Eurozone Bank Risks and the Carry Trade

VerifiedAdded on 2020/01/28

|11

|3067

|54

Report

AI Summary

This assignment delves into the complex issues surrounding eurozone bank risks and the phenomenon known as the 'carry trade'. It explores how external imbalances and self-fulfilling crises can threaten the stability of European banks. The analysis incorporates economic indicators such as inflation, bond yields, and cost of living across various Eurozone member states.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

GLOBAL FINANCE

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................3

Question 1........................................................................................................................................3

(1) Calculation of purchase power parity...............................................................................3

(2) Purchase power parity when inflation rate of Spain is considered...................................4

(3) Difference between equilibrium rates of A and B and valuation of Euro according to PPP 5

(d) Will Euro break in future..................................................................................................6

Question 2........................................................................................................................................7

(2) Whether or not Euro will survive from recent Euro-zone crisis.......................................7

CONCLUSION................................................................................................................................8

REFERENCES..............................................................................................................................10

APPENDIX....................................................................................................................................11

INDEX OF TABLES

Table 1: PPP when inflation rate is related to Germany..................................................................3

Table 2: PPP when inflation rate of Spain is taken in to consideration...........................................4

ILLUSTRATION INDEX

Illustration 1: Interest rate of member states of Euro-zone.............................................................6

Illustration 2: Inflation rate of member states of Euro-zone............................................................7

INTRODUCTION...........................................................................................................................3

Question 1........................................................................................................................................3

(1) Calculation of purchase power parity...............................................................................3

(2) Purchase power parity when inflation rate of Spain is considered...................................4

(3) Difference between equilibrium rates of A and B and valuation of Euro according to PPP 5

(d) Will Euro break in future..................................................................................................6

Question 2........................................................................................................................................7

(2) Whether or not Euro will survive from recent Euro-zone crisis.......................................7

CONCLUSION................................................................................................................................8

REFERENCES..............................................................................................................................10

APPENDIX....................................................................................................................................11

INDEX OF TABLES

Table 1: PPP when inflation rate is related to Germany..................................................................3

Table 2: PPP when inflation rate of Spain is taken in to consideration...........................................4

ILLUSTRATION INDEX

Illustration 1: Interest rate of member states of Euro-zone.............................................................6

Illustration 2: Inflation rate of member states of Euro-zone............................................................7

INTRODUCTION

Euro-zone is currently facing lots of problems which is known to everyone. In this report

various issued related to EU are discussed and answer of question whether EURO will survive is

identified by evaluating figures and theoretical models.

Question 1

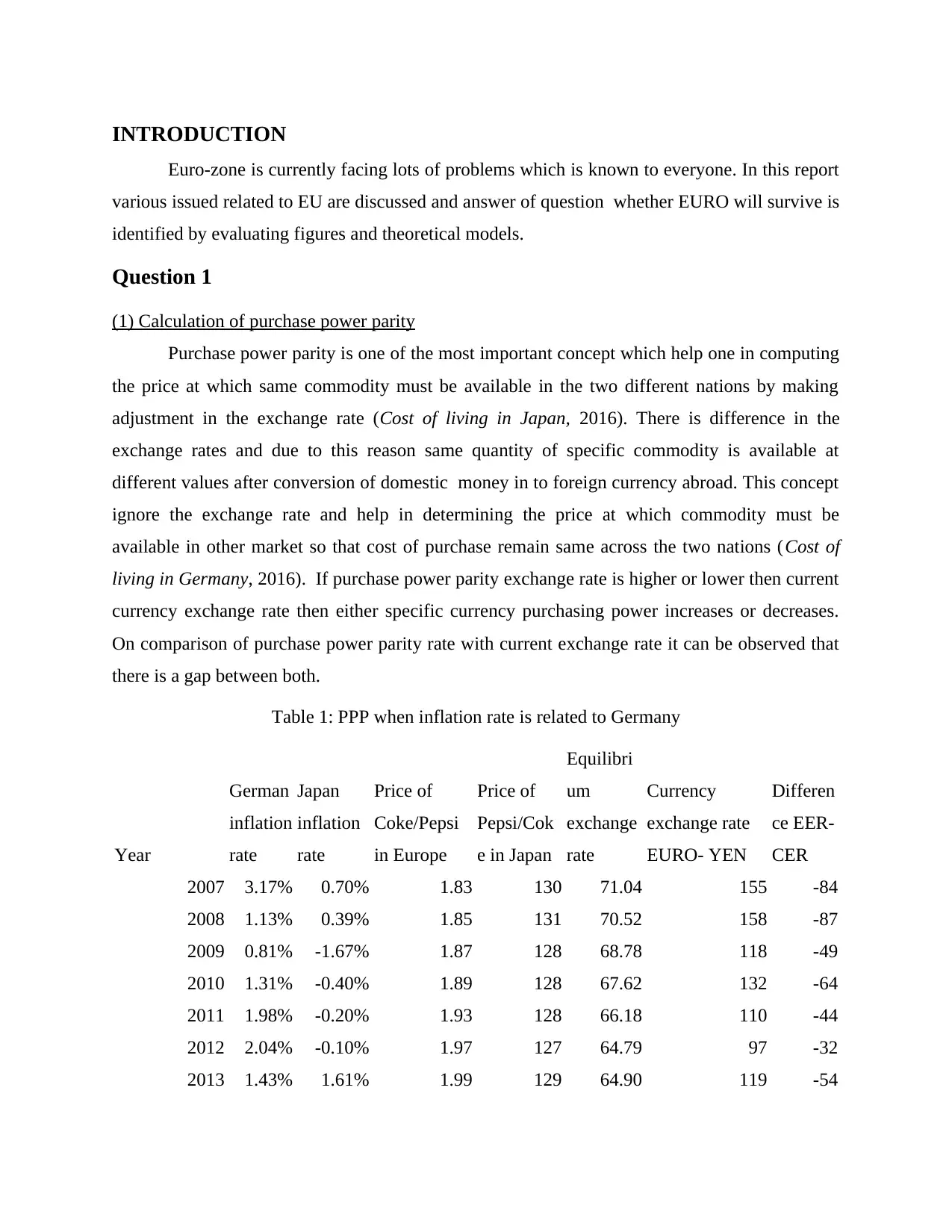

(1) Calculation of purchase power parity

Purchase power parity is one of the most important concept which help one in computing

the price at which same commodity must be available in the two different nations by making

adjustment in the exchange rate (Cost of living in Japan, 2016). There is difference in the

exchange rates and due to this reason same quantity of specific commodity is available at

different values after conversion of domestic money in to foreign currency abroad. This concept

ignore the exchange rate and help in determining the price at which commodity must be

available in other market so that cost of purchase remain same across the two nations (Cost of

living in Germany, 2016). If purchase power parity exchange rate is higher or lower then current

currency exchange rate then either specific currency purchasing power increases or decreases.

On comparison of purchase power parity rate with current exchange rate it can be observed that

there is a gap between both.

Table 1: PPP when inflation rate is related to Germany

Year

German

inflation

rate

Japan

inflation

rate

Price of

Coke/Pepsi

in Europe

Price of

Pepsi/Cok

e in Japan

Equilibri

um

exchange

rate

Currency

exchange rate

EURO- YEN

Differen

ce EER-

CER

2007 3.17% 0.70% 1.83 130 71.04 155 -84

2008 1.13% 0.39% 1.85 131 70.52 158 -87

2009 0.81% -1.67% 1.87 128 68.78 118 -49

2010 1.31% -0.40% 1.89 128 67.62 132 -64

2011 1.98% -0.20% 1.93 128 66.18 110 -44

2012 2.04% -0.10% 1.97 127 64.79 97 -32

2013 1.43% 1.61% 1.99 129 64.90 119 -54

Euro-zone is currently facing lots of problems which is known to everyone. In this report

various issued related to EU are discussed and answer of question whether EURO will survive is

identified by evaluating figures and theoretical models.

Question 1

(1) Calculation of purchase power parity

Purchase power parity is one of the most important concept which help one in computing

the price at which same commodity must be available in the two different nations by making

adjustment in the exchange rate (Cost of living in Japan, 2016). There is difference in the

exchange rates and due to this reason same quantity of specific commodity is available at

different values after conversion of domestic money in to foreign currency abroad. This concept

ignore the exchange rate and help in determining the price at which commodity must be

available in other market so that cost of purchase remain same across the two nations (Cost of

living in Germany, 2016). If purchase power parity exchange rate is higher or lower then current

currency exchange rate then either specific currency purchasing power increases or decreases.

On comparison of purchase power parity rate with current exchange rate it can be observed that

there is a gap between both.

Table 1: PPP when inflation rate is related to Germany

Year

German

inflation

rate

Japan

inflation

rate

Price of

Coke/Pepsi

in Europe

Price of

Pepsi/Cok

e in Japan

Equilibri

um

exchange

rate

Currency

exchange rate

EURO- YEN

Differen

ce EER-

CER

2007 3.17% 0.70% 1.83 130 71.04 155 -84

2008 1.13% 0.39% 1.85 131 70.52 158 -87

2009 0.81% -1.67% 1.87 128 68.78 118 -49

2010 1.31% -0.40% 1.89 128 67.62 132 -64

2011 1.98% -0.20% 1.93 128 66.18 110 -44

2012 2.04% -0.10% 1.97 127 64.79 97 -32

2013 1.43% 1.61% 1.99 129 64.90 119 -54

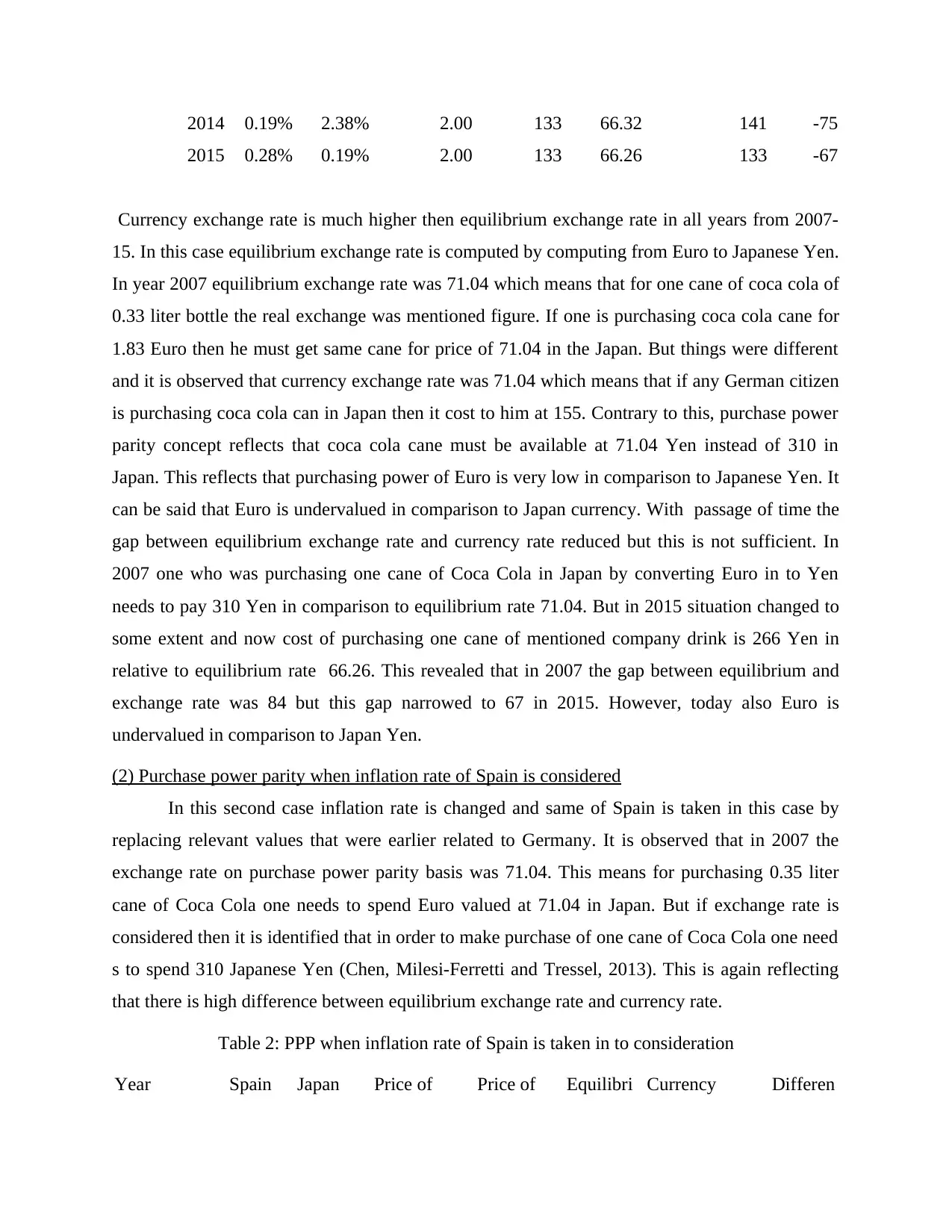

2014 0.19% 2.38% 2.00 133 66.32 141 -75

2015 0.28% 0.19% 2.00 133 66.26 133 -67

Currency exchange rate is much higher then equilibrium exchange rate in all years from 2007-

15. In this case equilibrium exchange rate is computed by computing from Euro to Japanese Yen.

In year 2007 equilibrium exchange rate was 71.04 which means that for one cane of coca cola of

0.33 liter bottle the real exchange was mentioned figure. If one is purchasing coca cola cane for

1.83 Euro then he must get same cane for price of 71.04 in the Japan. But things were different

and it is observed that currency exchange rate was 71.04 which means that if any German citizen

is purchasing coca cola can in Japan then it cost to him at 155. Contrary to this, purchase power

parity concept reflects that coca cola cane must be available at 71.04 Yen instead of 310 in

Japan. This reflects that purchasing power of Euro is very low in comparison to Japanese Yen. It

can be said that Euro is undervalued in comparison to Japan currency. With passage of time the

gap between equilibrium exchange rate and currency rate reduced but this is not sufficient. In

2007 one who was purchasing one cane of Coca Cola in Japan by converting Euro in to Yen

needs to pay 310 Yen in comparison to equilibrium rate 71.04. But in 2015 situation changed to

some extent and now cost of purchasing one cane of mentioned company drink is 266 Yen in

relative to equilibrium rate 66.26. This revealed that in 2007 the gap between equilibrium and

exchange rate was 84 but this gap narrowed to 67 in 2015. However, today also Euro is

undervalued in comparison to Japan Yen.

(2) Purchase power parity when inflation rate of Spain is considered

In this second case inflation rate is changed and same of Spain is taken in this case by

replacing relevant values that were earlier related to Germany. It is observed that in 2007 the

exchange rate on purchase power parity basis was 71.04. This means for purchasing 0.35 liter

cane of Coca Cola one needs to spend Euro valued at 71.04 in Japan. But if exchange rate is

considered then it is identified that in order to make purchase of one cane of Coca Cola one need

s to spend 310 Japanese Yen (Chen, Milesi-Ferretti and Tressel, 2013). This is again reflecting

that there is high difference between equilibrium exchange rate and currency rate.

Table 2: PPP when inflation rate of Spain is taken in to consideration

Year Spain Japan Price of Price of Equilibri Currency Differen

2015 0.28% 0.19% 2.00 133 66.26 133 -67

Currency exchange rate is much higher then equilibrium exchange rate in all years from 2007-

15. In this case equilibrium exchange rate is computed by computing from Euro to Japanese Yen.

In year 2007 equilibrium exchange rate was 71.04 which means that for one cane of coca cola of

0.33 liter bottle the real exchange was mentioned figure. If one is purchasing coca cola cane for

1.83 Euro then he must get same cane for price of 71.04 in the Japan. But things were different

and it is observed that currency exchange rate was 71.04 which means that if any German citizen

is purchasing coca cola can in Japan then it cost to him at 155. Contrary to this, purchase power

parity concept reflects that coca cola cane must be available at 71.04 Yen instead of 310 in

Japan. This reflects that purchasing power of Euro is very low in comparison to Japanese Yen. It

can be said that Euro is undervalued in comparison to Japan currency. With passage of time the

gap between equilibrium exchange rate and currency rate reduced but this is not sufficient. In

2007 one who was purchasing one cane of Coca Cola in Japan by converting Euro in to Yen

needs to pay 310 Yen in comparison to equilibrium rate 71.04. But in 2015 situation changed to

some extent and now cost of purchasing one cane of mentioned company drink is 266 Yen in

relative to equilibrium rate 66.26. This revealed that in 2007 the gap between equilibrium and

exchange rate was 84 but this gap narrowed to 67 in 2015. However, today also Euro is

undervalued in comparison to Japan Yen.

(2) Purchase power parity when inflation rate of Spain is considered

In this second case inflation rate is changed and same of Spain is taken in this case by

replacing relevant values that were earlier related to Germany. It is observed that in 2007 the

exchange rate on purchase power parity basis was 71.04. This means for purchasing 0.35 liter

cane of Coca Cola one needs to spend Euro valued at 71.04 in Japan. But if exchange rate is

considered then it is identified that in order to make purchase of one cane of Coca Cola one need

s to spend 310 Japanese Yen (Chen, Milesi-Ferretti and Tressel, 2013). This is again reflecting

that there is high difference between equilibrium exchange rate and currency rate.

Table 2: PPP when inflation rate of Spain is taken in to consideration

Year Spain Japan Price of Price of Equilibri Currency Differen

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

inflation

rate

inflation

rate

Coke/Pepsi

in Europe

Pepsi/Cok

e in Japan

um

exchange

rate

exchange rate

EURO- YEN

ce EER-

CER

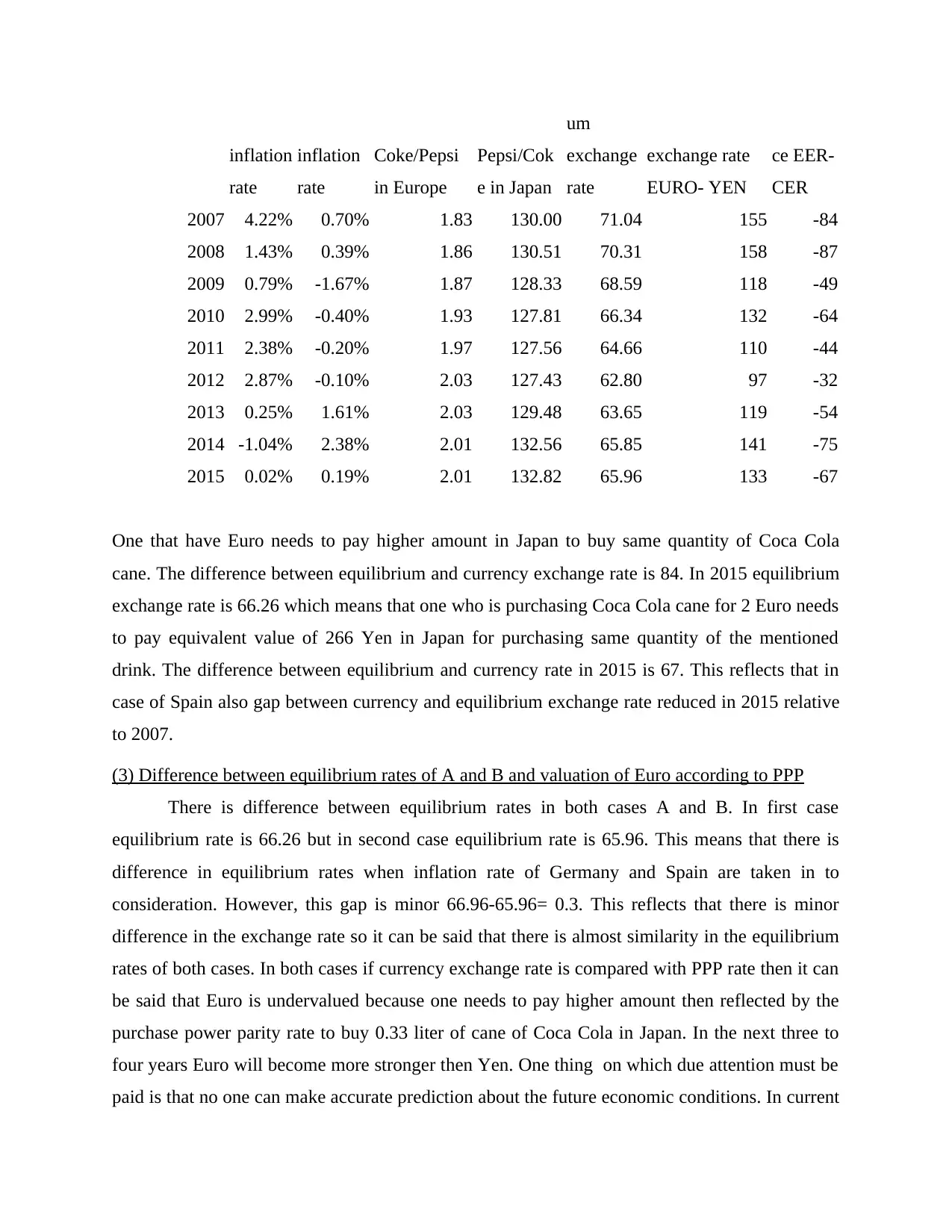

2007 4.22% 0.70% 1.83 130.00 71.04 155 -84

2008 1.43% 0.39% 1.86 130.51 70.31 158 -87

2009 0.79% -1.67% 1.87 128.33 68.59 118 -49

2010 2.99% -0.40% 1.93 127.81 66.34 132 -64

2011 2.38% -0.20% 1.97 127.56 64.66 110 -44

2012 2.87% -0.10% 2.03 127.43 62.80 97 -32

2013 0.25% 1.61% 2.03 129.48 63.65 119 -54

2014 -1.04% 2.38% 2.01 132.56 65.85 141 -75

2015 0.02% 0.19% 2.01 132.82 65.96 133 -67

One that have Euro needs to pay higher amount in Japan to buy same quantity of Coca Cola

cane. The difference between equilibrium and currency exchange rate is 84. In 2015 equilibrium

exchange rate is 66.26 which means that one who is purchasing Coca Cola cane for 2 Euro needs

to pay equivalent value of 266 Yen in Japan for purchasing same quantity of the mentioned

drink. The difference between equilibrium and currency rate in 2015 is 67. This reflects that in

case of Spain also gap between currency and equilibrium exchange rate reduced in 2015 relative

to 2007.

(3) Difference between equilibrium rates of A and B and valuation of Euro according to PPP

There is difference between equilibrium rates in both cases A and B. In first case

equilibrium rate is 66.26 but in second case equilibrium rate is 65.96. This means that there is

difference in equilibrium rates when inflation rate of Germany and Spain are taken in to

consideration. However, this gap is minor 66.96-65.96= 0.3. This reflects that there is minor

difference in the exchange rate so it can be said that there is almost similarity in the equilibrium

rates of both cases. In both cases if currency exchange rate is compared with PPP rate then it can

be said that Euro is undervalued because one needs to pay higher amount then reflected by the

purchase power parity rate to buy 0.33 liter of cane of Coca Cola in Japan. In the next three to

four years Euro will become more stronger then Yen. One thing on which due attention must be

paid is that no one can make accurate prediction about the future economic conditions. In current

rate

inflation

rate

Coke/Pepsi

in Europe

Pepsi/Cok

e in Japan

um

exchange

rate

exchange rate

EURO- YEN

ce EER-

CER

2007 4.22% 0.70% 1.83 130.00 71.04 155 -84

2008 1.43% 0.39% 1.86 130.51 70.31 158 -87

2009 0.79% -1.67% 1.87 128.33 68.59 118 -49

2010 2.99% -0.40% 1.93 127.81 66.34 132 -64

2011 2.38% -0.20% 1.97 127.56 64.66 110 -44

2012 2.87% -0.10% 2.03 127.43 62.80 97 -32

2013 0.25% 1.61% 2.03 129.48 63.65 119 -54

2014 -1.04% 2.38% 2.01 132.56 65.85 141 -75

2015 0.02% 0.19% 2.01 132.82 65.96 133 -67

One that have Euro needs to pay higher amount in Japan to buy same quantity of Coca Cola

cane. The difference between equilibrium and currency exchange rate is 84. In 2015 equilibrium

exchange rate is 66.26 which means that one who is purchasing Coca Cola cane for 2 Euro needs

to pay equivalent value of 266 Yen in Japan for purchasing same quantity of the mentioned

drink. The difference between equilibrium and currency rate in 2015 is 67. This reflects that in

case of Spain also gap between currency and equilibrium exchange rate reduced in 2015 relative

to 2007.

(3) Difference between equilibrium rates of A and B and valuation of Euro according to PPP

There is difference between equilibrium rates in both cases A and B. In first case

equilibrium rate is 66.26 but in second case equilibrium rate is 65.96. This means that there is

difference in equilibrium rates when inflation rate of Germany and Spain are taken in to

consideration. However, this gap is minor 66.96-65.96= 0.3. This reflects that there is minor

difference in the exchange rate so it can be said that there is almost similarity in the equilibrium

rates of both cases. In both cases if currency exchange rate is compared with PPP rate then it can

be said that Euro is undervalued because one needs to pay higher amount then reflected by the

purchase power parity rate to buy 0.33 liter of cane of Coca Cola in Japan. In the next three to

four years Euro will become more stronger then Yen. One thing on which due attention must be

paid is that no one can make accurate prediction about the future economic conditions. In current

economic environment there are some very important things that are expected to be continue in

future time period (Inflation in Euro area, 2016). In Japan interest rates are reduced to negative

which means that earlier investors were receiving interest on deposits but now they will need to

deposit specific portion of there deposits with bank in order to maintain same in financial

institution. This will reduce return on bonds in which investors makes an investment. This will

encourage investors to sale there bonds and equity in the Japanese market because such kind of

policy reflects that economic environment of the nation is not congenial for investment. Hence,

demand for Euro will increase and in this way mentioned currency will become more stronger

then Yen in next three to four years (De Grauwe and Ji, 2013). This prediction is reliable because

Japan economy is facing problem of deflation for last two decades and in order to pump

investment in same such kind of policy is bring by Shinzo Abe government. It is anticipated that

this policy will be implemented in the market for long time period (EMU convergence criterion

bond yields, 2016). Economic condition of some European nations get improved. So on the basis

of current improvements in Europe condition and prediction of long term implementation of

negative interest rate policy it is anticipated that Euro will be stronger then Yen in next three to

four years.

future time period (Inflation in Euro area, 2016). In Japan interest rates are reduced to negative

which means that earlier investors were receiving interest on deposits but now they will need to

deposit specific portion of there deposits with bank in order to maintain same in financial

institution. This will reduce return on bonds in which investors makes an investment. This will

encourage investors to sale there bonds and equity in the Japanese market because such kind of

policy reflects that economic environment of the nation is not congenial for investment. Hence,

demand for Euro will increase and in this way mentioned currency will become more stronger

then Yen in next three to four years (De Grauwe and Ji, 2013). This prediction is reliable because

Japan economy is facing problem of deflation for last two decades and in order to pump

investment in same such kind of policy is bring by Shinzo Abe government. It is anticipated that

this policy will be implemented in the market for long time period (EMU convergence criterion

bond yields, 2016). Economic condition of some European nations get improved. So on the basis

of current improvements in Europe condition and prediction of long term implementation of

negative interest rate policy it is anticipated that Euro will be stronger then Yen in next three to

four years.

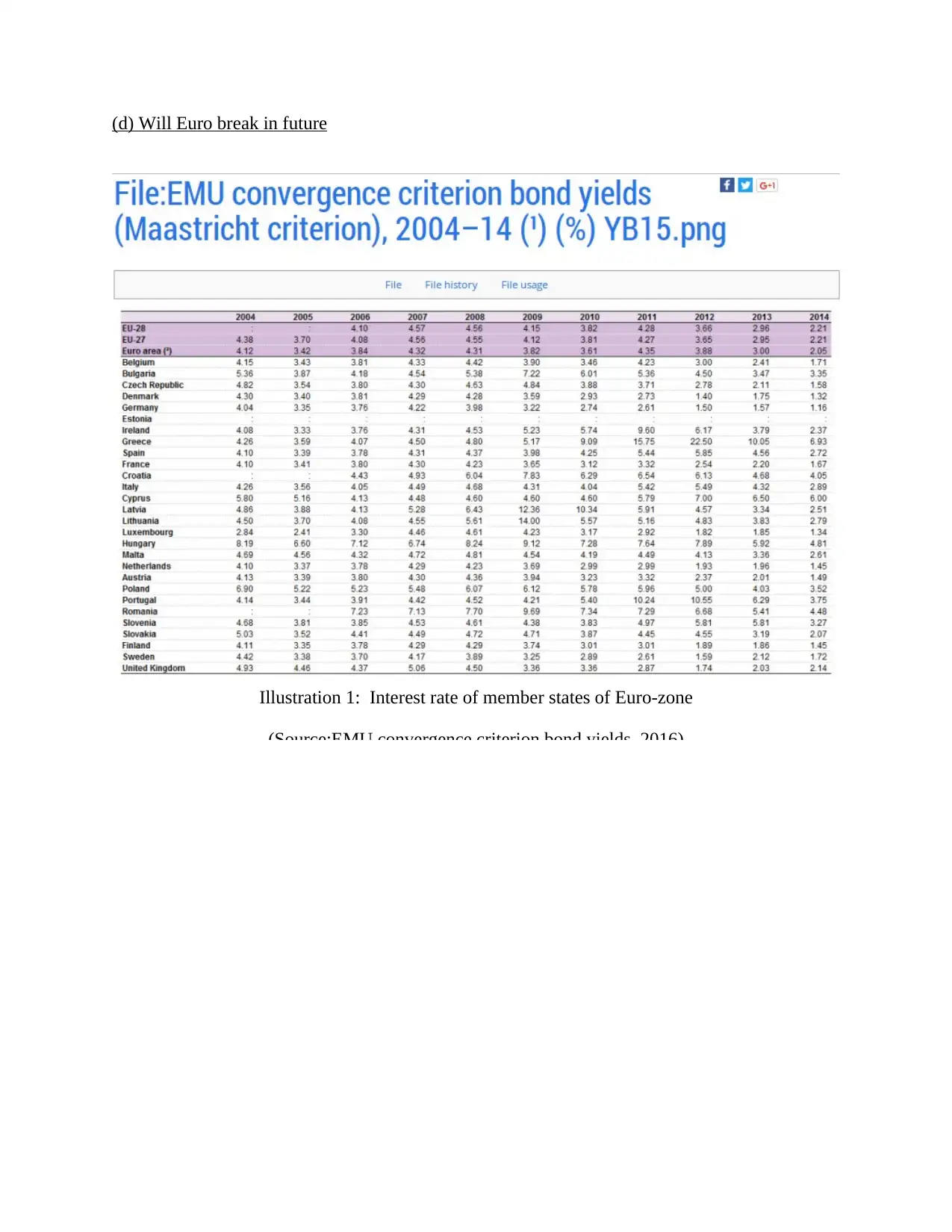

(d) Will Euro break in future

Illustration 1: Interest rate of member states of Euro-zone

(Source:EMU convergence criterion bond yields, 2016)

Illustration 1: Interest rate of member states of Euro-zone

(Source:EMU convergence criterion bond yields, 2016)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Difference in inflation rate is not significant enough to break Euro because there is not any big

difference between inflation rates prevailed across the nations in Euro-zone. If purchase power

parity model will be applied then it will be observed that there will very low PPP exchange rate.

Hence, inflation rate is not sufficient to break Euro. International Fisher model state the currency

exchange rate of two nations must be determined by using the difference that persists between

there interest rates. Huge gap is between interest rates of different member nations. If interest

rate is high inflation is on pick but if same rate is low then latter rate will also be very low. In

Europe single monetary policy is formulated that apply on all nations (Acharya and Steffen, S

2015). Difference in interest rates are clearly reflecting that there is huge difference in economic

conditions of member states. Hence, single monetary policy can not prove equally effective for

all countries that comes in Euro-zone. This is one of the main factor that makes it reasonable for

some member nations to quit Euro-zone. Those nations of Europe whose economy is in much

difference between inflation rates prevailed across the nations in Euro-zone. If purchase power

parity model will be applied then it will be observed that there will very low PPP exchange rate.

Hence, inflation rate is not sufficient to break Euro. International Fisher model state the currency

exchange rate of two nations must be determined by using the difference that persists between

there interest rates. Huge gap is between interest rates of different member nations. If interest

rate is high inflation is on pick but if same rate is low then latter rate will also be very low. In

Europe single monetary policy is formulated that apply on all nations (Acharya and Steffen, S

2015). Difference in interest rates are clearly reflecting that there is huge difference in economic

conditions of member states. Hence, single monetary policy can not prove equally effective for

all countries that comes in Euro-zone. This is one of the main factor that makes it reasonable for

some member nations to quit Euro-zone. Those nations of Europe whose economy is in much

better condition like Germany can not issue domestic currency. If they will be able to make use

of there currency then purchasing power of German people can be higher then other nations

people. Germany is not in conditions to reap this opportunity. Germany interest rate is only

1.16% which is very low in comparison to other nations. Hence, inflation is also low and if it

will be able to issue its own currency then same will appreciate and its people purchasing power

will also be high in comparison to other nations people. So, difference in interest rates in Euro-

zone are significant to break Euro in future.

Question 2

(2) Whether or not Euro will survive from recent Euro-zone crisis

In order to find out answer of “Whether or not Euro will survive” it is important to

evaluate structural issues faced by member nations and options available to them. Currently,

member nations of Euro-zone are facing serious problems specially after Britain decide to exit

from monetary union. Euro exchange rate is high in comparison to other currencies which put

negative impact directly on exports from Europe to nations that are in other continents of the

world. High value of Euro is put a destructive impact on the member nations. This is one side

from where being a member of European union nations are facing big problem (Fischer says

euro area can survive crisis, 2015). Second problem that is faced by member nations specially

Greece and those countries whose large potion of GDP is covered by debt is that finance

austerity is imposed on them by monetary union. Under finance austerity nations that have high

debt to GDP ratio are forced to increase tax rates and reduce public expenditure. So that situation

can be controlled. This put negative impact on member nations because due to elevation in tax

saving rate of people reduced and curtailment of public expenditures reduce monetary and non

monetary benefits that were received by people earlier. This entire scenario reduce demand and

foster anger among general public which become main cause responsible for unrest in the nation.

Hence, if any member nation exit from Euro-zone then it will be able to formulate its own policy

that best suits to relation to its economic condition (Lapavitsas, 2012). This may certainly

accelerate economic growth of the nation. This was one of the factor that motivate nations to exit

EU. There is common currency in the Europe which is Euro. As discussed earlier its value is

very high then other currencies of the world which is affecting exports of the member states. If

any member country leave EU then it will be able to issue its own currency and by devaluation

of there currency then purchasing power of German people can be higher then other nations

people. Germany is not in conditions to reap this opportunity. Germany interest rate is only

1.16% which is very low in comparison to other nations. Hence, inflation is also low and if it

will be able to issue its own currency then same will appreciate and its people purchasing power

will also be high in comparison to other nations people. So, difference in interest rates in Euro-

zone are significant to break Euro in future.

Question 2

(2) Whether or not Euro will survive from recent Euro-zone crisis

In order to find out answer of “Whether or not Euro will survive” it is important to

evaluate structural issues faced by member nations and options available to them. Currently,

member nations of Euro-zone are facing serious problems specially after Britain decide to exit

from monetary union. Euro exchange rate is high in comparison to other currencies which put

negative impact directly on exports from Europe to nations that are in other continents of the

world. High value of Euro is put a destructive impact on the member nations. This is one side

from where being a member of European union nations are facing big problem (Fischer says

euro area can survive crisis, 2015). Second problem that is faced by member nations specially

Greece and those countries whose large potion of GDP is covered by debt is that finance

austerity is imposed on them by monetary union. Under finance austerity nations that have high

debt to GDP ratio are forced to increase tax rates and reduce public expenditure. So that situation

can be controlled. This put negative impact on member nations because due to elevation in tax

saving rate of people reduced and curtailment of public expenditures reduce monetary and non

monetary benefits that were received by people earlier. This entire scenario reduce demand and

foster anger among general public which become main cause responsible for unrest in the nation.

Hence, if any member nation exit from Euro-zone then it will be able to formulate its own policy

that best suits to relation to its economic condition (Lapavitsas, 2012). This may certainly

accelerate economic growth of the nation. This was one of the factor that motivate nations to exit

EU. There is common currency in the Europe which is Euro. As discussed earlier its value is

very high then other currencies of the world which is affecting exports of the member states. If

any member country leave EU then it will be able to issue its own currency and by devaluation

of same it will increase export and will bring economy on track. These are two benefits that

nation will get by leaving membership of EU. These two ways can surely bring economy of the

European nations on track. In article “Euro can survive crisis” published in Financial times top

officer state that Euro can survive in crisis only when it will be able to bring prosperity in the

member states. Currently, some nations like Greece and Spain are facing stiff problem and

policies of European union is only creating problem for them and there people. EU policies are

not bringing prosperity instead it is creating complexities for the member nations. Solution to

handle situation (Currency devaluation and formulation of policies in own nation not in ECB

meetings) can be implemented only when membership will be leave by the nation in EU. This

reflects that EU will not survive because condition of member states are different from each

other and single monetary policy can not be effective for all nations (How Brexit may impact

European Union and the world, 2016). This evidenced from exit of Britain from EU. It is

difficult to identify the short term and medium term impact that exit of Britain will put on EU.

One thing is confirm that this incident will lead to origination of turmoil in the market which will

badly affect Euro-zone. Hence, it can be said that in future Euro may break because there are

number of factors that can act as motivating factor for member states to leave EU.

CONCLUSION

On the basis of findings of question 1 and question 2 it is concluded that in future Euro

may not survive because nations are facing lots of problems only because they are member of

EU. They are not able to prepare policies that best suit to there economic conditions. Apart from

this high currency rates also affect there export. Hence, in future some states may leave there

membership.

nation will get by leaving membership of EU. These two ways can surely bring economy of the

European nations on track. In article “Euro can survive crisis” published in Financial times top

officer state that Euro can survive in crisis only when it will be able to bring prosperity in the

member states. Currently, some nations like Greece and Spain are facing stiff problem and

policies of European union is only creating problem for them and there people. EU policies are

not bringing prosperity instead it is creating complexities for the member nations. Solution to

handle situation (Currency devaluation and formulation of policies in own nation not in ECB

meetings) can be implemented only when membership will be leave by the nation in EU. This

reflects that EU will not survive because condition of member states are different from each

other and single monetary policy can not be effective for all nations (How Brexit may impact

European Union and the world, 2016). This evidenced from exit of Britain from EU. It is

difficult to identify the short term and medium term impact that exit of Britain will put on EU.

One thing is confirm that this incident will lead to origination of turmoil in the market which will

badly affect Euro-zone. Hence, it can be said that in future Euro may break because there are

number of factors that can act as motivating factor for member states to leave EU.

CONCLUSION

On the basis of findings of question 1 and question 2 it is concluded that in future Euro

may not survive because nations are facing lots of problems only because they are member of

EU. They are not able to prepare policies that best suit to there economic conditions. Apart from

this high currency rates also affect there export. Hence, in future some states may leave there

membership.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

REFERENCES

Books & journals

Acharya, V.V. and Steffen, S., 2015. The “greatest” carry trade ever? Understanding eurozone

bank risks. Journal of Financial Economics. 115(2). pp.215-236.

Chen, R., Milesi-Ferretti, G.M. and Tressel, T., 2013. External imbalances in the eurozone.

Economic Policy. 28(73). pp.101-142.

De Grauwe, P. and Ji, Y., 2013. Self-fulfilling crises in the Eurozone: An empirical test. Journal

of International Money and Finance. 34. pp.15-36.

Lapavitsas, C., 2012. Crisis in the Eurozone. Verso Books.

Online

Cost of living in Germany, 2016. [Online]. Available through:< http://www.numbeo.com/cost-

of-living/country_result.jsp?country=Germany>. [Accessed on 13th August 2016].

Cost of living in Japan, 2016. [Online]. Available through:< http://www.numbeo.com/cost-of-

living/country_result.jsp?country=Japan>. [Accessed on 13th August 2016].

EMU convergence criterion bond yields, 2016. [Online]. Available through:<

c.europa.eu/eurostat/statisticsexplained/index.php/File:EMU_convergence_criterion_bon

d_yields_(Maastricht_criterion),_2004–14_(¹)_(%25)_YB15.png>. [Accessed on 13th

August 2016].

Fischer says euro area can survive crisis, 2015. [Online]. Available through:<

http://www.ft.com/cms/s/0/35fbe658-ffe5-11e4-abd5-

00144feabdc0.html#axzz4HBX7NOBR>. [Accessed on 13th August 2016].

How Brexit may impact European Union and the world, 2016. [Online]. Available

through:<http://blogs.economictimes.indiatimes.com/et-commentary/how-brexit-may-

impact-european-union-and-the-world/>. [Accessed on 13th August 2016].

Inflation in Euro area, 2016. [Online]. Available through:<

http://ec.europa.eu/eurostat/statistics-explained/index.php/Inflation_in_the_euro_area>.

[Accessed on 13th August 2016].

Books & journals

Acharya, V.V. and Steffen, S., 2015. The “greatest” carry trade ever? Understanding eurozone

bank risks. Journal of Financial Economics. 115(2). pp.215-236.

Chen, R., Milesi-Ferretti, G.M. and Tressel, T., 2013. External imbalances in the eurozone.

Economic Policy. 28(73). pp.101-142.

De Grauwe, P. and Ji, Y., 2013. Self-fulfilling crises in the Eurozone: An empirical test. Journal

of International Money and Finance. 34. pp.15-36.

Lapavitsas, C., 2012. Crisis in the Eurozone. Verso Books.

Online

Cost of living in Germany, 2016. [Online]. Available through:< http://www.numbeo.com/cost-

of-living/country_result.jsp?country=Germany>. [Accessed on 13th August 2016].

Cost of living in Japan, 2016. [Online]. Available through:< http://www.numbeo.com/cost-of-

living/country_result.jsp?country=Japan>. [Accessed on 13th August 2016].

EMU convergence criterion bond yields, 2016. [Online]. Available through:<

c.europa.eu/eurostat/statisticsexplained/index.php/File:EMU_convergence_criterion_bon

d_yields_(Maastricht_criterion),_2004–14_(¹)_(%25)_YB15.png>. [Accessed on 13th

August 2016].

Fischer says euro area can survive crisis, 2015. [Online]. Available through:<

http://www.ft.com/cms/s/0/35fbe658-ffe5-11e4-abd5-

00144feabdc0.html#axzz4HBX7NOBR>. [Accessed on 13th August 2016].

How Brexit may impact European Union and the world, 2016. [Online]. Available

through:<http://blogs.economictimes.indiatimes.com/et-commentary/how-brexit-may-

impact-european-union-and-the-world/>. [Accessed on 13th August 2016].

Inflation in Euro area, 2016. [Online]. Available through:<

http://ec.europa.eu/eurostat/statistics-explained/index.php/Inflation_in_the_euro_area>.

[Accessed on 13th August 2016].

1 out of 11

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.