ARIMA Model: Forecasting Future GDP of British Columbia, Canada

VerifiedAdded on 2023/04/19

|12

|2479

|211

Project

AI Summary

This project focuses on forecasting the Gross Domestic Product (GDP) of British Columbia using the Auto Regressive Integrated Moving Average (ARIMA) model. The study employs time series analysis, utilizing Auto Correlation Function (ACF) and Partial Auto Correlation Function (PACF) to identify suitable ARIMA parameters. The research objectives include testing for stationarity in GDP data using the Augmented Dickey-Fuller unit root test, studying autocorrelation, validating the model statistically with a portmanteau test, and forecasting GDP for the next ten years with upper and lower control levels. The methodology involves collecting GDP data from 1997 to 2017 and applying the Box-Jenkins approach to identify the stochastic process of the time series. The empirical results include model identification, stationarity testing, and ARIMA model application, culminating in GDP forecasts for British Columbia.

Forecasting the future GDP of British Columbia

using ARIMA model on Eviews

Student Name ******

Abstract

Basically, forecasting are important and it continually made in business, fund,

financial matters, government, and numerous different fields, and much relies on them.

Similarly, there are there are good and bad ways to forecast. The forecasting is used to

provide the great ways for current, quantitative, economic and statistical strategies for

evaluating and producing the forecasts. Forecasts are settled on to direct decisions in an

variety of fields. Gross Domestic Product (GDP) of a nation is the cash estimation of all

goods and administrations created by every one of the enterprises inside the bounds of a

nation in a year. It speaks to the total measurement of all financial action. The execution of

economy can be forecast with the assistance of GDP. As indicated by Euro stat, there are

three manners by which the GDP of a nation can be forecasts. This paper aims to displaying

and determining forecasting GDP of British Columbia utilizing ARIMA model. Here

analyzed by time series method. Auto Correlation Function (ACF) and Partial Auto

Correlation Function (PACF) are will calculated. Proper Box-Jenkins Auto Regressive

Integrated Moving Average (ARIMA) demonstrates the forecasting the future GDP of British

Columbia. Legitimacy of the model was tested using standard statistical techniques. And,

ARIMA model is used to show were utilized to forecasting zone and creation of British

Columbia for future years.

Keywords: Forecast, GDP, ACF, PACF and ARIMA

1

using ARIMA model on Eviews

Student Name ******

Abstract

Basically, forecasting are important and it continually made in business, fund,

financial matters, government, and numerous different fields, and much relies on them.

Similarly, there are there are good and bad ways to forecast. The forecasting is used to

provide the great ways for current, quantitative, economic and statistical strategies for

evaluating and producing the forecasts. Forecasts are settled on to direct decisions in an

variety of fields. Gross Domestic Product (GDP) of a nation is the cash estimation of all

goods and administrations created by every one of the enterprises inside the bounds of a

nation in a year. It speaks to the total measurement of all financial action. The execution of

economy can be forecast with the assistance of GDP. As indicated by Euro stat, there are

three manners by which the GDP of a nation can be forecasts. This paper aims to displaying

and determining forecasting GDP of British Columbia utilizing ARIMA model. Here

analyzed by time series method. Auto Correlation Function (ACF) and Partial Auto

Correlation Function (PACF) are will calculated. Proper Box-Jenkins Auto Regressive

Integrated Moving Average (ARIMA) demonstrates the forecasting the future GDP of British

Columbia. Legitimacy of the model was tested using standard statistical techniques. And,

ARIMA model is used to show were utilized to forecasting zone and creation of British

Columbia for future years.

Keywords: Forecast, GDP, ACF, PACF and ARIMA

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Introduction

The forecasting is used to provide the great ways for current, quantitative, economic

and statistical strategies for evaluating and producing the forecasts. Forecasts are settled on to

direct decisions in a variety of fields. Gross Domestic Product (GDP) of a nation is the cash

estimation of all goods and administrations created by every one of the enterprises inside the

bounds of a nation in a year. The execution of economy can be forecast with the assistance of

GDP. This paper aims to displaying and determining forecasting GDP of British Columbia

utilizing ARIMA model. Here analyzed by time series method. Auto Correlation Function

(ACF) and Partial Auto Correlation Function (PACF) are will calculated. Proper Box-Jenkins

Auto Regressive Integrated Moving Average (ARIMA) demonstrates the forecasting the

future GDP of British Columbia. Legitimacy of the model was tested using standard

statistical techniques. And, ARIMA model is used to show were utilized to forecasting zone

and creation of British Columbia for future years.

Research Objectives

1. To test the stationary in the data of GDP using the Augmented Dickey – Fullers unit

root test over the period.

2. To study Auto correlation in the observed series of GDP ACF and PACF values and

correlogram will be used to measure the AR and MA to predict which past series is a

fitter model for future value prediction.

3. To test the model validity statically a portmanteau test of Independence i.e. the BDS

test for time-based dependence in a series will be applied.

4. Finally Forecast the GDP for the next ten years using ARIMA Model along with the

upper control level (UCL) and the lower control level (LCL).

Literature Review

According to this paper (Dritsaki, 2015), the ARIMA model has be used extensively

by many researchers. This method is used to highlight the future rates of GDP. It easily

examines the forecasting of GDP growth rate for India using the ARIMA model. This model

is used to predicted the values follow an increasing the trend for a years. It establishes the

stationary of time series. Result of this paper is used to provide the policy makers to

formulate the effective policies for attracting the foreign direct investment. It also helpful the

2

The forecasting is used to provide the great ways for current, quantitative, economic

and statistical strategies for evaluating and producing the forecasts. Forecasts are settled on to

direct decisions in a variety of fields. Gross Domestic Product (GDP) of a nation is the cash

estimation of all goods and administrations created by every one of the enterprises inside the

bounds of a nation in a year. The execution of economy can be forecast with the assistance of

GDP. This paper aims to displaying and determining forecasting GDP of British Columbia

utilizing ARIMA model. Here analyzed by time series method. Auto Correlation Function

(ACF) and Partial Auto Correlation Function (PACF) are will calculated. Proper Box-Jenkins

Auto Regressive Integrated Moving Average (ARIMA) demonstrates the forecasting the

future GDP of British Columbia. Legitimacy of the model was tested using standard

statistical techniques. And, ARIMA model is used to show were utilized to forecasting zone

and creation of British Columbia for future years.

Research Objectives

1. To test the stationary in the data of GDP using the Augmented Dickey – Fullers unit

root test over the period.

2. To study Auto correlation in the observed series of GDP ACF and PACF values and

correlogram will be used to measure the AR and MA to predict which past series is a

fitter model for future value prediction.

3. To test the model validity statically a portmanteau test of Independence i.e. the BDS

test for time-based dependence in a series will be applied.

4. Finally Forecast the GDP for the next ten years using ARIMA Model along with the

upper control level (UCL) and the lower control level (LCL).

Literature Review

According to this paper (Dritsaki, 2015), the ARIMA model has be used extensively

by many researchers. This method is used to highlight the future rates of GDP. It easily

examines the forecasting of GDP growth rate for India using the ARIMA model. This model

is used to predicted the values follow an increasing the trend for a years. It establishes the

stationary of time series. Result of this paper is used to provide the policy makers to

formulate the effective policies for attracting the foreign direct investment. It also helpful the

2

managerial business executive for implementing or taking decision concerned with the

expansion of the existing business.

Methodology

The GDP data was collected over the time period from 1997 to 2017 were used for

forecasting the future values using Auto Regressive Integrated Moving Average (ARIMA)

models. The ARIMA procedure is likewise called as Box-Jenkins approach. The Box-Jenkins

method is worried about fitting an ARIMA model to a given data of information. The

objective in fitting ARIMA model is to distinguish the stochastic procedure of the time series

and predicted the future values correctly. These strategies have additionally been helpful in

numerous sorts of circumstances which include the working of models for discrete time series

and dynamic frameworks. Anyway this technique is not useful for seasonal series with a large

random component.

Data Description

The GDP data was collected over the time period from 1997 to 2017. The provided data was

contains the information about the forecast the GDP growth for the province of British

Columbia based on the overall annual expenditure. It is illustrated as below (Camacho &

Martinez-Martin, 2013).

3

expansion of the existing business.

Methodology

The GDP data was collected over the time period from 1997 to 2017 were used for

forecasting the future values using Auto Regressive Integrated Moving Average (ARIMA)

models. The ARIMA procedure is likewise called as Box-Jenkins approach. The Box-Jenkins

method is worried about fitting an ARIMA model to a given data of information. The

objective in fitting ARIMA model is to distinguish the stochastic procedure of the time series

and predicted the future values correctly. These strategies have additionally been helpful in

numerous sorts of circumstances which include the working of models for discrete time series

and dynamic frameworks. Anyway this technique is not useful for seasonal series with a large

random component.

Data Description

The GDP data was collected over the time period from 1997 to 2017. The provided data was

contains the information about the forecast the GDP growth for the province of British

Columbia based on the overall annual expenditure. It is illustrated as below (Camacho &

Martinez-Martin, 2013).

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

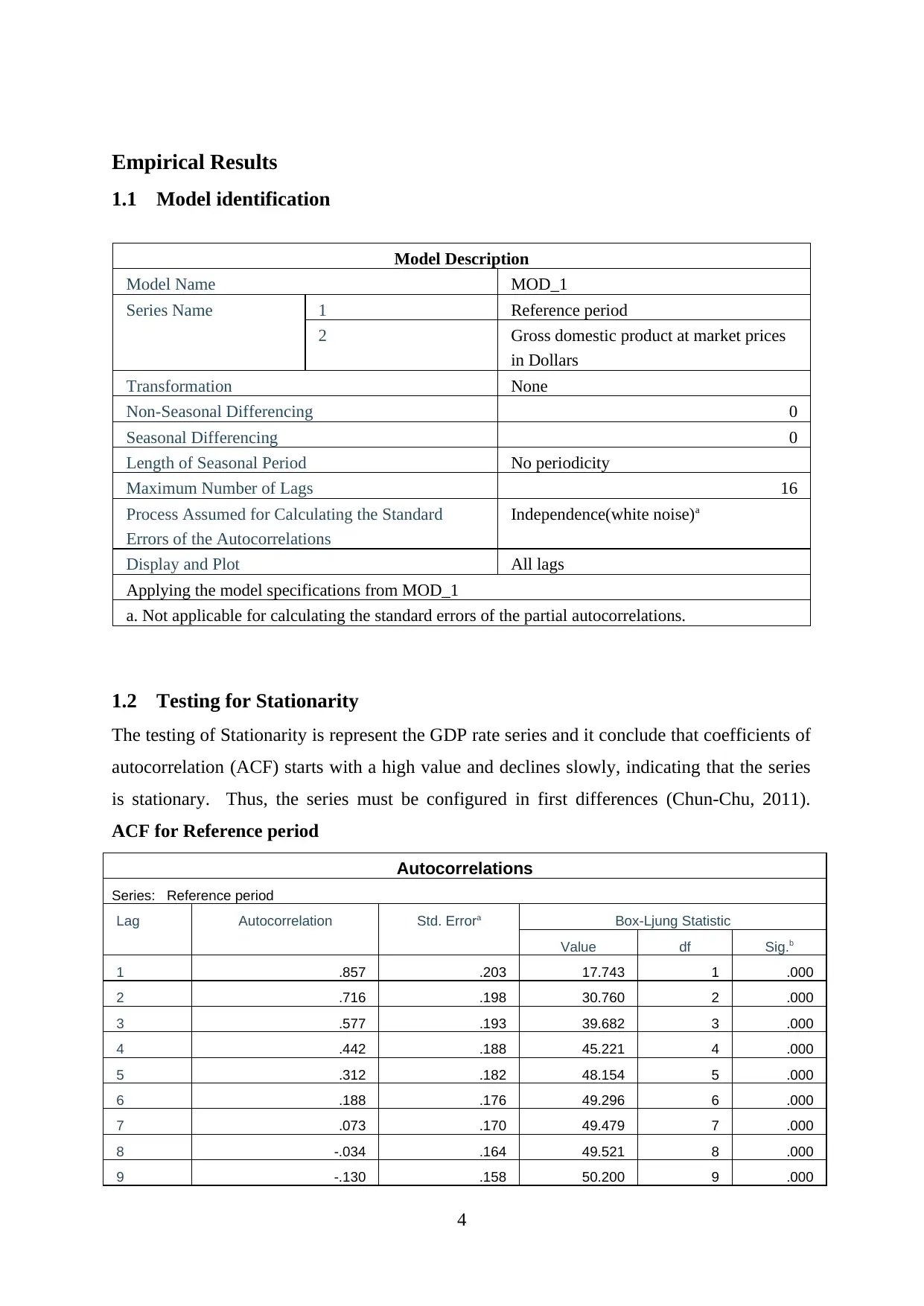

Empirical Results

1.1 Model identification

Model Description

Model Name MOD_1

Series Name 1 Reference period

2 Gross domestic product at market prices

in Dollars

Transformation None

Non-Seasonal Differencing 0

Seasonal Differencing 0

Length of Seasonal Period No periodicity

Maximum Number of Lags 16

Process Assumed for Calculating the Standard

Errors of the Autocorrelations

Independence(white noise)a

Display and Plot All lags

Applying the model specifications from MOD_1

a. Not applicable for calculating the standard errors of the partial autocorrelations.

1.2 Testing for Stationarity

The testing of Stationarity is represent the GDP rate series and it conclude that coefficients of

autocorrelation (ACF) starts with a high value and declines slowly, indicating that the series

is stationary. Thus, the series must be configured in first differences (Chun-Chu, 2011).

ACF for Reference period

Autocorrelations

Series: Reference period

Lag Autocorrelation Std. Errora Box-Ljung Statistic

Value df Sig.b

1 .857 .203 17.743 1 .000

2 .716 .198 30.760 2 .000

3 .577 .193 39.682 3 .000

4 .442 .188 45.221 4 .000

5 .312 .182 48.154 5 .000

6 .188 .176 49.296 6 .000

7 .073 .170 49.479 7 .000

8 -.034 .164 49.521 8 .000

9 -.130 .158 50.200 9 .000

4

1.1 Model identification

Model Description

Model Name MOD_1

Series Name 1 Reference period

2 Gross domestic product at market prices

in Dollars

Transformation None

Non-Seasonal Differencing 0

Seasonal Differencing 0

Length of Seasonal Period No periodicity

Maximum Number of Lags 16

Process Assumed for Calculating the Standard

Errors of the Autocorrelations

Independence(white noise)a

Display and Plot All lags

Applying the model specifications from MOD_1

a. Not applicable for calculating the standard errors of the partial autocorrelations.

1.2 Testing for Stationarity

The testing of Stationarity is represent the GDP rate series and it conclude that coefficients of

autocorrelation (ACF) starts with a high value and declines slowly, indicating that the series

is stationary. Thus, the series must be configured in first differences (Chun-Chu, 2011).

ACF for Reference period

Autocorrelations

Series: Reference period

Lag Autocorrelation Std. Errora Box-Ljung Statistic

Value df Sig.b

1 .857 .203 17.743 1 .000

2 .716 .198 30.760 2 .000

3 .577 .193 39.682 3 .000

4 .442 .188 45.221 4 .000

5 .312 .182 48.154 5 .000

6 .188 .176 49.296 6 .000

7 .073 .170 49.479 7 .000

8 -.034 .164 49.521 8 .000

9 -.130 .158 50.200 9 .000

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10 -.214 .151 52.216 10 .000

11 -.286 .144 56.159 11 .000

12 -.343 .137 62.467 12 .000

13 -.384 .129 71.389 13 .000

14 -.409 .120 82.937 14 .000

15 -.416 .111 96.840 15 .000

16 -.403 .102 112.497 16 .000

a. The underlying process assumed is independence (white noise).

b. Based on the asymptotic chi-square approximation.

ACF for Gross domestic product at market prices in Dollars

Autocorrelations

Series: Gross domestic product at market prices in Dollars

Lag Autocorrelation Std. Errora Box-Ljung Statistic

Value df Sig.b

1 .842 .203 17.108 1 .000

2 .686 .198 29.065 2 .000

3 .541 .193 36.929 3 .000

4 .408 .188 41.649 4 .000

5 .282 .182 44.044 5 .000

6 .167 .176 44.941 6 .000

7 .058 .170 45.056 7 .000

8 -.032 .164 45.094 8 .000

9 -.097 .158 45.470 9 .000

10 -.168 .151 46.713 10 .000

11 -.236 .144 49.394 11 .000

12 -.298 .137 54.152 12 .000

13 -.363 .129 62.094 13 .000

14 -.398 .120 73.047 14 .000

15 -.409 .111 86.482 15 .000

16 -.403 .102 102.134 16 .000

a. The underlying process assumed is independence (white noise).

b. Based on the asymptotic chi-square approximation.

PACF for Reference period

5

11 -.286 .144 56.159 11 .000

12 -.343 .137 62.467 12 .000

13 -.384 .129 71.389 13 .000

14 -.409 .120 82.937 14 .000

15 -.416 .111 96.840 15 .000

16 -.403 .102 112.497 16 .000

a. The underlying process assumed is independence (white noise).

b. Based on the asymptotic chi-square approximation.

ACF for Gross domestic product at market prices in Dollars

Autocorrelations

Series: Gross domestic product at market prices in Dollars

Lag Autocorrelation Std. Errora Box-Ljung Statistic

Value df Sig.b

1 .842 .203 17.108 1 .000

2 .686 .198 29.065 2 .000

3 .541 .193 36.929 3 .000

4 .408 .188 41.649 4 .000

5 .282 .182 44.044 5 .000

6 .167 .176 44.941 6 .000

7 .058 .170 45.056 7 .000

8 -.032 .164 45.094 8 .000

9 -.097 .158 45.470 9 .000

10 -.168 .151 46.713 10 .000

11 -.236 .144 49.394 11 .000

12 -.298 .137 54.152 12 .000

13 -.363 .129 62.094 13 .000

14 -.398 .120 73.047 14 .000

15 -.409 .111 86.482 15 .000

16 -.403 .102 102.134 16 .000

a. The underlying process assumed is independence (white noise).

b. Based on the asymptotic chi-square approximation.

PACF for Reference period

5

Partial Autocorrelations

Series: Reference period

Lag Partial Autocorrelation Std. Error

1 .857 .218

2 -.072 .218

3 -.073 .218

4 -.073 .218

5 -.074 .218

6 -.074 .218

7 -.074 .218

8 -.073 .218

9 -.072 .218

10 -.070 .218

11 -.066 .218

12 -.061 .218

13 -.054 .218

14 -.044 .218

15 -.031 .218

16 -.014 .218

PACF for Gross domestic product at market prices in Dollars

Partial Autocorrelations

Series: Gross domestic product at market prices in Dollars

Lag Partial Autocorrelation Std. Error

1 .842 .218

2 -.078 .218

3 -.053 .218

4 -.057 .218

5 -.067 .218

6 -.058 .218

7 -.079 .218

8 -.035 .218

9 -.010 .218

10 -.109 .218

11 -.080 .218

12 -.085 .218

13 -.121 .218

14 -.020 .218

6

Series: Reference period

Lag Partial Autocorrelation Std. Error

1 .857 .218

2 -.072 .218

3 -.073 .218

4 -.073 .218

5 -.074 .218

6 -.074 .218

7 -.074 .218

8 -.073 .218

9 -.072 .218

10 -.070 .218

11 -.066 .218

12 -.061 .218

13 -.054 .218

14 -.044 .218

15 -.031 .218

16 -.014 .218

PACF for Gross domestic product at market prices in Dollars

Partial Autocorrelations

Series: Gross domestic product at market prices in Dollars

Lag Partial Autocorrelation Std. Error

1 .842 .218

2 -.078 .218

3 -.053 .218

4 -.057 .218

5 -.067 .218

6 -.058 .218

7 -.079 .218

8 -.035 .218

9 -.010 .218

10 -.109 .218

11 -.080 .218

12 -.085 .218

13 -.121 .218

14 -.020 .218

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

15 -.019 .218

16 -.028 .218

1.3 ARIMA model

Subsequent to making the GDP series stationary the autocorrelation and partial

autocorrelation function were utilized. By examining the PACF values and correlogram term

AR and MA was observed to be fit for forecasts. The ARMA parameters were distinguished

utilizing Autocorrelation and Partial Autocorrelation Functions. It is illustrated as below

(Fildes & Allen, 2011).

Model Description

Model Type

Model ID Gross domestic product at

market prices in Dollars

Model_1 ARIMA(0,1,0)

Residual ACF Summary

Lag Mean SE Minim

um

Maxim

um

Percentile

5 10 25 50 75 90 95

Lag

1

.200 . .200 .200 .200 .200 .200 .200 .200 .200 .200

Lag

2

-.101 . -.101 -.101 -.101 -.101 -.101 -.101 -.101 -.101 -.101

Lag

3

-.134 . -.134 -.134 -.134 -.134 -.134 -.134 -.134 -.134 -.134

Lag

4

-.250 . -.250 -.250 -.250 -.250 -.250 -.250 -.250 -.250 -.250

Lag

5

-.157 . -.157 -.157 -.157 -.157 -.157 -.157 -.157 -.157 -.157

Lag

6

.034 . .034 .034 .034 .034 .034 .034 .034 .034 .034

Lag

7

-.119 . -.119 -.119 -.119 -.119 -.119 -.119 -.119 -.119 -.119

Lag

8

-.091 . -.091 -.091 -.091 -.091 -.091 -.091 -.091 -.091 -.091

Lag

9

-.121 . -.121 -.121 -.121 -.121 -.121 -.121 -.121 -.121 -.121

Lag

10

.119 . .119 .119 .119 .119 .119 .119 .119 .119 .119

Lag .257 . .257 .257 .257 .257 .257 .257 .257 .257 .257

7

16 -.028 .218

1.3 ARIMA model

Subsequent to making the GDP series stationary the autocorrelation and partial

autocorrelation function were utilized. By examining the PACF values and correlogram term

AR and MA was observed to be fit for forecasts. The ARMA parameters were distinguished

utilizing Autocorrelation and Partial Autocorrelation Functions. It is illustrated as below

(Fildes & Allen, 2011).

Model Description

Model Type

Model ID Gross domestic product at

market prices in Dollars

Model_1 ARIMA(0,1,0)

Residual ACF Summary

Lag Mean SE Minim

um

Maxim

um

Percentile

5 10 25 50 75 90 95

Lag

1

.200 . .200 .200 .200 .200 .200 .200 .200 .200 .200

Lag

2

-.101 . -.101 -.101 -.101 -.101 -.101 -.101 -.101 -.101 -.101

Lag

3

-.134 . -.134 -.134 -.134 -.134 -.134 -.134 -.134 -.134 -.134

Lag

4

-.250 . -.250 -.250 -.250 -.250 -.250 -.250 -.250 -.250 -.250

Lag

5

-.157 . -.157 -.157 -.157 -.157 -.157 -.157 -.157 -.157 -.157

Lag

6

.034 . .034 .034 .034 .034 .034 .034 .034 .034 .034

Lag

7

-.119 . -.119 -.119 -.119 -.119 -.119 -.119 -.119 -.119 -.119

Lag

8

-.091 . -.091 -.091 -.091 -.091 -.091 -.091 -.091 -.091 -.091

Lag

9

-.121 . -.121 -.121 -.121 -.121 -.121 -.121 -.121 -.121 -.121

Lag

10

.119 . .119 .119 .119 .119 .119 .119 .119 .119 .119

Lag .257 . .257 .257 .257 .257 .257 .257 .257 .257 .257

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11

Lag

12

.108 . .108 .108 .108 .108 .108 .108 .108 .108 .108

Lag

13

-.066 . -.066 -.066 -.066 -.066 -.066 -.066 -.066 -.066 -.066

Lag

14

.018 . .018 .018 .018 .018 .018 .018 .018 .018 .018

Lag

15

-.022 . -.022 -.022 -.022 -.022 -.022 -.022 -.022 -.022 -.022

Lag

16

-.109 . -.109 -.109 -.109 -.109 -.109 -.109 -.109 -.109 -.109

Lag

17

.040 . .040 .040 .040 .040 .040 .040 .040 .040 .040

Lag

18

-.040 . -.040 -.040 -.040 -.040 -.040 -.040 -.040 -.040 -.040

Lag

19

-.068 . -.068 -.068 -.068 -.068 -.068 -.068 -.068 -.068 -.068

Residual PACF Summary

Lag Mean SE Minim

um

Maxim

um

Percentile

5 10 25 50 75 90 95

Lag

1

.200 . .200 .200 .200 .200 .200 .200 .200 .200 .200

Lag

2

-.146 . -.146 -.146 -.146 -.146 -.146 -.146 -.146 -.146 -.146

Lag

3

-.087 . -.087 -.087 -.087 -.087 -.087 -.087 -.087 -.087 -.087

Lag

4

-.232 . -.232 -.232 -.232 -.232 -.232 -.232 -.232 -.232 -.232

Lag

5

-.097 . -.097 -.097 -.097 -.097 -.097 -.097 -.097 -.097 -.097

Lag

6

.015 . .015 .015 .015 .015 .015 .015 .015 .015 .015

Lag

7

-.233 . -.233 -.233 -.233 -.233 -.233 -.233 -.233 -.233 -.233

Lag

8

-.121 . -.121 -.121 -.121 -.121 -.121 -.121 -.121 -.121 -.121

Lag

9

-.236 . -.236 -.236 -.236 -.236 -.236 -.236 -.236 -.236 -.236

Lag

10

.109 . .109 .109 .109 .109 .109 .109 .109 .109 .109

8

Lag

12

.108 . .108 .108 .108 .108 .108 .108 .108 .108 .108

Lag

13

-.066 . -.066 -.066 -.066 -.066 -.066 -.066 -.066 -.066 -.066

Lag

14

.018 . .018 .018 .018 .018 .018 .018 .018 .018 .018

Lag

15

-.022 . -.022 -.022 -.022 -.022 -.022 -.022 -.022 -.022 -.022

Lag

16

-.109 . -.109 -.109 -.109 -.109 -.109 -.109 -.109 -.109 -.109

Lag

17

.040 . .040 .040 .040 .040 .040 .040 .040 .040 .040

Lag

18

-.040 . -.040 -.040 -.040 -.040 -.040 -.040 -.040 -.040 -.040

Lag

19

-.068 . -.068 -.068 -.068 -.068 -.068 -.068 -.068 -.068 -.068

Residual PACF Summary

Lag Mean SE Minim

um

Maxim

um

Percentile

5 10 25 50 75 90 95

Lag

1

.200 . .200 .200 .200 .200 .200 .200 .200 .200 .200

Lag

2

-.146 . -.146 -.146 -.146 -.146 -.146 -.146 -.146 -.146 -.146

Lag

3

-.087 . -.087 -.087 -.087 -.087 -.087 -.087 -.087 -.087 -.087

Lag

4

-.232 . -.232 -.232 -.232 -.232 -.232 -.232 -.232 -.232 -.232

Lag

5

-.097 . -.097 -.097 -.097 -.097 -.097 -.097 -.097 -.097 -.097

Lag

6

.015 . .015 .015 .015 .015 .015 .015 .015 .015 .015

Lag

7

-.233 . -.233 -.233 -.233 -.233 -.233 -.233 -.233 -.233 -.233

Lag

8

-.121 . -.121 -.121 -.121 -.121 -.121 -.121 -.121 -.121 -.121

Lag

9

-.236 . -.236 -.236 -.236 -.236 -.236 -.236 -.236 -.236 -.236

Lag

10

.109 . .109 .109 .109 .109 .109 .109 .109 .109 .109

8

Lag

11

.091 . .091 .091 .091 .091 .091 .091 .091 .091 .091

Lag

12

-.064 . -.064 -.064 -.064 -.064 -.064 -.064 -.064 -.064 -.064

Lag

13

-.126 . -.126 -.126 -.126 -.126 -.126 -.126 -.126 -.126 -.126

Lag

14

.084 . .084 .084 .084 .084 .084 .084 .084 .084 .084

Lag

15

.079 . .079 .079 .079 .079 .079 .079 .079 .079 .079

Lag

16

-.153 . -.153 -.153 -.153 -.153 -.153 -.153 -.153 -.153 -.153

Lag

17

.055 . .055 .055 .055 .055 .055 .055 .055 .055 .055

Lag

18

-.052 . -.052 -.052 -.052 -.052 -.052 -.052 -.052 -.052 -.052

Lag

19

.082 . .082 .082 .082 .082 .082 .082 .082 .082 .082

Model Statistics

Model Number of

Predictors

Model Fit

statistics

Ljung-Box Q(18) Number of

Outliers

Stationary R-

squared

Statistics DF Sig.

Gross domestic product at

market prices in Dollars-

Model_1

0 2.220E-16 12.190 18 .837 0

1.4 Model Validity

Model validity is illustrated as below.

9

11

.091 . .091 .091 .091 .091 .091 .091 .091 .091 .091

Lag

12

-.064 . -.064 -.064 -.064 -.064 -.064 -.064 -.064 -.064 -.064

Lag

13

-.126 . -.126 -.126 -.126 -.126 -.126 -.126 -.126 -.126 -.126

Lag

14

.084 . .084 .084 .084 .084 .084 .084 .084 .084 .084

Lag

15

.079 . .079 .079 .079 .079 .079 .079 .079 .079 .079

Lag

16

-.153 . -.153 -.153 -.153 -.153 -.153 -.153 -.153 -.153 -.153

Lag

17

.055 . .055 .055 .055 .055 .055 .055 .055 .055 .055

Lag

18

-.052 . -.052 -.052 -.052 -.052 -.052 -.052 -.052 -.052 -.052

Lag

19

.082 . .082 .082 .082 .082 .082 .082 .082 .082 .082

Model Statistics

Model Number of

Predictors

Model Fit

statistics

Ljung-Box Q(18) Number of

Outliers

Stationary R-

squared

Statistics DF Sig.

Gross domestic product at

market prices in Dollars-

Model_1

0 2.220E-16 12.190 18 .837 0

1.4 Model Validity

Model validity is illustrated as below.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1.5 GDP Forecast

Final GDP Forecast values for Forecasting the future GDP of British Columbia is illustrated

as below (Şen Doğan & Midiliç, 2018).

Reference

period

Gross domestic product at

market prices in Dollars

(Predicted Values)

LCL UCL

2018 262158 255011 269306

2019 267441 257333 277550

2020 272725 260344 285105

2021 278008 263712 292303

2022 283291 267308 299274

2023 288574 271066 306082

2024 293857 274946 312768

2025 299141 278924 319357

2026 304424 282981 325867

2027 309707 287104 332310

10

Final GDP Forecast values for Forecasting the future GDP of British Columbia is illustrated

as below (Şen Doğan & Midiliç, 2018).

Reference

period

Gross domestic product at

market prices in Dollars

(Predicted Values)

LCL UCL

2018 262158 255011 269306

2019 267441 257333 277550

2020 272725 260344 285105

2021 278008 263712 292303

2022 283291 267308 299274

2023 288574 271066 306082

2024 293857 274946 312768

2025 299141 278924 319357

2026 304424 282981 325867

2027 309707 287104 332310

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Conclusions and Future Research

This project was successfully predicted, displayed the GDP forecast of British

Columbia future utilizing by using the ARIMA model. The predicted value analyzed by time

series method. The Auto Correlation Function (ACF) and Partial Auto Correlation Function

(PACF) are effectively calculated. Used the Proper Box-Jenkins Auto Regressive Integrated

Moving Average (ARIMA) successfully demonstrated the forecasting the future GDP of

British Columbia. Legitimacy of the model was effectively tested by using standard statistical

techniques. And, ARIMA model is used to display the forecasting zone and creation of

British Columbia for future years.

References

Camacho, M., & Martinez-Martin, J. (2013). Real-time forecasting US GDP from small-scale

factor models. Empirical Economics, 47(1), 347-364. doi: 10.1007/s00181-013-0731-4

Chun-Chu. (2011). Forecasting the Spanish Stock Market Returns with Fractional and Non-

Fractional Models. American Journal Of Economics And Business Administration, 3(4),

586-588. doi: 10.3844/ajebasp.2011.586.588

Dritsaki, D. (2015). Forecasting Real GDP Rate through Econometric Models: An Empirical

Study from Greece. Journal Of International Business And Economics, 3(1). doi:

10.15640/jibe.v3n1a2

Fildes, R., & Allen, P. (2011). Forecasting. Los Angeles, Calif.: SAGE.

11

This project was successfully predicted, displayed the GDP forecast of British

Columbia future utilizing by using the ARIMA model. The predicted value analyzed by time

series method. The Auto Correlation Function (ACF) and Partial Auto Correlation Function

(PACF) are effectively calculated. Used the Proper Box-Jenkins Auto Regressive Integrated

Moving Average (ARIMA) successfully demonstrated the forecasting the future GDP of

British Columbia. Legitimacy of the model was effectively tested by using standard statistical

techniques. And, ARIMA model is used to display the forecasting zone and creation of

British Columbia for future years.

References

Camacho, M., & Martinez-Martin, J. (2013). Real-time forecasting US GDP from small-scale

factor models. Empirical Economics, 47(1), 347-364. doi: 10.1007/s00181-013-0731-4

Chun-Chu. (2011). Forecasting the Spanish Stock Market Returns with Fractional and Non-

Fractional Models. American Journal Of Economics And Business Administration, 3(4),

586-588. doi: 10.3844/ajebasp.2011.586.588

Dritsaki, D. (2015). Forecasting Real GDP Rate through Econometric Models: An Empirical

Study from Greece. Journal Of International Business And Economics, 3(1). doi:

10.15640/jibe.v3n1a2

Fildes, R., & Allen, P. (2011). Forecasting. Los Angeles, Calif.: SAGE.

11

Şen Doğan, B., & Midiliç, M. (2018). Forecasting Turkish real GDP growth in a data-rich

environment. Empirical Economics. doi: 10.1007/s00181-017-1357-8

12

environment. Empirical Economics. doi: 10.1007/s00181-017-1357-8

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.