Foreign Exchange Risk Management Strategies for Xinjiang Company

VerifiedAdded on 2023/06/03

|12

|2521

|245

AI Summary

This article discusses the different risk management strategies for foreign exchange risk exposure and their justification for Xinjiang Company. It covers hedging through forward contracts, money market hedge, and option contracts. The article also includes calculations and analysis of the different strategies.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

FIN61104 INDIVIDUAL ASSIGNMENT

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

TABLE OF CONTENTS

Introduction......................................................................................................................................3

A and B) Risk management strategies and justification..................................................................3

C).....................................................................................................................................................7

(i)..................................................................................................................................................7

(ii)................................................................................................................................................8

D).....................................................................................................................................................9

(i)..................................................................................................................................................9

(ii)..............................................................................................................................................10

References......................................................................................................................................11

Introduction......................................................................................................................................3

A and B) Risk management strategies and justification..................................................................3

C).....................................................................................................................................................7

(i)..................................................................................................................................................7

(ii)................................................................................................................................................8

D).....................................................................................................................................................9

(i)..................................................................................................................................................9

(ii)..............................................................................................................................................10

References......................................................................................................................................11

INTRODUCTION

Foreign exchange risk exposure refers to the financial risk which arises due to the financial

transactions stated in the foreign currency, which is other than the domestic currency (Fleten et

al. 2015). Due to the high volatility in the currency rates, the profit of the investor is significantly

affected (Bettis, Bizjak and Kalpathy, 2015). There are three types of foreign risk exposure such

as transaction exposure, operating exposure and translation exposure (Islam, and Chakraborti,

2015). However through the effective manner of the hedging, the foreign exchange risk can be

mitigated to some extent, some hedging techniques are described below-

1. To hedge with by entering into the forward contract

2. Hedging the risk by money market hedging

3. By entering into the option contract (Bhatia, and Bhat,2016)

In the present study, Xinjiang company which is China-based will receive the amount of $ 50

million in future by entering into the deal in June 2017. On the basis of the terms of the deal,

50% of the amount will receive in December 2017 and another 50% in June 2018. The company

has foreign exchange risk exposure due to the changing in the foreign currency rates. And if the

value of the dollar will decrease, then there is a chance of the loss to the company. Therefore the

company wants to hedge the foreign currency risk exposure. Through the following method, the

company can hedge the risk.

A AND B) RISK MANAGEMENT STRATEGIES AND JUSTIFICATION

Through the forward contract

Foreign exchange risk exposure refers to the financial risk which arises due to the financial

transactions stated in the foreign currency, which is other than the domestic currency (Fleten et

al. 2015). Due to the high volatility in the currency rates, the profit of the investor is significantly

affected (Bettis, Bizjak and Kalpathy, 2015). There are three types of foreign risk exposure such

as transaction exposure, operating exposure and translation exposure (Islam, and Chakraborti,

2015). However through the effective manner of the hedging, the foreign exchange risk can be

mitigated to some extent, some hedging techniques are described below-

1. To hedge with by entering into the forward contract

2. Hedging the risk by money market hedging

3. By entering into the option contract (Bhatia, and Bhat,2016)

In the present study, Xinjiang company which is China-based will receive the amount of $ 50

million in future by entering into the deal in June 2017. On the basis of the terms of the deal,

50% of the amount will receive in December 2017 and another 50% in June 2018. The company

has foreign exchange risk exposure due to the changing in the foreign currency rates. And if the

value of the dollar will decrease, then there is a chance of the loss to the company. Therefore the

company wants to hedge the foreign currency risk exposure. Through the following method, the

company can hedge the risk.

A AND B) RISK MANAGEMENT STRATEGIES AND JUSTIFICATION

Through the forward contract

If the company wants to cover its risk exposure through the forward contract, then the company

will sale $ 25 Million forward contracts today at the 180 days forward rate and remaining $25

million forward contracts today at 360 days forward rate.

The 180-days forward rate= 1 $= CNY 6.62335

In 180 days company will receive $ 25 Million and sale this $ at the CNY 6.62335 and receive

the CNY 165.584 M.

The 360-days forward rate= 1 $= CNY 6.22755

In 180 days company will receive $ 25 Million and sale this $ at the CNY 6.22755 and receive

the CNY 155.689 M.

The amount computed above is certain. In the future, the amount will not be impacted by any

volatility in the foreign exchange risk.

Through money market hedge

In the money market hedge technique, the company can hedge the amount by borrowing which is

equal to the present value of the amount of foreign currency, and after this, the borrowed amount

converted into the domestic currency through the spot rate. The amount will be invested into the

domestic currency, and the amount received in the maturity will be along with the interest rate.

Hedging of the amount which will be received in December 2017

Step 1. Borrow the $ 25 Million at the rate prevailing in the US that is at 4%. The present value

of the borrowed amount = $ 25 Million/1.04= $ 24.038 M.

So, the company will borrow the $ 24.038 M today and repay the amount with interest

will sale $ 25 Million forward contracts today at the 180 days forward rate and remaining $25

million forward contracts today at 360 days forward rate.

The 180-days forward rate= 1 $= CNY 6.62335

In 180 days company will receive $ 25 Million and sale this $ at the CNY 6.62335 and receive

the CNY 165.584 M.

The 360-days forward rate= 1 $= CNY 6.22755

In 180 days company will receive $ 25 Million and sale this $ at the CNY 6.22755 and receive

the CNY 155.689 M.

The amount computed above is certain. In the future, the amount will not be impacted by any

volatility in the foreign exchange risk.

Through money market hedge

In the money market hedge technique, the company can hedge the amount by borrowing which is

equal to the present value of the amount of foreign currency, and after this, the borrowed amount

converted into the domestic currency through the spot rate. The amount will be invested into the

domestic currency, and the amount received in the maturity will be along with the interest rate.

Hedging of the amount which will be received in December 2017

Step 1. Borrow the $ 25 Million at the rate prevailing in the US that is at 4%. The present value

of the borrowed amount = $ 25 Million/1.04= $ 24.038 M.

So, the company will borrow the $ 24.038 M today and repay the amount with interest

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Step 2. Convert the borrowed sum in the domestic currency of the company by applying the spot

rate

Spot rate= 1 $ =CNY 6.72475

= $24.038 Million*CNY 6.72475 = CNY 161.649 M

Step 3. The above sum invested in the domestic currency and the interest will be received at the

investing rate prevailing in China. The future value of the amount will be

= CNY 161.649*1.02452

= CNY 165.613 M

Hedging of the amount which will receive in December 2017

Step 1. Borrow the $ 25 Million at the borrowing rate prevailing in the US that is at 4.255%. The

present value of the borrowed amount = $ 25 Million/1.04255= $ 23.980 M.

So, the company will borrow the $ 23.980 M today and repay the amount with interest

Step 2. Convert the borrowed sum in the domestic currency of the company by applying the spot

rate

Spot rate= 1 $ =CNY 6.72475

= $23.980 Million*CNY 6.72475 = CNY 161.260 M

Step 3. The above sum invested in the domestic currency and the interest will be received at the

investing rate prevailing in China. The future value of the amount will be

= CNY 161.260*1.02225

rate

Spot rate= 1 $ =CNY 6.72475

= $24.038 Million*CNY 6.72475 = CNY 161.649 M

Step 3. The above sum invested in the domestic currency and the interest will be received at the

investing rate prevailing in China. The future value of the amount will be

= CNY 161.649*1.02452

= CNY 165.613 M

Hedging of the amount which will receive in December 2017

Step 1. Borrow the $ 25 Million at the borrowing rate prevailing in the US that is at 4.255%. The

present value of the borrowed amount = $ 25 Million/1.04255= $ 23.980 M.

So, the company will borrow the $ 23.980 M today and repay the amount with interest

Step 2. Convert the borrowed sum in the domestic currency of the company by applying the spot

rate

Spot rate= 1 $ =CNY 6.72475

= $23.980 Million*CNY 6.72475 = CNY 161.260 M

Step 3. The above sum invested in the domestic currency and the interest will be received at the

investing rate prevailing in China. The future value of the amount will be

= CNY 161.260*1.02225

= CNY 164.848 M

It has been assumed that the interest rate which was given in the question, the low-interest rate

reflects the borrowing interest rate and the high-interest rate reflect the investing rate.

Hedging through the option market

The company can cover the risk by buying the put option on $.

The company can purchase the 180 days put option on $ at a strike price of CNY 6.650/$ and a

premium of CNY .05/$. The cost of premium would be $25*.05= CNY 1.25 M.

The company is required to borrow this money at a borrowing rate prevailing in the china that is

2.323%. The total amount of borrowing = 1.25*1.02323 = CNY 1.279 M

The realisation by selling the $ at a strike price = 25*6.650= CNY 166.25 M

The net realisation to the company= 166.25-1.279 = CNY 164.971 M

Along with the above part, the company can purchase the 360 days put option on $ at a strike

price of CNY 6.250/$ and a premium of CNY .04/$. The cost of premium would be $25*.04=

CNY 1 M

The company is required to borrow this money at a borrowing rate prevailing in the china that is

2.323%. The total amount of borrowing = 1*1.02001 = CNY 1.02001 M

The realisation by selling the $ at a strike price = 25*6.250= CNY 156.25 M

The net realisation to the company= 156.25-1.02001 = CNY 155.23 M

It has been assumed that the interest rate which was given in the question, the low-interest rate

reflects the borrowing interest rate and the high-interest rate reflect the investing rate.

Hedging through the option market

The company can cover the risk by buying the put option on $.

The company can purchase the 180 days put option on $ at a strike price of CNY 6.650/$ and a

premium of CNY .05/$. The cost of premium would be $25*.05= CNY 1.25 M.

The company is required to borrow this money at a borrowing rate prevailing in the china that is

2.323%. The total amount of borrowing = 1.25*1.02323 = CNY 1.279 M

The realisation by selling the $ at a strike price = 25*6.650= CNY 166.25 M

The net realisation to the company= 166.25-1.279 = CNY 164.971 M

Along with the above part, the company can purchase the 360 days put option on $ at a strike

price of CNY 6.250/$ and a premium of CNY .04/$. The cost of premium would be $25*.04=

CNY 1 M

The company is required to borrow this money at a borrowing rate prevailing in the china that is

2.323%. The total amount of borrowing = 1*1.02001 = CNY 1.02001 M

The realisation by selling the $ at a strike price = 25*6.250= CNY 156.25 M

The net realisation to the company= 156.25-1.02001 = CNY 155.23 M

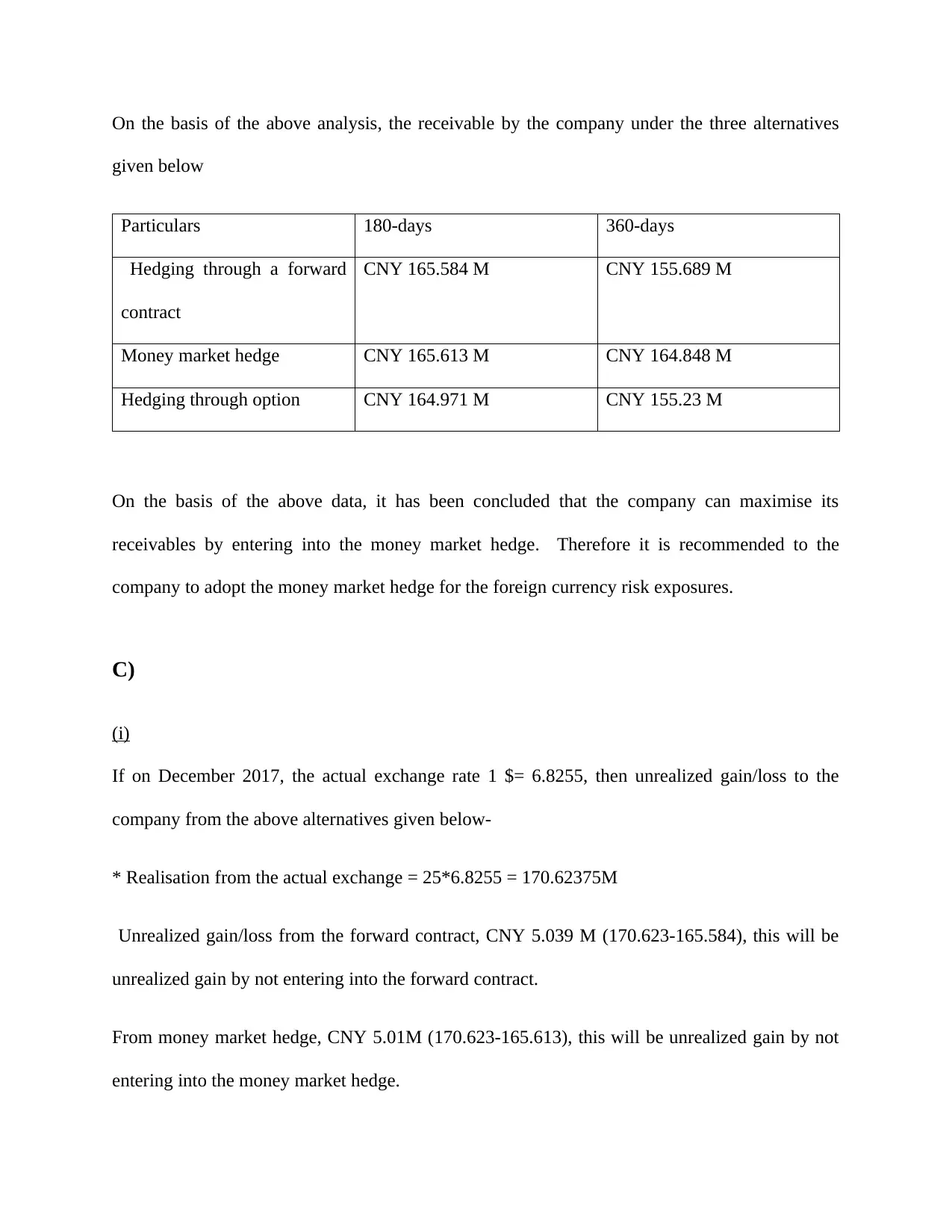

On the basis of the above analysis, the receivable by the company under the three alternatives

given below

Particulars 180-days 360-days

Hedging through a forward

contract

CNY 165.584 M CNY 155.689 M

Money market hedge CNY 165.613 M CNY 164.848 M

Hedging through option CNY 164.971 M CNY 155.23 M

On the basis of the above data, it has been concluded that the company can maximise its

receivables by entering into the money market hedge. Therefore it is recommended to the

company to adopt the money market hedge for the foreign currency risk exposures.

C)

(i)

If on December 2017, the actual exchange rate 1 $= 6.8255, then unrealized gain/loss to the

company from the above alternatives given below-

* Realisation from the actual exchange = 25*6.8255 = 170.62375M

Unrealized gain/loss from the forward contract, CNY 5.039 M (170.623-165.584), this will be

unrealized gain by not entering into the forward contract.

From money market hedge, CNY 5.01M (170.623-165.613), this will be unrealized gain by not

entering into the money market hedge.

given below

Particulars 180-days 360-days

Hedging through a forward

contract

CNY 165.584 M CNY 155.689 M

Money market hedge CNY 165.613 M CNY 164.848 M

Hedging through option CNY 164.971 M CNY 155.23 M

On the basis of the above data, it has been concluded that the company can maximise its

receivables by entering into the money market hedge. Therefore it is recommended to the

company to adopt the money market hedge for the foreign currency risk exposures.

C)

(i)

If on December 2017, the actual exchange rate 1 $= 6.8255, then unrealized gain/loss to the

company from the above alternatives given below-

* Realisation from the actual exchange = 25*6.8255 = 170.62375M

Unrealized gain/loss from the forward contract, CNY 5.039 M (170.623-165.584), this will be

unrealized gain by not entering into the forward contract.

From money market hedge, CNY 5.01M (170.623-165.613), this will be unrealized gain by not

entering into the money market hedge.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

From Option Contract, unrealized gain/or loss will be the difference from spot price of the June

and the spot price of December that is (6.72475-6.8255)*25M = CNY 2.519 M, which is the

unrealised gain by not entering into the option contract.

If on June 2018, the actual exchange rate 1 $= 6.950, then unrealized gain/loss to the company

from the above alternatives given below-

* Realisation from the actual exchange = 25*6.950 = 173.75M

Unrealized gain/loss from the forward contract, CNY 18.061 M (173.75-155.689), this will be

unrealized gain by not entering into the forward contract.

From money market hedge, CNY 8.902 M (173.75-164.848), this will be unrealized gain by not

entering into the money market hedge.

From Option Contract unrealized gain/or loss will be the difference from spot price of the June

2017 and the spot price of June 2018 that is (6.72475-6.950)*25M = CNY 5.631 M, which is the

unrealised gain by not entering into the option contract.

(ii)

Since, from hedging through the forward contract, the amount of realisation by the company is

certain. In this case for the 180 days, the company entered to sale the dollar at a fixed rate of

CNY 6.62335/$. However the present spot rate on December 2017 is CNY 6.8255/$. Therefore

the company sold the dollar at a less price than the spot rate. So there will be the gain which was

not realised by the company. In a similar manner, the 360 days forward rate CNY 6.22755/$,

while the spot rate on June 2018 CNY 6.950/$, which is more than the rate of the company,

therefore in this case also the gain, which was not realised by the company.

and the spot price of December that is (6.72475-6.8255)*25M = CNY 2.519 M, which is the

unrealised gain by not entering into the option contract.

If on June 2018, the actual exchange rate 1 $= 6.950, then unrealized gain/loss to the company

from the above alternatives given below-

* Realisation from the actual exchange = 25*6.950 = 173.75M

Unrealized gain/loss from the forward contract, CNY 18.061 M (173.75-155.689), this will be

unrealized gain by not entering into the forward contract.

From money market hedge, CNY 8.902 M (173.75-164.848), this will be unrealized gain by not

entering into the money market hedge.

From Option Contract unrealized gain/or loss will be the difference from spot price of the June

2017 and the spot price of June 2018 that is (6.72475-6.950)*25M = CNY 5.631 M, which is the

unrealised gain by not entering into the option contract.

(ii)

Since, from hedging through the forward contract, the amount of realisation by the company is

certain. In this case for the 180 days, the company entered to sale the dollar at a fixed rate of

CNY 6.62335/$. However the present spot rate on December 2017 is CNY 6.8255/$. Therefore

the company sold the dollar at a less price than the spot rate. So there will be the gain which was

not realised by the company. In a similar manner, the 360 days forward rate CNY 6.22755/$,

while the spot rate on June 2018 CNY 6.950/$, which is more than the rate of the company,

therefore in this case also the gain, which was not realised by the company.

By the money market hedge, company certain its realisation. Since, the realization by the

company from the money market hedge was less than, if the company did not enter in the money

market hedging. Therefore in this strategy also the company has unrealized gain by entering into

the money market hedging.

Further, by option contract hedging the company acquire the right to sale the dollar in the

market. Since the current spot price of the company in both the cases was more than the strike

price, therefore, the company will not exercise the option. However if the company receive the

payment in June 2017 then the realisation $ 50M * 6.72475 = CNY 336.2375, which is less than

the comparison with the actual spot rate of December 2017 and June 2018. Therefore the

company suffered from the unrealised gain in this case also.

D)

(i)

For mitigating the risk level in the business, many companies make the strategies. The risk may

arise due to volatility in the currency rates, inflation rate, interest rate and etc.it are very

important to make the strategy with an assist in reducing the risk of the foreign exchange

(Cenedese, Sarno, and Tsiakas, 2014). There is a various alternative to manage the risk from the

change in the exchange rate, which is already described above. By managing the foreign

exchange risk, an investor can protect their profit (Bandaly, Shanker, and Şatır, 2018). Along

with this, even if in the future, the exchange rate changes adversely, then also by the risk

management strategy investor can survive in the market. Moreover, the hedging risk not only

protects from the change in the currency rate, but an investor can also safeguard from the

commodity prices, interest rate, the rate of inflation and many others. An investor can maximise

company from the money market hedge was less than, if the company did not enter in the money

market hedging. Therefore in this strategy also the company has unrealized gain by entering into

the money market hedging.

Further, by option contract hedging the company acquire the right to sale the dollar in the

market. Since the current spot price of the company in both the cases was more than the strike

price, therefore, the company will not exercise the option. However if the company receive the

payment in June 2017 then the realisation $ 50M * 6.72475 = CNY 336.2375, which is less than

the comparison with the actual spot rate of December 2017 and June 2018. Therefore the

company suffered from the unrealised gain in this case also.

D)

(i)

For mitigating the risk level in the business, many companies make the strategies. The risk may

arise due to volatility in the currency rates, inflation rate, interest rate and etc.it are very

important to make the strategy with an assist in reducing the risk of the foreign exchange

(Cenedese, Sarno, and Tsiakas, 2014). There is a various alternative to manage the risk from the

change in the exchange rate, which is already described above. By managing the foreign

exchange risk, an investor can protect their profit (Bandaly, Shanker, and Şatır, 2018). Along

with this, even if in the future, the exchange rate changes adversely, then also by the risk

management strategy investor can survive in the market. Moreover, the hedging risk not only

protects from the change in the currency rate, but an investor can also safeguard from the

commodity prices, interest rate, the rate of inflation and many others. An investor can maximise

its profit by managing the risk. Although there is some cost involved in managing the risk, this

cost can easily cover by the profit from the investment (Apergis, and Artikis, 2016).

On the other side, if the investor does not make an effort to manage the foreign exchange risk,

then the investor has possessed so many risks due to the change in the market condition. Since

the change in the currency rate, interest rate, inflation rate, it is very typical to measure the

change in the future. Therefore in any case, if the condition of the market moves adverse with the

investment, then the chances of loss will very significant impact to the investor (Chong, Chang,

and Tan, 2014). So, it is worth full for the investor to make the efforts for managing the risk due

to the foreign exchange

(ii)

If the company remain unhedged, then the company sell the $ 25 Million at the spot price of

December 2017 and another $ 25 Million at the spot rate on the date of June 2018.

Realisation on December 2017 = $ 25 M * 6.8255 = CNY 170.6375

Realisation on June 2018 = $ 25M *6.950= CNY 173.75

On the basis of the above calculation, it has been seen that the company, if not adopt any hedging

alternative than obtaining the more realisation by selling the dollar at the spot prices.

cost can easily cover by the profit from the investment (Apergis, and Artikis, 2016).

On the other side, if the investor does not make an effort to manage the foreign exchange risk,

then the investor has possessed so many risks due to the change in the market condition. Since

the change in the currency rate, interest rate, inflation rate, it is very typical to measure the

change in the future. Therefore in any case, if the condition of the market moves adverse with the

investment, then the chances of loss will very significant impact to the investor (Chong, Chang,

and Tan, 2014). So, it is worth full for the investor to make the efforts for managing the risk due

to the foreign exchange

(ii)

If the company remain unhedged, then the company sell the $ 25 Million at the spot price of

December 2017 and another $ 25 Million at the spot rate on the date of June 2018.

Realisation on December 2017 = $ 25 M * 6.8255 = CNY 170.6375

Realisation on June 2018 = $ 25M *6.950= CNY 173.75

On the basis of the above calculation, it has been seen that the company, if not adopt any hedging

alternative than obtaining the more realisation by selling the dollar at the spot prices.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

REFERENCES

Apergis, N. and Artikis, P.G., 2016. Foreign exchange risk, equity risk factors and economic

growth. Atlantic Economic Journal, 44(4), pp.425-445.

Bandaly, D., Shanker, L. and Şatır, A., 2018. Integrated Financial and Operational Risk

Management of Foreign Exchange Risk, Input Commodity Price Risk and Demand

Uncertainty. IFAC-PapersOnLine, 51(11), pp.957-962.

Bettis, C., Bizjak, J. and Kalpathy, S., 2015. Why do insiders hedge their ownership? An

empirical examination. Financial Management, 44(3), pp.655-683.

Bhatia, A. and Bhat, S.P., 2016, May. Optimal Static Hedging of Uncertain Future Foreign

Currency Cash Flows Using FX Forwards. In Industrial Engineering, Management Science and

Application (ICIMSA), 2016 International Conference on (pp. 1-5). IEEE.

Cenedese, G., Sarno, L. and Tsiakas, I., 2014. Foreign exchange risk and the predictability of

carry trade returns. Journal of Banking & Finance, 42, pp.302-313.

Chong, L.L., Chang, X.J. and Tan, S.H., 2014. Determinants of corporate foreign exchange risk

hedging. Managerial Finance, 40(2), pp.176-188.

Fleten, S.E., Hagen, L.A., Nygård, M.T., Smith-Sivertsen, R. and Sollie, J.M., 2015. The

overnight risk premium in electricity forward contracts. Energy Economics, 49, pp.293-300.

Islam, M. and Chakraborti, J., 2015. Futures and forward contract as a route of hedging the

risk. Risk Governance & Control: Financial Markets & Institutions, 5(4), pp.68-78.

Apergis, N. and Artikis, P.G., 2016. Foreign exchange risk, equity risk factors and economic

growth. Atlantic Economic Journal, 44(4), pp.425-445.

Bandaly, D., Shanker, L. and Şatır, A., 2018. Integrated Financial and Operational Risk

Management of Foreign Exchange Risk, Input Commodity Price Risk and Demand

Uncertainty. IFAC-PapersOnLine, 51(11), pp.957-962.

Bettis, C., Bizjak, J. and Kalpathy, S., 2015. Why do insiders hedge their ownership? An

empirical examination. Financial Management, 44(3), pp.655-683.

Bhatia, A. and Bhat, S.P., 2016, May. Optimal Static Hedging of Uncertain Future Foreign

Currency Cash Flows Using FX Forwards. In Industrial Engineering, Management Science and

Application (ICIMSA), 2016 International Conference on (pp. 1-5). IEEE.

Cenedese, G., Sarno, L. and Tsiakas, I., 2014. Foreign exchange risk and the predictability of

carry trade returns. Journal of Banking & Finance, 42, pp.302-313.

Chong, L.L., Chang, X.J. and Tan, S.H., 2014. Determinants of corporate foreign exchange risk

hedging. Managerial Finance, 40(2), pp.176-188.

Fleten, S.E., Hagen, L.A., Nygård, M.T., Smith-Sivertsen, R. and Sollie, J.M., 2015. The

overnight risk premium in electricity forward contracts. Energy Economics, 49, pp.293-300.

Islam, M. and Chakraborti, J., 2015. Futures and forward contract as a route of hedging the

risk. Risk Governance & Control: Financial Markets & Institutions, 5(4), pp.68-78.

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.