HA3032 Auditing 1: Substantive Testing, Ratios & Assertions

VerifiedAdded on 2024/06/03

|19

|3635

|173

Report

AI Summary

This report provides a comprehensive analysis of auditing principles, focusing on substantive testing of balances for Alcidion Group Limited. It includes a detailed ratio analysis covering current ratio, fixed asset turnover, return on assets (ROA), and net profit margin, interpreting their implications for the company's financial health. The report further delves into materiality testing, establishing planning materiality levels based on total assets, and identifies material misstatements within the company's assets and liabilities. Finally, it addresses audit assertions related to material account balances, referencing ISA 315 to ensure financial statements align with applicable reporting frameworks. Desklib offers this assignment as a resource for students, alongside a wealth of other solved assignments and past papers.

HA3032 Auditing

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Introduction......................................................................................................................................3

Nature of the entity and its industry:...........................................................................................4

Ratio analysis...............................................................................................................................5

Materiality testing........................................................................................................................8

Materiality testing of the financial information of the company...............................................10

Audit assertions.........................................................................................................................12

Audit work steps........................................................................................................................14

Conclusion.....................................................................................................................................16

References......................................................................................................................................17

2

Introduction......................................................................................................................................3

Nature of the entity and its industry:...........................................................................................4

Ratio analysis...............................................................................................................................5

Materiality testing........................................................................................................................8

Materiality testing of the financial information of the company...............................................10

Audit assertions.........................................................................................................................12

Audit work steps........................................................................................................................14

Conclusion.....................................................................................................................................16

References......................................................................................................................................17

2

Introduction

Auditing is an important concept that is required to be followed in all the businesses. For this,

there are various tests which are to be performed so that the accuracy of the accounts can be

ensured. In this report, the substantive test of balances will be performed. The operations which

are carried in the business and all the investing and financing activities which are undertaken will

be taken into consideration. The ratio analysis will be performed and for that major ratios will be

calculated. The materiality test will be carried out in which all the accounts which are material

will be determined. All the assertion which are applicable in respect of the material items will be

considered. The work steps which are to be taken in relation to them will also be determined.

3

Auditing is an important concept that is required to be followed in all the businesses. For this,

there are various tests which are to be performed so that the accuracy of the accounts can be

ensured. In this report, the substantive test of balances will be performed. The operations which

are carried in the business and all the investing and financing activities which are undertaken will

be taken into consideration. The ratio analysis will be performed and for that major ratios will be

calculated. The materiality test will be carried out in which all the accounts which are material

will be determined. All the assertion which are applicable in respect of the material items will be

considered. The work steps which are to be taken in relation to them will also be determined.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Nature of the entity and its industry:

Alcidion Group limited is the company which deals in the healthcare technology. It provides the

software in the intelligent informatics and they are carrying the business in New Zealand and

Australia. In this, there are various equipment’s which are provided that are useful in the health

sector and one of them is Miya ED in which clinical dashboard is provided so that dedicated

display is made and by that risk management is made. In the current year, there are various

operations which took place by which growth has been achieved. The main technology of the

company is Miya by which safety is improved and risk is reduced (Alcidion group Limited,

2017). There are various benefits which will be received by the company with the help of this

such as fast recovery will be made as treatment of the patient is started earlier. Time and money

will be saved as the redundant test orders which are conducted are reduced.

The company makes various investments in the business and it is required that they shall be

managed in an appropriate manner. They are made so that returns can be earned from them and

they can again be used in the business so that further returns can be made with the help of that. In

the company, there is payment which is made in respect of plant and equipment in the current

year which amounts to 14567.

Financing activities are involved in this business in which the company will be obtaining funds

from various sources and then the transactions which are related to them will have to be recorded

by the company in the accounts. In the given case there are proceeds which are received from the

issue of shares and that is for the amount of 225000 and then the repayment has been made by

the company which amounted to 5104 (Alcidion group Limited, 2017).

The financial statements of the company are prepared by the company and in them, all the

standards which are made by the Australian accounting standard board have been followed.

Also, the reporting is made in accordance with the International financial reporting standards

which are issued by the IASB (Alcidion group Limited, 2017). The Corporation Act 2001 is also

followed by the company. By all of them, the reliable information is available in respect of the

events, transactions and which exist in the company.

4

Alcidion Group limited is the company which deals in the healthcare technology. It provides the

software in the intelligent informatics and they are carrying the business in New Zealand and

Australia. In this, there are various equipment’s which are provided that are useful in the health

sector and one of them is Miya ED in which clinical dashboard is provided so that dedicated

display is made and by that risk management is made. In the current year, there are various

operations which took place by which growth has been achieved. The main technology of the

company is Miya by which safety is improved and risk is reduced (Alcidion group Limited,

2017). There are various benefits which will be received by the company with the help of this

such as fast recovery will be made as treatment of the patient is started earlier. Time and money

will be saved as the redundant test orders which are conducted are reduced.

The company makes various investments in the business and it is required that they shall be

managed in an appropriate manner. They are made so that returns can be earned from them and

they can again be used in the business so that further returns can be made with the help of that. In

the company, there is payment which is made in respect of plant and equipment in the current

year which amounts to 14567.

Financing activities are involved in this business in which the company will be obtaining funds

from various sources and then the transactions which are related to them will have to be recorded

by the company in the accounts. In the given case there are proceeds which are received from the

issue of shares and that is for the amount of 225000 and then the repayment has been made by

the company which amounted to 5104 (Alcidion group Limited, 2017).

The financial statements of the company are prepared by the company and in them, all the

standards which are made by the Australian accounting standard board have been followed.

Also, the reporting is made in accordance with the International financial reporting standards

which are issued by the IASB (Alcidion group Limited, 2017). The Corporation Act 2001 is also

followed by the company. By all of them, the reliable information is available in respect of the

events, transactions and which exist in the company.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

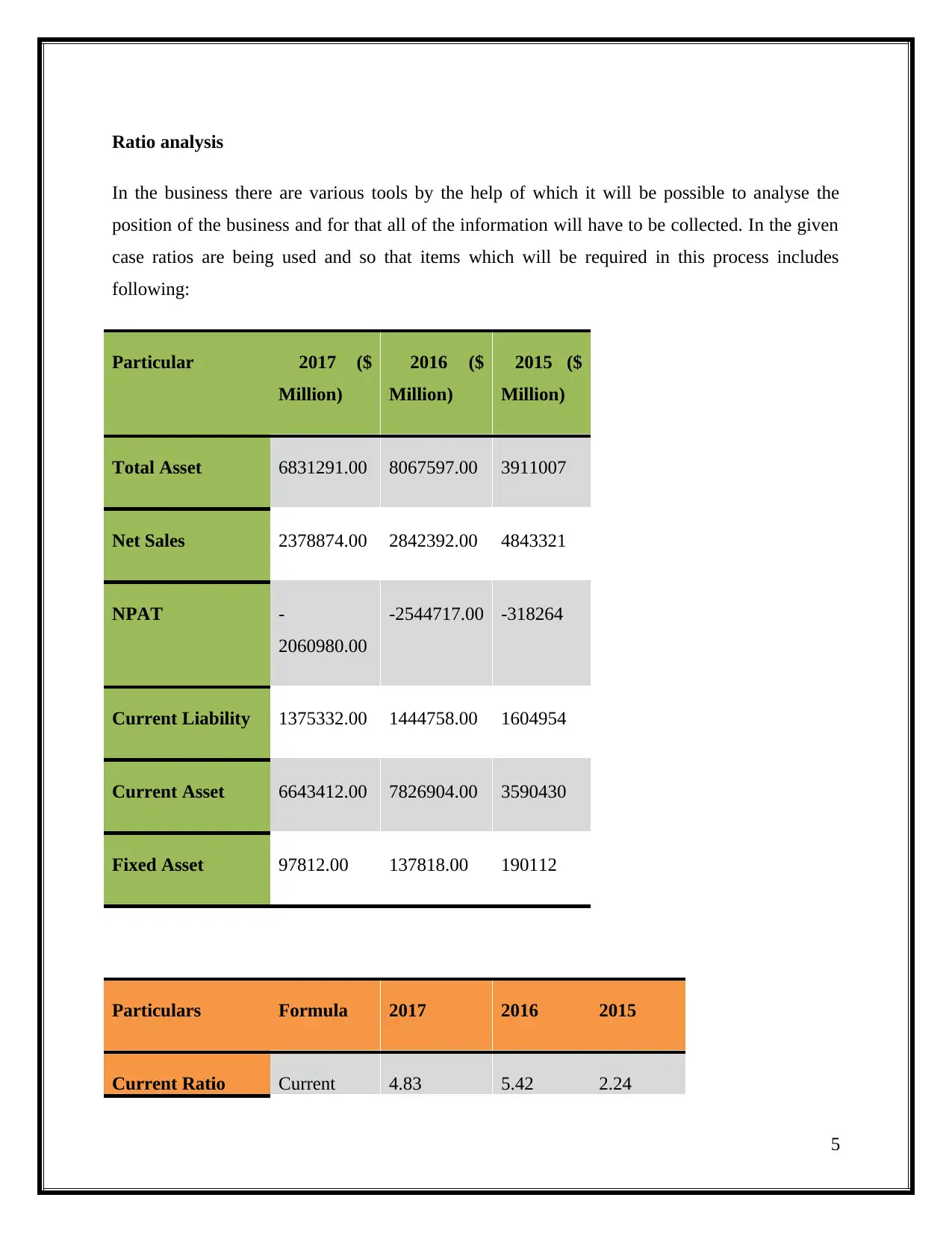

Ratio analysis

In the business there are various tools by the help of which it will be possible to analyse the

position of the business and for that all of the information will have to be collected. In the given

case ratios are being used and so that items which will be required in this process includes

following:

Particular 2017 ($

Million)

2016 ($

Million)

2015 ($

Million)

Total Asset 6831291.00 8067597.00 3911007

Net Sales 2378874.00 2842392.00 4843321

NPAT -

2060980.00

-2544717.00 -318264

Current Liability 1375332.00 1444758.00 1604954

Current Asset 6643412.00 7826904.00 3590430

Fixed Asset 97812.00 137818.00 190112

Particulars Formula 2017 2016 2015

Current Ratio Current 4.83 5.42 2.24

5

In the business there are various tools by the help of which it will be possible to analyse the

position of the business and for that all of the information will have to be collected. In the given

case ratios are being used and so that items which will be required in this process includes

following:

Particular 2017 ($

Million)

2016 ($

Million)

2015 ($

Million)

Total Asset 6831291.00 8067597.00 3911007

Net Sales 2378874.00 2842392.00 4843321

NPAT -

2060980.00

-2544717.00 -318264

Current Liability 1375332.00 1444758.00 1604954

Current Asset 6643412.00 7826904.00 3590430

Fixed Asset 97812.00 137818.00 190112

Particulars Formula 2017 2016 2015

Current Ratio Current 4.83 5.42 2.24

5

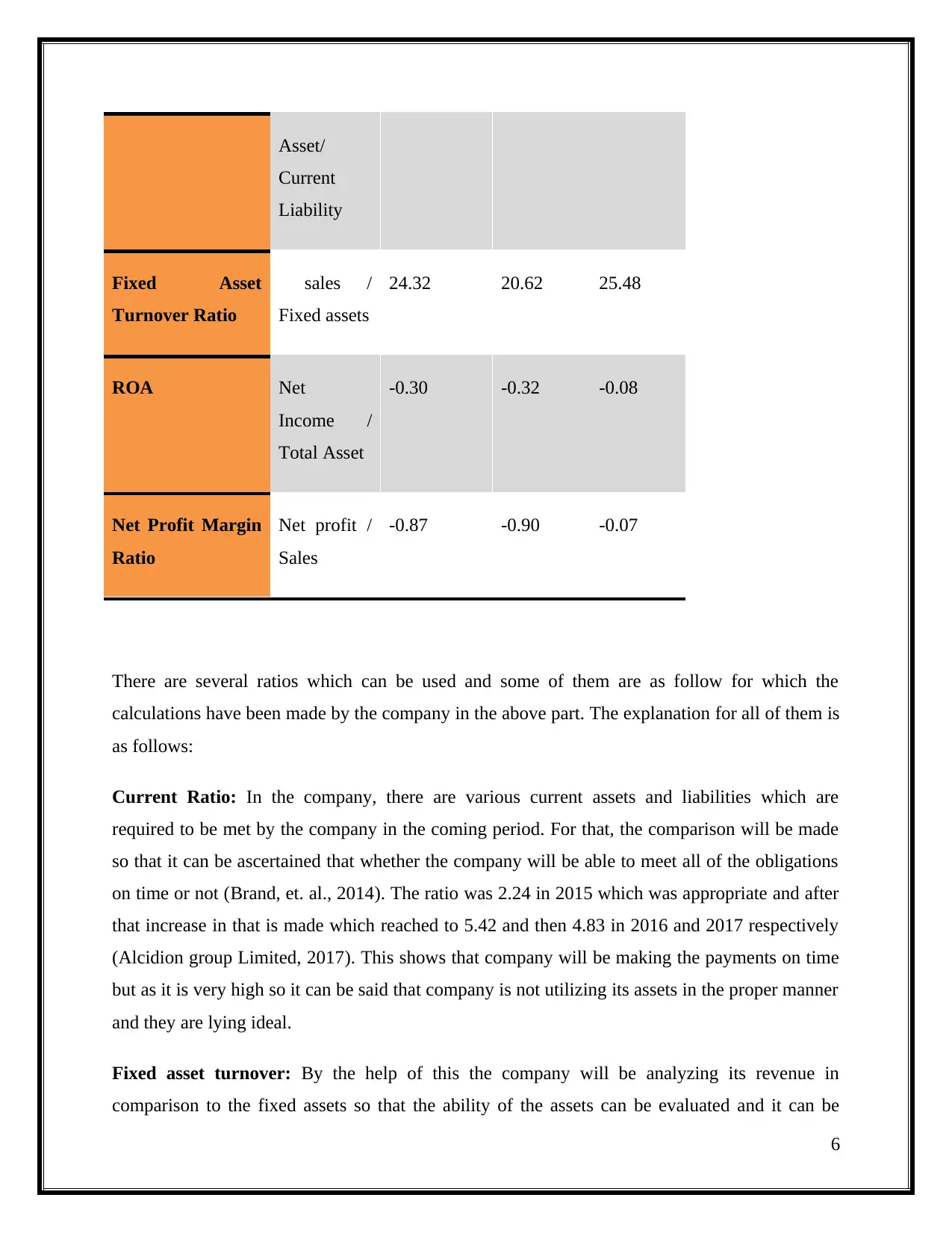

Asset/

Current

Liability

Fixed Asset

Turnover Ratio

sales /

Fixed assets

24.32 20.62 25.48

ROA Net

Income /

Total Asset

-0.30 -0.32 -0.08

Net Profit Margin

Ratio

Net profit /

Sales

-0.87 -0.90 -0.07

There are several ratios which can be used and some of them are as follow for which the

calculations have been made by the company in the above part. The explanation for all of them is

as follows:

Current Ratio: In the company, there are various current assets and liabilities which are

required to be met by the company in the coming period. For that, the comparison will be made

so that it can be ascertained that whether the company will be able to meet all of the obligations

on time or not (Brand, et. al., 2014). The ratio was 2.24 in 2015 which was appropriate and after

that increase in that is made which reached to 5.42 and then 4.83 in 2016 and 2017 respectively

(Alcidion group Limited, 2017). This shows that company will be making the payments on time

but as it is very high so it can be said that company is not utilizing its assets in the proper manner

and they are lying ideal.

Fixed asset turnover: By the help of this the company will be analyzing its revenue in

comparison to the fixed assets so that the ability of the assets can be evaluated and it can be

6

Current

Liability

Fixed Asset

Turnover Ratio

sales /

Fixed assets

24.32 20.62 25.48

ROA Net

Income /

Total Asset

-0.30 -0.32 -0.08

Net Profit Margin

Ratio

Net profit /

Sales

-0.87 -0.90 -0.07

There are several ratios which can be used and some of them are as follow for which the

calculations have been made by the company in the above part. The explanation for all of them is

as follows:

Current Ratio: In the company, there are various current assets and liabilities which are

required to be met by the company in the coming period. For that, the comparison will be made

so that it can be ascertained that whether the company will be able to meet all of the obligations

on time or not (Brand, et. al., 2014). The ratio was 2.24 in 2015 which was appropriate and after

that increase in that is made which reached to 5.42 and then 4.83 in 2016 and 2017 respectively

(Alcidion group Limited, 2017). This shows that company will be making the payments on time

but as it is very high so it can be said that company is not utilizing its assets in the proper manner

and they are lying ideal.

Fixed asset turnover: By the help of this the company will be analyzing its revenue in

comparison to the fixed assets so that the ability of the assets can be evaluated and it can be

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

determined that they are used in proper manner. This was 25.48 in 2015 and then a decline was

made in 2016 which made the ratio to be 20.62. There is again an increase in 2017 which made it

be 24.32. This shows that proper utilization is made by the company (Alcidion group Limited,

2017).

ROA: The return which is earned by the company will be evaluated on the basis of assets so that

the business will be ascertaining that all of them are providing the appropriate returns or not

(Kogadeeva & Zamboni, 2016). There is the negative earning which shows that company is not

able to make the required profits and the assets are not able to generate the needed income.

Net profit margin: the net profit which is earned in the year will be compared with the sales

which are made. By that, it will be identified that company maintains the profit ratio or not. If the

more expense is made on the sale then that will be considered as that affects the profit of the

company (Zolfani, et. al., 2018). In the given case there are losses and so the company is not

utilizing its sources in a proper manner. The loss is increasing and was highest in 2015 and after

that, there was a certain amount of decline (Alcidion group Limited, 2017).

7

made in 2016 which made the ratio to be 20.62. There is again an increase in 2017 which made it

be 24.32. This shows that proper utilization is made by the company (Alcidion group Limited,

2017).

ROA: The return which is earned by the company will be evaluated on the basis of assets so that

the business will be ascertaining that all of them are providing the appropriate returns or not

(Kogadeeva & Zamboni, 2016). There is the negative earning which shows that company is not

able to make the required profits and the assets are not able to generate the needed income.

Net profit margin: the net profit which is earned in the year will be compared with the sales

which are made. By that, it will be identified that company maintains the profit ratio or not. If the

more expense is made on the sale then that will be considered as that affects the profit of the

company (Zolfani, et. al., 2018). In the given case there are losses and so the company is not

utilizing its sources in a proper manner. The loss is increasing and was highest in 2015 and after

that, there was a certain amount of decline (Alcidion group Limited, 2017).

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Materiality testing

Materiality: Materiality for auditors means all the information disclosed in the financial

statement are free from misstatement and fraudulent figures. The aim behind the determination

of materiality in financial accounts is to obtain reasonable assurance regarding the availability of

material misstatement in financial accounts of the organization. Auditors do not provide 100%

assurance regarding the information disclosed in the financial statement of the company,

materiality testing provides reasonable assurance to the users of the financial statement of the

organization.

Account balances which need to be considered as material: To check materiality in financial

statement materiality base and percentage range need to be determined. For materiality testing;

base must be considered from the elements of financial statements like sales/ revenue, income

from continuing operations, current assets and liabilities, total assets and total expenses or total

asset value.

Auditors normally assign a lower level of percentage in order to determine the materiality of

each account balance during the audit procedures Generally auditors can adopt following

percentage base for checking the materiality and availability of risk of misstatements in financial

accounts of the company. The percentage basis is as follows:

5% of the cost of sales of goods

5% of net income

½ to 1% of total asset value

2% of revenue.

These materiality level or base are adopted by auditors as per their own assumption related

to the availability of risk. In case of testing materiality for Alcidion group limited we can

take material percentage base of 2% of total assets.

8

Materiality: Materiality for auditors means all the information disclosed in the financial

statement are free from misstatement and fraudulent figures. The aim behind the determination

of materiality in financial accounts is to obtain reasonable assurance regarding the availability of

material misstatement in financial accounts of the organization. Auditors do not provide 100%

assurance regarding the information disclosed in the financial statement of the company,

materiality testing provides reasonable assurance to the users of the financial statement of the

organization.

Account balances which need to be considered as material: To check materiality in financial

statement materiality base and percentage range need to be determined. For materiality testing;

base must be considered from the elements of financial statements like sales/ revenue, income

from continuing operations, current assets and liabilities, total assets and total expenses or total

asset value.

Auditors normally assign a lower level of percentage in order to determine the materiality of

each account balance during the audit procedures Generally auditors can adopt following

percentage base for checking the materiality and availability of risk of misstatements in financial

accounts of the company. The percentage basis is as follows:

5% of the cost of sales of goods

5% of net income

½ to 1% of total asset value

2% of revenue.

These materiality level or base are adopted by auditors as per their own assumption related

to the availability of risk. In case of testing materiality for Alcidion group limited we can

take material percentage base of 2% of total assets.

8

The process of calculating materiality: using the percentage base and materiality base

preliminary figures are calculated in order to consider qualitative items like:

a. Availability of fraud or illegal acts

b. The amount which affects earning trend of the company.

c. A misstatement that may affect or increase management compensation.

d. Industry conditions

e. Past number of misstatements

Justification of decision making

While testing materiality 5% of total assets is assumed to be taken because the total asset is the

part of the working capital of the firm which is important to be available for the continued

operation of the organization. Availability of asset is required for the future financial planning of

the organization. materiality base of 2% of total assets for checking materiality provides the

understatement and overstatement of the amount in financial statement and determine the

availability of risk in terms of material misstatement, in the financial reports of the company.

After determining the same important steps need to be taken to remove the available amount of

risk.

9

preliminary figures are calculated in order to consider qualitative items like:

a. Availability of fraud or illegal acts

b. The amount which affects earning trend of the company.

c. A misstatement that may affect or increase management compensation.

d. Industry conditions

e. Past number of misstatements

Justification of decision making

While testing materiality 5% of total assets is assumed to be taken because the total asset is the

part of the working capital of the firm which is important to be available for the continued

operation of the organization. Availability of asset is required for the future financial planning of

the organization. materiality base of 2% of total assets for checking materiality provides the

understatement and overstatement of the amount in financial statement and determine the

availability of risk in terms of material misstatement, in the financial reports of the company.

After determining the same important steps need to be taken to remove the available amount of

risk.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

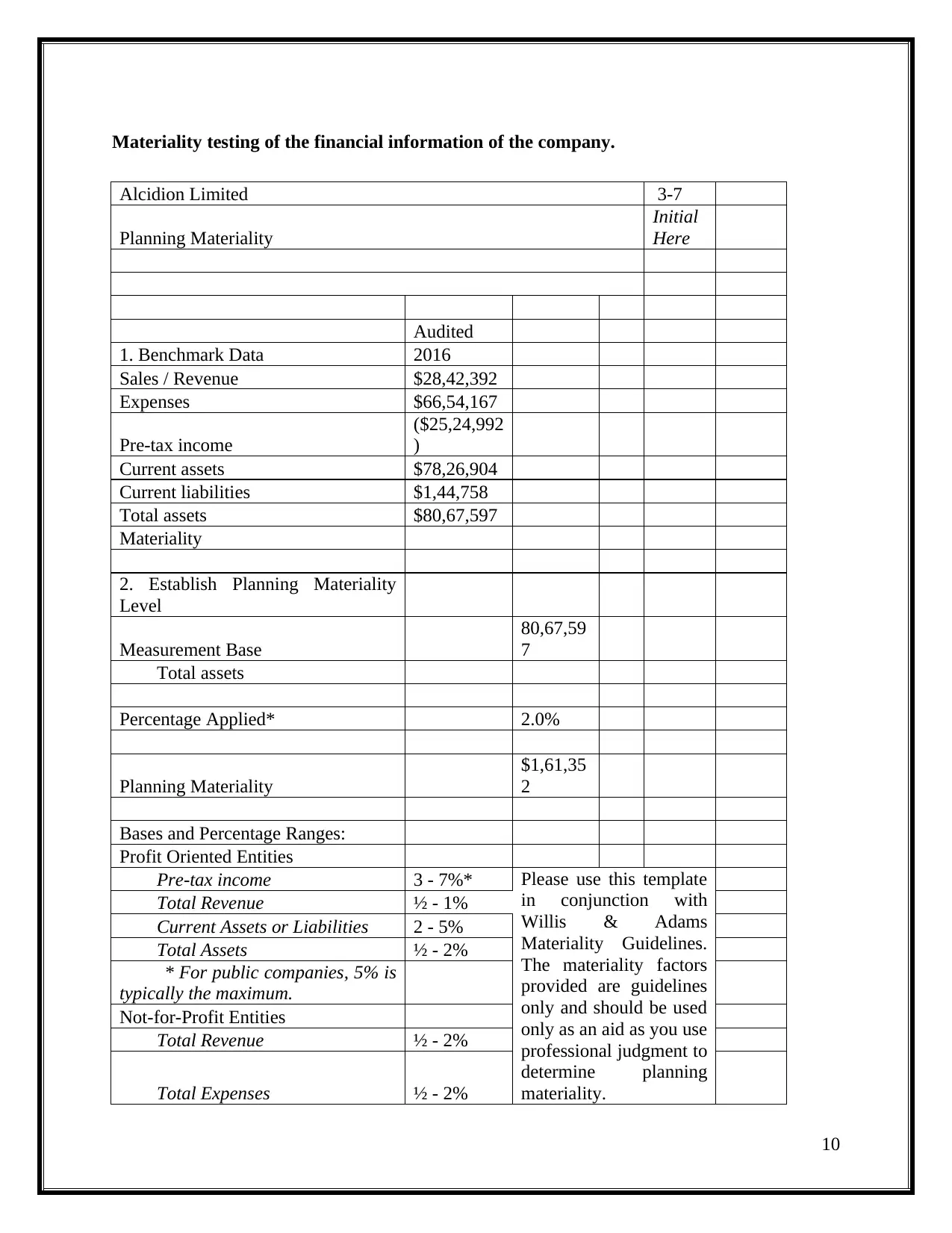

Materiality testing of the financial information of the company.

Alcidion Limited 3-7

Planning Materiality

Initial

Here

Audited

1. Benchmark Data 2016

Sales / Revenue $28,42,392

Expenses $66,54,167

Pre-tax income

($25,24,992

)

Current assets $78,26,904

Current liabilities $1,44,758

Total assets $80,67,597

Materiality

2. Establish Planning Materiality

Level

Measurement Base

80,67,59

7

Total assets

Percentage Applied* 2.0%

Planning Materiality

$1,61,35

2

Bases and Percentage Ranges:

Profit Oriented Entities

Pre-tax income 3 - 7%* Please use this template

in conjunction with

Willis & Adams

Materiality Guidelines.

The materiality factors

provided are guidelines

only and should be used

only as an aid as you use

professional judgment to

determine planning

materiality.

Total Revenue ½ - 1%

Current Assets or Liabilities 2 - 5%

Total Assets ½ - 2%

* For public companies, 5% is

typically the maximum.

Not-for-Profit Entities

Total Revenue ½ - 2%

Total Expenses ½ - 2%

10

Alcidion Limited 3-7

Planning Materiality

Initial

Here

Audited

1. Benchmark Data 2016

Sales / Revenue $28,42,392

Expenses $66,54,167

Pre-tax income

($25,24,992

)

Current assets $78,26,904

Current liabilities $1,44,758

Total assets $80,67,597

Materiality

2. Establish Planning Materiality

Level

Measurement Base

80,67,59

7

Total assets

Percentage Applied* 2.0%

Planning Materiality

$1,61,35

2

Bases and Percentage Ranges:

Profit Oriented Entities

Pre-tax income 3 - 7%* Please use this template

in conjunction with

Willis & Adams

Materiality Guidelines.

The materiality factors

provided are guidelines

only and should be used

only as an aid as you use

professional judgment to

determine planning

materiality.

Total Revenue ½ - 1%

Current Assets or Liabilities 2 - 5%

Total Assets ½ - 2%

* For public companies, 5% is

typically the maximum.

Not-for-Profit Entities

Total Revenue ½ - 2%

Total Expenses ½ - 2%

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Mutual Fund Entities

Net Asset Value ½ - 1%

11

Net Asset Value ½ - 1%

11

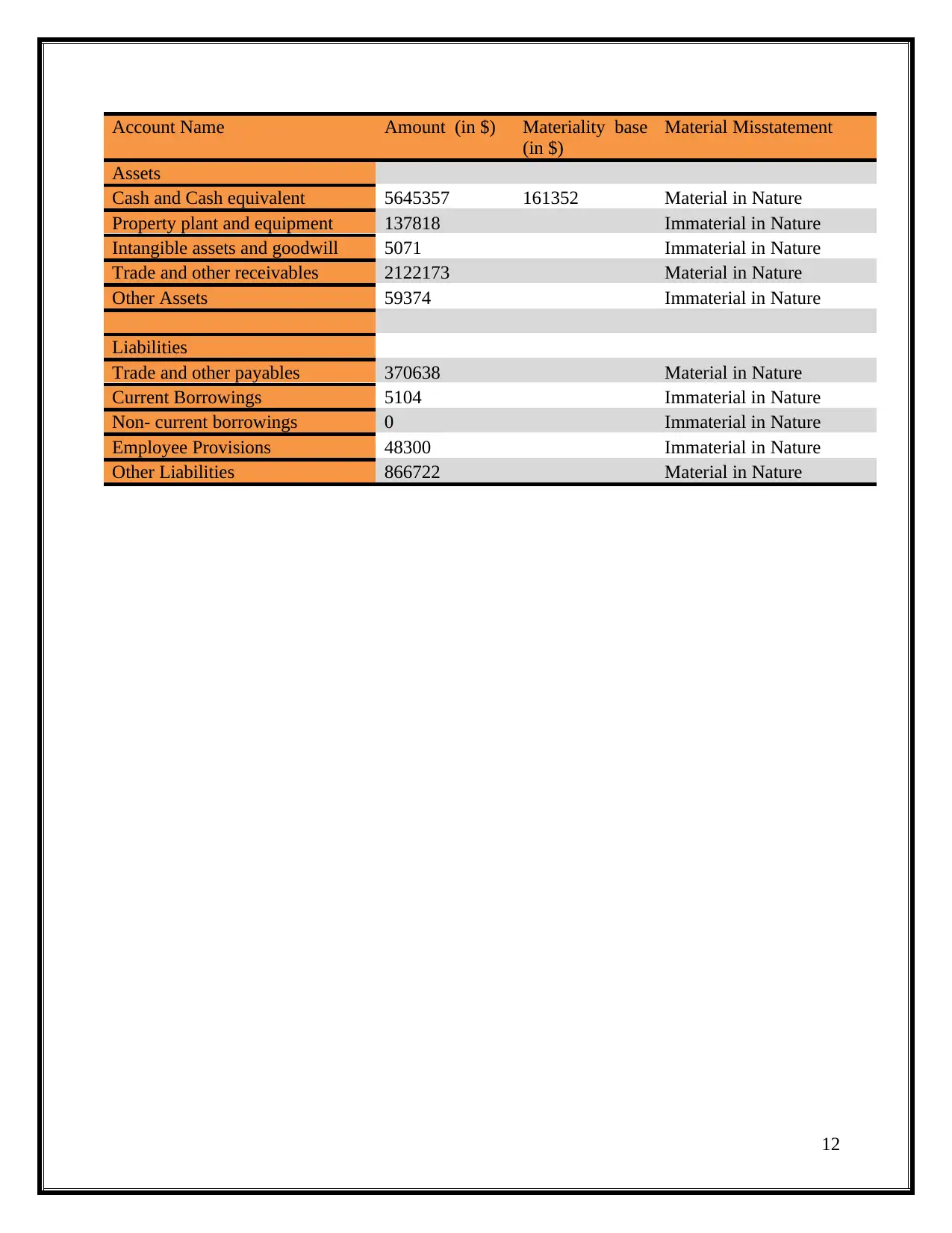

Account Name Amount (in $) Materiality base

(in $)

Material Misstatement

Assets

Cash and Cash equivalent 5645357 161352 Material in Nature

Property plant and equipment 137818 Immaterial in Nature

Intangible assets and goodwill 5071 Immaterial in Nature

Trade and other receivables 2122173 Material in Nature

Other Assets 59374 Immaterial in Nature

Liabilities

Trade and other payables 370638 Material in Nature

Current Borrowings 5104 Immaterial in Nature

Non- current borrowings 0 Immaterial in Nature

Employee Provisions 48300 Immaterial in Nature

Other Liabilities 866722 Material in Nature

12

(in $)

Material Misstatement

Assets

Cash and Cash equivalent 5645357 161352 Material in Nature

Property plant and equipment 137818 Immaterial in Nature

Intangible assets and goodwill 5071 Immaterial in Nature

Trade and other receivables 2122173 Material in Nature

Other Assets 59374 Immaterial in Nature

Liabilities

Trade and other payables 370638 Material in Nature

Current Borrowings 5104 Immaterial in Nature

Non- current borrowings 0 Immaterial in Nature

Employee Provisions 48300 Immaterial in Nature

Other Liabilities 866722 Material in Nature

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.