HI5020 Corporate Accounting: Financial Analysis of Galaxy Resources

VerifiedAdded on 2023/06/12

|13

|3516

|61

Report

AI Summary

This report provides a financial analysis of Galaxy Resources Limited, an ASX-listed company, focusing on its cash flow statement, other comprehensive income statement, and accounting for corporate income tax. The cash flow statement is analyzed by discussing each item reported and comparing the cash flow from operating, investing, and financing activities between 2016 and 2017. The report also explains the main items in the other comprehensive income statement, detailing why these items are reported in OCI rather than the profit and loss account. Furthermore, it examines the company's income tax expense, compares it with the tax rate, and discusses the reasons for deferred tax assets/liabilities. The analysis aims to enhance understanding of annual reports and their impact on investment decisions, with reference to IFRS standards and relevant accounting principles. Desklib offers more solved assignments for students.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

By student name

Professor

University

Date: 25 April 2018.

1 | P a g e

By student name

Professor

University

Date: 25 April 2018.

1 | P a g e

2

Executive Summary

In the given assignment a financial analysis has been done of the listed companies on the

Australian Stock Exchange. The company is a awidely known one and the financial statements

including the profit and loss account, the balance sheet, statement of changes in equity and the

cash flow statement has been analysed and discussed with regards to several aspects. Each item

of the cash flow statement has been discussed and the comparative analysis of the three major

categories has also been included. Similarly, each of the line items reported in the comprehensive

income statement has been analysed and reasons have been enlisted as to why they form a part o

the income statement. Finally, an in depth analysis of the income tax expense booked and paid

by the company along with the treatment of deferred income tax asset/liability has also been

articulated in the report. The report is aimed at increasing the level of understanding of the

annual report and how it impacts the decision of investment by the investor.

‘

2 | P a g e

Executive Summary

In the given assignment a financial analysis has been done of the listed companies on the

Australian Stock Exchange. The company is a awidely known one and the financial statements

including the profit and loss account, the balance sheet, statement of changes in equity and the

cash flow statement has been analysed and discussed with regards to several aspects. Each item

of the cash flow statement has been discussed and the comparative analysis of the three major

categories has also been included. Similarly, each of the line items reported in the comprehensive

income statement has been analysed and reasons have been enlisted as to why they form a part o

the income statement. Finally, an in depth analysis of the income tax expense booked and paid

by the company along with the treatment of deferred income tax asset/liability has also been

articulated in the report. The report is aimed at increasing the level of understanding of the

annual report and how it impacts the decision of investment by the investor.

‘

2 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

Contents

Cash Flow Statement...................................................................................................................................4

Reporting of each of the items of the cash flow statement.....................................................................4

Comparative analysis of the cash flow statement of Galaxy Resources Limited.....................................5

Other comprehensive income statement of the company..........................................................................7

Main items reported in Other comprehensive income statement..........................................................7

Understanding of each item reported in the above statement...............................................................7

Why these items reported in OCI and not Profit and loss account..........................................................8

Accounting for Corporate Income tax.........................................................................................................8

Income tax expense in the financial statements.....................................................................................8

Comparison with the tax rate..................................................................................................................9

Reason for deferred tax asset / liability in the balance sheet..................................................................9

Current tax assets or income tax payable recorded by company..........................................................10

Income Tax: Income statement vs Cash Flow statement.......................................................................10

Interesting, confusing, surprising or difficult aspects of Income tax treatment....................................11

References.................................................................................................................................................12

3 | P a g e

Contents

Cash Flow Statement...................................................................................................................................4

Reporting of each of the items of the cash flow statement.....................................................................4

Comparative analysis of the cash flow statement of Galaxy Resources Limited.....................................5

Other comprehensive income statement of the company..........................................................................7

Main items reported in Other comprehensive income statement..........................................................7

Understanding of each item reported in the above statement...............................................................7

Why these items reported in OCI and not Profit and loss account..........................................................8

Accounting for Corporate Income tax.........................................................................................................8

Income tax expense in the financial statements.....................................................................................8

Comparison with the tax rate..................................................................................................................9

Reason for deferred tax asset / liability in the balance sheet..................................................................9

Current tax assets or income tax payable recorded by company..........................................................10

Income Tax: Income statement vs Cash Flow statement.......................................................................10

Interesting, confusing, surprising or difficult aspects of Income tax treatment....................................11

References.................................................................................................................................................12

3 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

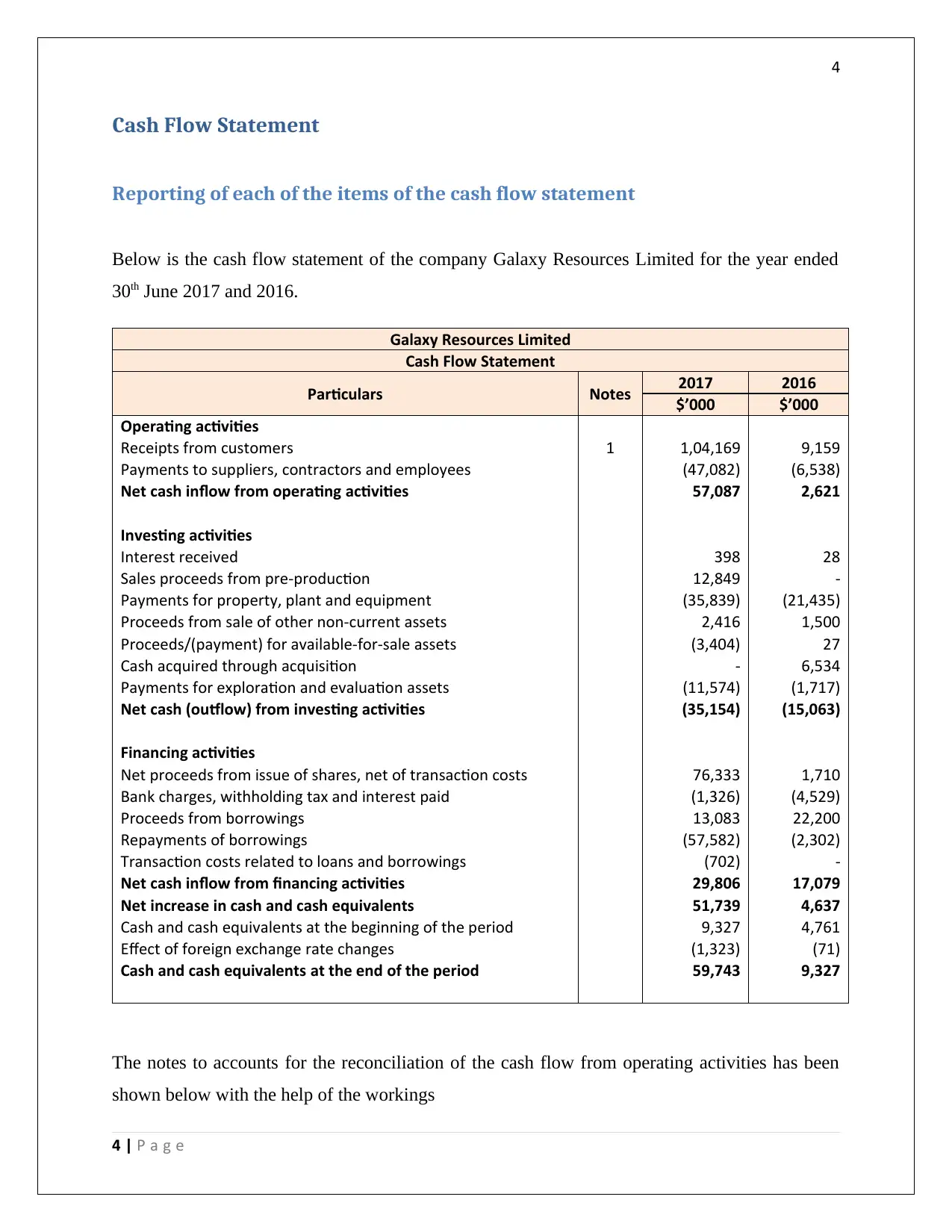

Cash Flow Statement

Reporting of each of the items of the cash flow statement

Below is the cash flow statement of the company Galaxy Resources Limited for the year ended

30th June 2017 and 2016.

Galaxy Resources Limited

Cash Flow Statement

Particulars Notes 2017 2016

$’000 $’000

Operating activities

Receipts from customers 1 1,04,169 9,159

Payments to suppliers, contractors and employees (47,082) (6,538)

Net cash inflow from operating activities 57,087 2,621

Investing activities

Interest received 398 28

Sales proceeds from pre-production 12,849 -

Payments for property, plant and equipment (35,839) (21,435)

Proceeds from sale of other non-current assets 2,416 1,500

Proceeds/(payment) for available-for-sale assets (3,404) 27

Cash acquired through acquisition - 6,534

Payments for exploration and evaluation assets (11,574) (1,717)

Net cash (outflow) from investing activities (35,154) (15,063)

Financing activities

Net proceeds from issue of shares, net of transaction costs 76,333 1,710

Bank charges, withholding tax and interest paid (1,326) (4,529)

Proceeds from borrowings 13,083 22,200

Repayments of borrowings (57,582) (2,302)

Transaction costs related to loans and borrowings (702) -

Net cash inflow from financing activities 29,806 17,079

Net increase in cash and cash equivalents 51,739 4,637

Cash and cash equivalents at the beginning of the period 9,327 4,761

Effect of foreign exchange rate changes (1,323) (71)

Cash and cash equivalents at the end of the period 59,743 9,327

The notes to accounts for the reconciliation of the cash flow from operating activities has been

shown below with the help of the workings

4 | P a g e

Cash Flow Statement

Reporting of each of the items of the cash flow statement

Below is the cash flow statement of the company Galaxy Resources Limited for the year ended

30th June 2017 and 2016.

Galaxy Resources Limited

Cash Flow Statement

Particulars Notes 2017 2016

$’000 $’000

Operating activities

Receipts from customers 1 1,04,169 9,159

Payments to suppliers, contractors and employees (47,082) (6,538)

Net cash inflow from operating activities 57,087 2,621

Investing activities

Interest received 398 28

Sales proceeds from pre-production 12,849 -

Payments for property, plant and equipment (35,839) (21,435)

Proceeds from sale of other non-current assets 2,416 1,500

Proceeds/(payment) for available-for-sale assets (3,404) 27

Cash acquired through acquisition - 6,534

Payments for exploration and evaluation assets (11,574) (1,717)

Net cash (outflow) from investing activities (35,154) (15,063)

Financing activities

Net proceeds from issue of shares, net of transaction costs 76,333 1,710

Bank charges, withholding tax and interest paid (1,326) (4,529)

Proceeds from borrowings 13,083 22,200

Repayments of borrowings (57,582) (2,302)

Transaction costs related to loans and borrowings (702) -

Net cash inflow from financing activities 29,806 17,079

Net increase in cash and cash equivalents 51,739 4,637

Cash and cash equivalents at the beginning of the period 9,327 4,761

Effect of foreign exchange rate changes (1,323) (71)

Cash and cash equivalents at the end of the period 59,743 9,327

The notes to accounts for the reconciliation of the cash flow from operating activities has been

shown below with the help of the workings

4 | P a g e

5

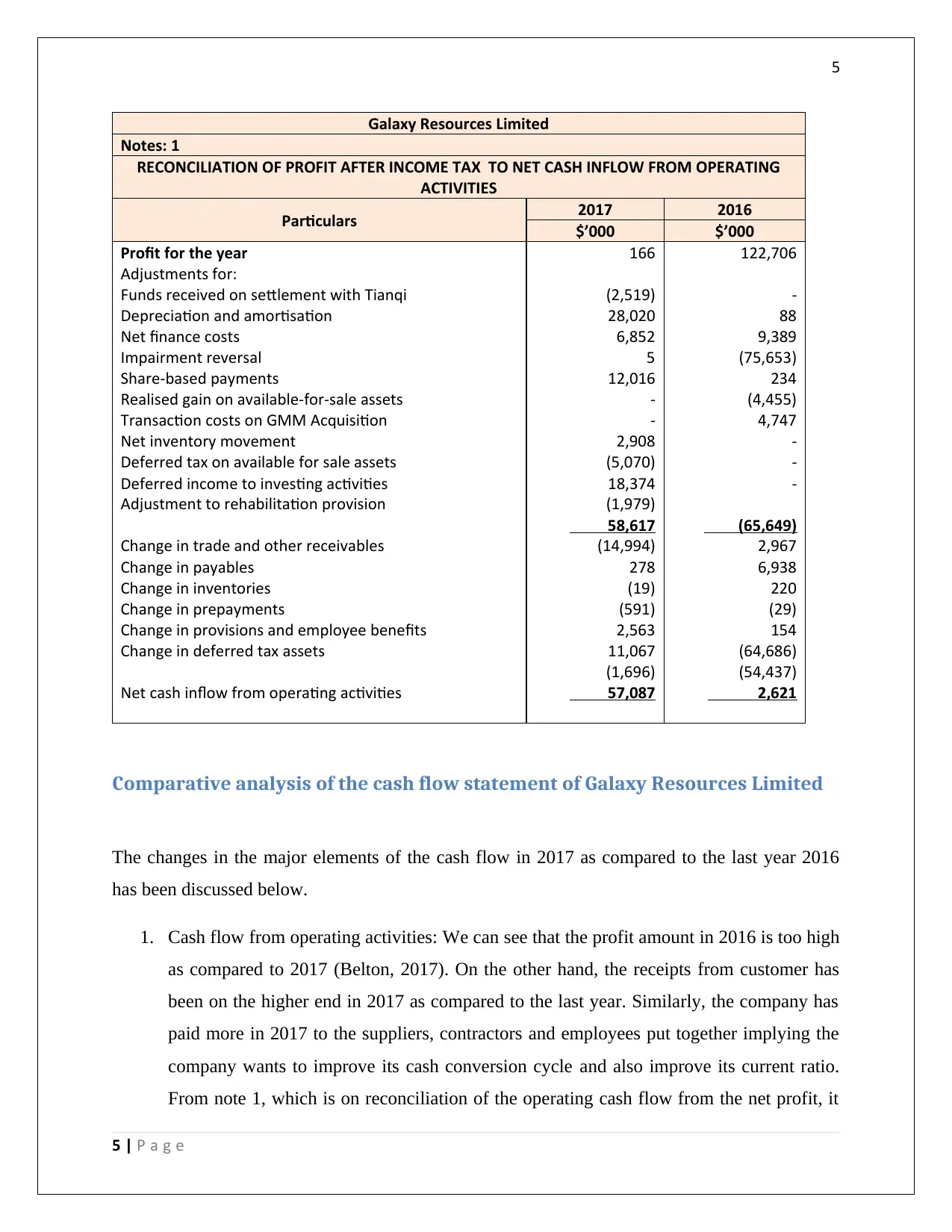

Galaxy Resources Limited

Notes: 1

RECONCILIATION OF PROFIT AFTER INCOME TAX TO NET CASH INFLOW FROM OPERATING

ACTIVITIES

Particulars 2017 2016

$’000 $’000

Profit for the year 166 122,706

Adjustments for:

Funds received on settlement with Tianqi (2,519) -

Depreciation and amortisation 28,020 88

Net finance costs 6,852 9,389

Impairment reversal 5 (75,653)

Share-based payments 12,016 234

Realised gain on available-for-sale assets - (4,455)

Transaction costs on GMM Acquisition - 4,747

Net inventory movement 2,908 -

Deferred tax on available for sale assets (5,070) -

Deferred income to investing activities 18,374 -

Adjustment to rehabilitation provision (1,979)

58,617 (65,649)

Change in trade and other receivables (14,994) 2,967

Change in payables 278 6,938

Change in inventories (19) 220

Change in prepayments (591) (29)

Change in provisions and employee benefits 2,563 154

Change in deferred tax assets 11,067 (64,686)

(1,696) (54,437)

Net cash inflow from operating activities 57,087 2,621

Comparative analysis of the cash flow statement of Galaxy Resources Limited

The changes in the major elements of the cash flow in 2017 as compared to the last year 2016

has been discussed below.

1. Cash flow from operating activities: We can see that the profit amount in 2016 is too high

as compared to 2017 (Belton, 2017). On the other hand, the receipts from customer has

been on the higher end in 2017 as compared to the last year. Similarly, the company has

paid more in 2017 to the suppliers, contractors and employees put together implying the

company wants to improve its cash conversion cycle and also improve its current ratio.

From note 1, which is on reconciliation of the operating cash flow from the net profit, it

5 | P a g e

Galaxy Resources Limited

Notes: 1

RECONCILIATION OF PROFIT AFTER INCOME TAX TO NET CASH INFLOW FROM OPERATING

ACTIVITIES

Particulars 2017 2016

$’000 $’000

Profit for the year 166 122,706

Adjustments for:

Funds received on settlement with Tianqi (2,519) -

Depreciation and amortisation 28,020 88

Net finance costs 6,852 9,389

Impairment reversal 5 (75,653)

Share-based payments 12,016 234

Realised gain on available-for-sale assets - (4,455)

Transaction costs on GMM Acquisition - 4,747

Net inventory movement 2,908 -

Deferred tax on available for sale assets (5,070) -

Deferred income to investing activities 18,374 -

Adjustment to rehabilitation provision (1,979)

58,617 (65,649)

Change in trade and other receivables (14,994) 2,967

Change in payables 278 6,938

Change in inventories (19) 220

Change in prepayments (591) (29)

Change in provisions and employee benefits 2,563 154

Change in deferred tax assets 11,067 (64,686)

(1,696) (54,437)

Net cash inflow from operating activities 57,087 2,621

Comparative analysis of the cash flow statement of Galaxy Resources Limited

The changes in the major elements of the cash flow in 2017 as compared to the last year 2016

has been discussed below.

1. Cash flow from operating activities: We can see that the profit amount in 2016 is too high

as compared to 2017 (Belton, 2017). On the other hand, the receipts from customer has

been on the higher end in 2017 as compared to the last year. Similarly, the company has

paid more in 2017 to the suppliers, contractors and employees put together implying the

company wants to improve its cash conversion cycle and also improve its current ratio.

From note 1, which is on reconciliation of the operating cash flow from the net profit, it

5 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

can be seen that there was huge impairment reversal in the last year amounting to nearly

$ 75.6 Mn which was the main reason for increase in profitability. The other non cash

items which have undergone major change is share based payment (increase in 2017),

depreciation and amortization (increase in 2017), Funds received on settlement with

Tianqi (only in 2017), tramsaction cost incurred on GMM acquisition in 2016. Besides all

these transactions, the adjustement has also been made for deferred tax on the sale of the

assets, deferred income on investing activities and adjustment to rehabilitation reserve.

Another reason for the increase in the cash flow from operating activities is the decrease

in trade receivables owing to huge receipts during the year, change in payables,

inventories, pre payments, provision and deferred tax assets (Alexander, 2016).

2. Cash Flow from investing activities: The net cash outflow from the investing activities

increased by more than $ 20 Mn, which was primarily due to increase in the investment

made in property, plant and equipmemt purchased during the year. It increased by around

$ 14 Mn. Furthermore, the payment for the available for sale assets amounted to nearly $

3 Mn. There was also a substantial increase in the payment for exploration and evaluation

of the assets during the year (Bromwich & Scapens, 2016). The other cash flows relating

to the investing activities were sale proceeds from the pre – production assets in 2017. In

the year 2016, there was also cash inflow from the acquisition which was not the case in

2017.

3. Cash Flow from financing activities: In case the financing activities are being analysed,

we can see that the net cash inflow has increased from $ 17 Mn in 2016 to $ 29 Mn in

2017. This is primarily on account of substantial increase in the inflow from the issue of

the shares (Bae, 2017). The company also made a huge repayment of the earlier loan and

also raised less loan in 2017 as compared to what was being raised in 2016. The bank

charges, interest paid and the withholding tax was less than the last year.

Due to the cumulative increase in the net cash inflow for the year 2017 to the tune of $ 51.74 Mn

($ 4.64 Mn in 2016), the end cash balance was $ 59.74 Mn in 2017. All this shows that the

company has had good cash flow during the year which is helping the company to have good

liquidity and hence resulting in strong operational position for the company.

6 | P a g e

can be seen that there was huge impairment reversal in the last year amounting to nearly

$ 75.6 Mn which was the main reason for increase in profitability. The other non cash

items which have undergone major change is share based payment (increase in 2017),

depreciation and amortization (increase in 2017), Funds received on settlement with

Tianqi (only in 2017), tramsaction cost incurred on GMM acquisition in 2016. Besides all

these transactions, the adjustement has also been made for deferred tax on the sale of the

assets, deferred income on investing activities and adjustment to rehabilitation reserve.

Another reason for the increase in the cash flow from operating activities is the decrease

in trade receivables owing to huge receipts during the year, change in payables,

inventories, pre payments, provision and deferred tax assets (Alexander, 2016).

2. Cash Flow from investing activities: The net cash outflow from the investing activities

increased by more than $ 20 Mn, which was primarily due to increase in the investment

made in property, plant and equipmemt purchased during the year. It increased by around

$ 14 Mn. Furthermore, the payment for the available for sale assets amounted to nearly $

3 Mn. There was also a substantial increase in the payment for exploration and evaluation

of the assets during the year (Bromwich & Scapens, 2016). The other cash flows relating

to the investing activities were sale proceeds from the pre – production assets in 2017. In

the year 2016, there was also cash inflow from the acquisition which was not the case in

2017.

3. Cash Flow from financing activities: In case the financing activities are being analysed,

we can see that the net cash inflow has increased from $ 17 Mn in 2016 to $ 29 Mn in

2017. This is primarily on account of substantial increase in the inflow from the issue of

the shares (Bae, 2017). The company also made a huge repayment of the earlier loan and

also raised less loan in 2017 as compared to what was being raised in 2016. The bank

charges, interest paid and the withholding tax was less than the last year.

Due to the cumulative increase in the net cash inflow for the year 2017 to the tune of $ 51.74 Mn

($ 4.64 Mn in 2016), the end cash balance was $ 59.74 Mn in 2017. All this shows that the

company has had good cash flow during the year which is helping the company to have good

liquidity and hence resulting in strong operational position for the company.

6 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

Other comprehensive income statement of the company

Main items reported in Other comprehensive income statement

The main items which have been reported in the other comprehensive statement of the company

are enlisted below:

1. Items which are subsequently being reclassified to the profit and loss account including

foreign exchange translation differences or the reserve – foreign operations

2. Revaluation on the assets – those available for sale

3. Income tax pertaining to the available for sale assets (Choy, 2018)

4. Change in the fair value of any item

5. Retirement benefits

6. Revaluation of the financial instruments

7. Revaluation of the fixed assets

8. Actuarial gain and losses

9. Pension and prior period service cost or credit on account of the same

10. Other non operating incomes and expenses

Understanding of each item reported in the above statement

The statement showing the other comprehensive income gives the overall view of the financial

status of the company besides the profit and loss account and the balance sheet. It includes many

other significant items other than regular sales and cost of goods sold which may have a

significant bearing on the financial status of the company. It also proves to be very critical in

terms of the investment decision making (Werner, 2017). Items which are generally being

reclassified during the year are reported here as this is not part of the normal Profit and loss

account but a continuation of the same. Reporting of these line items in OCI is as per the norms

of the International Financial Reporting Standards (IFRS). All the above mentioned line items

which are being adjusted in the other comprehensive income have been provided by the IFRS.

Reclassification of the change in fair value of any item from other comprehensive income to fair

value through profit and loss account is not as per the directions in IFRS standards. There are 3

7 | P a g e

Other comprehensive income statement of the company

Main items reported in Other comprehensive income statement

The main items which have been reported in the other comprehensive statement of the company

are enlisted below:

1. Items which are subsequently being reclassified to the profit and loss account including

foreign exchange translation differences or the reserve – foreign operations

2. Revaluation on the assets – those available for sale

3. Income tax pertaining to the available for sale assets (Choy, 2018)

4. Change in the fair value of any item

5. Retirement benefits

6. Revaluation of the financial instruments

7. Revaluation of the fixed assets

8. Actuarial gain and losses

9. Pension and prior period service cost or credit on account of the same

10. Other non operating incomes and expenses

Understanding of each item reported in the above statement

The statement showing the other comprehensive income gives the overall view of the financial

status of the company besides the profit and loss account and the balance sheet. It includes many

other significant items other than regular sales and cost of goods sold which may have a

significant bearing on the financial status of the company. It also proves to be very critical in

terms of the investment decision making (Werner, 2017). Items which are generally being

reclassified during the year are reported here as this is not part of the normal Profit and loss

account but a continuation of the same. Reporting of these line items in OCI is as per the norms

of the International Financial Reporting Standards (IFRS). All the above mentioned line items

which are being adjusted in the other comprehensive income have been provided by the IFRS.

Reclassification of the change in fair value of any item from other comprehensive income to fair

value through profit and loss account is not as per the directions in IFRS standards. There are 3

7 | P a g e

8

ways in which the change in fair value can be accounted for in the books which are fair value

change through profit and loss account, fair value change through other comprehensive income

and fair value change adjusted through the amortization method which is generally being done in

the case of financial instruments (Sithole, et al., 2017). Besides this, since all the retirement

benefits like gratuity and pension are being based on the actuarial caclulations, all the gains and

losses on account of the same is being shown through OCI.

Why these items reported in OCI and not Profit and loss account

Other comprehensive income statement mainly includes such items of revenue, incomes, profit

and losses which are being classified under both the IFRS as well as the local Generally

Accepted Accounting Principles. Normal income has a different classification from those

appearing in the OCI that’s why they are being shown exclusively in the Profit and loss account.

The main idea of classifying those items in OCI other than the P&L account is that these

incomes and expenses, profits and losses have not been realised as of now or it has been

partically recognised and booked (Dichev, 2017). For example, in case the company purchases

the bonds and the market value of the bonds increase, then the differential gain is recognised in

the OCI. Once these bonds are bineg sold in the future and the final gain or loss on account of

the same has been actually realized, then the same can be shifted to income statement from the

OCI as the same is a part of the other income. This treatment of the real income in in line with

the IFRS standards.

Accounting for Corporate Income tax

Income tax expense in the financial statements

The income tax expense for the company Galaxy Resources Limited as per the latest financial

statements is $ 5999000. Furthermore, the income tax on account of revaluation of the available

for sale assets amounts to $ 5070000 (Knechel & Salterio, 2016).

8 | P a g e

ways in which the change in fair value can be accounted for in the books which are fair value

change through profit and loss account, fair value change through other comprehensive income

and fair value change adjusted through the amortization method which is generally being done in

the case of financial instruments (Sithole, et al., 2017). Besides this, since all the retirement

benefits like gratuity and pension are being based on the actuarial caclulations, all the gains and

losses on account of the same is being shown through OCI.

Why these items reported in OCI and not Profit and loss account

Other comprehensive income statement mainly includes such items of revenue, incomes, profit

and losses which are being classified under both the IFRS as well as the local Generally

Accepted Accounting Principles. Normal income has a different classification from those

appearing in the OCI that’s why they are being shown exclusively in the Profit and loss account.

The main idea of classifying those items in OCI other than the P&L account is that these

incomes and expenses, profits and losses have not been realised as of now or it has been

partically recognised and booked (Dichev, 2017). For example, in case the company purchases

the bonds and the market value of the bonds increase, then the differential gain is recognised in

the OCI. Once these bonds are bineg sold in the future and the final gain or loss on account of

the same has been actually realized, then the same can be shifted to income statement from the

OCI as the same is a part of the other income. This treatment of the real income in in line with

the IFRS standards.

Accounting for Corporate Income tax

Income tax expense in the financial statements

The income tax expense for the company Galaxy Resources Limited as per the latest financial

statements is $ 5999000. Furthermore, the income tax on account of revaluation of the available

for sale assets amounts to $ 5070000 (Knechel & Salterio, 2016).

8 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

Comparison with the tax rate

In case the income tax expenses of the company and the rate of income tax applied on the net

income are reconciled, both of them are not same. A reconciliation of the income tax as per the

accounting books and that as per the income tax rules has been shown below in the table where

the effective tax rate for the group is being applied on the consolidated income for the group. The

reconciliation has been given for both the years 2016 as well as 2017 (Sithole, et al., 2017).

Galaxy Resources Limited

Particulars 2017 2016

$’000 $’000

Accounting profit before income tax 6,165 58,020

At the statutory income tax rate of @ 30% (2016:30%) (1,849) (17,406)

Deductible balancing adjustment/(non-deductible expenses) (3,930) 3,222

Tax effect on temporary differences brought to account (507) 18,382

Tax losses brought to account as a deferred tax asset - (63,081)

Utilisation of deferred tax asset previously recognised 434 -

Non-assessable income 356 -

Under provision in prior year (503) (2,593)

Income tax (expense)/benefit (5,999) 64,686

The statutory tax rate being applied to the company as per the taxation rules in Australia is 30%

for both the years 2016 as well as 2017 as can be seen from the above table. The main reason of

the difference in between the two amounts were non deductible expenses, temporary differences,

the utilisation of the prior years’ deferred tax asset balance, etc as can be seen from the above

table (Gooley, 2016).

Reason for deferred tax asset / liability in the balance sheet

The deferred tax asset balance for the company is $ 64686000 and $ 53619000 for the years

2017 and 2016 respectively. The deferred tax asset is regarded as an asset of the company which

may be used to reduce the taxable income in the future years. The same is created when tax is

paid in earlier years against the same and later on as per the accounting books, the benefit can be

taken in the future years (Knechel & Salterio, 2016). These are mainly on account of the timing

differences. Deferred tax assets and liabilities can either be off set against each other or can be

9 | P a g e

Comparison with the tax rate

In case the income tax expenses of the company and the rate of income tax applied on the net

income are reconciled, both of them are not same. A reconciliation of the income tax as per the

accounting books and that as per the income tax rules has been shown below in the table where

the effective tax rate for the group is being applied on the consolidated income for the group. The

reconciliation has been given for both the years 2016 as well as 2017 (Sithole, et al., 2017).

Galaxy Resources Limited

Particulars 2017 2016

$’000 $’000

Accounting profit before income tax 6,165 58,020

At the statutory income tax rate of @ 30% (2016:30%) (1,849) (17,406)

Deductible balancing adjustment/(non-deductible expenses) (3,930) 3,222

Tax effect on temporary differences brought to account (507) 18,382

Tax losses brought to account as a deferred tax asset - (63,081)

Utilisation of deferred tax asset previously recognised 434 -

Non-assessable income 356 -

Under provision in prior year (503) (2,593)

Income tax (expense)/benefit (5,999) 64,686

The statutory tax rate being applied to the company as per the taxation rules in Australia is 30%

for both the years 2016 as well as 2017 as can be seen from the above table. The main reason of

the difference in between the two amounts were non deductible expenses, temporary differences,

the utilisation of the prior years’ deferred tax asset balance, etc as can be seen from the above

table (Gooley, 2016).

Reason for deferred tax asset / liability in the balance sheet

The deferred tax asset balance for the company is $ 64686000 and $ 53619000 for the years

2017 and 2016 respectively. The deferred tax asset is regarded as an asset of the company which

may be used to reduce the taxable income in the future years. The same is created when tax is

paid in earlier years against the same and later on as per the accounting books, the benefit can be

taken in the future years (Knechel & Salterio, 2016). These are mainly on account of the timing

differences. Deferred tax assets and liabilities can either be off set against each other or can be

9 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

shown separately under the head current assets and current liabilities respectively. The deferred

tax asset can be created on account of the following reasons:

1. Revenues being recognised in one period for taxation purposes and in the other period for

accounting books.

2. Assets having different base for accounting and that for the different government

agencies.

3. Losses and expenses being recognised in the accounting books but not in the income tax

books.

Furthermore, the deferred tax assets and liabilities are being reported in the balance sheet to

comply with the requirements of the local GAAP and the IFRS.

Current tax assets or income tax payable recorded by company

The income tax payable and recorded by the company stands at $ 17406000 and $ 1849000 for

the years 2016 and 2017 respoectively. The rise in the tax payable in 2017 is on account of the

greater net profit base in 2017 (Goldmann, 2016). However, it does not matches with the income

tax expenses of the company as income tax payable is calculated as income tax rate being

applied on the profit on the company whereas the actual payment made to the tax authorities are

after considering the deferred tax adjustments. After taking into effect the past year’s deferred

tax asset/liability balance, the actual tax to be paid is being calculated and this is the reason why

two of them don’t match.

Income Tax: Income statement vs Cash Flow statement

The income tax being shown in the income statement and that is being paid or being shown in

the cash flow statement will not be the same. This is because of the reason that the income

statement shows the actual tax expense of the company on the profit earned whereas the cash

flow statement reflects the actual tax being paid by the company which might be more or less

than the actual income tax expense (Jefferson, 2017). Cash flow indicates only the outflow of

cash on account of tax and not the actual tax expenses. It might also be the case that the company

has made the provision of the tax expenses and might not have paid it in the current period. The

10 | P a g e

shown separately under the head current assets and current liabilities respectively. The deferred

tax asset can be created on account of the following reasons:

1. Revenues being recognised in one period for taxation purposes and in the other period for

accounting books.

2. Assets having different base for accounting and that for the different government

agencies.

3. Losses and expenses being recognised in the accounting books but not in the income tax

books.

Furthermore, the deferred tax assets and liabilities are being reported in the balance sheet to

comply with the requirements of the local GAAP and the IFRS.

Current tax assets or income tax payable recorded by company

The income tax payable and recorded by the company stands at $ 17406000 and $ 1849000 for

the years 2016 and 2017 respoectively. The rise in the tax payable in 2017 is on account of the

greater net profit base in 2017 (Goldmann, 2016). However, it does not matches with the income

tax expenses of the company as income tax payable is calculated as income tax rate being

applied on the profit on the company whereas the actual payment made to the tax authorities are

after considering the deferred tax adjustments. After taking into effect the past year’s deferred

tax asset/liability balance, the actual tax to be paid is being calculated and this is the reason why

two of them don’t match.

Income Tax: Income statement vs Cash Flow statement

The income tax being shown in the income statement and that is being paid or being shown in

the cash flow statement will not be the same. This is because of the reason that the income

statement shows the actual tax expense of the company on the profit earned whereas the cash

flow statement reflects the actual tax being paid by the company which might be more or less

than the actual income tax expense (Jefferson, 2017). Cash flow indicates only the outflow of

cash on account of tax and not the actual tax expenses. It might also be the case that the company

has made the provision of the tax expenses and might not have paid it in the current period. The

10 | P a g e

11

difference is also on account of different methods of tax calculation as per the accounting base

and as per the taxation base post the adjustment of the deferred taxes.

Interesting, confusing, surprising or difficult aspects of Income tax treatment

There have been many aspects in the annual report with respect to the calculation of the tax

which were interesting as well as confusing but the most interesting aspect has been the

calculation of tax using the statutory tax rate and how it differs from the actual tax amount being

paid to the government authority (Vieira, et al., 2017). Income tax treatment for revaluation of

the available for sale assets was a bit surprising as in common parlance, the same is not the case.

Overall, the entire exercise, analysis and discussion on the tax and its reconciliation mentioned

above was insightful and interesting as well.

11 | P a g e

difference is also on account of different methods of tax calculation as per the accounting base

and as per the taxation base post the adjustment of the deferred taxes.

Interesting, confusing, surprising or difficult aspects of Income tax treatment

There have been many aspects in the annual report with respect to the calculation of the tax

which were interesting as well as confusing but the most interesting aspect has been the

calculation of tax using the statutory tax rate and how it differs from the actual tax amount being

paid to the government authority (Vieira, et al., 2017). Income tax treatment for revaluation of

the available for sale assets was a bit surprising as in common parlance, the same is not the case.

Overall, the entire exercise, analysis and discussion on the tax and its reconciliation mentioned

above was insightful and interesting as well.

11 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.