HA 3011: Financial Accounting - Impairment and Lease Standard Analysis

VerifiedAdded on 2024/04/25

|18

|2907

|451

Report

AI Summary

This report provides a comprehensive analysis of financial accounting practices, focusing on impairment testing and lease accounting standards, using Qantas Airways Limited as a case study. Part A examines Qantas's asset impairment testing, including tangible and intangible assets, key estimates, and assumptions, highlighting the subjectivity involved in the process. Part B delves into the IASB's proposed changes to lease accounting standards, explaining why the former standard was deemed unrealistic and the implications of the new standard on companies' financial reporting, particularly regarding off-balance sheet liabilities and comparability among airline companies. The report concludes by emphasizing the potential impact of the new standard on companies' economic decisions and the importance of fair value measurement in impairment testing. Desklib offers a range of solved assignments and past papers to aid students in their studies.

HA 3011 Advanced Financial Accounting

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Introduction:...............................................................................................................................3

Part A:........................................................................................................................................4

1..............................................................................................................................................4

2..............................................................................................................................................5

3..............................................................................................................................................6

4..............................................................................................................................................7

5..............................................................................................................................................8

6..............................................................................................................................................9

7............................................................................................................................................10

8............................................................................................................................................11

Part B:.......................................................................................................................................12

1............................................................................................................................................12

2............................................................................................................................................13

3............................................................................................................................................14

4............................................................................................................................................15

5............................................................................................................................................16

Conclusion:..............................................................................................................................17

Bibliography.............................................................................................................................18

2

Introduction:...............................................................................................................................3

Part A:........................................................................................................................................4

1..............................................................................................................................................4

2..............................................................................................................................................5

3..............................................................................................................................................6

4..............................................................................................................................................7

5..............................................................................................................................................8

6..............................................................................................................................................9

7............................................................................................................................................10

8............................................................................................................................................11

Part B:.......................................................................................................................................12

1............................................................................................................................................12

2............................................................................................................................................13

3............................................................................................................................................14

4............................................................................................................................................15

5............................................................................................................................................16

Conclusion:..............................................................................................................................17

Bibliography.............................................................................................................................18

2

Introduction:

The report is made for getting a brief understanding of the financial accounting operations

conducted in the enterprise and analysing the treatment of impairment of assets of the

company. In order to achieve this purpose, Qantas Airways Limited has been taken as the

company which is an Australian airline company and has been considered to be the largest by

fleet size in Australia. The airline provides various services in the air travel providing

international and domestic travels across the world. The criteria adopted by the company in

impairing its assets and the analysis of the treatment in light of various estimations and

assumptions made by the company will be evaluated for corrective purposes. In the second

part of the report, an understanding will be obtained about the various comments received by

the chairman of IASB in order to adopt the new lease standard in the corporate framework of

company. This will give a brief understanding of the various concepts and fundamentals

issues related to financial accounting in the business environment.

3

The report is made for getting a brief understanding of the financial accounting operations

conducted in the enterprise and analysing the treatment of impairment of assets of the

company. In order to achieve this purpose, Qantas Airways Limited has been taken as the

company which is an Australian airline company and has been considered to be the largest by

fleet size in Australia. The airline provides various services in the air travel providing

international and domestic travels across the world. The criteria adopted by the company in

impairing its assets and the analysis of the treatment in light of various estimations and

assumptions made by the company will be evaluated for corrective purposes. In the second

part of the report, an understanding will be obtained about the various comments received by

the chairman of IASB in order to adopt the new lease standard in the corporate framework of

company. This will give a brief understanding of the various concepts and fundamentals

issues related to financial accounting in the business environment.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Part A:

1.

From your firm’s annual report find out the assets that your firm has tested for

impairment

As per the annual report of the company, Qantas Airways Limited presented for the year

2017 it can be established that the impairment has been conducted on the financial as well as

nonfinancial assets of the company forming part of the balance sheet of the company for the

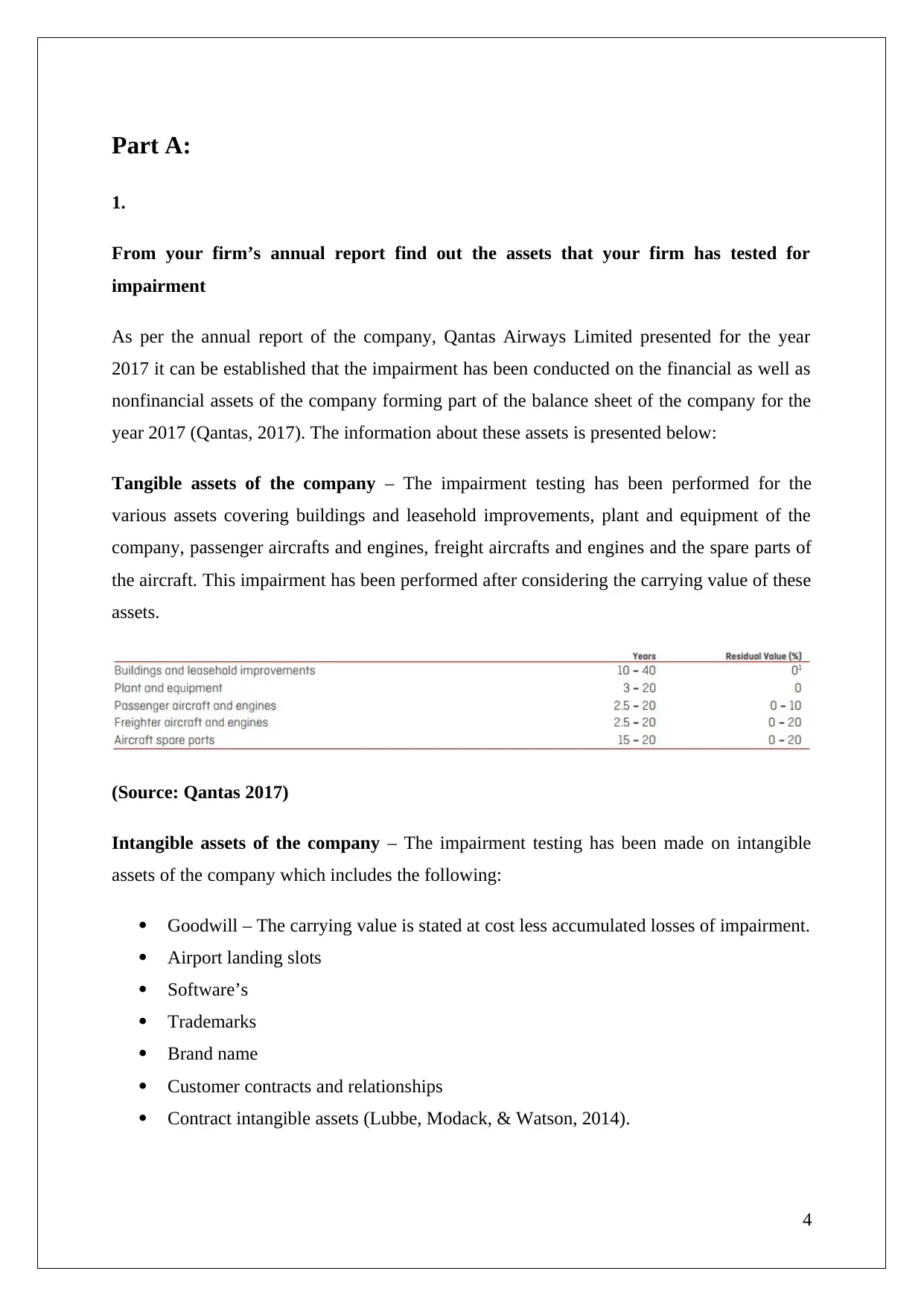

year 2017 (Qantas, 2017). The information about these assets is presented below:

Tangible assets of the company – The impairment testing has been performed for the

various assets covering buildings and leasehold improvements, plant and equipment of the

company, passenger aircrafts and engines, freight aircrafts and engines and the spare parts of

the aircraft. This impairment has been performed after considering the carrying value of these

assets.

(Source: Qantas 2017)

Intangible assets of the company – The impairment testing has been made on intangible

assets of the company which includes the following:

Goodwill – The carrying value is stated at cost less accumulated losses of impairment.

Airport landing slots

Software’s

Trademarks

Brand name

Customer contracts and relationships

Contract intangible assets (Lubbe, Modack, & Watson, 2014).

4

1.

From your firm’s annual report find out the assets that your firm has tested for

impairment

As per the annual report of the company, Qantas Airways Limited presented for the year

2017 it can be established that the impairment has been conducted on the financial as well as

nonfinancial assets of the company forming part of the balance sheet of the company for the

year 2017 (Qantas, 2017). The information about these assets is presented below:

Tangible assets of the company – The impairment testing has been performed for the

various assets covering buildings and leasehold improvements, plant and equipment of the

company, passenger aircrafts and engines, freight aircrafts and engines and the spare parts of

the aircraft. This impairment has been performed after considering the carrying value of these

assets.

(Source: Qantas 2017)

Intangible assets of the company – The impairment testing has been made on intangible

assets of the company which includes the following:

Goodwill – The carrying value is stated at cost less accumulated losses of impairment.

Airport landing slots

Software’s

Trademarks

Brand name

Customer contracts and relationships

Contract intangible assets (Lubbe, Modack, & Watson, 2014).

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2.

How did your firm conduct the impairment testing?

The impairment testing in the company has been conducted after identifying the cash

generating unit which can generate cash for the future years of the company and capable of

being recognized as the income producing unit of the company. The identification of this

cash generating unit of the company requires judgment to be made regarding how managers

consider the operations of Qantas Group and the decisions to be made about the acquisition

of assets has been made by the management (Hoyle, Schaefer, & Doupnik, 2015). The

management of the company has identified a lowest identifiable group of cash generating unit

which can generate cash flows being Qantas International, Qantas Domestic, Qantas Freight,

Qantas Loyalty and the Jet star Group CGUs

5

How did your firm conduct the impairment testing?

The impairment testing in the company has been conducted after identifying the cash

generating unit which can generate cash for the future years of the company and capable of

being recognized as the income producing unit of the company. The identification of this

cash generating unit of the company requires judgment to be made regarding how managers

consider the operations of Qantas Group and the decisions to be made about the acquisition

of assets has been made by the management (Hoyle, Schaefer, & Doupnik, 2015). The

management of the company has identified a lowest identifiable group of cash generating unit

which can generate cash flows being Qantas International, Qantas Domestic, Qantas Freight,

Qantas Loyalty and the Jet star Group CGUs

5

3.

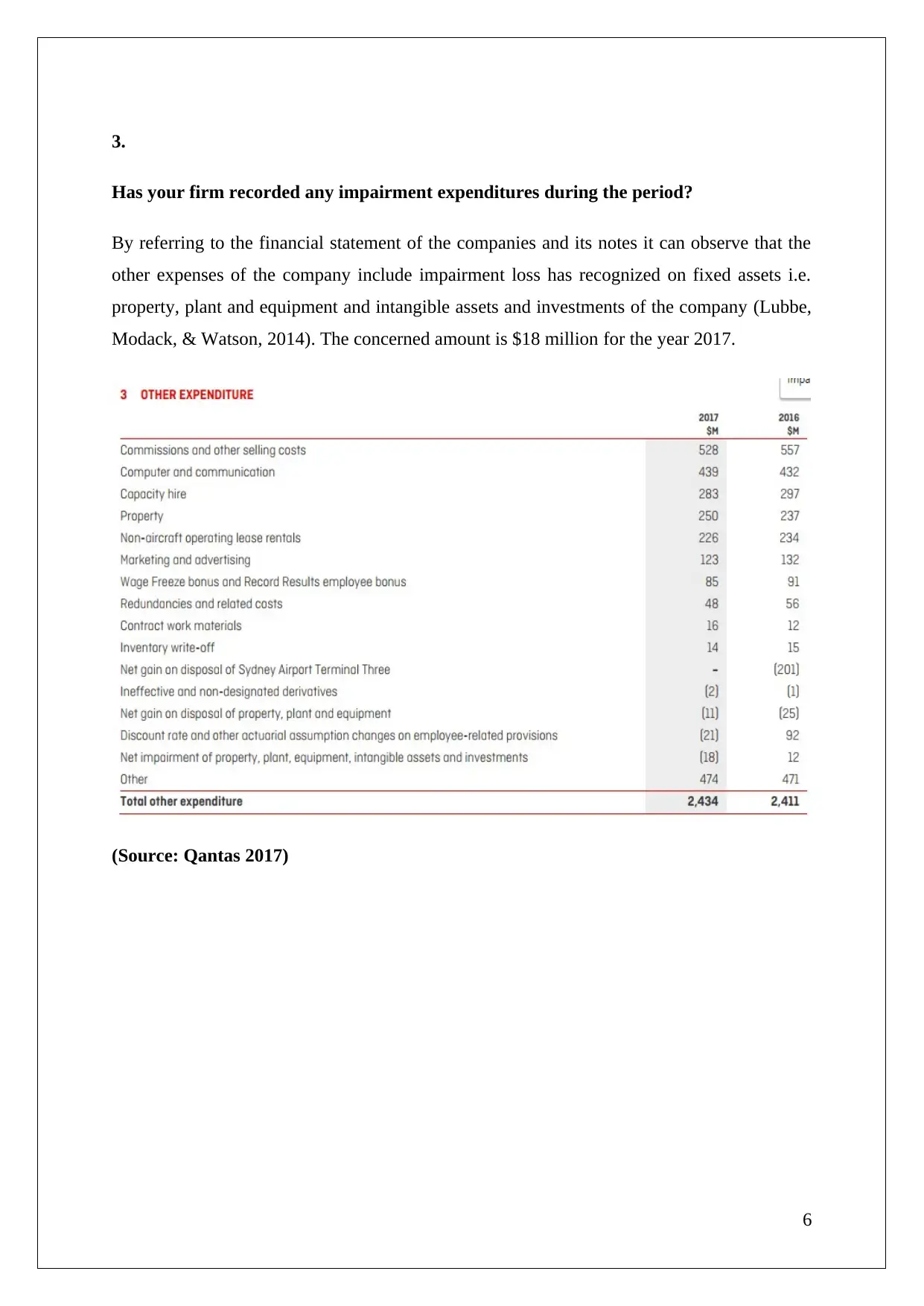

Has your firm recorded any impairment expenditures during the period?

By referring to the financial statement of the companies and its notes it can observe that the

other expenses of the company include impairment loss has recognized on fixed assets i.e.

property, plant and equipment and intangible assets and investments of the company (Lubbe,

Modack, & Watson, 2014). The concerned amount is $18 million for the year 2017.

(Source: Qantas 2017)

6

Has your firm recorded any impairment expenditures during the period?

By referring to the financial statement of the companies and its notes it can observe that the

other expenses of the company include impairment loss has recognized on fixed assets i.e.

property, plant and equipment and intangible assets and investments of the company (Lubbe,

Modack, & Watson, 2014). The concerned amount is $18 million for the year 2017.

(Source: Qantas 2017)

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4.

Identify the key estimates and assumptions used by your firm in conducting the

impairment testing.

The various assumptions and estimations are explained below:

Determination of value in use – The value in use recognized for the cash-generating unit

has-been calculated by discounted cash flow which can be obtained from continuous use of

the assets of the company and following assumptions has been made for the same:

The cash flows were forecasted considering the approved projected plan of the

company. Cash flows to decide a terminal value were extrapolated while using a constant

development rate of 2.5% p.a. which does not surpass the long-term average growth rate

for the industry. The cash outflows of the company which includes the purchase of

aircraft and other tangible assets do not include any of the capital expenditure which will

enhance the existing performance of the assets and the cash flows (Carlin & Finch, 2011).

Discounting rate – The discounting rate which has been considered for discounting

the cash flows of the cash generating unit has been considered to be 10% as pre-tax

discount rate. The same has been calculated after considering the market structure and the

weighted average cost of capital of the company. The discount rate is based on the risk-

free rate for 10-year Australian Government Bonds accustomed to a risk premium for

reflecting both the increased risk of investing in equities and the risk of the specific CGU.

Recognition and measurement – The intangible assets, as well as tangible assets of the

company, has been recognized at the carrying value less accumulated depreciation and other

accumulated impairment losses which are separate fro separate assets f the company.

Useful lives of the assets – The determination of the useful lives of the assets is based on the

management interpretation and judgment and the same has been determined after considering

the various policies and standards (Logeswary & Velnampy, 2014).

7

Identify the key estimates and assumptions used by your firm in conducting the

impairment testing.

The various assumptions and estimations are explained below:

Determination of value in use – The value in use recognized for the cash-generating unit

has-been calculated by discounted cash flow which can be obtained from continuous use of

the assets of the company and following assumptions has been made for the same:

The cash flows were forecasted considering the approved projected plan of the

company. Cash flows to decide a terminal value were extrapolated while using a constant

development rate of 2.5% p.a. which does not surpass the long-term average growth rate

for the industry. The cash outflows of the company which includes the purchase of

aircraft and other tangible assets do not include any of the capital expenditure which will

enhance the existing performance of the assets and the cash flows (Carlin & Finch, 2011).

Discounting rate – The discounting rate which has been considered for discounting

the cash flows of the cash generating unit has been considered to be 10% as pre-tax

discount rate. The same has been calculated after considering the market structure and the

weighted average cost of capital of the company. The discount rate is based on the risk-

free rate for 10-year Australian Government Bonds accustomed to a risk premium for

reflecting both the increased risk of investing in equities and the risk of the specific CGU.

Recognition and measurement – The intangible assets, as well as tangible assets of the

company, has been recognized at the carrying value less accumulated depreciation and other

accumulated impairment losses which are separate fro separate assets f the company.

Useful lives of the assets – The determination of the useful lives of the assets is based on the

management interpretation and judgment and the same has been determined after considering

the various policies and standards (Logeswary & Velnampy, 2014).

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5.

Do you find any sort of subjectivity involved in the impairment testing process? How

can this subjectivity influence the outcome of the impairment testing?

Yes by analysing the current treatment of the impairment loss to be recognized by the

company in its financial statements it can be observed that the management has to make

certain kinds of assumptions an estimations which are based on the perception of the

management about the future growth rate and performance of the company in respect of

market factors and therefore there is lot of subjectivity involved in impairment process of the

company (Lubbe, Modack, & Watson, 2014).

8

Do you find any sort of subjectivity involved in the impairment testing process? How

can this subjectivity influence the outcome of the impairment testing?

Yes by analysing the current treatment of the impairment loss to be recognized by the

company in its financial statements it can be observed that the management has to make

certain kinds of assumptions an estimations which are based on the perception of the

management about the future growth rate and performance of the company in respect of

market factors and therefore there is lot of subjectivity involved in impairment process of the

company (Lubbe, Modack, & Watson, 2014).

8

6.

What do you find interesting, confusing, surprising or difficult to understand about the

impairment testing?

It is interesting to note the recognition and measurement of various intangible assets of the

company which have been carried at the historical values less accumulated impairment loss.

The useful lives of these assets and the depreciation rates applicable to these assets have been

carefully adopted by the company but there exists some confusion regarding their accuracy

and correctness (Hoyle, Schaefer, & Doupnik, 2015).

9

What do you find interesting, confusing, surprising or difficult to understand about the

impairment testing?

It is interesting to note the recognition and measurement of various intangible assets of the

company which have been carried at the historical values less accumulated impairment loss.

The useful lives of these assets and the depreciation rates applicable to these assets have been

carefully adopted by the company but there exists some confusion regarding their accuracy

and correctness (Hoyle, Schaefer, & Doupnik, 2015).

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7.

What new insights, if any, have you gained about how companies conduct impairment

testing?

The phenomenon which can be established form the analysis of the impairment testing

conducted by modern companies is that the companies are adopting innovative of accounting

and adopting various standards for recognizing the correct and accurate value of the assets of

company. In order to fulfil these criteria, a new concept of considering the cash generating

unit has emerged which allows the more transparent view to be adopted for impairment

treatment of the company (Khokan Bepari, Rahman, & Taher Mollik, 2014).

10

What new insights, if any, have you gained about how companies conduct impairment

testing?

The phenomenon which can be established form the analysis of the impairment testing

conducted by modern companies is that the companies are adopting innovative of accounting

and adopting various standards for recognizing the correct and accurate value of the assets of

company. In order to fulfil these criteria, a new concept of considering the cash generating

unit has emerged which allows the more transparent view to be adopted for impairment

treatment of the company (Khokan Bepari, Rahman, & Taher Mollik, 2014).

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8.

Based on your assignment, comment on the “fair value measurement”.

Fair value measurement in impairment testing is of critical importance as the estimation of

this value helps in obtaining the recoverable amount of the concerned asset of company

which will form part of the cash generating unit. The fair value refers to the amount to be

obtained by the seller of the asset by selling or transferring the same to an independent buyer

in the market. In other words, it can be referred to the sale value of the asset in the market

way-out any biased conditions. The recognition of same is significant as it can impact the

impairment loss to be recognized by the company (Carlin & Finch, 2011).

11

Based on your assignment, comment on the “fair value measurement”.

Fair value measurement in impairment testing is of critical importance as the estimation of

this value helps in obtaining the recoverable amount of the concerned asset of company

which will form part of the cash generating unit. The fair value refers to the amount to be

obtained by the seller of the asset by selling or transferring the same to an independent buyer

in the market. In other words, it can be referred to the sale value of the asset in the market

way-out any biased conditions. The recognition of same is significant as it can impact the

impairment loss to be recognized by the company (Carlin & Finch, 2011).

11

Part B:

Introduction:

IASB is planning to change the current lease accounting standard and its applicability in the

valuing companies fixed assets and liabilities. The current lease accounting standard allows

organisations to presents good financial figures and presents a more lucrative statement to

investors. Thus, IASB has sorted some changes in it and that is reflected in the following

answers.

1.

Explain why the chairperson of the IASB believes that the former accounting standard

for leases did ‘not reflect economic reality’?

The article presents that there were large big retail chains that had large and long operating

leases (debts) but easily presents clean financial statements with no such high debts. Such

practice does not present true economic reality and financial situations of companies. Thus,

the chairman has presented its views that the financial statement (specifically statement of

financial position) does not present true economic reality (DiSalvio, 2014).

The companies in the past were recognizing all the leases as operating leases which resulted

in a wrong presentation of the financial position of company as not all the dents considering

the financial lease liability of the company has been represented in the company’s financial

statements.

12

Introduction:

IASB is planning to change the current lease accounting standard and its applicability in the

valuing companies fixed assets and liabilities. The current lease accounting standard allows

organisations to presents good financial figures and presents a more lucrative statement to

investors. Thus, IASB has sorted some changes in it and that is reflected in the following

answers.

1.

Explain why the chairperson of the IASB believes that the former accounting standard

for leases did ‘not reflect economic reality’?

The article presents that there were large big retail chains that had large and long operating

leases (debts) but easily presents clean financial statements with no such high debts. Such

practice does not present true economic reality and financial situations of companies. Thus,

the chairman has presented its views that the financial statement (specifically statement of

financial position) does not present true economic reality (DiSalvio, 2014).

The companies in the past were recognizing all the leases as operating leases which resulted

in a wrong presentation of the financial position of company as not all the dents considering

the financial lease liability of the company has been represented in the company’s financial

statements.

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.