is one of the component in order to make predictions for future weekly returns from

the stock. ASX 200 being a market index would be best for determining the statistical

relationship between the movement of ANZ stock prices and movement of market index.

The market index is the best indicator of future movement in the price of stock forming

it.

The variables that has been used in this report for the purpose of quantitative analysis &

forecasting are two which includes retlag (past returns of the stock) and the returns of the current

week for determining how much the past returns are powerful in predicting the future stock

returns of ANZ (Desboulets, 2018). The methods used for the analysis are graphical

representation to determine the trend in the weekly stock returns of ANZ, descriptive statistics

for determining the average returns provided by the ANZ stocks on weekly basis. At last,

regression analysis has been used for the purpose of testing the hypothesis in order to determine

whether the Retlag is powerful in predicting the future returns of the stock on weekly basis.

(market capitalization), profitability of the company or the book value of stock. This is

because these factors are better representative as well as highly affecting the stock prices

of the company. Thus, making predictions for future stock returns much simpler & easy.

The analysis could be improved by taking the data for greater term like five years which

can be both weekly or monthly to indicate how ANZ stock is providing returns on year

on year basis (Desboulets, 2018).

It is also recommended to include the time series data for the ASX index 200 of which

ANZ is one of the component in order to make predictions for future weekly returns from

the stock. ASX 200 being a market index would be best for determining the statistical

relationship between the movement of ANZ stock prices and movement of market index.

The market index is the best indicator of future movement in the price of stock forming

it.

The variables that has been used in this report for the purpose of quantitative analysis &

forecasting are two which includes retlag (past returns of the stock) and the returns of the current

week for determining how much the past returns are powerful in predicting the future stock

returns of ANZ (Desboulets, 2018). The methods used for the analysis are graphical

representation to determine the trend in the weekly stock returns of ANZ, descriptive statistics

for determining the average returns provided by the ANZ stocks on weekly basis. At last,

regression analysis has been used for the purpose of testing the hypothesis in order to determine

whether the Retlag is powerful in predicting the future returns of the stock on weekly basis.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals

Kemp, S. E., Hort, J. and Hollowood, T. eds., 2018. Descriptive analysis in sensory evaluation.

Bhatnagar, V., and et. al. 2021. Descriptive analysis of COVID-19 patients in the context of

India. Journal of Interdisciplinary Mathematics, 24(3), pp.489-504.

Desboulets, L. D. D., 2018. A review on variable selection in regression

analysis. Econometrics, 6(4), p.45.

Brook, R. J. and Arnold, G. C., 2018. Applied regression analysis and experimental design. CRC

Press.

Requioma, G.M.S., et. al. 2020, December. White noise analysis of the interplanetary magnetic

field for the minimum phase of solar cycle 23. In AIP Conference Proceedings (Vol.

2286, No. 1, p. 030006). AIP Publishing LLC.

Farzaneh, S., and et. al. 2020. Assessment of noise in time series analysis for Buoy tide

observations. International Journal of Maritime Technology, 13, pp.41-49.

Valaskova, K., Kliestik, T. and Kovacova, M., 2018. Management of financial risks in Slovak

enterprises using regression analysis. Oeconomia copernicana, 9(1), pp.105-121.

Gunst, R. F. and Mason, R. L., 2018. Regression analysis and its application: a data-oriented

approach. CRC Press.

Ghosal, S., and et. al. 2020. Linear Regression Analysis to predict the number of deaths in India

due to SARS-CoV-2 at 6 weeks from day 0 (100 cases-March 14th 2020). Diabetes &

Metabolic Syndrome: Clinical Research & Reviews, 14(4), pp.311-315.

Mishra, P. and et.al., 2019. Descriptive statistics and normality tests for statistical data. Annals of

cardiac anaesthesia. 22(1). p.67.

Kaur, P., Stoltzfus, J. and Yellapu, V., 2018. Descriptive statistics. International Journal of

Academic Medicine. 4(1). p.60.

Books and Journals

Kemp, S. E., Hort, J. and Hollowood, T. eds., 2018. Descriptive analysis in sensory evaluation.

Bhatnagar, V., and et. al. 2021. Descriptive analysis of COVID-19 patients in the context of

India. Journal of Interdisciplinary Mathematics, 24(3), pp.489-504.

Desboulets, L. D. D., 2018. A review on variable selection in regression

analysis. Econometrics, 6(4), p.45.

Brook, R. J. and Arnold, G. C., 2018. Applied regression analysis and experimental design. CRC

Press.

Requioma, G.M.S., et. al. 2020, December. White noise analysis of the interplanetary magnetic

field for the minimum phase of solar cycle 23. In AIP Conference Proceedings (Vol.

2286, No. 1, p. 030006). AIP Publishing LLC.

Farzaneh, S., and et. al. 2020. Assessment of noise in time series analysis for Buoy tide

observations. International Journal of Maritime Technology, 13, pp.41-49.

Valaskova, K., Kliestik, T. and Kovacova, M., 2018. Management of financial risks in Slovak

enterprises using regression analysis. Oeconomia copernicana, 9(1), pp.105-121.

Gunst, R. F. and Mason, R. L., 2018. Regression analysis and its application: a data-oriented

approach. CRC Press.

Ghosal, S., and et. al. 2020. Linear Regression Analysis to predict the number of deaths in India

due to SARS-CoV-2 at 6 weeks from day 0 (100 cases-March 14th 2020). Diabetes &

Metabolic Syndrome: Clinical Research & Reviews, 14(4), pp.311-315.

Mishra, P. and et.al., 2019. Descriptive statistics and normality tests for statistical data. Annals of

cardiac anaesthesia. 22(1). p.67.

Kaur, P., Stoltzfus, J. and Yellapu, V., 2018. Descriptive statistics. International Journal of

Academic Medicine. 4(1). p.60.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.