Forensic Accounting: A Case Study of AIG and Gen Re Fraudulent Transaction

VerifiedAdded on 2023/06/04

|21

|2991

|366

AI Summary

This report provides a case study of AIG and Gen Re fraudulent transaction, its presentation, detection, investigation, impact analysis, and recommendations for robust internal control procedures.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Forensic Accounting

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Introduction

• Mr Greenberg, former head of AIG, in 2016 had appeared in court for an

accounting fraud case dated back in 2005 to boost the prices of the

stocks. In the early times of year 2000, the allegation was that Mr

Greenberg presided over many accounting scandal case (Npr, 2016). Most

of the cases were successfully settled outside of the court but the case

against Mr Greenberg for the fraud charges in civil accounting is going on

for more than a decade. In the early 2017, Mr Greenberg now 91, and

Howard Smith former AIG CFO as the co-defended reached to a

settlement in the form of an agreement with the attorney general of New

York Eric T S Schneiderman (Smith, 2017). As part of the agreement two

defended acknowledge and revealed their participation is two inaccurate

projections based financial transaction for the AIG. They also agreed in

giving up the performance bonus received in the following four years

from 2001.

• Mr Greenberg, former head of AIG, in 2016 had appeared in court for an

accounting fraud case dated back in 2005 to boost the prices of the

stocks. In the early times of year 2000, the allegation was that Mr

Greenberg presided over many accounting scandal case (Npr, 2016). Most

of the cases were successfully settled outside of the court but the case

against Mr Greenberg for the fraud charges in civil accounting is going on

for more than a decade. In the early 2017, Mr Greenberg now 91, and

Howard Smith former AIG CFO as the co-defended reached to a

settlement in the form of an agreement with the attorney general of New

York Eric T S Schneiderman (Smith, 2017). As part of the agreement two

defended acknowledge and revealed their participation is two inaccurate

projections based financial transaction for the AIG. They also agreed in

giving up the performance bonus received in the following four years

from 2001.

• But this giving up amount of $9.9 m is far less than the demanded

amount of $50 m by the attorney general (Smith, 2017). The falling

reserve of AIG lead to fall in the share price and to recover that

AIG with ‘General Re Corporation’ struck a deal of fraudulent

nature where AIG was able to add close to $500 m in their reserve

in the form of acquired premium by supporting through phone

documents (Kirchgaessne, 2006). This led to false inflation of the

company’s valuation by close to $100m from the year 2000.

Considering this introductory note of this report the following

section of this report would provide case background,

presentation, detection, investigation, impact analysis and finally

recommending measures through learned lesson.

amount of $50 m by the attorney general (Smith, 2017). The falling

reserve of AIG lead to fall in the share price and to recover that

AIG with ‘General Re Corporation’ struck a deal of fraudulent

nature where AIG was able to add close to $500 m in their reserve

in the form of acquired premium by supporting through phone

documents (Kirchgaessne, 2006). This led to false inflation of the

company’s valuation by close to $100m from the year 2000.

Considering this introductory note of this report the following

section of this report would provide case background,

presentation, detection, investigation, impact analysis and finally

recommending measures through learned lesson.

Background

• AIG is one of the largest companies in the insurance industry worldwide. The

Q3 result of AIG in the year 2000, October 26, were able to show the

increment in the amount of premium for the insurance but the reserve of the

company of the company significantly by an amount of $59m (Hass et al.,

2012). This was a great setback for the market at that time and that led to a

%6 falls in the share price of the company in the New York stock exchange

(casact, 2009). The stock price fall is the result of two down gradation report

from two different analysts. Under this circumstances the head of AIG, Mr

Greenberg had to take some action to stop the fall of share price. Considering

this Mr Greenberg then called CEO of Gen Re Mr Ferguson for a transaction

structuring. In this meeting of October 31 2000, Mr Greenberg sought help

from Mr Ferguson to transfer an amount ranging from $200-500 m to the

account of AIG by the end of the year and the transaction would be treated

as the agreement of reinsurance between Gen Re and AIG (casact, 2009).

• AIG is one of the largest companies in the insurance industry worldwide. The

Q3 result of AIG in the year 2000, October 26, were able to show the

increment in the amount of premium for the insurance but the reserve of the

company of the company significantly by an amount of $59m (Hass et al.,

2012). This was a great setback for the market at that time and that led to a

%6 falls in the share price of the company in the New York stock exchange

(casact, 2009). The stock price fall is the result of two down gradation report

from two different analysts. Under this circumstances the head of AIG, Mr

Greenberg had to take some action to stop the fall of share price. Considering

this Mr Greenberg then called CEO of Gen Re Mr Ferguson for a transaction

structuring. In this meeting of October 31 2000, Mr Greenberg sought help

from Mr Ferguson to transfer an amount ranging from $200-500 m to the

account of AIG by the end of the year and the transaction would be treated

as the agreement of reinsurance between Gen Re and AIG (casact, 2009).

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

• In the form of risk less approach AIG should not incur any loss from

this transaction. Prior to this situation AIG used to have a very good

relation with Gen Re as AIG was the largest customer for the Gen

Re. The CEO of Gen Re specifically understood the fact that the

demand of AG was not a reinsurance transaction of bona fide

nature. To make this deal bona fide AIG has to bear the risk for

actual insurance (casact, 2009). Here AIG was asking a transaction

that would be like the reinsurance in the accounting term but actual

would have no risk. In the early part of the November of 2000, CFO,

vice president and the CEO of Gen Re decided that to go ahead with

the deal considering their good relationship with AIG (Hass et al.,

2012). This was the actual scenario of fraud before it was

perpetrated and detected.

this transaction. Prior to this situation AIG used to have a very good

relation with Gen Re as AIG was the largest customer for the Gen

Re. The CEO of Gen Re specifically understood the fact that the

demand of AG was not a reinsurance transaction of bona fide

nature. To make this deal bona fide AIG has to bear the risk for

actual insurance (casact, 2009). Here AIG was asking a transaction

that would be like the reinsurance in the accounting term but actual

would have no risk. In the early part of the November of 2000, CFO,

vice president and the CEO of Gen Re decided that to go ahead with

the deal considering their good relationship with AIG (Hass et al.,

2012). This was the actual scenario of fraud before it was

perpetrated and detected.

Presentation of fraud case

• This transaction fraud was widely known in the year

2004. This was the result of the ongoing

investigation for the accounting practices of the

insurance industry. During this time the ‘NY

insurance department’ and the office of attorney

general started to look into the matter of AIG more

seriously. Earlier the SEC showed their suspicion

because of theirs one insurance product named ‘loss

mitigation insurance’. But the fraud case came into

light slowly and the subsequent steps are as follows.

• This transaction fraud was widely known in the year

2004. This was the result of the ongoing

investigation for the accounting practices of the

insurance industry. During this time the ‘NY

insurance department’ and the office of attorney

general started to look into the matter of AIG more

seriously. Earlier the SEC showed their suspicion

because of theirs one insurance product named ‘loss

mitigation insurance’. But the fraud case came into

light slowly and the subsequent steps are as follows.

• SEC in the 2001 came to know about the AIG’s assistant to their clients

for balance sheet bolstering through the approach of insurance

transaction of fraud nature. This case was investigated by SEC and in

presence of department of justice AIG had to settle for a civil penalty of

$10m (Hass et al., 2012). Under this continuous investigation in 2005

February, IAG disclosed their earning of 2004. In the March of the 2005

AIG disclosed through deal with Gen Re for the reinsurance. In the

following court preceding the company Gen Re’s top executive revealed

that they were also aware about the deal and also had the knowledge

that AIG would use this transaction through applying accounting

procedure to fulfil the gap in loss reserve. After the deal AIG added close

to $500m in the reserve account of their balance sheet at the last and

first quarter of the 2000 and 2001 financial year (casact, 2009

for balance sheet bolstering through the approach of insurance

transaction of fraud nature. This case was investigated by SEC and in

presence of department of justice AIG had to settle for a civil penalty of

$10m (Hass et al., 2012). Under this continuous investigation in 2005

February, IAG disclosed their earning of 2004. In the March of the 2005

AIG disclosed through deal with Gen Re for the reinsurance. In the

following court preceding the company Gen Re’s top executive revealed

that they were also aware about the deal and also had the knowledge

that AIG would use this transaction through applying accounting

procedure to fulfil the gap in loss reserve. After the deal AIG added close

to $500m in the reserve account of their balance sheet at the last and

first quarter of the 2000 and 2001 financial year (casact, 2009

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

• Applying some accounting principle AIG showed it revenue.

AIG hope that this addition of $500m in their reserve would be

able to satisfy the critic in the stock market. This was a false

way of inflating the valuation of the company. Later many

executive of AIG also stated that the deal transaction in the

balance sheet must have been stated as loan and not the

insurance. In the insurance business the risk is reinsured

(Carter, 2013). Here the firm 1 would insure the risk of the

insurance policy written by firm 2 to fir 2’s customer. this was a

finite insure that firm 2 purchased from firm 1 and in the finite

insurance policy the insured firm distribute the insure policy

cost over the long period of time (Carter, 2013).

AIG hope that this addition of $500m in their reserve would be

able to satisfy the critic in the stock market. This was a false

way of inflating the valuation of the company. Later many

executive of AIG also stated that the deal transaction in the

balance sheet must have been stated as loan and not the

insurance. In the insurance business the risk is reinsured

(Carter, 2013). Here the firm 1 would insure the risk of the

insurance policy written by firm 2 to fir 2’s customer. this was a

finite insure that firm 2 purchased from firm 1 and in the finite

insurance policy the insured firm distribute the insure policy

cost over the long period of time (Carter, 2013).

• Therefore if firm 2 had to pay the cover amount to their

customer within the few year of the start of those policies,

firm 2 would be able to claim against their reinsurance with

firm 1. Because of this reinsurance policy firm 1 received a

large amount as premium from firm 2. In this insures under

the condition of claim scenario to firm 2 from their customer,

the reinsurance amount paid by the firm 2 to firm 1 would

return back to firm 2 (Blanchard, 2014). In this specific

insurance type context the present account principles were

based on the open interpretation. The accounting question

come as to state this transaction as reinsurance or the deposit.

customer within the few year of the start of those policies,

firm 2 would be able to claim against their reinsurance with

firm 1. Because of this reinsurance policy firm 1 received a

large amount as premium from firm 2. In this insures under

the condition of claim scenario to firm 2 from their customer,

the reinsurance amount paid by the firm 2 to firm 1 would

return back to firm 2 (Blanchard, 2014). In this specific

insurance type context the present account principles were

based on the open interpretation. The accounting question

come as to state this transaction as reinsurance or the deposit.

• AIG treated it reinsurance and Gen Re treated it a

deposit process of accounting. Actually AIG in

exchange of $5m of payment got insurance contract

of worth $500m and subsequent $500m premium

into AIG. This transaction increased cash reserve by

the same amount. This $5m is the payment of

premium from the AIG to Gen Re. Two separate

contract under the condition of reinsurance were

formulated and in two part $250m amount entered

into AIG (securities.stanford, 2005).

deposit process of accounting. Actually AIG in

exchange of $5m of payment got insurance contract

of worth $500m and subsequent $500m premium

into AIG. This transaction increased cash reserve by

the same amount. This $5m is the payment of

premium from the AIG to Gen Re. Two separate

contract under the condition of reinsurance were

formulated and in two part $250m amount entered

into AIG (securities.stanford, 2005).

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

• But under the circumstances of no claim in Gen Re the

amount would go back to Gen Re from AIG. Therefore

the amount can be classified as loan in the account. If it

had to be a insurance then some amount of risk factor

must have been transferred in to AIG which is not the

case as AIG already asked for no risk. Under this scenario

of no risk the loan would be treated as liability. The

fraudulent approach is that these contracts are not the

reinsurance contract. This lack of economic substantial

argument of these contracts makes them unworthy of

accounted for.

amount would go back to Gen Re from AIG. Therefore

the amount can be classified as loan in the account. If it

had to be a insurance then some amount of risk factor

must have been transferred in to AIG which is not the

case as AIG already asked for no risk. Under this scenario

of no risk the loan would be treated as liability. The

fraudulent approach is that these contracts are not the

reinsurance contract. This lack of economic substantial

argument of these contracts makes them unworthy of

accounted for.

Detection of fraud case

• The agreement of the contract is created by the Houldsworth. Along with

the reinsurance vice president and others, Houldsworth wrote the

contract. As per the contract Gen Re would receive a payment of $5.2 m

from AIG as fee of this deal. Then for the payment of $5.2m and another

$10m as pre-fund premium, National Union is to be paid through the

CRD obligation (Hass et al., 2012). In this context AIG and Gen Re went

for unrelated separate reinsurance contract and that happened between

subsidiary of AIG and Gen Re. The subsidiary is the ‘Hartford steam

boiler inspection and Insurance Company’ or HSB. This route was

specifically taken for masking the Gen Re and AIG’s transfer and its real

reason. In this total transaction process actually AIG solicited this

transaction deal. But Gen Re created a documentation that is a sham as

that made it look like Gen Re solicited for the deal.

• The agreement of the contract is created by the Houldsworth. Along with

the reinsurance vice president and others, Houldsworth wrote the

contract. As per the contract Gen Re would receive a payment of $5.2 m

from AIG as fee of this deal. Then for the payment of $5.2m and another

$10m as pre-fund premium, National Union is to be paid through the

CRD obligation (Hass et al., 2012). In this context AIG and Gen Re went

for unrelated separate reinsurance contract and that happened between

subsidiary of AIG and Gen Re. The subsidiary is the ‘Hartford steam

boiler inspection and Insurance Company’ or HSB. This route was

specifically taken for masking the Gen Re and AIG’s transfer and its real

reason. In this total transaction process actually AIG solicited this

transaction deal. But Gen Re created a documentation that is a sham as

that made it look like Gen Re solicited for the deal.

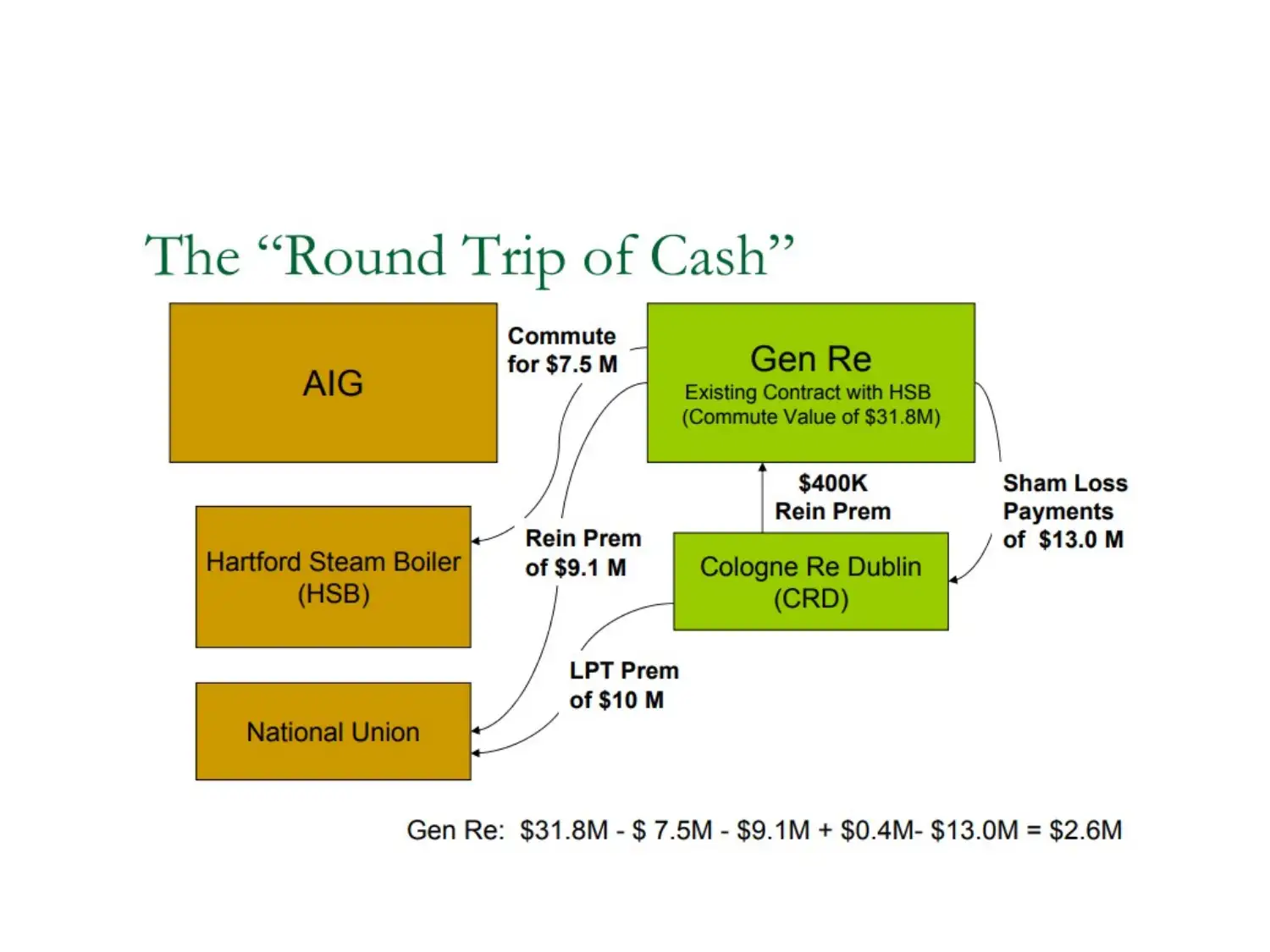

• In the process of leveraging this contract AIG was

supposed to receive $31.8m from the Gen Re. Here a

payment of $7.5m is done by the Gen Re for the

commutation of existing contract with HSB. Then around

$9.1m as premium is paid by Gen Re for the HSB’s

reinsure loss (securities.stanford, 2005). The sham

contract of reinsurance is used to pay $0.4m as premium

by CRD whereas it received a payment for loss of $13M.

This AIG received around $10m as LPT premium from

CRD. After all of these CRD and Gen Re used this $5.2m

for the fee covering.

supposed to receive $31.8m from the Gen Re. Here a

payment of $7.5m is done by the Gen Re for the

commutation of existing contract with HSB. Then around

$9.1m as premium is paid by Gen Re for the HSB’s

reinsure loss (securities.stanford, 2005). The sham

contract of reinsurance is used to pay $0.4m as premium

by CRD whereas it received a payment for loss of $13M.

This AIG received around $10m as LPT premium from

CRD. After all of these CRD and Gen Re used this $5.2m

for the fee covering.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

• Therefore at the end AIG paid $5m to Gen Re

as fee but the payment of $10m was not

followed by AIG as per the written contract

(casact, 2009). The daft contract also

discussed the no-risk part of the deal. All of

these are used as the prosecution evidence.

as fee but the payment of $10m was not

followed by AIG as per the written contract

(casact, 2009). The daft contract also

discussed the no-risk part of the deal. All of

these are used as the prosecution evidence.

Aftermath and investigation of fraud case

• In the prosecution process US Code is used. Under

that ‘Security investor protection laws’ and under

that ‘code of federal regulation’ is used. The

conspiracy law, mail fraud law, were also used in this

case for the prosecution process. After the

investigation process is over the several personnel

involved in this case were prosecuted. Gen Re CEO,

Ron Ferguson was convicted on 1 count of conspiracy,

7 counts of security fraud, 5 counts of false statement

and 3 counts of mail fraud (casact, 2009).

• In the prosecution process US Code is used. Under

that ‘Security investor protection laws’ and under

that ‘code of federal regulation’ is used. The

conspiracy law, mail fraud law, were also used in this

case for the prosecution process. After the

investigation process is over the several personnel

involved in this case were prosecuted. Gen Re CEO,

Ron Ferguson was convicted on 1 count of conspiracy,

7 counts of security fraud, 5 counts of false statement

and 3 counts of mail fraud (casact, 2009).

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

• After this he was sentenced to prison for 2 years, supervision release for 2

years, $200k in fine. Christopher Garand, chief underwriter and senior vice

president of Gen Re also got similar conviction and sentenced to 1 year prison,

supervision release for 1 years and $150k in fine. Then Christian Milton vice

president of AIG’s reinsurance also the similar conviction rate but the sentence

was of prison time 4 years, supervision release of 2 years and a fine of $200k.

Robert Graham the assistant general and SVP of Gen Re and Elizabeth Monrad

CFO of Gen Re also got the similar conviction. Elizabeth Monrad received a

prison term of 1.8 month adn Robert Graham received a sentence of super

vision release of 2 years and a fine of $100k (archive.boston, 2009; Johnson,

2011). In the 2017 Mr Greenberg the former head of AG and the CFO Mr Smith

reached an agreement with the office of attorney general of New York after

battling the decade long fraud charge of civil accounting. Here they would

forgo the performance bonus received during 2001 to 2004 as an amount of

$9.9m (Smith, 2017).

years, $200k in fine. Christopher Garand, chief underwriter and senior vice

president of Gen Re also got similar conviction and sentenced to 1 year prison,

supervision release for 1 years and $150k in fine. Then Christian Milton vice

president of AIG’s reinsurance also the similar conviction rate but the sentence

was of prison time 4 years, supervision release of 2 years and a fine of $200k.

Robert Graham the assistant general and SVP of Gen Re and Elizabeth Monrad

CFO of Gen Re also got the similar conviction. Elizabeth Monrad received a

prison term of 1.8 month adn Robert Graham received a sentence of super

vision release of 2 years and a fine of $100k (archive.boston, 2009; Johnson,

2011). In the 2017 Mr Greenberg the former head of AG and the CFO Mr Smith

reached an agreement with the office of attorney general of New York after

battling the decade long fraud charge of civil accounting. Here they would

forgo the performance bonus received during 2001 to 2004 as an amount of

$9.9m (Smith, 2017).

Fallout and impact of the case

• After the fallout of this case series of penalty had

been imposed on the perpetrator of this account

fraud case. Gen Re had agreed to pay $92.2m as

penalty to settle the case (nbcnews, 2010). This

was claimed by the shareholders and the federal

authority. The final settlement for the AIG cost

around $1.64bn which is the result of the lawsuit by

the shareholders (ifre, 2016). AIG also had to

restate the financial report of their five year

operation and lowered their 10% income.

• After the fallout of this case series of penalty had

been imposed on the perpetrator of this account

fraud case. Gen Re had agreed to pay $92.2m as

penalty to settle the case (nbcnews, 2010). This

was claimed by the shareholders and the federal

authority. The final settlement for the AIG cost

around $1.64bn which is the result of the lawsuit by

the shareholders (ifre, 2016). AIG also had to

restate the financial report of their five year

operation and lowered their 10% income.

Learned lesson

• This accounting fraud case provides a lesson for the robust for

the internal control process (Hoitash et al., 2009). Had the

auditor been independent in this case the situation would

have been averted at the first place. On the other hand the

role of the audit committee and its independence is also felt in

this case. The audit committee would have been a strong

monitoring body that would have prevented such incident to

happen in the organisation (Tanyi and Smith, 2014). Another

need is visible in this case analysis and that is the fear factor.

Had there been a strong law with stringent penalties it would

have acted as a prohibition for the top executive to engage in

such activity.

• This accounting fraud case provides a lesson for the robust for

the internal control process (Hoitash et al., 2009). Had the

auditor been independent in this case the situation would

have been averted at the first place. On the other hand the

role of the audit committee and its independence is also felt in

this case. The audit committee would have been a strong

monitoring body that would have prevented such incident to

happen in the organisation (Tanyi and Smith, 2014). Another

need is visible in this case analysis and that is the fear factor.

Had there been a strong law with stringent penalties it would

have acted as a prohibition for the top executive to engage in

such activity.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Recommendation

• Considering the above analysis the following recommendation

are provided.

• Establishing a string internal control procedure in the

organisation (Hoitash et al., 2009).

• Strictly maintain the independence of the auditor in the

organisation.

• Form an audit committee which would independent in nature.

• Provide monitoring mechanism and sufficient power to the

audit committee to detect these frauds (Tanyi and Smith, 2014).

• Create awareness about the legal, financial and criminal law

implication of these fraudulent activities.

• Considering the above analysis the following recommendation

are provided.

• Establishing a string internal control procedure in the

organisation (Hoitash et al., 2009).

• Strictly maintain the independence of the auditor in the

organisation.

• Form an audit committee which would independent in nature.

• Provide monitoring mechanism and sufficient power to the

audit committee to detect these frauds (Tanyi and Smith, 2014).

• Create awareness about the legal, financial and criminal law

implication of these fraudulent activities.

Reference

• archive.boston. (2009). Ex-General Re executive is sentenced. [online] Available at:

http://archive.boston.com/business/articles/2009/05/01/ex_general_re_executive_is_sentenced/ [Accessed 25 Sep. 2018].

• Blanchard, R. (2014). Accounting. Wiley StatsRef: Statistics Reference Online.

• Carter, R. L. (Ed.). (2013). Reinsurance. Springer Science & Business Media.

• casact, R. (2009). Actuarial Accounting: A Cautionary Report. [online] Available at: https://www.casact.org/education/spring/2009/handouts/young.pdf [Accessed 25

Sep. 2018].

• Hass, S., Nitkin, M., & Burnaby, P. (2012, January). AIG and General Re: Helping One Another or Reinsurance Scheme. In International Conference on Accounting and

Finance (AT). Proceedings (p. 215). Global Science and Technology Forum.

• Hoitash, U., Hoitash, R., & Bedard, J. C. (2009). Corporate governance and internal control over financial reporting: A comparison of regulatory regimes. The accounting

review, 84(3), 839-867.

• ifre, (2016). Former AIG chief Greenberg must face New York fraud trial. [online] Available at: http://www.ifre.com/former-aig-chief-greenberg-must-face-new-york-

fraud-trial/21250134.fullarticle [Accessed 25 Sep. 2018].

• Johnson, S. (2011). Once Facing a Prison Term, Ex-CFO Could Go Free. [online] Available at: http://ww2.cfo.com/fraud/2011/08/once-facing-a-prison-term-ex-cfo-

could-go-free/ [Accessed 25 Sep. 2018].

• Kirchgaessne, S. (2006). Ex-Gen Re and AIG executives on fraud charges. [online] Available at: https://www.ft.com/content/f96d9e7a-940a-11da-82ea-0000779e2340

[Accessed 25 Sep. 2018].

• Maury, M. D., McCarthy, I. N., & Shoaf, V. (2007). AIG: Accounting and Ethical Lapses. In Insurance Ethics for a More Ethical World (pp. 39-53). Emerald Group Publishing

Limited.

• nbcnews, (2010). Gen Re settles AIG fraud claims fo $92.2m. [online] Available at: http://www.nbcnews.com/id/34959105/ns/business-us_business/t/gen-re-settles-

aig-fraud-claims-m/#.W6o32tcza1s [Accessed 25 Sep. 2018].

• Npr. (2016). NPR Choice page. [online] Available at: https://www.npr.org/2016/09/13/493721864/after-11-years-accounting-fraud-case-against-former-aig-chief-to-

begin [Accessed 25 Sep. 2018].

• securities.stanford, (2005). CONSOLIDATED SECOND AMENDED CLASS ACTION COMPLAINT. [online] Available at:

http://securities.stanford.edu/filings-documents/1033/AIG04_01/2005927_r01c_048141.pdf [Accessed 25 Sep. 2018].

• Smith, R. (2017). Former A.I.G. Executives Reach Settlement in Accounting Fraud Case. [online] Available at:

https://www.nytimes.com/2017/02/10/business/dealbook/former-aig-executives-reach-settlement-in-accounting-fraud-case.html [Accessed 25 Sep. 2018].

• Tanyi, P. N., & Smith, D. B. (2014). Busyness, expertise, and financial reporting quality of audit committee chairs and financial experts. Auditing: A Journal of Practice &

Theory, 34(2), 59-89.

• archive.boston. (2009). Ex-General Re executive is sentenced. [online] Available at:

http://archive.boston.com/business/articles/2009/05/01/ex_general_re_executive_is_sentenced/ [Accessed 25 Sep. 2018].

• Blanchard, R. (2014). Accounting. Wiley StatsRef: Statistics Reference Online.

• Carter, R. L. (Ed.). (2013). Reinsurance. Springer Science & Business Media.

• casact, R. (2009). Actuarial Accounting: A Cautionary Report. [online] Available at: https://www.casact.org/education/spring/2009/handouts/young.pdf [Accessed 25

Sep. 2018].

• Hass, S., Nitkin, M., & Burnaby, P. (2012, January). AIG and General Re: Helping One Another or Reinsurance Scheme. In International Conference on Accounting and

Finance (AT). Proceedings (p. 215). Global Science and Technology Forum.

• Hoitash, U., Hoitash, R., & Bedard, J. C. (2009). Corporate governance and internal control over financial reporting: A comparison of regulatory regimes. The accounting

review, 84(3), 839-867.

• ifre, (2016). Former AIG chief Greenberg must face New York fraud trial. [online] Available at: http://www.ifre.com/former-aig-chief-greenberg-must-face-new-york-

fraud-trial/21250134.fullarticle [Accessed 25 Sep. 2018].

• Johnson, S. (2011). Once Facing a Prison Term, Ex-CFO Could Go Free. [online] Available at: http://ww2.cfo.com/fraud/2011/08/once-facing-a-prison-term-ex-cfo-

could-go-free/ [Accessed 25 Sep. 2018].

• Kirchgaessne, S. (2006). Ex-Gen Re and AIG executives on fraud charges. [online] Available at: https://www.ft.com/content/f96d9e7a-940a-11da-82ea-0000779e2340

[Accessed 25 Sep. 2018].

• Maury, M. D., McCarthy, I. N., & Shoaf, V. (2007). AIG: Accounting and Ethical Lapses. In Insurance Ethics for a More Ethical World (pp. 39-53). Emerald Group Publishing

Limited.

• nbcnews, (2010). Gen Re settles AIG fraud claims fo $92.2m. [online] Available at: http://www.nbcnews.com/id/34959105/ns/business-us_business/t/gen-re-settles-

aig-fraud-claims-m/#.W6o32tcza1s [Accessed 25 Sep. 2018].

• Npr. (2016). NPR Choice page. [online] Available at: https://www.npr.org/2016/09/13/493721864/after-11-years-accounting-fraud-case-against-former-aig-chief-to-

begin [Accessed 25 Sep. 2018].

• securities.stanford, (2005). CONSOLIDATED SECOND AMENDED CLASS ACTION COMPLAINT. [online] Available at:

http://securities.stanford.edu/filings-documents/1033/AIG04_01/2005927_r01c_048141.pdf [Accessed 25 Sep. 2018].

• Smith, R. (2017). Former A.I.G. Executives Reach Settlement in Accounting Fraud Case. [online] Available at:

https://www.nytimes.com/2017/02/10/business/dealbook/former-aig-executives-reach-settlement-in-accounting-fraud-case.html [Accessed 25 Sep. 2018].

• Tanyi, P. N., & Smith, D. B. (2014). Busyness, expertise, and financial reporting quality of audit committee chairs and financial experts. Auditing: A Journal of Practice &

Theory, 34(2), 59-89.

1 out of 21

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.