Investing Report: NPV, Payback Period, and Cost Allocation

VerifiedAdded on 2021/04/17

|10

|2012

|345

Report

AI Summary

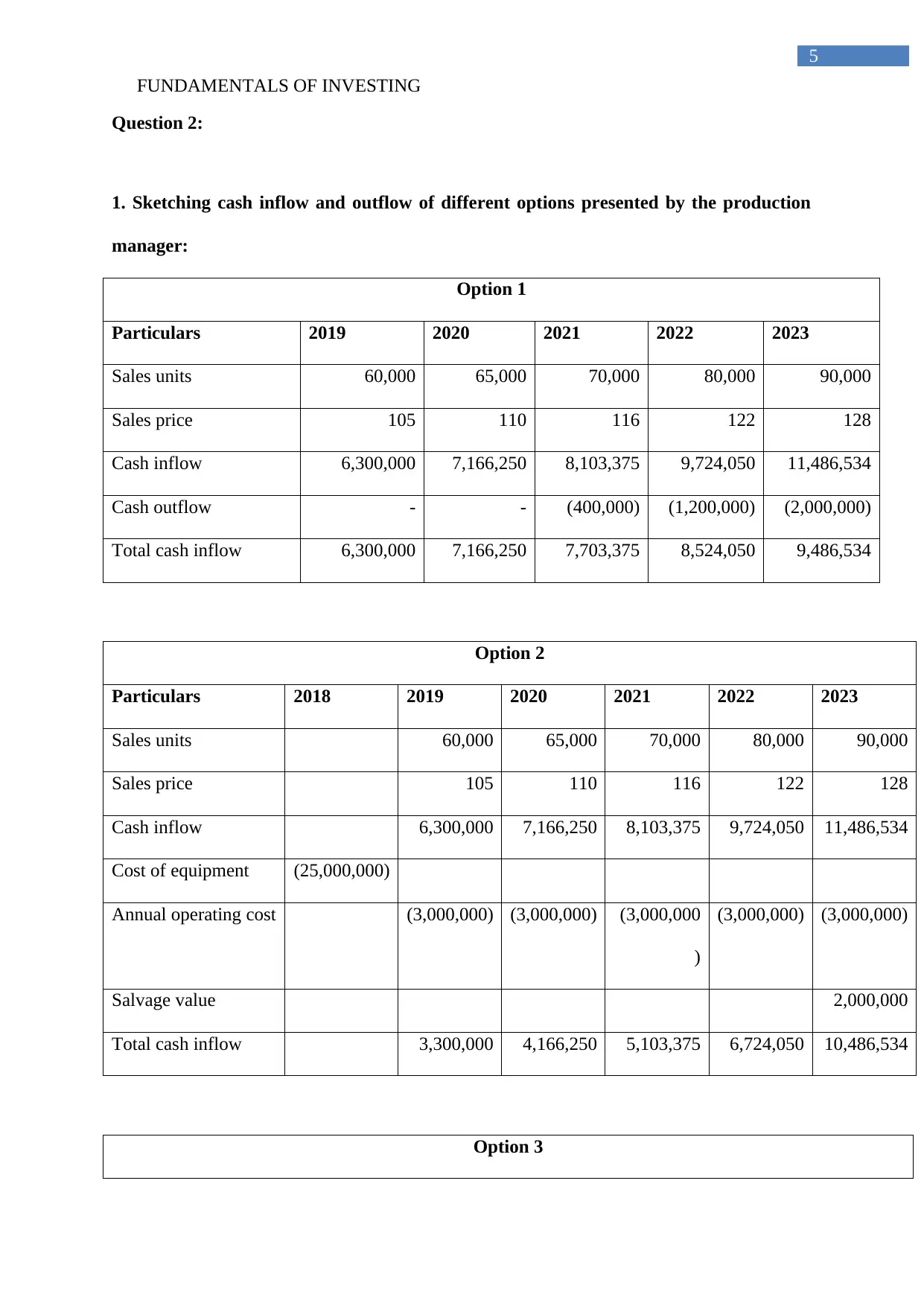

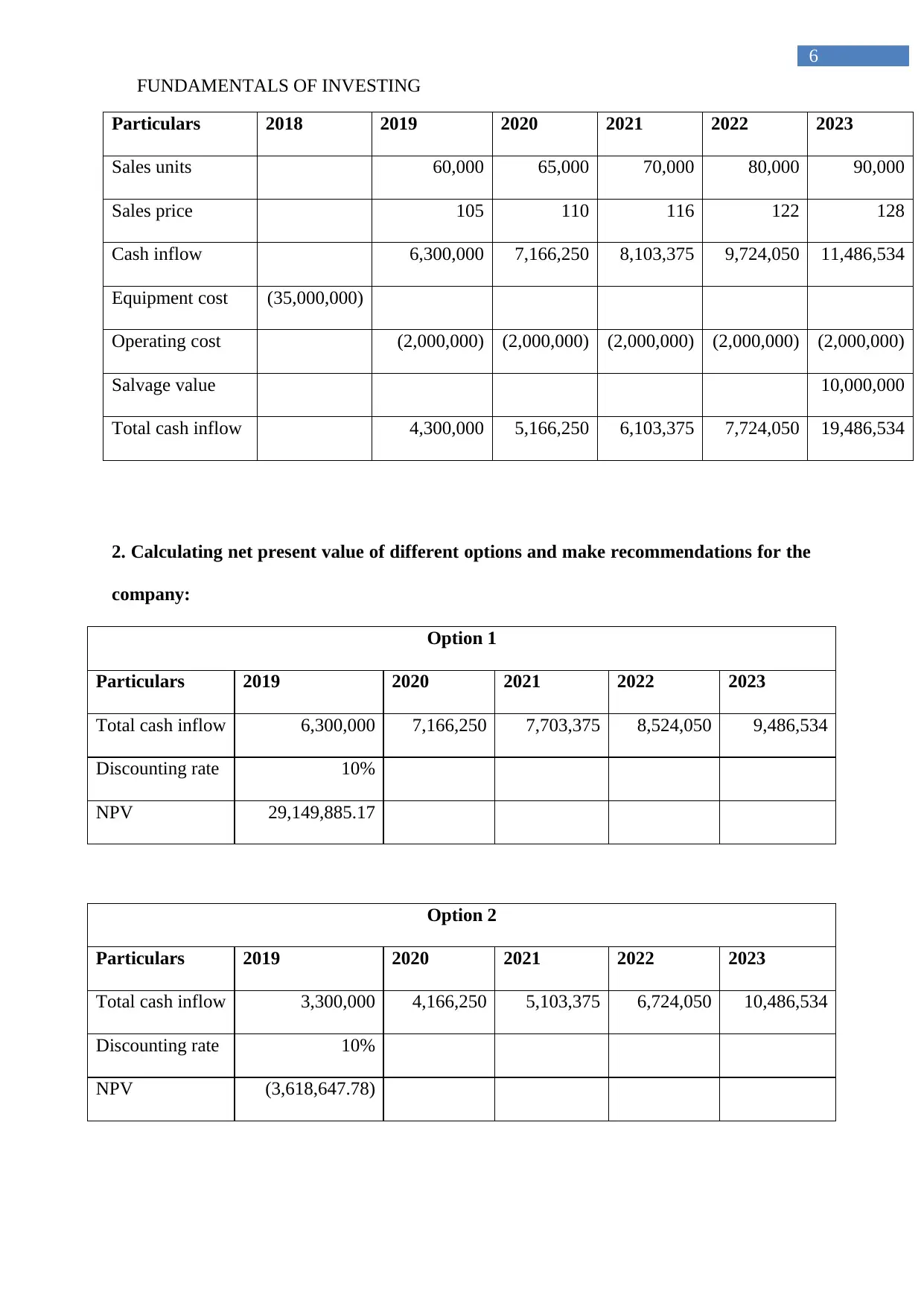

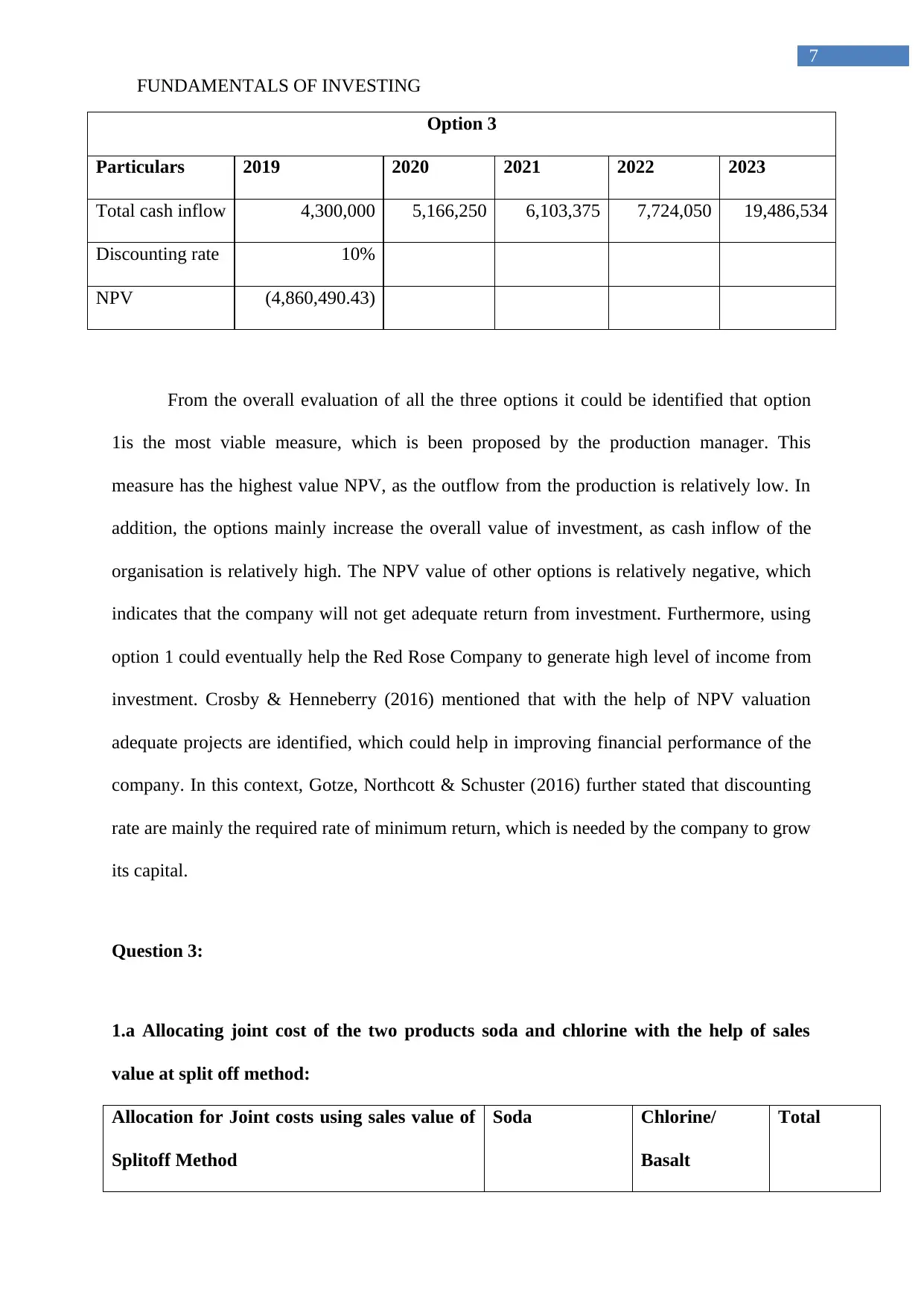

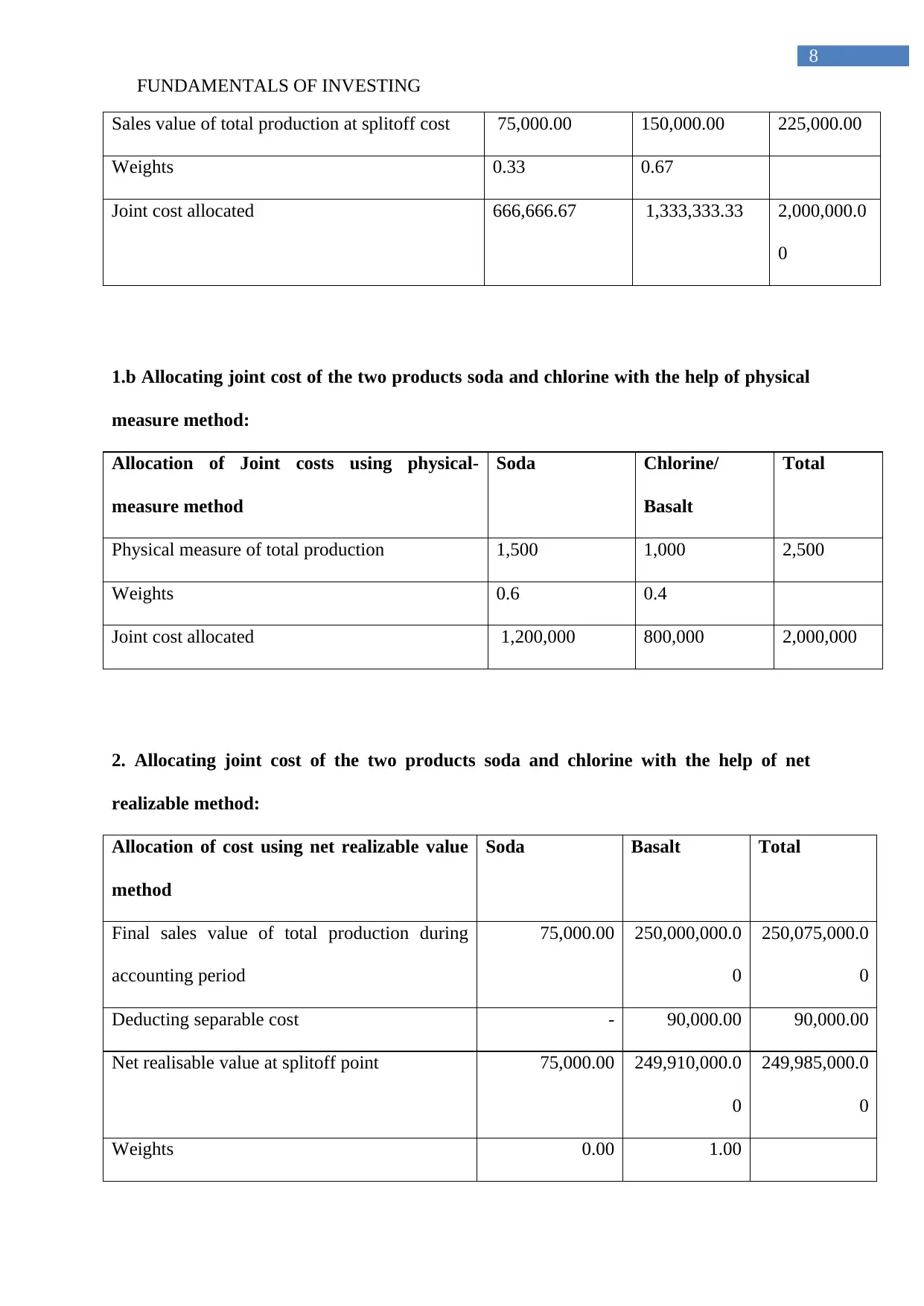

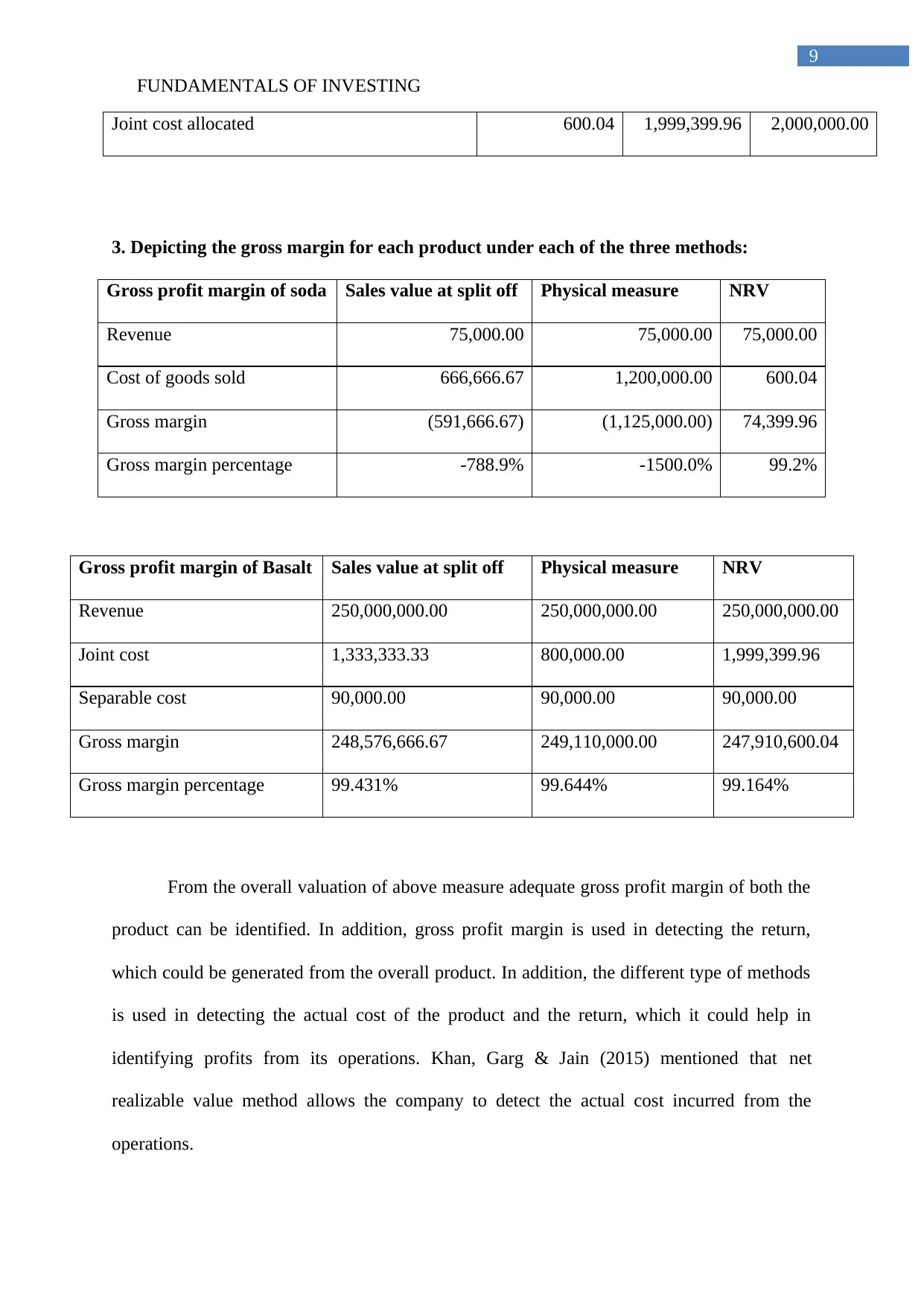

This report delves into the fundamentals of investing, presenting a detailed financial analysis. It begins by evaluating two investment projects using the Net Present Value (NPV) method and payback period, determining which project offers superior financial viability. The report then analyzes cash inflows and outflows of different options, calculating their NPV to provide recommendations. Finally, it explores cost allocation methods, specifically focusing on allocating joint costs for two products (soda and chlorine) using sales value at split-off, physical measure, and net realizable value methods, comparing the gross margin for each product under each method. The report provides detailed calculations, interpretations, and relevant references to support its findings, making it a comprehensive resource for understanding investment analysis and financial decision-making.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.