Functions of Accounting in Business Firms: Financial Statements, Ratios, and Budgets

VerifiedAdded on 2023/06/10

|15

|4326

|471

AI Summary

This report discusses the purpose of accounting and its functions in business firms, including the preparation of financial statements, computation and interpretation of financial ratios, and creation of budgets. It also covers the benefits and drawbacks of budgets and budgetary planning and control for an organization. The report emphasizes the importance of following accounting standards and principles and ethical practices in accounting. The report includes examples of financial statements and calculations of financial ratios.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Unit - 5

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Contents

INTRODUCTION...............................................................................................................................3

TASK.........................................................................................................................................3

1. Elaborate on the purpose of accounting..........................................................................3

2. Discussion on the functions of accounting that are needed in the business firm

pertaining to the regulatory and ethical constraints................................................................4

3. Present the financial statements in order to meet the accounting standards and

principles................................................................................................................................5

4. Computation and interpretation of the financial ratios...................................................6

5. Represent the contrast of the financial achievements and results for satisfying the

conditions of the financial ratios:...........................................................................................8

6. Preparation of the cash budget from given information for an organisation using a

spreadsheet.............................................................................................................................9

7. Description of the benefits and drawbacks linked with the budgets and budgetary

planning and control for an organisation..............................................................................11

CONCLUSION..................................................................................................................................13

References..........................................................................................................................................14

INTRODUCTION...............................................................................................................................3

TASK.........................................................................................................................................3

1. Elaborate on the purpose of accounting..........................................................................3

2. Discussion on the functions of accounting that are needed in the business firm

pertaining to the regulatory and ethical constraints................................................................4

3. Present the financial statements in order to meet the accounting standards and

principles................................................................................................................................5

4. Computation and interpretation of the financial ratios...................................................6

5. Represent the contrast of the financial achievements and results for satisfying the

conditions of the financial ratios:...........................................................................................8

6. Preparation of the cash budget from given information for an organisation using a

spreadsheet.............................................................................................................................9

7. Description of the benefits and drawbacks linked with the budgets and budgetary

planning and control for an organisation..............................................................................11

CONCLUSION..................................................................................................................................13

References..........................................................................................................................................14

INTRODUCTION

The term accounting refers to procedure of recording, analyzing and summarizing the

financial transactions to provide the business with the financial results. It is not possible for

the business to keep in mind all the transactions that takes place in the day – to – day

business, so it is very important for a business to work on maintain the reports and thus it has

become really very relevant to each and every organization. There are three main financial

statements. The reports look into the purpose and role of accounting standards in relation to

the moral practices and statutory compliances. Along with this the report along comprises of

the preparation of financial statements and trial balance. Furthermore, it also encompasses

with the calculation of ratio analysis with their interpretations. Moreover, it also contains the

creation of cash budget and the theoretical data on the limitations and advantages of the

budget and budgetary planning and control within the business organization.

TASK

1. Elaborate on the purpose of accounting

Accounting refers to the creation of financial information. With the help of such data a

company can see how much it has earned and paid in the financial year. It also provides the

ideas on the grounds to the company where it can make more money. Accounting is crucial

for the for the company for the various reasons. Accounting enables the business owner to

identify, analyze, interpret and record the business transactions and communicate the same to

the internal parties and track the position of a business concern.

The purpose of accounting is elaborated below:

It helps in the better management of business: Accounting data provides with the

accurate and reliable facts and figures that reflects the financial position of a business

concern. All this forms a base for decision making. It also helps in evaluating the

condition of assets and liabilities of a firm.

To create budget and make projections for future: The business firm can examine the

financial statements of the company and can make presumptions on the future cash

inflows and outflows. Present accounting reports gives an idea to the company about

how their assets and liabilities are going to perform in future and also provide the base

The term accounting refers to procedure of recording, analyzing and summarizing the

financial transactions to provide the business with the financial results. It is not possible for

the business to keep in mind all the transactions that takes place in the day – to – day

business, so it is very important for a business to work on maintain the reports and thus it has

become really very relevant to each and every organization. There are three main financial

statements. The reports look into the purpose and role of accounting standards in relation to

the moral practices and statutory compliances. Along with this the report along comprises of

the preparation of financial statements and trial balance. Furthermore, it also encompasses

with the calculation of ratio analysis with their interpretations. Moreover, it also contains the

creation of cash budget and the theoretical data on the limitations and advantages of the

budget and budgetary planning and control within the business organization.

TASK

1. Elaborate on the purpose of accounting

Accounting refers to the creation of financial information. With the help of such data a

company can see how much it has earned and paid in the financial year. It also provides the

ideas on the grounds to the company where it can make more money. Accounting is crucial

for the for the company for the various reasons. Accounting enables the business owner to

identify, analyze, interpret and record the business transactions and communicate the same to

the internal parties and track the position of a business concern.

The purpose of accounting is elaborated below:

It helps in the better management of business: Accounting data provides with the

accurate and reliable facts and figures that reflects the financial position of a business

concern. All this forms a base for decision making. It also helps in evaluating the

condition of assets and liabilities of a firm.

To create budget and make projections for future: The business firm can examine the

financial statements of the company and can make presumptions on the future cash

inflows and outflows. Present accounting reports gives an idea to the company about

how their assets and liabilities are going to perform in future and also provide the base

for the preparation of budgets which will help the company in achieving the better

results.

To present the reports for auditing: It is very important for a company to maintain the

accounting reports. During the time of audit, a company can present the record to the

auditors and can take their help regarding the corrective decisions that are to be taken.

For presenting the records to the interested parties: The firm provides record to the

external parties in order to seek investments from them. Without such data the

business enterprise cannot think of even raising funds as these records are very

important for the organization to gain trust of the shareholders, creditors, investors

and suppliers. These people are associated with the business and by analyzing the

financial statements they determine whether the company will be able to repay the

loan amount that it has taken or not (Oyewo and Akinsanmi., 2021)

Tracking the movements of cash inflows and outflows: Accounting makes it possible

to the business to track its expenses, losses, income and gains in the chronological

order. In short it helps in gaining insights on what it owns and what it owes to the

company.

To meet the legal requirements: It helps in meeting the statutory needs. A company

must have its accounting data for meeting the needs of law for different legal purposes

like annual accounts, income tax return, sales tax return etc.

To ascertain the profit and loss: Accounting assists the business in the evaluation of

how much profit and losses a company has incurred by making payment for its

expenses. It helps the company in estimating the activities which are not necessary to

perform and charges the higher cost.

2. Discussion on the functions of accounting that are needed in the business firm pertaining

to the regulatory and ethical constraints.

Accounting plays a significant role in various field of commerce, market, banks,

industries, and culture. The financial data is not only useful to the internal parties but they are

also useful to the external parties. This is because the investors, creditors, suppliers,

customers and other financial institutions can rake good reliable and accurate decisions based

on such data. To satisfy the users distinct accounting principles have been framed. The

accounting principles are mandatory to follow when the business is recording its day – to –

day transactions and settlements (Weygandt and et.al., 2019). These guidelines are applied in

and every organization in the world and is universal in nature. Different countries have

results.

To present the reports for auditing: It is very important for a company to maintain the

accounting reports. During the time of audit, a company can present the record to the

auditors and can take their help regarding the corrective decisions that are to be taken.

For presenting the records to the interested parties: The firm provides record to the

external parties in order to seek investments from them. Without such data the

business enterprise cannot think of even raising funds as these records are very

important for the organization to gain trust of the shareholders, creditors, investors

and suppliers. These people are associated with the business and by analyzing the

financial statements they determine whether the company will be able to repay the

loan amount that it has taken or not (Oyewo and Akinsanmi., 2021)

Tracking the movements of cash inflows and outflows: Accounting makes it possible

to the business to track its expenses, losses, income and gains in the chronological

order. In short it helps in gaining insights on what it owns and what it owes to the

company.

To meet the legal requirements: It helps in meeting the statutory needs. A company

must have its accounting data for meeting the needs of law for different legal purposes

like annual accounts, income tax return, sales tax return etc.

To ascertain the profit and loss: Accounting assists the business in the evaluation of

how much profit and losses a company has incurred by making payment for its

expenses. It helps the company in estimating the activities which are not necessary to

perform and charges the higher cost.

2. Discussion on the functions of accounting that are needed in the business firm pertaining

to the regulatory and ethical constraints.

Accounting plays a significant role in various field of commerce, market, banks,

industries, and culture. The financial data is not only useful to the internal parties but they are

also useful to the external parties. This is because the investors, creditors, suppliers,

customers and other financial institutions can rake good reliable and accurate decisions based

on such data. To satisfy the users distinct accounting principles have been framed. The

accounting principles are mandatory to follow when the business is recording its day – to –

day transactions and settlements (Weygandt and et.al., 2019). These guidelines are applied in

and every organization in the world and is universal in nature. Different countries have

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

different principles framed but they shall be abided by every business enterprise. The

accounting standards are the one that helps the company to bring the consistency and

uniformity in whole accounting system. It sets same rules and regulations for treating the

settlements and the objective behind this is that the company reports its transactions in the

same way so that it can be understandable and provide with the meaningful data. But it is

observed in many cases, that the auditors do not act in accordance with such principles and

standards and provide with the wrong data and judgements just for their personal interests.

So, to cope- up with such situations various laws should be implemented in the market place

and economy.

There are many organizations that compel the accounting professionals to represent the

misleading information by paying them in higher amounts. Because of such issues, the

interested parties cannot get a true picture of company’s financial position and they get

trapped by the data. The creditors, investors, suppliers and other fiscal institutions get

influenced by such information can make investments and as a result they have to face the

negative consequences and risk factors for the money they invested in the firm.

While performing any task, moral and ethical practices shall be kept in mind the very first is

that the accounting professionals should be clear and truthful in the relations that it holds with

other business concerns. They should not be bias and shall neglect their personal interests.

The companies shall work according to the laws that have been created. They should not even

leak the acquired financial data received because of the personal relationships to the third

parties as this is really unethical. The information should not be disclosed until and unless the

specific authorities and legal parties have asked for it. The concept of Cpas sets the standards

for the accounting task performers to help them in making full use of their knowledge and

techniques. The main impression of this constitution is the creation and generation of public

welfare, duties etc. So, by the use of this the experts would improve the image of society,

business and other sectors (Tsuji and Hiraiwa ., 2018)

3. Present the financial statements in order to meet the accounting standards and principles.

Income Statement

Income Statement

Particulars Amount

Sales 400000

accounting standards are the one that helps the company to bring the consistency and

uniformity in whole accounting system. It sets same rules and regulations for treating the

settlements and the objective behind this is that the company reports its transactions in the

same way so that it can be understandable and provide with the meaningful data. But it is

observed in many cases, that the auditors do not act in accordance with such principles and

standards and provide with the wrong data and judgements just for their personal interests.

So, to cope- up with such situations various laws should be implemented in the market place

and economy.

There are many organizations that compel the accounting professionals to represent the

misleading information by paying them in higher amounts. Because of such issues, the

interested parties cannot get a true picture of company’s financial position and they get

trapped by the data. The creditors, investors, suppliers and other fiscal institutions get

influenced by such information can make investments and as a result they have to face the

negative consequences and risk factors for the money they invested in the firm.

While performing any task, moral and ethical practices shall be kept in mind the very first is

that the accounting professionals should be clear and truthful in the relations that it holds with

other business concerns. They should not be bias and shall neglect their personal interests.

The companies shall work according to the laws that have been created. They should not even

leak the acquired financial data received because of the personal relationships to the third

parties as this is really unethical. The information should not be disclosed until and unless the

specific authorities and legal parties have asked for it. The concept of Cpas sets the standards

for the accounting task performers to help them in making full use of their knowledge and

techniques. The main impression of this constitution is the creation and generation of public

welfare, duties etc. So, by the use of this the experts would improve the image of society,

business and other sectors (Tsuji and Hiraiwa ., 2018)

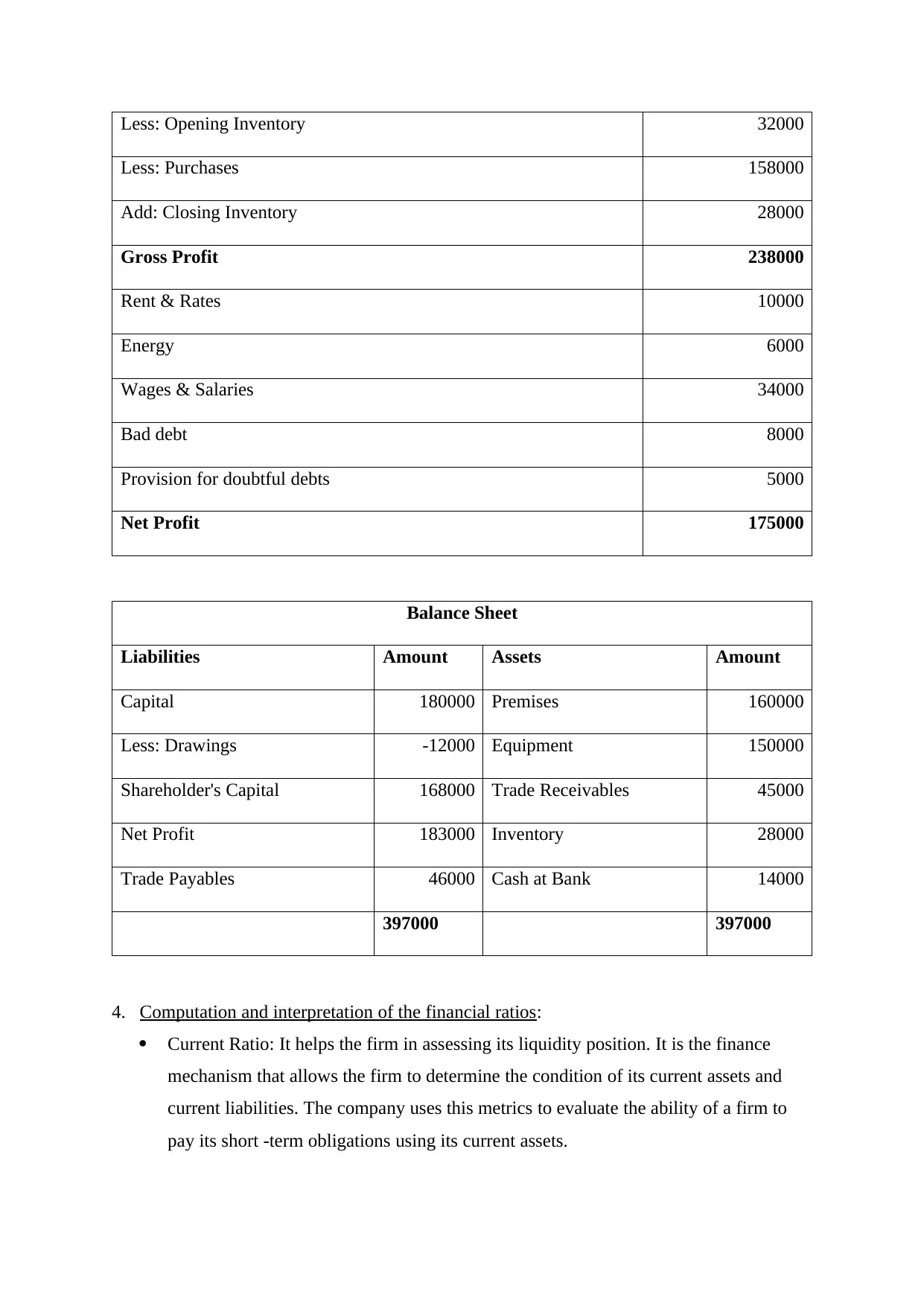

3. Present the financial statements in order to meet the accounting standards and principles.

Income Statement

Income Statement

Particulars Amount

Sales 400000

Less: Opening Inventory 32000

Less: Purchases 158000

Add: Closing Inventory 28000

Gross Profit 238000

Rent & Rates 10000

Energy 6000

Wages & Salaries 34000

Bad debt 8000

Provision for doubtful debts 5000

Net Profit 175000

Balance Sheet

Liabilities Amount Assets Amount

Capital 180000 Premises 160000

Less: Drawings -12000 Equipment 150000

Shareholder's Capital 168000 Trade Receivables 45000

Net Profit 183000 Inventory 28000

Trade Payables 46000 Cash at Bank 14000

397000 397000

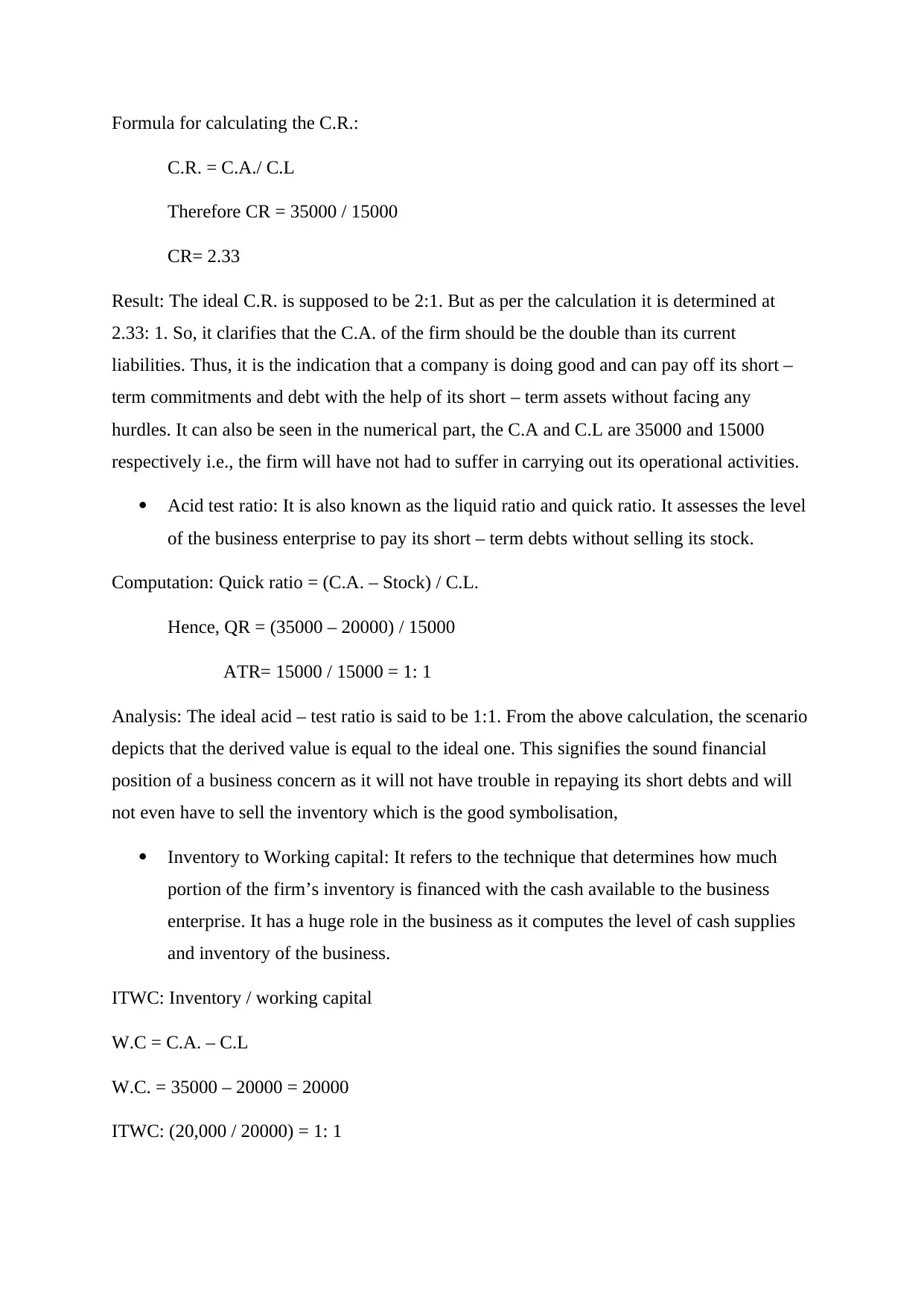

4. Computation and interpretation of the financial ratios:

Current Ratio: It helps the firm in assessing its liquidity position. It is the finance

mechanism that allows the firm to determine the condition of its current assets and

current liabilities. The company uses this metrics to evaluate the ability of a firm to

pay its short -term obligations using its current assets.

Less: Purchases 158000

Add: Closing Inventory 28000

Gross Profit 238000

Rent & Rates 10000

Energy 6000

Wages & Salaries 34000

Bad debt 8000

Provision for doubtful debts 5000

Net Profit 175000

Balance Sheet

Liabilities Amount Assets Amount

Capital 180000 Premises 160000

Less: Drawings -12000 Equipment 150000

Shareholder's Capital 168000 Trade Receivables 45000

Net Profit 183000 Inventory 28000

Trade Payables 46000 Cash at Bank 14000

397000 397000

4. Computation and interpretation of the financial ratios:

Current Ratio: It helps the firm in assessing its liquidity position. It is the finance

mechanism that allows the firm to determine the condition of its current assets and

current liabilities. The company uses this metrics to evaluate the ability of a firm to

pay its short -term obligations using its current assets.

Formula for calculating the C.R.:

C.R. = C.A./ C.L

Therefore CR = 35000 / 15000

CR= 2.33

Result: The ideal C.R. is supposed to be 2:1. But as per the calculation it is determined at

2.33: 1. So, it clarifies that the C.A. of the firm should be the double than its current

liabilities. Thus, it is the indication that a company is doing good and can pay off its short –

term commitments and debt with the help of its short – term assets without facing any

hurdles. It can also be seen in the numerical part, the C.A and C.L are 35000 and 15000

respectively i.e., the firm will have not had to suffer in carrying out its operational activities.

Acid test ratio: It is also known as the liquid ratio and quick ratio. It assesses the level

of the business enterprise to pay its short – term debts without selling its stock.

Computation: Quick ratio = (C.A. – Stock) / C.L.

Hence, QR = (35000 – 20000) / 15000

ATR= 15000 / 15000 = 1: 1

Analysis: The ideal acid – test ratio is said to be 1:1. From the above calculation, the scenario

depicts that the derived value is equal to the ideal one. This signifies the sound financial

position of a business concern as it will not have trouble in repaying its short debts and will

not even have to sell the inventory which is the good symbolisation,

Inventory to Working capital: It refers to the technique that determines how much

portion of the firm’s inventory is financed with the cash available to the business

enterprise. It has a huge role in the business as it computes the level of cash supplies

and inventory of the business.

ITWC: Inventory / working capital

W.C = C.A. – C.L

W.C. = 35000 – 20000 = 20000

ITWC: (20,000 / 20000) = 1: 1

C.R. = C.A./ C.L

Therefore CR = 35000 / 15000

CR= 2.33

Result: The ideal C.R. is supposed to be 2:1. But as per the calculation it is determined at

2.33: 1. So, it clarifies that the C.A. of the firm should be the double than its current

liabilities. Thus, it is the indication that a company is doing good and can pay off its short –

term commitments and debt with the help of its short – term assets without facing any

hurdles. It can also be seen in the numerical part, the C.A and C.L are 35000 and 15000

respectively i.e., the firm will have not had to suffer in carrying out its operational activities.

Acid test ratio: It is also known as the liquid ratio and quick ratio. It assesses the level

of the business enterprise to pay its short – term debts without selling its stock.

Computation: Quick ratio = (C.A. – Stock) / C.L.

Hence, QR = (35000 – 20000) / 15000

ATR= 15000 / 15000 = 1: 1

Analysis: The ideal acid – test ratio is said to be 1:1. From the above calculation, the scenario

depicts that the derived value is equal to the ideal one. This signifies the sound financial

position of a business concern as it will not have trouble in repaying its short debts and will

not even have to sell the inventory which is the good symbolisation,

Inventory to Working capital: It refers to the technique that determines how much

portion of the firm’s inventory is financed with the cash available to the business

enterprise. It has a huge role in the business as it computes the level of cash supplies

and inventory of the business.

ITWC: Inventory / working capital

W.C = C.A. – C.L

W.C. = 35000 – 20000 = 20000

ITWC: (20,000 / 20000) = 1: 1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

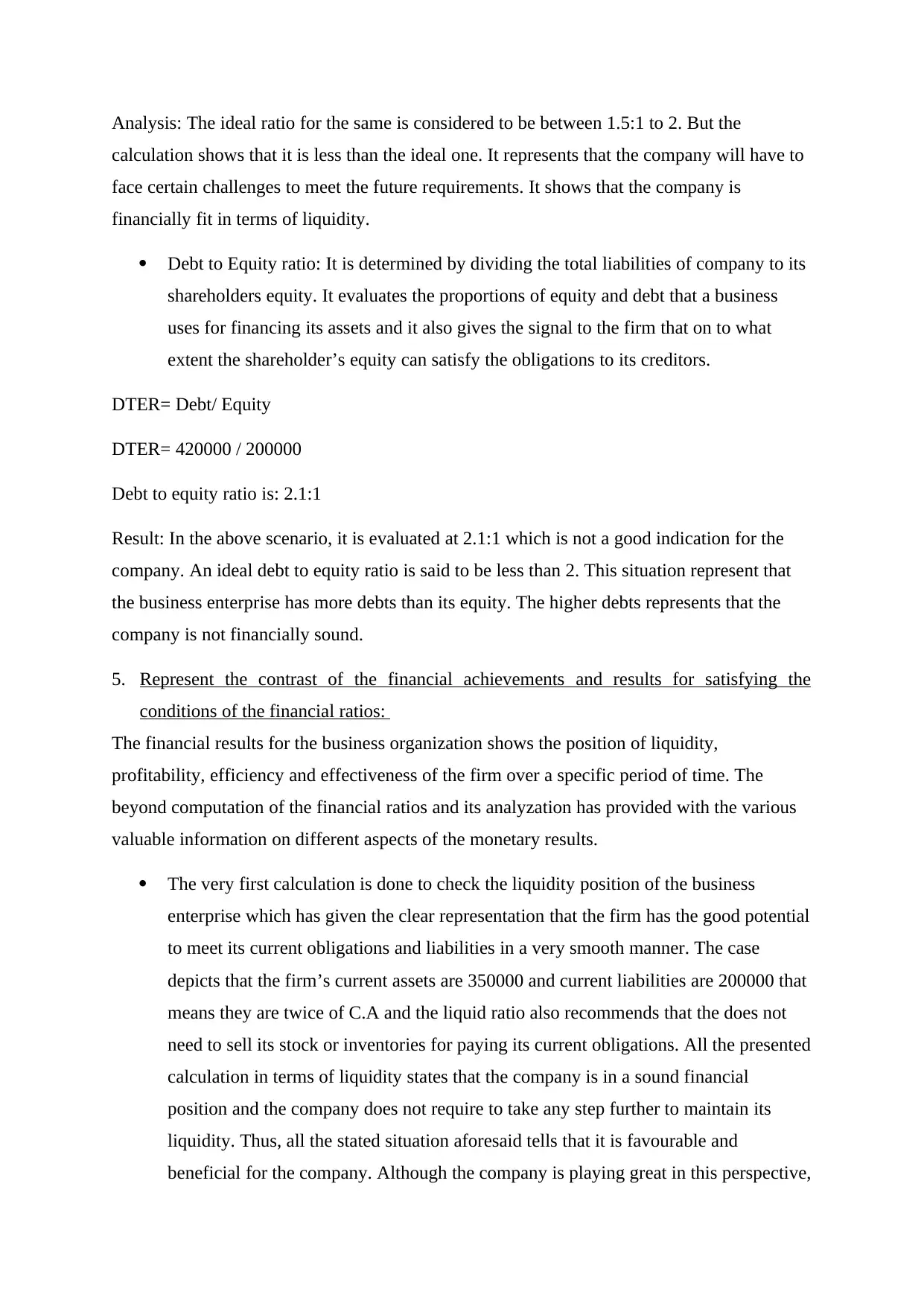

Analysis: The ideal ratio for the same is considered to be between 1.5:1 to 2. But the

calculation shows that it is less than the ideal one. It represents that the company will have to

face certain challenges to meet the future requirements. It shows that the company is

financially fit in terms of liquidity.

Debt to Equity ratio: It is determined by dividing the total liabilities of company to its

shareholders equity. It evaluates the proportions of equity and debt that a business

uses for financing its assets and it also gives the signal to the firm that on to what

extent the shareholder’s equity can satisfy the obligations to its creditors.

DTER= Debt/ Equity

DTER= 420000 / 200000

Debt to equity ratio is: 2.1:1

Result: In the above scenario, it is evaluated at 2.1:1 which is not a good indication for the

company. An ideal debt to equity ratio is said to be less than 2. This situation represent that

the business enterprise has more debts than its equity. The higher debts represents that the

company is not financially sound.

5. Represent the contrast of the financial achievements and results for satisfying the

conditions of the financial ratios:

The financial results for the business organization shows the position of liquidity,

profitability, efficiency and effectiveness of the firm over a specific period of time. The

beyond computation of the financial ratios and its analyzation has provided with the various

valuable information on different aspects of the monetary results.

The very first calculation is done to check the liquidity position of the business

enterprise which has given the clear representation that the firm has the good potential

to meet its current obligations and liabilities in a very smooth manner. The case

depicts that the firm’s current assets are 350000 and current liabilities are 200000 that

means they are twice of C.A and the liquid ratio also recommends that the does not

need to sell its stock or inventories for paying its current obligations. All the presented

calculation in terms of liquidity states that the company is in a sound financial

position and the company does not require to take any step further to maintain its

liquidity. Thus, all the stated situation aforesaid tells that it is favourable and

beneficial for the company. Although the company is playing great in this perspective,

calculation shows that it is less than the ideal one. It represents that the company will have to

face certain challenges to meet the future requirements. It shows that the company is

financially fit in terms of liquidity.

Debt to Equity ratio: It is determined by dividing the total liabilities of company to its

shareholders equity. It evaluates the proportions of equity and debt that a business

uses for financing its assets and it also gives the signal to the firm that on to what

extent the shareholder’s equity can satisfy the obligations to its creditors.

DTER= Debt/ Equity

DTER= 420000 / 200000

Debt to equity ratio is: 2.1:1

Result: In the above scenario, it is evaluated at 2.1:1 which is not a good indication for the

company. An ideal debt to equity ratio is said to be less than 2. This situation represent that

the business enterprise has more debts than its equity. The higher debts represents that the

company is not financially sound.

5. Represent the contrast of the financial achievements and results for satisfying the

conditions of the financial ratios:

The financial results for the business organization shows the position of liquidity,

profitability, efficiency and effectiveness of the firm over a specific period of time. The

beyond computation of the financial ratios and its analyzation has provided with the various

valuable information on different aspects of the monetary results.

The very first calculation is done to check the liquidity position of the business

enterprise which has given the clear representation that the firm has the good potential

to meet its current obligations and liabilities in a very smooth manner. The case

depicts that the firm’s current assets are 350000 and current liabilities are 200000 that

means they are twice of C.A and the liquid ratio also recommends that the does not

need to sell its stock or inventories for paying its current obligations. All the presented

calculation in terms of liquidity states that the company is in a sound financial

position and the company does not require to take any step further to maintain its

liquidity. Thus, all the stated situation aforesaid tells that it is favourable and

beneficial for the company. Although the company is playing great in this perspective,

but still, it will have to save its cash balances for the purpose of meeting future

requirements and uncertainties. It is obvious and every business shall do it

(Koekemoers., 2019)

Secondly, the calculation regarding the inventory to working capital ratio also

represents that the company will be able to overcome with this. It is because, the

variation is not very much, the working capital is equal to the amount of inventory.

And currently the firm is able to achieve it. But, for the coming time it will have to

increase its current assets and lower its short – term debts.

The fourth ratio, the debt – to - equity ratio has huge different. It is more than the it

should be. This might lead to the various risk and losses. The business enterprise can

also lose its image in front of the interested parties as well the internal parties because

the company has more obligations than the equity. So, it should take some steps to

direct and control its obligations and shall also cut down the unnecessary expenses.

In the end, it can be said that the overall result derived is in the favour of company but

it should take measures for the improvement in cash flows.

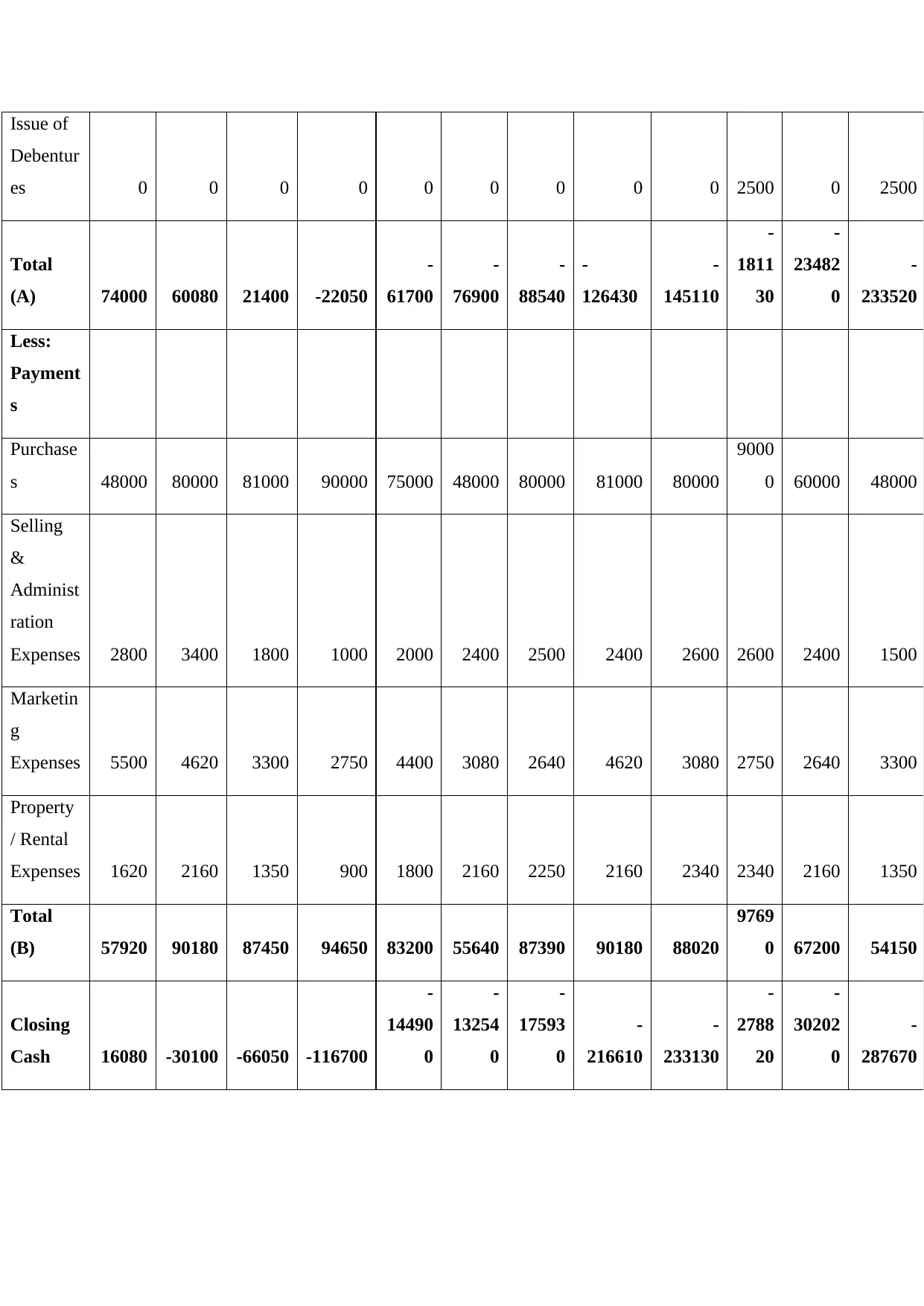

6. Preparation of the cash budget from given information for an organisation using a

spreadsheet.

Particul

ars

Janua

ry

Febru

ary March April May June July August

Septem

ber

Oct

ober

Nove

mber

Decem

ber

Receipts

Opening

Balance 8000 16080 -30100 -66050

-

11670

0

-

14490

0

-

13254

0

-

175930

-

216610

-

2331

30

-

27882

0

-

302020

Sales 66000 44000 49500 44000 55000 66000 44000 49500 71500

4950

0 44000 66000

Issue of

Shares 0 0 2000 0 0 2000 0 0 0 0 0 0

requirements and uncertainties. It is obvious and every business shall do it

(Koekemoers., 2019)

Secondly, the calculation regarding the inventory to working capital ratio also

represents that the company will be able to overcome with this. It is because, the

variation is not very much, the working capital is equal to the amount of inventory.

And currently the firm is able to achieve it. But, for the coming time it will have to

increase its current assets and lower its short – term debts.

The fourth ratio, the debt – to - equity ratio has huge different. It is more than the it

should be. This might lead to the various risk and losses. The business enterprise can

also lose its image in front of the interested parties as well the internal parties because

the company has more obligations than the equity. So, it should take some steps to

direct and control its obligations and shall also cut down the unnecessary expenses.

In the end, it can be said that the overall result derived is in the favour of company but

it should take measures for the improvement in cash flows.

6. Preparation of the cash budget from given information for an organisation using a

spreadsheet.

Particul

ars

Janua

ry

Febru

ary March April May June July August

Septem

ber

Oct

ober

Nove

mber

Decem

ber

Receipts

Opening

Balance 8000 16080 -30100 -66050

-

11670

0

-

14490

0

-

13254

0

-

175930

-

216610

-

2331

30

-

27882

0

-

302020

Sales 66000 44000 49500 44000 55000 66000 44000 49500 71500

4950

0 44000 66000

Issue of

Shares 0 0 2000 0 0 2000 0 0 0 0 0 0

Issue of

Debentur

es 0 0 0 0 0 0 0 0 0 2500 0 2500

Total

(A) 74000 60080 21400 -22050

-

61700

-

76900

-

88540

-

126430

-

145110

-

1811

30

-

23482

0

-

233520

Less:

Payment

s

Purchase

s 48000 80000 81000 90000 75000 48000 80000 81000 80000

9000

0 60000 48000

Selling

&

Administ

ration

Expenses 2800 3400 1800 1000 2000 2400 2500 2400 2600 2600 2400 1500

Marketin

g

Expenses 5500 4620 3300 2750 4400 3080 2640 4620 3080 2750 2640 3300

Property

/ Rental

Expenses 1620 2160 1350 900 1800 2160 2250 2160 2340 2340 2160 1350

Total

(B) 57920 90180 87450 94650 83200 55640 87390 90180 88020

9769

0 67200 54150

Closing

Cash 16080 -30100 -66050 -116700

-

14490

0

-

13254

0

-

17593

0

-

216610

-

233130

-

2788

20

-

30202

0

-

287670

Debentur

es 0 0 0 0 0 0 0 0 0 2500 0 2500

Total

(A) 74000 60080 21400 -22050

-

61700

-

76900

-

88540

-

126430

-

145110

-

1811

30

-

23482

0

-

233520

Less:

Payment

s

Purchase

s 48000 80000 81000 90000 75000 48000 80000 81000 80000

9000

0 60000 48000

Selling

&

Administ

ration

Expenses 2800 3400 1800 1000 2000 2400 2500 2400 2600 2600 2400 1500

Marketin

g

Expenses 5500 4620 3300 2750 4400 3080 2640 4620 3080 2750 2640 3300

Property

/ Rental

Expenses 1620 2160 1350 900 1800 2160 2250 2160 2340 2340 2160 1350

Total

(B) 57920 90180 87450 94650 83200 55640 87390 90180 88020

9769

0 67200 54150

Closing

Cash 16080 -30100 -66050 -116700

-

14490

0

-

13254

0

-

17593

0

-

216610

-

233130

-

2788

20

-

30202

0

-

287670

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

7. Description of the benefits and drawbacks linked with the budgets and budgetary

planning and control for an organisation.

Through appropriate financial planning the business organization can create the

successful strategies that assists and helps the company to make good use of its finances. The

budgets are created in the departments to bring coordination and cooperation between the

distinct departments. There are various departments like information technology, sales,

purchase, finance, marketing, operations etc. and these shall have enough money to

accomplish the task and meet their desired goals and objectives. Budgets helps the company

to bridge the gap between where it is today and where it has to reach in future. The budgets

are made and then they are transferred to the higher authorities so that they accept them and

find the best ways and approaches to accomplish the stated plans. The budgets are prepared in

order to achieve the long - term goals. If the manager makes good policies, then the company

will be able to achieve its desired goal. The budgetary control is that part of managerial

accounting where it guides the businesses in assessing the areas where the firm needs to

spend and how to attain the aim. It keeps track on costs associated with every and every

activity performed in an organisation. These have certain advantages and disadvantages that

are listed below:

Benefits:

Provides planning for executing the tasks: Budgets prove to be useful for the

businesses because they create standards for the results according to the time frames.

It helps the firm in gaining the valuable insights by matching the actual performance

with the planned or budgeted one. The company can find out the deviations by this

and finding out the reasons for such differences (Jeyaraj ., 2020).

It helps the company in planning: Budget makes the ground for planning. As it finds

out the differences and the reason behind them. So, the company can form plans for

such areas and control these factors at the right time.

Helps the managers in the delegation of responsibility: The budget is created for each

and every department in the company. A business firm can assign the work according

to the departments and can also have control on the activities performed by different

management levels.

It helps in the coordination and cooperation: Distinct departments are involved when

the budget is prepared. When the purchase budget is created, it is matched with the

planning and control for an organisation.

Through appropriate financial planning the business organization can create the

successful strategies that assists and helps the company to make good use of its finances. The

budgets are created in the departments to bring coordination and cooperation between the

distinct departments. There are various departments like information technology, sales,

purchase, finance, marketing, operations etc. and these shall have enough money to

accomplish the task and meet their desired goals and objectives. Budgets helps the company

to bridge the gap between where it is today and where it has to reach in future. The budgets

are made and then they are transferred to the higher authorities so that they accept them and

find the best ways and approaches to accomplish the stated plans. The budgets are prepared in

order to achieve the long - term goals. If the manager makes good policies, then the company

will be able to achieve its desired goal. The budgetary control is that part of managerial

accounting where it guides the businesses in assessing the areas where the firm needs to

spend and how to attain the aim. It keeps track on costs associated with every and every

activity performed in an organisation. These have certain advantages and disadvantages that

are listed below:

Benefits:

Provides planning for executing the tasks: Budgets prove to be useful for the

businesses because they create standards for the results according to the time frames.

It helps the firm in gaining the valuable insights by matching the actual performance

with the planned or budgeted one. The company can find out the deviations by this

and finding out the reasons for such differences (Jeyaraj ., 2020).

It helps the company in planning: Budget makes the ground for planning. As it finds

out the differences and the reason behind them. So, the company can form plans for

such areas and control these factors at the right time.

Helps the managers in the delegation of responsibility: The budget is created for each

and every department in the company. A business firm can assign the work according

to the departments and can also have control on the activities performed by different

management levels.

It helps in the coordination and cooperation: Distinct departments are involved when

the budget is prepared. When the purchase budget is created, it is matched with the

purchase budget, then it is later looked with the budget with respect to the manpower

and machines. In this way, the manager gets an idea and knowledge about the

workings of various managerial level and plan accordingly.

It helps in the future projection: The budget can help in forecasting and estimation of

cost. So it assists the managers to forecast the activities and position of the company

in the coming future (Jamu., 2018)

Limitations are:

Expansion In the spendings: There are areas and grounds that do not require cost, but

while making a plan, the company spends those areas also which results in the

implementation of the unnecessary cost and it leads to the more expenses in an

organization.

Inflexibility: Budget considers and put the amount estimated in the different activities.

There might be situations where the businesses will have to spend more and less in

some areas. But if the company is not left with the alternative or scope to make these

changes then it will lead to the over – spending in some cases and under – expenses

for the other.

No reliability in the projections: In businesses there are times when the predictions of

managers are not always accurate. The manager makes projections and plan according

to them, all this can have adverse effect on the operations and profitability of the firm.

Over- Focused: Managers only focuses on those areas that are allocated in the budget.

They become bounded from their thinking ability. Some others areas other than

mentioned in the budget could also help the firm to attain the objective that a firm is

desiring for. But this results in the neglection of those perspectives (Jermias and et.al.,

2022)

and machines. In this way, the manager gets an idea and knowledge about the

workings of various managerial level and plan accordingly.

It helps in the future projection: The budget can help in forecasting and estimation of

cost. So it assists the managers to forecast the activities and position of the company

in the coming future (Jamu., 2018)

Limitations are:

Expansion In the spendings: There are areas and grounds that do not require cost, but

while making a plan, the company spends those areas also which results in the

implementation of the unnecessary cost and it leads to the more expenses in an

organization.

Inflexibility: Budget considers and put the amount estimated in the different activities.

There might be situations where the businesses will have to spend more and less in

some areas. But if the company is not left with the alternative or scope to make these

changes then it will lead to the over – spending in some cases and under – expenses

for the other.

No reliability in the projections: In businesses there are times when the predictions of

managers are not always accurate. The manager makes projections and plan according

to them, all this can have adverse effect on the operations and profitability of the firm.

Over- Focused: Managers only focuses on those areas that are allocated in the budget.

They become bounded from their thinking ability. Some others areas other than

mentioned in the budget could also help the firm to attain the objective that a firm is

desiring for. But this results in the neglection of those perspectives (Jermias and et.al.,

2022)

CONCLUSION

It can be concluded from the above report and statements that the business

performances are affected by the various different particulars and items. Accounting has a

major role and is the base for each and activity that is going to take place at the management

level. Budgets are also created by looking at the fiscal data of the business enterprise. It helps

the organization in taking informed and accurate business decisions. In this research the OLC

eatery is the company’s portfolio, which is successful in the industry and has the capability to

add on some of the natures. These add on will help the company to take a competitive

advantage and stand in a market for long time duration.

It can be concluded from the above report and statements that the business

performances are affected by the various different particulars and items. Accounting has a

major role and is the base for each and activity that is going to take place at the management

level. Budgets are also created by looking at the fiscal data of the business enterprise. It helps

the organization in taking informed and accurate business decisions. In this research the OLC

eatery is the company’s portfolio, which is successful in the industry and has the capability to

add on some of the natures. These add on will help the company to take a competitive

advantage and stand in a market for long time duration.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

References

Books and Journals.

Weygandt and et.al., 2019. Accounting Principles, Volume 2. John Wiley & Sons.

Oyewo, B., Vo, X.V. and Akinsanmi, T., 2021. Strategy-related factors moderating the fit between

management accounting practice sophistication and organisational effectiveness: the

Global Management Accounting Principles (GMAP) perspective. Spanish Journal of

Finance and Accounting. 50(2). pp.187-223.

Tsuji, M. and Hiraiwa, M., 2018. An analysis of the internal consistency of the new accounting

standard for virtual currencies in generally accepted Japanese accounting principles:

A virtual currency user perspective. 8(2). pp.30-40.

Peters, M.D. and Chiu, C., INTERACTIVE SPREADSHEETING: A LEARNING STRATEGY

AND EXERCISES FOR CALCULATIVE MANAGEMENT ACCOUNTING

PRINCIPLES. Interactive Spreadsheets for Calculative Management Accounting

Principles. Issues in Accounting Education.

Tangngisalu, J., 2022. Current Ratio, Return on Asset, and Debt-to-Equity-Ratio on Stock-Price of

Sector Property and Real Estate. Golden Ratio of Finance Management. 2(1). pp.01-

14.

Koekemoer, S., 2019. Celebrating International Fraud Awareness Week through detection and

prevention of Fraud in the workplace. CIGFARO Journal (Chartered Institute of

Government Finance Audit and Risk Officers). 20(2). pp.10-13.

Ali, Z. and Motlak, J.B., 2021. The Role of Housing Finance system on the Housing Market Case

Study: Baghdad Province. Review of International Geographical Education Online.

11(9).

Wadesango and et.al., 2019. The impact of cash flow management on the profitability and

sustainability of small to medium sized enterprises. International Journal of

Entrepreneurship, 23(3). pp.1-19.

Pelz, M., 2019. Can management accounting be helpful for young and small companies?

Systematic review of a paradox. International Journal of Management

Reviews, 21(2). pp.256-274.

Books and Journals.

Weygandt and et.al., 2019. Accounting Principles, Volume 2. John Wiley & Sons.

Oyewo, B., Vo, X.V. and Akinsanmi, T., 2021. Strategy-related factors moderating the fit between

management accounting practice sophistication and organisational effectiveness: the

Global Management Accounting Principles (GMAP) perspective. Spanish Journal of

Finance and Accounting. 50(2). pp.187-223.

Tsuji, M. and Hiraiwa, M., 2018. An analysis of the internal consistency of the new accounting

standard for virtual currencies in generally accepted Japanese accounting principles:

A virtual currency user perspective. 8(2). pp.30-40.

Peters, M.D. and Chiu, C., INTERACTIVE SPREADSHEETING: A LEARNING STRATEGY

AND EXERCISES FOR CALCULATIVE MANAGEMENT ACCOUNTING

PRINCIPLES. Interactive Spreadsheets for Calculative Management Accounting

Principles. Issues in Accounting Education.

Tangngisalu, J., 2022. Current Ratio, Return on Asset, and Debt-to-Equity-Ratio on Stock-Price of

Sector Property and Real Estate. Golden Ratio of Finance Management. 2(1). pp.01-

14.

Koekemoer, S., 2019. Celebrating International Fraud Awareness Week through detection and

prevention of Fraud in the workplace. CIGFARO Journal (Chartered Institute of

Government Finance Audit and Risk Officers). 20(2). pp.10-13.

Ali, Z. and Motlak, J.B., 2021. The Role of Housing Finance system on the Housing Market Case

Study: Baghdad Province. Review of International Geographical Education Online.

11(9).

Wadesango and et.al., 2019. The impact of cash flow management on the profitability and

sustainability of small to medium sized enterprises. International Journal of

Entrepreneurship, 23(3). pp.1-19.

Pelz, M., 2019. Can management accounting be helpful for young and small companies?

Systematic review of a paradox. International Journal of Management

Reviews, 21(2). pp.256-274.

Jermias, J., Gani, L. and Juliana, C., 2018. Performance implications of misalignment among

business strategy, leadership style, organizational culture and management

accounting systems. Leadership Style, Organizational Culture and Management

Accounting Systems (January 9, 2018).

Jeyaraj, S.K., 2020. P121774 KRWSSP Audit Report 2019 and Balance Sheet.

Bruno, A. and Lapsley, I., 2018. The emergence of an accounting practice: The fabrication of a

government accrual accounting system. Accounting, Auditing & Accountability

Journal.

Maelah, R. and Yadzid, N.H.N., 2018. Budgetary control, corporate culture and performance of

small and medium enterprises (SMEs) in Malaysia. International Journal of

Globalisation and Small Business. 10(1). pp.77-99.

Jermias and et.al., 2022. Budgetary control and risk management institutionalization: a field study

of three state-owned enterprises in China. Journal of Accounting & Organizational

Change, (ahead-of-print).

Jamu, V., 2018. An Evaluation of the effectiveness of budgeting and budgetary control on the

financial performance of Delta Beverages Transport Services.

Aliabadi, F.J., Gal, G. and Mashyekhi, B., 2020. Public budgetary roles in Iran: perceptions and

consequences. Qualitative Research in Accounting & Management.

Berland, N., Curtis, E. and Sponem, S., 2018. Exposing organizational tensions with a non-

Traditional budgeting system. Journal of Applied Accounting Research.

business strategy, leadership style, organizational culture and management

accounting systems. Leadership Style, Organizational Culture and Management

Accounting Systems (January 9, 2018).

Jeyaraj, S.K., 2020. P121774 KRWSSP Audit Report 2019 and Balance Sheet.

Bruno, A. and Lapsley, I., 2018. The emergence of an accounting practice: The fabrication of a

government accrual accounting system. Accounting, Auditing & Accountability

Journal.

Maelah, R. and Yadzid, N.H.N., 2018. Budgetary control, corporate culture and performance of

small and medium enterprises (SMEs) in Malaysia. International Journal of

Globalisation and Small Business. 10(1). pp.77-99.

Jermias and et.al., 2022. Budgetary control and risk management institutionalization: a field study

of three state-owned enterprises in China. Journal of Accounting & Organizational

Change, (ahead-of-print).

Jamu, V., 2018. An Evaluation of the effectiveness of budgeting and budgetary control on the

financial performance of Delta Beverages Transport Services.

Aliabadi, F.J., Gal, G. and Mashyekhi, B., 2020. Public budgetary roles in Iran: perceptions and

consequences. Qualitative Research in Accounting & Management.

Berland, N., Curtis, E. and Sponem, S., 2018. Exposing organizational tensions with a non-

Traditional budgeting system. Journal of Applied Accounting Research.

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.