HA3032 Auditing Final Assessment T2 2021

VerifiedAdded on 2023/06/18

|10

|2701

|356

AI Summary

This assessment consists of six (6) questions and is designed to assess your level of knowledge of the key topics covered in this unit. The questions cover topics such as materiality, audit risk model, independence, audit procedures, subsequent events, and audit opinion. The subject is HA3032 Auditing and the course code is not mentioned. The course name is Auditing and the college/university is not mentioned.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Student Number: (enter on the line below)

Student Name: (enter on the line below)

HA3032

AUDITING

FINAL ASSESSMENT

TRIMESTER T2, 2021

Assessment Weight: 50 total marks

Instructions:

All questions must be answered by using the answer boxes provided in this paper.

Completed answers must be submitted to Blackboard by the published due date

and time.

Submission instructions are at the end of this paper.

Purpose:

This assessment consists of six (6) questions and is designed to assess your level of

knowledge of the key topics covered in this unit

HA3032 – Auditing - Final Assessment T2 2021

Student Name: (enter on the line below)

HA3032

AUDITING

FINAL ASSESSMENT

TRIMESTER T2, 2021

Assessment Weight: 50 total marks

Instructions:

All questions must be answered by using the answer boxes provided in this paper.

Completed answers must be submitted to Blackboard by the published due date

and time.

Submission instructions are at the end of this paper.

Purpose:

This assessment consists of six (6) questions and is designed to assess your level of

knowledge of the key topics covered in this unit

HA3032 – Auditing - Final Assessment T2 2021

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Question 1 – Materiality (7 marks)

As stated in ASA 320;

“The auditor’s determination of materiality is a matter of professional judgement, and is affected

by the auditor’s perception of the financial information needs of users of the financial report.”

(AUASB, 2015)

With reference to the statement above from ASA 320, define materiality and discuss how the

“needs of users” will affect how materiality is determined.

ANSWER: ** Answer box will enlarge as you type

Materiality in audit is being defined as the convention which relates with accounting and

auditing signifying its importance and inclusion of all material information within the working.

The reason underlying this fact is that with help of inclusion of material information all this will

present the actual working position of the company. The need of users affects the materiality

level which is being defined by the company. The reason pertaining to the fact is that there are

many different types of the users of financial statement and in case all the material information

will be provided then this will assist users in taking proper decision. For instance, investor is a

user of accounting information and when auditor states that all the information provided is

correct and material then this will motivate investor to invest within the company.

Question 2 - Audit Risk Model (7 marks)

What is the purpose of tests of controls? With reference to the three (3) main risk components

of the Audit Risk Model, explain the circumstances where it is NOT appropriate for the Auditor

to test the controls of the client entity.

ANSWER:

The purpose of test of control in audit is to determine the fact that whether the internal control

of the company is enough to detect or to prevent the various types of risk relating to material

misstatement. On the basis of audit risk model, there are three risk that is inherent, detection

and control risk. Thus, out of these, the circumstance wherein it is not appropriate for the

auditor for test control of client is control risk. The reason pertaining to the fact is that in case

the control is not effective then it can result in high risk. Thus, here the test of control can be

skipped and it reveals ineffectviness of control system.

Question 3 – Independence (7 marks)

HA3032 – Auditing - Final Assessment T2 2021

As stated in ASA 320;

“The auditor’s determination of materiality is a matter of professional judgement, and is affected

by the auditor’s perception of the financial information needs of users of the financial report.”

(AUASB, 2015)

With reference to the statement above from ASA 320, define materiality and discuss how the

“needs of users” will affect how materiality is determined.

ANSWER: ** Answer box will enlarge as you type

Materiality in audit is being defined as the convention which relates with accounting and

auditing signifying its importance and inclusion of all material information within the working.

The reason underlying this fact is that with help of inclusion of material information all this will

present the actual working position of the company. The need of users affects the materiality

level which is being defined by the company. The reason pertaining to the fact is that there are

many different types of the users of financial statement and in case all the material information

will be provided then this will assist users in taking proper decision. For instance, investor is a

user of accounting information and when auditor states that all the information provided is

correct and material then this will motivate investor to invest within the company.

Question 2 - Audit Risk Model (7 marks)

What is the purpose of tests of controls? With reference to the three (3) main risk components

of the Audit Risk Model, explain the circumstances where it is NOT appropriate for the Auditor

to test the controls of the client entity.

ANSWER:

The purpose of test of control in audit is to determine the fact that whether the internal control

of the company is enough to detect or to prevent the various types of risk relating to material

misstatement. On the basis of audit risk model, there are three risk that is inherent, detection

and control risk. Thus, out of these, the circumstance wherein it is not appropriate for the

auditor for test control of client is control risk. The reason pertaining to the fact is that in case

the control is not effective then it can result in high risk. Thus, here the test of control can be

skipped and it reveals ineffectviness of control system.

Question 3 – Independence (7 marks)

HA3032 – Auditing - Final Assessment T2 2021

A senior partner in a large incorporated accounting firm has 400 shares in a large client’s

company. Whilst this ownership stake is considered an insignificant part of the partner’s total

share portfolio, the firm has strict requirements about equity investments in clients based on

s307C of the Corporations Act and the APES 110 Code of Ethics for Professional Accountants.

Required:

a) Has the partner violated the independence requirements of the firm? Discuss (3 marks)

b) Explain whether the ownership is likely to affect the partner’s independence in fact.

(4 marks)

ANSWER:

A

In the present situation, the partner has violated that independence requirement as the person

has committed to have an insignificant part in the partner’s total of share portfolio. This is not

good for the company, as the partner is having a stake but it is insignificant and this is not the

independence requirement.

B

Yes, the ownership of the partner’s will definitely affect the independence of the partner. The

reason pertaining to the fact that, the partner has violated the requirement of independence

requirement and as a result of this, there independence will be affected.

Question 4 - Audit Procedures (7 marks)

Your firm Temasek, Smith & Partridge are currently auditing the financial accounts of Riddell Ltd

for the year ending 30 June 2021. You are the Audit Manager on this engagement and one of

your new graduates has performed the following audit procedures in relation to the sales and

collection process of Riddell Ltd, as follows:

1. Examined a sample of shipping documents to determine whether each document has a

sales invoice number included on it.

2. Added the columns on the aged trial balance and compared it to the total noted on the

general ledger.

3. Observed whether the financial accountant makes an independent comparison of the

total in the general ledger with the trial balance of accounts receivable.

HA3032 – Auditing - Final Assessment T2 2021

company. Whilst this ownership stake is considered an insignificant part of the partner’s total

share portfolio, the firm has strict requirements about equity investments in clients based on

s307C of the Corporations Act and the APES 110 Code of Ethics for Professional Accountants.

Required:

a) Has the partner violated the independence requirements of the firm? Discuss (3 marks)

b) Explain whether the ownership is likely to affect the partner’s independence in fact.

(4 marks)

ANSWER:

A

In the present situation, the partner has violated that independence requirement as the person

has committed to have an insignificant part in the partner’s total of share portfolio. This is not

good for the company, as the partner is having a stake but it is insignificant and this is not the

independence requirement.

B

Yes, the ownership of the partner’s will definitely affect the independence of the partner. The

reason pertaining to the fact that, the partner has violated the requirement of independence

requirement and as a result of this, there independence will be affected.

Question 4 - Audit Procedures (7 marks)

Your firm Temasek, Smith & Partridge are currently auditing the financial accounts of Riddell Ltd

for the year ending 30 June 2021. You are the Audit Manager on this engagement and one of

your new graduates has performed the following audit procedures in relation to the sales and

collection process of Riddell Ltd, as follows:

1. Examined a sample of shipping documents to determine whether each document has a

sales invoice number included on it.

2. Added the columns on the aged trial balance and compared it to the total noted on the

general ledger.

3. Observed whether the financial accountant makes an independent comparison of the

total in the general ledger with the trial balance of accounts receivable.

HA3032 – Auditing - Final Assessment T2 2021

4. Examined a sample of customer orders to see whether each order has a credit

authorisation.

5. Compared the date on a sample of shipping documents a few days before and after the

balance sheet date with related sales journal transactions.

6. Computed the ratio of the provision for doubtful debts divided by accounts receivable

and compared it with previous years.

7. Examine a sample of non-cash credit entries in the accounts receivable master file to

determine whether the internal auditor has initialled each one.

Required:

For each audit procedure stated above from 1) – 7), identify the applicable type of audit

evidence, type of test and provide an explanation of the purpose of the audit procedure.

Please use the following table to complete your responses:

ANSWER:

a.

TYPE OF EVIDENCE

b.

TYPE OF TEST

c.

EXPLANATION

Documentation Inquiry In the present case, the

evidence used will be

documentation as it will

assist auditor in examining

the shipping document and

checking the invoice

number. Also, the use of

inquiry will be assistive to

the compay in analysing the

fact that whether the invoice

number used is correct or

not.

HA3032 – Auditing - Final Assessment T2 2021

authorisation.

5. Compared the date on a sample of shipping documents a few days before and after the

balance sheet date with related sales journal transactions.

6. Computed the ratio of the provision for doubtful debts divided by accounts receivable

and compared it with previous years.

7. Examine a sample of non-cash credit entries in the accounts receivable master file to

determine whether the internal auditor has initialled each one.

Required:

For each audit procedure stated above from 1) – 7), identify the applicable type of audit

evidence, type of test and provide an explanation of the purpose of the audit procedure.

Please use the following table to complete your responses:

ANSWER:

a.

TYPE OF EVIDENCE

b.

TYPE OF TEST

c.

EXPLANATION

Documentation Inquiry In the present case, the

evidence used will be

documentation as it will

assist auditor in examining

the shipping document and

checking the invoice

number. Also, the use of

inquiry will be assistive to

the compay in analysing the

fact that whether the invoice

number used is correct or

not.

HA3032 – Auditing - Final Assessment T2 2021

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

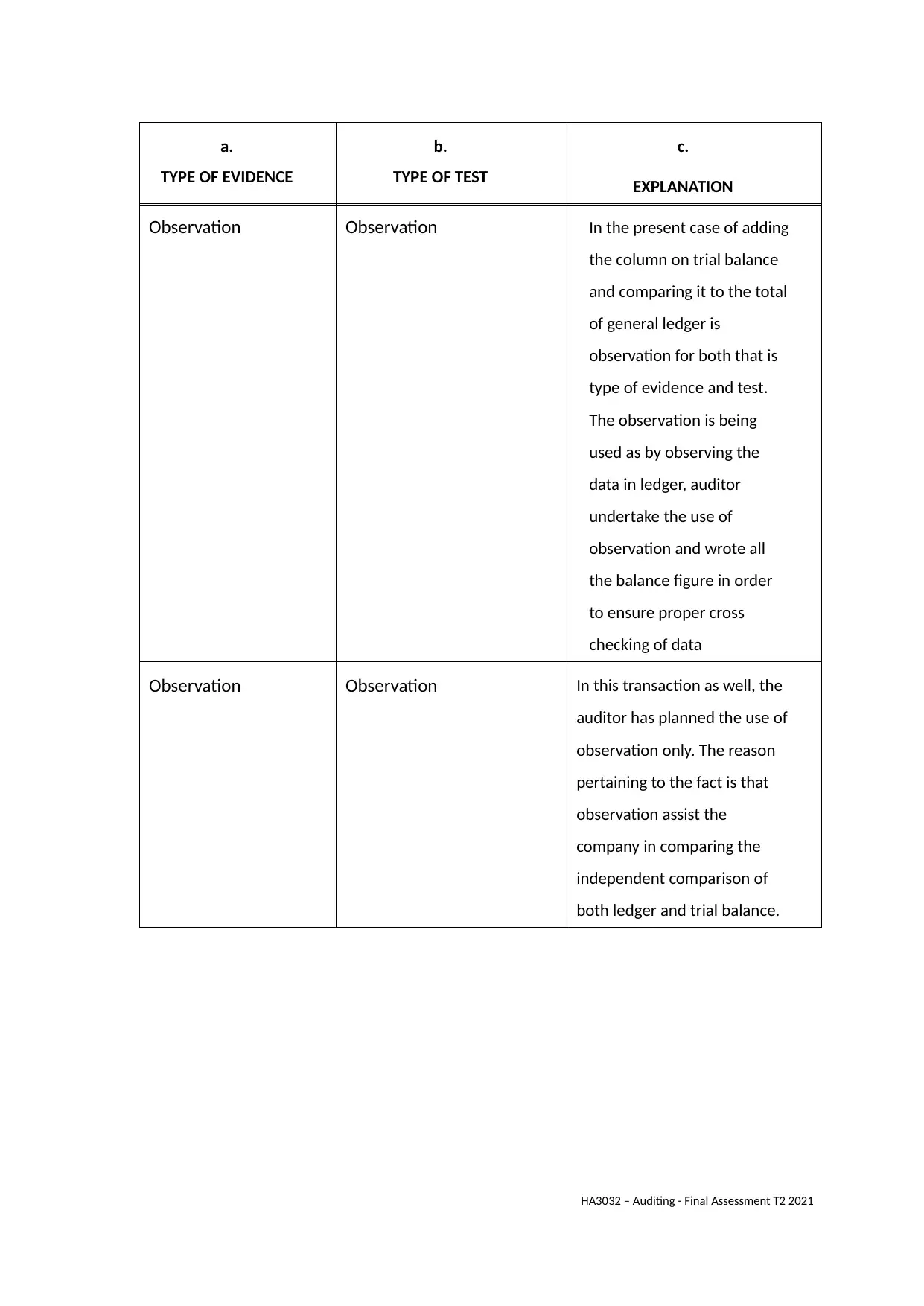

a.

TYPE OF EVIDENCE

b.

TYPE OF TEST

c.

EXPLANATION

Observation Observation In the present case of adding

the column on trial balance

and comparing it to the total

of general ledger is

observation for both that is

type of evidence and test.

The observation is being

used as by observing the

data in ledger, auditor

undertake the use of

observation and wrote all

the balance figure in order

to ensure proper cross

checking of data

Observation Observation In this transaction as well, the

auditor has planned the use of

observation only. The reason

pertaining to the fact is that

observation assist the

company in comparing the

independent comparison of

both ledger and trial balance.

HA3032 – Auditing - Final Assessment T2 2021

TYPE OF EVIDENCE

b.

TYPE OF TEST

c.

EXPLANATION

Observation Observation In the present case of adding

the column on trial balance

and comparing it to the total

of general ledger is

observation for both that is

type of evidence and test.

The observation is being

used as by observing the

data in ledger, auditor

undertake the use of

observation and wrote all

the balance figure in order

to ensure proper cross

checking of data

Observation Observation In this transaction as well, the

auditor has planned the use of

observation only. The reason

pertaining to the fact is that

observation assist the

company in comparing the

independent comparison of

both ledger and trial balance.

HA3032 – Auditing - Final Assessment T2 2021

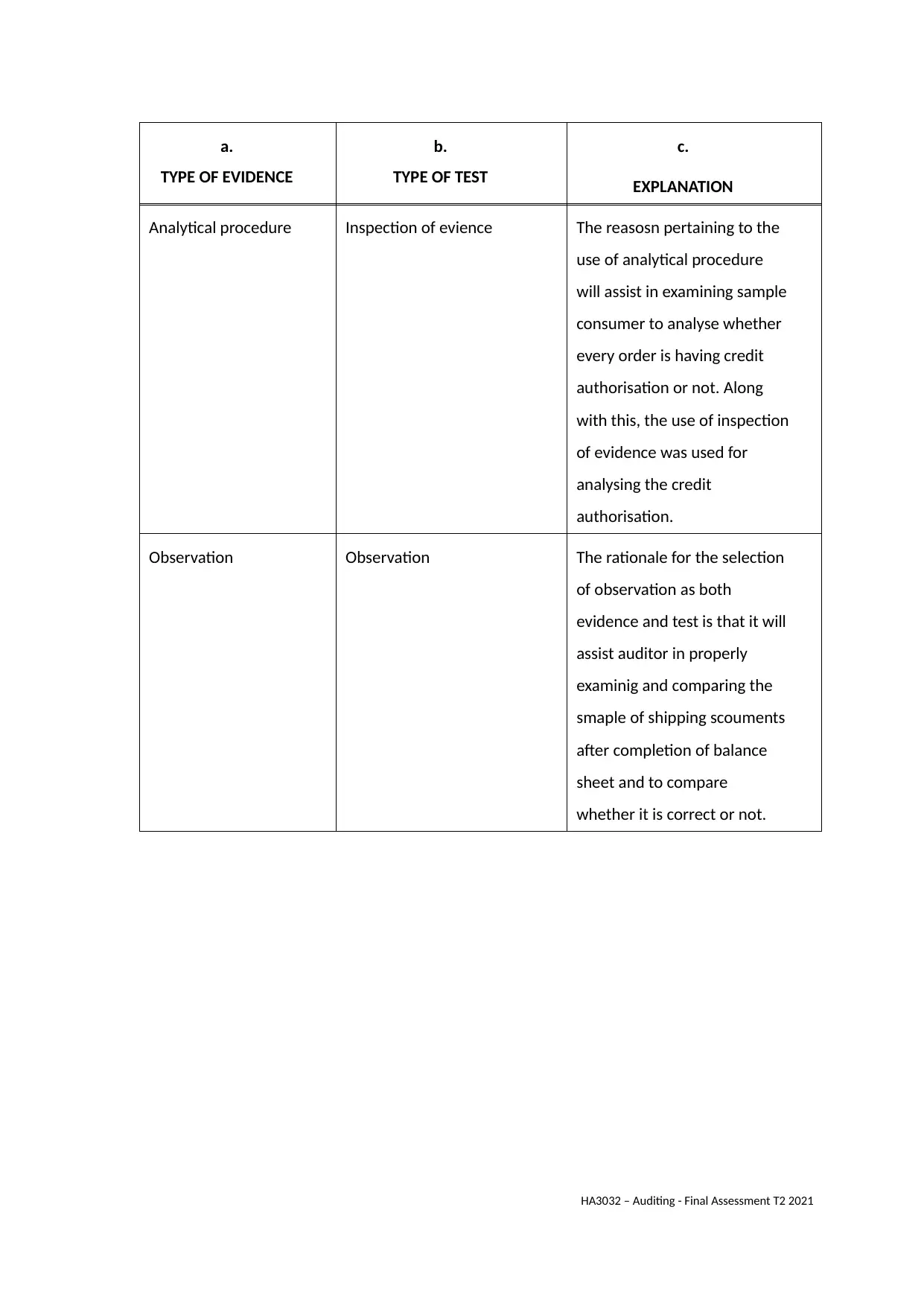

a.

TYPE OF EVIDENCE

b.

TYPE OF TEST

c.

EXPLANATION

Analytical procedure Inspection of evience The reasosn pertaining to the

use of analytical procedure

will assist in examining sample

consumer to analyse whether

every order is having credit

authorisation or not. Along

with this, the use of inspection

of evidence was used for

analysing the credit

authorisation.

Observation Observation The rationale for the selection

of observation as both

evidence and test is that it will

assist auditor in properly

examinig and comparing the

smaple of shipping scouments

after completion of balance

sheet and to compare

whether it is correct or not.

HA3032 – Auditing - Final Assessment T2 2021

TYPE OF EVIDENCE

b.

TYPE OF TEST

c.

EXPLANATION

Analytical procedure Inspection of evience The reasosn pertaining to the

use of analytical procedure

will assist in examining sample

consumer to analyse whether

every order is having credit

authorisation or not. Along

with this, the use of inspection

of evidence was used for

analysing the credit

authorisation.

Observation Observation The rationale for the selection

of observation as both

evidence and test is that it will

assist auditor in properly

examinig and comparing the

smaple of shipping scouments

after completion of balance

sheet and to compare

whether it is correct or not.

HA3032 – Auditing - Final Assessment T2 2021

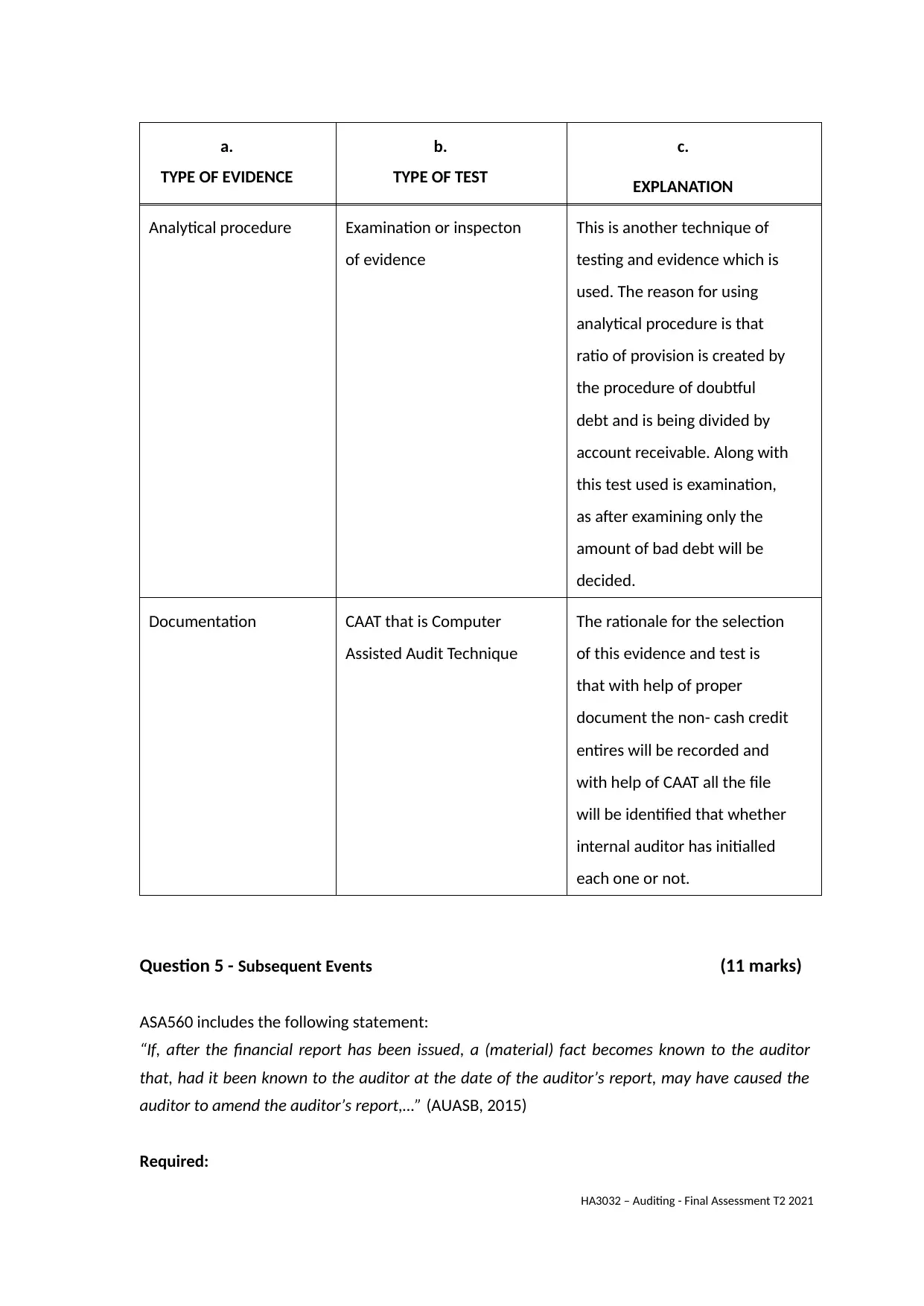

a.

TYPE OF EVIDENCE

b.

TYPE OF TEST

c.

EXPLANATION

Analytical procedure Examination or inspecton

of evidence

This is another technique of

testing and evidence which is

used. The reason for using

analytical procedure is that

ratio of provision is created by

the procedure of doubtful

debt and is being divided by

account receivable. Along with

this test used is examination,

as after examining only the

amount of bad debt will be

decided.

Documentation CAAT that is Computer

Assisted Audit Technique

The rationale for the selection

of this evidence and test is

that with help of proper

document the non- cash credit

entires will be recorded and

with help of CAAT all the file

will be identified that whether

internal auditor has initialled

each one or not.

Question 5 - Subsequent Events (11 marks)

ASA560 includes the following statement:

“If, after the financial report has been issued, a (material) fact becomes known to the auditor

that, had it been known to the auditor at the date of the auditor’s report, may have caused the

auditor to amend the auditor’s report,…” (AUASB, 2015)

Required:

HA3032 – Auditing - Final Assessment T2 2021

TYPE OF EVIDENCE

b.

TYPE OF TEST

c.

EXPLANATION

Analytical procedure Examination or inspecton

of evidence

This is another technique of

testing and evidence which is

used. The reason for using

analytical procedure is that

ratio of provision is created by

the procedure of doubtful

debt and is being divided by

account receivable. Along with

this test used is examination,

as after examining only the

amount of bad debt will be

decided.

Documentation CAAT that is Computer

Assisted Audit Technique

The rationale for the selection

of this evidence and test is

that with help of proper

document the non- cash credit

entires will be recorded and

with help of CAAT all the file

will be identified that whether

internal auditor has initialled

each one or not.

Question 5 - Subsequent Events (11 marks)

ASA560 includes the following statement:

“If, after the financial report has been issued, a (material) fact becomes known to the auditor

that, had it been known to the auditor at the date of the auditor’s report, may have caused the

auditor to amend the auditor’s report,…” (AUASB, 2015)

Required:

HA3032 – Auditing - Final Assessment T2 2021

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

a) Based on the statement provided above from ASA560, explain the actions required of

the auditor in this situation, that is, where a material fact arises after the financial report

was issued. (4 marks)

b) What are the potential risks to the auditor when this problem arises? Discuss. (7 marks)

ANSWER:

A

Based on the statement from ASA560 the action which auditor can undertake in the present

situation is that the auditor need to include that infromaiton within the report again and then

need to issue it. This is necessary because in case the information is material then it need to be

included in the financial reports.

B

The potential risk to the auditor in case of this problem is that there can be risk of

miscommunication. The reason pertaining to the fact is that when the information is outlined

after issue of financial statement then this will be impacting the financial position of company.

Along with this another risk is that when the information is not shared the other people might

think that they have unintentionally not provided the information. Hence, this can reduce the

goodwill of the company to a great extent.

Question 6 - Audit Opinion (11 marks)

Required:

The following are four (4) independent situations. For each case, state the type of audit opinion

which should be expressed and provide an explanation for your choice of audit opinion in each

case shown below a) – d), as follows:

a. Whilst auditing the Long-Term Investments account of Brownllow Medal Ltd., the auditor

has been unable to obtain the audited financial statements for a material investment of

an entity located in an overseas jurisdiction. The auditor concludes that sufficient and

appropriate evidential matter regarding this investment cannot be obtained in the

required time. Additionally, as the Audit Manager in charge of the audit-engagement,

you have to weigh up the requirements of the audit-engagement with the additional cost

of spending extra time at the client’s premises. (2 marks)

HA3032 – Auditing - Final Assessment T2 2021

the auditor in this situation, that is, where a material fact arises after the financial report

was issued. (4 marks)

b) What are the potential risks to the auditor when this problem arises? Discuss. (7 marks)

ANSWER:

A

Based on the statement from ASA560 the action which auditor can undertake in the present

situation is that the auditor need to include that infromaiton within the report again and then

need to issue it. This is necessary because in case the information is material then it need to be

included in the financial reports.

B

The potential risk to the auditor in case of this problem is that there can be risk of

miscommunication. The reason pertaining to the fact is that when the information is outlined

after issue of financial statement then this will be impacting the financial position of company.

Along with this another risk is that when the information is not shared the other people might

think that they have unintentionally not provided the information. Hence, this can reduce the

goodwill of the company to a great extent.

Question 6 - Audit Opinion (11 marks)

Required:

The following are four (4) independent situations. For each case, state the type of audit opinion

which should be expressed and provide an explanation for your choice of audit opinion in each

case shown below a) – d), as follows:

a. Whilst auditing the Long-Term Investments account of Brownllow Medal Ltd., the auditor

has been unable to obtain the audited financial statements for a material investment of

an entity located in an overseas jurisdiction. The auditor concludes that sufficient and

appropriate evidential matter regarding this investment cannot be obtained in the

required time. Additionally, as the Audit Manager in charge of the audit-engagement,

you have to weigh up the requirements of the audit-engagement with the additional cost

of spending extra time at the client’s premises. (2 marks)

HA3032 – Auditing - Final Assessment T2 2021

b. Due to recurring operating losses and ongoing working capital deficiencies, the auditor

has some serious doubts about BMP Ltd.’s ability to continue as a going concern for a

reasonable period of time. However, the financial statement disclosures concerning

these matters, which you have now reviewed and evaluated, are adequate, and the BMP

Ltd. senior management team has been co-operative and helpful with all information

requests. Nonetheless, your professional scepticism leads you to suspect there are likely

to be serious operational challenges for BMP Ltd in the next twelve months. (3 marks)

c. Mirrabella Pty Ltd has completed the preparation of its financial statements for 2020/2021,

but it has decided to exclude the Income Statement. The Chief Financial Officer (CFO) of

Mirrabella Pty Ltd explains to you that the users of their financial statements find the

Income statement confusing, too long and unnecessary because the Balance Sheet already

has the essential information which shareholders require. Accordingly, the CFO has refused

to have the Income Statement in the annual report for the year ending 30/06/21.

Furthermore, the CFO has implied that Mirrabella Pty Ltd will be seeking to appoint a

different auditor for the next audit. (3 marks)

d. Your client, Metro-Quinn Ltd, operates a chain of fast-food outlets throughout Australia. It is

now the end of the audit and it was found that major internal control deficiencies exist in

relation to the completeness of recording and banking of cash sales. Cash register tapes are

not available to determine which cash sales amounts should have been recorded and

banked. There is a lack of separation of duties between the custody of cash and its

recording. Metro-Quinn Ltd senior management have not provided any explanation for

these deficiencies, nor have they indicated that they will act on your recommendations to

remediate the problems and issues in the internal control environment. (3 marks)

ANSWER:

A

In the case of Browllow Medal ltd the audit opinion provided is the qualitifed opinion as in this

type of opinion the auditor is not confident relating to some specific aspect of financial

statement. Thus, in the present case of company, the auditor was not able to find financial

statement relating to material investment of the company.

B

HA3032 – Auditing - Final Assessment T2 2021

has some serious doubts about BMP Ltd.’s ability to continue as a going concern for a

reasonable period of time. However, the financial statement disclosures concerning

these matters, which you have now reviewed and evaluated, are adequate, and the BMP

Ltd. senior management team has been co-operative and helpful with all information

requests. Nonetheless, your professional scepticism leads you to suspect there are likely

to be serious operational challenges for BMP Ltd in the next twelve months. (3 marks)

c. Mirrabella Pty Ltd has completed the preparation of its financial statements for 2020/2021,

but it has decided to exclude the Income Statement. The Chief Financial Officer (CFO) of

Mirrabella Pty Ltd explains to you that the users of their financial statements find the

Income statement confusing, too long and unnecessary because the Balance Sheet already

has the essential information which shareholders require. Accordingly, the CFO has refused

to have the Income Statement in the annual report for the year ending 30/06/21.

Furthermore, the CFO has implied that Mirrabella Pty Ltd will be seeking to appoint a

different auditor for the next audit. (3 marks)

d. Your client, Metro-Quinn Ltd, operates a chain of fast-food outlets throughout Australia. It is

now the end of the audit and it was found that major internal control deficiencies exist in

relation to the completeness of recording and banking of cash sales. Cash register tapes are

not available to determine which cash sales amounts should have been recorded and

banked. There is a lack of separation of duties between the custody of cash and its

recording. Metro-Quinn Ltd senior management have not provided any explanation for

these deficiencies, nor have they indicated that they will act on your recommendations to

remediate the problems and issues in the internal control environment. (3 marks)

ANSWER:

A

In the case of Browllow Medal ltd the audit opinion provided is the qualitifed opinion as in this

type of opinion the auditor is not confident relating to some specific aspect of financial

statement. Thus, in the present case of company, the auditor was not able to find financial

statement relating to material investment of the company.

B

HA3032 – Auditing - Final Assessment T2 2021

In the present case of BMP ltd the audit opinion which is suitable is the adverse opinion. The

reason pertaining to the fact is that, here the auditors are not at all satisfied with the

performance of the company. Here the auditor does not think that the company will continue on

the basis of going concern concept as financial statement of company discloses very concerning

matter.

C

With respect to the present case of Mirrabella Pty Ltd, the auditor will provide a disclaimer of

opnion that is disclaimer report. This audit opinion is provided in case when auditor is avoiding

to provide some opinion to position of company. In connection with the case of Mirrabella Pty

Ltd it was seen that they are not including income statement within their annual report. Hence,

this is not a good because it will not outline the actual postion of the company.

D

In this case as well the auditor will be providing adverse opinion to the company. The reason

underlying this fact is that when the auditor completed it was analysed that there is major

internal control deficiency an this affects the cash sales. Hecne, this is not providing any of the

clear position of the company. Thus, auditor will provide a adverse opinion or the adverse audit

report.

END OF FINAL ASSESSMENT

Submission Instructions:

Save submission with your STUDENT ID NUMBER and UNIT CODE e.g. EMV54897

HA3032

Submission must be in MICROSOFT WORD FORMAT ONLY

Upload your submission to the appropriate link on Blackboard

Only one submission is accepted. Please ensure your submission is the correct

document.

All submissions are automatically passed through SafeAssign to assess academic integrity.

HA3032 – Auditing - Final Assessment T2 2021

reason pertaining to the fact is that, here the auditors are not at all satisfied with the

performance of the company. Here the auditor does not think that the company will continue on

the basis of going concern concept as financial statement of company discloses very concerning

matter.

C

With respect to the present case of Mirrabella Pty Ltd, the auditor will provide a disclaimer of

opnion that is disclaimer report. This audit opinion is provided in case when auditor is avoiding

to provide some opinion to position of company. In connection with the case of Mirrabella Pty

Ltd it was seen that they are not including income statement within their annual report. Hence,

this is not a good because it will not outline the actual postion of the company.

D

In this case as well the auditor will be providing adverse opinion to the company. The reason

underlying this fact is that when the auditor completed it was analysed that there is major

internal control deficiency an this affects the cash sales. Hecne, this is not providing any of the

clear position of the company. Thus, auditor will provide a adverse opinion or the adverse audit

report.

END OF FINAL ASSESSMENT

Submission Instructions:

Save submission with your STUDENT ID NUMBER and UNIT CODE e.g. EMV54897

HA3032

Submission must be in MICROSOFT WORD FORMAT ONLY

Upload your submission to the appropriate link on Blackboard

Only one submission is accepted. Please ensure your submission is the correct

document.

All submissions are automatically passed through SafeAssign to assess academic integrity.

HA3032 – Auditing - Final Assessment T2 2021

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.