Project Evaluation Report: BAF-5-FOF Fundamentals of Finance

VerifiedAdded on 2022/08/23

|8

|2061

|15

Report

AI Summary

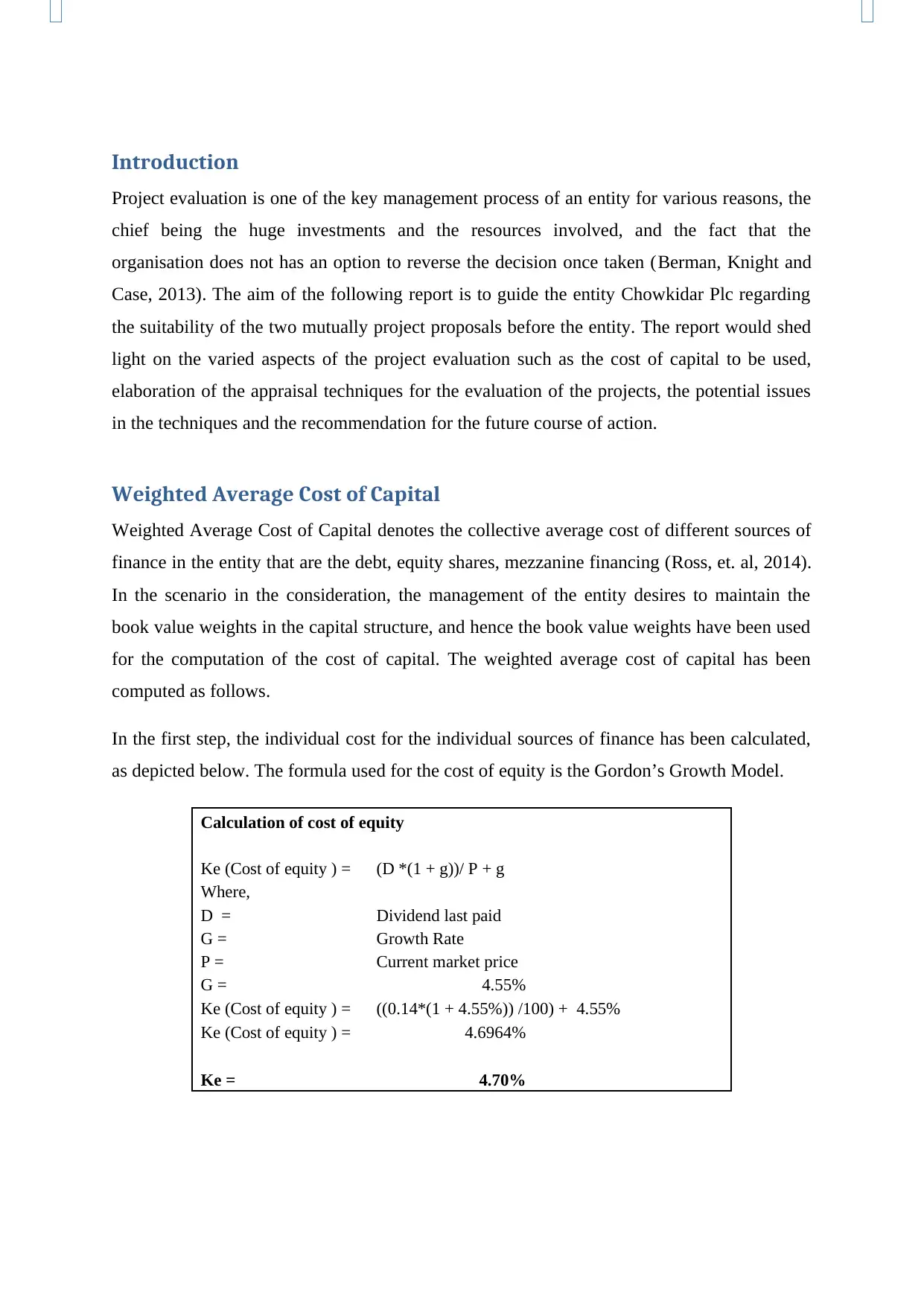

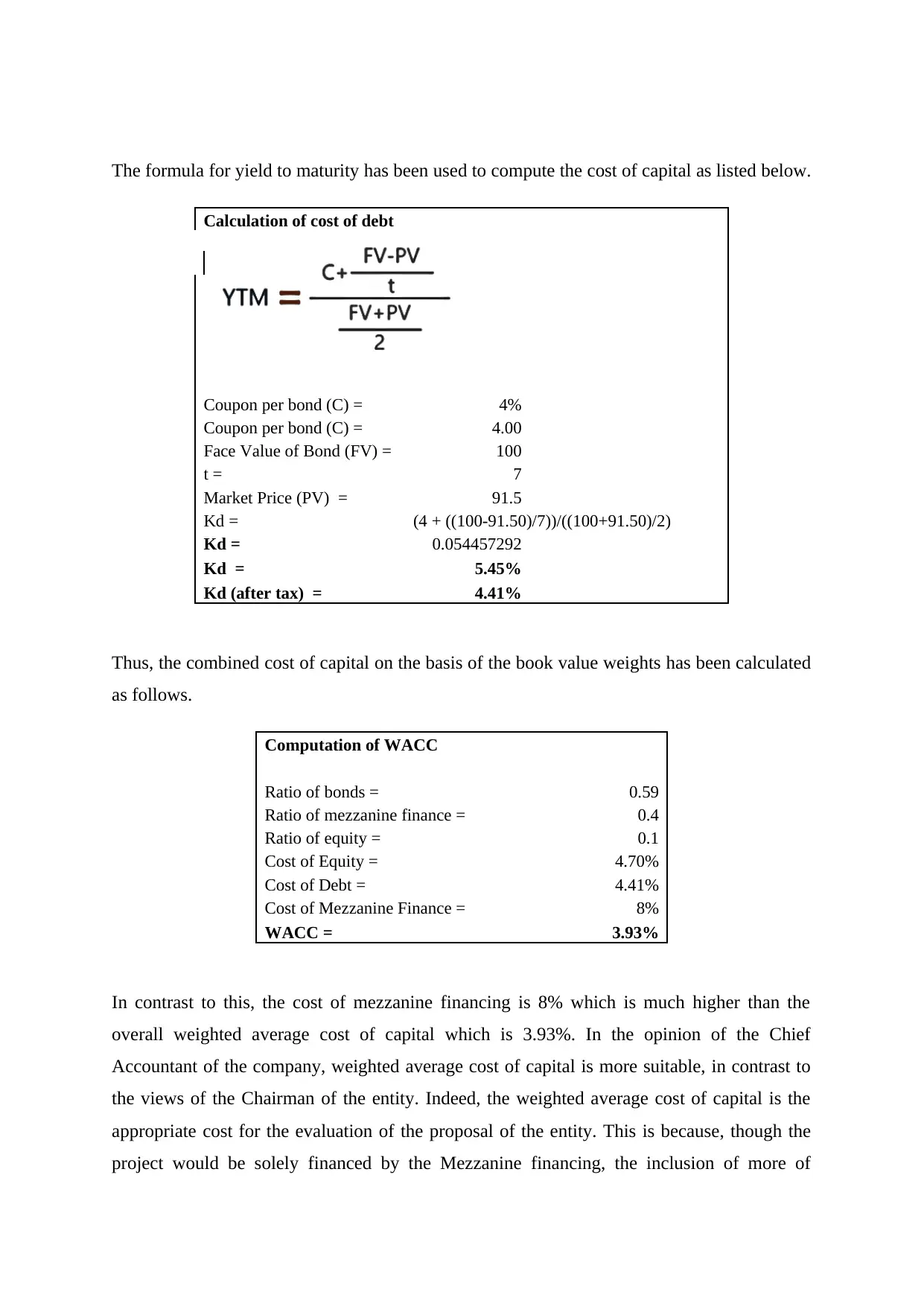

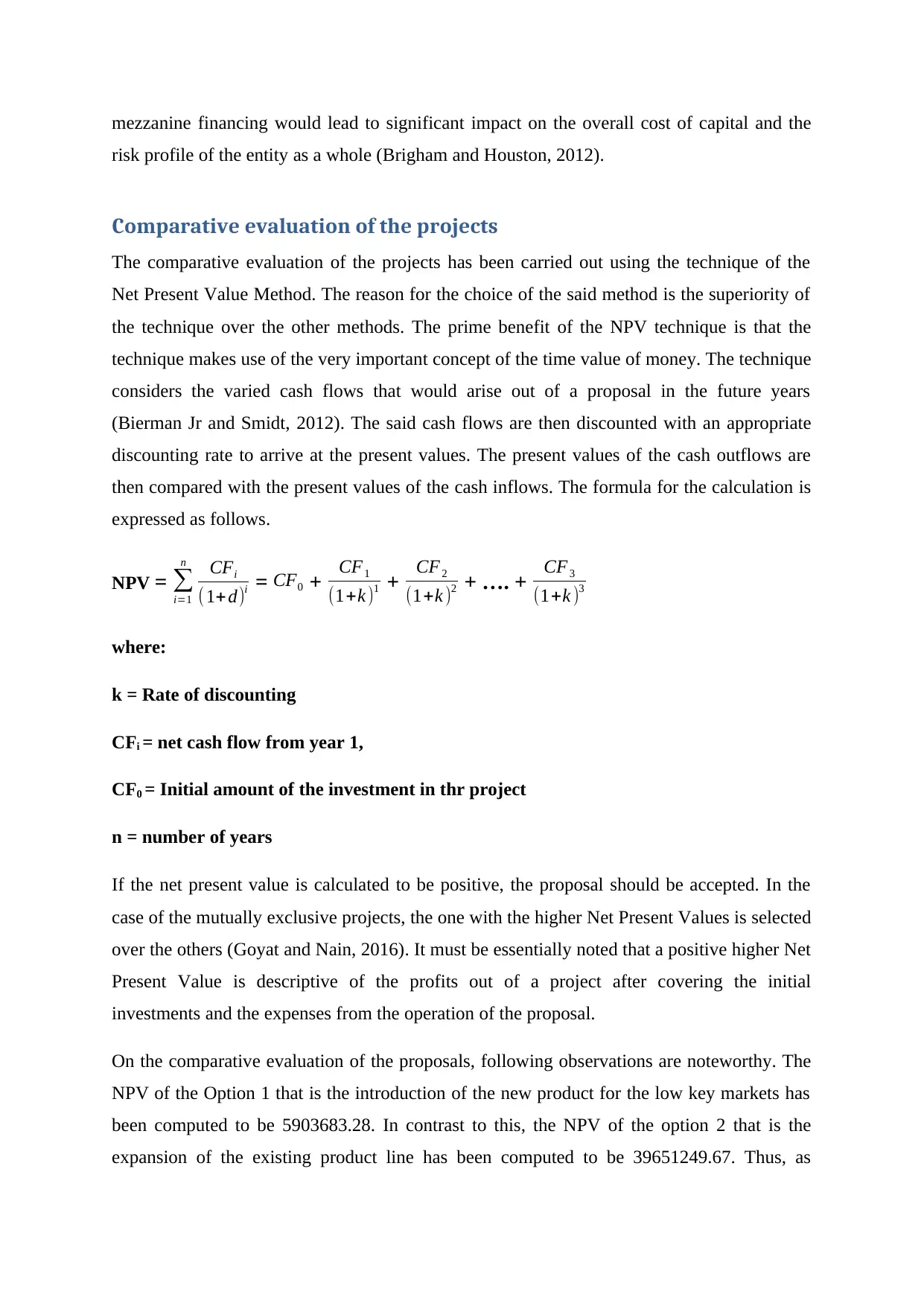

This report evaluates two project proposals for Chowkidar Plc, focusing on financial analysis and investment decision-making. It begins by calculating the Weighted Average Cost of Capital (WACC), comparing the cost of equity, debt, and mezzanine financing to determine the appropriate discount rate. The report then employs the Net Present Value (NPV) method to assess the projects, explaining the treatment of costs like research and development and opportunity costs. Furthermore, it explores the Internal Rate of Return (IRR) and cash payback period techniques, while acknowledging their limitations. The analysis recommends a specific project based on the WACC and considers external factors like market conditions. The report concludes with recommendations and a comprehensive list of references.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.