Australian Income Tax Calculation

VerifiedAdded on 2020/02/18

|12

|3161

|130

AI Summary

This assignment presents a detailed example of calculating income tax in Australia. It outlines various components like income, allowable deductions, low-income tax offset, Medicare levy, and ultimately arrives at the total tax payable. The example is useful for understanding how Australian income tax works.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: TAXATION LAW OF AUSTRALIA

Taxation Law of Australia

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Taxation Law of Australia

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1TAXATION LAW OF AUSTRALIA

Table of Contents

Answer to Question 1:.....................................................................................................................2

Answer to Part i:..........................................................................................................................2

Answer to Part ii:.........................................................................................................................2

Answer to Part iii:........................................................................................................................3

Answer to Part iv:........................................................................................................................3

Answer to Part v:.........................................................................................................................4

Answer to Part vi:........................................................................................................................4

Answer to Part vii:.......................................................................................................................5

Answer to Part viii:......................................................................................................................5

Answer to Part ix:........................................................................................................................6

Answer to Part x:.........................................................................................................................6

Answer to Question 2:.....................................................................................................................7

References:....................................................................................................................................11

Table of Contents

Answer to Question 1:.....................................................................................................................2

Answer to Part i:..........................................................................................................................2

Answer to Part ii:.........................................................................................................................2

Answer to Part iii:........................................................................................................................3

Answer to Part iv:........................................................................................................................3

Answer to Part v:.........................................................................................................................4

Answer to Part vi:........................................................................................................................4

Answer to Part vii:.......................................................................................................................5

Answer to Part viii:......................................................................................................................5

Answer to Part ix:........................................................................................................................6

Answer to Part x:.........................................................................................................................6

Answer to Question 2:.....................................................................................................................7

References:....................................................................................................................................11

2TAXATION LAW OF AUSTRALIA

Answer to Question 1:

Answer to Part i:

The condition mainly identifies that there are pertinent benefits given to a business

analyst availing Webjet. Under the normal scenario, such benefits that the airline firms have

provided are not taken into account under taxable income, as laid out in “Taxation Ruling of TR

1999/6”. However, the ruling of Australian taxation depicts that certain criteria are evident that is

required to be met before allowing the expenditure in the form of tax exemption. The total

benefit that Webjet has provided is not taken into account under fringe benefit tax or taxable

income until such influential dynamics are proved. An association between an employer and an

employee exists, when they treat each other as family members. Moreover, the reward points are

provided to the staffs in relation to the agreement of employment. Finally, Webjet has made

certain arrangements for the flight points. However, dissection of the scenario primarily depicts

no agreement between the staffs and Webjet or the employer and Webjet, in which the benefit is

excluded from taxable income (McGregor-Lowndes 2014).

Answer to Part ii:

According to the case study, the organisation has received a pertinent compensation from

a customer in lieu of damages carried out on the capital asset. In compliance with the taxation

law of Australia, the payment of total damage could not be taken into consideration under

taxable income. In addition, there are various criteria that an organisation should follow for

excluding the payment of damage related to capital assets in the form of capital income. Initially,

the organisation needs to utilise its assets effectively that would help in minimising the taxable

income. The second measure depicts that the capital asset is listed on the annual report, in which

Answer to Question 1:

Answer to Part i:

The condition mainly identifies that there are pertinent benefits given to a business

analyst availing Webjet. Under the normal scenario, such benefits that the airline firms have

provided are not taken into account under taxable income, as laid out in “Taxation Ruling of TR

1999/6”. However, the ruling of Australian taxation depicts that certain criteria are evident that is

required to be met before allowing the expenditure in the form of tax exemption. The total

benefit that Webjet has provided is not taken into account under fringe benefit tax or taxable

income until such influential dynamics are proved. An association between an employer and an

employee exists, when they treat each other as family members. Moreover, the reward points are

provided to the staffs in relation to the agreement of employment. Finally, Webjet has made

certain arrangements for the flight points. However, dissection of the scenario primarily depicts

no agreement between the staffs and Webjet or the employer and Webjet, in which the benefit is

excluded from taxable income (McGregor-Lowndes 2014).

Answer to Part ii:

According to the case study, the organisation has received a pertinent compensation from

a customer in lieu of damages carried out on the capital asset. In compliance with the taxation

law of Australia, the payment of total damage could not be taken into consideration under

taxable income. In addition, there are various criteria that an organisation should follow for

excluding the payment of damage related to capital assets in the form of capital income. Initially,

the organisation needs to utilise its assets effectively that would help in minimising the taxable

income. The second measure depicts that the capital asset is listed on the annual report, in which

3TAXATION LAW OF AUSTRALIA

the conduction of sufficient depreciation is made. This is extremely significant, since it enables

the taxation authority of the nation in understanding that the organisation uses the capital asset

for above a fiscal year (Bryan, Vann and Thomas 2017).

Answer to Part iii:

According to the provided scenario, the manager of the nightclub has been provided with

a pertinent holiday package on the part of the alcohol supplier. The pertinent arrangement

primarily denotes that the alcohol supplier has provided a gift or benefit having relatively greater

value. In accordance with the taxation authority of Australia, the gifts of low budget are

exempted from taxable income, while the gifts of high budget are included in taxable income.

This enables in reducing any type of unscrupulous actions carried out on the part of owners and

staffs. Along with this, the scenario denotes that the holiday package has greater value, in which

the nightclub manager is needed to include benefits in the taxable income. As remarked by

McKerchar, Bloomquist and Pope (2013), the individual staffs receiving advantages from the

employers are adjudged mainly as fringe benefit tax, which is incurred on the part of the

employer.

Answer to Part iv:

According to the case study, pertinent fund is returned to the members of the Canoe Club,

since the collection of additional amount is made. The monetary return from the club is primarily

a refund and it could be adjudged as member income. In accordance with the taxation law, any

type of expenditure carried out on clubs for private entertainment is not deductible in nature.

Hence, the total fund returns could not be highlighted that the Canoe Club members have

received. It could be stated that the fund return of the members of the Canoe Club could not be

taken into account.

the conduction of sufficient depreciation is made. This is extremely significant, since it enables

the taxation authority of the nation in understanding that the organisation uses the capital asset

for above a fiscal year (Bryan, Vann and Thomas 2017).

Answer to Part iii:

According to the provided scenario, the manager of the nightclub has been provided with

a pertinent holiday package on the part of the alcohol supplier. The pertinent arrangement

primarily denotes that the alcohol supplier has provided a gift or benefit having relatively greater

value. In accordance with the taxation authority of Australia, the gifts of low budget are

exempted from taxable income, while the gifts of high budget are included in taxable income.

This enables in reducing any type of unscrupulous actions carried out on the part of owners and

staffs. Along with this, the scenario denotes that the holiday package has greater value, in which

the nightclub manager is needed to include benefits in the taxable income. As remarked by

McKerchar, Bloomquist and Pope (2013), the individual staffs receiving advantages from the

employers are adjudged mainly as fringe benefit tax, which is incurred on the part of the

employer.

Answer to Part iv:

According to the case study, pertinent fund is returned to the members of the Canoe Club,

since the collection of additional amount is made. The monetary return from the club is primarily

a refund and it could be adjudged as member income. In accordance with the taxation law, any

type of expenditure carried out on clubs for private entertainment is not deductible in nature.

Hence, the total fund returns could not be highlighted that the Canoe Club members have

received. It could be stated that the fund return of the members of the Canoe Club could not be

taken into account.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4TAXATION LAW OF AUSTRALIA

Answer to Part v:

The television organisation has paid a football player to participate in the sports field

diligently, under the circumstances that the sportsperson is responsible for adding the amount in

taxable income. The “Taxation Ruling TR 1999/17” mainly states this situation, in which it is

represented that any type of advantage that the sports person has obtained in Australia would be

adjudged as taxable income. Hence, as per the ruling, the sports person needs to take into

account the benefits provided on the part of the television firm in the taxable income and

pertinent access to the government of Australia. As stated by Lang (2014), the measure of

taxation is utilised in minimising unscrupulous measures for reducing the taxable income.

Answer to Part vi:

The circumstance many states that general costs are been directed in the building, where

applicable costs is been considered from the student. As per the Australian tax assessment law,

the circumstance for the most part expresses that student is specifically viewed as under the

remuneration of building work. The measures that are utilized as a part of distinguishing the

costs of building are delineated under the tax assessment decision of TR 95/22, where pertinent

costs and pay are straightforwardly uncovered (Barkoczy 2016). As per the tax assessment

administer applicable costs should be considered before recognizing the understudy as a building

worker. The primary measure primarily expresses that development site is looked at when as a

boss work is being led on the premises. The second measure expresses that works were utilized

for building the premises is thought to be a representative. The third measure expresses that

important learners, disciple and woodworkers are considered under the utilized works. In

addition, a development site is likewise considered where venture chief is utilized for finishing

and directing applicable measures for the development of the building. In this manner, from the

Answer to Part v:

The television organisation has paid a football player to participate in the sports field

diligently, under the circumstances that the sportsperson is responsible for adding the amount in

taxable income. The “Taxation Ruling TR 1999/17” mainly states this situation, in which it is

represented that any type of advantage that the sports person has obtained in Australia would be

adjudged as taxable income. Hence, as per the ruling, the sports person needs to take into

account the benefits provided on the part of the television firm in the taxable income and

pertinent access to the government of Australia. As stated by Lang (2014), the measure of

taxation is utilised in minimising unscrupulous measures for reducing the taxable income.

Answer to Part vi:

The circumstance many states that general costs are been directed in the building, where

applicable costs is been considered from the student. As per the Australian tax assessment law,

the circumstance for the most part expresses that student is specifically viewed as under the

remuneration of building work. The measures that are utilized as a part of distinguishing the

costs of building are delineated under the tax assessment decision of TR 95/22, where pertinent

costs and pay are straightforwardly uncovered (Barkoczy 2016). As per the tax assessment

administer applicable costs should be considered before recognizing the understudy as a building

worker. The primary measure primarily expresses that development site is looked at when as a

boss work is being led on the premises. The second measure expresses that works were utilized

for building the premises is thought to be a representative. The third measure expresses that

important learners, disciple and woodworkers are considered under the utilized works. In

addition, a development site is likewise considered where venture chief is utilized for finishing

and directing applicable measures for the development of the building. In this manner, from the

5TAXATION LAW OF AUSTRALIA

assessment it could be comprehended that costs led on student is considered as work

remuneration for the building and can be deducted in the yearly report.

Answer to Part vii:

Costs is been led on here and now course to become a workmanship executive, which has

an important arrangements in the Australian tax collection office. Short course that is utilized by

a person to improve his vocation in the brief timeframe is basically thought to be imposing

deductible cost. This sort of assessment deductible cost is just considered when the investigation

courses is short, for long examination courses there is no exemptions in the assessable pay

(Snape and De Souza 2016). Also applicable measures as delineated by the Australian tax

assessment office should be assessed by the assessable individual. At that point it is to be

insignificant instruction module and programming for the course. What's more, charges for the

course should be for brief length has applicable dinners and travel costs ought to be incorporated.

These measures are given by Australian tax assessment office should be assessed before utilizing

the fleeting course, as a duty deductible cost. Subsequently, important expense conclusion is led

by the artisanship executive, which helps in decreasing the assessable pay.

Answer to Part viii:

There are significant costs directed on both cosmetics and dresses on a person,

which is a deductible in nature as said by the Australian tax assessment office. Be that as it may,

there are sure criteria, which should be fulfilled earlier enabling the costs to be assessing

deductible. The costs led on Makeup and dresses for the performing craftsman are predominantly

deductible in nature. Additionally, performing craftsman is thought to be a mystical performer,

vocalist, on-screen character, circus entertainer, assortment craftsman, and an artist (Braithwaite

2017). Any sort of costs directed on these people are thought to be an assessment reasoning cost.

assessment it could be comprehended that costs led on student is considered as work

remuneration for the building and can be deducted in the yearly report.

Answer to Part vii:

Costs is been led on here and now course to become a workmanship executive, which has

an important arrangements in the Australian tax collection office. Short course that is utilized by

a person to improve his vocation in the brief timeframe is basically thought to be imposing

deductible cost. This sort of assessment deductible cost is just considered when the investigation

courses is short, for long examination courses there is no exemptions in the assessable pay

(Snape and De Souza 2016). Also applicable measures as delineated by the Australian tax

assessment office should be assessed by the assessable individual. At that point it is to be

insignificant instruction module and programming for the course. What's more, charges for the

course should be for brief length has applicable dinners and travel costs ought to be incorporated.

These measures are given by Australian tax assessment office should be assessed before utilizing

the fleeting course, as a duty deductible cost. Subsequently, important expense conclusion is led

by the artisanship executive, which helps in decreasing the assessable pay.

Answer to Part viii:

There are significant costs directed on both cosmetics and dresses on a person,

which is a deductible in nature as said by the Australian tax assessment office. Be that as it may,

there are sure criteria, which should be fulfilled earlier enabling the costs to be assessing

deductible. The costs led on Makeup and dresses for the performing craftsman are predominantly

deductible in nature. Additionally, performing craftsman is thought to be a mystical performer,

vocalist, on-screen character, circus entertainer, assortment craftsman, and an artist (Braithwaite

2017). Any sort of costs directed on these people are thought to be an assessment reasoning cost.

6TAXATION LAW OF AUSTRALIA

In this way, the situation expresses that significant costs are directed on cosmetics and dresses,

however no divulgence is given with respect to on whom the costs are led. Henceforth, important

suspicions are made that the consumption are led on performing craftsman, which could be

deductible from the assessable salary and enable the person to diminish the expense payable.

Answer to Part ix:

Costs directed by the person by making a trip from home to work environment, is for the

most part thought to be a movement of work (Cao et al. 2015). However there is no certain

confirmation gave in the situation which could help in distinguishing the lawfulness, where costs

are led for office purposes. The Australian tax assessment office basically expresses that any sort

of costs led by a person with the end goal of office is deductible in nature from its assessable

pay. In any case, any sort of thought process instead of office costs is not deductible under the

tax collection law in this specific situation. Along these lines, the individual needs to distinguish

real cost intention before utilizing it as assessable derivations. Saad (2014) contended that

without sufficient observing it is extremely unlikely where government could distinguish the cost

led by people in their pay impose record. Consequently, it could be expressed that if the costs

directed for office purposes then it could be deducted from the assessable pay. In any case, this

won't lessen if the costs are directed for individual utilize.

Answer to Part x:

The circumstance for the most part expresses that important costs are been led by a

person from heading out to one representative to another. This principally expresses the

individual is directing individual cost and setting out starting with one place then onto the next

looking for work, as one individual cannot be utilized by two organizations. In this manner it

could be comprehended that this sort of travel cost is an individual attempt, which can't be

In this way, the situation expresses that significant costs are directed on cosmetics and dresses,

however no divulgence is given with respect to on whom the costs are led. Henceforth, important

suspicions are made that the consumption are led on performing craftsman, which could be

deductible from the assessable salary and enable the person to diminish the expense payable.

Answer to Part ix:

Costs directed by the person by making a trip from home to work environment, is for the

most part thought to be a movement of work (Cao et al. 2015). However there is no certain

confirmation gave in the situation which could help in distinguishing the lawfulness, where costs

are led for office purposes. The Australian tax assessment office basically expresses that any sort

of costs led by a person with the end goal of office is deductible in nature from its assessable

pay. In any case, any sort of thought process instead of office costs is not deductible under the

tax collection law in this specific situation. Along these lines, the individual needs to distinguish

real cost intention before utilizing it as assessable derivations. Saad (2014) contended that

without sufficient observing it is extremely unlikely where government could distinguish the cost

led by people in their pay impose record. Consequently, it could be expressed that if the costs

directed for office purposes then it could be deducted from the assessable pay. In any case, this

won't lessen if the costs are directed for individual utilize.

Answer to Part x:

The circumstance for the most part expresses that important costs are been led by a

person from heading out to one representative to another. This principally expresses the

individual is directing individual cost and setting out starting with one place then onto the next

looking for work, as one individual cannot be utilized by two organizations. In this manner it

could be comprehended that this sort of travel cost is an individual attempt, which can't be

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW OF AUSTRALIA

deducted from the assessable salary. As per the Australian tax assessment law, the individual

can't deduct the costs from its assessable pay. Taylor and Richardson (2013) specified that with

the assistance of laws gave by the Australian tax assessment expert, the Australian government is

essentially ready to decrease the general tax avoidance directed by person. In this manner it

could be comprehended that the costs led by the person on venture out starting with one worker

then onto the next is not deductible in nature, which couldn't diminish its general assessable

salary.

Answer to Question 2:

The provisions of the Income Tax Assessment Ac 1936 and 1997 govern the

determination of income tax payable in Australia. In addition to this the Taxation Rulings,

judgment of the cases and the ATO interpretive directions also plays an important role in

ascertaining the income tax liability of the taxpayer. The section 4-1 of the Income tax

Assessment Act 1997 states that an individual, companies and other entities are required to pay

tax on their taxable income. The section 4-15 of the ITAA 97 states that taxable income should

be calculated by reducing the deduction that are allowed under tax from the assessable income.

The act classifies the income according to the ordinary income under section 6-5 of the Income

Tax Assessment Act 1997 and the statutory income under section 6-10 of the ITAA 97. The

section 6-5(2) and section 6-10(4) of the ITAA 97 provides that if the taxpayer is an Australian

resident in that case income from all the sources should be included in the assessable income. In

case the taxpayer is non-resident then income received from Australian, sources are included in

the assessable income. Therefore, it can be seen that it is necessary to determine the residential

status of the individual before determining the income tax liability (Pearson 2017).

deducted from the assessable salary. As per the Australian tax assessment law, the individual

can't deduct the costs from its assessable pay. Taylor and Richardson (2013) specified that with

the assistance of laws gave by the Australian tax assessment expert, the Australian government is

essentially ready to decrease the general tax avoidance directed by person. In this manner it

could be comprehended that the costs led by the person on venture out starting with one worker

then onto the next is not deductible in nature, which couldn't diminish its general assessable

salary.

Answer to Question 2:

The provisions of the Income Tax Assessment Ac 1936 and 1997 govern the

determination of income tax payable in Australia. In addition to this the Taxation Rulings,

judgment of the cases and the ATO interpretive directions also plays an important role in

ascertaining the income tax liability of the taxpayer. The section 4-1 of the Income tax

Assessment Act 1997 states that an individual, companies and other entities are required to pay

tax on their taxable income. The section 4-15 of the ITAA 97 states that taxable income should

be calculated by reducing the deduction that are allowed under tax from the assessable income.

The act classifies the income according to the ordinary income under section 6-5 of the Income

Tax Assessment Act 1997 and the statutory income under section 6-10 of the ITAA 97. The

section 6-5(2) and section 6-10(4) of the ITAA 97 provides that if the taxpayer is an Australian

resident in that case income from all the sources should be included in the assessable income. In

case the taxpayer is non-resident then income received from Australian, sources are included in

the assessable income. Therefore, it can be seen that it is necessary to determine the residential

status of the individual before determining the income tax liability (Pearson 2017).

8TAXATION LAW OF AUSTRALIA

The term Australian resident is defined under section 995-1 of the ITAA 1936 and it

means a person who is resident in Australia as per the act. The definition of the term resident

provided in section 6-1 of the ITAA 1936 mentions four tests that can be applied in determining

the residential status. The para 32 of the Taxation Ruling98/17 states that the four tests for

determining the residential status of individual are:

Determining residency according to the ordinary concept;

Test of residency based on domicile;

The 183 days test;

Superannuation test;

In this case, Manpreet came to Australia for studies and so he is not a resident according to

the ordinary concept. Therefore, his residential status should be determined by applying statutory

tests. The Para 50 of the Taxation Ruling 98/17 provides that an individual entering Australia

to take up employment opportunity or a study course for more than 6 months is considered as

resident for the purpose of tax. Therefore, based on the above discussion it can be said that

Manpreet was a resident of Australia for the purpose of tax. That means income received from

Australian sources should be included in assessable income under Division 6 of the ITAA 97.

Manpreet has enrolled in a course and has incurred substantial expenditure for the self-

education purpose. In order to determine whether the self-education expenses will be deducted is

determined by the Taxation Ruling 98/9. The section 8-1 of the ITAA 97 provides that expenses

that areconnected to self-education expenses that related to the income earning activity are

allowed as education. The Para 13 of the Taxation Ruling 98/9 states that if the income earning

activity of the taxpayer is based on certain skill and the self-education helps in improving those

kills then the expenses incurred in the self-education expenses are allowed as deduction. The

The term Australian resident is defined under section 995-1 of the ITAA 1936 and it

means a person who is resident in Australia as per the act. The definition of the term resident

provided in section 6-1 of the ITAA 1936 mentions four tests that can be applied in determining

the residential status. The para 32 of the Taxation Ruling98/17 states that the four tests for

determining the residential status of individual are:

Determining residency according to the ordinary concept;

Test of residency based on domicile;

The 183 days test;

Superannuation test;

In this case, Manpreet came to Australia for studies and so he is not a resident according to

the ordinary concept. Therefore, his residential status should be determined by applying statutory

tests. The Para 50 of the Taxation Ruling 98/17 provides that an individual entering Australia

to take up employment opportunity or a study course for more than 6 months is considered as

resident for the purpose of tax. Therefore, based on the above discussion it can be said that

Manpreet was a resident of Australia for the purpose of tax. That means income received from

Australian sources should be included in assessable income under Division 6 of the ITAA 97.

Manpreet has enrolled in a course and has incurred substantial expenditure for the self-

education purpose. In order to determine whether the self-education expenses will be deducted is

determined by the Taxation Ruling 98/9. The section 8-1 of the ITAA 97 provides that expenses

that areconnected to self-education expenses that related to the income earning activity are

allowed as education. The Para 13 of the Taxation Ruling 98/9 states that if the income earning

activity of the taxpayer is based on certain skill and the self-education helps in improving those

kills then the expenses incurred in the self-education expenses are allowed as deduction. The

9TAXATION LAW OF AUSTRALIA

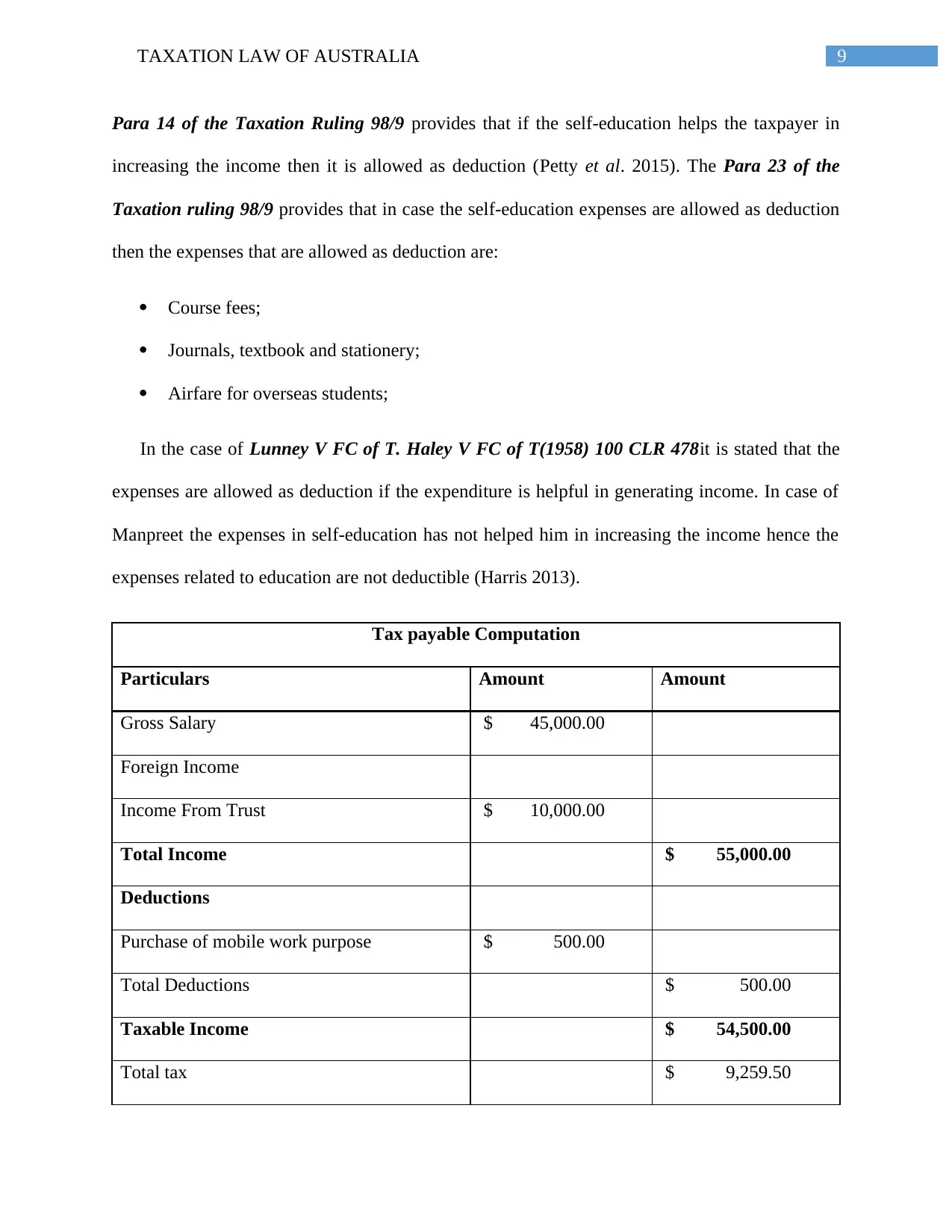

Para 14 of the Taxation Ruling 98/9 provides that if the self-education helps the taxpayer in

increasing the income then it is allowed as deduction (Petty et al. 2015). The Para 23 of the

Taxation ruling 98/9 provides that in case the self-education expenses are allowed as deduction

then the expenses that are allowed as deduction are:

Course fees;

Journals, textbook and stationery;

Airfare for overseas students;

In the case of Lunney V FC of T. Haley V FC of T(1958) 100 CLR 478it is stated that the

expenses are allowed as deduction if the expenditure is helpful in generating income. In case of

Manpreet the expenses in self-education has not helped him in increasing the income hence the

expenses related to education are not deductible (Harris 2013).

Tax payable Computation

Particulars Amount Amount

Gross Salary $ 45,000.00

Foreign Income

Income From Trust $ 10,000.00

Total Income $ 55,000.00

Deductions

Purchase of mobile work purpose $ 500.00

Total Deductions $ 500.00

Taxable Income $ 54,500.00

Total tax $ 9,259.50

Para 14 of the Taxation Ruling 98/9 provides that if the self-education helps the taxpayer in

increasing the income then it is allowed as deduction (Petty et al. 2015). The Para 23 of the

Taxation ruling 98/9 provides that in case the self-education expenses are allowed as deduction

then the expenses that are allowed as deduction are:

Course fees;

Journals, textbook and stationery;

Airfare for overseas students;

In the case of Lunney V FC of T. Haley V FC of T(1958) 100 CLR 478it is stated that the

expenses are allowed as deduction if the expenditure is helpful in generating income. In case of

Manpreet the expenses in self-education has not helped him in increasing the income hence the

expenses related to education are not deductible (Harris 2013).

Tax payable Computation

Particulars Amount Amount

Gross Salary $ 45,000.00

Foreign Income

Income From Trust $ 10,000.00

Total Income $ 55,000.00

Deductions

Purchase of mobile work purpose $ 500.00

Total Deductions $ 500.00

Taxable Income $ 54,500.00

Total tax $ 9,259.50

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10TAXATION LAW OF AUSTRALIA

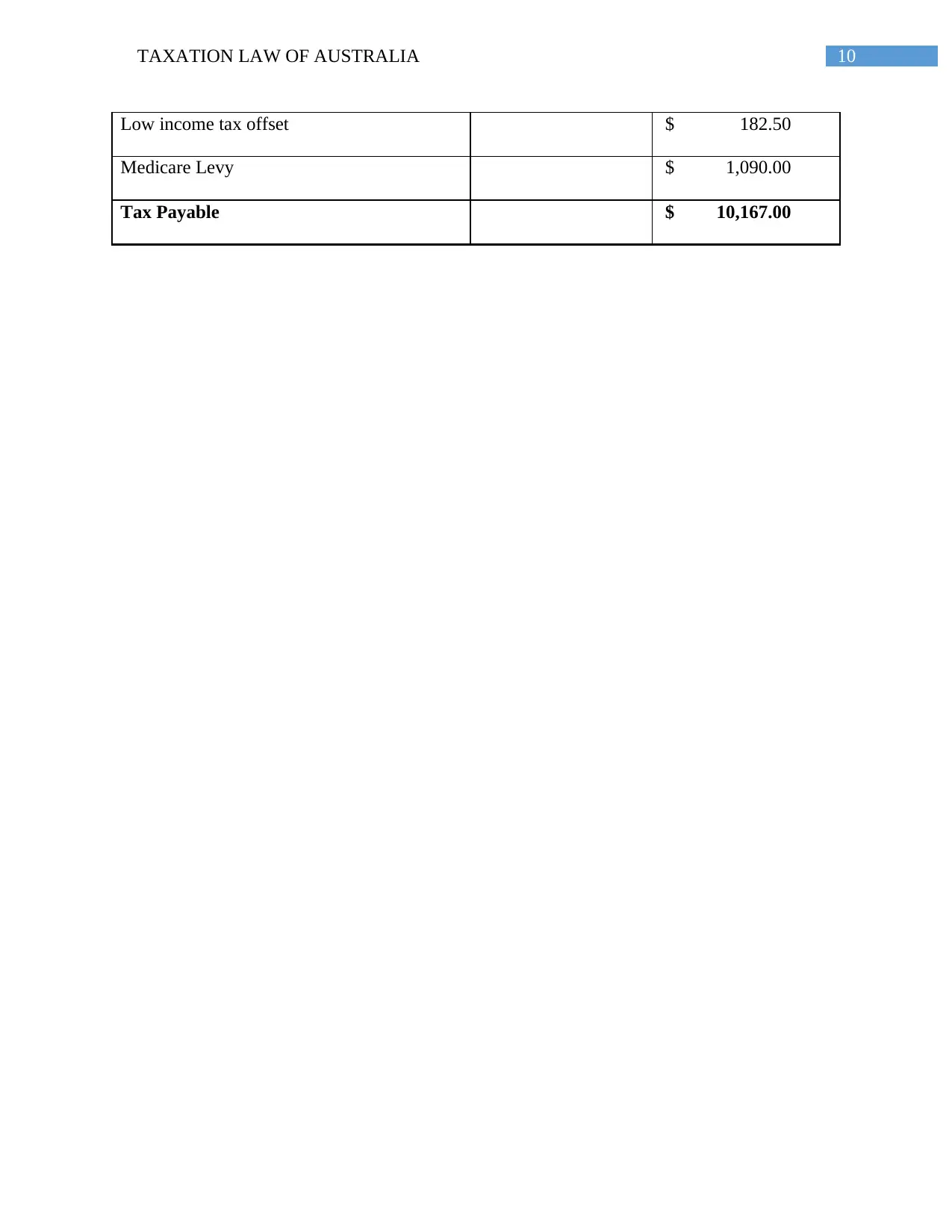

Low income tax offset $ 182.50

Medicare Levy $ 1,090.00

Tax Payable $ 10,167.00

Low income tax offset $ 182.50

Medicare Levy $ 1,090.00

Tax Payable $ 10,167.00

11TAXATION LAW OF AUSTRALIA

References:

Barkoczy, S., 2016. Foundations of Taxation Law 2016. OUP Catalogue.

Braithwaite, V. ed., 2017. Taxing democracy: Understanding tax avoidance and evasion.

Routledge.

Bryan, M., Vann, V. and Thomas, S.B., 2017. Equity and trusts in Australia. Cambridge

University Press.

Cao, L., Hosking, A., Kouparitsas, M., Mullaly, D., Rimmer, X., Shi, Q., Stark, W. and Wende,

S., 2015. Understanding the economy-wide efficiency and incidence of major Australian

taxes. Treasury WP, 1.

Harris, P., 2013. Corporate tax law: Structure, policy and practice. Cambridge University Press.

James, S., Sawyer, A. and Wallschutzky, I., 2015. Tax simplification: A review of initiatives in

Australia, New Zealand and the United Kingdom. eJournal of Tax Research, 13(1), p.280.

Lang, M., 2014. Introduction to the law of double taxation conventions. Linde Verlag GmbH.

McGregor-Lowndes, M., 2014. The not for profit sector in Australia: Fact sheet. ACPNS Current

Issues Information Sheet 2014/4.

McKerchar, M., Bloomquist, K. and Pope, J., 2013. Indicators of tax morale: an exploratory

study. eJournal of Tax Research, 11(1), p.5.

Pearson, G., 2017. Further challenges for Australian consumer law. In Consumer Law and

Socioeconomic Development (pp. 287-305). Springer, Cham.

References:

Barkoczy, S., 2016. Foundations of Taxation Law 2016. OUP Catalogue.

Braithwaite, V. ed., 2017. Taxing democracy: Understanding tax avoidance and evasion.

Routledge.

Bryan, M., Vann, V. and Thomas, S.B., 2017. Equity and trusts in Australia. Cambridge

University Press.

Cao, L., Hosking, A., Kouparitsas, M., Mullaly, D., Rimmer, X., Shi, Q., Stark, W. and Wende,

S., 2015. Understanding the economy-wide efficiency and incidence of major Australian

taxes. Treasury WP, 1.

Harris, P., 2013. Corporate tax law: Structure, policy and practice. Cambridge University Press.

James, S., Sawyer, A. and Wallschutzky, I., 2015. Tax simplification: A review of initiatives in

Australia, New Zealand and the United Kingdom. eJournal of Tax Research, 13(1), p.280.

Lang, M., 2014. Introduction to the law of double taxation conventions. Linde Verlag GmbH.

McGregor-Lowndes, M., 2014. The not for profit sector in Australia: Fact sheet. ACPNS Current

Issues Information Sheet 2014/4.

McKerchar, M., Bloomquist, K. and Pope, J., 2013. Indicators of tax morale: an exploratory

study. eJournal of Tax Research, 11(1), p.5.

Pearson, G., 2017. Further challenges for Australian consumer law. In Consumer Law and

Socioeconomic Development (pp. 287-305). Springer, Cham.

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.