Forecasting & Valuation: A Case Study of Cleanaway Report

VerifiedAdded on 2020/05/08

|16

|3556

|73

Report

AI Summary

This report presents a comprehensive case study of Cleanaway, focusing on financial forecasting and valuation. It begins with an introduction to the importance of these concepts in management decision-making and stock valuation. The report then details the forecasting process, including key assumptions and calculations for sales growth, asset turnover, profit margins, and various financial ratios. The core of the report involves applying and comparing four valuation models: Dividend Discount Model (DDM), Residual Income Model (RIM), Residual Operating Income Model (ROIM), and Free Cash Flow Model (FCF) to determine the company's stock price. The report also includes a sensitivity analysis using the Residual Operating Income Model and concludes with a recommendation on whether Cleanaway's stock is overvalued or undervalued based on the analysis. The detailed tables in the appendices support the calculations and assumptions presented throughout the report.

Running Head: Forecasting & Valuation: A Case Study Of Cleanaway

Student Name:

Forecasting & Valuation: A Case Study Of Cleanaway

Institute name:

Affiliation:

1

Student Name:

Forecasting & Valuation: A Case Study Of Cleanaway

Institute name:

Affiliation:

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Running Head: Forecasting & Valuation: A Case Study Of Cleanaway

Table of Contents

1.0 Introduction................................................................................................................................3

2.0 Forecasting:................................................................................................................................4

2.1 Forecasting: An Overview.....................................................................................................4

2.2 Sales Growth..........................................................................................................................4

2.3 Asset Turnover Ratio (ATO).................................................................................................5

2.4 Profit Margin..........................................................................................................................5

2.5 Net Dividend Payout Ratio....................................................................................................5

2.6 Cost of Debt...........................................................................................................................5

2.7 Cost of Equity........................................................................................................................6

2.8 Free Cash Flow (FCF)............................................................................................................6

3.0 Valuation:..................................................................................................................................7

3.1 Valuation: An Overview........................................................................................................7

3.2 Dividend Discount Model (DDM).........................................................................................7

3.3 Residual Income Model (RIM)..............................................................................................8

3.4 Residual Operating Income Model (ROIM)..........................................................................8

3.5 Free Cash Flow Model (FCF)................................................................................................9

3.6 Sensitivity Analysis: Residual Operating Income Model....................................................10

3.7 Recommendation.................................................................................................................10

4.0 Conclusion...............................................................................................................................11

References......................................................................................................................................12

Appendices....................................................................................................................................13

2

Table of Contents

1.0 Introduction................................................................................................................................3

2.0 Forecasting:................................................................................................................................4

2.1 Forecasting: An Overview.....................................................................................................4

2.2 Sales Growth..........................................................................................................................4

2.3 Asset Turnover Ratio (ATO).................................................................................................5

2.4 Profit Margin..........................................................................................................................5

2.5 Net Dividend Payout Ratio....................................................................................................5

2.6 Cost of Debt...........................................................................................................................5

2.7 Cost of Equity........................................................................................................................6

2.8 Free Cash Flow (FCF)............................................................................................................6

3.0 Valuation:..................................................................................................................................7

3.1 Valuation: An Overview........................................................................................................7

3.2 Dividend Discount Model (DDM).........................................................................................7

3.3 Residual Income Model (RIM)..............................................................................................8

3.4 Residual Operating Income Model (ROIM)..........................................................................8

3.5 Free Cash Flow Model (FCF)................................................................................................9

3.6 Sensitivity Analysis: Residual Operating Income Model....................................................10

3.7 Recommendation.................................................................................................................10

4.0 Conclusion...............................................................................................................................11

References......................................................................................................................................12

Appendices....................................................................................................................................13

2

Running Head: Forecasting & Valuation: A Case Study Of Cleanaway

1.0 Introduction

Forecasting and valuation may be considered to be one of the most success critical roles and

responsibilities of management. Efficient and effective forecasting provides the management an

overview of future the financial performance of the business in terms of the projection and also

contributes towards understanding a fair valuation of the stock of the firm floating in the market

(Damodaran, 2016). Based on the valuation, the management may get an idea about the stock

performance n the market and accordingly take the strategic decisions such as divestment, share

issue, acquisition and corporate investment etc. The instant report deals with one of such case

study of Cleanaway where the revenue and profit has been forecasted for next five years based

on various parameters and assumptions. The report presents the brief discussion on those

presumptive elements and provides an estimated revenue projection for next five years. In the

next part of the study, the report attempts to value the stock of the firm applying different

valuation models. In addition, the report also presents a concise sensitivity analysis on valuation

and finally recommends as to whether the stock of the firm is overvalued or undervalued. At the

last, the researcher wraps up the discussion by way of concluding note.

3

1.0 Introduction

Forecasting and valuation may be considered to be one of the most success critical roles and

responsibilities of management. Efficient and effective forecasting provides the management an

overview of future the financial performance of the business in terms of the projection and also

contributes towards understanding a fair valuation of the stock of the firm floating in the market

(Damodaran, 2016). Based on the valuation, the management may get an idea about the stock

performance n the market and accordingly take the strategic decisions such as divestment, share

issue, acquisition and corporate investment etc. The instant report deals with one of such case

study of Cleanaway where the revenue and profit has been forecasted for next five years based

on various parameters and assumptions. The report presents the brief discussion on those

presumptive elements and provides an estimated revenue projection for next five years. In the

next part of the study, the report attempts to value the stock of the firm applying different

valuation models. In addition, the report also presents a concise sensitivity analysis on valuation

and finally recommends as to whether the stock of the firm is overvalued or undervalued. At the

last, the researcher wraps up the discussion by way of concluding note.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Running Head: Forecasting & Valuation: A Case Study Of Cleanaway

2.0 Forecasting:

2.1 Forecasting: An Overview

Forecasting is a process by which the historical data is used to identify the future trends. In the

business context, the process of forecasting includes the collection of past data related to revenue

or profit or any other key performance indicators (KPIs) of the business and recognize the inbuilt

trend in those data set to visualize the future data. Forecasting process employs several financial

tools for the purpose of such estimation. As a result, the forecasting and trend analysis may be

construed to be similar at times (Yermack, 1996). It is interesting to note that the forecasting

requires a lot of assumptions and the accuracy of prediction largely depends on relevance and

logic behind those assumptions. The subsequent sections of the report discuss about the various

assumptions behind the process of forecasting for Cleanaway.

Trend analysis may be defined to be dependent on the simple formula of change in the figures as

compared to previous period. For example, if the revenue is AUD 100 million in FY 2015 and

the same for FY 2016 is AUD 120 million, then the growth in revenue may be calculated to 20%

(i.e. excess of figures for FY 2016 over FY 2015, with reference to the figure for FY 2015).

Trend=Current yea r' s data – Previous yea r' s data

Previous yea r' s data

Based on such simple formula, trend for all the below mentioned parameters have been

calculated in the instant case study. In the case of multiple reporting periods, an average of all

trend percentage may be considered to be overall growth rate.

2.2 Sales Growth

As discussed previously, the sales growth has been calculated using the aforementioned formula.

The tables in appendices show the calculation in details. Sales growth may be construed to be the

combined effect of marketing strategy of the firm and market linked factors such as inflation,

national economy and also various externalities. In the given case, the average growth rate in

revenue is computed to be less than 1 %. This is because of the reason that the firm has

4

2.0 Forecasting:

2.1 Forecasting: An Overview

Forecasting is a process by which the historical data is used to identify the future trends. In the

business context, the process of forecasting includes the collection of past data related to revenue

or profit or any other key performance indicators (KPIs) of the business and recognize the inbuilt

trend in those data set to visualize the future data. Forecasting process employs several financial

tools for the purpose of such estimation. As a result, the forecasting and trend analysis may be

construed to be similar at times (Yermack, 1996). It is interesting to note that the forecasting

requires a lot of assumptions and the accuracy of prediction largely depends on relevance and

logic behind those assumptions. The subsequent sections of the report discuss about the various

assumptions behind the process of forecasting for Cleanaway.

Trend analysis may be defined to be dependent on the simple formula of change in the figures as

compared to previous period. For example, if the revenue is AUD 100 million in FY 2015 and

the same for FY 2016 is AUD 120 million, then the growth in revenue may be calculated to 20%

(i.e. excess of figures for FY 2016 over FY 2015, with reference to the figure for FY 2015).

Trend=Current yea r' s data – Previous yea r' s data

Previous yea r' s data

Based on such simple formula, trend for all the below mentioned parameters have been

calculated in the instant case study. In the case of multiple reporting periods, an average of all

trend percentage may be considered to be overall growth rate.

2.2 Sales Growth

As discussed previously, the sales growth has been calculated using the aforementioned formula.

The tables in appendices show the calculation in details. Sales growth may be construed to be the

combined effect of marketing strategy of the firm and market linked factors such as inflation,

national economy and also various externalities. In the given case, the average growth rate in

revenue is computed to be less than 1 %. This is because of the reason that the firm has

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Running Head: Forecasting & Valuation: A Case Study Of Cleanaway

witnessed the fluctuations in the sales figure in last few years. As a result, the top line has not

been able to provide any specific growth trends and averaged to be 0.82% approximately.

2.3 Asset Turnover Ratio (ATO)

Assets Turnover Ratio (ATO) may be defined to be the ratio that defines the capacity of asset

base of the firm to generate revenue. As the ratio suggests, ATO signifies the ability of per unit

assets to generate revenue (Koceska and Koceski, 2014). Therefore, an ATO of more than 1

denotes an efficient asset base of the company and vice versa. In the given scenario, ATO has

been computed with reference to the provided figures for past few years and computed to be

63.4% on an average. In this context, it may be noted that assets here mean the net operating

assets and revenue includes other income also. Since the Cleanaway has ATO of less than 1, it

may be asserted that the management has not been able to utilize the asset base effectively to

produce more sales for the business,

2.4 Profit Margin

Profit margin may be computed with reference to the gross profit, operating profit or net profit

after tax. Since the intention of the entire paper is to create a forecasting and valuation based on

such prediction, the after-tax figure may be considered as the same has direct bearing with the

various valuation models used for the intended purpose (Palepu et al. 2013). However, non-

operating items may be deducted to arrive at the net operating profit after tax (NOPAT). Average

margin, based on NOPAT, may be calculated to be at around 5.8% during last five years.

2.5 Net Dividend Payout Ratio

Net dividend payout ratio may be defined to be the ratio of dividend paid and total earnings

available to equity shareholders. In the instant case, the ratio suggests the proportion of EPS that

has been paid out as dividend. Since the payment of dividend is not a charge against profit but

appropriation of profit, dividend payout has significant implication on the share valuation for the

company (Richard, 2014). This is because of the fact that the dividend payout ratio will show the

strategy of the firm to satisfy the financial needs of the shareholders by way of paying dividends

and thus retaining rest portion of the EPS for the expansion and growth of the firm. Since the

stock price largely depends on the dividend announcement and lots of other market linked

factors, dividend payout may have considerable influence on the valuation process of the firm.

5

witnessed the fluctuations in the sales figure in last few years. As a result, the top line has not

been able to provide any specific growth trends and averaged to be 0.82% approximately.

2.3 Asset Turnover Ratio (ATO)

Assets Turnover Ratio (ATO) may be defined to be the ratio that defines the capacity of asset

base of the firm to generate revenue. As the ratio suggests, ATO signifies the ability of per unit

assets to generate revenue (Koceska and Koceski, 2014). Therefore, an ATO of more than 1

denotes an efficient asset base of the company and vice versa. In the given scenario, ATO has

been computed with reference to the provided figures for past few years and computed to be

63.4% on an average. In this context, it may be noted that assets here mean the net operating

assets and revenue includes other income also. Since the Cleanaway has ATO of less than 1, it

may be asserted that the management has not been able to utilize the asset base effectively to

produce more sales for the business,

2.4 Profit Margin

Profit margin may be computed with reference to the gross profit, operating profit or net profit

after tax. Since the intention of the entire paper is to create a forecasting and valuation based on

such prediction, the after-tax figure may be considered as the same has direct bearing with the

various valuation models used for the intended purpose (Palepu et al. 2013). However, non-

operating items may be deducted to arrive at the net operating profit after tax (NOPAT). Average

margin, based on NOPAT, may be calculated to be at around 5.8% during last five years.

2.5 Net Dividend Payout Ratio

Net dividend payout ratio may be defined to be the ratio of dividend paid and total earnings

available to equity shareholders. In the instant case, the ratio suggests the proportion of EPS that

has been paid out as dividend. Since the payment of dividend is not a charge against profit but

appropriation of profit, dividend payout has significant implication on the share valuation for the

company (Richard, 2014). This is because of the fact that the dividend payout ratio will show the

strategy of the firm to satisfy the financial needs of the shareholders by way of paying dividends

and thus retaining rest portion of the EPS for the expansion and growth of the firm. Since the

stock price largely depends on the dividend announcement and lots of other market linked

factors, dividend payout may have considerable influence on the valuation process of the firm.

5

Running Head: Forecasting & Valuation: A Case Study Of Cleanaway

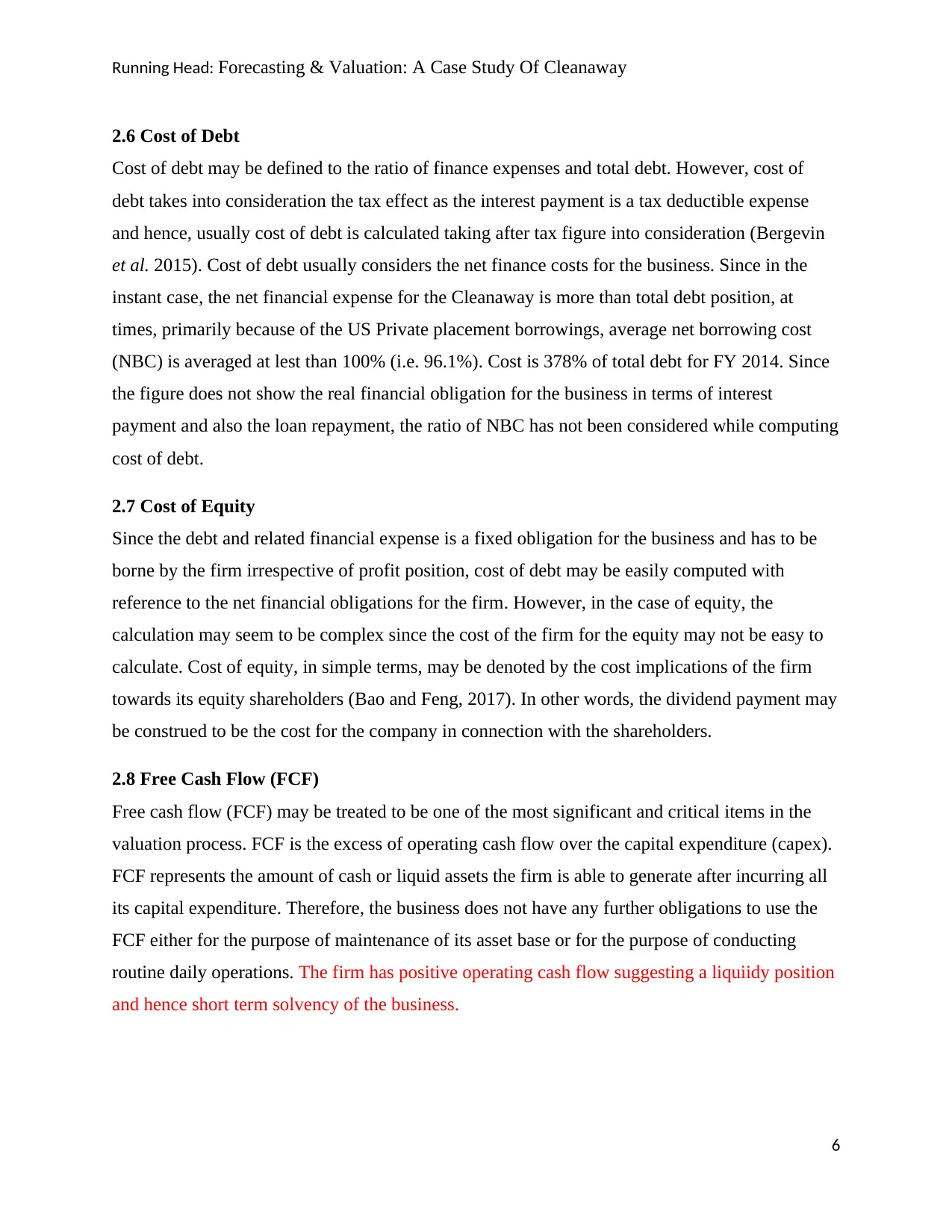

2.6 Cost of Debt

Cost of debt may be defined to the ratio of finance expenses and total debt. However, cost of

debt takes into consideration the tax effect as the interest payment is a tax deductible expense

and hence, usually cost of debt is calculated taking after tax figure into consideration (Bergevin

et al. 2015). Cost of debt usually considers the net finance costs for the business. Since in the

instant case, the net financial expense for the Cleanaway is more than total debt position, at

times, primarily because of the US Private placement borrowings, average net borrowing cost

(NBC) is averaged at lest than 100% (i.e. 96.1%). Cost is 378% of total debt for FY 2014. Since

the figure does not show the real financial obligation for the business in terms of interest

payment and also the loan repayment, the ratio of NBC has not been considered while computing

cost of debt.

2.7 Cost of Equity

Since the debt and related financial expense is a fixed obligation for the business and has to be

borne by the firm irrespective of profit position, cost of debt may be easily computed with

reference to the net financial obligations for the firm. However, in the case of equity, the

calculation may seem to be complex since the cost of the firm for the equity may not be easy to

calculate. Cost of equity, in simple terms, may be denoted by the cost implications of the firm

towards its equity shareholders (Bao and Feng, 2017). In other words, the dividend payment may

be construed to be the cost for the company in connection with the shareholders.

2.8 Free Cash Flow (FCF)

Free cash flow (FCF) may be treated to be one of the most significant and critical items in the

valuation process. FCF is the excess of operating cash flow over the capital expenditure (capex).

FCF represents the amount of cash or liquid assets the firm is able to generate after incurring all

its capital expenditure. Therefore, the business does not have any further obligations to use the

FCF either for the purpose of maintenance of its asset base or for the purpose of conducting

routine daily operations. The firm has positive operating cash flow suggesting a liquiidy position

and hence short term solvency of the business.

6

2.6 Cost of Debt

Cost of debt may be defined to the ratio of finance expenses and total debt. However, cost of

debt takes into consideration the tax effect as the interest payment is a tax deductible expense

and hence, usually cost of debt is calculated taking after tax figure into consideration (Bergevin

et al. 2015). Cost of debt usually considers the net finance costs for the business. Since in the

instant case, the net financial expense for the Cleanaway is more than total debt position, at

times, primarily because of the US Private placement borrowings, average net borrowing cost

(NBC) is averaged at lest than 100% (i.e. 96.1%). Cost is 378% of total debt for FY 2014. Since

the figure does not show the real financial obligation for the business in terms of interest

payment and also the loan repayment, the ratio of NBC has not been considered while computing

cost of debt.

2.7 Cost of Equity

Since the debt and related financial expense is a fixed obligation for the business and has to be

borne by the firm irrespective of profit position, cost of debt may be easily computed with

reference to the net financial obligations for the firm. However, in the case of equity, the

calculation may seem to be complex since the cost of the firm for the equity may not be easy to

calculate. Cost of equity, in simple terms, may be denoted by the cost implications of the firm

towards its equity shareholders (Bao and Feng, 2017). In other words, the dividend payment may

be construed to be the cost for the company in connection with the shareholders.

2.8 Free Cash Flow (FCF)

Free cash flow (FCF) may be treated to be one of the most significant and critical items in the

valuation process. FCF is the excess of operating cash flow over the capital expenditure (capex).

FCF represents the amount of cash or liquid assets the firm is able to generate after incurring all

its capital expenditure. Therefore, the business does not have any further obligations to use the

FCF either for the purpose of maintenance of its asset base or for the purpose of conducting

routine daily operations. The firm has positive operating cash flow suggesting a liquiidy position

and hence short term solvency of the business.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Running Head: Forecasting & Valuation: A Case Study Of Cleanaway

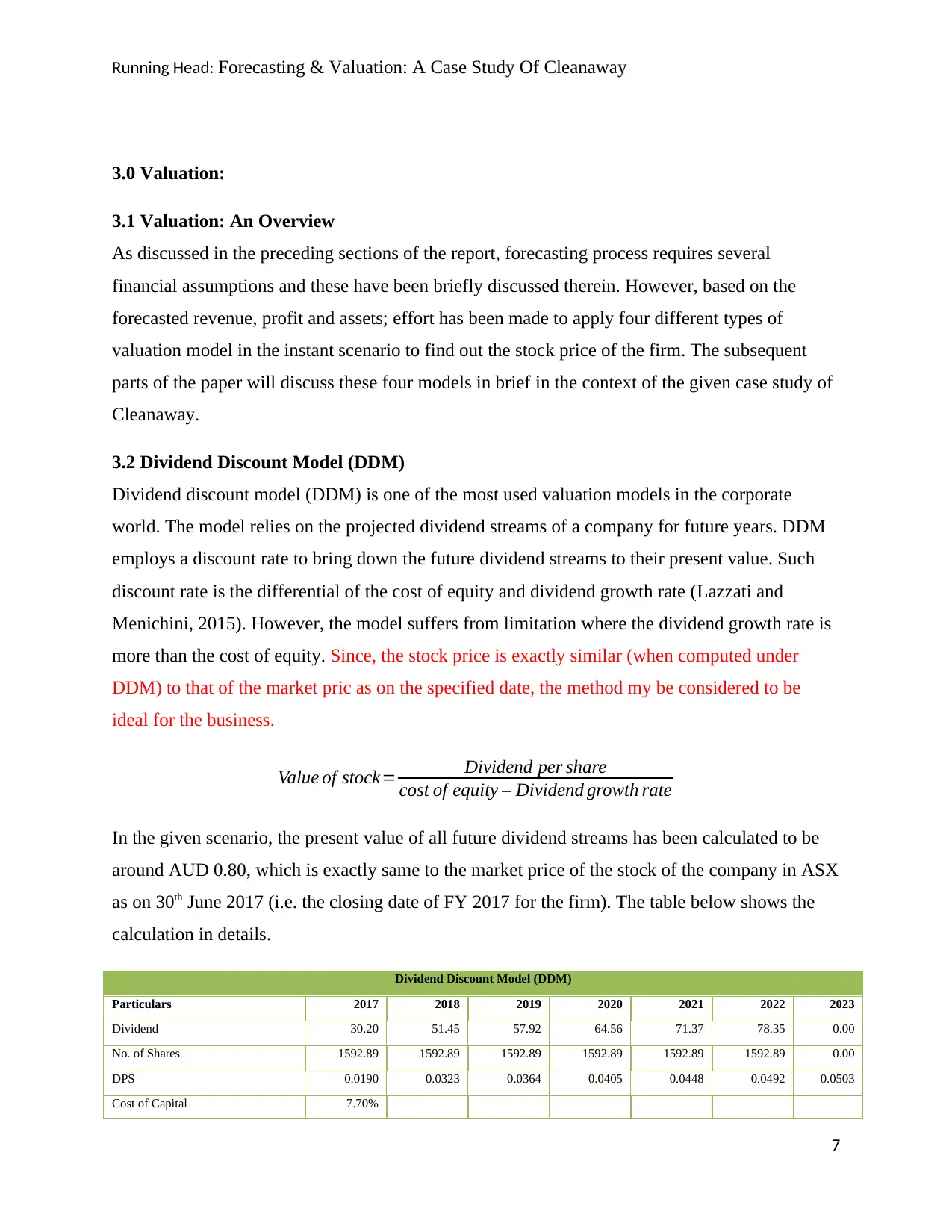

3.0 Valuation:

3.1 Valuation: An Overview

As discussed in the preceding sections of the report, forecasting process requires several

financial assumptions and these have been briefly discussed therein. However, based on the

forecasted revenue, profit and assets; effort has been made to apply four different types of

valuation model in the instant scenario to find out the stock price of the firm. The subsequent

parts of the paper will discuss these four models in brief in the context of the given case study of

Cleanaway.

3.2 Dividend Discount Model (DDM)

Dividend discount model (DDM) is one of the most used valuation models in the corporate

world. The model relies on the projected dividend streams of a company for future years. DDM

employs a discount rate to bring down the future dividend streams to their present value. Such

discount rate is the differential of the cost of equity and dividend growth rate (Lazzati and

Menichini, 2015). However, the model suffers from limitation where the dividend growth rate is

more than the cost of equity. Since, the stock price is exactly similar (when computed under

DDM) to that of the market pric as on the specified date, the method my be considered to be

ideal for the business.

Value of stock= Dividend per share

cost of equity – Dividend growth rate

In the given scenario, the present value of all future dividend streams has been calculated to be

around AUD 0.80, which is exactly same to the market price of the stock of the company in ASX

as on 30th June 2017 (i.e. the closing date of FY 2017 for the firm). The table below shows the

calculation in details.

Dividend Discount Model (DDM)

Particulars 2017 2018 2019 2020 2021 2022 2023

Dividend 30.20 51.45 57.92 64.56 71.37 78.35 0.00

No. of Shares 1592.89 1592.89 1592.89 1592.89 1592.89 1592.89 0.00

DPS 0.0190 0.0323 0.0364 0.0405 0.0448 0.0492 0.0503

Cost of Capital 7.70%

7

3.0 Valuation:

3.1 Valuation: An Overview

As discussed in the preceding sections of the report, forecasting process requires several

financial assumptions and these have been briefly discussed therein. However, based on the

forecasted revenue, profit and assets; effort has been made to apply four different types of

valuation model in the instant scenario to find out the stock price of the firm. The subsequent

parts of the paper will discuss these four models in brief in the context of the given case study of

Cleanaway.

3.2 Dividend Discount Model (DDM)

Dividend discount model (DDM) is one of the most used valuation models in the corporate

world. The model relies on the projected dividend streams of a company for future years. DDM

employs a discount rate to bring down the future dividend streams to their present value. Such

discount rate is the differential of the cost of equity and dividend growth rate (Lazzati and

Menichini, 2015). However, the model suffers from limitation where the dividend growth rate is

more than the cost of equity. Since, the stock price is exactly similar (when computed under

DDM) to that of the market pric as on the specified date, the method my be considered to be

ideal for the business.

Value of stock= Dividend per share

cost of equity – Dividend growth rate

In the given scenario, the present value of all future dividend streams has been calculated to be

around AUD 0.80, which is exactly same to the market price of the stock of the company in ASX

as on 30th June 2017 (i.e. the closing date of FY 2017 for the firm). The table below shows the

calculation in details.

Dividend Discount Model (DDM)

Particulars 2017 2018 2019 2020 2021 2022 2023

Dividend 30.20 51.45 57.92 64.56 71.37 78.35 0.00

No. of Shares 1592.89 1592.89 1592.89 1592.89 1592.89 1592.89 0.00

DPS 0.0190 0.0323 0.0364 0.0405 0.0448 0.0492 0.0503

Cost of Capital 7.70%

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Running Head: Forecasting & Valuation: A Case Study Of Cleanaway

Terminal growth rate 2.25%

Dividend Forecast 0.16

Terminal Value 0.64

Share Price 0.80

Table 1: Share Valuation of Cleanaway under Dividend Discount Model (DDM)

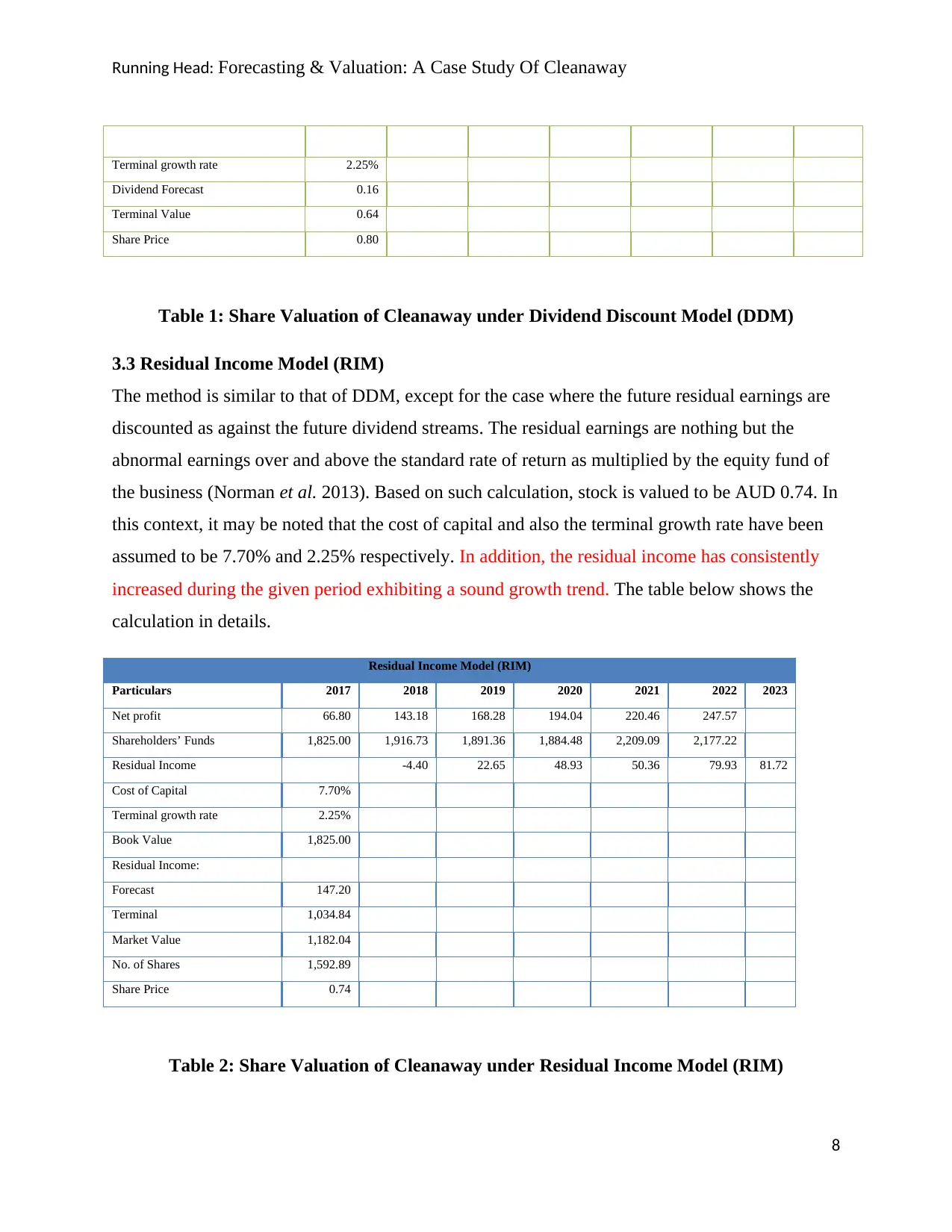

3.3 Residual Income Model (RIM)

The method is similar to that of DDM, except for the case where the future residual earnings are

discounted as against the future dividend streams. The residual earnings are nothing but the

abnormal earnings over and above the standard rate of return as multiplied by the equity fund of

the business (Norman et al. 2013). Based on such calculation, stock is valued to be AUD 0.74. In

this context, it may be noted that the cost of capital and also the terminal growth rate have been

assumed to be 7.70% and 2.25% respectively. In addition, the residual income has consistently

increased during the given period exhibiting a sound growth trend. The table below shows the

calculation in details.

Residual Income Model (RIM)

Particulars 2017 2018 2019 2020 2021 2022 2023

Net profit 66.80 143.18 168.28 194.04 220.46 247.57

Shareholders’ Funds 1,825.00 1,916.73 1,891.36 1,884.48 2,209.09 2,177.22

Residual Income -4.40 22.65 48.93 50.36 79.93 81.72

Cost of Capital 7.70%

Terminal growth rate 2.25%

Book Value 1,825.00

Residual Income:

Forecast 147.20

Terminal 1,034.84

Market Value 1,182.04

No. of Shares 1,592.89

Share Price 0.74

Table 2: Share Valuation of Cleanaway under Residual Income Model (RIM)

8

Terminal growth rate 2.25%

Dividend Forecast 0.16

Terminal Value 0.64

Share Price 0.80

Table 1: Share Valuation of Cleanaway under Dividend Discount Model (DDM)

3.3 Residual Income Model (RIM)

The method is similar to that of DDM, except for the case where the future residual earnings are

discounted as against the future dividend streams. The residual earnings are nothing but the

abnormal earnings over and above the standard rate of return as multiplied by the equity fund of

the business (Norman et al. 2013). Based on such calculation, stock is valued to be AUD 0.74. In

this context, it may be noted that the cost of capital and also the terminal growth rate have been

assumed to be 7.70% and 2.25% respectively. In addition, the residual income has consistently

increased during the given period exhibiting a sound growth trend. The table below shows the

calculation in details.

Residual Income Model (RIM)

Particulars 2017 2018 2019 2020 2021 2022 2023

Net profit 66.80 143.18 168.28 194.04 220.46 247.57

Shareholders’ Funds 1,825.00 1,916.73 1,891.36 1,884.48 2,209.09 2,177.22

Residual Income -4.40 22.65 48.93 50.36 79.93 81.72

Cost of Capital 7.70%

Terminal growth rate 2.25%

Book Value 1,825.00

Residual Income:

Forecast 147.20

Terminal 1,034.84

Market Value 1,182.04

No. of Shares 1,592.89

Share Price 0.74

Table 2: Share Valuation of Cleanaway under Residual Income Model (RIM)

8

Running Head: Forecasting & Valuation: A Case Study Of Cleanaway

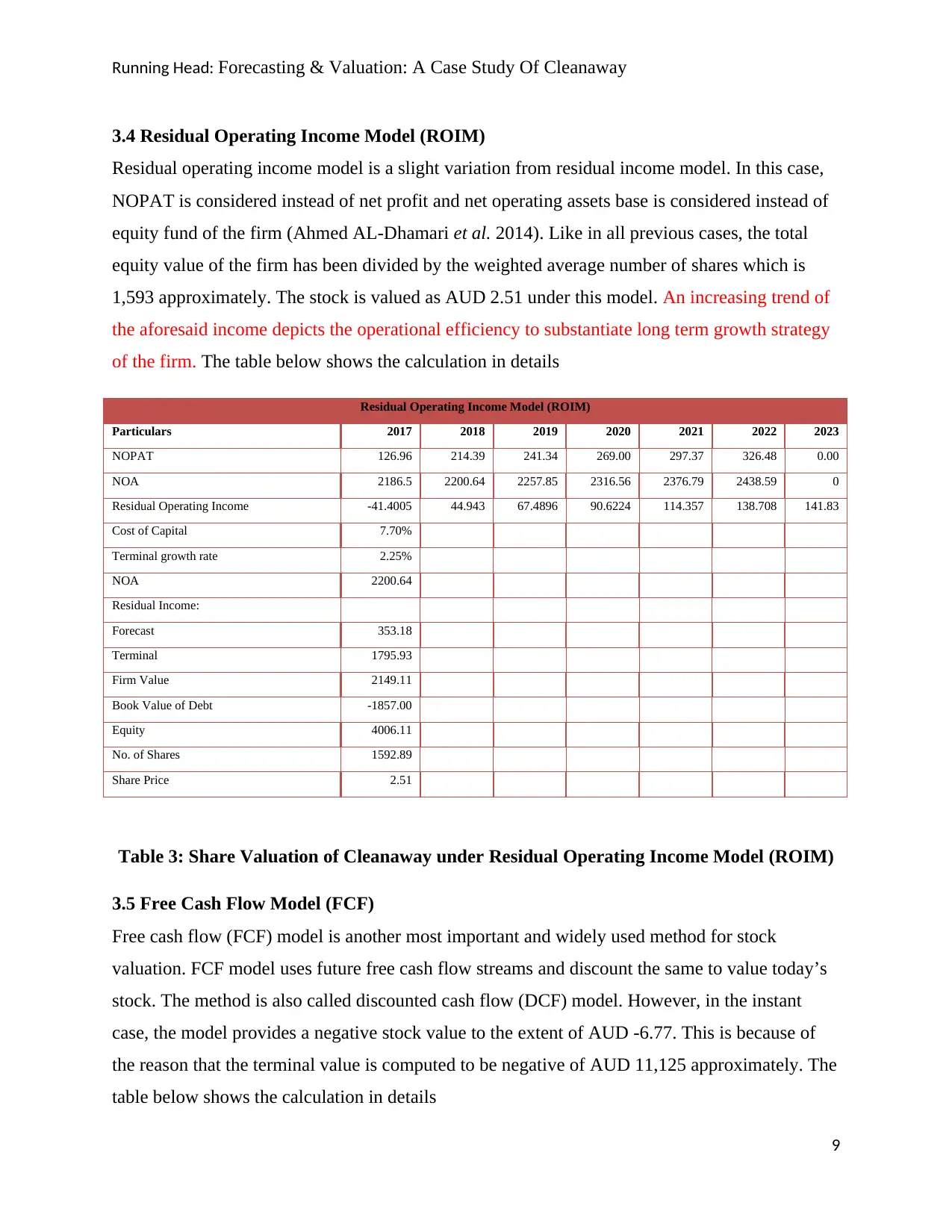

3.4 Residual Operating Income Model (ROIM)

Residual operating income model is a slight variation from residual income model. In this case,

NOPAT is considered instead of net profit and net operating assets base is considered instead of

equity fund of the firm (Ahmed AL-Dhamari et al. 2014). Like in all previous cases, the total

equity value of the firm has been divided by the weighted average number of shares which is

1,593 approximately. The stock is valued as AUD 2.51 under this model. An increasing trend of

the aforesaid income depicts the operational efficiency to substantiate long term growth strategy

of the firm. The table below shows the calculation in details

Residual Operating Income Model (ROIM)

Particulars 2017 2018 2019 2020 2021 2022 2023

NOPAT 126.96 214.39 241.34 269.00 297.37 326.48 0.00

NOA 2186.5 2200.64 2257.85 2316.56 2376.79 2438.59 0

Residual Operating Income -41.4005 44.943 67.4896 90.6224 114.357 138.708 141.83

Cost of Capital 7.70%

Terminal growth rate 2.25%

NOA 2200.64

Residual Income:

Forecast 353.18

Terminal 1795.93

Firm Value 2149.11

Book Value of Debt -1857.00

Equity 4006.11

No. of Shares 1592.89

Share Price 2.51

Table 3: Share Valuation of Cleanaway under Residual Operating Income Model (ROIM)

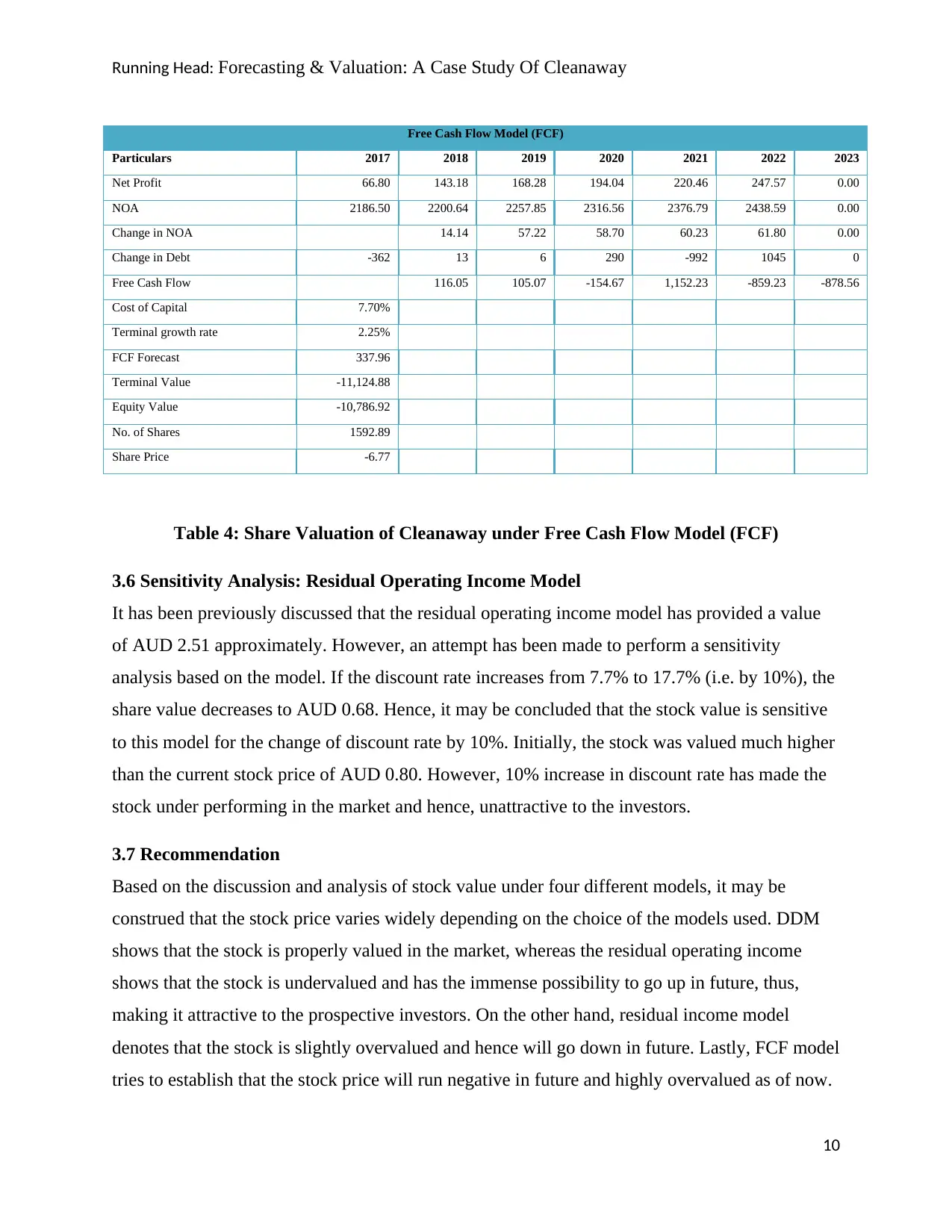

3.5 Free Cash Flow Model (FCF)

Free cash flow (FCF) model is another most important and widely used method for stock

valuation. FCF model uses future free cash flow streams and discount the same to value today’s

stock. The method is also called discounted cash flow (DCF) model. However, in the instant

case, the model provides a negative stock value to the extent of AUD -6.77. This is because of

the reason that the terminal value is computed to be negative of AUD 11,125 approximately. The

table below shows the calculation in details

9

3.4 Residual Operating Income Model (ROIM)

Residual operating income model is a slight variation from residual income model. In this case,

NOPAT is considered instead of net profit and net operating assets base is considered instead of

equity fund of the firm (Ahmed AL-Dhamari et al. 2014). Like in all previous cases, the total

equity value of the firm has been divided by the weighted average number of shares which is

1,593 approximately. The stock is valued as AUD 2.51 under this model. An increasing trend of

the aforesaid income depicts the operational efficiency to substantiate long term growth strategy

of the firm. The table below shows the calculation in details

Residual Operating Income Model (ROIM)

Particulars 2017 2018 2019 2020 2021 2022 2023

NOPAT 126.96 214.39 241.34 269.00 297.37 326.48 0.00

NOA 2186.5 2200.64 2257.85 2316.56 2376.79 2438.59 0

Residual Operating Income -41.4005 44.943 67.4896 90.6224 114.357 138.708 141.83

Cost of Capital 7.70%

Terminal growth rate 2.25%

NOA 2200.64

Residual Income:

Forecast 353.18

Terminal 1795.93

Firm Value 2149.11

Book Value of Debt -1857.00

Equity 4006.11

No. of Shares 1592.89

Share Price 2.51

Table 3: Share Valuation of Cleanaway under Residual Operating Income Model (ROIM)

3.5 Free Cash Flow Model (FCF)

Free cash flow (FCF) model is another most important and widely used method for stock

valuation. FCF model uses future free cash flow streams and discount the same to value today’s

stock. The method is also called discounted cash flow (DCF) model. However, in the instant

case, the model provides a negative stock value to the extent of AUD -6.77. This is because of

the reason that the terminal value is computed to be negative of AUD 11,125 approximately. The

table below shows the calculation in details

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Running Head: Forecasting & Valuation: A Case Study Of Cleanaway

Free Cash Flow Model (FCF)

Particulars 2017 2018 2019 2020 2021 2022 2023

Net Profit 66.80 143.18 168.28 194.04 220.46 247.57 0.00

NOA 2186.50 2200.64 2257.85 2316.56 2376.79 2438.59 0.00

Change in NOA 14.14 57.22 58.70 60.23 61.80 0.00

Change in Debt -362 13 6 290 -992 1045 0

Free Cash Flow 116.05 105.07 -154.67 1,152.23 -859.23 -878.56

Cost of Capital 7.70%

Terminal growth rate 2.25%

FCF Forecast 337.96

Terminal Value -11,124.88

Equity Value -10,786.92

No. of Shares 1592.89

Share Price -6.77

Table 4: Share Valuation of Cleanaway under Free Cash Flow Model (FCF)

3.6 Sensitivity Analysis: Residual Operating Income Model

It has been previously discussed that the residual operating income model has provided a value

of AUD 2.51 approximately. However, an attempt has been made to perform a sensitivity

analysis based on the model. If the discount rate increases from 7.7% to 17.7% (i.e. by 10%), the

share value decreases to AUD 0.68. Hence, it may be concluded that the stock value is sensitive

to this model for the change of discount rate by 10%. Initially, the stock was valued much higher

than the current stock price of AUD 0.80. However, 10% increase in discount rate has made the

stock under performing in the market and hence, unattractive to the investors.

3.7 Recommendation

Based on the discussion and analysis of stock value under four different models, it may be

construed that the stock price varies widely depending on the choice of the models used. DDM

shows that the stock is properly valued in the market, whereas the residual operating income

shows that the stock is undervalued and has the immense possibility to go up in future, thus,

making it attractive to the prospective investors. On the other hand, residual income model

denotes that the stock is slightly overvalued and hence will go down in future. Lastly, FCF model

tries to establish that the stock price will run negative in future and highly overvalued as of now.

10

Free Cash Flow Model (FCF)

Particulars 2017 2018 2019 2020 2021 2022 2023

Net Profit 66.80 143.18 168.28 194.04 220.46 247.57 0.00

NOA 2186.50 2200.64 2257.85 2316.56 2376.79 2438.59 0.00

Change in NOA 14.14 57.22 58.70 60.23 61.80 0.00

Change in Debt -362 13 6 290 -992 1045 0

Free Cash Flow 116.05 105.07 -154.67 1,152.23 -859.23 -878.56

Cost of Capital 7.70%

Terminal growth rate 2.25%

FCF Forecast 337.96

Terminal Value -11,124.88

Equity Value -10,786.92

No. of Shares 1592.89

Share Price -6.77

Table 4: Share Valuation of Cleanaway under Free Cash Flow Model (FCF)

3.6 Sensitivity Analysis: Residual Operating Income Model

It has been previously discussed that the residual operating income model has provided a value

of AUD 2.51 approximately. However, an attempt has been made to perform a sensitivity

analysis based on the model. If the discount rate increases from 7.7% to 17.7% (i.e. by 10%), the

share value decreases to AUD 0.68. Hence, it may be concluded that the stock value is sensitive

to this model for the change of discount rate by 10%. Initially, the stock was valued much higher

than the current stock price of AUD 0.80. However, 10% increase in discount rate has made the

stock under performing in the market and hence, unattractive to the investors.

3.7 Recommendation

Based on the discussion and analysis of stock value under four different models, it may be

construed that the stock price varies widely depending on the choice of the models used. DDM

shows that the stock is properly valued in the market, whereas the residual operating income

shows that the stock is undervalued and has the immense possibility to go up in future, thus,

making it attractive to the prospective investors. On the other hand, residual income model

denotes that the stock is slightly overvalued and hence will go down in future. Lastly, FCF model

tries to establish that the stock price will run negative in future and highly overvalued as of now.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Running Head: Forecasting & Valuation: A Case Study Of Cleanaway

Since the stock price cannot be negative, the value so derived under FCF model may be ignored

as not all the models are appropriate for all situations. Therefore, based on the results of rest

three models, the average price is calculated to be AUD 1.35, which is higher than the present

share price of AUD 0.80. In other words, it may be recommended that the share of the

Cleanaway is presently undervalued and the price of the share will increase in the near future.

Therefore, it may be advised to the prospective investors to buy the stock and present investors

to hold the same to get the benefit of dividend as well as capital appreciation.

4.0 Conclusion

From the detailed discussion, computation, analysis and recommendation, it may be observed

that the forecasting and valuation process is complex and involves lots of variables. It may not be

necessary that all the parameters and variables will be applicable to a given case, as explained

earlier. However, the management should be careful and vigilant enough to judiciously apply the

relevant theory and model into the practical situation to deduce and finalize the corporate

strategy. Finally, it may be concluded that the forecasting is futuristic and hence based on

uncertain factors and probability and the valuation is situational and market linked. Therefore,

the management should always plan accordingly to accommodate for alternative strategies.

11

Since the stock price cannot be negative, the value so derived under FCF model may be ignored

as not all the models are appropriate for all situations. Therefore, based on the results of rest

three models, the average price is calculated to be AUD 1.35, which is higher than the present

share price of AUD 0.80. In other words, it may be recommended that the share of the

Cleanaway is presently undervalued and the price of the share will increase in the near future.

Therefore, it may be advised to the prospective investors to buy the stock and present investors

to hold the same to get the benefit of dividend as well as capital appreciation.

4.0 Conclusion

From the detailed discussion, computation, analysis and recommendation, it may be observed

that the forecasting and valuation process is complex and involves lots of variables. It may not be

necessary that all the parameters and variables will be applicable to a given case, as explained

earlier. However, the management should be careful and vigilant enough to judiciously apply the

relevant theory and model into the practical situation to deduce and finalize the corporate

strategy. Finally, it may be concluded that the forecasting is futuristic and hence based on

uncertain factors and probability and the valuation is situational and market linked. Therefore,

the management should always plan accordingly to accommodate for alternative strategies.

11

Running Head: Forecasting & Valuation: A Case Study Of Cleanaway

References

Ahmed AL-Dhamari, R. and Nor Izah Ku Ismail, K., (2014). An investigation into the effect of

surplus free cash flow, corporate governance and firm size on earnings predictability.

nternational Journal of Accounting and Information Management, 22(2), pp.118-133.

Bao, G. and Feng, G., (2017). Testing the Dividend Discount Model in Housing Markets: the

Role of Risk. The Journal of Real Estate Finance and Economics, pp.1-25.

Bergevin, P., MacQueen, M. and Mitchell, L., (2015). Financial Statement Analysis: Content

and Context. BVT Publishing.

Damodaran, A., (2016). Damodaran on valuation: security analysis for investment and

corporate finance (Vol. 324). John Wiley & Sons.

Koceska, N. and Koceski, S., (2014). Financial-Economic Time Series Modeling and Prediction

Techniques–Review. Journal of Applied Economics and Business, 2(4), pp.28-33.

Lazzati, N. and Menichini, A.A., (2015). A dynamic approach to the dividend discount model.

Review of Pacific Basin Financial Markets and Policies, 18(03), p.1550018.

Norman, S., Schlaudraff, J., White, K. and Wills, D., (2013). Deriving the dividend discount

model in the intermediate microeconomics class. The Journal of Economic Education, 44(1),

pp.58-63.

Palepu, K.G., Healy, P.M. and Peek, E., (2013). Business analysis and valuation: IFRS edition.

Cengage Learning.

Richard, P., (2014). The Role of the Accounting Rate of Return in Financial Statement Analysis.

The Continuing Debate Over Depreciation, Capital and Income (RLE Accounting), 67(2), p.235.

Yermack, D., (1996). Higher market valuation of companies with a small board of directors.

Journal of financial economics, 40(2), pp.185-211.

12

References

Ahmed AL-Dhamari, R. and Nor Izah Ku Ismail, K., (2014). An investigation into the effect of

surplus free cash flow, corporate governance and firm size on earnings predictability.

nternational Journal of Accounting and Information Management, 22(2), pp.118-133.

Bao, G. and Feng, G., (2017). Testing the Dividend Discount Model in Housing Markets: the

Role of Risk. The Journal of Real Estate Finance and Economics, pp.1-25.

Bergevin, P., MacQueen, M. and Mitchell, L., (2015). Financial Statement Analysis: Content

and Context. BVT Publishing.

Damodaran, A., (2016). Damodaran on valuation: security analysis for investment and

corporate finance (Vol. 324). John Wiley & Sons.

Koceska, N. and Koceski, S., (2014). Financial-Economic Time Series Modeling and Prediction

Techniques–Review. Journal of Applied Economics and Business, 2(4), pp.28-33.

Lazzati, N. and Menichini, A.A., (2015). A dynamic approach to the dividend discount model.

Review of Pacific Basin Financial Markets and Policies, 18(03), p.1550018.

Norman, S., Schlaudraff, J., White, K. and Wills, D., (2013). Deriving the dividend discount

model in the intermediate microeconomics class. The Journal of Economic Education, 44(1),

pp.58-63.

Palepu, K.G., Healy, P.M. and Peek, E., (2013). Business analysis and valuation: IFRS edition.

Cengage Learning.

Richard, P., (2014). The Role of the Accounting Rate of Return in Financial Statement Analysis.

The Continuing Debate Over Depreciation, Capital and Income (RLE Accounting), 67(2), p.235.

Yermack, D., (1996). Higher market valuation of companies with a small board of directors.

Journal of financial economics, 40(2), pp.185-211.

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.