Financial Ratio Analysis Report: Gatsby Grange Hotel Industry

VerifiedAdded on 2023/01/06

|12

|3238

|67

Report

AI Summary

This report provides a comprehensive analysis of financial management within the hotel industry, specifically using the case of Gatsby Grange, a small boutique hotel chain. The report begins with an introduction to financial management principles and their application in the hospitality sector, emphasizing the importance of budgeting, financial monitoring, and reporting. The core of the report involves a detailed ratio analysis for the years 2018 and 2019, including profitability, liquidity, and gearing ratios. Each ratio is calculated and interpreted, highlighting fluctuations and trends in the company's financial performance. The analysis includes gross profit ratio, net profit ratio, return on assets, return on capital employed, current ratio, quick ratio, debt to equity ratio, and debt ratio. Furthermore, the report discusses the understanding of ratio fluctuations, emphasizing the importance of interpreting financial statements and the use of ratios in identifying areas for improvement and strategic planning. Finally, the report outlines the benefits and limitations of ratio analysis in decision-making, providing insights into how financial ratios can be used to assess a company's strengths and weaknesses, identify market vulnerabilities, and compare performance with industry benchmarks, while also acknowledging the limitations related to market conditions, accounting practices and changing prices.

Financial Management for

the Hotel Industry

the Hotel Industry

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION...........................................................................................................................................3

TASK............................................................................................................................................................3

Calculation of ratio to analysis financial information..............................................................................3

(b) Understanding of ratio and their fluctuations.....................................................................................7

(c) Benefits and limitation of ration analysis for decision making...........................................................8

TASK 2........................................................................................................................................................10

Covered in PPT.....................................................................................................................................10

CONCLUSION.............................................................................................................................................10

REFERENCES..............................................................................................................................................11

INTRODUCTION...........................................................................................................................................3

TASK............................................................................................................................................................3

Calculation of ratio to analysis financial information..............................................................................3

(b) Understanding of ratio and their fluctuations.....................................................................................7

(c) Benefits and limitation of ration analysis for decision making...........................................................8

TASK 2........................................................................................................................................................10

Covered in PPT.....................................................................................................................................10

CONCLUSION.............................................................................................................................................10

REFERENCES..............................................................................................................................................11

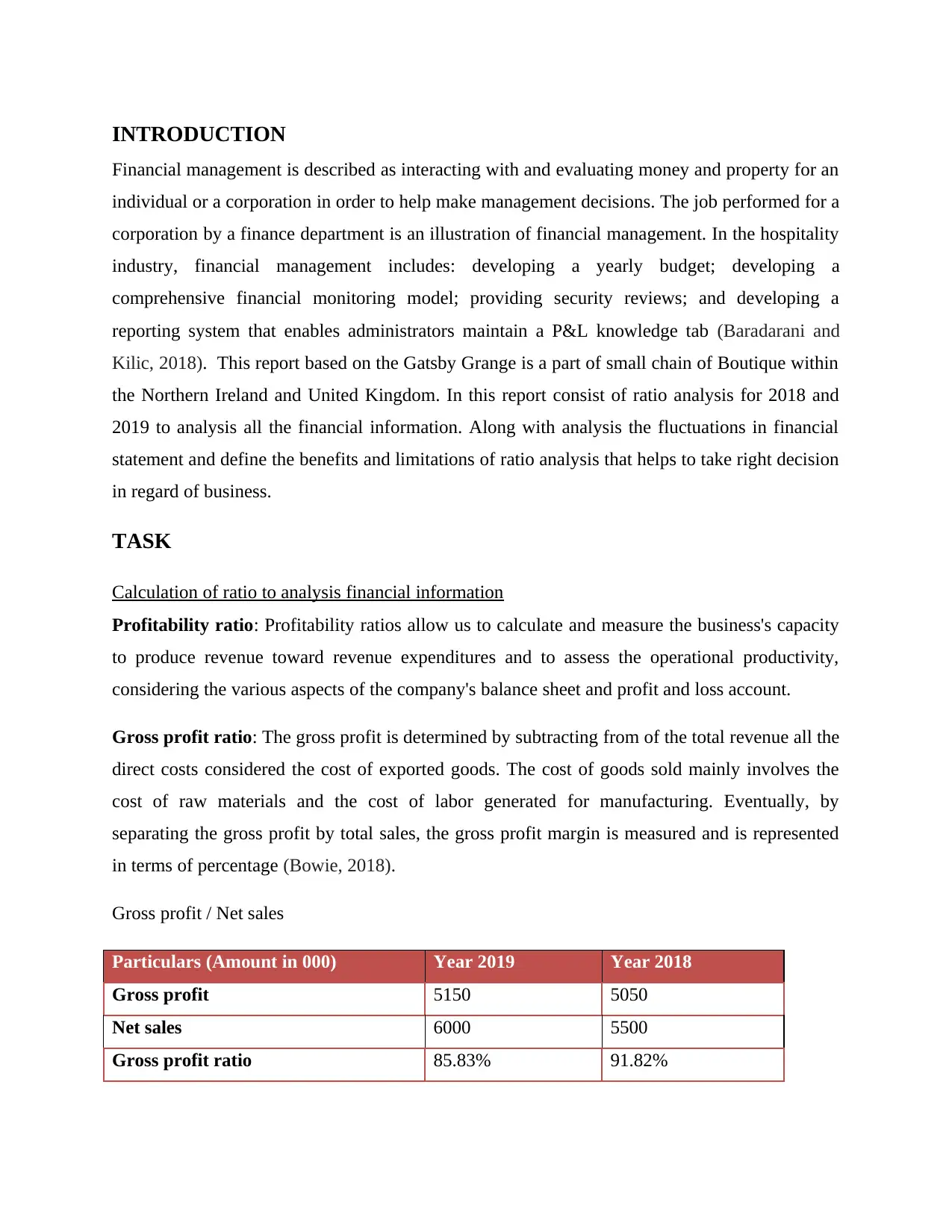

INTRODUCTION

Financial management is described as interacting with and evaluating money and property for an

individual or a corporation in order to help make management decisions. The job performed for a

corporation by a finance department is an illustration of financial management. In the hospitality

industry, financial management includes: developing a yearly budget; developing a

comprehensive financial monitoring model; providing security reviews; and developing a

reporting system that enables administrators maintain a P&L knowledge tab (Baradarani and

Kilic, 2018). This report based on the Gatsby Grange is a part of small chain of Boutique within

the Northern Ireland and United Kingdom. In this report consist of ratio analysis for 2018 and

2019 to analysis all the financial information. Along with analysis the fluctuations in financial

statement and define the benefits and limitations of ratio analysis that helps to take right decision

in regard of business.

TASK

Calculation of ratio to analysis financial information

Profitability ratio: Profitability ratios allow us to calculate and measure the business's capacity

to produce revenue toward revenue expenditures and to assess the operational productivity,

considering the various aspects of the company's balance sheet and profit and loss account.

Gross profit ratio: The gross profit is determined by subtracting from of the total revenue all the

direct costs considered the cost of exported goods. The cost of goods sold mainly involves the

cost of raw materials and the cost of labor generated for manufacturing. Eventually, by

separating the gross profit by total sales, the gross profit margin is measured and is represented

in terms of percentage (Bowie, 2018).

Gross profit / Net sales

Particulars (Amount in 000) Year 2019 Year 2018

Gross profit 5150 5050

Net sales 6000 5500

Gross profit ratio 85.83% 91.82%

Financial management is described as interacting with and evaluating money and property for an

individual or a corporation in order to help make management decisions. The job performed for a

corporation by a finance department is an illustration of financial management. In the hospitality

industry, financial management includes: developing a yearly budget; developing a

comprehensive financial monitoring model; providing security reviews; and developing a

reporting system that enables administrators maintain a P&L knowledge tab (Baradarani and

Kilic, 2018). This report based on the Gatsby Grange is a part of small chain of Boutique within

the Northern Ireland and United Kingdom. In this report consist of ratio analysis for 2018 and

2019 to analysis all the financial information. Along with analysis the fluctuations in financial

statement and define the benefits and limitations of ratio analysis that helps to take right decision

in regard of business.

TASK

Calculation of ratio to analysis financial information

Profitability ratio: Profitability ratios allow us to calculate and measure the business's capacity

to produce revenue toward revenue expenditures and to assess the operational productivity,

considering the various aspects of the company's balance sheet and profit and loss account.

Gross profit ratio: The gross profit is determined by subtracting from of the total revenue all the

direct costs considered the cost of exported goods. The cost of goods sold mainly involves the

cost of raw materials and the cost of labor generated for manufacturing. Eventually, by

separating the gross profit by total sales, the gross profit margin is measured and is represented

in terms of percentage (Bowie, 2018).

Gross profit / Net sales

Particulars (Amount in 000) Year 2019 Year 2018

Gross profit 5150 5050

Net sales 6000 5500

Gross profit ratio 85.83% 91.82%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

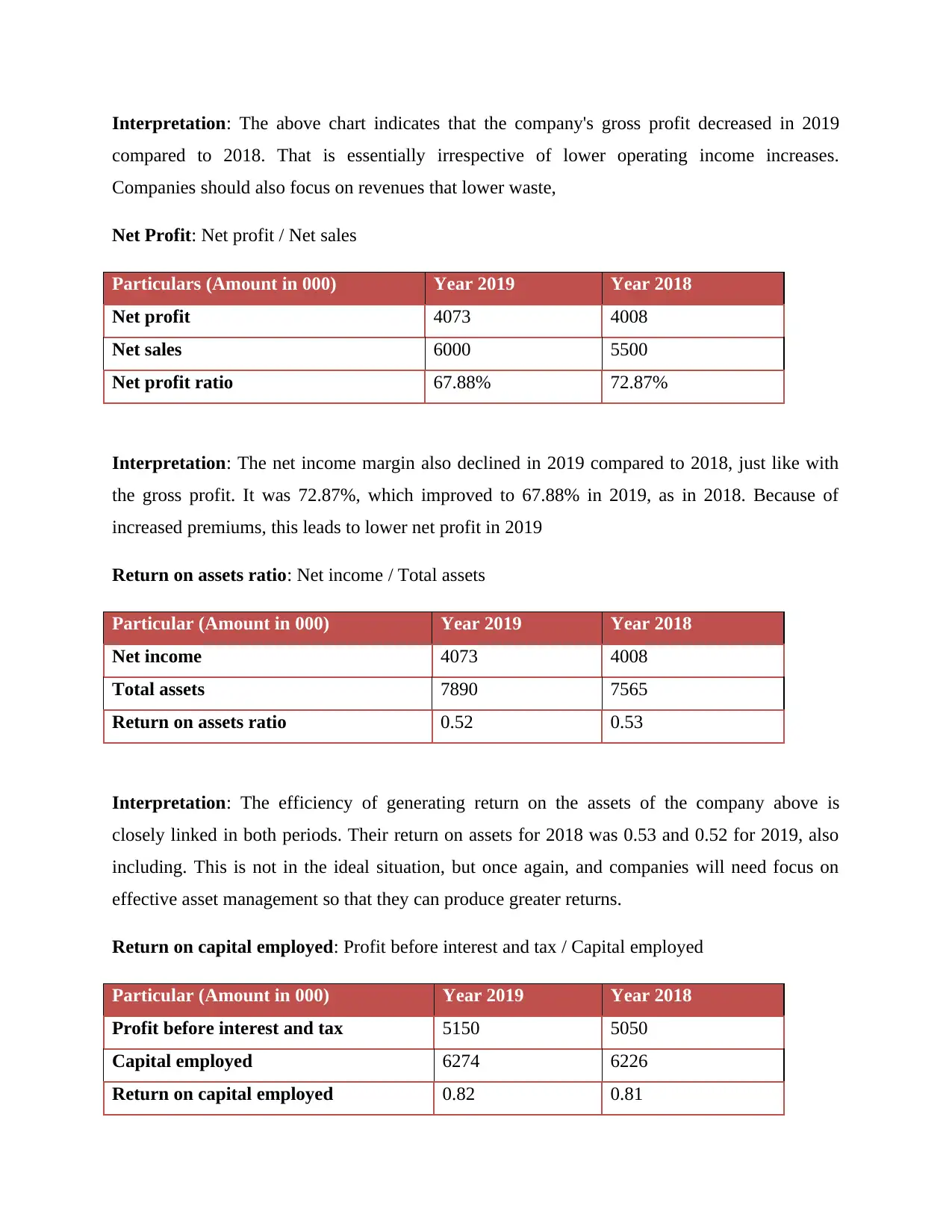

Interpretation: The above chart indicates that the company's gross profit decreased in 2019

compared to 2018. That is essentially irrespective of lower operating income increases.

Companies should also focus on revenues that lower waste,

Net Profit: Net profit / Net sales

Particulars (Amount in 000) Year 2019 Year 2018

Net profit 4073 4008

Net sales 6000 5500

Net profit ratio 67.88% 72.87%

Interpretation: The net income margin also declined in 2019 compared to 2018, just like with

the gross profit. It was 72.87%, which improved to 67.88% in 2019, as in 2018. Because of

increased premiums, this leads to lower net profit in 2019

Return on assets ratio: Net income / Total assets

Particular (Amount in 000) Year 2019 Year 2018

Net income 4073 4008

Total assets 7890 7565

Return on assets ratio 0.52 0.53

Interpretation: The efficiency of generating return on the assets of the company above is

closely linked in both periods. Their return on assets for 2018 was 0.53 and 0.52 for 2019, also

including. This is not in the ideal situation, but once again, and companies will need focus on

effective asset management so that they can produce greater returns.

Return on capital employed: Profit before interest and tax / Capital employed

Particular (Amount in 000) Year 2019 Year 2018

Profit before interest and tax 5150 5050

Capital employed 6274 6226

Return on capital employed 0.82 0.81

compared to 2018. That is essentially irrespective of lower operating income increases.

Companies should also focus on revenues that lower waste,

Net Profit: Net profit / Net sales

Particulars (Amount in 000) Year 2019 Year 2018

Net profit 4073 4008

Net sales 6000 5500

Net profit ratio 67.88% 72.87%

Interpretation: The net income margin also declined in 2019 compared to 2018, just like with

the gross profit. It was 72.87%, which improved to 67.88% in 2019, as in 2018. Because of

increased premiums, this leads to lower net profit in 2019

Return on assets ratio: Net income / Total assets

Particular (Amount in 000) Year 2019 Year 2018

Net income 4073 4008

Total assets 7890 7565

Return on assets ratio 0.52 0.53

Interpretation: The efficiency of generating return on the assets of the company above is

closely linked in both periods. Their return on assets for 2018 was 0.53 and 0.52 for 2019, also

including. This is not in the ideal situation, but once again, and companies will need focus on

effective asset management so that they can produce greater returns.

Return on capital employed: Profit before interest and tax / Capital employed

Particular (Amount in 000) Year 2019 Year 2018

Profit before interest and tax 5150 5050

Capital employed 6274 6226

Return on capital employed 0.82 0.81

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

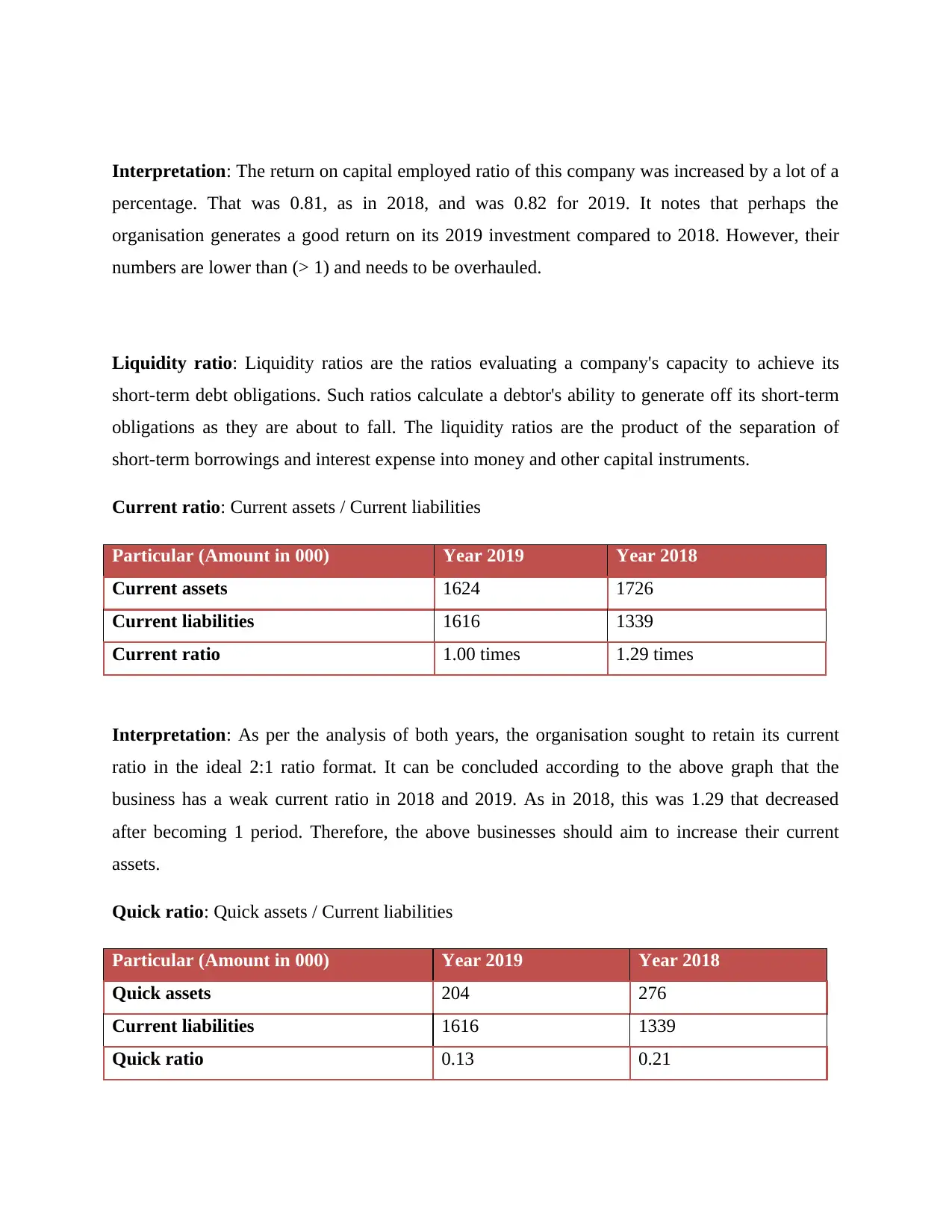

Interpretation: The return on capital employed ratio of this company was increased by a lot of a

percentage. That was 0.81, as in 2018, and was 0.82 for 2019. It notes that perhaps the

organisation generates a good return on its 2019 investment compared to 2018. However, their

numbers are lower than (> 1) and needs to be overhauled.

Liquidity ratio: Liquidity ratios are the ratios evaluating a company's capacity to achieve its

short-term debt obligations. Such ratios calculate a debtor's ability to generate off its short-term

obligations as they are about to fall. The liquidity ratios are the product of the separation of

short-term borrowings and interest expense into money and other capital instruments.

Current ratio: Current assets / Current liabilities

Particular (Amount in 000) Year 2019 Year 2018

Current assets 1624 1726

Current liabilities 1616 1339

Current ratio 1.00 times 1.29 times

Interpretation: As per the analysis of both years, the organisation sought to retain its current

ratio in the ideal 2:1 ratio format. It can be concluded according to the above graph that the

business has a weak current ratio in 2018 and 2019. As in 2018, this was 1.29 that decreased

after becoming 1 period. Therefore, the above businesses should aim to increase their current

assets.

Quick ratio: Quick assets / Current liabilities

Particular (Amount in 000) Year 2019 Year 2018

Quick assets 204 276

Current liabilities 1616 1339

Quick ratio 0.13 0.21

percentage. That was 0.81, as in 2018, and was 0.82 for 2019. It notes that perhaps the

organisation generates a good return on its 2019 investment compared to 2018. However, their

numbers are lower than (> 1) and needs to be overhauled.

Liquidity ratio: Liquidity ratios are the ratios evaluating a company's capacity to achieve its

short-term debt obligations. Such ratios calculate a debtor's ability to generate off its short-term

obligations as they are about to fall. The liquidity ratios are the product of the separation of

short-term borrowings and interest expense into money and other capital instruments.

Current ratio: Current assets / Current liabilities

Particular (Amount in 000) Year 2019 Year 2018

Current assets 1624 1726

Current liabilities 1616 1339

Current ratio 1.00 times 1.29 times

Interpretation: As per the analysis of both years, the organisation sought to retain its current

ratio in the ideal 2:1 ratio format. It can be concluded according to the above graph that the

business has a weak current ratio in 2018 and 2019. As in 2018, this was 1.29 that decreased

after becoming 1 period. Therefore, the above businesses should aim to increase their current

assets.

Quick ratio: Quick assets / Current liabilities

Particular (Amount in 000) Year 2019 Year 2018

Quick assets 204 276

Current liabilities 1616 1339

Quick ratio 0.13 0.21

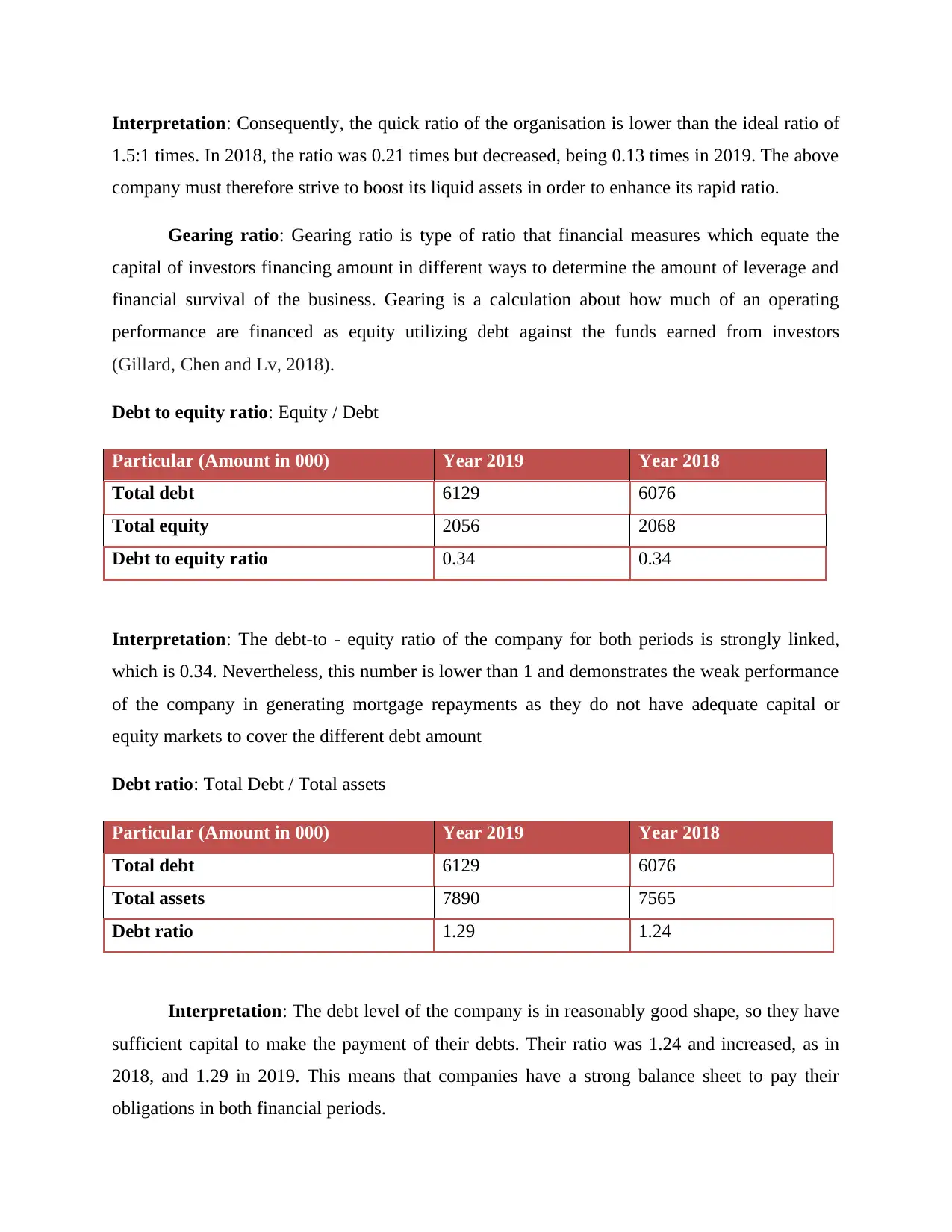

Interpretation: Consequently, the quick ratio of the organisation is lower than the ideal ratio of

1.5:1 times. In 2018, the ratio was 0.21 times but decreased, being 0.13 times in 2019. The above

company must therefore strive to boost its liquid assets in order to enhance its rapid ratio.

Gearing ratio: Gearing ratio is type of ratio that financial measures which equate the

capital of investors financing amount in different ways to determine the amount of leverage and

financial survival of the business. Gearing is a calculation about how much of an operating

performance are financed as equity utilizing debt against the funds earned from investors

(Gillard, Chen and Lv, 2018).

Debt to equity ratio: Equity / Debt

Particular (Amount in 000) Year 2019 Year 2018

Total debt 6129 6076

Total equity 2056 2068

Debt to equity ratio 0.34 0.34

Interpretation: The debt-to - equity ratio of the company for both periods is strongly linked,

which is 0.34. Nevertheless, this number is lower than 1 and demonstrates the weak performance

of the company in generating mortgage repayments as they do not have adequate capital or

equity markets to cover the different debt amount

Debt ratio: Total Debt / Total assets

Particular (Amount in 000) Year 2019 Year 2018

Total debt 6129 6076

Total assets 7890 7565

Debt ratio 1.29 1.24

Interpretation: The debt level of the company is in reasonably good shape, so they have

sufficient capital to make the payment of their debts. Their ratio was 1.24 and increased, as in

2018, and 1.29 in 2019. This means that companies have a strong balance sheet to pay their

obligations in both financial periods.

1.5:1 times. In 2018, the ratio was 0.21 times but decreased, being 0.13 times in 2019. The above

company must therefore strive to boost its liquid assets in order to enhance its rapid ratio.

Gearing ratio: Gearing ratio is type of ratio that financial measures which equate the

capital of investors financing amount in different ways to determine the amount of leverage and

financial survival of the business. Gearing is a calculation about how much of an operating

performance are financed as equity utilizing debt against the funds earned from investors

(Gillard, Chen and Lv, 2018).

Debt to equity ratio: Equity / Debt

Particular (Amount in 000) Year 2019 Year 2018

Total debt 6129 6076

Total equity 2056 2068

Debt to equity ratio 0.34 0.34

Interpretation: The debt-to - equity ratio of the company for both periods is strongly linked,

which is 0.34. Nevertheless, this number is lower than 1 and demonstrates the weak performance

of the company in generating mortgage repayments as they do not have adequate capital or

equity markets to cover the different debt amount

Debt ratio: Total Debt / Total assets

Particular (Amount in 000) Year 2019 Year 2018

Total debt 6129 6076

Total assets 7890 7565

Debt ratio 1.29 1.24

Interpretation: The debt level of the company is in reasonably good shape, so they have

sufficient capital to make the payment of their debts. Their ratio was 1.24 and increased, as in

2018, and 1.29 in 2019. This means that companies have a strong balance sheet to pay their

obligations in both financial periods.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

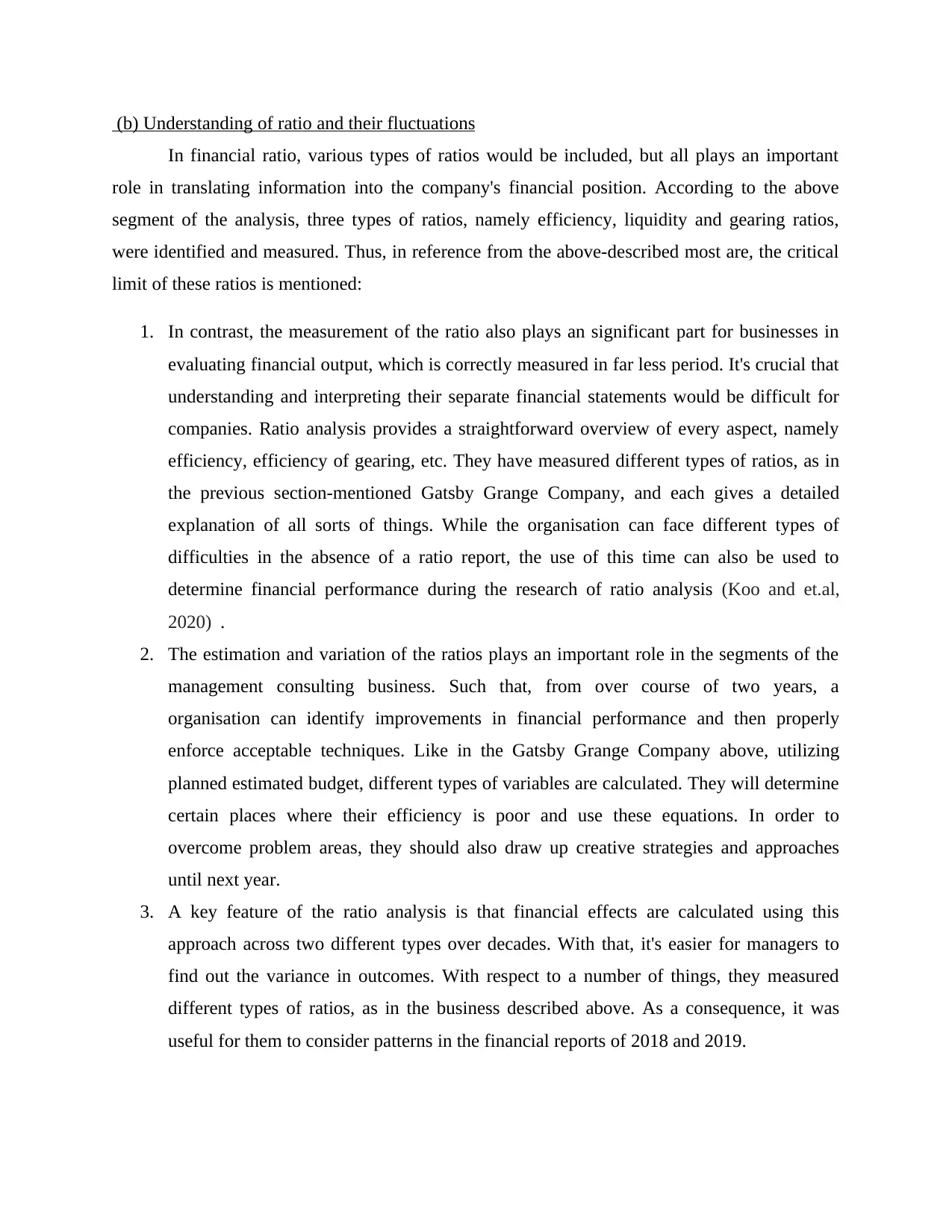

(b) Understanding of ratio and their fluctuations

In financial ratio, various types of ratios would be included, but all plays an important

role in translating information into the company's financial position. According to the above

segment of the analysis, three types of ratios, namely efficiency, liquidity and gearing ratios,

were identified and measured. Thus, in reference from the above-described most are, the critical

limit of these ratios is mentioned:

1. In contrast, the measurement of the ratio also plays an significant part for businesses in

evaluating financial output, which is correctly measured in far less period. It's crucial that

understanding and interpreting their separate financial statements would be difficult for

companies. Ratio analysis provides a straightforward overview of every aspect, namely

efficiency, efficiency of gearing, etc. They have measured different types of ratios, as in

the previous section-mentioned Gatsby Grange Company, and each gives a detailed

explanation of all sorts of things. While the organisation can face different types of

difficulties in the absence of a ratio report, the use of this time can also be used to

determine financial performance during the research of ratio analysis (Koo and et.al,

2020) .

2. The estimation and variation of the ratios plays an important role in the segments of the

management consulting business. Such that, from over course of two years, a

organisation can identify improvements in financial performance and then properly

enforce acceptable techniques. Like in the Gatsby Grange Company above, utilizing

planned estimated budget, different types of variables are calculated. They will determine

certain places where their efficiency is poor and use these equations. In order to

overcome problem areas, they should also draw up creative strategies and approaches

until next year.

3. A key feature of the ratio analysis is that financial effects are calculated using this

approach across two different types over decades. With that, it's easier for managers to

find out the variance in outcomes. With respect to a number of things, they measured

different types of ratios, as in the business described above. As a consequence, it was

useful for them to consider patterns in the financial reports of 2018 and 2019.

In financial ratio, various types of ratios would be included, but all plays an important

role in translating information into the company's financial position. According to the above

segment of the analysis, three types of ratios, namely efficiency, liquidity and gearing ratios,

were identified and measured. Thus, in reference from the above-described most are, the critical

limit of these ratios is mentioned:

1. In contrast, the measurement of the ratio also plays an significant part for businesses in

evaluating financial output, which is correctly measured in far less period. It's crucial that

understanding and interpreting their separate financial statements would be difficult for

companies. Ratio analysis provides a straightforward overview of every aspect, namely

efficiency, efficiency of gearing, etc. They have measured different types of ratios, as in

the previous section-mentioned Gatsby Grange Company, and each gives a detailed

explanation of all sorts of things. While the organisation can face different types of

difficulties in the absence of a ratio report, the use of this time can also be used to

determine financial performance during the research of ratio analysis (Koo and et.al,

2020) .

2. The estimation and variation of the ratios plays an important role in the segments of the

management consulting business. Such that, from over course of two years, a

organisation can identify improvements in financial performance and then properly

enforce acceptable techniques. Like in the Gatsby Grange Company above, utilizing

planned estimated budget, different types of variables are calculated. They will determine

certain places where their efficiency is poor and use these equations. In order to

overcome problem areas, they should also draw up creative strategies and approaches

until next year.

3. A key feature of the ratio analysis is that financial effects are calculated using this

approach across two different types over decades. With that, it's easier for managers to

find out the variance in outcomes. With respect to a number of things, they measured

different types of ratios, as in the business described above. As a consequence, it was

useful for them to consider patterns in the financial reports of 2018 and 2019.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

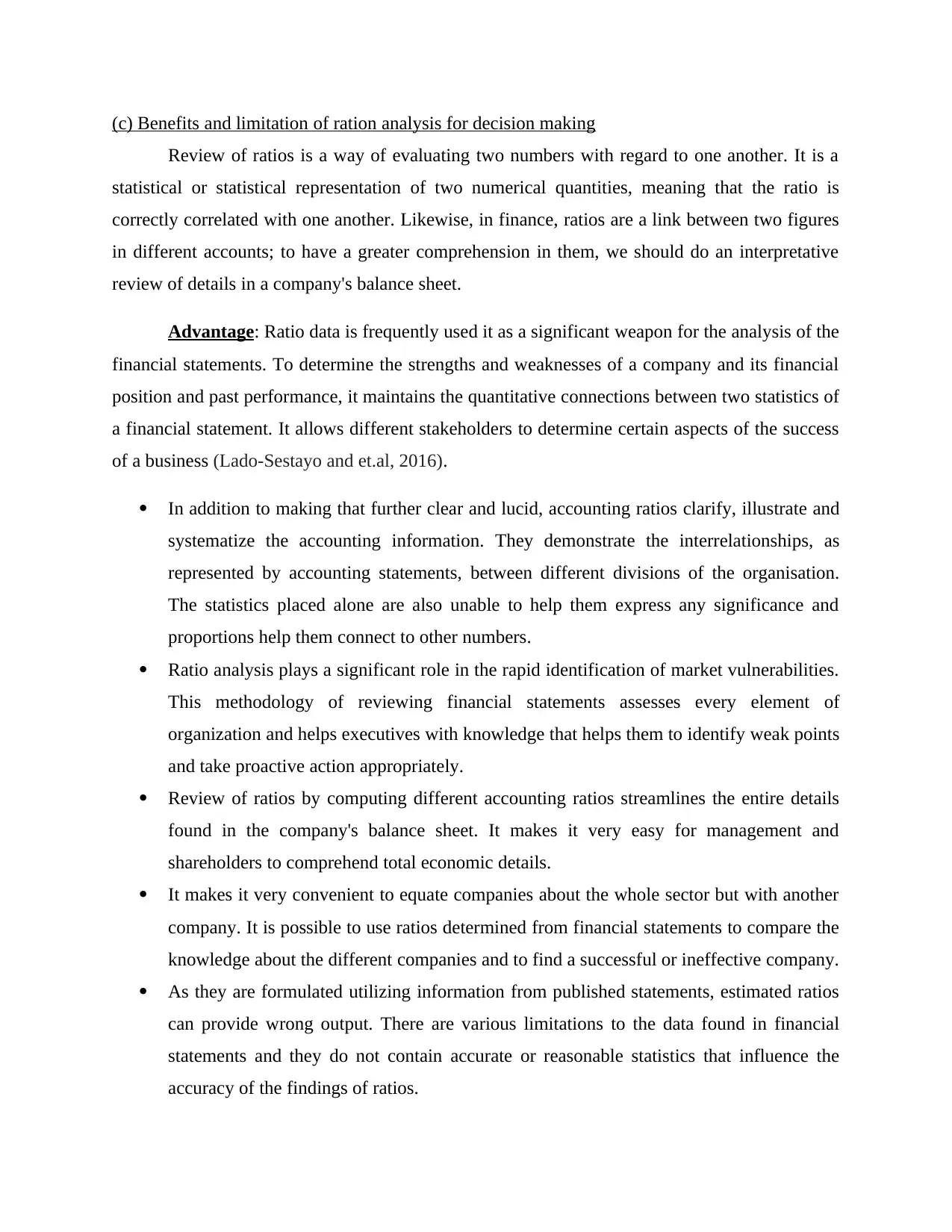

(c) Benefits and limitation of ration analysis for decision making

Review of ratios is a way of evaluating two numbers with regard to one another. It is a

statistical or statistical representation of two numerical quantities, meaning that the ratio is

correctly correlated with one another. Likewise, in finance, ratios are a link between two figures

in different accounts; to have a greater comprehension in them, we should do an interpretative

review of details in a company's balance sheet.

Advantage: Ratio data is frequently used it as a significant weapon for the analysis of the

financial statements. To determine the strengths and weaknesses of a company and its financial

position and past performance, it maintains the quantitative connections between two statistics of

a financial statement. It allows different stakeholders to determine certain aspects of the success

of a business (Lado-Sestayo and et.al, 2016).

In addition to making that further clear and lucid, accounting ratios clarify, illustrate and

systematize the accounting information. They demonstrate the interrelationships, as

represented by accounting statements, between different divisions of the organisation.

The statistics placed alone are also unable to help them express any significance and

proportions help them connect to other numbers.

Ratio analysis plays a significant role in the rapid identification of market vulnerabilities.

This methodology of reviewing financial statements assesses every element of

organization and helps executives with knowledge that helps them to identify weak points

and take proactive action appropriately.

Review of ratios by computing different accounting ratios streamlines the entire details

found in the company's balance sheet. It makes it very easy for management and

shareholders to comprehend total economic details.

It makes it very convenient to equate companies about the whole sector but with another

company. It is possible to use ratios determined from financial statements to compare the

knowledge about the different companies and to find a successful or ineffective company.

As they are formulated utilizing information from published statements, estimated ratios

can provide wrong output. There are various limitations to the data found in financial

statements and they do not contain accurate or reasonable statistics that influence the

accuracy of the findings of ratios.

Review of ratios is a way of evaluating two numbers with regard to one another. It is a

statistical or statistical representation of two numerical quantities, meaning that the ratio is

correctly correlated with one another. Likewise, in finance, ratios are a link between two figures

in different accounts; to have a greater comprehension in them, we should do an interpretative

review of details in a company's balance sheet.

Advantage: Ratio data is frequently used it as a significant weapon for the analysis of the

financial statements. To determine the strengths and weaknesses of a company and its financial

position and past performance, it maintains the quantitative connections between two statistics of

a financial statement. It allows different stakeholders to determine certain aspects of the success

of a business (Lado-Sestayo and et.al, 2016).

In addition to making that further clear and lucid, accounting ratios clarify, illustrate and

systematize the accounting information. They demonstrate the interrelationships, as

represented by accounting statements, between different divisions of the organisation.

The statistics placed alone are also unable to help them express any significance and

proportions help them connect to other numbers.

Ratio analysis plays a significant role in the rapid identification of market vulnerabilities.

This methodology of reviewing financial statements assesses every element of

organization and helps executives with knowledge that helps them to identify weak points

and take proactive action appropriately.

Review of ratios by computing different accounting ratios streamlines the entire details

found in the company's balance sheet. It makes it very easy for management and

shareholders to comprehend total economic details.

It makes it very convenient to equate companies about the whole sector but with another

company. It is possible to use ratios determined from financial statements to compare the

knowledge about the different companies and to find a successful or ineffective company.

As they are formulated utilizing information from published statements, estimated ratios

can provide wrong output. There are various limitations to the data found in financial

statements and they do not contain accurate or reasonable statistics that influence the

accuracy of the findings of ratios.

Accounting ratios tend us get an understanding of how a problem works. If analysis is

conducted on accounting ratios, the productivity of the business appears obvious. By

determining liquidity, solvency, profitability, etc., they assess economic health. It enables

the customer to decide cash obligations and the capacities of different business segments

(Nicoli and Papadopoulou, 2017).

When accounting ratios are evaluated for an amount of decades, then a pattern is formed.

In drawing up specific aspirations and predictions, these important places. Expenditures

as a proportion of revenue, for example, can accurately be estimated on the analysis of

previous years' revenue and expenses.

Limitations:

In various markets, various businesses operate, each with different environmental factors,

such as legislation, financial market, etc. Such variables have become so important that it

may be deceptive to equate two businesses from multiple companies.

Financial accounting information is influenced by projections and assessments. Financial

accounts allow for various financial accounting that hinder consistency and, thus, in such

cases, ratio analysis is less valuable.

The credibility of correlations of ratios measured over multiple intervals periods can be

seriously affected by a change in its price, especially in the case of ratios which integrand

and standard deviation are represented in various types of rupees.

Finding an acceptable level is often a difficult task. The results taken from the ratios can

be no different than the criteria they are compared to.

It avoids the shifts in price levels adjusted for inflation. Most ratios are measured using

discretionary accruals, and the current price shifts between the times are ignored. The

right financial condition is not reflected in this (Polemis, Stengos and Tzeremes, 2020).

No associated with the proposed of ratios are available. So companies can use diverse

conditions for the proportions. This one instance is the Current Ratio, in which some

company takes all current liabilities into account, but the others neglect bank overdraft

charges from current liabilities when measuring the current ratio.

conducted on accounting ratios, the productivity of the business appears obvious. By

determining liquidity, solvency, profitability, etc., they assess economic health. It enables

the customer to decide cash obligations and the capacities of different business segments

(Nicoli and Papadopoulou, 2017).

When accounting ratios are evaluated for an amount of decades, then a pattern is formed.

In drawing up specific aspirations and predictions, these important places. Expenditures

as a proportion of revenue, for example, can accurately be estimated on the analysis of

previous years' revenue and expenses.

Limitations:

In various markets, various businesses operate, each with different environmental factors,

such as legislation, financial market, etc. Such variables have become so important that it

may be deceptive to equate two businesses from multiple companies.

Financial accounting information is influenced by projections and assessments. Financial

accounts allow for various financial accounting that hinder consistency and, thus, in such

cases, ratio analysis is less valuable.

The credibility of correlations of ratios measured over multiple intervals periods can be

seriously affected by a change in its price, especially in the case of ratios which integrand

and standard deviation are represented in various types of rupees.

Finding an acceptable level is often a difficult task. The results taken from the ratios can

be no different than the criteria they are compared to.

It avoids the shifts in price levels adjusted for inflation. Most ratios are measured using

discretionary accruals, and the current price shifts between the times are ignored. The

right financial condition is not reflected in this (Polemis, Stengos and Tzeremes, 2020).

No associated with the proposed of ratios are available. So companies can use diverse

conditions for the proportions. This one instance is the Current Ratio, in which some

company takes all current liabilities into account, but the others neglect bank overdraft

charges from current liabilities when measuring the current ratio.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

For financial issues, ratios will not provide a definitive response. The difficulty of

decision still remains as to what importance the statistics should be provided. Therefore,

in choosing and determining the ratios, one must depend on one's own common sense.

TASK 2

Covered in PPT

CONCLUSION

As per the above report it has been concluded that financial management essential part of

any organisation and apply in every type of industry. In order to analysis the actual financial

condition of business and which type of changes is occurring in the business identify by the ratio

analysis.

decision still remains as to what importance the statistics should be provided. Therefore,

in choosing and determining the ratios, one must depend on one's own common sense.

TASK 2

Covered in PPT

CONCLUSION

As per the above report it has been concluded that financial management essential part of

any organisation and apply in every type of industry. In order to analysis the actual financial

condition of business and which type of changes is occurring in the business identify by the ratio

analysis.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and journal

Baradarani, S. and Kilic, H., 2018. Service innovation in the hotel industry: culture, behavior,

performance. The Service Industries Journal. 38(13-14). pp.897-924.

Bowie, D., 2018. Innovation and 19th century hotel industry evolution. Tourism

Management. 64. pp.314-323.

Gillard, E., Chen, M. H. and Lv, W. Q., 2018. Procedural corruption in the North American hotel

industry. International Journal of Hospitality Management. 72. pp.154-167.

Ionescu, G.H., Firoiu, D., Pîrvu, R., Bădîrcea, R. and Drăgan, C., 2018. Implementation of

integrated management systems and corporate social responsibility initiatives—a

Romanian hospitality industry perspective. Sustainability. 10(10). p.3684.

Koo, B. and et.al, 2020. Relationships among emotional and material rewards, job satisfaction,

burnout, affective commitment, job performance, and turnover intention in the hotel

industry. Journal of Quality Assurance in Hospitality & Tourism. 21(4). pp.371-401.

Lado-Sestayo, R. and et.al, 2016. Impact of location on profitability in the Spanish hotel

sector. Tourism Management. 52. pp.405-415.

Nicoli, N. and Papadopoulou, E., 2017. TripAdvisor and reputation: a case study of the hotel

industry in Cyprus. EuroMed Journal of Business.

Polemis, M. L., Stengos, T. and Tzeremes, N. G., 2020. Advertising expenses and operational

performance: Evidence from the global hotel industry. Economics Letters, p.109220.

Qoura, O. and Khalifa, G. S., 2016. The Impact of Reputation Management on Hotel Image

among Internal Customers: The Case of Egyptian Hotels. International Journal of

Heritage, Tourism, and Hospitality. 7(2).

Radojevic, T., Stanisic, N. and Stanic, N., 2017. Inside the rating scores: a multilevel analysis of

the factors influencing customer satisfaction in the hotel industry. Cornell Hospitality

Quarterly. 58(2). pp.134-164.

Köseoglu, M.A., Putra, E.D., Yi, X., Okumus, F. and Zhao, X., 2019. Strategic Decision Tools and

Organizational Performance in the Hotel Industry. Journal of China Tourism Research, 15(1),

pp.15-32.

Attila, A.T., 2016. The impact of the hotel industry on the competitiveness of tourism

destinations in Hungary. Journal of Competitiveness, 8(4), pp.85-104.

Úbeda-García, M., Claver-Cortés, E., Marco-Lajara, B. and Zaragoza-Sáez, P., 2016. Toward

organizational ambidexterity in the hotel industry: The role of human resources. Cornell

Hospitality Quarterly, 57(4), pp.367-378.

Books and journal

Baradarani, S. and Kilic, H., 2018. Service innovation in the hotel industry: culture, behavior,

performance. The Service Industries Journal. 38(13-14). pp.897-924.

Bowie, D., 2018. Innovation and 19th century hotel industry evolution. Tourism

Management. 64. pp.314-323.

Gillard, E., Chen, M. H. and Lv, W. Q., 2018. Procedural corruption in the North American hotel

industry. International Journal of Hospitality Management. 72. pp.154-167.

Ionescu, G.H., Firoiu, D., Pîrvu, R., Bădîrcea, R. and Drăgan, C., 2018. Implementation of

integrated management systems and corporate social responsibility initiatives—a

Romanian hospitality industry perspective. Sustainability. 10(10). p.3684.

Koo, B. and et.al, 2020. Relationships among emotional and material rewards, job satisfaction,

burnout, affective commitment, job performance, and turnover intention in the hotel

industry. Journal of Quality Assurance in Hospitality & Tourism. 21(4). pp.371-401.

Lado-Sestayo, R. and et.al, 2016. Impact of location on profitability in the Spanish hotel

sector. Tourism Management. 52. pp.405-415.

Nicoli, N. and Papadopoulou, E., 2017. TripAdvisor and reputation: a case study of the hotel

industry in Cyprus. EuroMed Journal of Business.

Polemis, M. L., Stengos, T. and Tzeremes, N. G., 2020. Advertising expenses and operational

performance: Evidence from the global hotel industry. Economics Letters, p.109220.

Qoura, O. and Khalifa, G. S., 2016. The Impact of Reputation Management on Hotel Image

among Internal Customers: The Case of Egyptian Hotels. International Journal of

Heritage, Tourism, and Hospitality. 7(2).

Radojevic, T., Stanisic, N. and Stanic, N., 2017. Inside the rating scores: a multilevel analysis of

the factors influencing customer satisfaction in the hotel industry. Cornell Hospitality

Quarterly. 58(2). pp.134-164.

Köseoglu, M.A., Putra, E.D., Yi, X., Okumus, F. and Zhao, X., 2019. Strategic Decision Tools and

Organizational Performance in the Hotel Industry. Journal of China Tourism Research, 15(1),

pp.15-32.

Attila, A.T., 2016. The impact of the hotel industry on the competitiveness of tourism

destinations in Hungary. Journal of Competitiveness, 8(4), pp.85-104.

Úbeda-García, M., Claver-Cortés, E., Marco-Lajara, B. and Zaragoza-Sáez, P., 2016. Toward

organizational ambidexterity in the hotel industry: The role of human resources. Cornell

Hospitality Quarterly, 57(4), pp.367-378.

Hodari, D., Turner, M.J. and Sturman, M.C., 2017. How hotel owner-operator goal congruence

and GM autonomy influence hotel performance. International journal of hospitality

management, 61, pp.119-128.

Lappas, T., Sabnis, G. and Valkanas, G., 2016. The impact of fake reviews on online visibility:

A vulnerability assessment of the hotel industry. Information Systems Research, 27(4),

pp.940-961.

Bora, P., 2017. Scope Of Stress Management In Hotel Industry. International Journal of

Management, IT and Engineering, 7(7), pp.475-480.

Sajjad, A., Jillani, A. and Raziq, M.M., 2018. Sustainability in the Pakistani hotel industry: an

empirical study. Corporate Governance: The International Journal of Business in

Society.

Josephi, S.H., Stierand, M.B. and Van Mourik, A., 2016. Hotel revenue management: Then, now

and tomorrow. Journal of revenue and pricing management, 15(3-4), pp.252-257.

Ivanov, S. and Stavrinoudis, T.A., 2018. Impacts of the refugee crisis on the hotel industry:

Evidence from four Greek islands. Tourism Management, 67, pp.214-223.

Nieves, J. and Diaz-Meneses, G., 2018. Knowledge sources and innovation in the hotel

industry. International Journal of Contemporary Hospitality Management.

and GM autonomy influence hotel performance. International journal of hospitality

management, 61, pp.119-128.

Lappas, T., Sabnis, G. and Valkanas, G., 2016. The impact of fake reviews on online visibility:

A vulnerability assessment of the hotel industry. Information Systems Research, 27(4),

pp.940-961.

Bora, P., 2017. Scope Of Stress Management In Hotel Industry. International Journal of

Management, IT and Engineering, 7(7), pp.475-480.

Sajjad, A., Jillani, A. and Raziq, M.M., 2018. Sustainability in the Pakistani hotel industry: an

empirical study. Corporate Governance: The International Journal of Business in

Society.

Josephi, S.H., Stierand, M.B. and Van Mourik, A., 2016. Hotel revenue management: Then, now

and tomorrow. Journal of revenue and pricing management, 15(3-4), pp.252-257.

Ivanov, S. and Stavrinoudis, T.A., 2018. Impacts of the refugee crisis on the hotel industry:

Evidence from four Greek islands. Tourism Management, 67, pp.214-223.

Nieves, J. and Diaz-Meneses, G., 2018. Knowledge sources and innovation in the hotel

industry. International Journal of Contemporary Hospitality Management.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.