Report on Fundamentals of Accounting & Finance for Holiday Ltd

VerifiedAdded on 2023/06/17

|9

|2115

|225

Report

AI Summary

This report provides solutions to questions related to the fundamentals of accounting and finance. It includes an income statement analysis for Holiday Ltd, adhering to IAS 2 and IFRS 8 standards. The report discusses inventory valuation, operating segment identification, and the treatment of provisions, contingent liabilities, and assets under IAS 37. Revenue recognition as per IFRS 15 is explained, along with the calculation of earnings per share (EPS) according to IAS 33. Furthermore, the document explores creative accounting practices like provisioning and off-balance sheet financing, and compares invoice discounting and factoring. Finally, it includes calculations for yield to maturity and discusses characteristics of a good credit management system. Desklib provides access to this and many other solved assignments for students.

Fundamentals of Accounting

& Finance

& Finance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

SECTION A.....................................................................................................................................3

Question 1...................................................................................................................................3

SECTION B.....................................................................................................................................4

Question 3...................................................................................................................................4

Question 4...................................................................................................................................5

SECTION C.....................................................................................................................................6

Question 6...................................................................................................................................6

REFERENCES................................................................................................................................9

SECTION A.....................................................................................................................................3

Question 1...................................................................................................................................3

SECTION B.....................................................................................................................................4

Question 3...................................................................................................................................4

Question 4...................................................................................................................................5

SECTION C.....................................................................................................................................6

Question 6...................................................................................................................................6

REFERENCES................................................................................................................................9

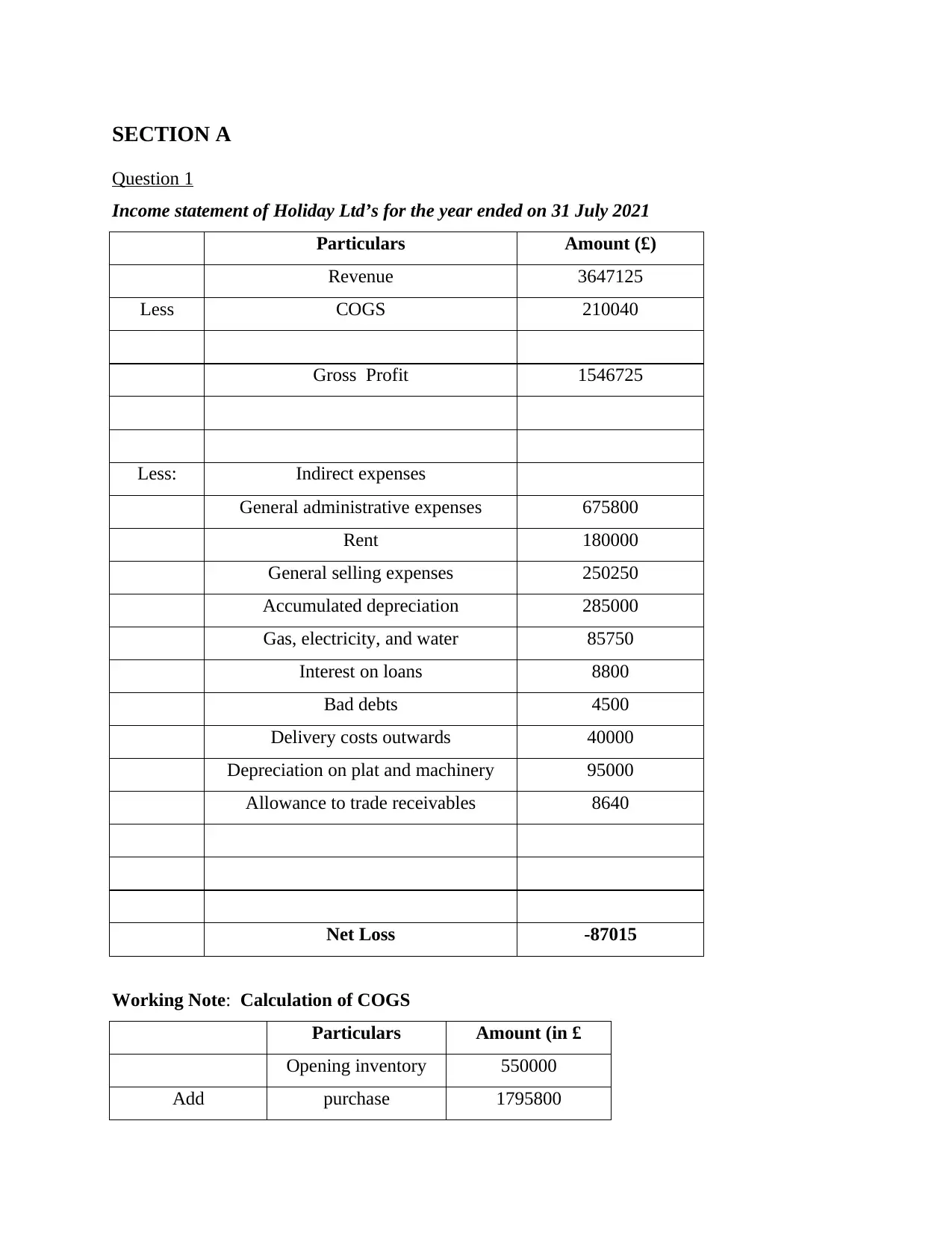

SECTION A

Question 1

Income statement of Holiday Ltd’s for the year ended on 31 July 2021

Particulars Amount (£)

Revenue 3647125

Less COGS 210040

Gross Profit 1546725

Less: Indirect expenses

General administrative expenses 675800

Rent 180000

General selling expenses 250250

Accumulated depreciation 285000

Gas, electricity, and water 85750

Interest on loans 8800

Bad debts 4500

Delivery costs outwards 40000

Depreciation on plat and machinery 95000

Allowance to trade receivables 8640

Net Loss -87015

Working Note: Calculation of COGS

Particulars Amount (in £

Opening inventory 550000

Add purchase 1795800

Question 1

Income statement of Holiday Ltd’s for the year ended on 31 July 2021

Particulars Amount (£)

Revenue 3647125

Less COGS 210040

Gross Profit 1546725

Less: Indirect expenses

General administrative expenses 675800

Rent 180000

General selling expenses 250250

Accumulated depreciation 285000

Gas, electricity, and water 85750

Interest on loans 8800

Bad debts 4500

Delivery costs outwards 40000

Depreciation on plat and machinery 95000

Allowance to trade receivables 8640

Net Loss -87015

Working Note: Calculation of COGS

Particulars Amount (in £

Opening inventory 550000

Add purchase 1795800

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

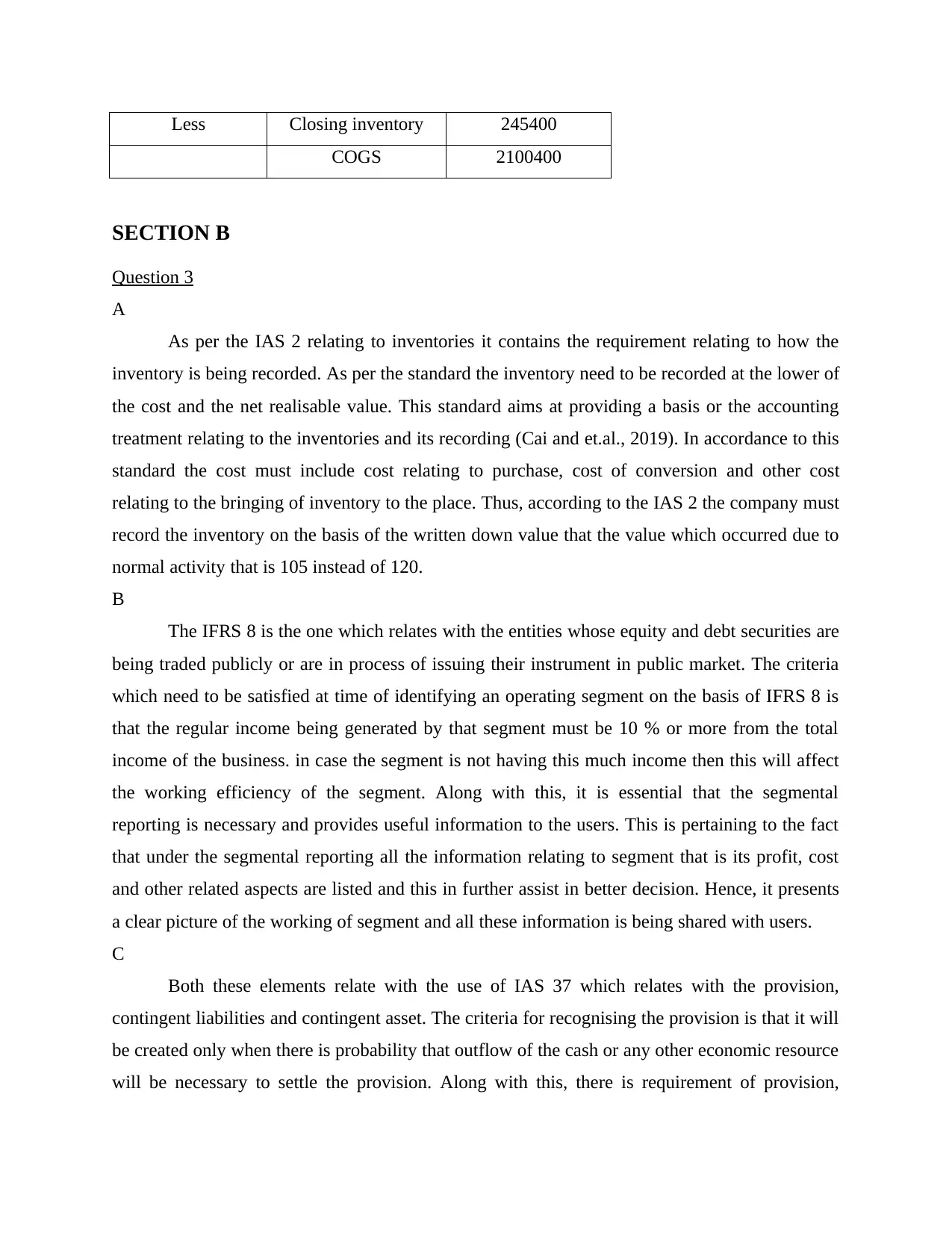

Less Closing inventory 245400

COGS 2100400

SECTION B

Question 3

A

As per the IAS 2 relating to inventories it contains the requirement relating to how the

inventory is being recorded. As per the standard the inventory need to be recorded at the lower of

the cost and the net realisable value. This standard aims at providing a basis or the accounting

treatment relating to the inventories and its recording (Cai and et.al., 2019). In accordance to this

standard the cost must include cost relating to purchase, cost of conversion and other cost

relating to the bringing of inventory to the place. Thus, according to the IAS 2 the company must

record the inventory on the basis of the written down value that the value which occurred due to

normal activity that is 105 instead of 120.

B

The IFRS 8 is the one which relates with the entities whose equity and debt securities are

being traded publicly or are in process of issuing their instrument in public market. The criteria

which need to be satisfied at time of identifying an operating segment on the basis of IFRS 8 is

that the regular income being generated by that segment must be 10 % or more from the total

income of the business. in case the segment is not having this much income then this will affect

the working efficiency of the segment. Along with this, it is essential that the segmental

reporting is necessary and provides useful information to the users. This is pertaining to the fact

that under the segmental reporting all the information relating to segment that is its profit, cost

and other related aspects are listed and this in further assist in better decision. Hence, it presents

a clear picture of the working of segment and all these information is being shared with users.

C

Both these elements relate with the use of IAS 37 which relates with the provision,

contingent liabilities and contingent asset. The criteria for recognising the provision is that it will

be created only when there is probability that outflow of the cash or any other economic resource

will be necessary to settle the provision. Along with this, there is requirement of provision,

COGS 2100400

SECTION B

Question 3

A

As per the IAS 2 relating to inventories it contains the requirement relating to how the

inventory is being recorded. As per the standard the inventory need to be recorded at the lower of

the cost and the net realisable value. This standard aims at providing a basis or the accounting

treatment relating to the inventories and its recording (Cai and et.al., 2019). In accordance to this

standard the cost must include cost relating to purchase, cost of conversion and other cost

relating to the bringing of inventory to the place. Thus, according to the IAS 2 the company must

record the inventory on the basis of the written down value that the value which occurred due to

normal activity that is 105 instead of 120.

B

The IFRS 8 is the one which relates with the entities whose equity and debt securities are

being traded publicly or are in process of issuing their instrument in public market. The criteria

which need to be satisfied at time of identifying an operating segment on the basis of IFRS 8 is

that the regular income being generated by that segment must be 10 % or more from the total

income of the business. in case the segment is not having this much income then this will affect

the working efficiency of the segment. Along with this, it is essential that the segmental

reporting is necessary and provides useful information to the users. This is pertaining to the fact

that under the segmental reporting all the information relating to segment that is its profit, cost

and other related aspects are listed and this in further assist in better decision. Hence, it presents

a clear picture of the working of segment and all these information is being shared with users.

C

Both these elements relate with the use of IAS 37 which relates with the provision,

contingent liabilities and contingent asset. The criteria for recognising the provision is that it will

be created only when there is probability that outflow of the cash or any other economic resource

will be necessary to settle the provision. Along with this, there is requirement of provision,

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

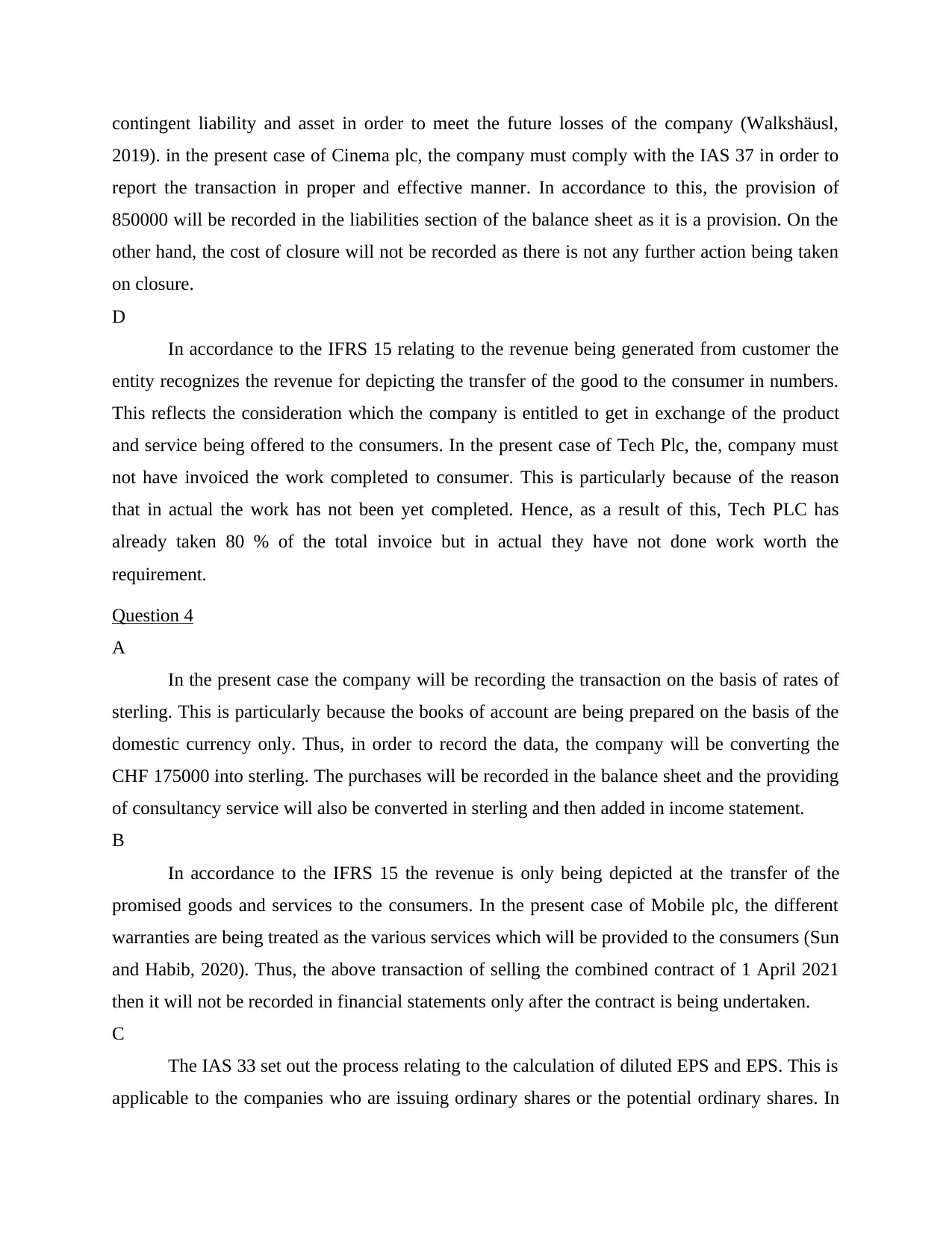

contingent liability and asset in order to meet the future losses of the company (Walkshäusl,

2019). in the present case of Cinema plc, the company must comply with the IAS 37 in order to

report the transaction in proper and effective manner. In accordance to this, the provision of

850000 will be recorded in the liabilities section of the balance sheet as it is a provision. On the

other hand, the cost of closure will not be recorded as there is not any further action being taken

on closure.

D

In accordance to the IFRS 15 relating to the revenue being generated from customer the

entity recognizes the revenue for depicting the transfer of the good to the consumer in numbers.

This reflects the consideration which the company is entitled to get in exchange of the product

and service being offered to the consumers. In the present case of Tech Plc, the, company must

not have invoiced the work completed to consumer. This is particularly because of the reason

that in actual the work has not been yet completed. Hence, as a result of this, Tech PLC has

already taken 80 % of the total invoice but in actual they have not done work worth the

requirement.

Question 4

A

In the present case the company will be recording the transaction on the basis of rates of

sterling. This is particularly because the books of account are being prepared on the basis of the

domestic currency only. Thus, in order to record the data, the company will be converting the

CHF 175000 into sterling. The purchases will be recorded in the balance sheet and the providing

of consultancy service will also be converted in sterling and then added in income statement.

B

In accordance to the IFRS 15 the revenue is only being depicted at the transfer of the

promised goods and services to the consumers. In the present case of Mobile plc, the different

warranties are being treated as the various services which will be provided to the consumers (Sun

and Habib, 2020). Thus, the above transaction of selling the combined contract of 1 April 2021

then it will not be recorded in financial statements only after the contract is being undertaken.

C

The IAS 33 set out the process relating to the calculation of diluted EPS and EPS. This is

applicable to the companies who are issuing ordinary shares or the potential ordinary shares. In

2019). in the present case of Cinema plc, the company must comply with the IAS 37 in order to

report the transaction in proper and effective manner. In accordance to this, the provision of

850000 will be recorded in the liabilities section of the balance sheet as it is a provision. On the

other hand, the cost of closure will not be recorded as there is not any further action being taken

on closure.

D

In accordance to the IFRS 15 relating to the revenue being generated from customer the

entity recognizes the revenue for depicting the transfer of the good to the consumer in numbers.

This reflects the consideration which the company is entitled to get in exchange of the product

and service being offered to the consumers. In the present case of Tech Plc, the, company must

not have invoiced the work completed to consumer. This is particularly because of the reason

that in actual the work has not been yet completed. Hence, as a result of this, Tech PLC has

already taken 80 % of the total invoice but in actual they have not done work worth the

requirement.

Question 4

A

In the present case the company will be recording the transaction on the basis of rates of

sterling. This is particularly because the books of account are being prepared on the basis of the

domestic currency only. Thus, in order to record the data, the company will be converting the

CHF 175000 into sterling. The purchases will be recorded in the balance sheet and the providing

of consultancy service will also be converted in sterling and then added in income statement.

B

In accordance to the IFRS 15 the revenue is only being depicted at the transfer of the

promised goods and services to the consumers. In the present case of Mobile plc, the different

warranties are being treated as the various services which will be provided to the consumers (Sun

and Habib, 2020). Thus, the above transaction of selling the combined contract of 1 April 2021

then it will not be recorded in financial statements only after the contract is being undertaken.

C

The IAS 33 set out the process relating to the calculation of diluted EPS and EPS. This is

applicable to the companies who are issuing ordinary shares or the potential ordinary shares. In

the present case of Violin plc, the earning per share will be recorded at the 180 only and this will

be attributable to the ordinary shareholders only.

D

The use of provision is a type of creative accounting which is assistive to the business in

order to create better working condition within the company (Hutton, 2017). in case there is any

contingent liability or expense which might occur in future, the provision is being created from

current period only. For example, the provision of the doubtful debt is being created in order to

have some fund available in case the debt is not recovered.

Along with this, off balance sheet financing is a method of accounting wherein company

record the current liability of asset in such a manner that it prevents them from appearing within

the balance sheet. For example, the joint venture, operating lease are common example of off-

balance sheet.

Furthermore, reclassifying debt as equity is another method of creative accounting,

wherein any party to which company owes some debt is being replaced with the equity

(Carolina, 2017). For example, ABS is the having debt of 100000, then in exchange of this they

are issued shared worth 100000 and debt is being settled.

SECTION C

Question 6

a. Differences and similarities between invoice discounting and factoring

Similarities which are present between invoice discounting and factoring is that

discounting is a loan which is secured against the outstanding invoice in which the company

purchases the unpaid invoices outright (Goh, 2017). Factoring helps in providing a factor which

can help the company towards controlling the credit. Thus, both of these techniques of banking

institutions. However, the differences between these two techniques are,

Invoice discounting is a loan which secures the outstanding invoices but in factoring the

company actually purchases the unpaid invoices outright.

Invoice factoring may sell the invoice as if the factoring company or the customer refuses

to pay then they will not be obligated to repay the money. On the other hand invoice

discounting is a loan which helps in making the sale which can create the money for

being repaid.

be attributable to the ordinary shareholders only.

D

The use of provision is a type of creative accounting which is assistive to the business in

order to create better working condition within the company (Hutton, 2017). in case there is any

contingent liability or expense which might occur in future, the provision is being created from

current period only. For example, the provision of the doubtful debt is being created in order to

have some fund available in case the debt is not recovered.

Along with this, off balance sheet financing is a method of accounting wherein company

record the current liability of asset in such a manner that it prevents them from appearing within

the balance sheet. For example, the joint venture, operating lease are common example of off-

balance sheet.

Furthermore, reclassifying debt as equity is another method of creative accounting,

wherein any party to which company owes some debt is being replaced with the equity

(Carolina, 2017). For example, ABS is the having debt of 100000, then in exchange of this they

are issued shared worth 100000 and debt is being settled.

SECTION C

Question 6

a. Differences and similarities between invoice discounting and factoring

Similarities which are present between invoice discounting and factoring is that

discounting is a loan which is secured against the outstanding invoice in which the company

purchases the unpaid invoices outright (Goh, 2017). Factoring helps in providing a factor which

can help the company towards controlling the credit. Thus, both of these techniques of banking

institutions. However, the differences between these two techniques are,

Invoice discounting is a loan which secures the outstanding invoices but in factoring the

company actually purchases the unpaid invoices outright.

Invoice factoring may sell the invoice as if the factoring company or the customer refuses

to pay then they will not be obligated to repay the money. On the other hand invoice

discounting is a loan which helps in making the sale which can create the money for

being repaid.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The collection of these invoices is the main difference as in discounting the customer has

full control of collection but in invoice factoring the company purchases the unpaid

invoices to take over the collections.

b.

Heston ltd has just paid a dividend per share of £0.20. The dividend per share was £0.18 five

years ago. Heston has a market beta of 1.15, the risk-free rate is 4% and the expected market

return is 12%.

E(Ri) = r + βi [E(Rm) − r]

= .04 + 1.15 [.12 - .04]

= .04 + .09

= .13

P0 = 1 / (0.13 − 0.11)

= $50

c. What is the yield to maturity of bond X?

Particulars Figures (in $)

Par value 1000

Current market price 1120

Coupon Rate (%) 8

Years to Maturity 5

Payment Interval Annually

CY = C / P * 100

Where:

C is the periodic coupon payment,

P is the price of a bond,

Current yield = 80 / 1120 * 100

= 7.14%

Yield to maturity (YTM) = P = C × (1 + r) -1 + C×(1 + r) -2 + . . . + C×(1 + r) -Y + B×(1 + r) –Y

1120 = 80 * (1 + r) -1 + 80×(1 + r) -2 + 80×(1 + r) -3 + 80×(1 + r) -4 + 80×(1 + r) -5 + 1000×(1 + r) -5

YTM = 5.21%

d. Characteristic of good credit management system

full control of collection but in invoice factoring the company purchases the unpaid

invoices to take over the collections.

b.

Heston ltd has just paid a dividend per share of £0.20. The dividend per share was £0.18 five

years ago. Heston has a market beta of 1.15, the risk-free rate is 4% and the expected market

return is 12%.

E(Ri) = r + βi [E(Rm) − r]

= .04 + 1.15 [.12 - .04]

= .04 + .09

= .13

P0 = 1 / (0.13 − 0.11)

= $50

c. What is the yield to maturity of bond X?

Particulars Figures (in $)

Par value 1000

Current market price 1120

Coupon Rate (%) 8

Years to Maturity 5

Payment Interval Annually

CY = C / P * 100

Where:

C is the periodic coupon payment,

P is the price of a bond,

Current yield = 80 / 1120 * 100

= 7.14%

Yield to maturity (YTM) = P = C × (1 + r) -1 + C×(1 + r) -2 + . . . + C×(1 + r) -Y + B×(1 + r) –Y

1120 = 80 * (1 + r) -1 + 80×(1 + r) -2 + 80×(1 + r) -3 + 80×(1 + r) -4 + 80×(1 + r) -5 + 1000×(1 + r) -5

YTM = 5.21%

d. Characteristic of good credit management system

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

A good credit management system is the system which is able to handle all the credit

accounts with the help of having assess of the risk that can determine how much credit is needed

to be offered during sending the bills for collection (Tran, Ly and Nguyen, 2020). The following

characteristics is what makes the credit management system a good one,

It helps in evaluating the customer credit which is helpful for being applied against the

credit which is needed for the system to be automated and be able to determine the credit

worthiness.

The credit management system needs to be very efficient in the collection of the credit.

It needs to be practical for understanding the practical outlook of invaluable credit control

for tackling the problems with effectiveness.

It needs to have accuracy so that the lenders are satisfied with the performance of the

credit control system.

Perseverance is also very important for this system as it helps it to address the

management of the credit with patience.

Politeness is also important for recovering the credit so that positive relations can be maintained.

accounts with the help of having assess of the risk that can determine how much credit is needed

to be offered during sending the bills for collection (Tran, Ly and Nguyen, 2020). The following

characteristics is what makes the credit management system a good one,

It helps in evaluating the customer credit which is helpful for being applied against the

credit which is needed for the system to be automated and be able to determine the credit

worthiness.

The credit management system needs to be very efficient in the collection of the credit.

It needs to be practical for understanding the practical outlook of invaluable credit control

for tackling the problems with effectiveness.

It needs to have accuracy so that the lenders are satisfied with the performance of the

credit control system.

Perseverance is also very important for this system as it helps it to address the

management of the credit with patience.

Politeness is also important for recovering the credit so that positive relations can be maintained.

REFERENCES

Books and Journals

Cai, C. W., and et.al., 2019. Machine Learning and Expert Judgement: Analyzing Emerging

Topics in Accounting and Finance Research in the Asia–Pacific. Abacus. 55(4). pp.709-

733.

Carolina, Y., 2017. Understanding AIS User Knowledge, AIS Quality, and Accounting

Information Quality. Accounting and Finance Review (AFR) Vol. 2(3).

Goh, K., 2017. Trading places: Benefits of invoice finance for small and medium sized

enterprises as opposed to bank lending. Aberdeen Student L. Rev.. 7. p.56.

Hutton, A. P., 2017. Discussion of “Aggregate Margin Debt and the Divergence of Price from

Accounting Fundamentals”. Contemporary Accounting Research. 34(3). pp.1446-1452.

Sun, S. L. and Habib, A., 2020. Determinants and consequences of tournament incentives: A

survey of the literature in accounting and finance. Research in International Business

and Finance. 54. p.101256.

Tran, Q. T., Ly, H. A. and Nguyen, K. T., 2020. The effectiveness of the internal control system

in Vietnamese credit institutions. Banks and Bank Systems. 15(4). p.26.

Walkshäusl, C., 2019. The fundamentals of momentum investing: European evidence on

understanding momentum through fundamentals. Accounting & Finance. 59. pp.831-

857.

Books and Journals

Cai, C. W., and et.al., 2019. Machine Learning and Expert Judgement: Analyzing Emerging

Topics in Accounting and Finance Research in the Asia–Pacific. Abacus. 55(4). pp.709-

733.

Carolina, Y., 2017. Understanding AIS User Knowledge, AIS Quality, and Accounting

Information Quality. Accounting and Finance Review (AFR) Vol. 2(3).

Goh, K., 2017. Trading places: Benefits of invoice finance for small and medium sized

enterprises as opposed to bank lending. Aberdeen Student L. Rev.. 7. p.56.

Hutton, A. P., 2017. Discussion of “Aggregate Margin Debt and the Divergence of Price from

Accounting Fundamentals”. Contemporary Accounting Research. 34(3). pp.1446-1452.

Sun, S. L. and Habib, A., 2020. Determinants and consequences of tournament incentives: A

survey of the literature in accounting and finance. Research in International Business

and Finance. 54. p.101256.

Tran, Q. T., Ly, H. A. and Nguyen, K. T., 2020. The effectiveness of the internal control system

in Vietnamese credit institutions. Banks and Bank Systems. 15(4). p.26.

Walkshäusl, C., 2019. The fundamentals of momentum investing: European evidence on

understanding momentum through fundamentals. Accounting & Finance. 59. pp.831-

857.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.