Fundamentals of Accounting II: Case Studies and Depreciation Methods

VerifiedAdded on 2023/06/03

|11

|1795

|124

AI Summary

This article covers case studies and depreciation methods for Fundamentals of Accounting II course. It includes topics such as purchase price, straight-line method, diminishing balance method, sum of year digit method, and units of production method.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Unit: ACC102 – Fundamentals of Accounting II

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

TABLE OF CONTENTS

Case study one.................................................................................................................................3

Part (a).........................................................................................................................................3

Part (b).........................................................................................................................................3

Part (c).........................................................................................................................................3

Part (d).........................................................................................................................................5

Part (e).........................................................................................................................................5

Case study two.................................................................................................................................6

Part (a).........................................................................................................................................6

Part (b).........................................................................................................................................7

Part (c).........................................................................................................................................7

Case study three...............................................................................................................................8

1. Depreciation by the straight line method.................................................................................8

2. Depreciation by Diminishing balance method........................................................................8

3. Deprecation by the sum of year digit method..........................................................................9

4. Depreciation by units of production........................................................................................9

References......................................................................................................................................11

Case study one.................................................................................................................................3

Part (a).........................................................................................................................................3

Part (b).........................................................................................................................................3

Part (c).........................................................................................................................................3

Part (d).........................................................................................................................................5

Part (e).........................................................................................................................................5

Case study two.................................................................................................................................6

Part (a).........................................................................................................................................6

Part (b).........................................................................................................................................7

Part (c).........................................................................................................................................7

Case study three...............................................................................................................................8

1. Depreciation by the straight line method.................................................................................8

2. Depreciation by Diminishing balance method........................................................................8

3. Deprecation by the sum of year digit method..........................................................................9

4. Depreciation by units of production........................................................................................9

References......................................................................................................................................11

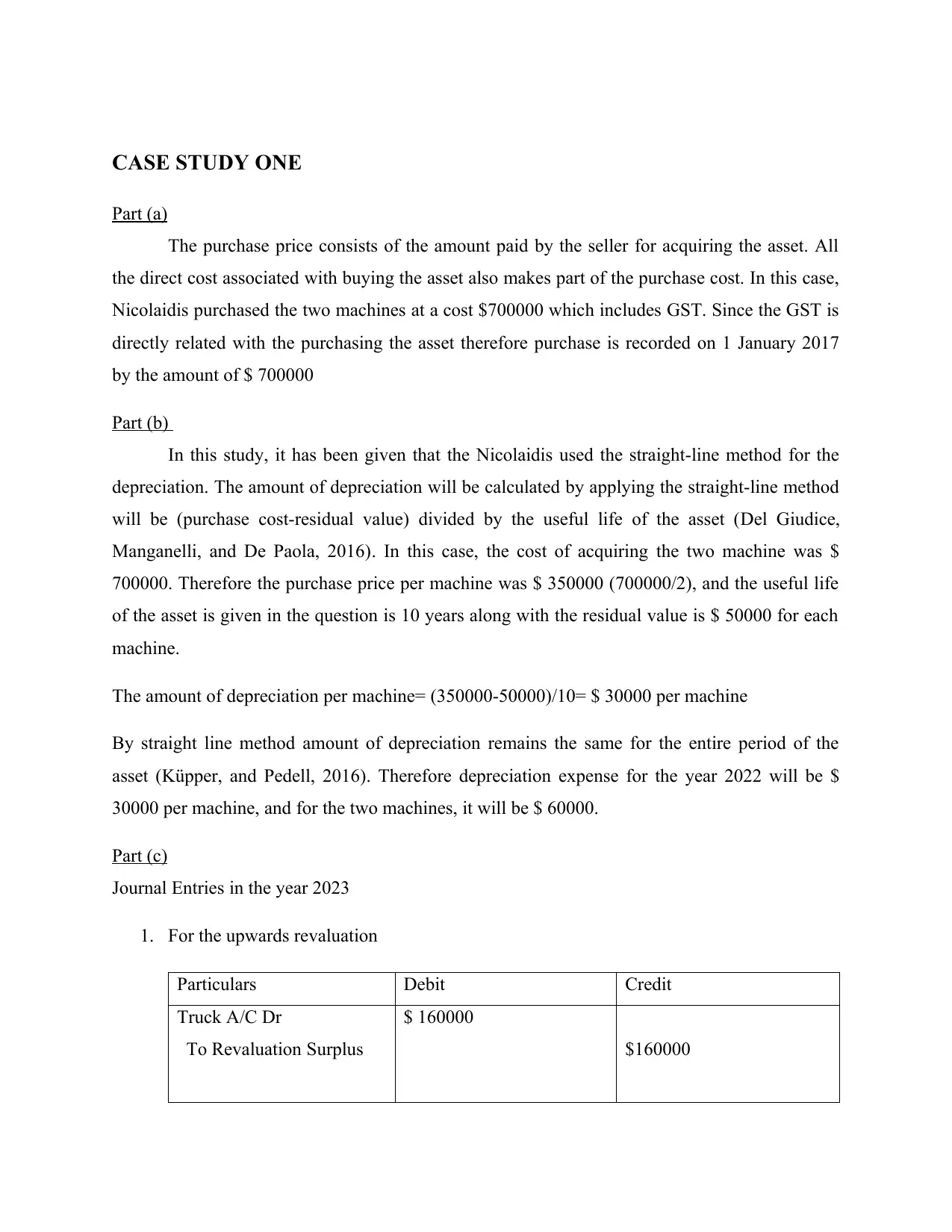

CASE STUDY ONE

Part (a)

The purchase price consists of the amount paid by the seller for acquiring the asset. All

the direct cost associated with buying the asset also makes part of the purchase cost. In this case,

Nicolaidis purchased the two machines at a cost $700000 which includes GST. Since the GST is

directly related with the purchasing the asset therefore purchase is recorded on 1 January 2017

by the amount of $ 700000

Part (b)

In this study, it has been given that the Nicolaidis used the straight-line method for the

depreciation. The amount of depreciation will be calculated by applying the straight-line method

will be (purchase cost-residual value) divided by the useful life of the asset (Del Giudice,

Manganelli, and De Paola, 2016). In this case, the cost of acquiring the two machine was $

700000. Therefore the purchase price per machine was $ 350000 (700000/2), and the useful life

of the asset is given in the question is 10 years along with the residual value is $ 50000 for each

machine.

The amount of depreciation per machine= (350000-50000)/10= $ 30000 per machine

By straight line method amount of depreciation remains the same for the entire period of the

asset (Küpper, and Pedell, 2016). Therefore depreciation expense for the year 2022 will be $

30000 per machine, and for the two machines, it will be $ 60000.

Part (c)

Journal Entries in the year 2023

1. For the upwards revaluation

Particulars Debit Credit

Truck A/C Dr

To Revaluation Surplus

$ 160000

$160000

Part (a)

The purchase price consists of the amount paid by the seller for acquiring the asset. All

the direct cost associated with buying the asset also makes part of the purchase cost. In this case,

Nicolaidis purchased the two machines at a cost $700000 which includes GST. Since the GST is

directly related with the purchasing the asset therefore purchase is recorded on 1 January 2017

by the amount of $ 700000

Part (b)

In this study, it has been given that the Nicolaidis used the straight-line method for the

depreciation. The amount of depreciation will be calculated by applying the straight-line method

will be (purchase cost-residual value) divided by the useful life of the asset (Del Giudice,

Manganelli, and De Paola, 2016). In this case, the cost of acquiring the two machine was $

700000. Therefore the purchase price per machine was $ 350000 (700000/2), and the useful life

of the asset is given in the question is 10 years along with the residual value is $ 50000 for each

machine.

The amount of depreciation per machine= (350000-50000)/10= $ 30000 per machine

By straight line method amount of depreciation remains the same for the entire period of the

asset (Küpper, and Pedell, 2016). Therefore depreciation expense for the year 2022 will be $

30000 per machine, and for the two machines, it will be $ 60000.

Part (c)

Journal Entries in the year 2023

1. For the upwards revaluation

Particulars Debit Credit

Truck A/C Dr

To Revaluation Surplus

$ 160000

$160000

2. Depreciation on the truck after revaluation

Particulars Debit Credit

Depreciation Dr

To Truck

$ 70000

$70000

Working Note

year Depreciation Price at the end of year

2017 30000 320000

2018 30000 290000

2019 30000 260000

2020 30000 230000

2021 30000 200000

2022 30000 170000

2023 30000 140000

2024 30000 110000

2025 30000 80000

2026 30000 50000

From the above table, it has been seen that the value of each truck at the end of 2022 is $

170000, for the two trucks it was $ 340000. The trucks were revalued upward at the beginning of

2023 by $ 80000 each. Total revaluation for both the machine was $ 160000. The revised price

of an asset is $ 340000+$160000 that is 500000; however, the residual value would be $ 80000

and the revised life of the asset 6 years.

Therefore the depreciation (500000-80000)/6= $70000 for both machines

It has been assumed that the residual value given in the question was for both the machines.

3. Transfer of the depreciation in the income statement

Particulars Debit Credit

Particulars Debit Credit

Depreciation Dr

To Truck

$ 70000

$70000

Working Note

year Depreciation Price at the end of year

2017 30000 320000

2018 30000 290000

2019 30000 260000

2020 30000 230000

2021 30000 200000

2022 30000 170000

2023 30000 140000

2024 30000 110000

2025 30000 80000

2026 30000 50000

From the above table, it has been seen that the value of each truck at the end of 2022 is $

170000, for the two trucks it was $ 340000. The trucks were revalued upward at the beginning of

2023 by $ 80000 each. Total revaluation for both the machine was $ 160000. The revised price

of an asset is $ 340000+$160000 that is 500000; however, the residual value would be $ 80000

and the revised life of the asset 6 years.

Therefore the depreciation (500000-80000)/6= $70000 for both machines

It has been assumed that the residual value given in the question was for both the machines.

3. Transfer of the depreciation in the income statement

Particulars Debit Credit

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

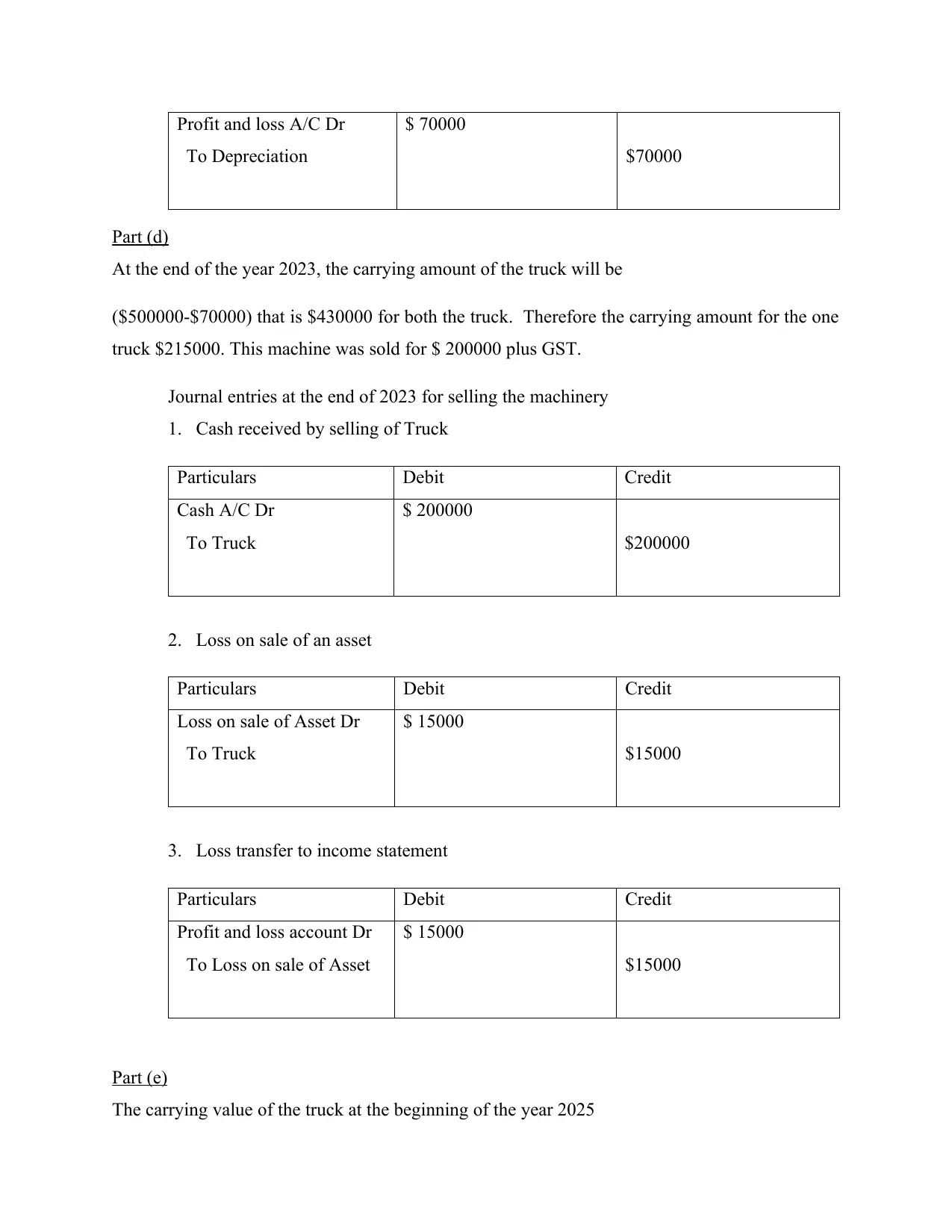

Profit and loss A/C Dr

To Depreciation

$ 70000

$70000

Part (d)

At the end of the year 2023, the carrying amount of the truck will be

($500000-$70000) that is $430000 for both the truck. Therefore the carrying amount for the one

truck $215000. This machine was sold for $ 200000 plus GST.

Journal entries at the end of 2023 for selling the machinery

1. Cash received by selling of Truck

Particulars Debit Credit

Cash A/C Dr

To Truck

$ 200000

$200000

2. Loss on sale of an asset

Particulars Debit Credit

Loss on sale of Asset Dr

To Truck

$ 15000

$15000

3. Loss transfer to income statement

Particulars Debit Credit

Profit and loss account Dr

To Loss on sale of Asset

$ 15000

$15000

Part (e)

The carrying value of the truck at the beginning of the year 2025

To Depreciation

$ 70000

$70000

Part (d)

At the end of the year 2023, the carrying amount of the truck will be

($500000-$70000) that is $430000 for both the truck. Therefore the carrying amount for the one

truck $215000. This machine was sold for $ 200000 plus GST.

Journal entries at the end of 2023 for selling the machinery

1. Cash received by selling of Truck

Particulars Debit Credit

Cash A/C Dr

To Truck

$ 200000

$200000

2. Loss on sale of an asset

Particulars Debit Credit

Loss on sale of Asset Dr

To Truck

$ 15000

$15000

3. Loss transfer to income statement

Particulars Debit Credit

Profit and loss account Dr

To Loss on sale of Asset

$ 15000

$15000

Part (e)

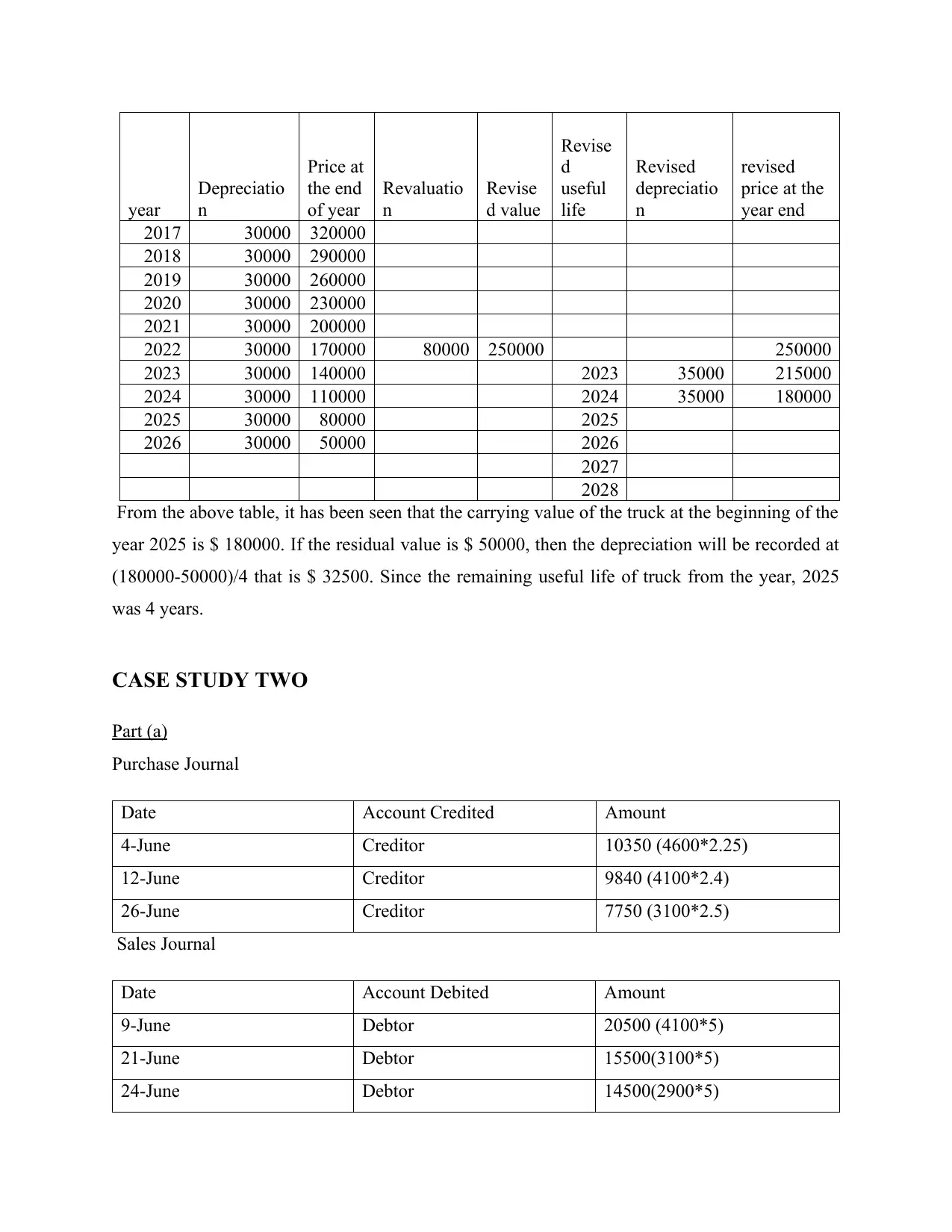

The carrying value of the truck at the beginning of the year 2025

year

Depreciatio

n

Price at

the end

of year

Revaluatio

n

Revise

d value

Revise

d

useful

life

Revised

depreciatio

n

revised

price at the

year end

2017 30000 320000

2018 30000 290000

2019 30000 260000

2020 30000 230000

2021 30000 200000

2022 30000 170000 80000 250000 250000

2023 30000 140000 2023 35000 215000

2024 30000 110000 2024 35000 180000

2025 30000 80000 2025

2026 30000 50000 2026

2027

2028

From the above table, it has been seen that the carrying value of the truck at the beginning of the

year 2025 is $ 180000. If the residual value is $ 50000, then the depreciation will be recorded at

(180000-50000)/4 that is $ 32500. Since the remaining useful life of truck from the year, 2025

was 4 years.

CASE STUDY TWO

Part (a)

Purchase Journal

Date Account Credited Amount

4-June Creditor 10350 (4600*2.25)

12-June Creditor 9840 (4100*2.4)

26-June Creditor 7750 (3100*2.5)

Sales Journal

Date Account Debited Amount

9-June Debtor 20500 (4100*5)

21-June Debtor 15500(3100*5)

24-June Debtor 14500(2900*5)

Depreciatio

n

Price at

the end

of year

Revaluatio

n

Revise

d value

Revise

d

useful

life

Revised

depreciatio

n

revised

price at the

year end

2017 30000 320000

2018 30000 290000

2019 30000 260000

2020 30000 230000

2021 30000 200000

2022 30000 170000 80000 250000 250000

2023 30000 140000 2023 35000 215000

2024 30000 110000 2024 35000 180000

2025 30000 80000 2025

2026 30000 50000 2026

2027

2028

From the above table, it has been seen that the carrying value of the truck at the beginning of the

year 2025 is $ 180000. If the residual value is $ 50000, then the depreciation will be recorded at

(180000-50000)/4 that is $ 32500. Since the remaining useful life of truck from the year, 2025

was 4 years.

CASE STUDY TWO

Part (a)

Purchase Journal

Date Account Credited Amount

4-June Creditor 10350 (4600*2.25)

12-June Creditor 9840 (4100*2.4)

26-June Creditor 7750 (3100*2.5)

Sales Journal

Date Account Debited Amount

9-June Debtor 20500 (4100*5)

21-June Debtor 15500(3100*5)

24-June Debtor 14500(2900*5)

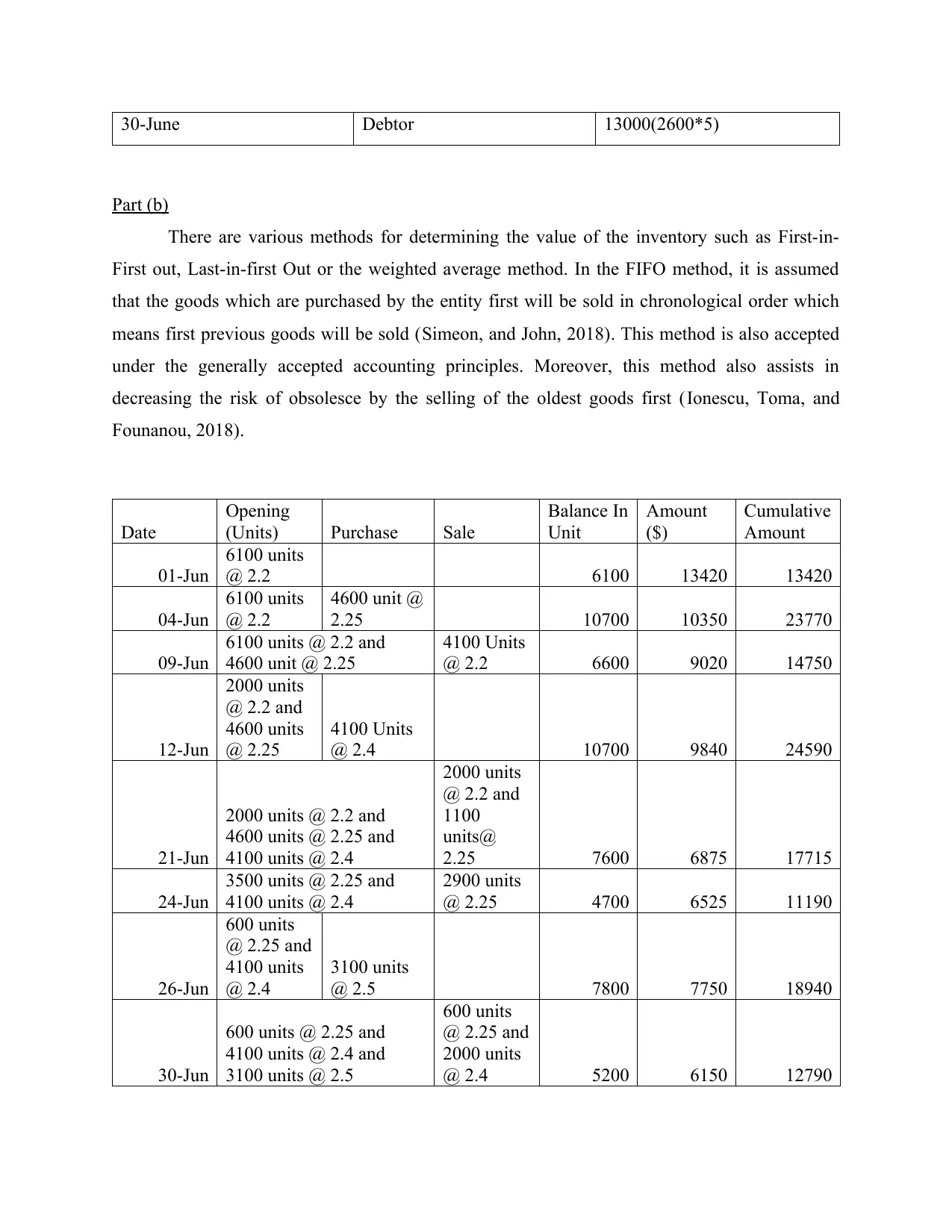

30-June Debtor 13000(2600*5)

Part (b)

There are various methods for determining the value of the inventory such as First-in-

First out, Last-in-first Out or the weighted average method. In the FIFO method, it is assumed

that the goods which are purchased by the entity first will be sold in chronological order which

means first previous goods will be sold (Simeon, and John, 2018). This method is also accepted

under the generally accepted accounting principles. Moreover, this method also assists in

decreasing the risk of obsolesce by the selling of the oldest goods first (Ionescu, Toma, and

Founanou, 2018).

Date

Opening

(Units) Purchase Sale

Balance In

Unit

Amount

($)

Cumulative

Amount

01-Jun

6100 units

@ 2.2 6100 13420 13420

04-Jun

6100 units

@ 2.2

4600 unit @

2.25 10700 10350 23770

09-Jun

6100 units @ 2.2 and

4600 unit @ 2.25

4100 Units

@ 2.2 6600 9020 14750

12-Jun

2000 units

@ 2.2 and

4600 units

@ 2.25

4100 Units

@ 2.4 10700 9840 24590

21-Jun

2000 units @ 2.2 and

4600 units @ 2.25 and

4100 units @ 2.4

2000 units

@ 2.2 and

1100

units@

2.25 7600 6875 17715

24-Jun

3500 units @ 2.25 and

4100 units @ 2.4

2900 units

@ 2.25 4700 6525 11190

26-Jun

600 units

@ 2.25 and

4100 units

@ 2.4

3100 units

@ 2.5 7800 7750 18940

30-Jun

600 units @ 2.25 and

4100 units @ 2.4 and

3100 units @ 2.5

600 units

@ 2.25 and

2000 units

@ 2.4 5200 6150 12790

Part (b)

There are various methods for determining the value of the inventory such as First-in-

First out, Last-in-first Out or the weighted average method. In the FIFO method, it is assumed

that the goods which are purchased by the entity first will be sold in chronological order which

means first previous goods will be sold (Simeon, and John, 2018). This method is also accepted

under the generally accepted accounting principles. Moreover, this method also assists in

decreasing the risk of obsolesce by the selling of the oldest goods first (Ionescu, Toma, and

Founanou, 2018).

Date

Opening

(Units) Purchase Sale

Balance In

Unit

Amount

($)

Cumulative

Amount

01-Jun

6100 units

@ 2.2 6100 13420 13420

04-Jun

6100 units

@ 2.2

4600 unit @

2.25 10700 10350 23770

09-Jun

6100 units @ 2.2 and

4600 unit @ 2.25

4100 Units

@ 2.2 6600 9020 14750

12-Jun

2000 units

@ 2.2 and

4600 units

@ 2.25

4100 Units

@ 2.4 10700 9840 24590

21-Jun

2000 units @ 2.2 and

4600 units @ 2.25 and

4100 units @ 2.4

2000 units

@ 2.2 and

1100

units@

2.25 7600 6875 17715

24-Jun

3500 units @ 2.25 and

4100 units @ 2.4

2900 units

@ 2.25 4700 6525 11190

26-Jun

600 units

@ 2.25 and

4100 units

@ 2.4

3100 units

@ 2.5 7800 7750 18940

30-Jun

600 units @ 2.25 and

4100 units @ 2.4 and

3100 units @ 2.5

600 units

@ 2.25 and

2000 units

@ 2.4 5200 6150 12790

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

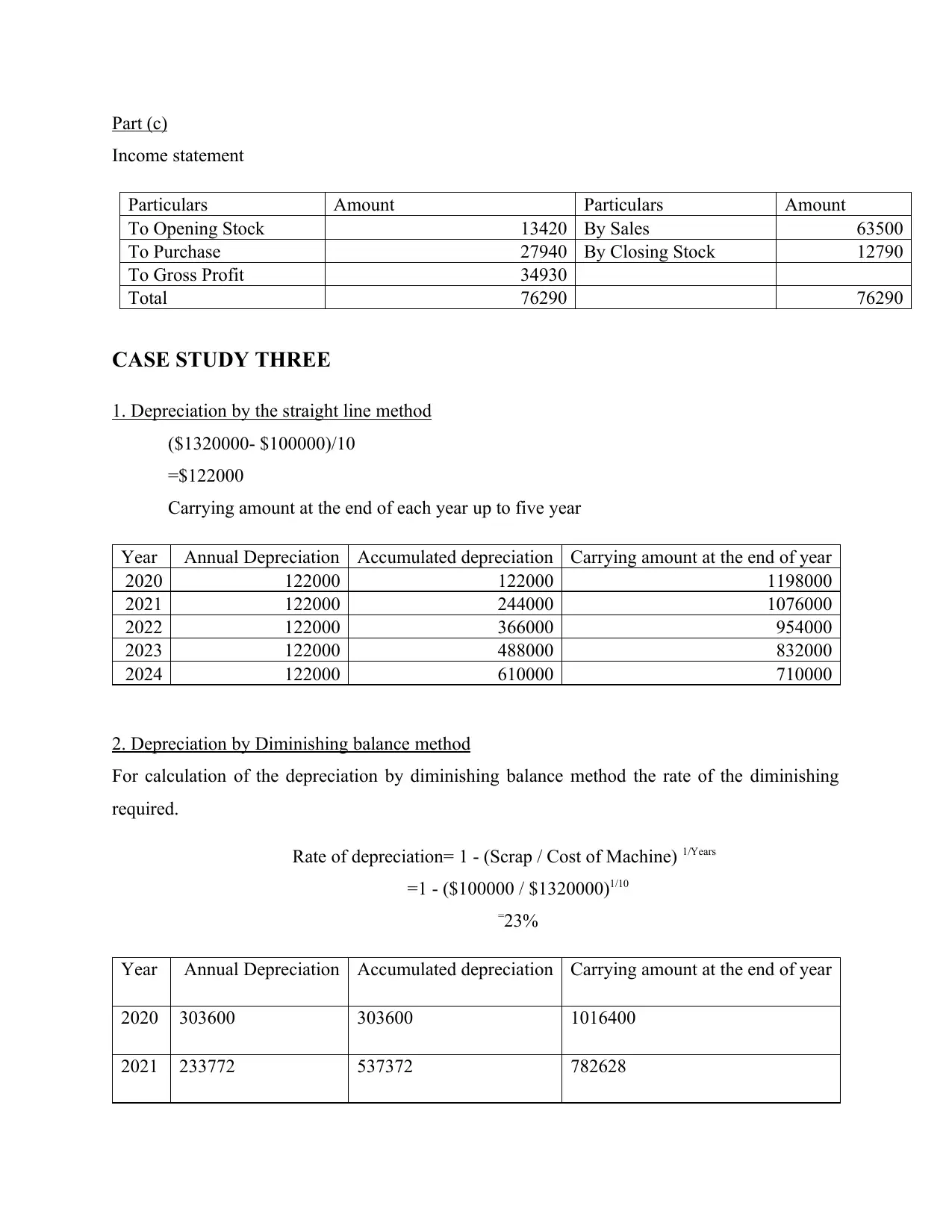

Part (c)

Income statement

Particulars Amount Particulars Amount

To Opening Stock 13420 By Sales 63500

To Purchase 27940 By Closing Stock 12790

To Gross Profit 34930

Total 76290 76290

CASE STUDY THREE

1. Depreciation by the straight line method

($1320000- $100000)/10

=$122000

Carrying amount at the end of each year up to five year

Year Annual Depreciation Accumulated depreciation Carrying amount at the end of year

2020 122000 122000 1198000

2021 122000 244000 1076000

2022 122000 366000 954000

2023 122000 488000 832000

2024 122000 610000 710000

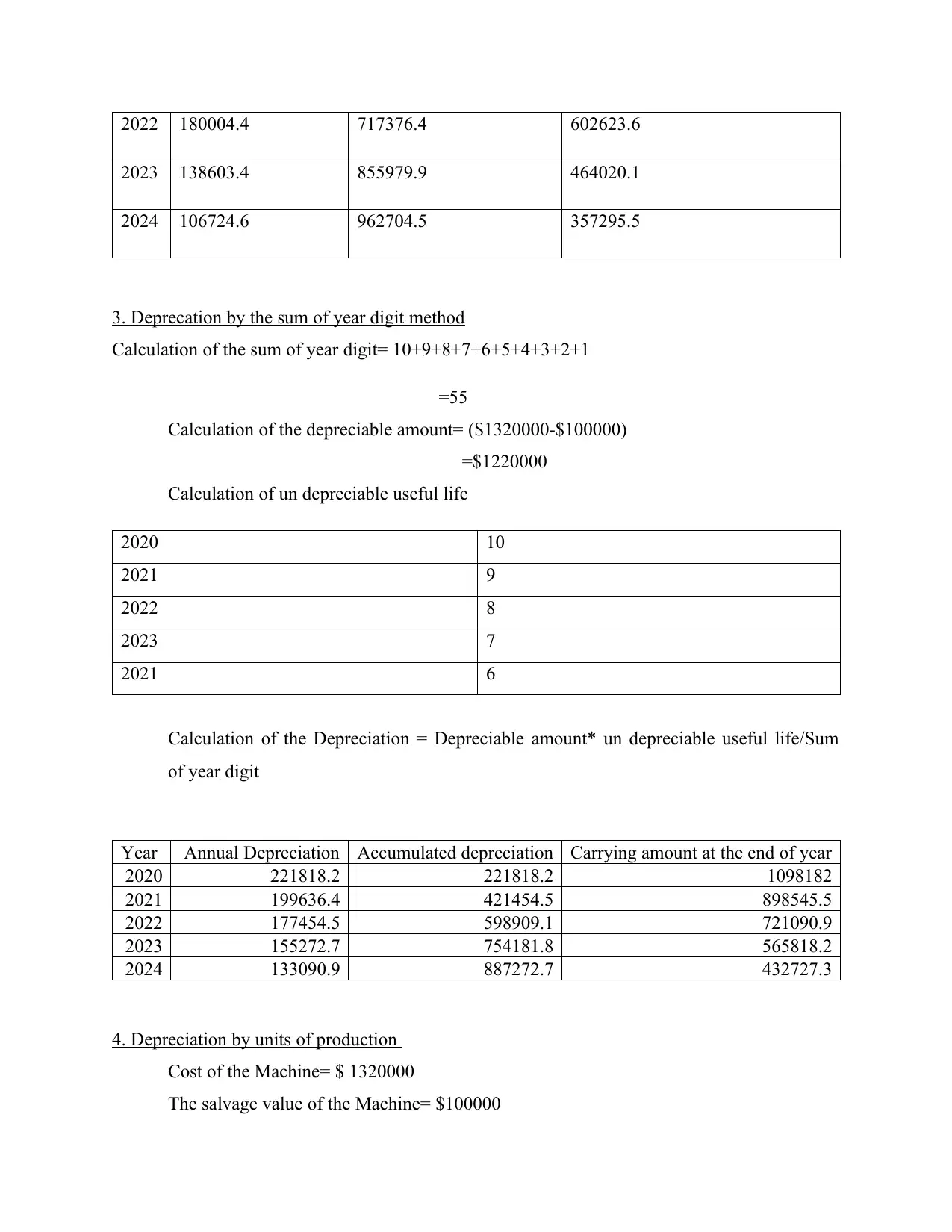

2. Depreciation by Diminishing balance method

For calculation of the depreciation by diminishing balance method the rate of the diminishing

required.

Rate of depreciation= 1 - (Scrap / Cost of Machine) 1/Years

=1 - ($100000 / $1320000)1/10

=23%

Year Annual Depreciation Accumulated depreciation Carrying amount at the end of year

2020 303600 303600 1016400

2021 233772 537372 782628

Income statement

Particulars Amount Particulars Amount

To Opening Stock 13420 By Sales 63500

To Purchase 27940 By Closing Stock 12790

To Gross Profit 34930

Total 76290 76290

CASE STUDY THREE

1. Depreciation by the straight line method

($1320000- $100000)/10

=$122000

Carrying amount at the end of each year up to five year

Year Annual Depreciation Accumulated depreciation Carrying amount at the end of year

2020 122000 122000 1198000

2021 122000 244000 1076000

2022 122000 366000 954000

2023 122000 488000 832000

2024 122000 610000 710000

2. Depreciation by Diminishing balance method

For calculation of the depreciation by diminishing balance method the rate of the diminishing

required.

Rate of depreciation= 1 - (Scrap / Cost of Machine) 1/Years

=1 - ($100000 / $1320000)1/10

=23%

Year Annual Depreciation Accumulated depreciation Carrying amount at the end of year

2020 303600 303600 1016400

2021 233772 537372 782628

2022 180004.4 717376.4 602623.6

2023 138603.4 855979.9 464020.1

2024 106724.6 962704.5 357295.5

3. Deprecation by the sum of year digit method

Calculation of the sum of year digit= 10+9+8+7+6+5+4+3+2+1

=55

Calculation of the depreciable amount= ($1320000-$100000)

=$1220000

Calculation of un depreciable useful life

2020 10

2021 9

2022 8

2023 7

2021 6

Calculation of the Depreciation = Depreciable amount* un depreciable useful life/Sum

of year digit

Year Annual Depreciation Accumulated depreciation Carrying amount at the end of year

2020 221818.2 221818.2 1098182

2021 199636.4 421454.5 898545.5

2022 177454.5 598909.1 721090.9

2023 155272.7 754181.8 565818.2

2024 133090.9 887272.7 432727.3

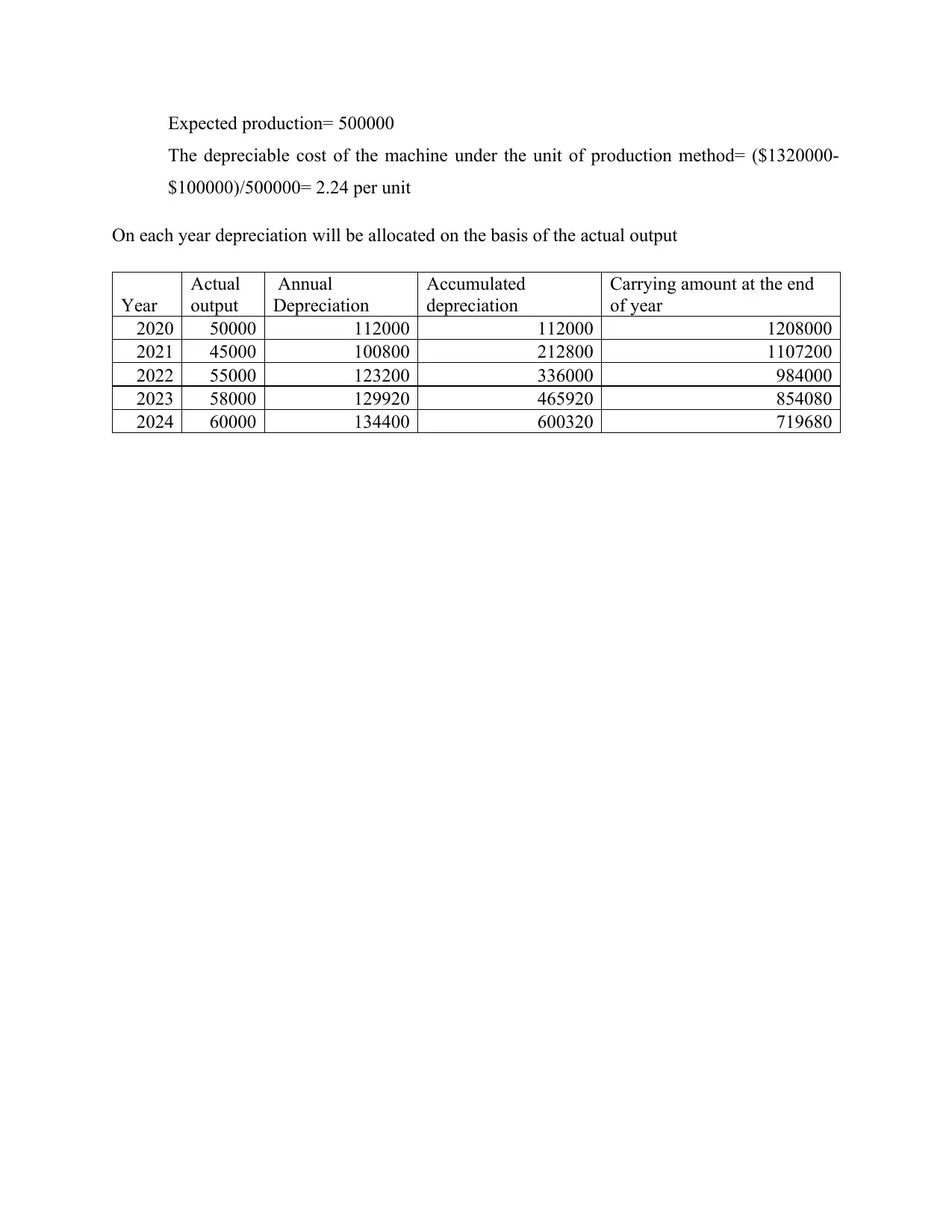

4. Depreciation by units of production

Cost of the Machine= $ 1320000

The salvage value of the Machine= $100000

2023 138603.4 855979.9 464020.1

2024 106724.6 962704.5 357295.5

3. Deprecation by the sum of year digit method

Calculation of the sum of year digit= 10+9+8+7+6+5+4+3+2+1

=55

Calculation of the depreciable amount= ($1320000-$100000)

=$1220000

Calculation of un depreciable useful life

2020 10

2021 9

2022 8

2023 7

2021 6

Calculation of the Depreciation = Depreciable amount* un depreciable useful life/Sum

of year digit

Year Annual Depreciation Accumulated depreciation Carrying amount at the end of year

2020 221818.2 221818.2 1098182

2021 199636.4 421454.5 898545.5

2022 177454.5 598909.1 721090.9

2023 155272.7 754181.8 565818.2

2024 133090.9 887272.7 432727.3

4. Depreciation by units of production

Cost of the Machine= $ 1320000

The salvage value of the Machine= $100000

Expected production= 500000

The depreciable cost of the machine under the unit of production method= ($1320000-

$100000)/500000= 2.24 per unit

On each year depreciation will be allocated on the basis of the actual output

Year

Actual

output

Annual

Depreciation

Accumulated

depreciation

Carrying amount at the end

of year

2020 50000 112000 112000 1208000

2021 45000 100800 212800 1107200

2022 55000 123200 336000 984000

2023 58000 129920 465920 854080

2024 60000 134400 600320 719680

The depreciable cost of the machine under the unit of production method= ($1320000-

$100000)/500000= 2.24 per unit

On each year depreciation will be allocated on the basis of the actual output

Year

Actual

output

Annual

Depreciation

Accumulated

depreciation

Carrying amount at the end

of year

2020 50000 112000 112000 1208000

2021 45000 100800 212800 1107200

2022 55000 123200 336000 984000

2023 58000 129920 465920 854080

2024 60000 134400 600320 719680

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

REFERENCES

Del Giudice, V., Manganelli, B. and De Paola, P., (2016). Depreciation methods for firm’s

assets. In International Conference on Computational Science and Its Applications(pp.

214-227). Springer, Cham.

Ionescu, L., Toma, M. and Founanou, M., (2018). Applied Analysis of the Impact of Inventory

Valuation Methods on the Financial Situation and Financial Performance. Valahian

Journal of Economic Studies, 1(ahead-of-print).

Küpper, H.U. and Pedell, B., (2016). Which asset valuation and depreciation method should be

used for regulated utilities? An analytical and simulation-based comparison. Utilities

Policy, 40, pp.88-103.

Simeon, E.D. and John, O., (2018). The implication of Choice of Inventory Valuation Methods

on Profit, Tax and Closing Inventory. Account and Financial Management

Journal, 3(07), pp.1639-1645.

Del Giudice, V., Manganelli, B. and De Paola, P., (2016). Depreciation methods for firm’s

assets. In International Conference on Computational Science and Its Applications(pp.

214-227). Springer, Cham.

Ionescu, L., Toma, M. and Founanou, M., (2018). Applied Analysis of the Impact of Inventory

Valuation Methods on the Financial Situation and Financial Performance. Valahian

Journal of Economic Studies, 1(ahead-of-print).

Küpper, H.U. and Pedell, B., (2016). Which asset valuation and depreciation method should be

used for regulated utilities? An analytical and simulation-based comparison. Utilities

Policy, 40, pp.88-103.

Simeon, E.D. and John, O., (2018). The implication of Choice of Inventory Valuation Methods

on Profit, Tax and Closing Inventory. Account and Financial Management

Journal, 3(07), pp.1639-1645.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.