Fundamentals of Finance: In-depth Project Report on Bond Valuation

VerifiedAdded on 2023/06/15

|7

|1194

|490

Report

AI Summary

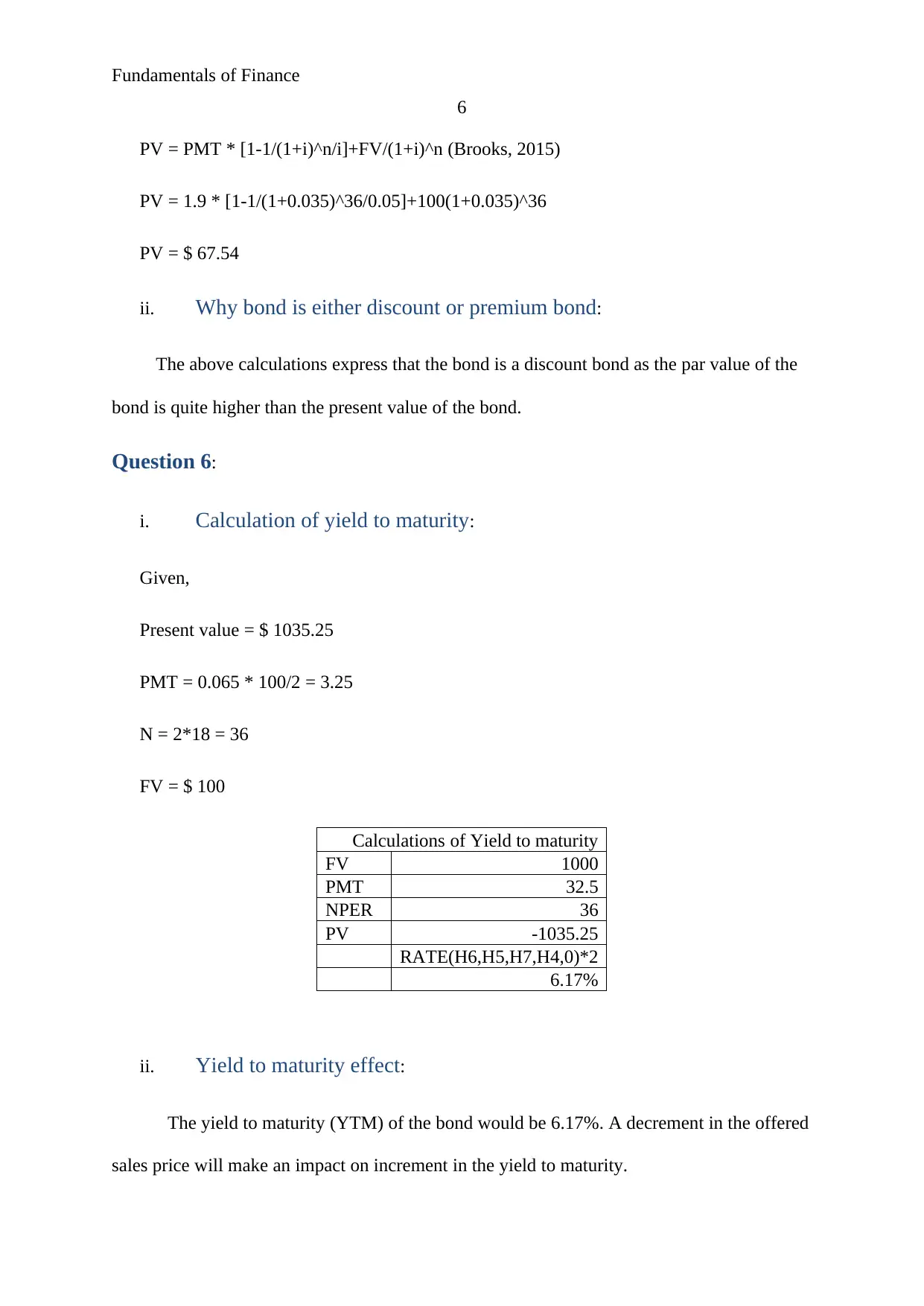

This report provides a comprehensive overview of bond valuation within the context of fundamental finance principles. It covers key concepts such as call provisions, discount and premium bonds, and the inverse relationship between market interest rates and bond prices. The report includes calculations for zero-coupon bond prices and explains the rationale behind steep discounts. It also demonstrates how to calculate bond prices and determine whether a bond is trading at a discount or premium. Furthermore, the report details the calculation of yield to maturity (YTM) and discusses the impact of sales price changes on YTM. The analysis is supported by relevant academic references, offering a solid foundation for understanding bond valuation techniques and their practical implications. Desklib provides access to this and many other solved assignments for students.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.