Financial Report: Analysis of Futures and Options Markets, Semester 2

VerifiedAdded on 2020/12/30

|11

|3463

|481

Report

AI Summary

This report provides a comprehensive analysis of futures and options contracts, beginning with an introduction to these financial derivatives. It explores the exploitation of arbitrage opportunities, defines and differentiates forward and future prices, and outlines various transaction types within the futures market. The report then delves into speculative strategies in the forward market, including calculations of potential profits and losses. Further analysis includes the interest rate derivatives market, examining concepts such as delta, theta, and gamma hedging, along with a case study on Alcoa involving interest rate swaps. The report concludes with an examination of option's implied volatility and the Ho & Lee model, providing a detailed overview of key concepts and their practical applications within the financial markets.

FUTURE AND OPTIONS

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

QUESTION 1...................................................................................................................................1

a. Presence of Arbitrage opportunity with its exploitation.....................................................1

b. Defining forward and future prices with its difference......................................................2

c. Types of transactions in the future market.........................................................................2

QUESTION 2...................................................................................................................................3

a. Assumption to buy or sell £1000000..................................................................................3

b. Actions for speculating in forward market with its expected dollar profit ........................3

c. Speculative profit in dollar when spot exchange rate turns $1.86/£...................................4

QUESTION 3...................................................................................................................................4

a. Explaining interest rate derivatives market........................................................................4

b. Alcoa case...........................................................................................................................4

b.1 Conversion of interest rate swap with obligation of interest into one synthetic fixed rate

loan.........................................................................................................................................5

b.2 Interest rate firm pays on synthetic fixed rate loan..........................................................5

QUESTION 4...................................................................................................................................5

a. Delta hedging......................................................................................................................5

b. Theta...................................................................................................................................5

c. Gamma Hedging.................................................................................................................6

d. Relationship among delta hedging, theta and gamma hedging..........................................6

QUESTION 5...................................................................................................................................6

a. Explaining Option's implied volatility and method for calculating....................................6

b. Explaining strength and weakness of Implied Volatility Function ...................................7

c. Explaining Ho & Lee model with graphical presentation and note on building interest rate

tree..........................................................................................................................................7

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

INTRODUCTION...........................................................................................................................1

QUESTION 1...................................................................................................................................1

a. Presence of Arbitrage opportunity with its exploitation.....................................................1

b. Defining forward and future prices with its difference......................................................2

c. Types of transactions in the future market.........................................................................2

QUESTION 2...................................................................................................................................3

a. Assumption to buy or sell £1000000..................................................................................3

b. Actions for speculating in forward market with its expected dollar profit ........................3

c. Speculative profit in dollar when spot exchange rate turns $1.86/£...................................4

QUESTION 3...................................................................................................................................4

a. Explaining interest rate derivatives market........................................................................4

b. Alcoa case...........................................................................................................................4

b.1 Conversion of interest rate swap with obligation of interest into one synthetic fixed rate

loan.........................................................................................................................................5

b.2 Interest rate firm pays on synthetic fixed rate loan..........................................................5

QUESTION 4...................................................................................................................................5

a. Delta hedging......................................................................................................................5

b. Theta...................................................................................................................................5

c. Gamma Hedging.................................................................................................................6

d. Relationship among delta hedging, theta and gamma hedging..........................................6

QUESTION 5...................................................................................................................................6

a. Explaining Option's implied volatility and method for calculating....................................6

b. Explaining strength and weakness of Implied Volatility Function ...................................7

c. Explaining Ho & Lee model with graphical presentation and note on building interest rate

tree..........................................................................................................................................7

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

INTRODUCTION

The future contracts are one which allows selling or buy underlying stock or index at

price which is set on prior basis for purpose of delivery on future date. Futures and option reflect

two and very common form of derivatives. Derivaties are considered as financial instruments

which derive value through underlying. It could be stock issued through currency, gold, company

etc. The present report will discuss about exploitation of arbitrage opportunity along with

elaboration of future and forward prices with there difference and types of transaction. In the

similar aspect, it will specify interest rate derivative market along with delta and gamma hedging

and theta.

QUESTION 1

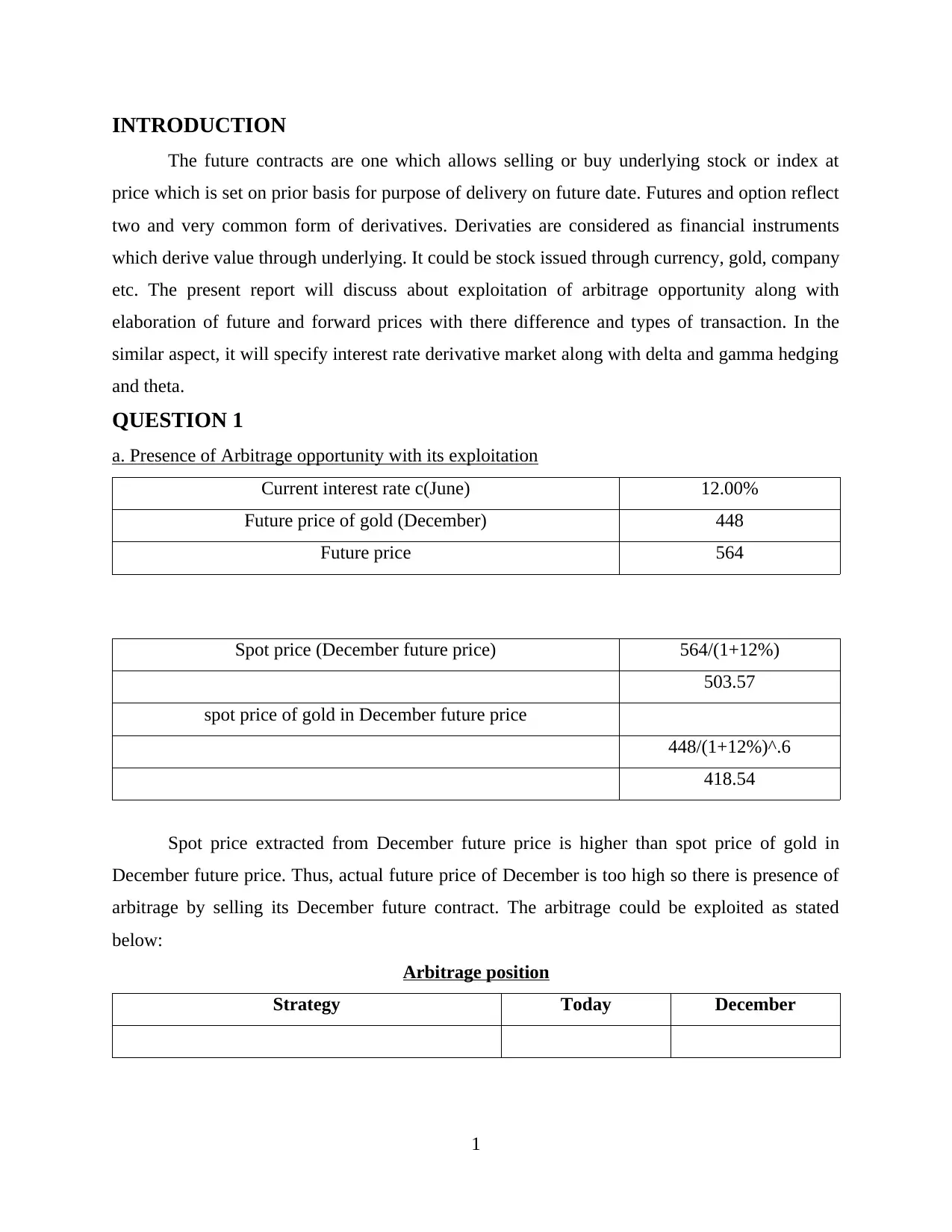

a. Presence of Arbitrage opportunity with its exploitation

Current interest rate c(June) 12.00%

Future price of gold (December) 448

Future price 564

Spot price (December future price) 564/(1+12%)

503.57

spot price of gold in December future price

448/(1+12%)^.6

418.54

Spot price extracted from December future price is higher than spot price of gold in

December future price. Thus, actual future price of December is too high so there is presence of

arbitrage by selling its December future contract. The arbitrage could be exploited as stated

below:

Arbitrage position

Strategy Today December

1

The future contracts are one which allows selling or buy underlying stock or index at

price which is set on prior basis for purpose of delivery on future date. Futures and option reflect

two and very common form of derivatives. Derivaties are considered as financial instruments

which derive value through underlying. It could be stock issued through currency, gold, company

etc. The present report will discuss about exploitation of arbitrage opportunity along with

elaboration of future and forward prices with there difference and types of transaction. In the

similar aspect, it will specify interest rate derivative market along with delta and gamma hedging

and theta.

QUESTION 1

a. Presence of Arbitrage opportunity with its exploitation

Current interest rate c(June) 12.00%

Future price of gold (December) 448

Future price 564

Spot price (December future price) 564/(1+12%)

503.57

spot price of gold in December future price

448/(1+12%)^.6

418.54

Spot price extracted from December future price is higher than spot price of gold in

December future price. Thus, actual future price of December is too high so there is presence of

arbitrage by selling its December future contract. The arbitrage could be exploited as stated

below:

Arbitrage position

Strategy Today December

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

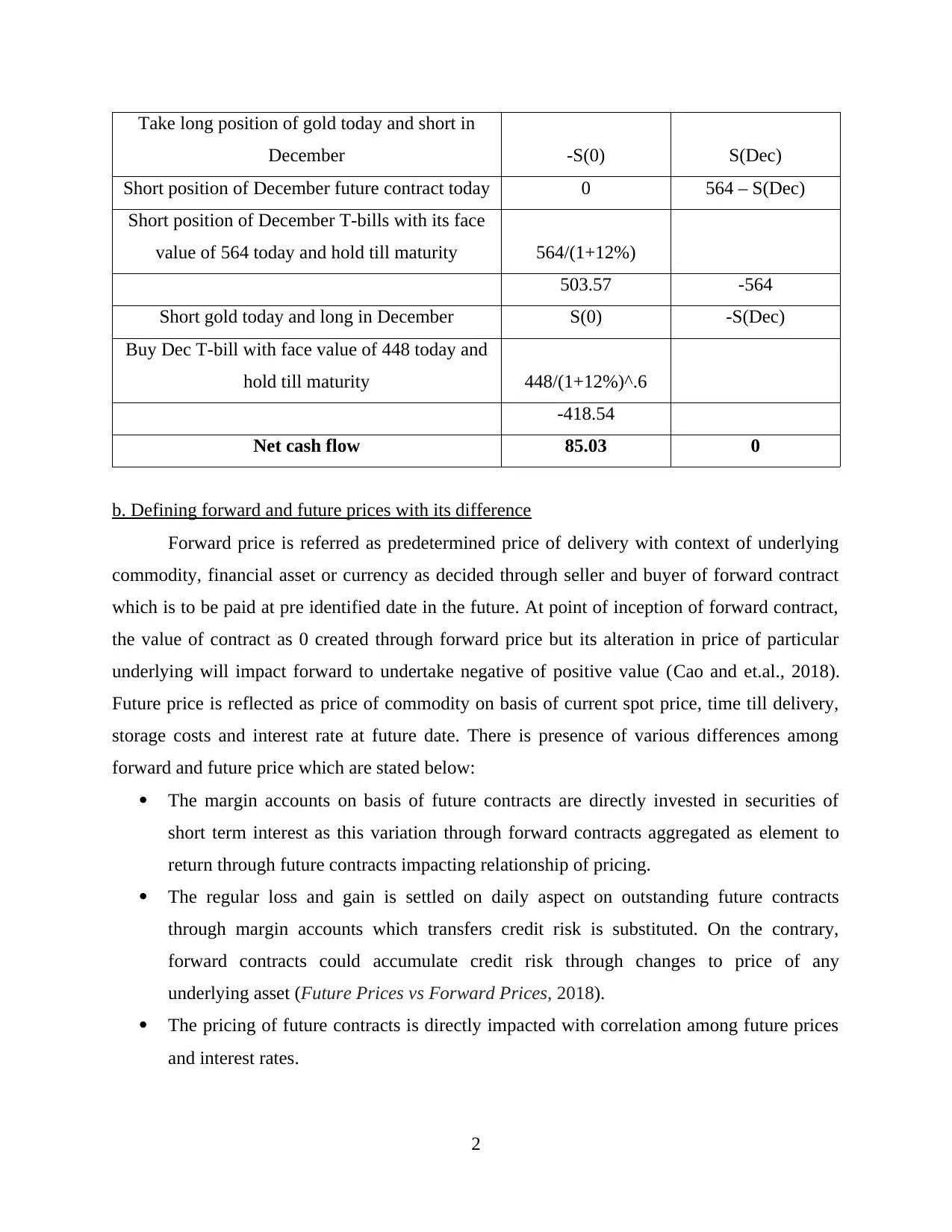

Take long position of gold today and short in

December -S(0) S(Dec)

Short position of December future contract today 0 564 – S(Dec)

Short position of December T-bills with its face

value of 564 today and hold till maturity 564/(1+12%)

503.57 -564

Short gold today and long in December S(0) -S(Dec)

Buy Dec T-bill with face value of 448 today and

hold till maturity 448/(1+12%)^.6

-418.54

Net cash flow 85.03 0

b. Defining forward and future prices with its difference

Forward price is referred as predetermined price of delivery with context of underlying

commodity, financial asset or currency as decided through seller and buyer of forward contract

which is to be paid at pre identified date in the future. At point of inception of forward contract,

the value of contract as 0 created through forward price but its alteration in price of particular

underlying will impact forward to undertake negative of positive value (Cao and et.al., 2018).

Future price is reflected as price of commodity on basis of current spot price, time till delivery,

storage costs and interest rate at future date. There is presence of various differences among

forward and future price which are stated below:

The margin accounts on basis of future contracts are directly invested in securities of

short term interest as this variation through forward contracts aggregated as element to

return through future contracts impacting relationship of pricing.

The regular loss and gain is settled on daily aspect on outstanding future contracts

through margin accounts which transfers credit risk is substituted. On the contrary,

forward contracts could accumulate credit risk through changes to price of any

underlying asset (Future Prices vs Forward Prices, 2018).

The pricing of future contracts is directly impacted with correlation among future prices

and interest rates.

2

December -S(0) S(Dec)

Short position of December future contract today 0 564 – S(Dec)

Short position of December T-bills with its face

value of 564 today and hold till maturity 564/(1+12%)

503.57 -564

Short gold today and long in December S(0) -S(Dec)

Buy Dec T-bill with face value of 448 today and

hold till maturity 448/(1+12%)^.6

-418.54

Net cash flow 85.03 0

b. Defining forward and future prices with its difference

Forward price is referred as predetermined price of delivery with context of underlying

commodity, financial asset or currency as decided through seller and buyer of forward contract

which is to be paid at pre identified date in the future. At point of inception of forward contract,

the value of contract as 0 created through forward price but its alteration in price of particular

underlying will impact forward to undertake negative of positive value (Cao and et.al., 2018).

Future price is reflected as price of commodity on basis of current spot price, time till delivery,

storage costs and interest rate at future date. There is presence of various differences among

forward and future price which are stated below:

The margin accounts on basis of future contracts are directly invested in securities of

short term interest as this variation through forward contracts aggregated as element to

return through future contracts impacting relationship of pricing.

The regular loss and gain is settled on daily aspect on outstanding future contracts

through margin accounts which transfers credit risk is substituted. On the contrary,

forward contracts could accumulate credit risk through changes to price of any

underlying asset (Future Prices vs Forward Prices, 2018).

The pricing of future contracts is directly impacted with correlation among future prices

and interest rates.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

If there is presence of positive correlation then buyer of future contract is benefited as

gaining higher through margin account interest and increment in contract price.

c. Types of transactions in the future market

The trader who long future contracts has absences of other position of exchange is long.

If this purchase in not offset through any equivalent sale of futures then its buyer will undertake

delivery of its actual commodity (Tamvakis, 2018). On the contrary, trader who sell any future

contract with absence of offsetting purchase of future is referred to be short.

With this perspective, traders who undertake position in market with two methods of

liquidating it as first engages with actual delivery or good's receipt. Generally, second option is

selected with huge probability as canceling obligation to sell or buy through carrying any reverse

operation as offsetting transaction. Through purchasing any matching contract a future trader in

position of short would be released through obligation for delivering. Simultaneously, trader who

is long could offset the outstanding purchases through selling. The basic types of transaction in

future contract are:

Against actual: It is highly possible for liquidating futures position in privately at spot

market with context of per-arranged trade. This transaction is replicated as against actual

trade and ignores complexities of creating physical delivery under future contract.

Conversely, these transactions should take place with various riles related to exchange

which supervises these future contracts (Chang, Ho and Hsiao, 2018).

Open interest: The sum of clearing house's short and long position outstanding at

specified moment is replicated as open interest. In the end of every trading day, there is

assumption of clearing house of one side of every open contracts as if any trader has long

positioned where clearing house undertakes short position and vice versa situation

(Futures markets-Offsetting transactions, 2018).

Cash and carry transaction: It is considered as kind of trade in future market where

price of any commodity is less than future contracts price. These transactions are

replicated as arbitrage and undertakes with cash or on spot market.

QUESTION 2

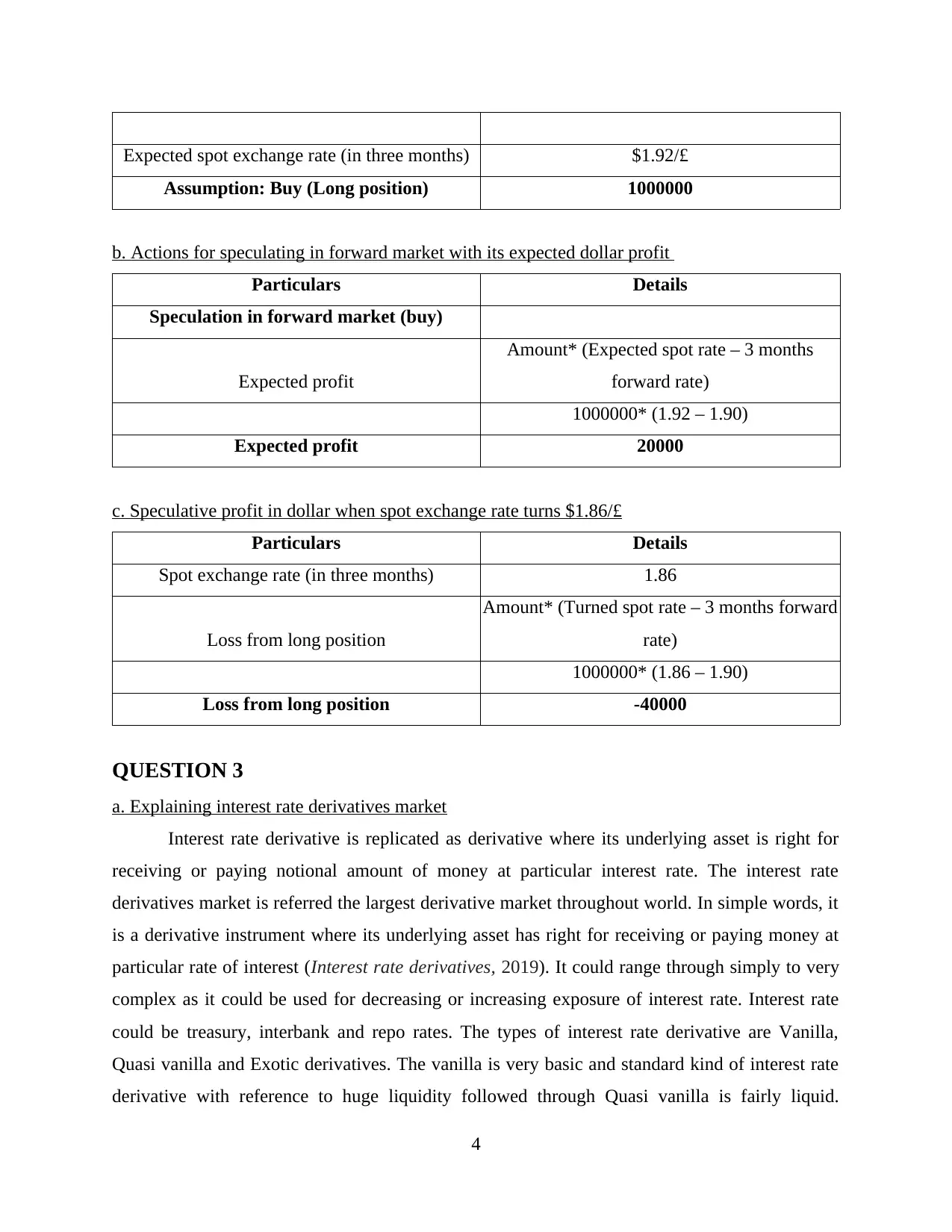

a. Assumption to buy or sell £1000000

Current spot exchange rate $1.95/£

3 month forward rate $1.90/£

3

gaining higher through margin account interest and increment in contract price.

c. Types of transactions in the future market

The trader who long future contracts has absences of other position of exchange is long.

If this purchase in not offset through any equivalent sale of futures then its buyer will undertake

delivery of its actual commodity (Tamvakis, 2018). On the contrary, trader who sell any future

contract with absence of offsetting purchase of future is referred to be short.

With this perspective, traders who undertake position in market with two methods of

liquidating it as first engages with actual delivery or good's receipt. Generally, second option is

selected with huge probability as canceling obligation to sell or buy through carrying any reverse

operation as offsetting transaction. Through purchasing any matching contract a future trader in

position of short would be released through obligation for delivering. Simultaneously, trader who

is long could offset the outstanding purchases through selling. The basic types of transaction in

future contract are:

Against actual: It is highly possible for liquidating futures position in privately at spot

market with context of per-arranged trade. This transaction is replicated as against actual

trade and ignores complexities of creating physical delivery under future contract.

Conversely, these transactions should take place with various riles related to exchange

which supervises these future contracts (Chang, Ho and Hsiao, 2018).

Open interest: The sum of clearing house's short and long position outstanding at

specified moment is replicated as open interest. In the end of every trading day, there is

assumption of clearing house of one side of every open contracts as if any trader has long

positioned where clearing house undertakes short position and vice versa situation

(Futures markets-Offsetting transactions, 2018).

Cash and carry transaction: It is considered as kind of trade in future market where

price of any commodity is less than future contracts price. These transactions are

replicated as arbitrage and undertakes with cash or on spot market.

QUESTION 2

a. Assumption to buy or sell £1000000

Current spot exchange rate $1.95/£

3 month forward rate $1.90/£

3

Expected spot exchange rate (in three months) $1.92/£

Assumption: Buy (Long position) 1000000

b. Actions for speculating in forward market with its expected dollar profit

Particulars Details

Speculation in forward market (buy)

Expected profit

Amount* (Expected spot rate – 3 months

forward rate)

1000000* (1.92 – 1.90)

Expected profit 20000

c. Speculative profit in dollar when spot exchange rate turns $1.86/£

Particulars Details

Spot exchange rate (in three months) 1.86

Loss from long position

Amount* (Turned spot rate – 3 months forward

rate)

1000000* (1.86 – 1.90)

Loss from long position -40000

QUESTION 3

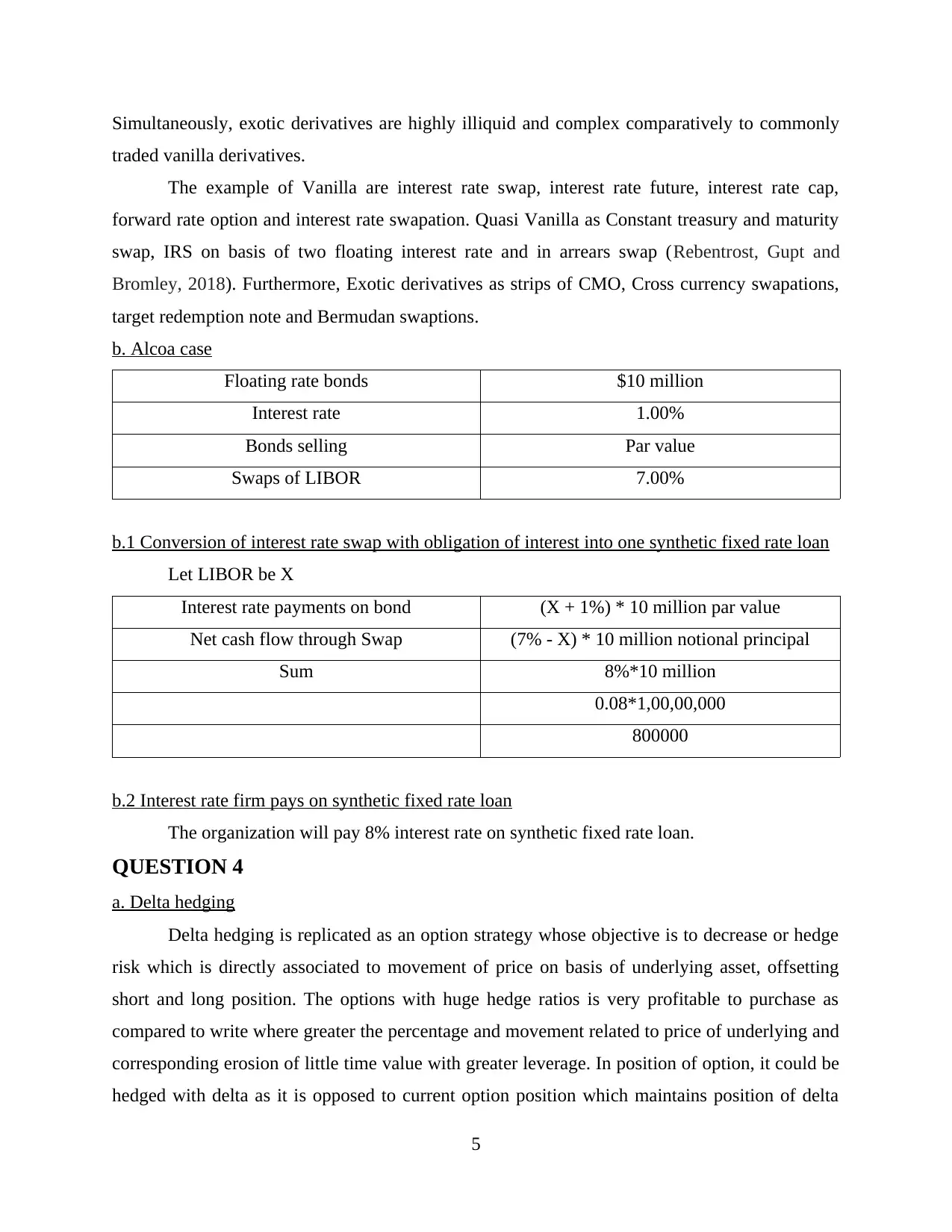

a. Explaining interest rate derivatives market

Interest rate derivative is replicated as derivative where its underlying asset is right for

receiving or paying notional amount of money at particular interest rate. The interest rate

derivatives market is referred the largest derivative market throughout world. In simple words, it

is a derivative instrument where its underlying asset has right for receiving or paying money at

particular rate of interest (Interest rate derivatives, 2019). It could range through simply to very

complex as it could be used for decreasing or increasing exposure of interest rate. Interest rate

could be treasury, interbank and repo rates. The types of interest rate derivative are Vanilla,

Quasi vanilla and Exotic derivatives. The vanilla is very basic and standard kind of interest rate

derivative with reference to huge liquidity followed through Quasi vanilla is fairly liquid.

4

Assumption: Buy (Long position) 1000000

b. Actions for speculating in forward market with its expected dollar profit

Particulars Details

Speculation in forward market (buy)

Expected profit

Amount* (Expected spot rate – 3 months

forward rate)

1000000* (1.92 – 1.90)

Expected profit 20000

c. Speculative profit in dollar when spot exchange rate turns $1.86/£

Particulars Details

Spot exchange rate (in three months) 1.86

Loss from long position

Amount* (Turned spot rate – 3 months forward

rate)

1000000* (1.86 – 1.90)

Loss from long position -40000

QUESTION 3

a. Explaining interest rate derivatives market

Interest rate derivative is replicated as derivative where its underlying asset is right for

receiving or paying notional amount of money at particular interest rate. The interest rate

derivatives market is referred the largest derivative market throughout world. In simple words, it

is a derivative instrument where its underlying asset has right for receiving or paying money at

particular rate of interest (Interest rate derivatives, 2019). It could range through simply to very

complex as it could be used for decreasing or increasing exposure of interest rate. Interest rate

could be treasury, interbank and repo rates. The types of interest rate derivative are Vanilla,

Quasi vanilla and Exotic derivatives. The vanilla is very basic and standard kind of interest rate

derivative with reference to huge liquidity followed through Quasi vanilla is fairly liquid.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Simultaneously, exotic derivatives are highly illiquid and complex comparatively to commonly

traded vanilla derivatives.

The example of Vanilla are interest rate swap, interest rate future, interest rate cap,

forward rate option and interest rate swapation. Quasi Vanilla as Constant treasury and maturity

swap, IRS on basis of two floating interest rate and in arrears swap (Rebentrost, Gupt and

Bromley, 2018). Furthermore, Exotic derivatives as strips of CMO, Cross currency swapations,

target redemption note and Bermudan swaptions.

b. Alcoa case

Floating rate bonds $10 million

Interest rate 1.00%

Bonds selling Par value

Swaps of LIBOR 7.00%

b.1 Conversion of interest rate swap with obligation of interest into one synthetic fixed rate loan

Let LIBOR be X

Interest rate payments on bond (X + 1%) * 10 million par value

Net cash flow through Swap (7% - X) * 10 million notional principal

Sum 8%*10 million

0.08*1,00,00,000

800000

b.2 Interest rate firm pays on synthetic fixed rate loan

The organization will pay 8% interest rate on synthetic fixed rate loan.

QUESTION 4

a. Delta hedging

Delta hedging is replicated as an option strategy whose objective is to decrease or hedge

risk which is directly associated to movement of price on basis of underlying asset, offsetting

short and long position. The options with huge hedge ratios is very profitable to purchase as

compared to write where greater the percentage and movement related to price of underlying and

corresponding erosion of little time value with greater leverage. In position of option, it could be

hedged with delta as it is opposed to current option position which maintains position of delta

5

traded vanilla derivatives.

The example of Vanilla are interest rate swap, interest rate future, interest rate cap,

forward rate option and interest rate swapation. Quasi Vanilla as Constant treasury and maturity

swap, IRS on basis of two floating interest rate and in arrears swap (Rebentrost, Gupt and

Bromley, 2018). Furthermore, Exotic derivatives as strips of CMO, Cross currency swapations,

target redemption note and Bermudan swaptions.

b. Alcoa case

Floating rate bonds $10 million

Interest rate 1.00%

Bonds selling Par value

Swaps of LIBOR 7.00%

b.1 Conversion of interest rate swap with obligation of interest into one synthetic fixed rate loan

Let LIBOR be X

Interest rate payments on bond (X + 1%) * 10 million par value

Net cash flow through Swap (7% - X) * 10 million notional principal

Sum 8%*10 million

0.08*1,00,00,000

800000

b.2 Interest rate firm pays on synthetic fixed rate loan

The organization will pay 8% interest rate on synthetic fixed rate loan.

QUESTION 4

a. Delta hedging

Delta hedging is replicated as an option strategy whose objective is to decrease or hedge

risk which is directly associated to movement of price on basis of underlying asset, offsetting

short and long position. The options with huge hedge ratios is very profitable to purchase as

compared to write where greater the percentage and movement related to price of underlying and

corresponding erosion of little time value with greater leverage. In position of option, it could be

hedged with delta as it is opposed to current option position which maintains position of delta

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

neutral. In simple words, delta neutral position is one where overall delta is zero and reduces

price movements related to underlying asset (Chen, 2018).

b. Theta

Theta helps in measuring exposure of price of option to particular time passage. In simple

words, rate has been measured at option price especially with context of time value, alterations

or decrement with time to expire has been approached. The option premium comprises time

value which decline to near time to expiration and declining with incur in expiration. In simple

words, it could be elaborated as measure of this time decay and reflected loss of time value per

day. It is minimal for purpose of long term option due to slowly time value decay but raises

expiration (Ghafarian, Hanafizadeh and Qahi, 2018). The theta of -.1 reflect option of losing $.10

of time value per day. Theta is at greatest when option is at money due to price where time value

is at greatest and has huge potential for decay.

In the same series, it measures alterations in option value of portfolio because of passage

of time and holdings of option has theta at negative position due to option value which declined

continuously along with time. Due to time decay which will favour option writer where short

position in option have positive position theta.

c. Gamma Hedging

Gamma hedging is referred as option of hedging strategy framed to eliminate, decrease

risk created with alteration in option delta. In simple words, it is change in delta for change in

each unit and underlying price. Furthermore, the absolute magnitude of delta raises time to

expiration of option decreases along with increment in intrinsic value.

d. Relationship among delta hedging, theta and gamma hedging

Delta gamma hedging is option strategy which mix both gamma and delta hedges for

purpose of mitigating risk of changes with context of underlying asset and delta as well. Delta

and gamma alters when stock price moves down or option moves in and out of money. The price

of at the money options will alter on significant aspect as compared to price of in and out of

money options with similar expiration. In this aspect, theta is very crucial concept as it gives

explanation about effect of time on option of premium sold or purchased.

6

price movements related to underlying asset (Chen, 2018).

b. Theta

Theta helps in measuring exposure of price of option to particular time passage. In simple

words, rate has been measured at option price especially with context of time value, alterations

or decrement with time to expire has been approached. The option premium comprises time

value which decline to near time to expiration and declining with incur in expiration. In simple

words, it could be elaborated as measure of this time decay and reflected loss of time value per

day. It is minimal for purpose of long term option due to slowly time value decay but raises

expiration (Ghafarian, Hanafizadeh and Qahi, 2018). The theta of -.1 reflect option of losing $.10

of time value per day. Theta is at greatest when option is at money due to price where time value

is at greatest and has huge potential for decay.

In the same series, it measures alterations in option value of portfolio because of passage

of time and holdings of option has theta at negative position due to option value which declined

continuously along with time. Due to time decay which will favour option writer where short

position in option have positive position theta.

c. Gamma Hedging

Gamma hedging is referred as option of hedging strategy framed to eliminate, decrease

risk created with alteration in option delta. In simple words, it is change in delta for change in

each unit and underlying price. Furthermore, the absolute magnitude of delta raises time to

expiration of option decreases along with increment in intrinsic value.

d. Relationship among delta hedging, theta and gamma hedging

Delta gamma hedging is option strategy which mix both gamma and delta hedges for

purpose of mitigating risk of changes with context of underlying asset and delta as well. Delta

and gamma alters when stock price moves down or option moves in and out of money. The price

of at the money options will alter on significant aspect as compared to price of in and out of

money options with similar expiration. In this aspect, theta is very crucial concept as it gives

explanation about effect of time on option of premium sold or purchased.

6

QUESTION 5

a. Explaining Option's implied volatility and method for calculating

Implied volatility is replicated parameter part with context of pricing model of option like

Black Scholes model which specifies market price of option. In simple words, it helps in

reflecting views of marketplace that where marketplace considers about volatility in the future.

The option's implied volatility is forward looking as it helps in gauging sentiment related to

stock's volatility or market as well (Markellos and Psychoyios, 2018). On the contrary, implied

volatility does not predict direction where option is headed. It is a dynamic figure which alters on

basis of activity in options market . Generally, when there is increment in implied volatility then

option price will also raise along with assumption that else all other things are constant

(Volatility, 2019). Thus, if there is raise in implied volatility after trade which is placed and good

for owner of option and worse for its seller.

Implied volatility could be extracted by undertaking market price of option, and

considering it in formula of black scholes model and solving for purpose of extracting volatility's

value. Simultaneously, there are multiple approaches for calculating implied volatility such as

application of iterative approach or trial and error method to calculate value of implied volatility

of option.

b. Explaining strength and weakness of Implied Volatility Function

Strength

It is very important input with context of valuation model of option as its input is referred

as user defined variable (not similar to dividend or interest rates). It is the only input which alters

because of demand and supply of its underlying options along with expectation of market

through direction of share price. In case expectations will raise then there will be increment in

demand of option along with rise in implied volatility (Fernandes and et.al., 2018). Generally,

options which have huge level of implied volatility whose outcome is related to premium of high

priced option. In simple words, it is very significant due to rise and fall in implied volatility will

identify about cheap and expensive time value to option and in turn it will give direct impact on

success options of trade.

Weakness

It had been evaluated that belief about prevailing sentiment about investor revealed with

price, open interest configuration and volume is wrong where predictive approach for activity of

7

a. Explaining Option's implied volatility and method for calculating

Implied volatility is replicated parameter part with context of pricing model of option like

Black Scholes model which specifies market price of option. In simple words, it helps in

reflecting views of marketplace that where marketplace considers about volatility in the future.

The option's implied volatility is forward looking as it helps in gauging sentiment related to

stock's volatility or market as well (Markellos and Psychoyios, 2018). On the contrary, implied

volatility does not predict direction where option is headed. It is a dynamic figure which alters on

basis of activity in options market . Generally, when there is increment in implied volatility then

option price will also raise along with assumption that else all other things are constant

(Volatility, 2019). Thus, if there is raise in implied volatility after trade which is placed and good

for owner of option and worse for its seller.

Implied volatility could be extracted by undertaking market price of option, and

considering it in formula of black scholes model and solving for purpose of extracting volatility's

value. Simultaneously, there are multiple approaches for calculating implied volatility such as

application of iterative approach or trial and error method to calculate value of implied volatility

of option.

b. Explaining strength and weakness of Implied Volatility Function

Strength

It is very important input with context of valuation model of option as its input is referred

as user defined variable (not similar to dividend or interest rates). It is the only input which alters

because of demand and supply of its underlying options along with expectation of market

through direction of share price. In case expectations will raise then there will be increment in

demand of option along with rise in implied volatility (Fernandes and et.al., 2018). Generally,

options which have huge level of implied volatility whose outcome is related to premium of high

priced option. In simple words, it is very significant due to rise and fall in implied volatility will

identify about cheap and expensive time value to option and in turn it will give direct impact on

success options of trade.

Weakness

It had been evaluated that belief about prevailing sentiment about investor revealed with

price, open interest configuration and volume is wrong where predictive approach for activity of

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

option where actual information reveals along with its challenges. It is used for determining

significant alteration in price direction such as signals of buy and sell is produced when reading

directly hit extreme level in reaction for identifiable event. Volatility is non directional which

signifies about magnitude and probability of price moving but not with direction and could not

be used for predictive indicator.

c. Explaining Ho & Lee model with graphical presentation and note on building interest rate tree

It is an interest rate option model which implies short rates related to pricing interest rate

derivatives like swapations and bond options or to value fixed income securities along with

embedded options like puttable and callable bonds etc. In simple words, it could be elaborated as

model with uncertain behaviour of structure of interest rate as whole but not with certain point on

curve. At the end, arbitrage free and term structure model assumes about interest rate with

context of yield curve correlated with irreversible to its mean (Kumar, 2018). The Ho-lee model

could be represented with this below stated tree:

Here u and u' is estimated for ensuring about short rate process which is consistent with

recent term structure of its interest rates. In this example, 0.5 is assumed with risk neutral

probability of its up movement.

Building interest rate tree

The derivation of interest rate follows process of four steps such as building perturbation

function as it is mathematical method which is used for gaining an approximate solution to a

problem because of inability to extract exact one. It will lead to build exact solution on basis of

related problem. In next step, calculation of risk neutral probabilities dependent on Cox-Ross-

8

significant alteration in price direction such as signals of buy and sell is produced when reading

directly hit extreme level in reaction for identifiable event. Volatility is non directional which

signifies about magnitude and probability of price moving but not with direction and could not

be used for predictive indicator.

c. Explaining Ho & Lee model with graphical presentation and note on building interest rate tree

It is an interest rate option model which implies short rates related to pricing interest rate

derivatives like swapations and bond options or to value fixed income securities along with

embedded options like puttable and callable bonds etc. In simple words, it could be elaborated as

model with uncertain behaviour of structure of interest rate as whole but not with certain point on

curve. At the end, arbitrage free and term structure model assumes about interest rate with

context of yield curve correlated with irreversible to its mean (Kumar, 2018). The Ho-lee model

could be represented with this below stated tree:

Here u and u' is estimated for ensuring about short rate process which is consistent with

recent term structure of its interest rates. In this example, 0.5 is assumed with risk neutral

probability of its up movement.

Building interest rate tree

The derivation of interest rate follows process of four steps such as building perturbation

function as it is mathematical method which is used for gaining an approximate solution to a

problem because of inability to extract exact one. It will lead to build exact solution on basis of

related problem. In next step, calculation of risk neutral probabilities dependent on Cox-Ross-

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Rubinstein model and then deriving path dependence condition with application of binomial tree.

Atlast, combination of previous steps. In simple words, binomial tree is graphical representation

of all possible intrinsic values where option might undertake various nodes or time period.

CONCLUSION

On basis of above report it could be concluded that future and options are very important

for purpose of mitigating risk. In the same series, it has shown that arbitrage strategy is very

useful for reducing risk to gain benefit. Lastly, it could be said that Implied volatility function is

very important as it has both pros and cons as well but useful to eliminate issues.

9

Atlast, combination of previous steps. In simple words, binomial tree is graphical representation

of all possible intrinsic values where option might undertake various nodes or time period.

CONCLUSION

On basis of above report it could be concluded that future and options are very important

for purpose of mitigating risk. In the same series, it has shown that arbitrage strategy is very

useful for reducing risk to gain benefit. Lastly, it could be said that Implied volatility function is

very important as it has both pros and cons as well but useful to eliminate issues.

9

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.