Understanding Financial Statements of General Mills Inc.

VerifiedAdded on 2022/11/27

|11

|1963

|436

AI Summary

This document provides an in-depth understanding of the financial statements of General Mills Inc. including their income statement, balance sheet, and cash flow statement. It also discusses the stakeholders interested in the company's financial information and the auditors responsible for auditing their financial statements.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: GENERAL MILLS INC. – UNDERSTANDING FINANCIAL

STATEMENTS

General Mills Inc. – Understanding Financial Statements

Name of the Student

Name of the University

Author’s Note

STATEMENTS

General Mills Inc. – Understanding Financial Statements

Name of the Student

Name of the University

Author’s Note

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1GENERAL MILLS INC. – UNDERSTANDING FINANCIAL STATEMENTS

Table of Contents

Answer to [a]..............................................................................................................................1

Answer to [b]..............................................................................................................................1

Answer to [c]..............................................................................................................................1

Answer to [d]..............................................................................................................................1

Answer to [e]..............................................................................................................................2

Answer to [f]..............................................................................................................................2

Answer to [g]..............................................................................................................................4

Requirement i.........................................................................................................................4

Requirement ii........................................................................................................................5

Requirement iii.......................................................................................................................5

Requirement iv.......................................................................................................................6

Answer to [h]..............................................................................................................................6

Requirement i.........................................................................................................................6

Requirement ii........................................................................................................................7

Requirement iii.......................................................................................................................7

Requirement iv.......................................................................................................................7

Requirement v........................................................................................................................7

Requirement vi.......................................................................................................................7

Answer to [i]..............................................................................................................................8

Requirement i.........................................................................................................................8

Requirement ii........................................................................................................................8

Requirement iii.......................................................................................................................8

Answer to [j]..............................................................................................................................8

References................................................................................................................................10

Table of Contents

Answer to [a]..............................................................................................................................1

Answer to [b]..............................................................................................................................1

Answer to [c]..............................................................................................................................1

Answer to [d]..............................................................................................................................1

Answer to [e]..............................................................................................................................2

Answer to [f]..............................................................................................................................2

Answer to [g]..............................................................................................................................4

Requirement i.........................................................................................................................4

Requirement ii........................................................................................................................5

Requirement iii.......................................................................................................................5

Requirement iv.......................................................................................................................6

Answer to [h]..............................................................................................................................6

Requirement i.........................................................................................................................6

Requirement ii........................................................................................................................7

Requirement iii.......................................................................................................................7

Requirement iv.......................................................................................................................7

Requirement v........................................................................................................................7

Requirement vi.......................................................................................................................7

Answer to [i]..............................................................................................................................8

Requirement i.........................................................................................................................8

Requirement ii........................................................................................................................8

Requirement iii.......................................................................................................................8

Answer to [j]..............................................................................................................................8

References................................................................................................................................10

2GENERAL MILLS INC. – UNDERSTANDING FINANCIAL STATEMENTS

Answer to [a]

General Mills is regarded as one of the leading producers of packaged consumer

goods. The company operates through three segments; they are U.S. Retail segment,

International segment and Bakeries and Foodservices.

General Mills makes money through selling ready-to-eat cereals, frozen dough

products, meals, snacks, baking products, yogurts and organic foods.

Answer to [b]

Three financial statements are commonly prepared for the purpose of external

reporting; they are income statement, balance sheet and cash flow statement.

The titles provided by General Mills to these statements are Consolidated statements

of Earnings, Consolidated Balance Sheets and Consolidated Statements of Cash Flows.

‘Consolidated’ means to combine assets, liabilities and other financial items of two or

more companies into one (Carraher & Van Auken, 2013).

Answer to [c]

Publicly traded corporations need to prepare financial statements within 45 days of

each end of quarter and 90 days of each year’s end. In total, these companies are needed to

prepare financial statements total four times a year (Van Auken & Carraher, 2013).

Answer to [d]

The managements of the companies are responsible for financial statements.

The potential users of the financial statements of General Mills are their management,

competitors, customers, employees, investors, government, investment analysts, creditors and

lenders. These stakeholders are interested in the information of the company’s assets,

liabilities, profitability, debt’s position, liquidity position and equity position.

Answer to [a]

General Mills is regarded as one of the leading producers of packaged consumer

goods. The company operates through three segments; they are U.S. Retail segment,

International segment and Bakeries and Foodservices.

General Mills makes money through selling ready-to-eat cereals, frozen dough

products, meals, snacks, baking products, yogurts and organic foods.

Answer to [b]

Three financial statements are commonly prepared for the purpose of external

reporting; they are income statement, balance sheet and cash flow statement.

The titles provided by General Mills to these statements are Consolidated statements

of Earnings, Consolidated Balance Sheets and Consolidated Statements of Cash Flows.

‘Consolidated’ means to combine assets, liabilities and other financial items of two or

more companies into one (Carraher & Van Auken, 2013).

Answer to [c]

Publicly traded corporations need to prepare financial statements within 45 days of

each end of quarter and 90 days of each year’s end. In total, these companies are needed to

prepare financial statements total four times a year (Van Auken & Carraher, 2013).

Answer to [d]

The managements of the companies are responsible for financial statements.

The potential users of the financial statements of General Mills are their management,

competitors, customers, employees, investors, government, investment analysts, creditors and

lenders. These stakeholders are interested in the information of the company’s assets,

liabilities, profitability, debt’s position, liquidity position and equity position.

3GENERAL MILLS INC. – UNDERSTANDING FINANCIAL STATEMENTS

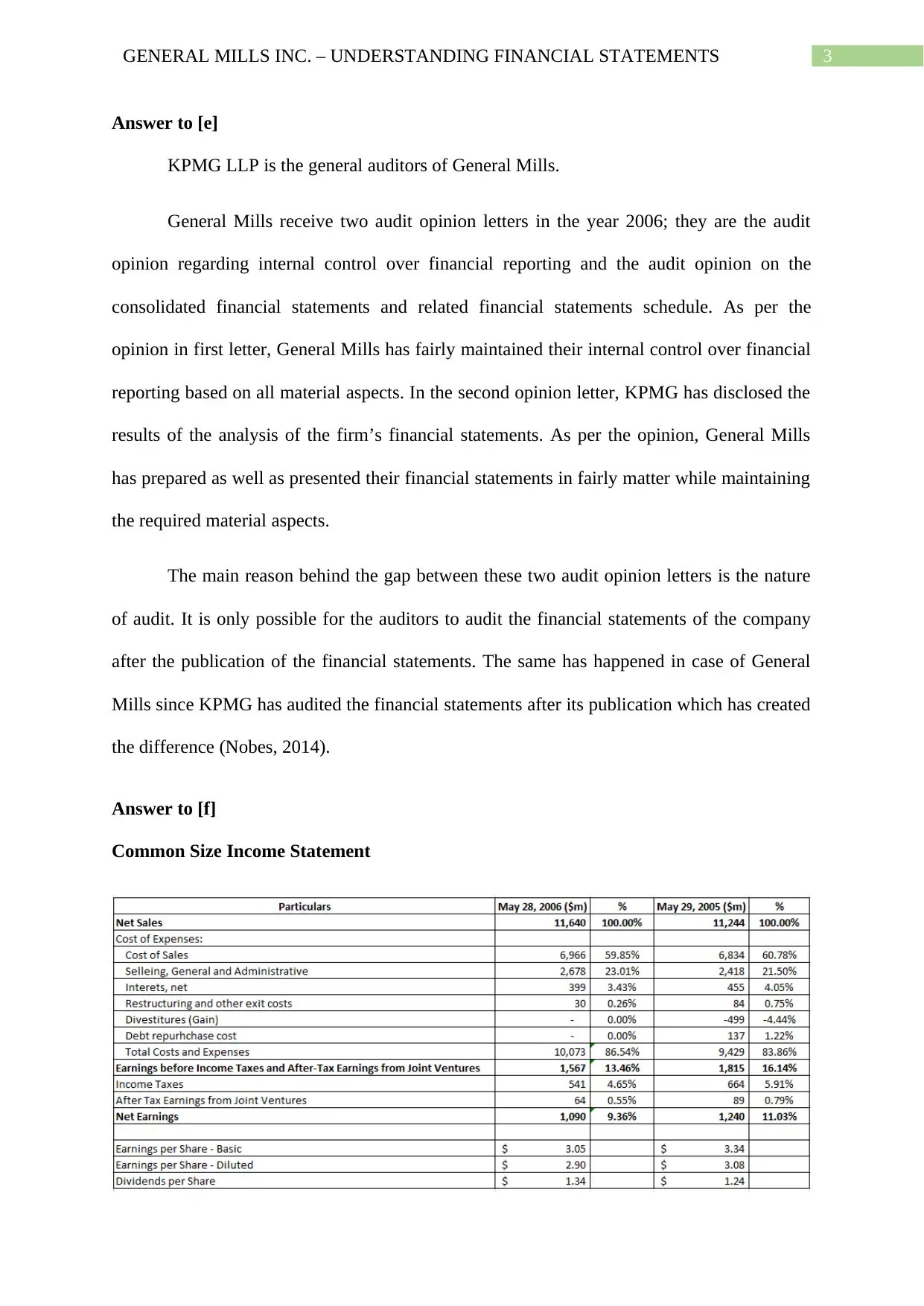

Answer to [e]

KPMG LLP is the general auditors of General Mills.

General Mills receive two audit opinion letters in the year 2006; they are the audit

opinion regarding internal control over financial reporting and the audit opinion on the

consolidated financial statements and related financial statements schedule. As per the

opinion in first letter, General Mills has fairly maintained their internal control over financial

reporting based on all material aspects. In the second opinion letter, KPMG has disclosed the

results of the analysis of the firm’s financial statements. As per the opinion, General Mills

has prepared as well as presented their financial statements in fairly matter while maintaining

the required material aspects.

The main reason behind the gap between these two audit opinion letters is the nature

of audit. It is only possible for the auditors to audit the financial statements of the company

after the publication of the financial statements. The same has happened in case of General

Mills since KPMG has audited the financial statements after its publication which has created

the difference (Nobes, 2014).

Answer to [f]

Common Size Income Statement

Answer to [e]

KPMG LLP is the general auditors of General Mills.

General Mills receive two audit opinion letters in the year 2006; they are the audit

opinion regarding internal control over financial reporting and the audit opinion on the

consolidated financial statements and related financial statements schedule. As per the

opinion in first letter, General Mills has fairly maintained their internal control over financial

reporting based on all material aspects. In the second opinion letter, KPMG has disclosed the

results of the analysis of the firm’s financial statements. As per the opinion, General Mills

has prepared as well as presented their financial statements in fairly matter while maintaining

the required material aspects.

The main reason behind the gap between these two audit opinion letters is the nature

of audit. It is only possible for the auditors to audit the financial statements of the company

after the publication of the financial statements. The same has happened in case of General

Mills since KPMG has audited the financial statements after its publication which has created

the difference (Nobes, 2014).

Answer to [f]

Common Size Income Statement

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4GENERAL MILLS INC. – UNDERSTANDING FINANCIAL STATEMENTS

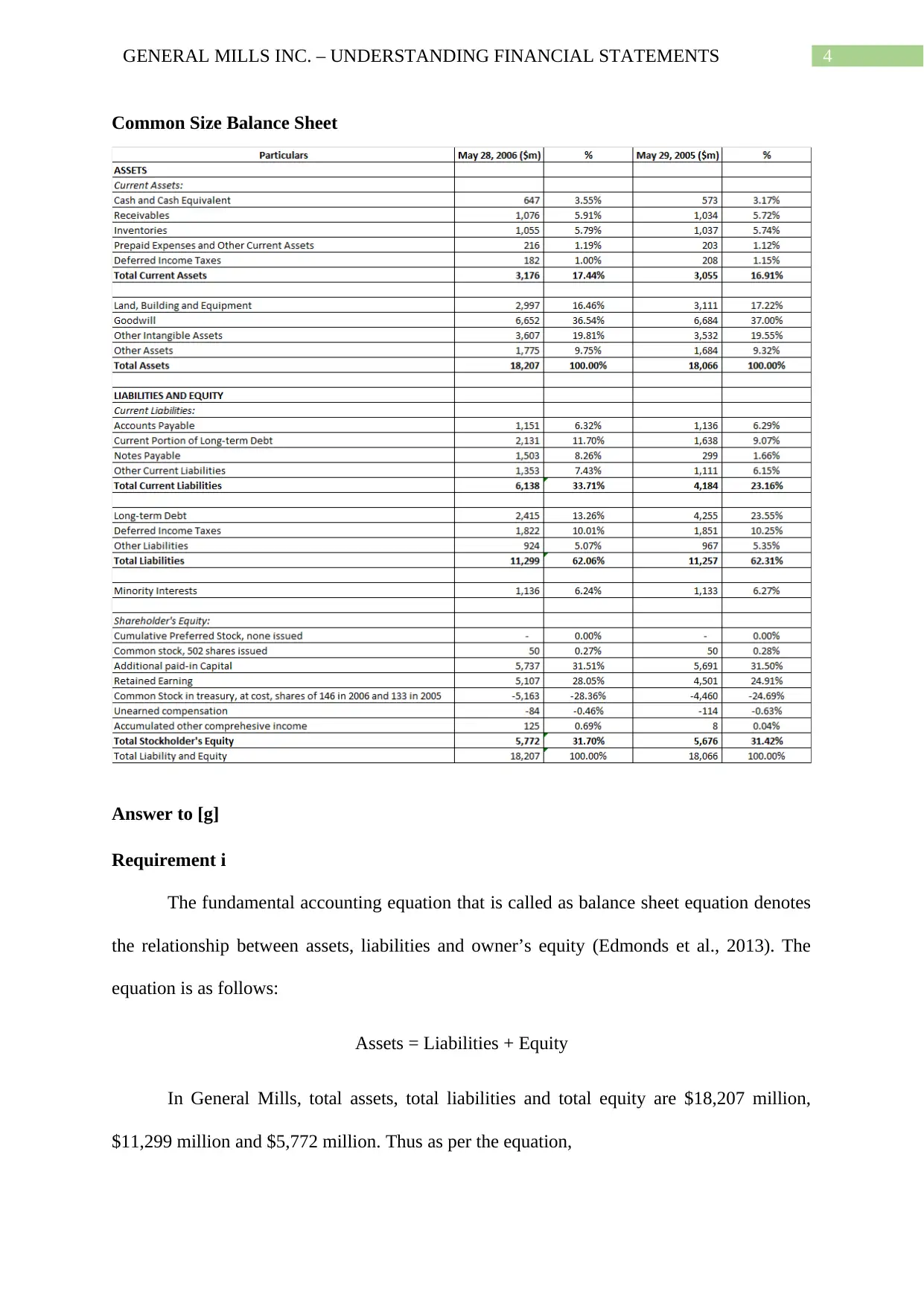

Common Size Balance Sheet

Answer to [g]

Requirement i

The fundamental accounting equation that is called as balance sheet equation denotes

the relationship between assets, liabilities and owner’s equity (Edmonds et al., 2013). The

equation is as follows:

Assets = Liabilities + Equity

In General Mills, total assets, total liabilities and total equity are $18,207 million,

$11,299 million and $5,772 million. Thus as per the equation,

Common Size Balance Sheet

Answer to [g]

Requirement i

The fundamental accounting equation that is called as balance sheet equation denotes

the relationship between assets, liabilities and owner’s equity (Edmonds et al., 2013). The

equation is as follows:

Assets = Liabilities + Equity

In General Mills, total assets, total liabilities and total equity are $18,207 million,

$11,299 million and $5,772 million. Thus as per the equation,

5GENERAL MILLS INC. – UNDERSTANDING FINANCIAL STATEMENTS

Assets = Liabilities + Equity

$18,207 million = $11,299 million + $5,772 million

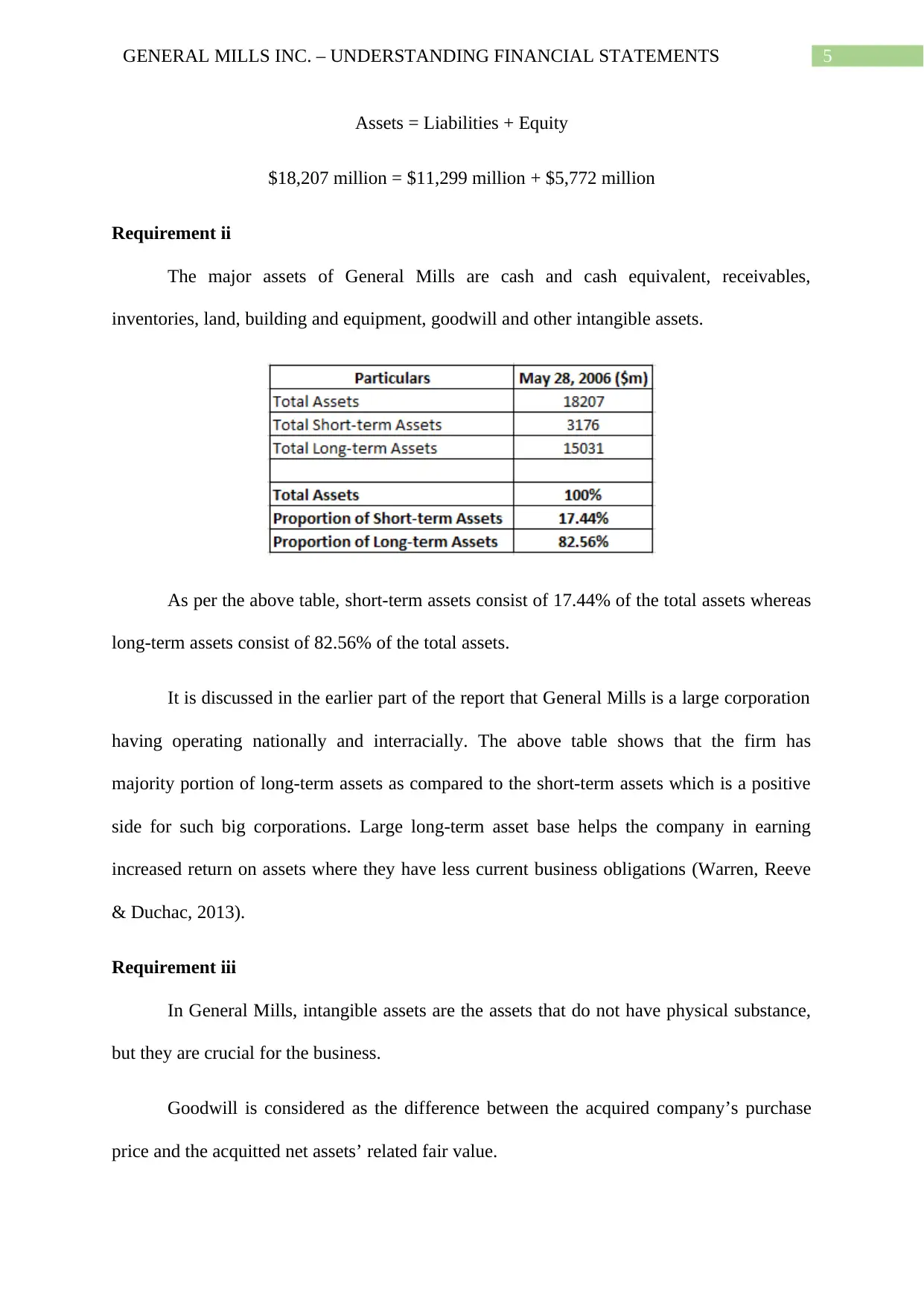

Requirement ii

The major assets of General Mills are cash and cash equivalent, receivables,

inventories, land, building and equipment, goodwill and other intangible assets.

As per the above table, short-term assets consist of 17.44% of the total assets whereas

long-term assets consist of 82.56% of the total assets.

It is discussed in the earlier part of the report that General Mills is a large corporation

having operating nationally and interracially. The above table shows that the firm has

majority portion of long-term assets as compared to the short-term assets which is a positive

side for such big corporations. Large long-term asset base helps the company in earning

increased return on assets where they have less current business obligations (Warren, Reeve

& Duchac, 2013).

Requirement iii

In General Mills, intangible assets are the assets that do not have physical substance,

but they are crucial for the business.

Goodwill is considered as the difference between the acquired company’s purchase

price and the acquitted net assets’ related fair value.

Assets = Liabilities + Equity

$18,207 million = $11,299 million + $5,772 million

Requirement ii

The major assets of General Mills are cash and cash equivalent, receivables,

inventories, land, building and equipment, goodwill and other intangible assets.

As per the above table, short-term assets consist of 17.44% of the total assets whereas

long-term assets consist of 82.56% of the total assets.

It is discussed in the earlier part of the report that General Mills is a large corporation

having operating nationally and interracially. The above table shows that the firm has

majority portion of long-term assets as compared to the short-term assets which is a positive

side for such big corporations. Large long-term asset base helps the company in earning

increased return on assets where they have less current business obligations (Warren, Reeve

& Duchac, 2013).

Requirement iii

In General Mills, intangible assets are the assets that do not have physical substance,

but they are crucial for the business.

Goodwill is considered as the difference between the acquired company’s purchase

price and the acquitted net assets’ related fair value.

6GENERAL MILLS INC. – UNDERSTANDING FINANCIAL STATEMENTS

General Mills might have intangible assets such as patents and copyrights (Yallwe &

Buscemi, 2014).

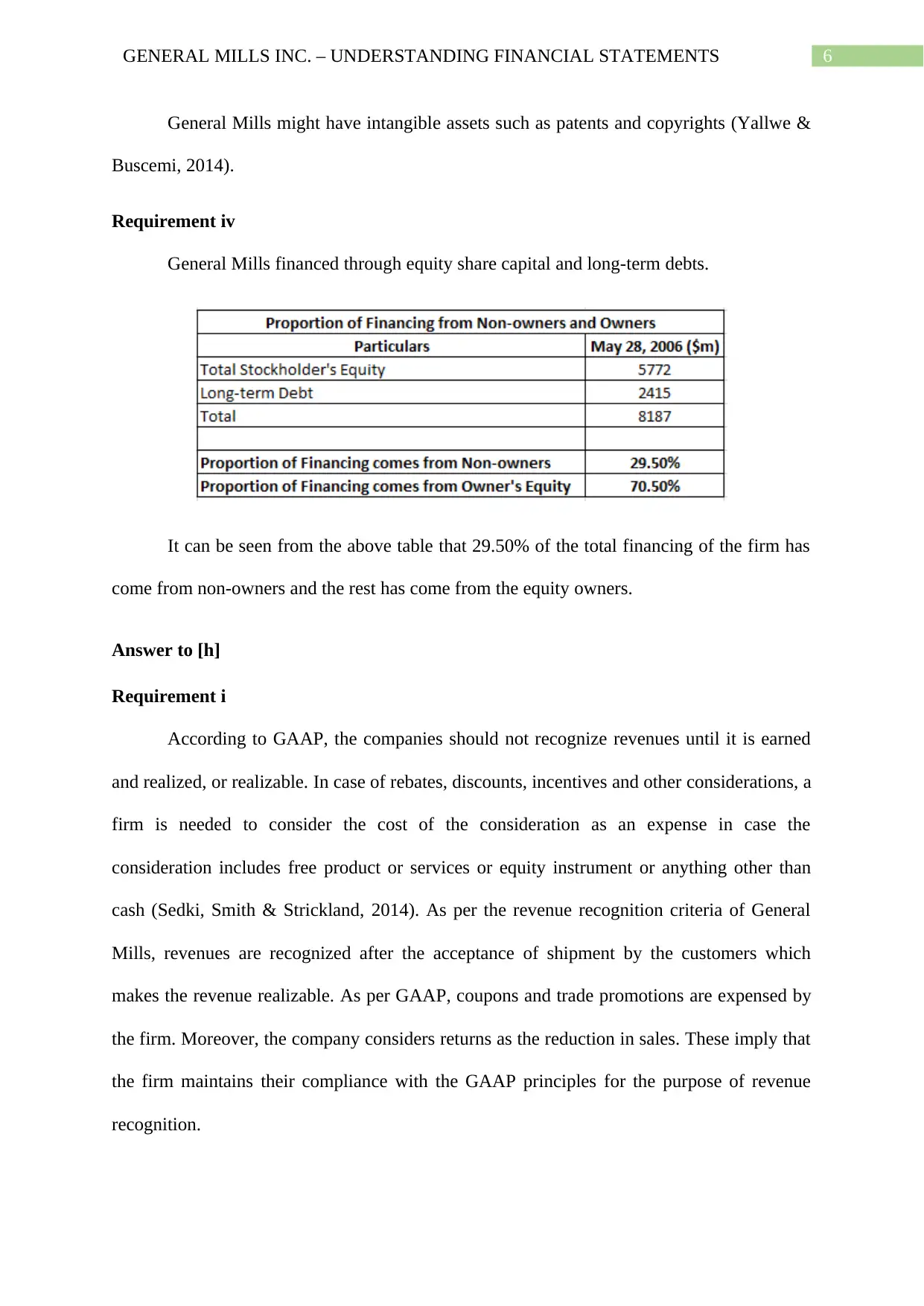

Requirement iv

General Mills financed through equity share capital and long-term debts.

It can be seen from the above table that 29.50% of the total financing of the firm has

come from non-owners and the rest has come from the equity owners.

Answer to [h]

Requirement i

According to GAAP, the companies should not recognize revenues until it is earned

and realized, or realizable. In case of rebates, discounts, incentives and other considerations, a

firm is needed to consider the cost of the consideration as an expense in case the

consideration includes free product or services or equity instrument or anything other than

cash (Sedki, Smith & Strickland, 2014). As per the revenue recognition criteria of General

Mills, revenues are recognized after the acceptance of shipment by the customers which

makes the revenue realizable. As per GAAP, coupons and trade promotions are expensed by

the firm. Moreover, the company considers returns as the reduction in sales. These imply that

the firm maintains their compliance with the GAAP principles for the purpose of revenue

recognition.

General Mills might have intangible assets such as patents and copyrights (Yallwe &

Buscemi, 2014).

Requirement iv

General Mills financed through equity share capital and long-term debts.

It can be seen from the above table that 29.50% of the total financing of the firm has

come from non-owners and the rest has come from the equity owners.

Answer to [h]

Requirement i

According to GAAP, the companies should not recognize revenues until it is earned

and realized, or realizable. In case of rebates, discounts, incentives and other considerations, a

firm is needed to consider the cost of the consideration as an expense in case the

consideration includes free product or services or equity instrument or anything other than

cash (Sedki, Smith & Strickland, 2014). As per the revenue recognition criteria of General

Mills, revenues are recognized after the acceptance of shipment by the customers which

makes the revenue realizable. As per GAAP, coupons and trade promotions are expensed by

the firm. Moreover, the company considers returns as the reduction in sales. These imply that

the firm maintains their compliance with the GAAP principles for the purpose of revenue

recognition.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7GENERAL MILLS INC. – UNDERSTANDING FINANCIAL STATEMENTS

Requirement ii

The major expenses of General Mills are cost of sales and selling, general and

administrative expenses that are $6,966 million and $2,678 million respectively.

Requirement iii

There is not any significant change in the cost structure of General Mills in the recent

year. However, 2005 registered divestiture (gain) and debt repurchase costs and these cannot

be seen in 2006.

Requirement iv

Selling, administrative and general expenses are considered as common expenses for

General Mills that it must incur for keeping the business going. On the other hand, expenses

such as restructuring and other exit costs, divestitures and debt repurchase costs are

uncommon and exceptional expenses which depend on the market condition and thus, there is

not any surety of their occurrence every year. Hence, these expenses have been shown

separately (Needles, Powers & Crosson, 2013).

Requirement v

General Mills was profitable in both 2005 and 2006 since the company registered net

earnings of $1,090 million and $1,240 million in these two years respectively.

Profitable can be described as the situation when a company uses its resources for

revenue generation purpose which exceeds its expenses (Needles, Powers & Crosson, 2013).

Requirement vi

Percentage Change in Net Earnings

Percentage Change in Net Earnings after the exclusion of Special Items

Requirement ii

The major expenses of General Mills are cost of sales and selling, general and

administrative expenses that are $6,966 million and $2,678 million respectively.

Requirement iii

There is not any significant change in the cost structure of General Mills in the recent

year. However, 2005 registered divestiture (gain) and debt repurchase costs and these cannot

be seen in 2006.

Requirement iv

Selling, administrative and general expenses are considered as common expenses for

General Mills that it must incur for keeping the business going. On the other hand, expenses

such as restructuring and other exit costs, divestitures and debt repurchase costs are

uncommon and exceptional expenses which depend on the market condition and thus, there is

not any surety of their occurrence every year. Hence, these expenses have been shown

separately (Needles, Powers & Crosson, 2013).

Requirement v

General Mills was profitable in both 2005 and 2006 since the company registered net

earnings of $1,090 million and $1,240 million in these two years respectively.

Profitable can be described as the situation when a company uses its resources for

revenue generation purpose which exceeds its expenses (Needles, Powers & Crosson, 2013).

Requirement vi

Percentage Change in Net Earnings

Percentage Change in Net Earnings after the exclusion of Special Items

8GENERAL MILLS INC. – UNDERSTANDING FINANCIAL STATEMENTS

As per the above table, the exclusion of the special items decreases the net earnings of

General Mills in 2005 which changes the percentage change in net earnings.

Answer to [i]

Requirement i

The net income of General Mills is $1,090 million where the net cash provided by

operating activities is $1,771 million. The main reason of this difference is that net earnings

is the profit earned by the firm whereas cash flow from operating activities measures the

amount of cash going in and out due to daily business operations. Thus, the calculation of

cash flow from operating activities is done as the sum of net income after the adjustments of

non-cash expenses and changes in working capital (Bhandari & Iyer, 2013). This created the

difference.

Requirement ii

General Mills used $360 million in 2006 for expenditure for land, buildings and

equipment.

Requirement iii

In 2006, General Mills paid a dividend of $485 million.

Answer to [j]

The accounts in the balance sheet of General Mills that need estimates are receivables,

inventories, deferred income taxes, land, building and equipment, goodwill, other intangible

assets, other assets, current portion of long-term debt, notes payable and long-term debt.

As per the above table, the exclusion of the special items decreases the net earnings of

General Mills in 2005 which changes the percentage change in net earnings.

Answer to [i]

Requirement i

The net income of General Mills is $1,090 million where the net cash provided by

operating activities is $1,771 million. The main reason of this difference is that net earnings

is the profit earned by the firm whereas cash flow from operating activities measures the

amount of cash going in and out due to daily business operations. Thus, the calculation of

cash flow from operating activities is done as the sum of net income after the adjustments of

non-cash expenses and changes in working capital (Bhandari & Iyer, 2013). This created the

difference.

Requirement ii

General Mills used $360 million in 2006 for expenditure for land, buildings and

equipment.

Requirement iii

In 2006, General Mills paid a dividend of $485 million.

Answer to [j]

The accounts in the balance sheet of General Mills that need estimates are receivables,

inventories, deferred income taxes, land, building and equipment, goodwill, other intangible

assets, other assets, current portion of long-term debt, notes payable and long-term debt.

9GENERAL MILLS INC. – UNDERSTANDING FINANCIAL STATEMENTS

In addition, there are certain accounts that are estimation free; they are cash and cash

equivalent, prepaid expenses and other current assets, accounts payable and common stock

(Collier, 2015).

In addition, there are certain accounts that are estimation free; they are cash and cash

equivalent, prepaid expenses and other current assets, accounts payable and common stock

(Collier, 2015).

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10GENERAL MILLS INC. – UNDERSTANDING FINANCIAL STATEMENTS

References

Bhandari, S. B., & Iyer, R. (2013). Predicting business failure using cash flow statement

based measures. Managerial Finance, 39(7), 667-676.

Carraher, S., & Van Auken, H. (2013). The use of financial statements for decision making

by small firms. Journal of Small Business & Entrepreneurship, 26(3), 323-336.

Collier, P. M. (2015). Accounting for managers: Interpreting accounting information for

decision making. John Wiley & Sons.

Edmonds, T. P., McNair, F. M., Olds, P. R., & Milam, E. E. (2013). Fundamental financial

accounting concepts. New York, NY: McGraw-Hill Irwin.

Needles, B. E., Powers, M., & Crosson, S. V. (2013). Principles of accounting. Cengage

Learning.

Nobes, C. (2014). International classification of financial reporting. Routledge.

Sedki, S. S., Smith, A., & Strickland, A. (2014). Differences and similarities between IFRS

and GAAP on inventory, revenue recognition and consolidated financial

statements. Journal of Accounting and Finance, 14(2), 120.

Van Auken, H., & Carraher, S. (2013). Influences on frequency of preparation of financial

statements among SMEs. Journal of Innovation Management, 1(1), 143.

Warren, C., Reeve, J. M., & Duchac, J. (2013). Financial & managerial accounting. Cengage

Learning.

Yallwe, A. H., & Buscemi, A. (2014). An era of intangible assets. Journal of Applied

Finance and Banking, 4(5), 17.

References

Bhandari, S. B., & Iyer, R. (2013). Predicting business failure using cash flow statement

based measures. Managerial Finance, 39(7), 667-676.

Carraher, S., & Van Auken, H. (2013). The use of financial statements for decision making

by small firms. Journal of Small Business & Entrepreneurship, 26(3), 323-336.

Collier, P. M. (2015). Accounting for managers: Interpreting accounting information for

decision making. John Wiley & Sons.

Edmonds, T. P., McNair, F. M., Olds, P. R., & Milam, E. E. (2013). Fundamental financial

accounting concepts. New York, NY: McGraw-Hill Irwin.

Needles, B. E., Powers, M., & Crosson, S. V. (2013). Principles of accounting. Cengage

Learning.

Nobes, C. (2014). International classification of financial reporting. Routledge.

Sedki, S. S., Smith, A., & Strickland, A. (2014). Differences and similarities between IFRS

and GAAP on inventory, revenue recognition and consolidated financial

statements. Journal of Accounting and Finance, 14(2), 120.

Van Auken, H., & Carraher, S. (2013). Influences on frequency of preparation of financial

statements among SMEs. Journal of Innovation Management, 1(1), 143.

Warren, C., Reeve, J. M., & Duchac, J. (2013). Financial & managerial accounting. Cengage

Learning.

Yallwe, A. H., & Buscemi, A. (2014). An era of intangible assets. Journal of Applied

Finance and Banking, 4(5), 17.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.