Financial Valuation: Approaches, Models, and Forecasting Techniques

VerifiedAdded on 2023/01/09

|5

|1765

|80

Homework Assignment

AI Summary

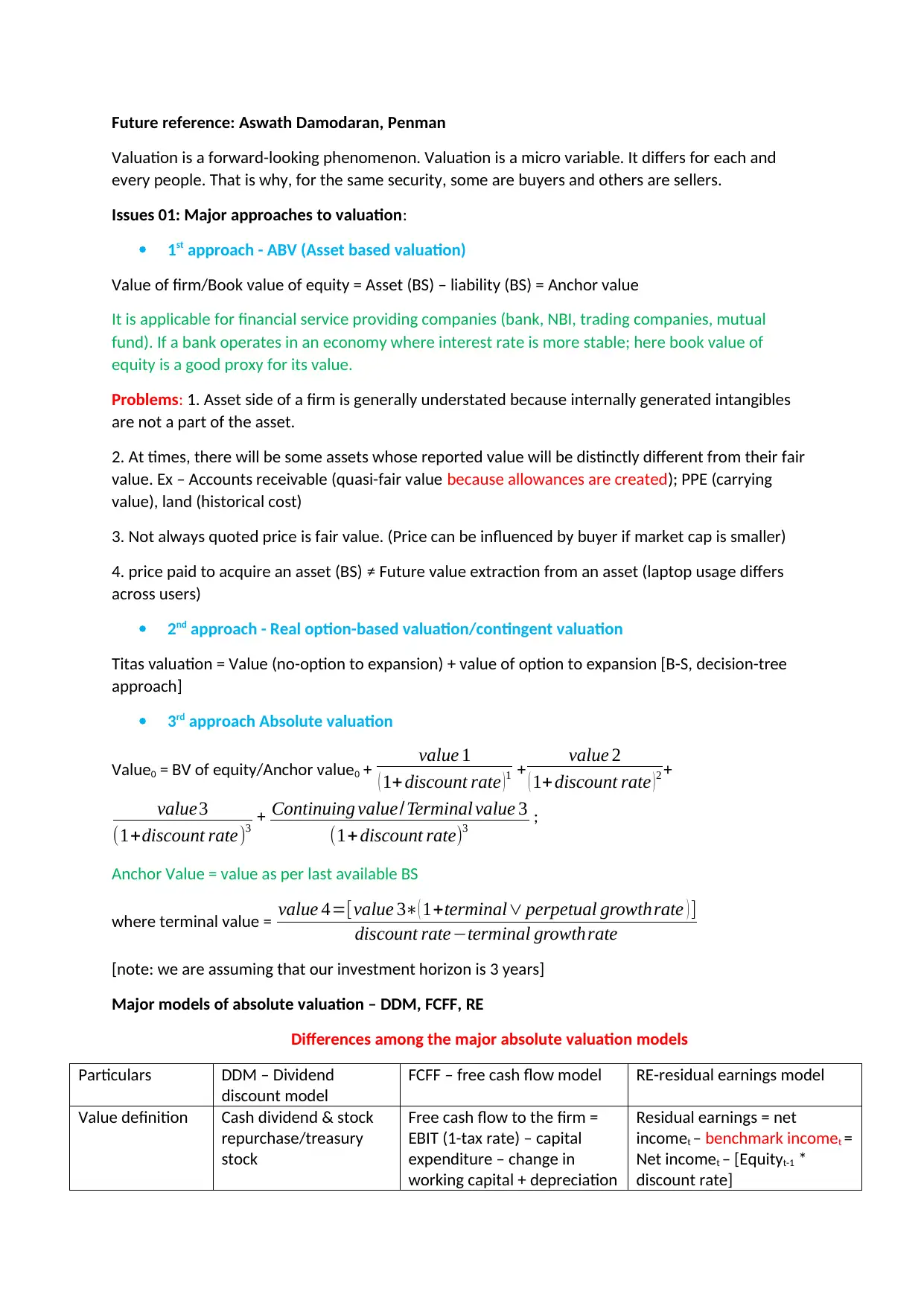

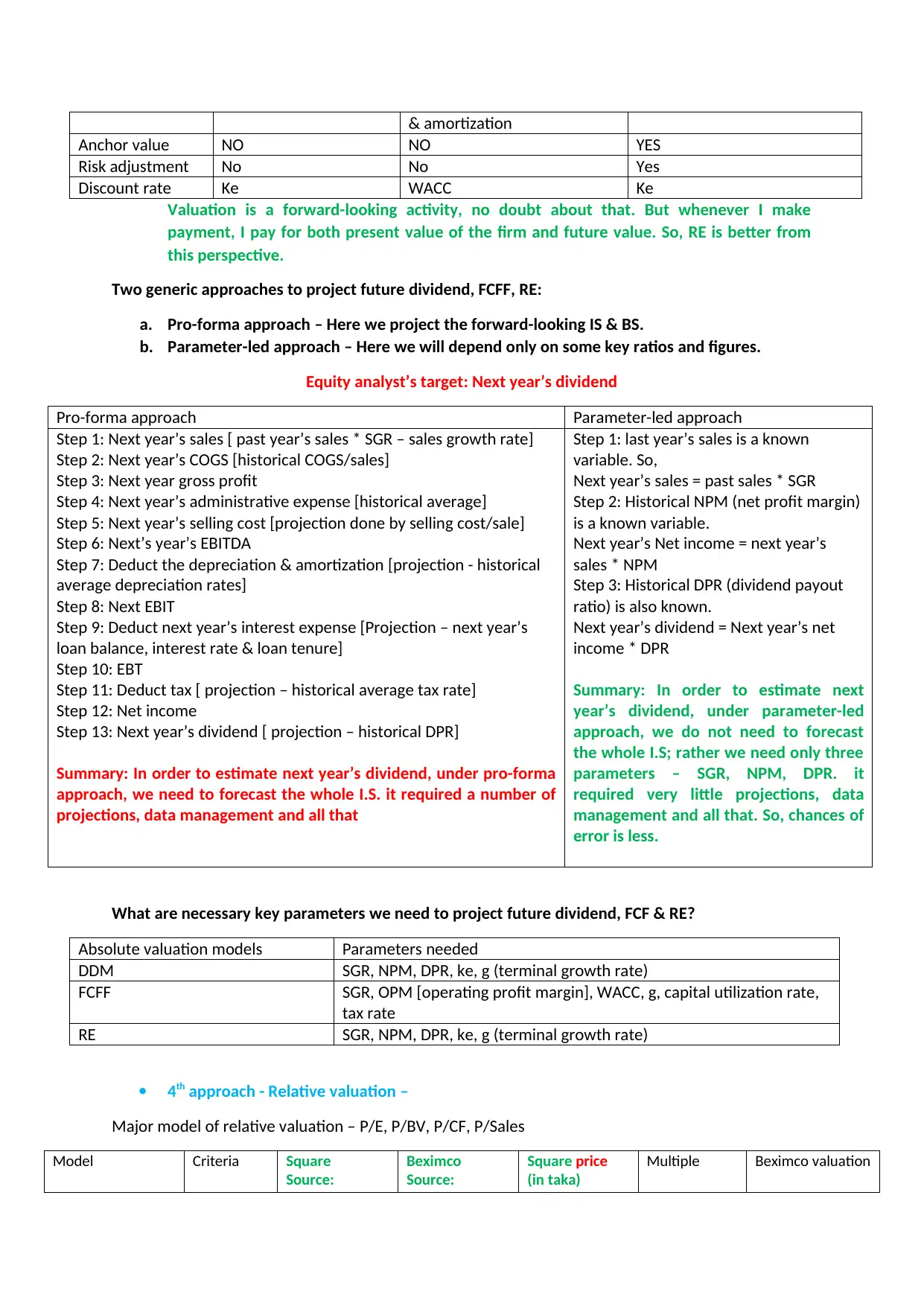

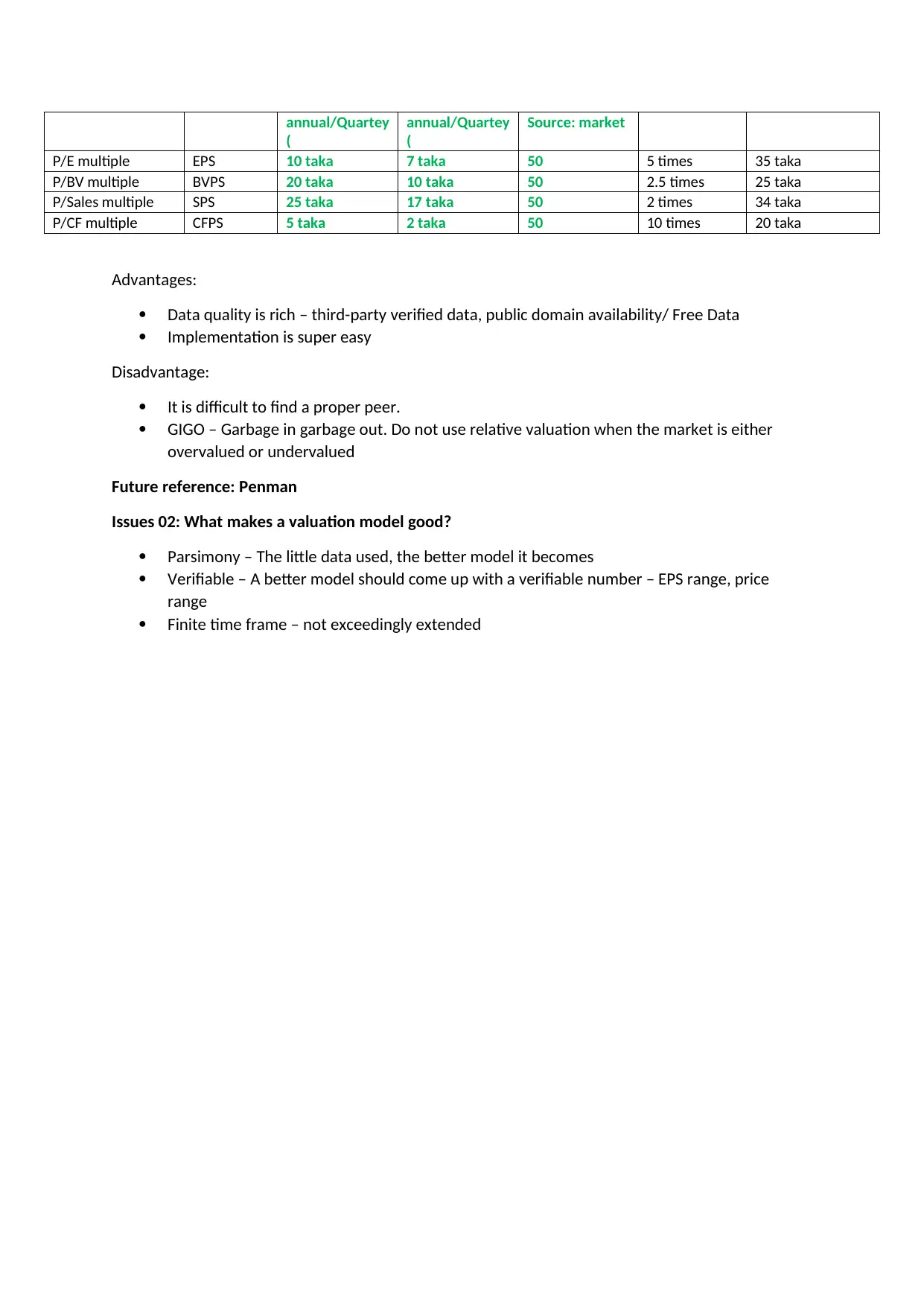

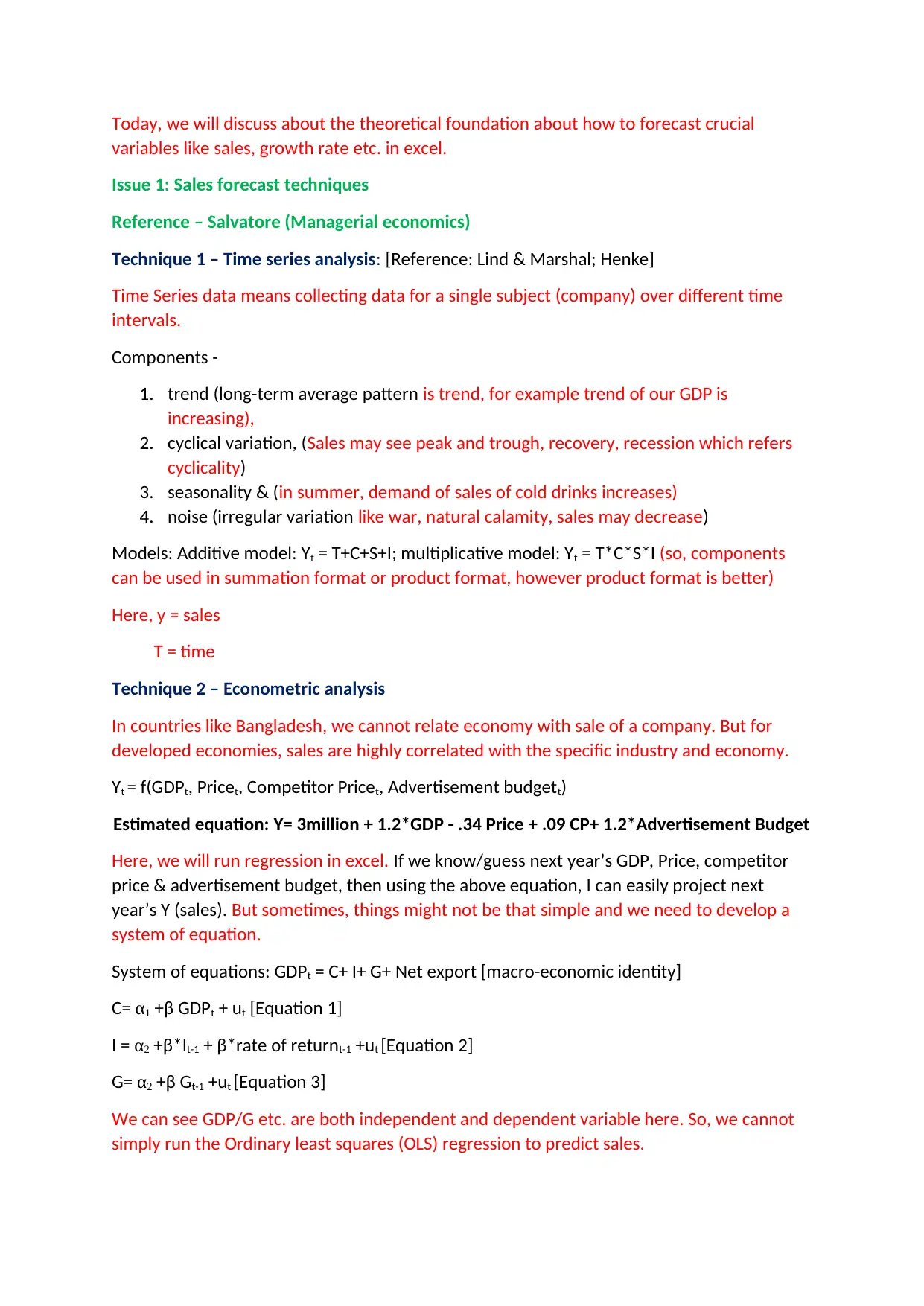

This assignment explores various approaches to financial valuation, including asset-based, real option-based, absolute, and relative valuation techniques. It delves into specific models like Dividend Discount Model (DDM), Free Cash Flow to the Firm (FCFF), and Residual Earnings (RE) models, comparing their value definitions, risk adjustments, and discount rates. The assignment also covers different methods for projecting future dividends, free cash flow, and residual earnings, such as pro-forma and parameter-led approaches. Furthermore, it discusses relative valuation models like P/E, P/BV, P/CF, and P/Sales, highlighting their advantages and disadvantages. The document also examines sales forecasting techniques, including time series analysis, econometric analysis, smoothing techniques, and economic barometer tools, providing insights into how to forecast crucial variables in financial analysis. Finally, it emphasizes the importance of parsimony and verifiability in building a good valuation model.

1 out of 5

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.