Foundation Degree in Business and Management

VerifiedAdded on 2022/04/28

|17

|3984

|39

AI Summary

The business report will be assessed using a variety of financial methodologies, including investment appraisals from a number of different enterprises. The PBP and NPV techniques will be used to determine which investment project is most suitable for the investors out of seven options. The most prospective initiatives are Projects A and G, which are perfect for investment in K Plc.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Foundation Degree in Business and Management (Year 2)

Business Finance (BMS512)

Title: Business Report

Words: 2870

1

Business Finance (BMS512)

Title: Business Report

Words: 2870

1

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Introduction......................................................................................................................................4

Task A Table of Contents

.........................................................................................................................................................5

a) Payback Period for All Projects...............................................................................................5

b) Net Present Value for All Projects..........................................................................................5

c) Ranking the Projects Using PBP and NPV Values.................................................................6

d) The Selection of the Appropriate Project for Investment Decision (Mutually Exclusive).....6

e) Discussing Strengths and Weaknesses of PBP and NPV Methods for Investment Appraisal 7

Payback Period........................................................................................................................7

Net Present Value........................................................................................................................7

f) Five Qualitative Factors for Directors Before Making Investment Decision..........................8

Task B..............................................................................................................................................9

a) Suggesting Three Alternative Methods of Funding for K Plc.................................................9

b) Link between the above Financing Decision and Investment Decision..................................9

Task C............................................................................................................................................10

a) Preparing a Variance Analysis Statement of The Variable Cost Elements...........................10

b) Suggesting Possible Explanations for the Variances Identified............................................11

Task D............................................................................................................................................12

Distinguishing between Centralised and Decentralised Procurement.......................................12

Benefits of Centralised and Decentralised Purchasing..............................................................13

Conclusion.....................................................................................................................................15

References......................................................................................................................................16

2

Task A Table of Contents

.........................................................................................................................................................5

a) Payback Period for All Projects...............................................................................................5

b) Net Present Value for All Projects..........................................................................................5

c) Ranking the Projects Using PBP and NPV Values.................................................................6

d) The Selection of the Appropriate Project for Investment Decision (Mutually Exclusive).....6

e) Discussing Strengths and Weaknesses of PBP and NPV Methods for Investment Appraisal 7

Payback Period........................................................................................................................7

Net Present Value........................................................................................................................7

f) Five Qualitative Factors for Directors Before Making Investment Decision..........................8

Task B..............................................................................................................................................9

a) Suggesting Three Alternative Methods of Funding for K Plc.................................................9

b) Link between the above Financing Decision and Investment Decision..................................9

Task C............................................................................................................................................10

a) Preparing a Variance Analysis Statement of The Variable Cost Elements...........................10

b) Suggesting Possible Explanations for the Variances Identified............................................11

Task D............................................................................................................................................12

Distinguishing between Centralised and Decentralised Procurement.......................................12

Benefits of Centralised and Decentralised Purchasing..............................................................13

Conclusion.....................................................................................................................................15

References......................................................................................................................................16

2

Table of Figures

Figure 1: Payback Period for all Projects (source: self-calculated).................................................5

Figure 2: Net Present Value for All Projects (Source: self-calculated)...........................................5

Figure 3: Variance Analysis for K plc (source: self-included)......................................................11

3

Figure 1: Payback Period for all Projects (source: self-calculated).................................................5

Figure 2: Net Present Value for All Projects (Source: self-calculated)...........................................5

Figure 3: Variance Analysis for K plc (source: self-included)......................................................11

3

Introduction

The business report will be evaluated in light of various financial techniques, including

investment appraisals from several projects. Among seven investment projects, the PBP and

NPV methodologies will be utilised to identify which investment project is the most suited for

the investors. Projects A and G, which are the ideal projects for investment in K Plc, are among

the most promising. In addition, the variance analysis for K Plc is addressed in the evaluation,

with the majority of the variance analysis, such as materials, labour, and variable overhead,

requiring more control and oversight from the management. Along with the necessity of

centralised procurement, decentralised procurement will be covered for the organisation. There

are various benefits to centralised and decentralised buying, which every company organisation

should examine before adopting a procurement management option.

4

The business report will be evaluated in light of various financial techniques, including

investment appraisals from several projects. Among seven investment projects, the PBP and

NPV methodologies will be utilised to identify which investment project is the most suited for

the investors. Projects A and G, which are the ideal projects for investment in K Plc, are among

the most promising. In addition, the variance analysis for K Plc is addressed in the evaluation,

with the majority of the variance analysis, such as materials, labour, and variable overhead,

requiring more control and oversight from the management. Along with the necessity of

centralised procurement, decentralised procurement will be covered for the organisation. There

are various benefits to centralised and decentralised buying, which every company organisation

should examine before adopting a procurement management option.

4

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Task A

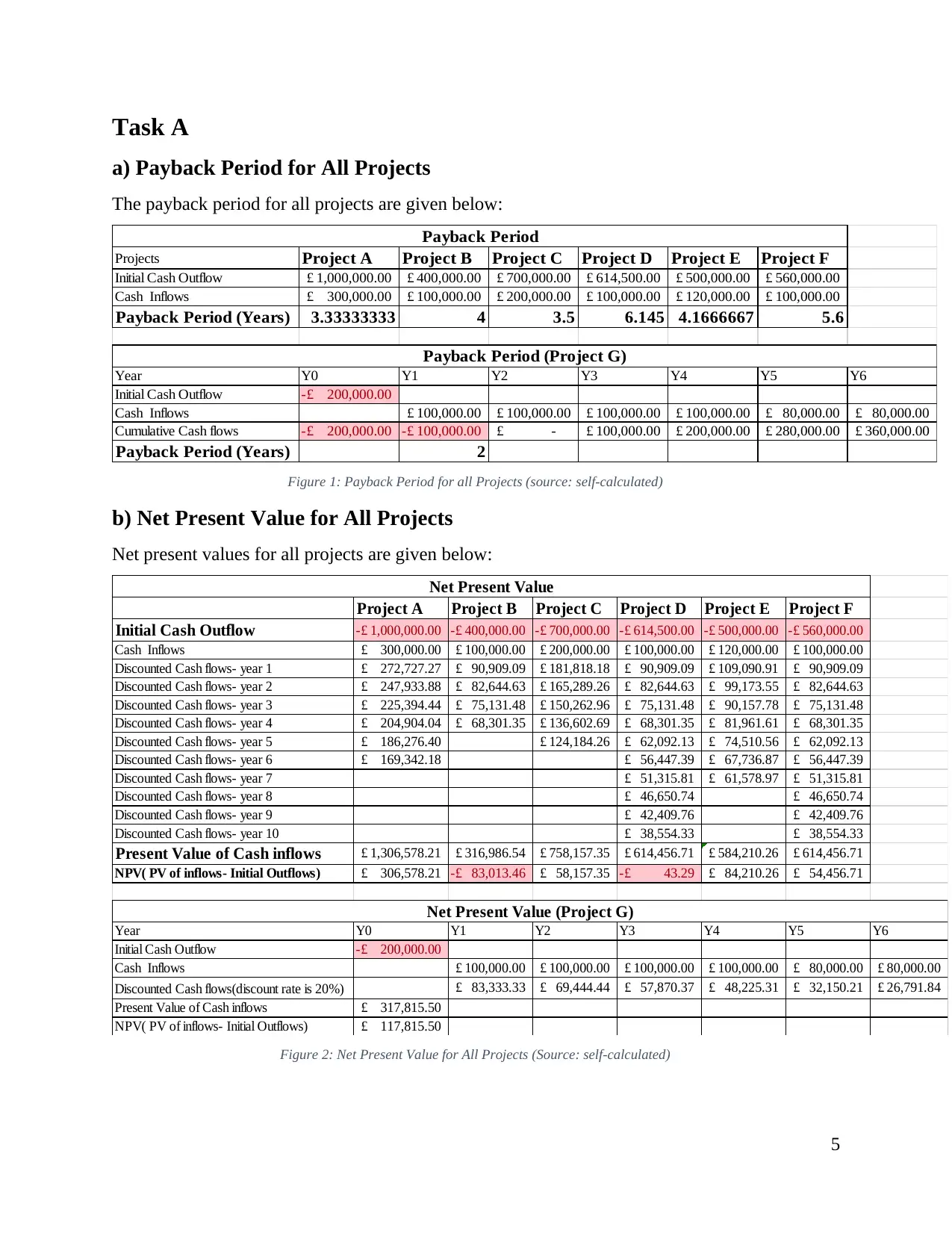

a) Payback Period for All Projects

The payback period for all projects are given below:

Projects Project A Project B Project C Project D Project E Project F

Initial Cash Outflow 1,000,000.00£ 400,000.00£ 700,000.00£ 614,500.00£ 500,000.00£ 560,000.00£

Cash Inflows 300,000.00£ 100,000.00£ 200,000.00£ 100,000.00£ 120,000.00£ 100,000.00£

Payback Period (Years) 3.33333333 4 3.5 6.145 4.1666667 5.6

Year Y0 Y1 Y2 Y3 Y4 Y5 Y6

Initial Cash Outflow 200,000.00-£

Cash Inflows 100,000.00£ 100,000.00£ 100,000.00£ 100,000.00£ 80,000.00£ 80,000.00£

Cumulative Cash flows 200,000.00-£ 100,000.00-£ -£ 100,000.00£ 200,000.00£ 280,000.00£ 360,000.00£

Payback Period (Years) 2

Payback Period

Payback Period (Project G)

Figure 1: Payback Period for all Projects (source: self-calculated)

b) Net Present Value for All Projects

Net present values for all projects are given below:

Project A Project B Project C Project D Project E Project F

Initial Cash Outflow 1,000,000.00-£ 400,000.00-£ 700,000.00-£ 614,500.00-£ 500,000.00-£ 560,000.00-£

Cash Inflows 300,000.00£ 100,000.00£ 200,000.00£ 100,000.00£ 120,000.00£ 100,000.00£

Discounted Cash flows- year 1 272,727.27£ 90,909.09£ 181,818.18£ 90,909.09£ 109,090.91£ 90,909.09£

Discounted Cash flows- year 2 247,933.88£ 82,644.63£ 165,289.26£ 82,644.63£ 99,173.55£ 82,644.63£

Discounted Cash flows- year 3 225,394.44£ 75,131.48£ 150,262.96£ 75,131.48£ 90,157.78£ 75,131.48£

Discounted Cash flows- year 4 204,904.04£ 68,301.35£ 136,602.69£ 68,301.35£ 81,961.61£ 68,301.35£

Discounted Cash flows- year 5 186,276.40£ 124,184.26£ 62,092.13£ 74,510.56£ 62,092.13£

Discounted Cash flows- year 6 169,342.18£ 56,447.39£ 67,736.87£ 56,447.39£

Discounted Cash flows- year 7 51,315.81£ 61,578.97£ 51,315.81£

Discounted Cash flows- year 8 46,650.74£ 46,650.74£

Discounted Cash flows- year 9 42,409.76£ 42,409.76£

Discounted Cash flows- year 10 38,554.33£ 38,554.33£

Present Value of Cash inflows 1,306,578.21£ 316,986.54£ 758,157.35£ 614,456.71£ 584,210.26£ 614,456.71£

NPV( PV of inflows- Initial Outflows) 306,578.21£ 83,013.46-£ 58,157.35£ 43.29-£ 84,210.26£ 54,456.71£

Year Y0 Y1 Y2 Y3 Y4 Y5 Y6

Initial Cash Outflow 200,000.00-£

Cash Inflows 100,000.00£ 100,000.00£ 100,000.00£ 100,000.00£ 80,000.00£ 80,000.00£

Discounted Cash flows(discount rate is 20%) 83,333.33£ 69,444.44£ 57,870.37£ 48,225.31£ 32,150.21£ 26,791.84£

Present Value of Cash inflows 317,815.50£

NPV( PV of inflows- Initial Outflows) 117,815.50£

Net Present Value

Net Present Value (Project G)

Figure 2: Net Present Value for All Projects (Source: self-calculated)

5

a) Payback Period for All Projects

The payback period for all projects are given below:

Projects Project A Project B Project C Project D Project E Project F

Initial Cash Outflow 1,000,000.00£ 400,000.00£ 700,000.00£ 614,500.00£ 500,000.00£ 560,000.00£

Cash Inflows 300,000.00£ 100,000.00£ 200,000.00£ 100,000.00£ 120,000.00£ 100,000.00£

Payback Period (Years) 3.33333333 4 3.5 6.145 4.1666667 5.6

Year Y0 Y1 Y2 Y3 Y4 Y5 Y6

Initial Cash Outflow 200,000.00-£

Cash Inflows 100,000.00£ 100,000.00£ 100,000.00£ 100,000.00£ 80,000.00£ 80,000.00£

Cumulative Cash flows 200,000.00-£ 100,000.00-£ -£ 100,000.00£ 200,000.00£ 280,000.00£ 360,000.00£

Payback Period (Years) 2

Payback Period

Payback Period (Project G)

Figure 1: Payback Period for all Projects (source: self-calculated)

b) Net Present Value for All Projects

Net present values for all projects are given below:

Project A Project B Project C Project D Project E Project F

Initial Cash Outflow 1,000,000.00-£ 400,000.00-£ 700,000.00-£ 614,500.00-£ 500,000.00-£ 560,000.00-£

Cash Inflows 300,000.00£ 100,000.00£ 200,000.00£ 100,000.00£ 120,000.00£ 100,000.00£

Discounted Cash flows- year 1 272,727.27£ 90,909.09£ 181,818.18£ 90,909.09£ 109,090.91£ 90,909.09£

Discounted Cash flows- year 2 247,933.88£ 82,644.63£ 165,289.26£ 82,644.63£ 99,173.55£ 82,644.63£

Discounted Cash flows- year 3 225,394.44£ 75,131.48£ 150,262.96£ 75,131.48£ 90,157.78£ 75,131.48£

Discounted Cash flows- year 4 204,904.04£ 68,301.35£ 136,602.69£ 68,301.35£ 81,961.61£ 68,301.35£

Discounted Cash flows- year 5 186,276.40£ 124,184.26£ 62,092.13£ 74,510.56£ 62,092.13£

Discounted Cash flows- year 6 169,342.18£ 56,447.39£ 67,736.87£ 56,447.39£

Discounted Cash flows- year 7 51,315.81£ 61,578.97£ 51,315.81£

Discounted Cash flows- year 8 46,650.74£ 46,650.74£

Discounted Cash flows- year 9 42,409.76£ 42,409.76£

Discounted Cash flows- year 10 38,554.33£ 38,554.33£

Present Value of Cash inflows 1,306,578.21£ 316,986.54£ 758,157.35£ 614,456.71£ 584,210.26£ 614,456.71£

NPV( PV of inflows- Initial Outflows) 306,578.21£ 83,013.46-£ 58,157.35£ 43.29-£ 84,210.26£ 54,456.71£

Year Y0 Y1 Y2 Y3 Y4 Y5 Y6

Initial Cash Outflow 200,000.00-£

Cash Inflows 100,000.00£ 100,000.00£ 100,000.00£ 100,000.00£ 80,000.00£ 80,000.00£

Discounted Cash flows(discount rate is 20%) 83,333.33£ 69,444.44£ 57,870.37£ 48,225.31£ 32,150.21£ 26,791.84£

Present Value of Cash inflows 317,815.50£

NPV( PV of inflows- Initial Outflows) 117,815.50£

Net Present Value

Net Present Value (Project G)

Figure 2: Net Present Value for All Projects (Source: self-calculated)

5

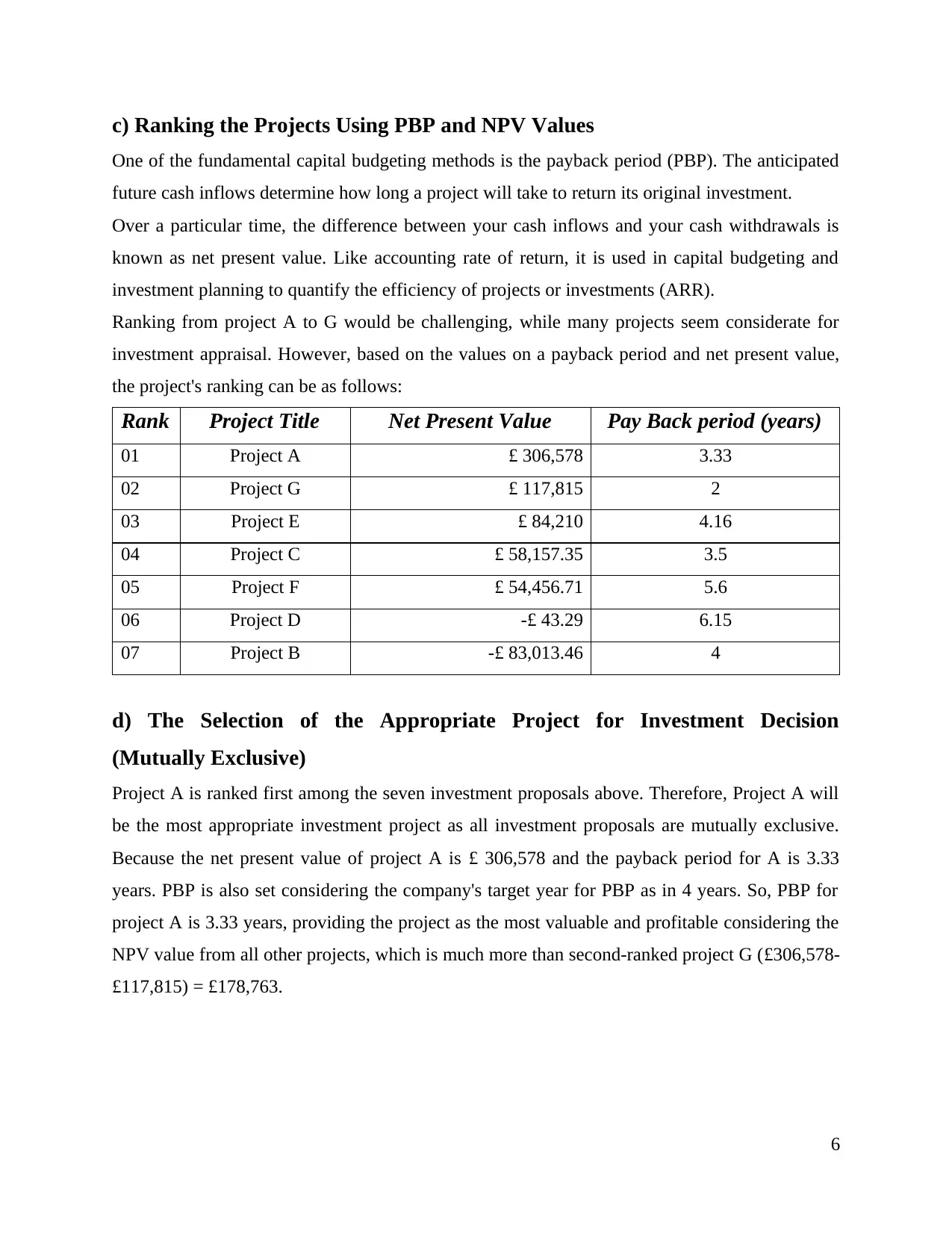

c) Ranking the Projects Using PBP and NPV Values

One of the fundamental capital budgeting methods is the payback period (PBP). The anticipated

future cash inflows determine how long a project will take to return its original investment.

Over a particular time, the difference between your cash inflows and your cash withdrawals is

known as net present value. Like accounting rate of return, it is used in capital budgeting and

investment planning to quantify the efficiency of projects or investments (ARR).

Ranking from project A to G would be challenging, while many projects seem considerate for

investment appraisal. However, based on the values on a payback period and net present value,

the project's ranking can be as follows:

Rank Project Title Net Present Value Pay Back period (years)

01 Project A £ 306,578 3.33

02 Project G £ 117,815 2

03 Project E £ 84,210 4.16

04 Project C £ 58,157.35 3.5

05 Project F £ 54,456.71 5.6

06 Project D -£ 43.29 6.15

07 Project B -£ 83,013.46 4

d) The Selection of the Appropriate Project for Investment Decision

(Mutually Exclusive)

Project A is ranked first among the seven investment proposals above. Therefore, Project A will

be the most appropriate investment project as all investment proposals are mutually exclusive.

Because the net present value of project A is £ 306,578 and the payback period for A is 3.33

years. PBP is also set considering the company's target year for PBP as in 4 years. So, PBP for

project A is 3.33 years, providing the project as the most valuable and profitable considering the

NPV value from all other projects, which is much more than second-ranked project G (£306,578-

£117,815) = £178,763.

6

One of the fundamental capital budgeting methods is the payback period (PBP). The anticipated

future cash inflows determine how long a project will take to return its original investment.

Over a particular time, the difference between your cash inflows and your cash withdrawals is

known as net present value. Like accounting rate of return, it is used in capital budgeting and

investment planning to quantify the efficiency of projects or investments (ARR).

Ranking from project A to G would be challenging, while many projects seem considerate for

investment appraisal. However, based on the values on a payback period and net present value,

the project's ranking can be as follows:

Rank Project Title Net Present Value Pay Back period (years)

01 Project A £ 306,578 3.33

02 Project G £ 117,815 2

03 Project E £ 84,210 4.16

04 Project C £ 58,157.35 3.5

05 Project F £ 54,456.71 5.6

06 Project D -£ 43.29 6.15

07 Project B -£ 83,013.46 4

d) The Selection of the Appropriate Project for Investment Decision

(Mutually Exclusive)

Project A is ranked first among the seven investment proposals above. Therefore, Project A will

be the most appropriate investment project as all investment proposals are mutually exclusive.

Because the net present value of project A is £ 306,578 and the payback period for A is 3.33

years. PBP is also set considering the company's target year for PBP as in 4 years. So, PBP for

project A is 3.33 years, providing the project as the most valuable and profitable considering the

NPV value from all other projects, which is much more than second-ranked project G (£306,578-

£117,815) = £178,763.

6

e) Discussing Strengths and Weaknesses of PBP and NPV Methods for

Investment Appraisal

Payback Period

Once a project's net cash flows match the project's original investment, the payback period is

complete. As an initial screening procedure, this technique is often used to estimate how long it

will take to recoup an investment's original financial expenditure (Burns, 2014).

Strengths of PBP: Pay Back Period requires fewer inputs and is simpler to compute than other

capital budgeting techniques. The payback time is calculated using the project's original cost and

yearly cash flows. Other approaches utilise the same inputs but need extra assumptions. Like the

cost of capital, other methodologies require managers to make assumptions. No other capital

budgeting tool provides the payback period (Agung, Hasnawati & Huzaimah, 2021). A project

with a shorter payback time is usually less risky. Uncertainty makes forecasting future yearly

cash inflows challenging. Using and completing projects with short PBP reduces the risk of loss

due to obsolescence. Managers can easily determine the payback time of initiatives since it is

simple to compute. This aids managers in making rapid judgments, which is vital in firms with

limited resources.

Weaknesses of PBP: The payback period overlooks the time worth of money, which is a crucial

weakness for any investment tool. The money obtained sooner is worth more than the money

received later because it may be reinvested and yield a higher return. The PBP technique ignores

this, misrepresenting the real worth of cash flows. Here's a workaround. The Discounted

Payback Period may eliminate this disadvantage. The payback technique solely examines cash

flows up to the first investment. It ignores future cash flows. You may miss out on a project that

might create significant revenue flows later. A project's payback time is not a guarantee of

profitability (Mclaney, 2017). In both circumstances, the project would be unprofitable after

repayment. Project return on investment is ignored - certain organisations need capital

investments to produce returns far over a specific rate. And if not, it's a bust, But the payback

technique overlooks the project's ROI.

Net Present Value

NPV involves the comparison of future cash flows (benefits) to the capital needed now. This

means the project meets or surpasses your "hurdle" rate or projected rate of return.

7

Investment Appraisal

Payback Period

Once a project's net cash flows match the project's original investment, the payback period is

complete. As an initial screening procedure, this technique is often used to estimate how long it

will take to recoup an investment's original financial expenditure (Burns, 2014).

Strengths of PBP: Pay Back Period requires fewer inputs and is simpler to compute than other

capital budgeting techniques. The payback time is calculated using the project's original cost and

yearly cash flows. Other approaches utilise the same inputs but need extra assumptions. Like the

cost of capital, other methodologies require managers to make assumptions. No other capital

budgeting tool provides the payback period (Agung, Hasnawati & Huzaimah, 2021). A project

with a shorter payback time is usually less risky. Uncertainty makes forecasting future yearly

cash inflows challenging. Using and completing projects with short PBP reduces the risk of loss

due to obsolescence. Managers can easily determine the payback time of initiatives since it is

simple to compute. This aids managers in making rapid judgments, which is vital in firms with

limited resources.

Weaknesses of PBP: The payback period overlooks the time worth of money, which is a crucial

weakness for any investment tool. The money obtained sooner is worth more than the money

received later because it may be reinvested and yield a higher return. The PBP technique ignores

this, misrepresenting the real worth of cash flows. Here's a workaround. The Discounted

Payback Period may eliminate this disadvantage. The payback technique solely examines cash

flows up to the first investment. It ignores future cash flows. You may miss out on a project that

might create significant revenue flows later. A project's payback time is not a guarantee of

profitability (Mclaney, 2017). In both circumstances, the project would be unprofitable after

repayment. Project return on investment is ignored - certain organisations need capital

investments to produce returns far over a specific rate. And if not, it's a bust, But the payback

technique overlooks the project's ROI.

Net Present Value

NPV involves the comparison of future cash flows (benefits) to the capital needed now. This

means the project meets or surpasses your "hurdle" rate or projected rate of return.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Strengths of NPV: NPV is a clear metric using the discount rate; it calculates the present value

of the anticipated investment (Mendell, 2020). NPV measures investment magnitude. Compare

minor forestry investments to billion-dollar initiatives or acquisitions. NPV is easy to calculate

using a spreadsheet (Investopedia, 2022). No non-cash costs like depreciation are included in

NPV. Unlike CAGR or a simple payback period, NPV acknowledges the temporal value of

money. This is crucial for long-term forestry investments. NPVs pile up. If you have numerous

projects and surplus funds, you may sum them together to see the total wealth created.

Weaknesses of NPV: It is necessary to choose a discount rate. Furthermore, the net present

value (NPV) presupposes that the discount rate remains constant throughout the life of the

investment or project. Unlike interest rates, which remain constant yearly, discount rates

fluctuate. Depending on the investor, opportunity costs might fluctuate and vary significantly. If

you can reliably analyse and estimate future cash flows, you can calculate the net present value

(NPV). On the other hand, "my crystal ball has sometimes shown flaws, but yours may be

unbreakable" - The notion might be challenging for some people to understand since it is not

instantly obvious (Investopedia, 2022).

f) Five Qualitative Factors for Directors Before Making Investment Decision

All company investments are fraught with risk, which is possible that the desired result may not

materialise. An investment must provide a sufficient return to compensate for the risk.

The duration of the project: The greater the project's duration, the higher the likelihood that

projected revenues, expenses, and cash flows may show to be unrealistic.

The source of information: If the management estimates project earnings and cash flows, the

investors should profile all the sources of this information about the suitable project needs to be

considered whether they are appropriate or not.

The amount of money that will be invested: A project that consumes a significant amount of

the available business finances is, by definition, riskier than a project that consumes a lesser

fraction of the available company funds. Furthermore, the risk is concerned with the

ramifications to a firm should anything go wrong (Benaroch & Dhar, 2010).

The current economic and market situation: This is a significant concern for most big

investments. Most initiatives will make assumptions about demand, expenses, pricing, and other

factors that may become spectacularly wrong due to shifting market and economic

circumstances.

8

of the anticipated investment (Mendell, 2020). NPV measures investment magnitude. Compare

minor forestry investments to billion-dollar initiatives or acquisitions. NPV is easy to calculate

using a spreadsheet (Investopedia, 2022). No non-cash costs like depreciation are included in

NPV. Unlike CAGR or a simple payback period, NPV acknowledges the temporal value of

money. This is crucial for long-term forestry investments. NPVs pile up. If you have numerous

projects and surplus funds, you may sum them together to see the total wealth created.

Weaknesses of NPV: It is necessary to choose a discount rate. Furthermore, the net present

value (NPV) presupposes that the discount rate remains constant throughout the life of the

investment or project. Unlike interest rates, which remain constant yearly, discount rates

fluctuate. Depending on the investor, opportunity costs might fluctuate and vary significantly. If

you can reliably analyse and estimate future cash flows, you can calculate the net present value

(NPV). On the other hand, "my crystal ball has sometimes shown flaws, but yours may be

unbreakable" - The notion might be challenging for some people to understand since it is not

instantly obvious (Investopedia, 2022).

f) Five Qualitative Factors for Directors Before Making Investment Decision

All company investments are fraught with risk, which is possible that the desired result may not

materialise. An investment must provide a sufficient return to compensate for the risk.

The duration of the project: The greater the project's duration, the higher the likelihood that

projected revenues, expenses, and cash flows may show to be unrealistic.

The source of information: If the management estimates project earnings and cash flows, the

investors should profile all the sources of this information about the suitable project needs to be

considered whether they are appropriate or not.

The amount of money that will be invested: A project that consumes a significant amount of

the available business finances is, by definition, riskier than a project that consumes a lesser

fraction of the available company funds. Furthermore, the risk is concerned with the

ramifications to a firm should anything go wrong (Benaroch & Dhar, 2010).

The current economic and market situation: This is a significant concern for most big

investments. Most initiatives will make assumptions about demand, expenses, pricing, and other

factors that may become spectacularly wrong due to shifting market and economic

circumstances.

8

Knowledge of the management team: The executive staff has a wealth of knowledge and

expertise. Compared to projects involving the company entering a new market, projects carried

out in markets where the management team has extensive expertise are lower-risk propositions

(Gusni, Silviana & Hamdani, 2018).

Task B

a) Suggesting Three Alternative Methods of Funding for K Plc

To enter new markets or regions, support R&D, or stay one step ahead of the competition,

companies often turn to the outside world for financial assistance. While organisations generally

try to leverage the cash flow from their current operations to support these initiatives, it is

sometimes more advantageous to look for other funding sources.

Debenture/ Debt Capital

When a company prefers debt over equity, debentures are a frequent form of financing.

Compared to equity, debt is seen as a more cost-effective form of financing. Investors do not

have a say in how the company is run (BBC Bitesize, 2022). Because the interest paid to

debenture holders is tax-deductible, it is advantageous. Debentures are issued in much the same

way that stock is. Because it is available to the general public, all applicable laws and regulations

must be followed. Some of the firm's assets are used to collateralise the issue of debentures,

which also have a cost to the company.

Term Loan/ Bank Loan

Term loans or bank loans have many of the same qualities as debentures, except they are issued

at a lower cost since a financial institution provides them. The general public has no say in the

matter. Debt servicing capability is determined by thoroughly examining the bank's finances and

plans. There is a collateral requirement for these loans, as well.

Venture Capital

In return for a portion of the company's revenues, venture capitalists and business angels are

prepared to put money into a start-up or a developing enterprise. Investors will want a return on

their money and control over its operations. Similar to stock shares, but with a distinct group of

individuals as investors. Known as "venture capitalists," these investors often make early

investments in start-up companies after doing thorough due diligence on the business.

9

expertise. Compared to projects involving the company entering a new market, projects carried

out in markets where the management team has extensive expertise are lower-risk propositions

(Gusni, Silviana & Hamdani, 2018).

Task B

a) Suggesting Three Alternative Methods of Funding for K Plc

To enter new markets or regions, support R&D, or stay one step ahead of the competition,

companies often turn to the outside world for financial assistance. While organisations generally

try to leverage the cash flow from their current operations to support these initiatives, it is

sometimes more advantageous to look for other funding sources.

Debenture/ Debt Capital

When a company prefers debt over equity, debentures are a frequent form of financing.

Compared to equity, debt is seen as a more cost-effective form of financing. Investors do not

have a say in how the company is run (BBC Bitesize, 2022). Because the interest paid to

debenture holders is tax-deductible, it is advantageous. Debentures are issued in much the same

way that stock is. Because it is available to the general public, all applicable laws and regulations

must be followed. Some of the firm's assets are used to collateralise the issue of debentures,

which also have a cost to the company.

Term Loan/ Bank Loan

Term loans or bank loans have many of the same qualities as debentures, except they are issued

at a lower cost since a financial institution provides them. The general public has no say in the

matter. Debt servicing capability is determined by thoroughly examining the bank's finances and

plans. There is a collateral requirement for these loans, as well.

Venture Capital

In return for a portion of the company's revenues, venture capitalists and business angels are

prepared to put money into a start-up or a developing enterprise. Investors will want a return on

their money and control over its operations. Similar to stock shares, but with a distinct group of

individuals as investors. Known as "venture capitalists," these investors often make early

investments in start-up companies after doing thorough due diligence on the business.

9

b) Link between the above Financing Decision and Investment Decision

Making smart financial decisions is critical to a company's function and flourishing. It is logical

to believe that private and public companies make specific investment and finance decisions

because of their differing levels of regulation and opportunity (Agung, Hasnawati & Huzaimah,

2021). Decision-making in financial management is a topic that occupies a significant place in

contemporary finance thought because it is critical to achieving goals such as maximisation of

profits and shareholder wealth while at the same time ensuring the long-term viability of

businesses and financial institutions (Drobetz, Janzen & Meier, 2016). Decisions on how to

improve shareholder wealth, boost profitability, and build financial strategies based on rules set

for the value-added market must be made by enterprises.

For any organisation like K Plc to develop or persist, it is critical to have a good investment,

finance, or dividend payout resolution. Investment and finance choices are two distinct types of

financial decisions (Chiarella, Pham, Sim & Tan, 2012). There are a variety of investment

projects to choose from, including short-term projects and long-term projects, and any

investment proposal put in front of the directors is evaluated and approved by the board of

directors based on specific methods for evaluating investment projects, which take into account

that the facility's primary goal is to increase the wealth of its owners (Nazar, 2021).

Task C

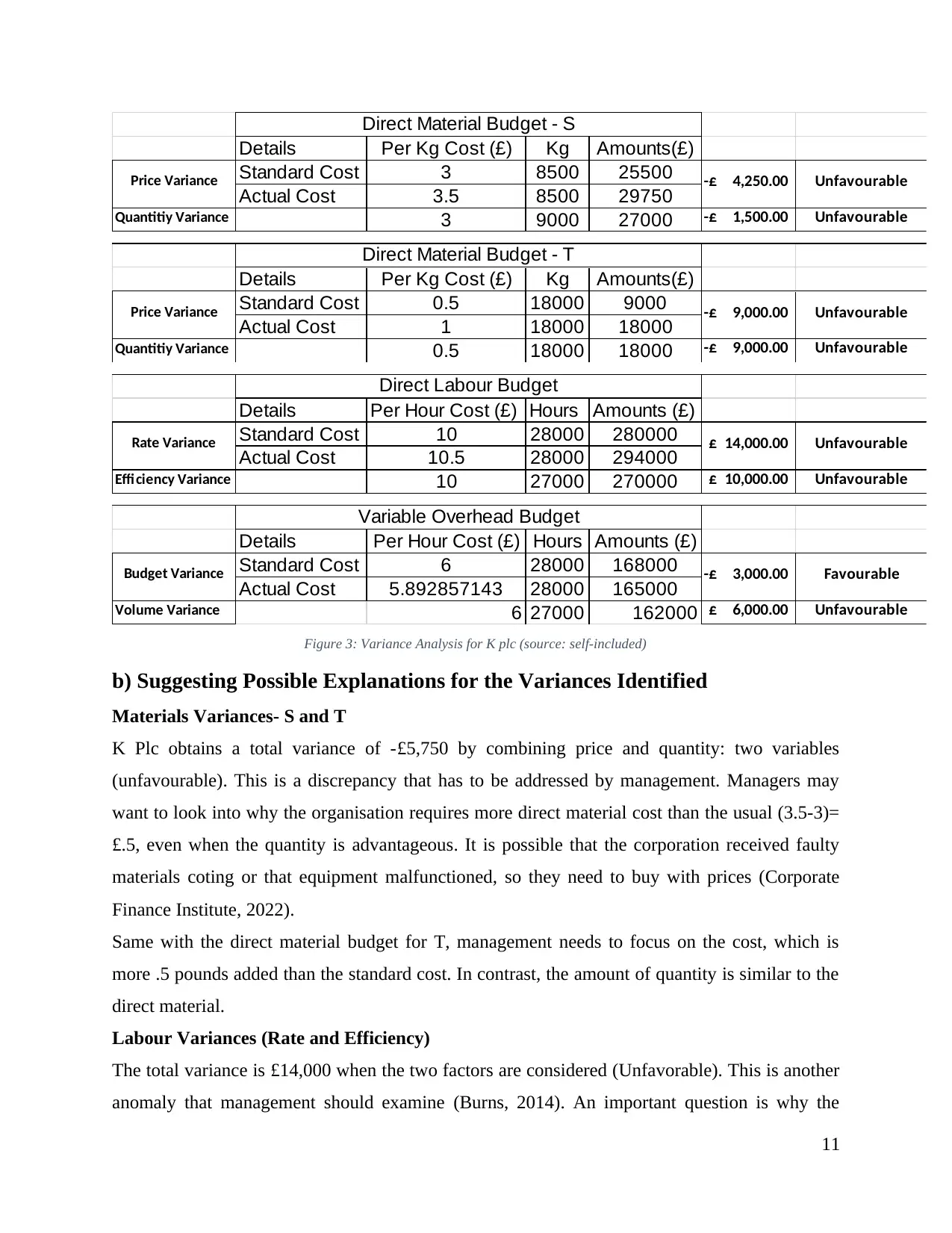

a) Preparing a Variance Analysis Statement of The Variable Cost Elements

A variance analysis statement for K Plc is attached in the following:

10

Making smart financial decisions is critical to a company's function and flourishing. It is logical

to believe that private and public companies make specific investment and finance decisions

because of their differing levels of regulation and opportunity (Agung, Hasnawati & Huzaimah,

2021). Decision-making in financial management is a topic that occupies a significant place in

contemporary finance thought because it is critical to achieving goals such as maximisation of

profits and shareholder wealth while at the same time ensuring the long-term viability of

businesses and financial institutions (Drobetz, Janzen & Meier, 2016). Decisions on how to

improve shareholder wealth, boost profitability, and build financial strategies based on rules set

for the value-added market must be made by enterprises.

For any organisation like K Plc to develop or persist, it is critical to have a good investment,

finance, or dividend payout resolution. Investment and finance choices are two distinct types of

financial decisions (Chiarella, Pham, Sim & Tan, 2012). There are a variety of investment

projects to choose from, including short-term projects and long-term projects, and any

investment proposal put in front of the directors is evaluated and approved by the board of

directors based on specific methods for evaluating investment projects, which take into account

that the facility's primary goal is to increase the wealth of its owners (Nazar, 2021).

Task C

a) Preparing a Variance Analysis Statement of The Variable Cost Elements

A variance analysis statement for K Plc is attached in the following:

10

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Details Per Kg Cost (£) Kg Amounts(£)

Standard Cost 3 8500 25500

Actual Cost 3.5 8500 29750

Quantitiy Variance 3 9000 27000 1,500.00-£ Unfavourable

UnfavourablePrice Variance

Direct Material Budget - S

4,250.00-£

Details Per Kg Cost (£) Kg Amounts(£)

Standard Cost 0.5 18000 9000

Actual Cost 1 18000 18000

Quantitiy Variance 0.5 18000 18000 9,000.00-£ Unfavourable

Price Variance 9,000.00-£ Unfavourable

Direct Material Budget - T

Details Per Hour Cost (£) Hours Amounts (£)

Standard Cost 10 28000 280000

Actual Cost 10.5 28000 294000

Efficiency Variance 10 27000 270000 10,000.00£ Unfavourable

Rate Variance 14,000.00£ Unfavourable

Direct Labour Budget

Details Per Hour Cost (£) Hours Amounts (£)

Standard Cost 6 28000 168000

Actual Cost 5.892857143 28000 165000

Volume Variance 6 27000 162000 6,000.00£ Unfavourable

Budget Variance 3,000.00-£ Favourable

Variable Overhead Budget

Figure 3: Variance Analysis for K plc (source: self-included)

b) Suggesting Possible Explanations for the Variances Identified

Materials Variances- S and T

K Plc obtains a total variance of -£5,750 by combining price and quantity: two variables

(unfavourable). This is a discrepancy that has to be addressed by management. Managers may

want to look into why the organisation requires more direct material cost than the usual (3.5-3)=

£.5, even when the quantity is advantageous. It is possible that the corporation received faulty

materials coting or that equipment malfunctioned, so they need to buy with prices (Corporate

Finance Institute, 2022).

Same with the direct material budget for T, management needs to focus on the cost, which is

more .5 pounds added than the standard cost. In contrast, the amount of quantity is similar to the

direct material.

Labour Variances (Rate and Efficiency)

The total variance is £14,000 when the two factors are considered (Unfavorable). This is another

anomaly that management should examine (Burns, 2014). An important question is why the

11

Standard Cost 3 8500 25500

Actual Cost 3.5 8500 29750

Quantitiy Variance 3 9000 27000 1,500.00-£ Unfavourable

UnfavourablePrice Variance

Direct Material Budget - S

4,250.00-£

Details Per Kg Cost (£) Kg Amounts(£)

Standard Cost 0.5 18000 9000

Actual Cost 1 18000 18000

Quantitiy Variance 0.5 18000 18000 9,000.00-£ Unfavourable

Price Variance 9,000.00-£ Unfavourable

Direct Material Budget - T

Details Per Hour Cost (£) Hours Amounts (£)

Standard Cost 10 28000 280000

Actual Cost 10.5 28000 294000

Efficiency Variance 10 27000 270000 10,000.00£ Unfavourable

Rate Variance 14,000.00£ Unfavourable

Direct Labour Budget

Details Per Hour Cost (£) Hours Amounts (£)

Standard Cost 6 28000 168000

Actual Cost 5.892857143 28000 165000

Volume Variance 6 27000 162000 6,000.00£ Unfavourable

Budget Variance 3,000.00-£ Favourable

Variable Overhead Budget

Figure 3: Variance Analysis for K plc (source: self-included)

b) Suggesting Possible Explanations for the Variances Identified

Materials Variances- S and T

K Plc obtains a total variance of -£5,750 by combining price and quantity: two variables

(unfavourable). This is a discrepancy that has to be addressed by management. Managers may

want to look into why the organisation requires more direct material cost than the usual (3.5-3)=

£.5, even when the quantity is advantageous. It is possible that the corporation received faulty

materials coting or that equipment malfunctioned, so they need to buy with prices (Corporate

Finance Institute, 2022).

Same with the direct material budget for T, management needs to focus on the cost, which is

more .5 pounds added than the standard cost. In contrast, the amount of quantity is similar to the

direct material.

Labour Variances (Rate and Efficiency)

The total variance is £14,000 when the two factors are considered (Unfavorable). This is another

anomaly that management should examine (Burns, 2014). An important question is why the

11

actual labour price is half a pound more than the norm and why an additional 1,000 hours of

manufacturing are necessary. In addition to variable overhead expenses, the column technique

may be used to track fixed overhead costs.

Variable Overhead Expenses

The overall unfavourable variance is £3,000 when the budget and volume variances are added

together. Again, this is something management should consider. This is another strange

occurrence that needs to be investigated by upper management. It's crucial to examine why the

additional variable expense is lower than the usual and why an extra 1,000 hours of manufacture

are required, which adds the more unfavourable costing in labour variance analysis and variable

overhead variance analysis.

Task D

Distinguishing between Centralised and Decentralised Procurement

Procurement may be centralised or decentralised, depending on the company's needs and the

location of the buying department. A leader's operational model will be evaluated as a company

grows and matures to see its performance. The differences between centralised and decentralised

procurement are discussed in the following.

Centralised procurement refers to buying control at the corporate level, while decentralised

procurement refers to purchasing across several business units and locations. CPOs must

regularly re-evaluate their structure and goals to align with stakeholders, particularly when

beginning any transformation initiative (Vagstad, 2010). Leaders will examine their operational

model as procurement organisations evolve to see its performance. In full centralisation, all

buying decisions are decided by a single entity, either at corporate headquarters or regional or

divisional levels. Centralised purchasing authority is better at expenditure management which

leads to scale advantages. Enhanced compliance and standardisation and a Dedicated buying

team are favourable possessions in the organisation's centralised procurement. A centralised

procurement system has better relationship management with important suppliers. Also, applying

category-wide strategies and tactics, centralised data and info management, better risk reduction,

integrated environmental, sustainability, and governance management can be more advantageous

in centralised procurement than decentralised procurement.

12

manufacturing are necessary. In addition to variable overhead expenses, the column technique

may be used to track fixed overhead costs.

Variable Overhead Expenses

The overall unfavourable variance is £3,000 when the budget and volume variances are added

together. Again, this is something management should consider. This is another strange

occurrence that needs to be investigated by upper management. It's crucial to examine why the

additional variable expense is lower than the usual and why an extra 1,000 hours of manufacture

are required, which adds the more unfavourable costing in labour variance analysis and variable

overhead variance analysis.

Task D

Distinguishing between Centralised and Decentralised Procurement

Procurement may be centralised or decentralised, depending on the company's needs and the

location of the buying department. A leader's operational model will be evaluated as a company

grows and matures to see its performance. The differences between centralised and decentralised

procurement are discussed in the following.

Centralised procurement refers to buying control at the corporate level, while decentralised

procurement refers to purchasing across several business units and locations. CPOs must

regularly re-evaluate their structure and goals to align with stakeholders, particularly when

beginning any transformation initiative (Vagstad, 2010). Leaders will examine their operational

model as procurement organisations evolve to see its performance. In full centralisation, all

buying decisions are decided by a single entity, either at corporate headquarters or regional or

divisional levels. Centralised purchasing authority is better at expenditure management which

leads to scale advantages. Enhanced compliance and standardisation and a Dedicated buying

team are favourable possessions in the organisation's centralised procurement. A centralised

procurement system has better relationship management with important suppliers. Also, applying

category-wide strategies and tactics, centralised data and info management, better risk reduction,

integrated environmental, sustainability, and governance management can be more advantageous

in centralised procurement than decentralised procurement.

12

A completely decentralised procurement system means that purchases are made by each business

unit, functional group, or geographic entity on their dime. As a result, procurement operations

are dispersed over several nations and geographical areas (Vagstad, 2010). Decentralisation is

often an issue of practicality for big, multinational corporations. A corporation with operations

worldwide may find it impractical to funnel all purchases via a single location. Supplier variety

and the growth of small and medium-sized firms (SMEs) are better supported (OECD, 2000).

Purchase choices may be made more promptly to take advantage of seasonal discounts and

prevent stock-out situations.

It is more cost-efficient to maintain interpersonal interactions on a local level in most cases.

Decentralised structures may result in poor adherence to company policies and procedures.

Teams may be unable to exchange best business practices with other business units because of

their decentralised nature (Mclaney, 2017). Key worldwide suppliers are experiencing

difficulties, resulting in a lack of consistent performance. Compared to a centralised strategy, it is

probable that the overall operational expenses of procurement will be greater. Supplier

diversification and the utilisation of locally sourced alternatives are forwarded assistance in

business by taking the model. Personal contacts and supplier knowledge are important as

decisions are made more quickly. Delivery in a short period is another comfort in decentralised

procurement. Specialisation and the local community's needs also help the decentralised

procurement in the business more efficiently than centralised procurement.

Benefits of Centralised and Decentralised Purchasing

Purchasing all necessities via a single central site is "Centralised Purchase." A similar concept is

a Decentralised Purchase, which describes how each facility purchases its supplies. Neither a

centralised nor a decentralised purchasing system must be followed blindly. Consider these

criteria before deciding whether to centralise or decentralise your purchasing department.

Suitability of Centralised Purchasing

One or more manufacturing hubs or factories are close to one another.

The plant utilises a single basic raw material or production centre to manufacture

conventional items.

Improved management of materials and storage space arrangement.

High-tech skills are used

No need for a lot of money (Mclaney, 2017).

13

unit, functional group, or geographic entity on their dime. As a result, procurement operations

are dispersed over several nations and geographical areas (Vagstad, 2010). Decentralisation is

often an issue of practicality for big, multinational corporations. A corporation with operations

worldwide may find it impractical to funnel all purchases via a single location. Supplier variety

and the growth of small and medium-sized firms (SMEs) are better supported (OECD, 2000).

Purchase choices may be made more promptly to take advantage of seasonal discounts and

prevent stock-out situations.

It is more cost-efficient to maintain interpersonal interactions on a local level in most cases.

Decentralised structures may result in poor adherence to company policies and procedures.

Teams may be unable to exchange best business practices with other business units because of

their decentralised nature (Mclaney, 2017). Key worldwide suppliers are experiencing

difficulties, resulting in a lack of consistent performance. Compared to a centralised strategy, it is

probable that the overall operational expenses of procurement will be greater. Supplier

diversification and the utilisation of locally sourced alternatives are forwarded assistance in

business by taking the model. Personal contacts and supplier knowledge are important as

decisions are made more quickly. Delivery in a short period is another comfort in decentralised

procurement. Specialisation and the local community's needs also help the decentralised

procurement in the business more efficiently than centralised procurement.

Benefits of Centralised and Decentralised Purchasing

Purchasing all necessities via a single central site is "Centralised Purchase." A similar concept is

a Decentralised Purchase, which describes how each facility purchases its supplies. Neither a

centralised nor a decentralised purchasing system must be followed blindly. Consider these

criteria before deciding whether to centralise or decentralise your purchasing department.

Suitability of Centralised Purchasing

One or more manufacturing hubs or factories are close to one another.

The plant utilises a single basic raw material or production centre to manufacture

conventional items.

Improved management of materials and storage space arrangement.

High-tech skills are used

No need for a lot of money (Mclaney, 2017).

13

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Better control over the use of resources.

The ability to conduct retail audits has been greatly improved.

Quick inventory with less expensive insurance premiums

Benefits of decentralised purchase

To begin with, the production hubs are spread apart.

Raw ingredients for various goods are produced at separate factories.

Internal transportation is less expensive.

Materials are readily available as needed.

It is less likely that the product will become obsolete.

14

The ability to conduct retail audits has been greatly improved.

Quick inventory with less expensive insurance premiums

Benefits of decentralised purchase

To begin with, the production hubs are spread apart.

Raw ingredients for various goods are produced at separate factories.

Internal transportation is less expensive.

Materials are readily available as needed.

It is less likely that the product will become obsolete.

14

Conclusion

The business report is assessed with various financial strategies, including investment appraisal

from several projects. The PBP and NPV methods determine the suitable investment project

among seven investment projects. Project A and G can be the most suitable investment in K Plc.

Also, variance analysis for K Plc is addressed in the assessment. Most of the variances like

materials, labour and variable overhead should be more controlled and checked by eh

management. The importance of centralised and decentralised procurement is also included for

the company. Centralised and decentralised purchasing has several benefits that any business

organisation should consider before making procurement management decisions.

15

The business report is assessed with various financial strategies, including investment appraisal

from several projects. The PBP and NPV methods determine the suitable investment project

among seven investment projects. Project A and G can be the most suitable investment in K Plc.

Also, variance analysis for K Plc is addressed in the assessment. Most of the variances like

materials, labour and variable overhead should be more controlled and checked by eh

management. The importance of centralised and decentralised procurement is also included for

the company. Centralised and decentralised purchasing has several benefits that any business

organisation should consider before making procurement management decisions.

15

References

Agung, G., Hasnawati, S. and Huzaimah, R., 2021. The Effect of Investment Decision,

Financing Decision, Dividend Policy on Firm Value. Jurnal Bisnis dan Manajemen, pp.1-12.

BBC Bitesize, 2022. Internal and external sources of finance - Sources of finance - Eduqas -

GCSE Business Revision - Eduqas - BBC Bitesize. [online] BBC Bitesize. Available at:

<https://www.bbc.co.uk/bitesize/guides/zj7yy9q/revision/1#:~:text=External%20sources%20of

%20finance%20refer,hire%20purchase%2C%20and%20government%20grants.> [Accessed 28

January 2022].

Benaroch, M. and Dhar, V., 2010. Controlling the complexity of investment decisions using

qualitative reasoning techniques. Decision Support Systems, 15(2), pp.115-131.

Burns, P., 2014. Business Finance. 7th ed. Elsevier Science, pp.49-189.

Chiarella, C., Pham, T., Sim, A. and Tan, M., 2012. The interaction of the financing and

investment decisions: Preliminary results in the Australian context. Asia Pacific Journal of

Management, 9(2), pp.209-229.

Corporate Finance Institute, 2022. Variance Analysis. [online] Corporate Finance Institute.

Available at: <https://corporatefinanceinstitute.com/resources/knowledge/accounting/variance-

analysis/> [Accessed 28 January 2022].

Drobetz, W., Janzen, M. and Meier, I., 2016. Investment and Financing Decisions of Private and

Public Firms. SSRN Electronic Journal,.

Gusni, Silviana and Hamdani, F., 2018. Factors affecting equity mutual fund performance:

evidence from Indonesia. Investment Management and Financial Innovations, 15(1), pp.1-9.

Investopedia, 2022. What Is the Formula for Calculating Net Present Value (NPV)?. [online]

Investopedia. Available at: <https://www.investopedia.com/ask/answers/032615/what-formula-

calculating-net-present-value-npv.asp> [Accessed 28 January 2022].

Mclaney, E., 2017. Business finance. 5th ed. Harlow, United Kingdom: Pearson Education

Limited, pp.71-212.

Mendell, B., 2020. Pros and Cons of Using Net Present Value (NPV) - Forisk. [online] Forisk.

Available at: <https://forisk.com/blog/2020/05/31/pros-and-cons-of-using-net-present-value-

npv/> [Accessed 28 January 2022].

16

Agung, G., Hasnawati, S. and Huzaimah, R., 2021. The Effect of Investment Decision,

Financing Decision, Dividend Policy on Firm Value. Jurnal Bisnis dan Manajemen, pp.1-12.

BBC Bitesize, 2022. Internal and external sources of finance - Sources of finance - Eduqas -

GCSE Business Revision - Eduqas - BBC Bitesize. [online] BBC Bitesize. Available at:

<https://www.bbc.co.uk/bitesize/guides/zj7yy9q/revision/1#:~:text=External%20sources%20of

%20finance%20refer,hire%20purchase%2C%20and%20government%20grants.> [Accessed 28

January 2022].

Benaroch, M. and Dhar, V., 2010. Controlling the complexity of investment decisions using

qualitative reasoning techniques. Decision Support Systems, 15(2), pp.115-131.

Burns, P., 2014. Business Finance. 7th ed. Elsevier Science, pp.49-189.

Chiarella, C., Pham, T., Sim, A. and Tan, M., 2012. The interaction of the financing and

investment decisions: Preliminary results in the Australian context. Asia Pacific Journal of

Management, 9(2), pp.209-229.

Corporate Finance Institute, 2022. Variance Analysis. [online] Corporate Finance Institute.

Available at: <https://corporatefinanceinstitute.com/resources/knowledge/accounting/variance-

analysis/> [Accessed 28 January 2022].

Drobetz, W., Janzen, M. and Meier, I., 2016. Investment and Financing Decisions of Private and

Public Firms. SSRN Electronic Journal,.

Gusni, Silviana and Hamdani, F., 2018. Factors affecting equity mutual fund performance:

evidence from Indonesia. Investment Management and Financial Innovations, 15(1), pp.1-9.

Investopedia, 2022. What Is the Formula for Calculating Net Present Value (NPV)?. [online]

Investopedia. Available at: <https://www.investopedia.com/ask/answers/032615/what-formula-

calculating-net-present-value-npv.asp> [Accessed 28 January 2022].

Mclaney, E., 2017. Business finance. 5th ed. Harlow, United Kingdom: Pearson Education

Limited, pp.71-212.

Mendell, B., 2020. Pros and Cons of Using Net Present Value (NPV) - Forisk. [online] Forisk.

Available at: <https://forisk.com/blog/2020/05/31/pros-and-cons-of-using-net-present-value-

npv/> [Accessed 28 January 2022].

16

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Nazar, M., 2021. Does Financing Decisions Influence Investment Decisions? Empirical

Evidence from Sri Lanka. Journal of Economics, Finance and Accounting Studies, 3(1), pp.33-

38.

OECD, 2000. SIGMA Papers. Centralised and Decentralised Public Procurement,.

Vagstad, S., 2010. Centralised vs. decentralised procurement: Does dispersed information call

for decentralised decision-making?. International Journal of Industrial Organization, 18(6),

pp.949-963.

17

Evidence from Sri Lanka. Journal of Economics, Finance and Accounting Studies, 3(1), pp.33-

38.

OECD, 2000. SIGMA Papers. Centralised and Decentralised Public Procurement,.

Vagstad, S., 2010. Centralised vs. decentralised procurement: Does dispersed information call

for decentralised decision-making?. International Journal of Industrial Organization, 18(6),

pp.949-963.

17

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.