Difference between GAAP and Non-GAAP Earnings: A Case Study of Qantas Airways and Star Entertainment Group Limited

VerifiedAdded on 2023/06/13

|16

|3139

|78

AI Summary

This research study analyzes the difference between GAAP and Non-GAAP earnings with a case study of Qantas Airways and Star Entertainment Group Limited. The study focuses on the impact of GAAP and Non-GAAP earnings on the share price of the companies. The methodology used is the event study method. The data is collected from secondary sources like academic journals and financial documents. The study concludes that GAAP earnings are more reliable and informative than Non-GAAP earnings.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: RESEARCH PROJECT

Research Project

Name of the Student:

Name of the University:

Author Note

Research Project

Name of the Student:

Name of the University:

Author Note

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1RESEARCH PROJECT

Table of Contents

Introduction......................................................................................................................................2

Quantas Airways Limited................................................................................................................2

Star Entertainment Group Limited..................................................................................................2

Distinction between the Earnings method utilized by the different corporate entities....................3

Literature Review............................................................................................................................4

GAAP earnings and Non-GAAP earnings..................................................................................4

Quantas and Star Entertainment Group Limited.........................................................................5

Methodology....................................................................................................................................5

Conclusion.......................................................................................................................................5

References........................................................................................................................................7

Table of Contents

Introduction......................................................................................................................................2

Quantas Airways Limited................................................................................................................2

Star Entertainment Group Limited..................................................................................................2

Distinction between the Earnings method utilized by the different corporate entities....................3

Literature Review............................................................................................................................4

GAAP earnings and Non-GAAP earnings..................................................................................4

Quantas and Star Entertainment Group Limited.........................................................................5

Methodology....................................................................................................................................5

Conclusion.......................................................................................................................................5

References........................................................................................................................................7

2RESEARCH PROJECT

Introduction

The Generally Accepted Accounting Principles had been developed by the Financial

Accounting Standards Board for the purpose of standardizing the process of financial reporting

by the providence of formats and rules and is essentially carried out for facilitating of the

financial position of an organization by the creditors and investors. The utilization of the

Generally Accepted Accounting Principles method of earning facilitates the reflection of the fair

image of the business entity. Moreover, the annual reports of the different business entities that

have been prepared on the basis of the GAAP can be reliably compared and analyzed.

The Non–GAAP earnings on the other hand, refers to the accounting regulation that has

been utilized by the corporate entities for the purpose of displaying their own accounting figures.

Such an accounting regulation is also legally supported as long as these accounting treatments

have been disclosed as Non-GAAP in the annual report of the company and the providence of

the reconciliation is carried out between the adjusted and regular results.

This particular study aims to focus on the difference between the GAAP and the Non-

GAAP earnings. Moreover, the organizations that have been further selected for the better

understanding of the research study are the Quantas Airways Limited and Star Entertainment

Group Limited. These examples of the corporate entities have been utilized for the purpose of

developing the particular research proposal that whether the accounting regulation of GAAP

earnings are more useful in comparison to the Non-GAAP earnings.

Qantas Airways Limited

The first company that has been selected for the purpose of the study is the Quantas

Airways Limited that has been a domestic and international airline service provider. This airline

Introduction

The Generally Accepted Accounting Principles had been developed by the Financial

Accounting Standards Board for the purpose of standardizing the process of financial reporting

by the providence of formats and rules and is essentially carried out for facilitating of the

financial position of an organization by the creditors and investors. The utilization of the

Generally Accepted Accounting Principles method of earning facilitates the reflection of the fair

image of the business entity. Moreover, the annual reports of the different business entities that

have been prepared on the basis of the GAAP can be reliably compared and analyzed.

The Non–GAAP earnings on the other hand, refers to the accounting regulation that has

been utilized by the corporate entities for the purpose of displaying their own accounting figures.

Such an accounting regulation is also legally supported as long as these accounting treatments

have been disclosed as Non-GAAP in the annual report of the company and the providence of

the reconciliation is carried out between the adjusted and regular results.

This particular study aims to focus on the difference between the GAAP and the Non-

GAAP earnings. Moreover, the organizations that have been further selected for the better

understanding of the research study are the Quantas Airways Limited and Star Entertainment

Group Limited. These examples of the corporate entities have been utilized for the purpose of

developing the particular research proposal that whether the accounting regulation of GAAP

earnings are more useful in comparison to the Non-GAAP earnings.

Qantas Airways Limited

The first company that has been selected for the purpose of the study is the Quantas

Airways Limited that has been a domestic and international airline service provider. This airline

3RESEARCH PROJECT

service provider has been operating globally and is based out of Australia. The profitability

graph of the selected company has gone through regular crests and troughs until the financial

year of 2016.

Star Entertainment Group Limited

The Star Entertainment Group Limited has been one of the largest entertainment and

gaming groups on Australia. The Star Entertainment Group Limited has essentially been a

corporate entity that has demerged from the parent entity in June 2011. The initial name of the

corporate entity had been Echo Entertainment Group Limited. The demerger from the parent

entity resulted in the occupying of the casinos business and from November 2015, the parent

entity came to be known as Star Entertainment Group Limited. The Star Entertainment Group

Limited has been listed under the top 100 listed corporate entities of Australia and operates under

three major hotels and casinos of Australia namely Treasury Casino and Hotel in Brisbane, The

Star Gold Coast on the Gold Coast and The Star, Sydney. The net profit that has been derived by

the firm for the financial year of 2017 revolves around the figure of $264.4 million.

Distinction between the Earnings method utilized by the different corporate entities

The particular distinction between the corporate entities utilizing the particular mode of

accounting regulations is that Quantas Airways does utilize the Non-GAAP methods while the

corporate entity of Star Entertainment Group Limited utilizes the GAAP earning method. The

particular rationale that has been provided by the executives of the particular airlines entity is

that the utilization of the non-statutory metrics for the purpose of preparation of the financial

statements have resulted in the resolving of the particular issues like the arrival at the adjusted

underlying profit and is generally higher than the reported number that is arrived at, by utilizing

GAAP. The management of the corporate entity further claims that the utilization of the Non-

service provider has been operating globally and is based out of Australia. The profitability

graph of the selected company has gone through regular crests and troughs until the financial

year of 2016.

Star Entertainment Group Limited

The Star Entertainment Group Limited has been one of the largest entertainment and

gaming groups on Australia. The Star Entertainment Group Limited has essentially been a

corporate entity that has demerged from the parent entity in June 2011. The initial name of the

corporate entity had been Echo Entertainment Group Limited. The demerger from the parent

entity resulted in the occupying of the casinos business and from November 2015, the parent

entity came to be known as Star Entertainment Group Limited. The Star Entertainment Group

Limited has been listed under the top 100 listed corporate entities of Australia and operates under

three major hotels and casinos of Australia namely Treasury Casino and Hotel in Brisbane, The

Star Gold Coast on the Gold Coast and The Star, Sydney. The net profit that has been derived by

the firm for the financial year of 2017 revolves around the figure of $264.4 million.

Distinction between the Earnings method utilized by the different corporate entities

The particular distinction between the corporate entities utilizing the particular mode of

accounting regulations is that Quantas Airways does utilize the Non-GAAP methods while the

corporate entity of Star Entertainment Group Limited utilizes the GAAP earning method. The

particular rationale that has been provided by the executives of the particular airlines entity is

that the utilization of the non-statutory metrics for the purpose of preparation of the financial

statements have resulted in the resolving of the particular issues like the arrival at the adjusted

underlying profit and is generally higher than the reported number that is arrived at, by utilizing

GAAP. The management of the corporate entity further claims that the utilization of the Non-

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4RESEARCH PROJECT

GAAP standards that is non-regulated and the non-audited standards have been more informative

and reflective in nature (Baginski caes et al 2016).

On the other hand, the firm utilizing the traditional process of accounting that is the

generally accepted accounting principles, have to go through a defined and detailed guideline of

accounting standards for the purpose of preparing the financial statements. The reflection of the

performance of the corporate entity is better reflected by the provision of the regulatory

guidelines that has been established by the regulatory bodies in Australia. The Star Entertainment

group has been utilizing the generally accepted accounting principles for the preparation of the

financial statements. The management of the corporate entity has been of the opinion that the

utilization of the accounting regulatory principles as prescribed by the regulatory bodies like the

Australian Accounting Standards Board not only results in the preparation of the accounting

statements that reflect a fair view of the financial position of the company but also help the firm

to acquire the trust of the stakeholders thus increasing the number of potential shareholders of

the firm. This can be further explained with the help of the fact that the preparation of the

accounting statement on the basis of the prescribed accounting framework provides the

stakeholders of the firm with the required level of trust and confidence in the financial position

of the firm as they are aware of the particular guidelines that have been followed in regards to the

preparation of the accounting statements (Baginski caes et al 2016).

Literature Review

GAAP earnings and Non-GAAP earnings

The generally accepted accounting principles effectively reflect standards, regulations

and rules that have been utilized by the standard setters for the purpose of governing the

accounting practices and the preparation of the financial statements. The generally accepted

GAAP standards that is non-regulated and the non-audited standards have been more informative

and reflective in nature (Baginski caes et al 2016).

On the other hand, the firm utilizing the traditional process of accounting that is the

generally accepted accounting principles, have to go through a defined and detailed guideline of

accounting standards for the purpose of preparing the financial statements. The reflection of the

performance of the corporate entity is better reflected by the provision of the regulatory

guidelines that has been established by the regulatory bodies in Australia. The Star Entertainment

group has been utilizing the generally accepted accounting principles for the preparation of the

financial statements. The management of the corporate entity has been of the opinion that the

utilization of the accounting regulatory principles as prescribed by the regulatory bodies like the

Australian Accounting Standards Board not only results in the preparation of the accounting

statements that reflect a fair view of the financial position of the company but also help the firm

to acquire the trust of the stakeholders thus increasing the number of potential shareholders of

the firm. This can be further explained with the help of the fact that the preparation of the

accounting statement on the basis of the prescribed accounting framework provides the

stakeholders of the firm with the required level of trust and confidence in the financial position

of the firm as they are aware of the particular guidelines that have been followed in regards to the

preparation of the accounting statements (Baginski caes et al 2016).

Literature Review

GAAP earnings and Non-GAAP earnings

The generally accepted accounting principles effectively reflect standards, regulations

and rules that have been utilized by the standard setters for the purpose of governing the

accounting practices and the preparation of the financial statements. The generally accepted

5RESEARCH PROJECT

accounting principles can be summarized as a set of accounting regulations that have been

established for the purpose of financial reporting. These principles ensure the fundamental

features of the books of accounts that are transparency, reliability and consistency. It can be

further stated that GAAP imposes a certain degree of uniformity in the financial reporting. The

utilization of the GAAP framework also ensures or facilitates the feature of comparability of the

accounting statements (Bentley caes et al 2016).

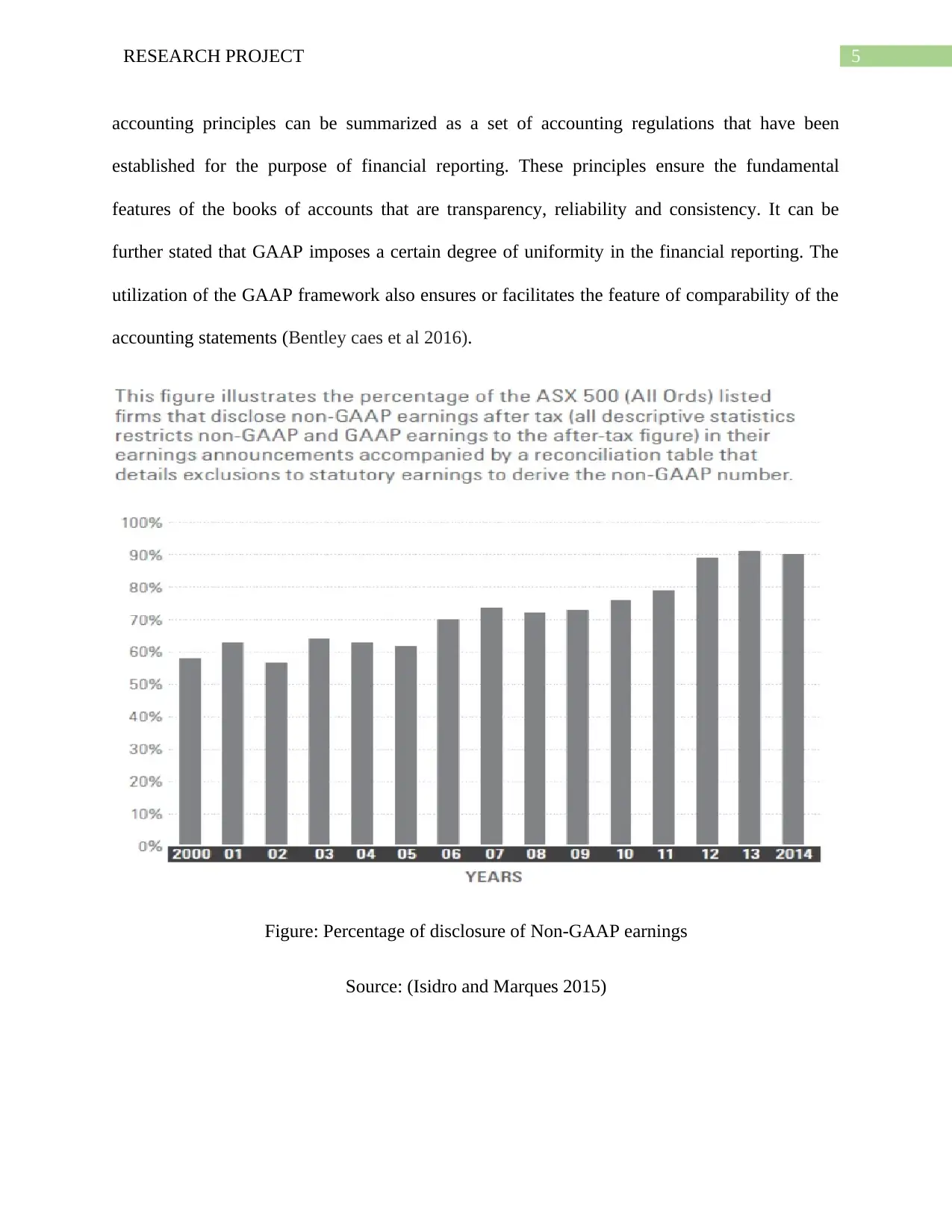

Figure: Percentage of disclosure of Non-GAAP earnings

Source: (Isidro and Marques 2015)

accounting principles can be summarized as a set of accounting regulations that have been

established for the purpose of financial reporting. These principles ensure the fundamental

features of the books of accounts that are transparency, reliability and consistency. It can be

further stated that GAAP imposes a certain degree of uniformity in the financial reporting. The

utilization of the GAAP framework also ensures or facilitates the feature of comparability of the

accounting statements (Bentley caes et al 2016).

Figure: Percentage of disclosure of Non-GAAP earnings

Source: (Isidro and Marques 2015)

6RESEARCH PROJECT

The particular figure that has been demonstrated above show the percentage in regards to

the number of firms that utilize the Non-GAAP earnings method in the preparation of the

financial statements. Furthermore, these are among the top 500 ASX listed firms. It can be

observed that the percentage has declined in 2014.

However, it must be noted here that the particular feature of GAAP imposing a degree of

uniformity over financial reporting has resulted in the negative effect over the corporations

especially with substantial heterogeneity of economic and activities and the essential operations

of business. This is because the earnings that are reported by these corporate entities in regards to

the accounting system might fail to provide a reflection at the right time in regards to the

underlying operating performance of the firm. Therefore, this has been the major reason behind

the firms switching from GAAP to non-GAAP earnings mode (Bentley caes et al 2016).

The other reasons that can be cited behind the prevalence of the Non-GAAP earnings are

that the firms, which are featured with low GAAP earnings, reflect less profit when utilizing the

GAAP earnings method. Moreover, when the GAAP earnings are less relevant in regards to the

value and where there has been a history of prior losses (Christensen caes et al., 2017).

However, this particular trend had been observed by the accounting regulatory bodies and

the required amendments had been carried out by the regulatory bodies in Australia in order to

increase the number of the firms adopting the generally accepted accounting principles or the

particular standards that have been established by the Australian Accounting Standards Board in

the reflection of the same. This can be further evidenced by the fact that particular reporting

standards like the AASB 1018. Moreover, the particular announcement that the all publicly listed

Australian companies will be mandatorily required to adopt the Australian standards equivalent

to the International Financial Reporting Standards (Christensen caes et al., 2017).

The particular figure that has been demonstrated above show the percentage in regards to

the number of firms that utilize the Non-GAAP earnings method in the preparation of the

financial statements. Furthermore, these are among the top 500 ASX listed firms. It can be

observed that the percentage has declined in 2014.

However, it must be noted here that the particular feature of GAAP imposing a degree of

uniformity over financial reporting has resulted in the negative effect over the corporations

especially with substantial heterogeneity of economic and activities and the essential operations

of business. This is because the earnings that are reported by these corporate entities in regards to

the accounting system might fail to provide a reflection at the right time in regards to the

underlying operating performance of the firm. Therefore, this has been the major reason behind

the firms switching from GAAP to non-GAAP earnings mode (Bentley caes et al 2016).

The other reasons that can be cited behind the prevalence of the Non-GAAP earnings are

that the firms, which are featured with low GAAP earnings, reflect less profit when utilizing the

GAAP earnings method. Moreover, when the GAAP earnings are less relevant in regards to the

value and where there has been a history of prior losses (Christensen caes et al., 2017).

However, this particular trend had been observed by the accounting regulatory bodies and

the required amendments had been carried out by the regulatory bodies in Australia in order to

increase the number of the firms adopting the generally accepted accounting principles or the

particular standards that have been established by the Australian Accounting Standards Board in

the reflection of the same. This can be further evidenced by the fact that particular reporting

standards like the AASB 1018. Moreover, the particular announcement that the all publicly listed

Australian companies will be mandatorily required to adopt the Australian standards equivalent

to the International Financial Reporting Standards (Christensen caes et al., 2017).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7RESEARCH PROJECT

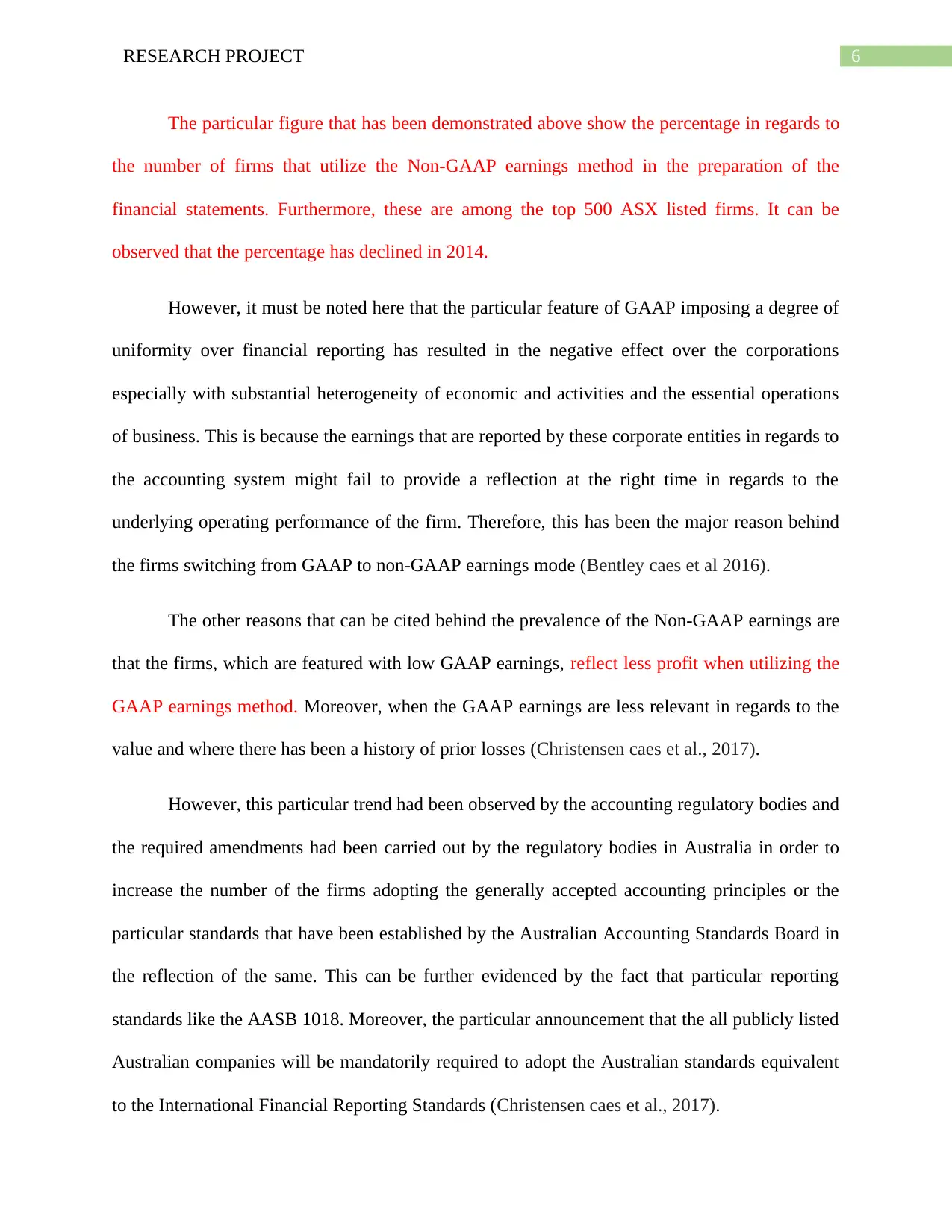

Figure: Frequency of Non-GAAP Disclosures

Source: (Isidro and Marques 2015)

The above graph depicts the firms providing proper disclosures for utilizing the Non-

GAAP disclosure method. It must be noted here that the companies have been categorized on the

basis of their industries.

In contrast to the GAAP reporting, the non-GAAP disclosures in the country of Australia

have been largely unregulated in nature. A major reason behind this has been that the accounting

standards and the Corporations Act do not necessarily restrict the presentation of the non-GAAP

disclosures in the financial report of the organizations (Parrino 2016).

The feature of no restriction is a potential loophole that is utilized by firms for the

purpose of preparing the financial report on the basis of Non-GAAP earning method. The

regulators like the ASIC has mandated the adoption of the GAAP regulatory standards for the

purpose of the preparation of the accounting statements.

Figure: Frequency of Non-GAAP Disclosures

Source: (Isidro and Marques 2015)

The above graph depicts the firms providing proper disclosures for utilizing the Non-

GAAP disclosure method. It must be noted here that the companies have been categorized on the

basis of their industries.

In contrast to the GAAP reporting, the non-GAAP disclosures in the country of Australia

have been largely unregulated in nature. A major reason behind this has been that the accounting

standards and the Corporations Act do not necessarily restrict the presentation of the non-GAAP

disclosures in the financial report of the organizations (Parrino 2016).

The feature of no restriction is a potential loophole that is utilized by firms for the

purpose of preparing the financial report on the basis of Non-GAAP earning method. The

regulators like the ASIC has mandated the adoption of the GAAP regulatory standards for the

purpose of the preparation of the accounting statements.

8RESEARCH PROJECT

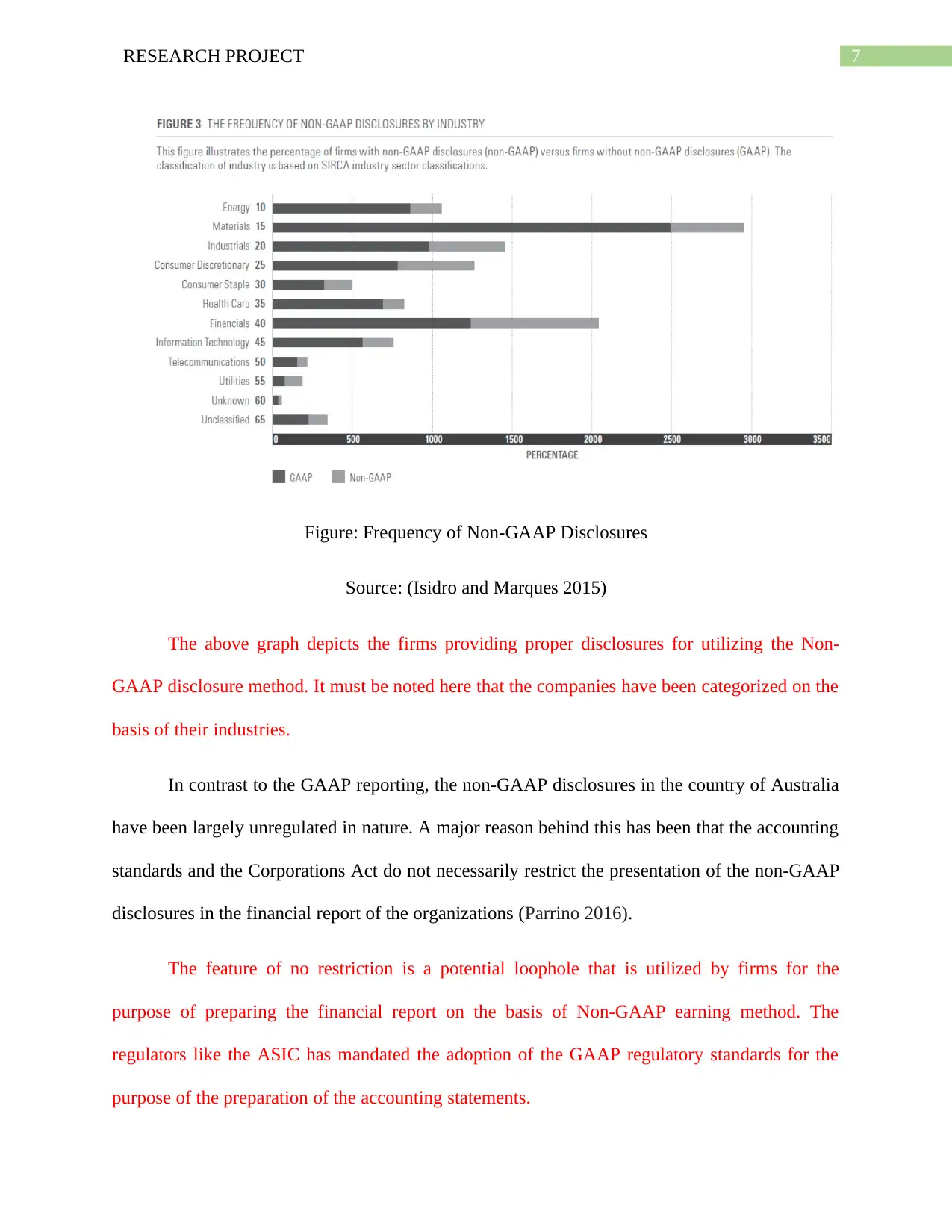

Figure: the absolute value of Non-GAAP exclusions in relation to the equivalent GAAP earnings

result

Source: (Isidro and Marques 2015)

The above figure shows the mean and the median in regards to the GAAP and Non-

GAAP earnings. Moreover, potential concerns were raised in regards to the Non-GAAP

reporting when the particular scandal in relation to the corporate entities of Enron and

WorldCom scandals came into the light. Therefore, it can be evidently concluded that the

preparation of the financial statements on the basis of GAAP reporting is expected to be carried

out by the financial entities (Parrino 2016).

It can also be stated that the importance of accounting disclosures that form an essential

part of the GAAP regulations play a major role in helping the stakeholders and the third party

investors to take the important economic decisions. This is because the accounting disclosures

facilitate the true and fair view of the financial report of the corporate entity. This is not

guaranteed by the non-GAAP earnings regulatory method.

Figure: the absolute value of Non-GAAP exclusions in relation to the equivalent GAAP earnings

result

Source: (Isidro and Marques 2015)

The above figure shows the mean and the median in regards to the GAAP and Non-

GAAP earnings. Moreover, potential concerns were raised in regards to the Non-GAAP

reporting when the particular scandal in relation to the corporate entities of Enron and

WorldCom scandals came into the light. Therefore, it can be evidently concluded that the

preparation of the financial statements on the basis of GAAP reporting is expected to be carried

out by the financial entities (Parrino 2016).

It can also be stated that the importance of accounting disclosures that form an essential

part of the GAAP regulations play a major role in helping the stakeholders and the third party

investors to take the important economic decisions. This is because the accounting disclosures

facilitate the true and fair view of the financial report of the corporate entity. This is not

guaranteed by the non-GAAP earnings regulatory method.

9RESEARCH PROJECT

Methodology

This research study has been based upon secondary information that has been collected

from different financial documents and academic journals. Therefore, the particular method that

has been utilized for the purpose of conducting the required research in this particular study is

that a number of academic journal articles have been referred to and other related financial or

documents related to accounting have been considered. It must be noted here that the nature of

the data that has been collected for this particular study is secondary in nature. This means that

the information has not been derived from primary sources therefore, may suffer due to certain

limitations. The particular limitations that this particular study is exposed to is that as

information has not been collected from the primary sources the data is vulnerable to biasness,

objectivity and error on the part of the researcher who has prepared the particular academic

journal.

The method that has been applied to study the effect of the GAAP and Non GAAP

earning announcement on the share price of the selected companies are the event study method.

The statistical methodology and process are applied for performing event study analysis. The

most common model that is used for the event study is the market model. In this method, the

actual return of the baseline reference and the stock is compared to understand the effect of the

event. The event study aims to measure the effect on valuation because of corporate

announcement. It is a process of measuring the response of the share price movement in case of a

merger or earning announcement. The main assumption of this theory is that the market process

the information in an efficient and unbiased manner. This helps in analyzing the effect of event

in the share price of the company.

Methodology

This research study has been based upon secondary information that has been collected

from different financial documents and academic journals. Therefore, the particular method that

has been utilized for the purpose of conducting the required research in this particular study is

that a number of academic journal articles have been referred to and other related financial or

documents related to accounting have been considered. It must be noted here that the nature of

the data that has been collected for this particular study is secondary in nature. This means that

the information has not been derived from primary sources therefore, may suffer due to certain

limitations. The particular limitations that this particular study is exposed to is that as

information has not been collected from the primary sources the data is vulnerable to biasness,

objectivity and error on the part of the researcher who has prepared the particular academic

journal.

The method that has been applied to study the effect of the GAAP and Non GAAP

earning announcement on the share price of the selected companies are the event study method.

The statistical methodology and process are applied for performing event study analysis. The

most common model that is used for the event study is the market model. In this method, the

actual return of the baseline reference and the stock is compared to understand the effect of the

event. The event study aims to measure the effect on valuation because of corporate

announcement. It is a process of measuring the response of the share price movement in case of a

merger or earning announcement. The main assumption of this theory is that the market process

the information in an efficient and unbiased manner. This helps in analyzing the effect of event

in the share price of the company.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10RESEARCH PROJECT

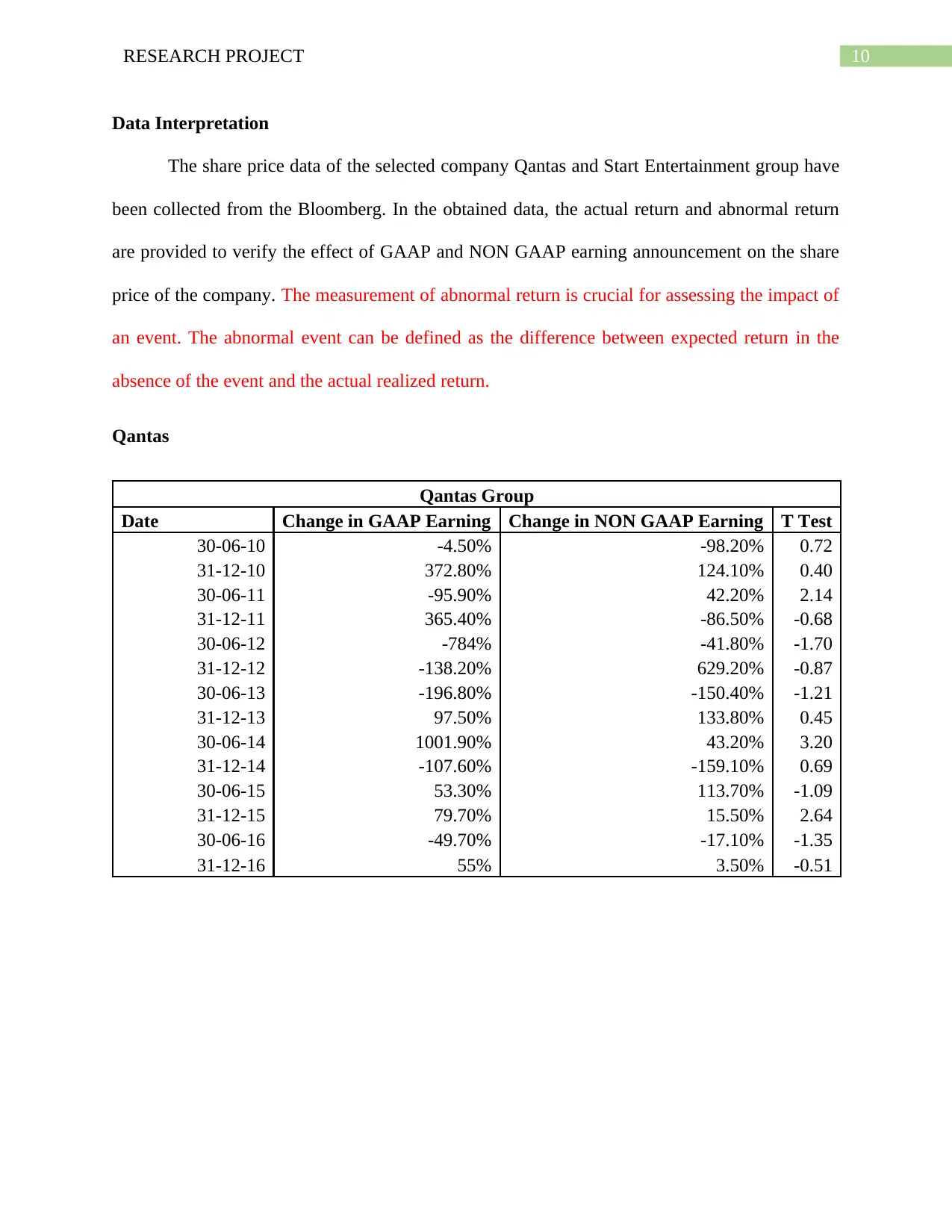

Data Interpretation

The share price data of the selected company Qantas and Start Entertainment group have

been collected from the Bloomberg. In the obtained data, the actual return and abnormal return

are provided to verify the effect of GAAP and NON GAAP earning announcement on the share

price of the company. The measurement of abnormal return is crucial for assessing the impact of

an event. The abnormal event can be defined as the difference between expected return in the

absence of the event and the actual realized return.

Qantas

Qantas Group

Date Change in GAAP Earning Change in NON GAAP Earning T Test

30-06-10 -4.50% -98.20% 0.72

31-12-10 372.80% 124.10% 0.40

30-06-11 -95.90% 42.20% 2.14

31-12-11 365.40% -86.50% -0.68

30-06-12 -784% -41.80% -1.70

31-12-12 -138.20% 629.20% -0.87

30-06-13 -196.80% -150.40% -1.21

31-12-13 97.50% 133.80% 0.45

30-06-14 1001.90% 43.20% 3.20

31-12-14 -107.60% -159.10% 0.69

30-06-15 53.30% 113.70% -1.09

31-12-15 79.70% 15.50% 2.64

30-06-16 -49.70% -17.10% -1.35

31-12-16 55% 3.50% -0.51

Data Interpretation

The share price data of the selected company Qantas and Start Entertainment group have

been collected from the Bloomberg. In the obtained data, the actual return and abnormal return

are provided to verify the effect of GAAP and NON GAAP earning announcement on the share

price of the company. The measurement of abnormal return is crucial for assessing the impact of

an event. The abnormal event can be defined as the difference between expected return in the

absence of the event and the actual realized return.

Qantas

Qantas Group

Date Change in GAAP Earning Change in NON GAAP Earning T Test

30-06-10 -4.50% -98.20% 0.72

31-12-10 372.80% 124.10% 0.40

30-06-11 -95.90% 42.20% 2.14

31-12-11 365.40% -86.50% -0.68

30-06-12 -784% -41.80% -1.70

31-12-12 -138.20% 629.20% -0.87

30-06-13 -196.80% -150.40% -1.21

31-12-13 97.50% 133.80% 0.45

30-06-14 1001.90% 43.20% 3.20

31-12-14 -107.60% -159.10% 0.69

30-06-15 53.30% 113.70% -1.09

31-12-15 79.70% 15.50% 2.64

30-06-16 -49.70% -17.10% -1.35

31-12-16 55% 3.50% -0.51

11RESEARCH PROJECT

7/6/2009 11/18/2010 4/1/2012 8/14/2013 12/27/2014 5/10/2016 9/22/2017

-1000.00%

-500.00%

0.00%

500.00%

1000.00%

1500.00%

Qantas Group

Change in GAAP Earning Change in NON GAAP Earning T Test

The table and the figure above indicates the relationship between the announcement and

the movement in the return of the share price from the expected return. It can be clearly seen

from T test that the market reacts more to the results of the GAAP earning than the NON GAAP

earnings. Therefore, in case of Qantas share price reacts to the GAAP earnings more than the

NON GAAP earnings.

Star Entertainment Group

Star entertainment Group

7/6/2009 11/18/2010 4/1/2012 8/14/2013 12/27/2014 5/10/2016 9/22/2017

-1000.00%

-500.00%

0.00%

500.00%

1000.00%

1500.00%

Qantas Group

Change in GAAP Earning Change in NON GAAP Earning T Test

The table and the figure above indicates the relationship between the announcement and

the movement in the return of the share price from the expected return. It can be clearly seen

from T test that the market reacts more to the results of the GAAP earning than the NON GAAP

earnings. Therefore, in case of Qantas share price reacts to the GAAP earnings more than the

NON GAAP earnings.

Star Entertainment Group

Star entertainment Group

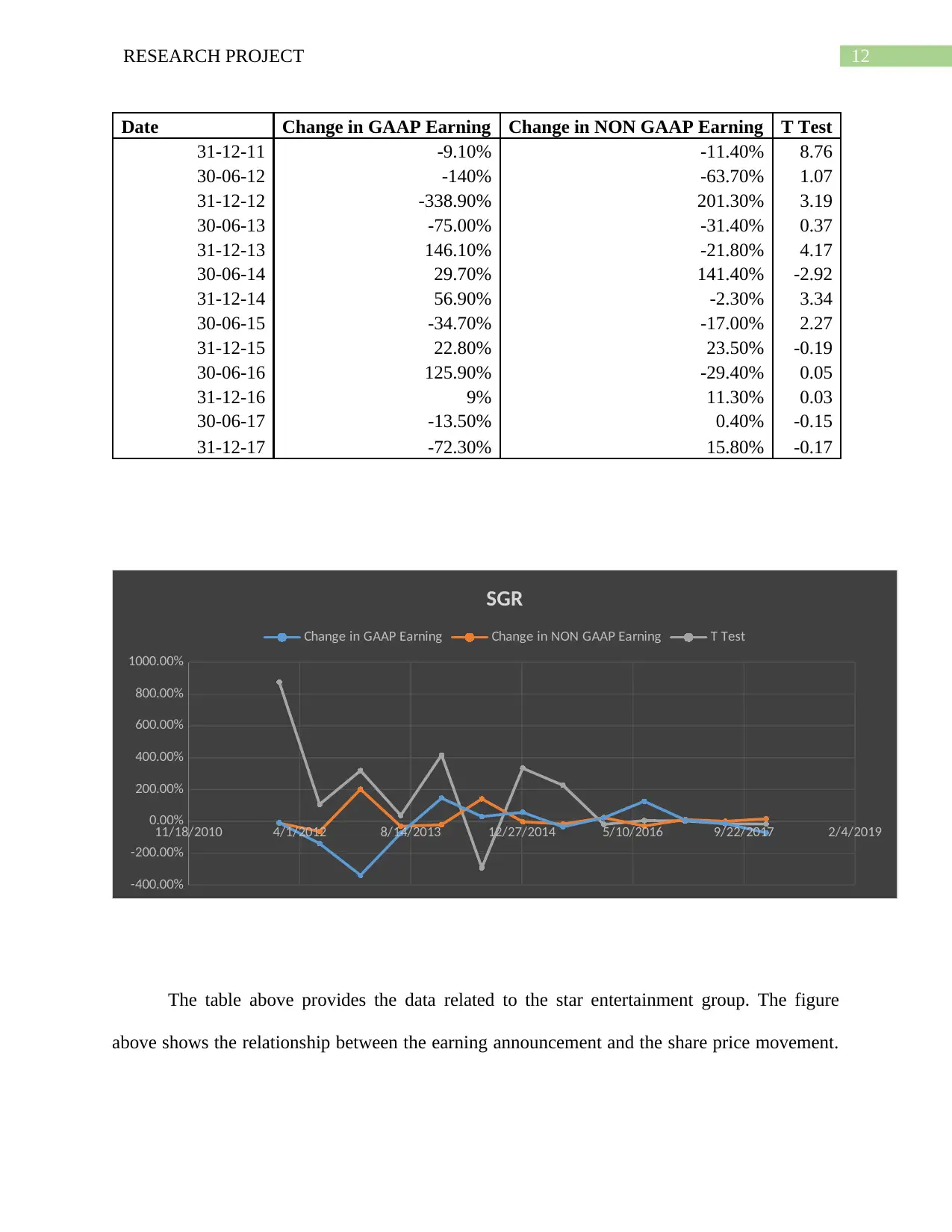

12RESEARCH PROJECT

Date Change in GAAP Earning Change in NON GAAP Earning T Test

31-12-11 -9.10% -11.40% 8.76

30-06-12 -140% -63.70% 1.07

31-12-12 -338.90% 201.30% 3.19

30-06-13 -75.00% -31.40% 0.37

31-12-13 146.10% -21.80% 4.17

30-06-14 29.70% 141.40% -2.92

31-12-14 56.90% -2.30% 3.34

30-06-15 -34.70% -17.00% 2.27

31-12-15 22.80% 23.50% -0.19

30-06-16 125.90% -29.40% 0.05

31-12-16 9% 11.30% 0.03

30-06-17 -13.50% 0.40% -0.15

31-12-17 -72.30% 15.80% -0.17

11/18/2010 4/1/2012 8/14/2013 12/27/2014 5/10/2016 9/22/2017 2/4/2019

-400.00%

-200.00%

0.00%

200.00%

400.00%

600.00%

800.00%

1000.00%

SGR

Change in GAAP Earning Change in NON GAAP Earning T Test

The table above provides the data related to the star entertainment group. The figure

above shows the relationship between the earning announcement and the share price movement.

Date Change in GAAP Earning Change in NON GAAP Earning T Test

31-12-11 -9.10% -11.40% 8.76

30-06-12 -140% -63.70% 1.07

31-12-12 -338.90% 201.30% 3.19

30-06-13 -75.00% -31.40% 0.37

31-12-13 146.10% -21.80% 4.17

30-06-14 29.70% 141.40% -2.92

31-12-14 56.90% -2.30% 3.34

30-06-15 -34.70% -17.00% 2.27

31-12-15 22.80% 23.50% -0.19

30-06-16 125.90% -29.40% 0.05

31-12-16 9% 11.30% 0.03

30-06-17 -13.50% 0.40% -0.15

31-12-17 -72.30% 15.80% -0.17

11/18/2010 4/1/2012 8/14/2013 12/27/2014 5/10/2016 9/22/2017 2/4/2019

-400.00%

-200.00%

0.00%

200.00%

400.00%

600.00%

800.00%

1000.00%

SGR

Change in GAAP Earning Change in NON GAAP Earning T Test

The table above provides the data related to the star entertainment group. The figure

above shows the relationship between the earning announcement and the share price movement.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

13RESEARCH PROJECT

The figure above clearly shows that in case of star entertainment group the share price is more

effected with the NON GAAP earning announcement.

Conclusion

The particular conclusion that can be derived from the information that has been derived

from the preceding paragraphs is that though non-GAAP reporting looks lucrative and is favored

by the executives , the prevalence of GAAP reporting is accepted and honored by the majority of

the corporate entities in Australia. However, the analysis above shows that investor in case of

Qantas Group is more reactive to the GAAP earning announcement where as in case of SGR the

investors reacts more to NON GAAP earning announcements.

The figure above clearly shows that in case of star entertainment group the share price is more

effected with the NON GAAP earning announcement.

Conclusion

The particular conclusion that can be derived from the information that has been derived

from the preceding paragraphs is that though non-GAAP reporting looks lucrative and is favored

by the executives , the prevalence of GAAP reporting is accepted and honored by the majority of

the corporate entities in Australia. However, the analysis above shows that investor in case of

Qantas Group is more reactive to the GAAP earning announcement where as in case of SGR the

investors reacts more to NON GAAP earning announcements.

14RESEARCH PROJECT

References

Baginski, S., Demers, E., Wang, C., Yu, J., Jiang, D., Kumar, A. and Law, K.K., 2016. Using

adverse-selection cost as a proxy for information asymmetry, we find evidence that non-GAAP

earnings numbers issued by management (pro forma earnings) and analysts (street earnings)

improve price discovery. First, information asymmetry before an earnings announcement is

positively associated with the probability of a non-GAAP earnings number at the forthcoming

earnings announcement. Second,... Review of Accounting Studies, 21(1), pp.198-250.

Bentley, J.W., Christensen, T.E., Gee, K.H. and Whipple, B.C., 2016. Disentangling managers’

and analysts’ non-GAAP reporting incentives.

Bhattacharya, N., Christensen, T., Liao, Q. and Ouyang, B., 2015. Can Short Sellers Constrain

Opportunistic Non-GAAP Earnings Reporting?.

Black, E.L., Christensen, T.E., Kiosse, P.V. and Steffen, T.D., 2017. Has the Regulation of Non-

GAAP Disclosures Influenced Managers’ Use of Aggressive Earnings Exclusions?. Journal of

Accounting, Auditing & Finance, 32(2), pp.209-240.

Black, E.L., Christensen, T.E., Taylor Joo, T. and Schmardebeck, R., 2017. The Relation

Between Earnings Management and Non‐GAAP Reporting. Contemporary Accounting

Research, 34(2), pp.750-782.

Christensen, T., Pei, H., Pierce, S. and Tan, L., 2017. Non-GAAP reporting following debt

covenant violations.

Guest, N.M., Kothari, S.P. and Pozen, R., 2017. High Non-GAAP Earnings Predict Abnormally

High CEO Pay.

References

Baginski, S., Demers, E., Wang, C., Yu, J., Jiang, D., Kumar, A. and Law, K.K., 2016. Using

adverse-selection cost as a proxy for information asymmetry, we find evidence that non-GAAP

earnings numbers issued by management (pro forma earnings) and analysts (street earnings)

improve price discovery. First, information asymmetry before an earnings announcement is

positively associated with the probability of a non-GAAP earnings number at the forthcoming

earnings announcement. Second,... Review of Accounting Studies, 21(1), pp.198-250.

Bentley, J.W., Christensen, T.E., Gee, K.H. and Whipple, B.C., 2016. Disentangling managers’

and analysts’ non-GAAP reporting incentives.

Bhattacharya, N., Christensen, T., Liao, Q. and Ouyang, B., 2015. Can Short Sellers Constrain

Opportunistic Non-GAAP Earnings Reporting?.

Black, E.L., Christensen, T.E., Kiosse, P.V. and Steffen, T.D., 2017. Has the Regulation of Non-

GAAP Disclosures Influenced Managers’ Use of Aggressive Earnings Exclusions?. Journal of

Accounting, Auditing & Finance, 32(2), pp.209-240.

Black, E.L., Christensen, T.E., Taylor Joo, T. and Schmardebeck, R., 2017. The Relation

Between Earnings Management and Non‐GAAP Reporting. Contemporary Accounting

Research, 34(2), pp.750-782.

Christensen, T., Pei, H., Pierce, S. and Tan, L., 2017. Non-GAAP reporting following debt

covenant violations.

Guest, N.M., Kothari, S.P. and Pozen, R., 2017. High Non-GAAP Earnings Predict Abnormally

High CEO Pay.

15RESEARCH PROJECT

Isidro, H. and Marques, A., 2015. The role of institutional and economic factors in the strategic

use of non-GAAP disclosures to beat earnings benchmarks. European Accounting Review, 24(1),

pp.95-128.

Parrino, R.J., 2016. New compliance guidance by SEC staff signals increased scrutiny of non-

GAAP financial measures. Journal of Investment Compliance, 17(4), pp.23-33.

Twardus, I. and Bhattacharjee, S., 2018. Effect of Non-Gaap Emphasis and Voluntary

Disclosures on Nonprofessional Investor Decision Making in the Equity Crowdfunding

Environment

Isidro, H. and Marques, A., 2015. The role of institutional and economic factors in the strategic

use of non-GAAP disclosures to beat earnings benchmarks. European Accounting Review, 24(1),

pp.95-128.

Parrino, R.J., 2016. New compliance guidance by SEC staff signals increased scrutiny of non-

GAAP financial measures. Journal of Investment Compliance, 17(4), pp.23-33.

Twardus, I. and Bhattacharjee, S., 2018. Effect of Non-Gaap Emphasis and Voluntary

Disclosures on Nonprofessional Investor Decision Making in the Equity Crowdfunding

Environment

1 out of 16

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.