Internal Control Weaknesses in Expenditure Cycle of Adam & Co

Added on 2022-11-03

12 Pages2543 Words222 Views

HA2042

Case Study – Adam & Co

Student name

Student Id

Case Study – Adam & Co

Student name

Student Id

1

TABLE OF CONTENTS

TOPIC PAGE NUMBER

Executive summary 2

Introduction 2-3

System flowchart of purchases system 2

Internal control weaknesses in the Purchase

system

4-5

System flowchart of cash disbursement system 6

Internal control weaknesses in the cash dis-

bursement system

7

System flowchart of payroll system 8

Internal control weaknesses in the payroll sys-

tem

9

Conclusion 10

References 11

TABLE OF CONTENTS

TOPIC PAGE NUMBER

Executive summary 2

Introduction 2-3

System flowchart of purchases system 2

Internal control weaknesses in the Purchase

system

4-5

System flowchart of cash disbursement system 6

Internal control weaknesses in the cash dis-

bursement system

7

System flowchart of payroll system 8

Internal control weaknesses in the payroll sys-

tem

9

Conclusion 10

References 11

2

EXECUTIVE SUMMARY

A Perth-based wholesaler of industrial supplies, Adam & Co, outsources its inventories from the

manufacturers in countries such as China, Thailand and Vietnam. Being a business Analyst, I

have been given the task of analyzing the expenditure cycle of the company. The company’s ex-

penses are operated using a centralized accounting system software with the networking termi-

nals at different locations. Purchasing clerk, receivable clerk and accounts payable clerk are in-

cluded in the purchase system of the company for deliberately keeping an eye on the overall

process, that is, from checking the inventory to updating accounts and ledgers, preparing com-

pany reports and sending it to cash disbursement department where the clerk would be held re-

sponsible for keeping checks and updating systems. The whole payroll process in accounts

payable department and the payroll department are operated under the surveillance of the clerks.

A close observance of the weaknesses in the internal control of the expenditure systems deter-

mines the risks associated, which generally includes financial losses, debt accumulation, reputa-

tion loss etc. which are normally incidental to a business.

INTRODUCTION

The expenditure at Adam & Co, is carried along using a centralized accounting system with net-

working terminal software at different locations. There are specific systems installed with respect

to purchase, cash disbursement and payroll functions which are followed as per the company

policies and regulations. On keeping a close track of the processes, it is observed that all the

three exhibited expenditure processes primarily including internal control weaknesses needs to

be removed by conducting regular and random audits.

The report starts with a review of the literature stating the important internal control techniques

and benefits of conducting audits. This report also lays down to identify the internal control

weaknesses in each of the three expenditure systems and the risk associated with those weak-

nesses.

Zhang, Zhou and Zhou (2007) defined internal control as “a process, effected by an

entity's board of directors, management and other personnel, designed to provide

reasonable assurance regarding the achievement of objectives”.

2 | Page

EXECUTIVE SUMMARY

A Perth-based wholesaler of industrial supplies, Adam & Co, outsources its inventories from the

manufacturers in countries such as China, Thailand and Vietnam. Being a business Analyst, I

have been given the task of analyzing the expenditure cycle of the company. The company’s ex-

penses are operated using a centralized accounting system software with the networking termi-

nals at different locations. Purchasing clerk, receivable clerk and accounts payable clerk are in-

cluded in the purchase system of the company for deliberately keeping an eye on the overall

process, that is, from checking the inventory to updating accounts and ledgers, preparing com-

pany reports and sending it to cash disbursement department where the clerk would be held re-

sponsible for keeping checks and updating systems. The whole payroll process in accounts

payable department and the payroll department are operated under the surveillance of the clerks.

A close observance of the weaknesses in the internal control of the expenditure systems deter-

mines the risks associated, which generally includes financial losses, debt accumulation, reputa-

tion loss etc. which are normally incidental to a business.

INTRODUCTION

The expenditure at Adam & Co, is carried along using a centralized accounting system with net-

working terminal software at different locations. There are specific systems installed with respect

to purchase, cash disbursement and payroll functions which are followed as per the company

policies and regulations. On keeping a close track of the processes, it is observed that all the

three exhibited expenditure processes primarily including internal control weaknesses needs to

be removed by conducting regular and random audits.

The report starts with a review of the literature stating the important internal control techniques

and benefits of conducting audits. This report also lays down to identify the internal control

weaknesses in each of the three expenditure systems and the risk associated with those weak-

nesses.

Zhang, Zhou and Zhou (2007) defined internal control as “a process, effected by an

entity's board of directors, management and other personnel, designed to provide

reasonable assurance regarding the achievement of objectives”.

2 | Page

3

The large private companies in Australia, are forced to conduct the audits (Carey, Simnett and

Tanewski, 2000) On the contrary, the research has shown that carrying out the voluntary audits

is beneficial to the organisation.

In the assurance of the corporate accountability, auditing forepays primarily giving the accurate

financial report (Carcello and Neal, 2000) and an important governance mechanism (Zhang et

al., 2007).

Blackwell et al. (2008) had laid in their study that 37% of the private firms independantly au-

dited in the US. Lower interest rates are paid by these firms significantly on rotating the bank

loans than the unaudited firms. Minnis (2011) reported that auditing lowers down the asymme-

try in information by improving the ability of the expected net income for future cash flows,

thereby reducing the firm’s cost of debt with audited financial statements in opposition to the

unaudited financial statements.

At last, the audits of the private company are economically fruitful by giving the lower interest

rates on debt, thereby increasing the credit ratings and always trying to have better access to

credit (Lennox and Pittman, 2011).

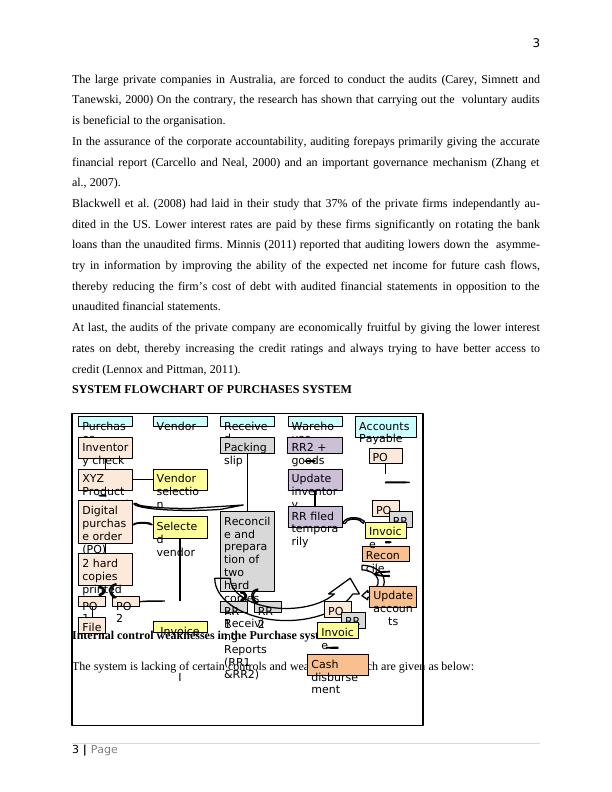

SYSTEM FLOWCHART OF PURCHASES SYSTEM

Internal control weaknesses in the Purchase system

The system is lacking of certain controls and weaknesses which are given as below:

3 | Page

Purchas

es

Inventor

y check

XYZ

Product

required

Vendor Receive

d

Wareho

use

Accounts

Payable

Vendor

selectio

n

Digital

purchas

e order

(PO)

created2 hard

copies

printed

PO

1

PO

2

Selecte

d

vendor

File Invoice

I

Packing

slip

Reconcil

e and

prepara

tion of

two

hard

copies

of

Receivi

ng

Reports

(RR1

&RR2)

RR

1

RR

2

RR2 +

goods

Update

inventor

y

RR filed

tempora

rily

PO

Recon

cile

PO RR

Invoic

e

Cash

disburse

ment

Update

accoun

ts

PO RR

Invoic

e

The large private companies in Australia, are forced to conduct the audits (Carey, Simnett and

Tanewski, 2000) On the contrary, the research has shown that carrying out the voluntary audits

is beneficial to the organisation.

In the assurance of the corporate accountability, auditing forepays primarily giving the accurate

financial report (Carcello and Neal, 2000) and an important governance mechanism (Zhang et

al., 2007).

Blackwell et al. (2008) had laid in their study that 37% of the private firms independantly au-

dited in the US. Lower interest rates are paid by these firms significantly on rotating the bank

loans than the unaudited firms. Minnis (2011) reported that auditing lowers down the asymme-

try in information by improving the ability of the expected net income for future cash flows,

thereby reducing the firm’s cost of debt with audited financial statements in opposition to the

unaudited financial statements.

At last, the audits of the private company are economically fruitful by giving the lower interest

rates on debt, thereby increasing the credit ratings and always trying to have better access to

credit (Lennox and Pittman, 2011).

SYSTEM FLOWCHART OF PURCHASES SYSTEM

Internal control weaknesses in the Purchase system

The system is lacking of certain controls and weaknesses which are given as below:

3 | Page

Purchas

es

Inventor

y check

XYZ

Product

required

Vendor Receive

d

Wareho

use

Accounts

Payable

Vendor

selectio

n

Digital

purchas

e order

(PO)

created2 hard

copies

printed

PO

1

PO

2

Selecte

d

vendor

File Invoice

I

Packing

slip

Reconcil

e and

prepara

tion of

two

hard

copies

of

Receivi

ng

Reports

(RR1

&RR2)

RR

1

RR

2

RR2 +

goods

Update

inventor

y

RR filed

tempora

rily

PO

Recon

cile

PO RR

Invoic

e

Cash

disburse

ment

Update

accoun

ts

PO RR

Invoic

e

End of preview

Want to access all the pages? Upload your documents or become a member.

Related Documents

Case Study - Adam & Co.lg...

|10

|2756

|119

Case Study - Adam & Co: Evaluation of Internal Control Systemlg...

|15

|3252

|333

Expenditure Cycle of Adam & Co.lg...

|14

|2429

|339

Accounting Information System 14lg...

|14

|2633

|66

The analysis has identified the problemslg...

|13

|2979

|31

Analysis of Internal Control Weaknesses in Adam & Co.'s Expenditure Cyclelg...

|17

|3472

|343