Forecasting Sales Techniques

Added on 2023-01-09

5 Pages1765 Words80 Views

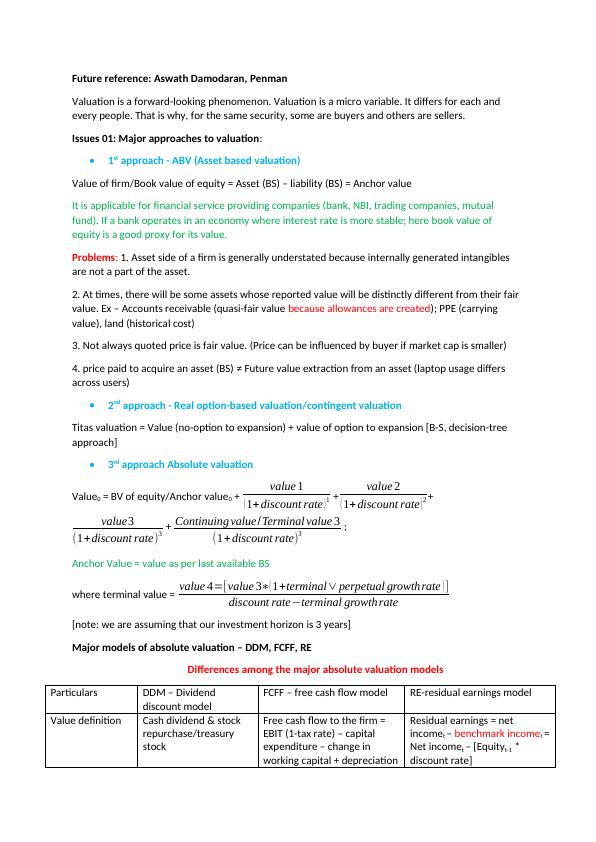

Future reference: Aswath Damodaran, Penman

Valuation is a forward-looking phenomenon. Valuation is a micro variable. It differs for each and

every people. That is why, for the same security, some are buyers and others are sellers.

Issues 01: Major approaches to valuation:

1st approach - ABV (Asset based valuation)

Value of firm/Book value of equity = Asset (BS) – liability (BS) = Anchor value

It is applicable for financial service providing companies (bank, NBI, trading companies, mutual

fund). If a bank operates in an economy where interest rate is more stable; here book value of

equity is a good proxy for its value.

Problems: 1. Asset side of a firm is generally understated because internally generated intangibles

are not a part of the asset.

2. At times, there will be some assets whose reported value will be distinctly different from their fair

value. Ex – Accounts receivable (quasi-fair value because allowances are created); PPE (carrying

value), land (historical cost)

3. Not always quoted price is fair value. (Price can be influenced by buyer if market cap is smaller)

4. price paid to acquire an asset (BS) ≠ Future value extraction from an asset (laptop usage differs

across users)

2nd approach - Real option-based valuation/contingent valuation

Titas valuation = Value (no-option to expansion) + value of option to expansion [B-S, decision-tree

approach]

3rd approach Absolute valuation

Value0 = BV of equity/Anchor value0 + value 1

( 1+ discount rate ) 1 + value 2

( 1+ discount rate )2 +

value3

(1+discount rate)3 + Continuing value/Terminal value 3

(1+ discount rate)3 ;

Anchor Value = value as per last available BS

where terminal value = value 4=[value 3∗( 1+terminal∨ perpetual growthrate ) ]

discount rate−terminal growthrate

[note: we are assuming that our investment horizon is 3 years]

Major models of absolute valuation – DDM, FCFF, RE

Differences among the major absolute valuation models

Particulars DDM – Dividend

discount model

FCFF – free cash flow model RE-residual earnings model

Value definition Cash dividend & stock

repurchase/treasury

stock

Free cash flow to the firm =

EBIT (1-tax rate) – capital

expenditure – change in

working capital + depreciation

Residual earnings = net

incomet – benchmark incomet =

Net incomet – [Equityt-1 *

discount rate]

Valuation is a forward-looking phenomenon. Valuation is a micro variable. It differs for each and

every people. That is why, for the same security, some are buyers and others are sellers.

Issues 01: Major approaches to valuation:

1st approach - ABV (Asset based valuation)

Value of firm/Book value of equity = Asset (BS) – liability (BS) = Anchor value

It is applicable for financial service providing companies (bank, NBI, trading companies, mutual

fund). If a bank operates in an economy where interest rate is more stable; here book value of

equity is a good proxy for its value.

Problems: 1. Asset side of a firm is generally understated because internally generated intangibles

are not a part of the asset.

2. At times, there will be some assets whose reported value will be distinctly different from their fair

value. Ex – Accounts receivable (quasi-fair value because allowances are created); PPE (carrying

value), land (historical cost)

3. Not always quoted price is fair value. (Price can be influenced by buyer if market cap is smaller)

4. price paid to acquire an asset (BS) ≠ Future value extraction from an asset (laptop usage differs

across users)

2nd approach - Real option-based valuation/contingent valuation

Titas valuation = Value (no-option to expansion) + value of option to expansion [B-S, decision-tree

approach]

3rd approach Absolute valuation

Value0 = BV of equity/Anchor value0 + value 1

( 1+ discount rate ) 1 + value 2

( 1+ discount rate )2 +

value3

(1+discount rate)3 + Continuing value/Terminal value 3

(1+ discount rate)3 ;

Anchor Value = value as per last available BS

where terminal value = value 4=[value 3∗( 1+terminal∨ perpetual growthrate ) ]

discount rate−terminal growthrate

[note: we are assuming that our investment horizon is 3 years]

Major models of absolute valuation – DDM, FCFF, RE

Differences among the major absolute valuation models

Particulars DDM – Dividend

discount model

FCFF – free cash flow model RE-residual earnings model

Value definition Cash dividend & stock

repurchase/treasury

stock

Free cash flow to the firm =

EBIT (1-tax rate) – capital

expenditure – change in

working capital + depreciation

Residual earnings = net

incomet – benchmark incomet =

Net incomet – [Equityt-1 *

discount rate]

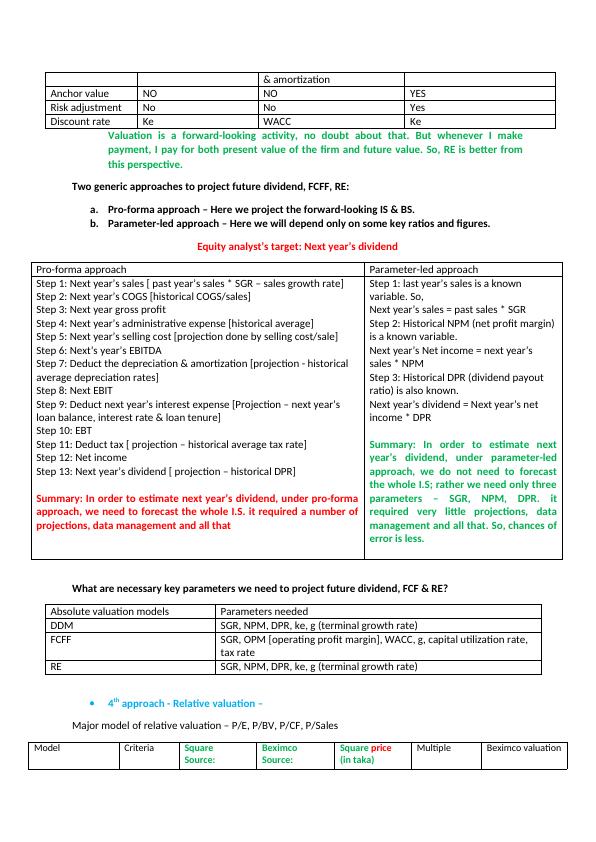

& amortization

Anchor value NO NO YES

Risk adjustment No No Yes

Discount rate Ke WACC Ke

Valuation is a forward-looking activity, no doubt about that. But whenever I make

payment, I pay for both present value of the firm and future value. So, RE is better from

this perspective.

Two generic approaches to project future dividend, FCFF, RE:

a. Pro-forma approach – Here we project the forward-looking IS & BS.

b. Parameter-led approach – Here we will depend only on some key ratios and figures.

Equity analyst’s target: Next year’s dividend

Pro-forma approach Parameter-led approach

Step 1: Next year’s sales [ past year’s sales * SGR – sales growth rate]

Step 2: Next year’s COGS [historical COGS/sales]

Step 3: Next year gross profit

Step 4: Next year’s administrative expense [historical average]

Step 5: Next year’s selling cost [projection done by selling cost/sale]

Step 6: Next’s year’s EBITDA

Step 7: Deduct the depreciation & amortization [projection - historical

average depreciation rates]

Step 8: Next EBIT

Step 9: Deduct next year’s interest expense [Projection – next year’s

loan balance, interest rate & loan tenure]

Step 10: EBT

Step 11: Deduct tax [ projection – historical average tax rate]

Step 12: Net income

Step 13: Next year’s dividend [ projection – historical DPR]

Summary: In order to estimate next year’s dividend, under pro-forma

approach, we need to forecast the whole I.S. it required a number of

projections, data management and all that

Step 1: last year’s sales is a known

variable. So,

Next year’s sales = past sales * SGR

Step 2: Historical NPM (net profit margin)

is a known variable.

Next year’s Net income = next year’s

sales * NPM

Step 3: Historical DPR (dividend payout

ratio) is also known.

Next year’s dividend = Next year’s net

income * DPR

Summary: In order to estimate next

year’s dividend, under parameter-led

approach, we do not need to forecast

the whole I.S; rather we need only three

parameters – SGR, NPM, DPR. it

required very little projections, data

management and all that. So, chances of

error is less.

What are necessary key parameters we need to project future dividend, FCF & RE?

Absolute valuation models Parameters needed

DDM SGR, NPM, DPR, ke, g (terminal growth rate)

FCFF SGR, OPM [operating profit margin], WACC, g, capital utilization rate,

tax rate

RE SGR, NPM, DPR, ke, g (terminal growth rate)

4th approach - Relative valuation –

Major model of relative valuation – P/E, P/BV, P/CF, P/Sales

Model Criteria Square

Source:

Beximco

Source:

Square price

(in taka)

Multiple Beximco valuation

Anchor value NO NO YES

Risk adjustment No No Yes

Discount rate Ke WACC Ke

Valuation is a forward-looking activity, no doubt about that. But whenever I make

payment, I pay for both present value of the firm and future value. So, RE is better from

this perspective.

Two generic approaches to project future dividend, FCFF, RE:

a. Pro-forma approach – Here we project the forward-looking IS & BS.

b. Parameter-led approach – Here we will depend only on some key ratios and figures.

Equity analyst’s target: Next year’s dividend

Pro-forma approach Parameter-led approach

Step 1: Next year’s sales [ past year’s sales * SGR – sales growth rate]

Step 2: Next year’s COGS [historical COGS/sales]

Step 3: Next year gross profit

Step 4: Next year’s administrative expense [historical average]

Step 5: Next year’s selling cost [projection done by selling cost/sale]

Step 6: Next’s year’s EBITDA

Step 7: Deduct the depreciation & amortization [projection - historical

average depreciation rates]

Step 8: Next EBIT

Step 9: Deduct next year’s interest expense [Projection – next year’s

loan balance, interest rate & loan tenure]

Step 10: EBT

Step 11: Deduct tax [ projection – historical average tax rate]

Step 12: Net income

Step 13: Next year’s dividend [ projection – historical DPR]

Summary: In order to estimate next year’s dividend, under pro-forma

approach, we need to forecast the whole I.S. it required a number of

projections, data management and all that

Step 1: last year’s sales is a known

variable. So,

Next year’s sales = past sales * SGR

Step 2: Historical NPM (net profit margin)

is a known variable.

Next year’s Net income = next year’s

sales * NPM

Step 3: Historical DPR (dividend payout

ratio) is also known.

Next year’s dividend = Next year’s net

income * DPR

Summary: In order to estimate next

year’s dividend, under parameter-led

approach, we do not need to forecast

the whole I.S; rather we need only three

parameters – SGR, NPM, DPR. it

required very little projections, data

management and all that. So, chances of

error is less.

What are necessary key parameters we need to project future dividend, FCF & RE?

Absolute valuation models Parameters needed

DDM SGR, NPM, DPR, ke, g (terminal growth rate)

FCFF SGR, OPM [operating profit margin], WACC, g, capital utilization rate,

tax rate

RE SGR, NPM, DPR, ke, g (terminal growth rate)

4th approach - Relative valuation –

Major model of relative valuation – P/E, P/BV, P/CF, P/Sales

Model Criteria Square

Source:

Beximco

Source:

Square price

(in taka)

Multiple Beximco valuation

End of preview

Want to access all the pages? Upload your documents or become a member.

Related Documents

Financial Management: Valuation Techniques and Investment Appraisallg...

|15

|3763

|50

Report On Debenhams's Corporate Financial Strategylg...

|24

|6240

|32