Financial Analysis and Break-Even Calculations

VerifiedAdded on 2020/05/04

|10

|1328

|112

AI Summary

This assignment presents a detailed financial analysis of a hypothetical company. It includes calculations of operating profit, fixed costs, and the breakeven point. Furthermore, it examines the effects of various scenarios, such as a 10% increase in fixed costs, a 15% rise in sales price, and a combination of changes in sales price, volume, variable costs, and fixed costs. The analysis demonstrates how different factors influence profitability and break-even points.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: FUNDAMENTAL OF ACCOUNTING

Fundamental of Accounting

Name of the Student:

Name of the University:

Authors Note:

Fundamental of Accounting

Name of the Student:

Name of the University:

Authors Note:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

FUNDAMENTAL OF ACCOUNTING

1

Table of Contents

Exercise 19.5..............................................................................................................................2

1. Moving average Method:.......................................................................................................2

2. Specific Identifications:.........................................................................................................3

3. FIFO Method:.........................................................................................................................3

Exercise 21.2..............................................................................................................................5

Exercise 22.3..............................................................................................................................6

Exercise 9.2................................................................................................................................7

A. Calculating the overhead rate applicable to each room:.......................................................7

B. Depicting the directly labour and direct expenses that are likely to be applicable to hotel

room for pricing the room rate:..................................................................................................8

Exercise 11.10............................................................................................................................8

A. Calculating the breakeven sales units and breakeven point in dollars:.................................8

B. Calculating the margin safety of the company:.....................................................................9

C. Calculating the company’s profit under different circumstances:.......................................10

1. Variable cost increase by 10%:............................................................................................10

2. Sales volume decrease by 20%:...........................................................................................10

3. Fixed cost increase by 10%:.................................................................................................11

4. Sales price increase by 15%:................................................................................................11

5. Sales price increases by 20%, sales volume decreases by 20%, variable costs increase by

20%, and fixed costs decrease by 20%....................................................................................11

Reference and Bibliography:....................................................................................................13

1

Table of Contents

Exercise 19.5..............................................................................................................................2

1. Moving average Method:.......................................................................................................2

2. Specific Identifications:.........................................................................................................3

3. FIFO Method:.........................................................................................................................3

Exercise 21.2..............................................................................................................................5

Exercise 22.3..............................................................................................................................6

Exercise 9.2................................................................................................................................7

A. Calculating the overhead rate applicable to each room:.......................................................7

B. Depicting the directly labour and direct expenses that are likely to be applicable to hotel

room for pricing the room rate:..................................................................................................8

Exercise 11.10............................................................................................................................8

A. Calculating the breakeven sales units and breakeven point in dollars:.................................8

B. Calculating the margin safety of the company:.....................................................................9

C. Calculating the company’s profit under different circumstances:.......................................10

1. Variable cost increase by 10%:............................................................................................10

2. Sales volume decrease by 20%:...........................................................................................10

3. Fixed cost increase by 10%:.................................................................................................11

4. Sales price increase by 15%:................................................................................................11

5. Sales price increases by 20%, sales volume decreases by 20%, variable costs increase by

20%, and fixed costs decrease by 20%....................................................................................11

Reference and Bibliography:....................................................................................................13

FUNDAMENTAL OF ACCOUNTING

2

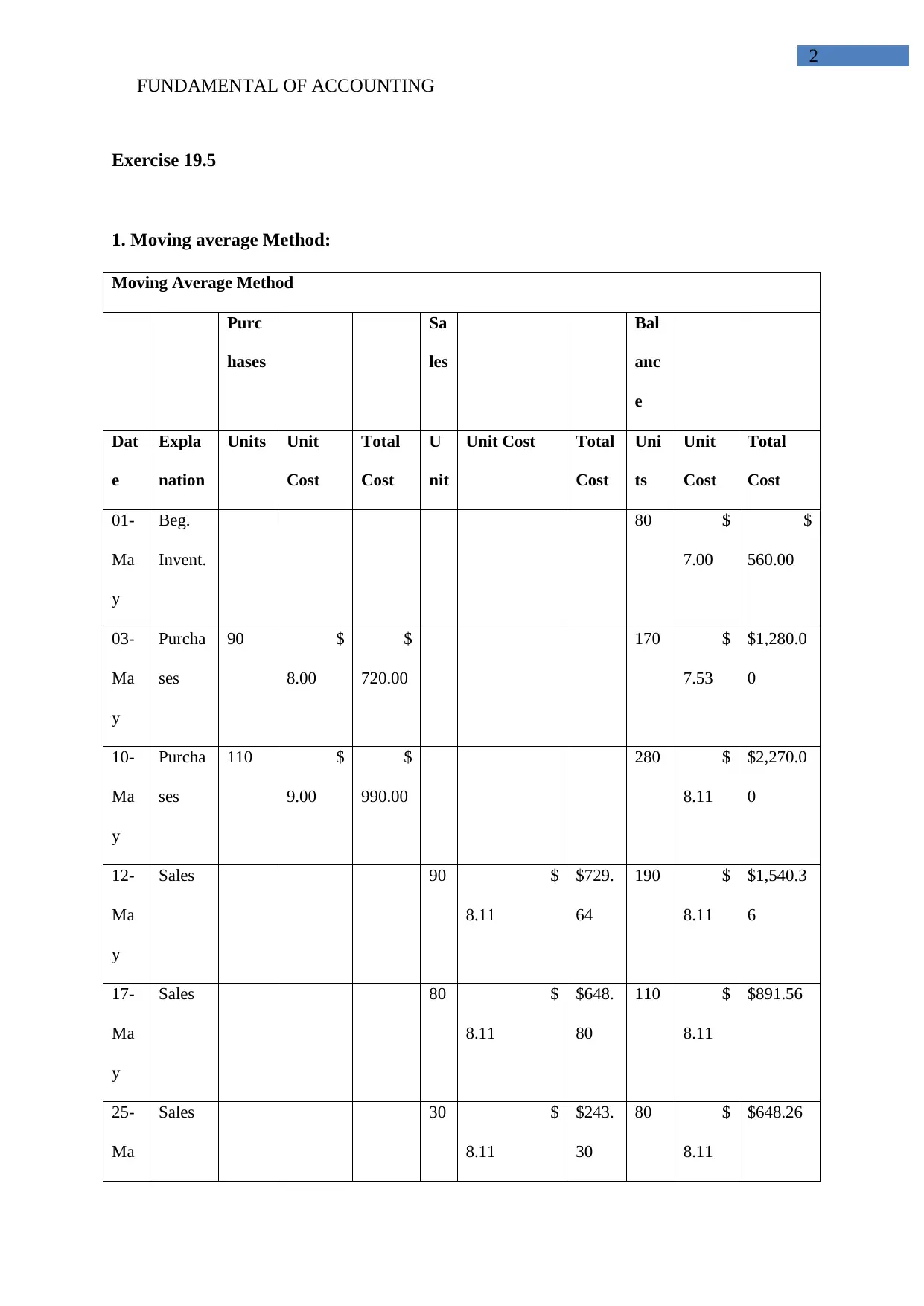

Exercise 19.5

1. Moving average Method:

Moving Average Method

Purc

hases

Sa

les

Bal

anc

e

Dat

e

Expla

nation

Units Unit

Cost

Total

Cost

U

nit

Unit Cost Total

Cost

Uni

ts

Unit

Cost

Total

Cost

01-

Ma

y

Beg.

Invent.

80 $

7.00

$

560.00

03-

Ma

y

Purcha

ses

90 $

8.00

$

720.00

170 $

7.53

$1,280.0

0

10-

Ma

y

Purcha

ses

110 $

9.00

$

990.00

280 $

8.11

$2,270.0

0

12-

Ma

y

Sales 90 $

8.11

$729.

64

190 $

8.11

$1,540.3

6

17-

Ma

y

Sales 80 $

8.11

$648.

80

110 $

8.11

$891.56

25-

Ma

Sales 30 $

8.11

$243.

30

80 $

8.11

$648.26

2

Exercise 19.5

1. Moving average Method:

Moving Average Method

Purc

hases

Sa

les

Bal

anc

e

Dat

e

Expla

nation

Units Unit

Cost

Total

Cost

U

nit

Unit Cost Total

Cost

Uni

ts

Unit

Cost

Total

Cost

01-

Ma

y

Beg.

Invent.

80 $

7.00

$

560.00

03-

Ma

y

Purcha

ses

90 $

8.00

$

720.00

170 $

7.53

$1,280.0

0

10-

Ma

y

Purcha

ses

110 $

9.00

$

990.00

280 $

8.11

$2,270.0

0

12-

Ma

y

Sales 90 $

8.11

$729.

64

190 $

8.11

$1,540.3

6

17-

Ma

y

Sales 80 $

8.11

$648.

80

110 $

8.11

$891.56

25-

Ma

Sales 30 $

8.11

$243.

30

80 $

8.11

$648.26

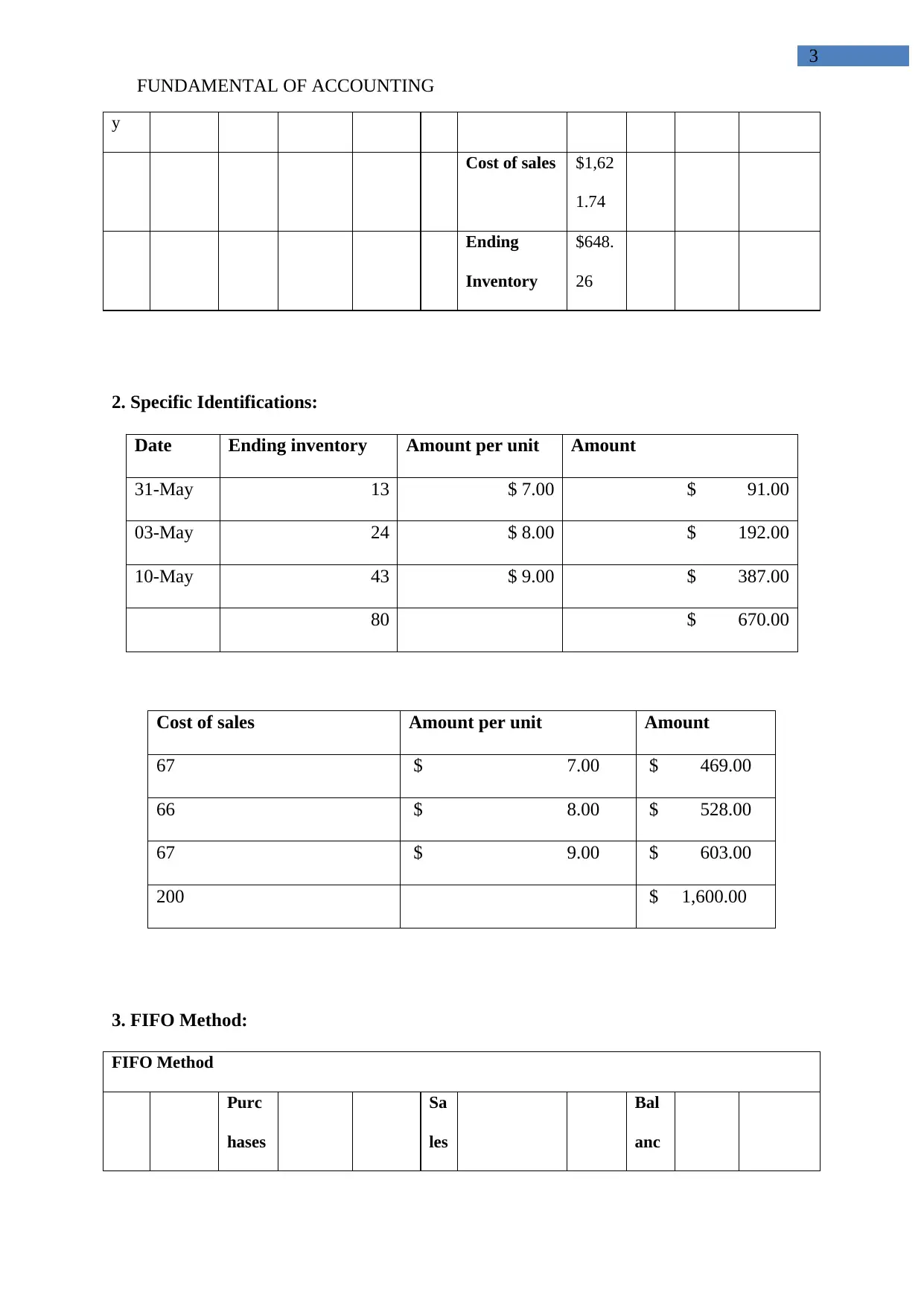

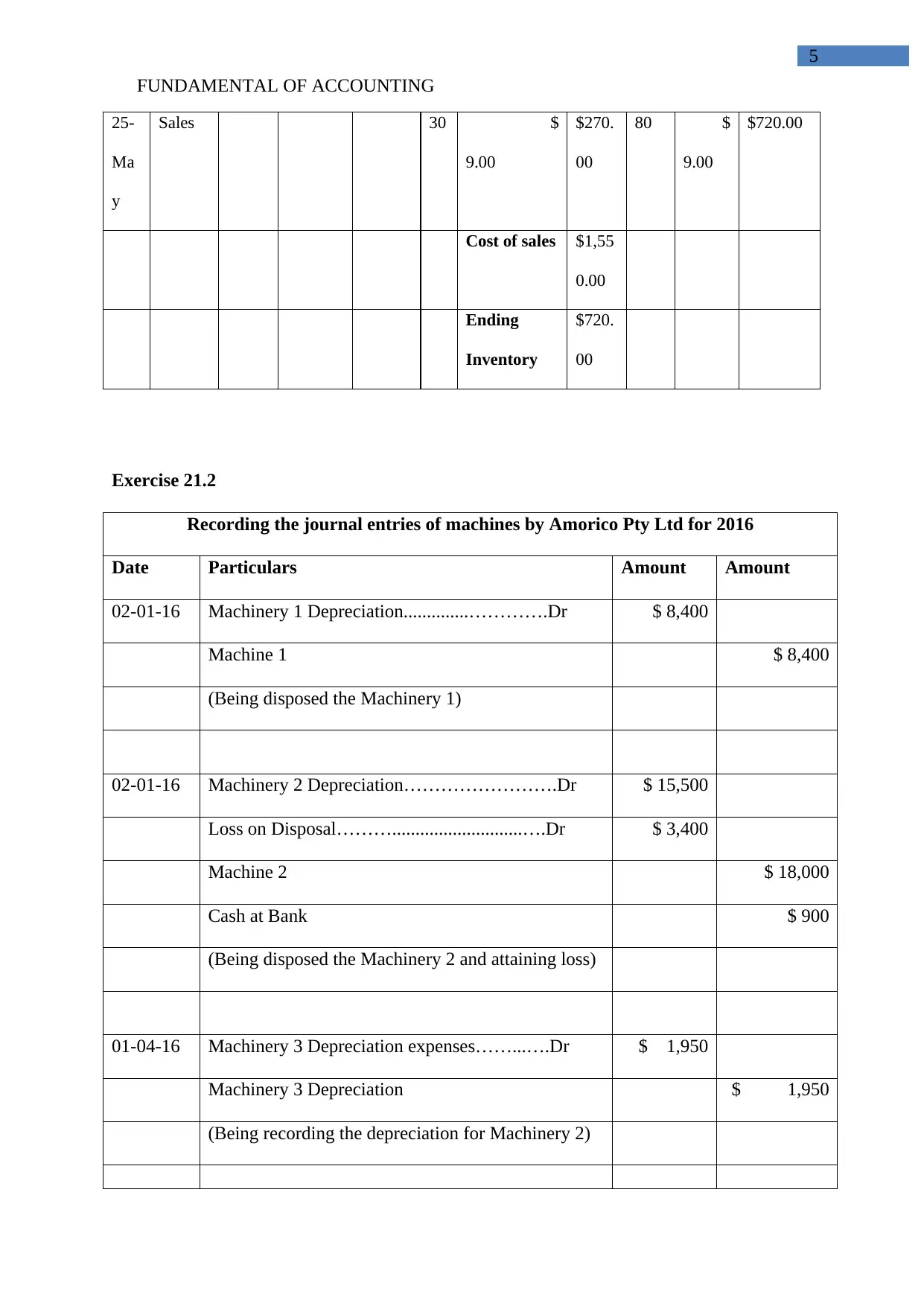

FUNDAMENTAL OF ACCOUNTING

3

y

Cost of sales $1,62

1.74

Ending

Inventory

$648.

26

2. Specific Identifications:

Date Ending inventory Amount per unit Amount

31-May 13 $ 7.00 $ 91.00

03-May 24 $ 8.00 $ 192.00

10-May 43 $ 9.00 $ 387.00

80 $ 670.00

Cost of sales Amount per unit Amount

67 $ 7.00 $ 469.00

66 $ 8.00 $ 528.00

67 $ 9.00 $ 603.00

200 $ 1,600.00

3. FIFO Method:

FIFO Method

Purc

hases

Sa

les

Bal

anc

3

y

Cost of sales $1,62

1.74

Ending

Inventory

$648.

26

2. Specific Identifications:

Date Ending inventory Amount per unit Amount

31-May 13 $ 7.00 $ 91.00

03-May 24 $ 8.00 $ 192.00

10-May 43 $ 9.00 $ 387.00

80 $ 670.00

Cost of sales Amount per unit Amount

67 $ 7.00 $ 469.00

66 $ 8.00 $ 528.00

67 $ 9.00 $ 603.00

200 $ 1,600.00

3. FIFO Method:

FIFO Method

Purc

hases

Sa

les

Bal

anc

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

FUNDAMENTAL OF ACCOUNTING

4

e

Dat

e

Expla

nation

Units Unit

Cost

Total

Cost

U

nit

Unit Cost Total

Cost

Uni

ts

Unit

Cost

Total

Cost

01-

Ma

y

Beg.

Invent.

80 $

7.00

$

560.00

80 $

7.00

03-

Ma

y

Purcha

ses

90 $

8.00

$

720.00

90 $

8.00

$1,280.0

0

80 $

7.00

90 $

8.00

10-

Ma

y

Purcha

ses

110 $

9.00

$

990.00

110 $

9.00

$2,270.0

0

12-

Ma

y

Sales 80 $

7.00

$560.

00

80 $

8.00

12-

Ma

y

Sales 10 $

8.00

$80.0

0

110 $

9.00

$1,630.0

0

17-

Ma

y

Sales 80 $

8.00

$640.

00

110 $

9.00

$990.00

4

e

Dat

e

Expla

nation

Units Unit

Cost

Total

Cost

U

nit

Unit Cost Total

Cost

Uni

ts

Unit

Cost

Total

Cost

01-

Ma

y

Beg.

Invent.

80 $

7.00

$

560.00

80 $

7.00

03-

Ma

y

Purcha

ses

90 $

8.00

$

720.00

90 $

8.00

$1,280.0

0

80 $

7.00

90 $

8.00

10-

Ma

y

Purcha

ses

110 $

9.00

$

990.00

110 $

9.00

$2,270.0

0

12-

Ma

y

Sales 80 $

7.00

$560.

00

80 $

8.00

12-

Ma

y

Sales 10 $

8.00

$80.0

0

110 $

9.00

$1,630.0

0

17-

Ma

y

Sales 80 $

8.00

$640.

00

110 $

9.00

$990.00

FUNDAMENTAL OF ACCOUNTING

5

25-

Ma

y

Sales 30 $

9.00

$270.

00

80 $

9.00

$720.00

Cost of sales $1,55

0.00

Ending

Inventory

$720.

00

Exercise 21.2

Recording the journal entries of machines by Amorico Pty Ltd for 2016

Date Particulars Amount Amount

02-01-16 Machinery 1 Depreciation..............………….Dr $ 8,400

Machine 1 $ 8,400

(Being disposed the Machinery 1)

02-01-16 Machinery 2 Depreciation…………………….Dr $ 15,500

Loss on Disposal………............................….Dr $ 3,400

Machine 2 $ 18,000

Cash at Bank $ 900

(Being disposed the Machinery 2 and attaining loss)

01-04-16 Machinery 3 Depreciation expenses……...….Dr $ 1,950

Machinery 3 Depreciation $ 1,950

(Being recording the depreciation for Machinery 2)

5

25-

Ma

y

Sales 30 $

9.00

$270.

00

80 $

9.00

$720.00

Cost of sales $1,55

0.00

Ending

Inventory

$720.

00

Exercise 21.2

Recording the journal entries of machines by Amorico Pty Ltd for 2016

Date Particulars Amount Amount

02-01-16 Machinery 1 Depreciation..............………….Dr $ 8,400

Machine 1 $ 8,400

(Being disposed the Machinery 1)

02-01-16 Machinery 2 Depreciation…………………….Dr $ 15,500

Loss on Disposal………............................….Dr $ 3,400

Machine 2 $ 18,000

Cash at Bank $ 900

(Being disposed the Machinery 2 and attaining loss)

01-04-16 Machinery 3 Depreciation expenses……...….Dr $ 1,950

Machinery 3 Depreciation $ 1,950

(Being recording the depreciation for Machinery 2)

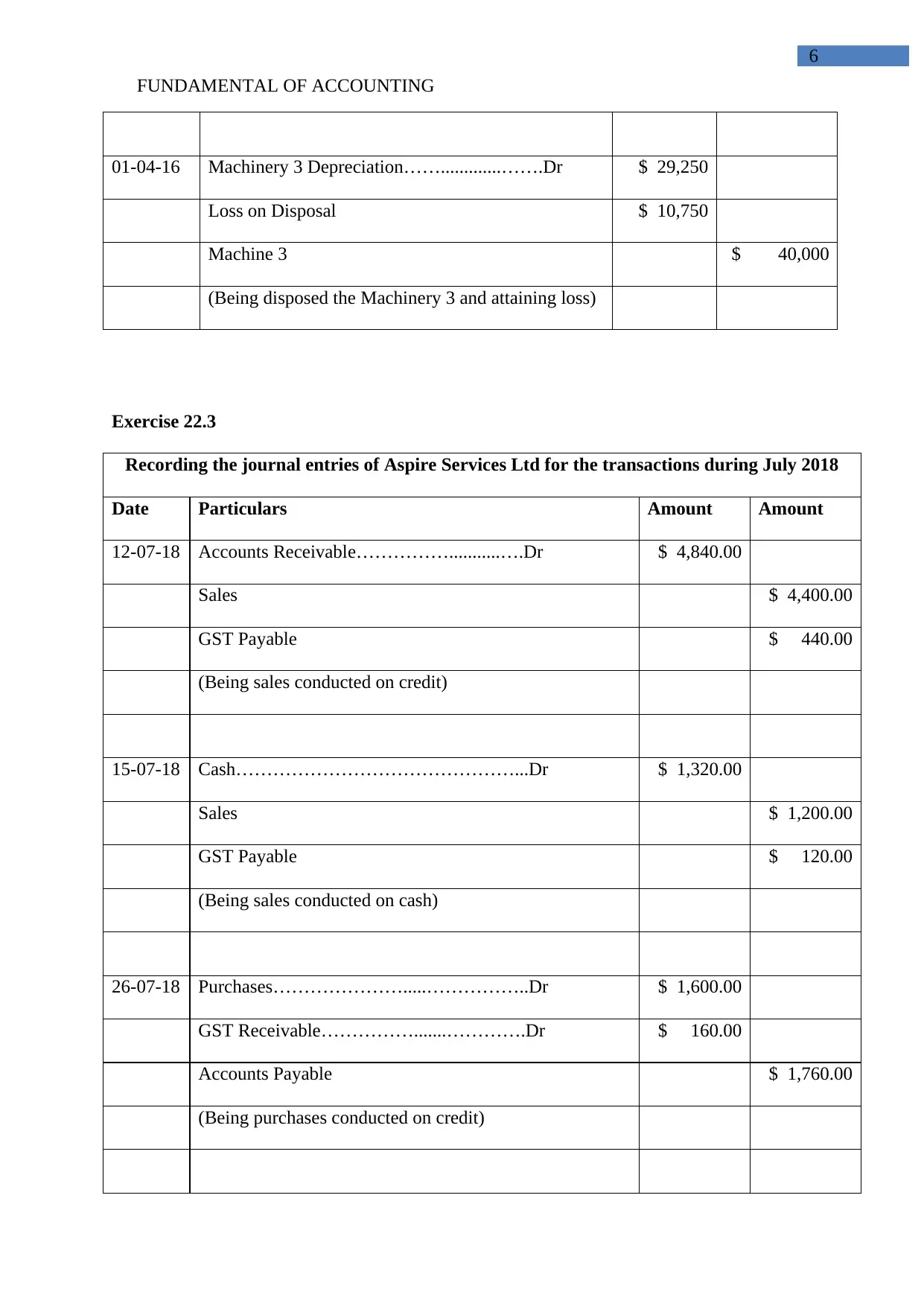

FUNDAMENTAL OF ACCOUNTING

6

01-04-16 Machinery 3 Depreciation…….............…….Dr $ 29,250

Loss on Disposal $ 10,750

Machine 3 $ 40,000

(Being disposed the Machinery 3 and attaining loss)

Exercise 22.3

Recording the journal entries of Aspire Services Ltd for the transactions during July 2018

Date Particulars Amount Amount

12-07-18 Accounts Receivable……………...........….Dr $ 4,840.00

Sales $ 4,400.00

GST Payable $ 440.00

(Being sales conducted on credit)

15-07-18 Cash………………………………………...Dr $ 1,320.00

Sales $ 1,200.00

GST Payable $ 120.00

(Being sales conducted on cash)

26-07-18 Purchases………………….....……………..Dr $ 1,600.00

GST Receivable…………….......………….Dr $ 160.00

Accounts Payable $ 1,760.00

(Being purchases conducted on credit)

6

01-04-16 Machinery 3 Depreciation…….............…….Dr $ 29,250

Loss on Disposal $ 10,750

Machine 3 $ 40,000

(Being disposed the Machinery 3 and attaining loss)

Exercise 22.3

Recording the journal entries of Aspire Services Ltd for the transactions during July 2018

Date Particulars Amount Amount

12-07-18 Accounts Receivable……………...........….Dr $ 4,840.00

Sales $ 4,400.00

GST Payable $ 440.00

(Being sales conducted on credit)

15-07-18 Cash………………………………………...Dr $ 1,320.00

Sales $ 1,200.00

GST Payable $ 120.00

(Being sales conducted on cash)

26-07-18 Purchases………………….....……………..Dr $ 1,600.00

GST Receivable…………….......………….Dr $ 160.00

Accounts Payable $ 1,760.00

(Being purchases conducted on credit)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

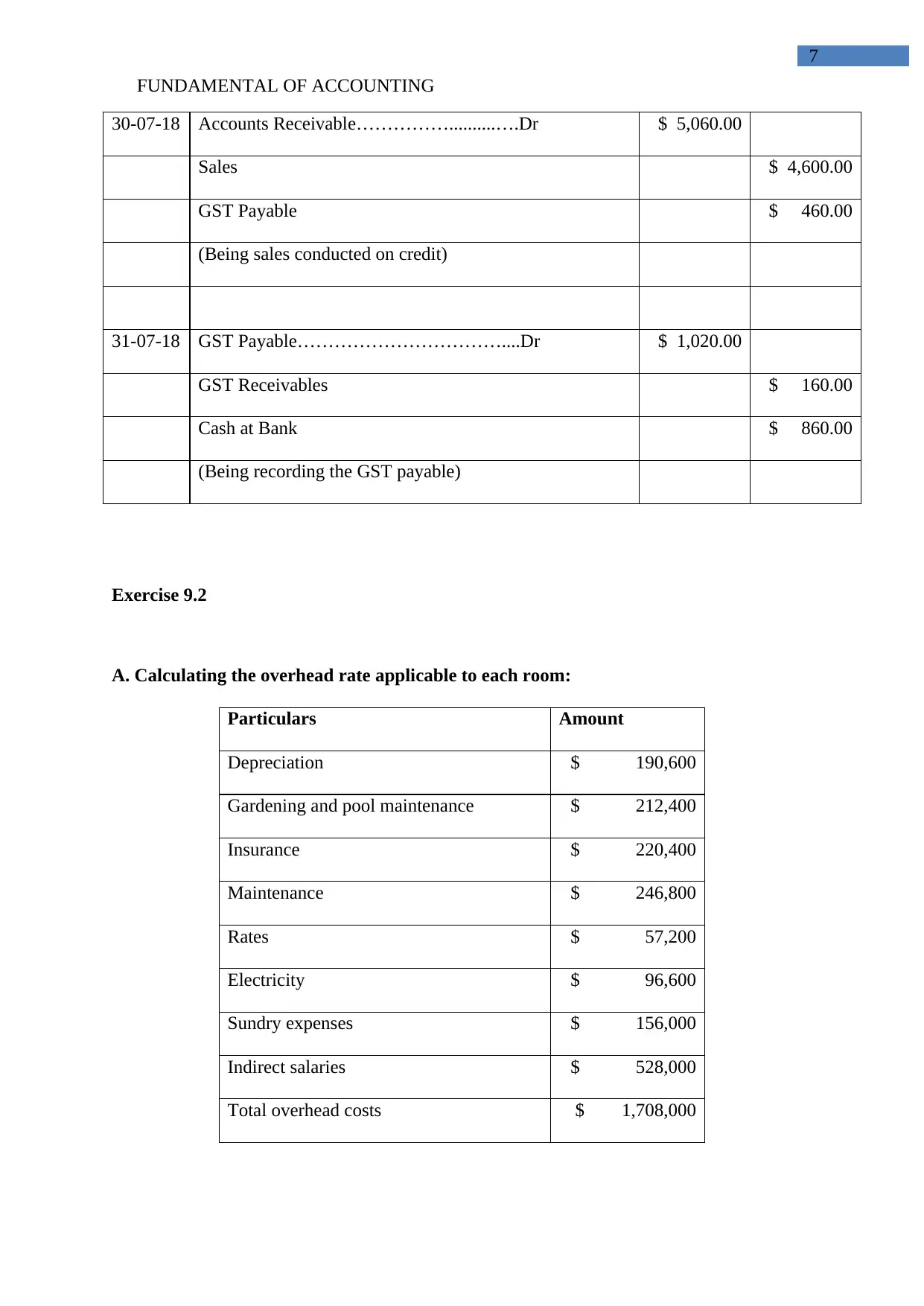

FUNDAMENTAL OF ACCOUNTING

7

30-07-18 Accounts Receivable……………..........….Dr $ 5,060.00

Sales $ 4,600.00

GST Payable $ 460.00

(Being sales conducted on credit)

31-07-18 GST Payable……………………………....Dr $ 1,020.00

GST Receivables $ 160.00

Cash at Bank $ 860.00

(Being recording the GST payable)

Exercise 9.2

A. Calculating the overhead rate applicable to each room:

Particulars Amount

Depreciation $ 190,600

Gardening and pool maintenance $ 212,400

Insurance $ 220,400

Maintenance $ 246,800

Rates $ 57,200

Electricity $ 96,600

Sundry expenses $ 156,000

Indirect salaries $ 528,000

Total overhead costs $ 1,708,000

7

30-07-18 Accounts Receivable……………..........….Dr $ 5,060.00

Sales $ 4,600.00

GST Payable $ 460.00

(Being sales conducted on credit)

31-07-18 GST Payable……………………………....Dr $ 1,020.00

GST Receivables $ 160.00

Cash at Bank $ 860.00

(Being recording the GST payable)

Exercise 9.2

A. Calculating the overhead rate applicable to each room:

Particulars Amount

Depreciation $ 190,600

Gardening and pool maintenance $ 212,400

Insurance $ 220,400

Maintenance $ 246,800

Rates $ 57,200

Electricity $ 96,600

Sundry expenses $ 156,000

Indirect salaries $ 528,000

Total overhead costs $ 1,708,000

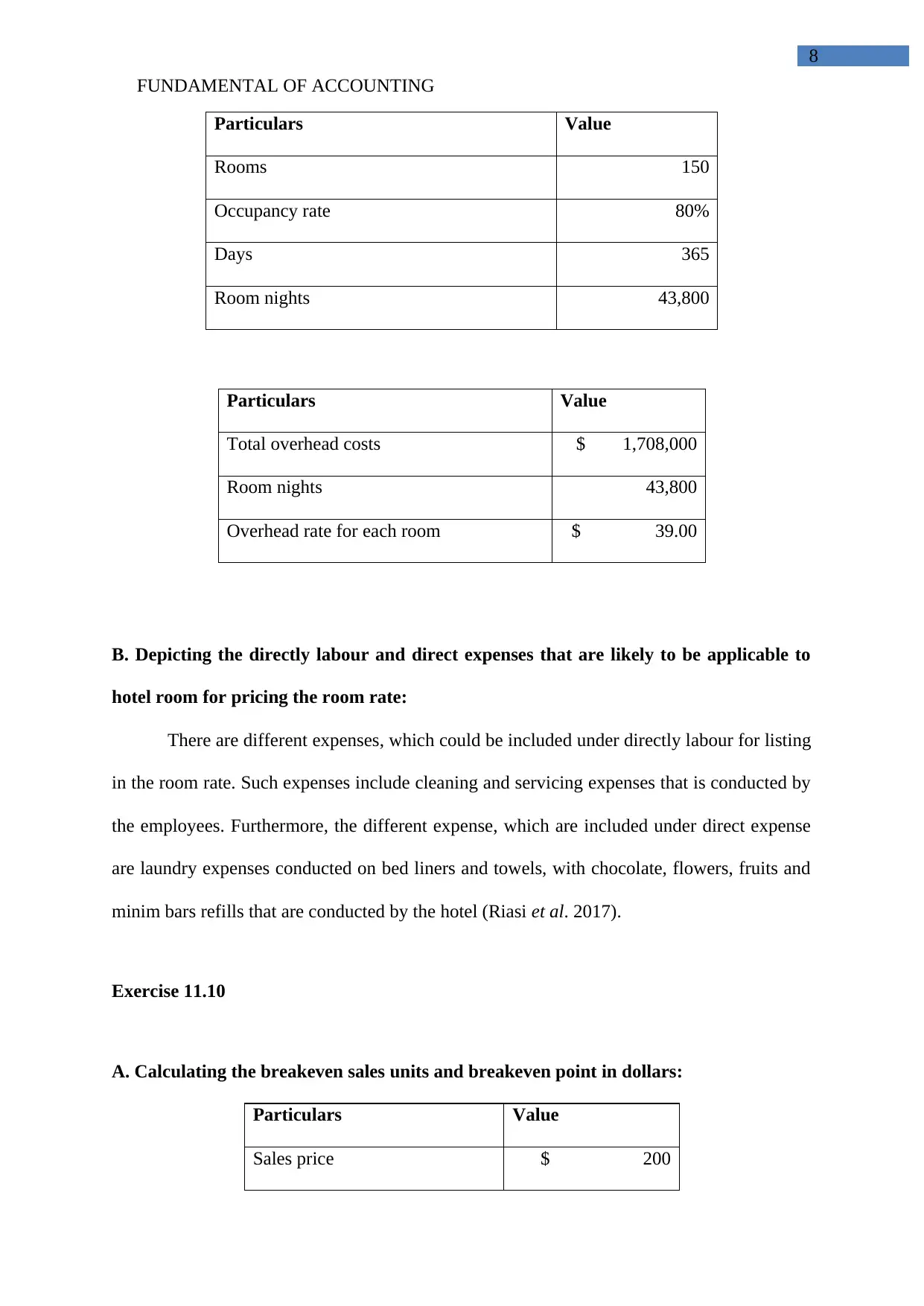

FUNDAMENTAL OF ACCOUNTING

8

Particulars Value

Rooms 150

Occupancy rate 80%

Days 365

Room nights 43,800

Particulars Value

Total overhead costs $ 1,708,000

Room nights 43,800

Overhead rate for each room $ 39.00

B. Depicting the directly labour and direct expenses that are likely to be applicable to

hotel room for pricing the room rate:

There are different expenses, which could be included under directly labour for listing

in the room rate. Such expenses include cleaning and servicing expenses that is conducted by

the employees. Furthermore, the different expense, which are included under direct expense

are laundry expenses conducted on bed liners and towels, with chocolate, flowers, fruits and

minim bars refills that are conducted by the hotel (Riasi et al. 2017).

Exercise 11.10

A. Calculating the breakeven sales units and breakeven point in dollars:

Particulars Value

Sales price $ 200

8

Particulars Value

Rooms 150

Occupancy rate 80%

Days 365

Room nights 43,800

Particulars Value

Total overhead costs $ 1,708,000

Room nights 43,800

Overhead rate for each room $ 39.00

B. Depicting the directly labour and direct expenses that are likely to be applicable to

hotel room for pricing the room rate:

There are different expenses, which could be included under directly labour for listing

in the room rate. Such expenses include cleaning and servicing expenses that is conducted by

the employees. Furthermore, the different expense, which are included under direct expense

are laundry expenses conducted on bed liners and towels, with chocolate, flowers, fruits and

minim bars refills that are conducted by the hotel (Riasi et al. 2017).

Exercise 11.10

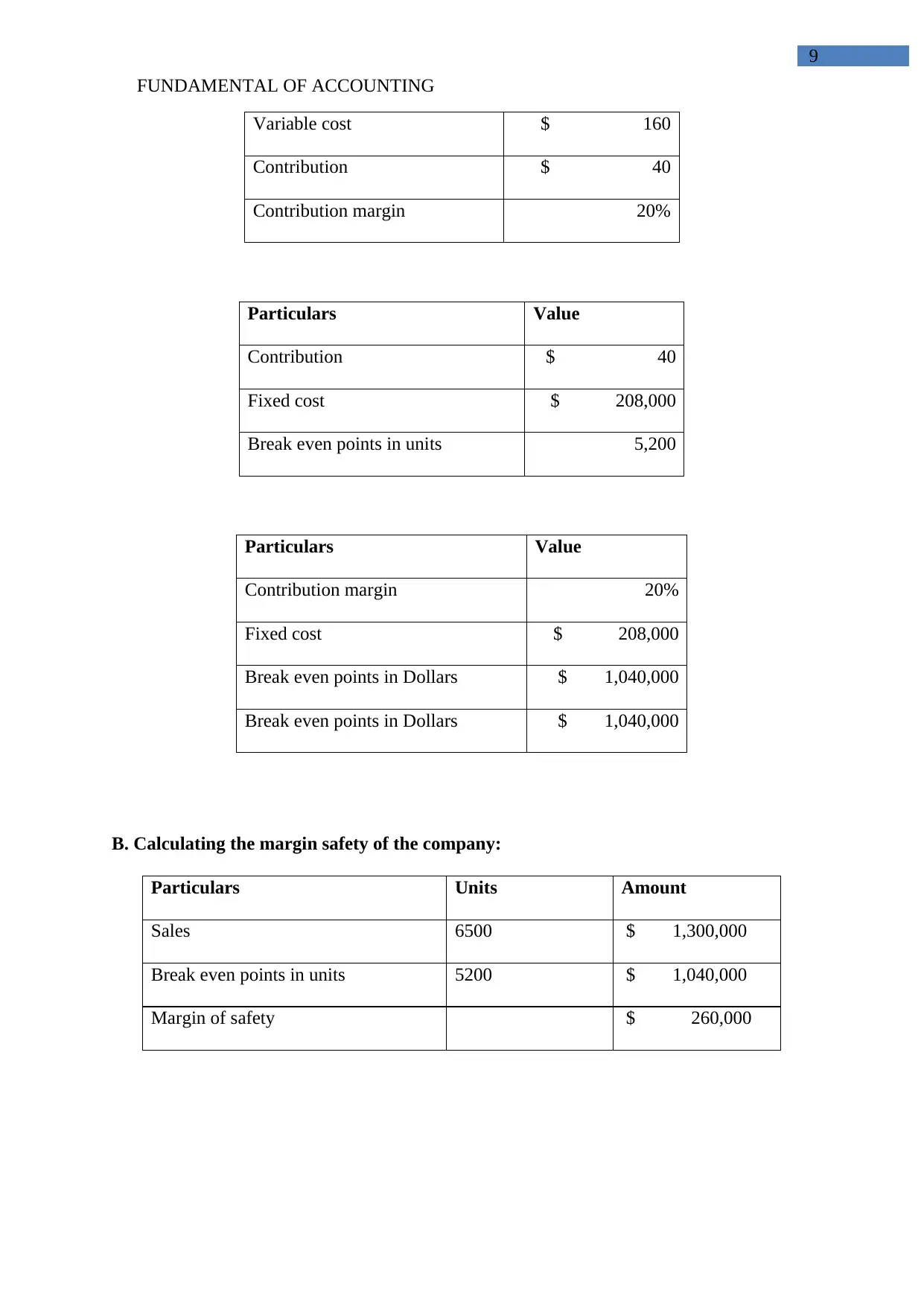

A. Calculating the breakeven sales units and breakeven point in dollars:

Particulars Value

Sales price $ 200

FUNDAMENTAL OF ACCOUNTING

9

Variable cost $ 160

Contribution $ 40

Contribution margin 20%

Particulars Value

Contribution $ 40

Fixed cost $ 208,000

Break even points in units 5,200

Particulars Value

Contribution margin 20%

Fixed cost $ 208,000

Break even points in Dollars $ 1,040,000

Break even points in Dollars $ 1,040,000

B. Calculating the margin safety of the company:

Particulars Units Amount

Sales 6500 $ 1,300,000

Break even points in units 5200 $ 1,040,000

Margin of safety $ 260,000

9

Variable cost $ 160

Contribution $ 40

Contribution margin 20%

Particulars Value

Contribution $ 40

Fixed cost $ 208,000

Break even points in units 5,200

Particulars Value

Contribution margin 20%

Fixed cost $ 208,000

Break even points in Dollars $ 1,040,000

Break even points in Dollars $ 1,040,000

B. Calculating the margin safety of the company:

Particulars Units Amount

Sales 6500 $ 1,300,000

Break even points in units 5200 $ 1,040,000

Margin of safety $ 260,000

1 out of 10

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.