Accounting Harmonisation and Its Success in Singapore: A Report

VerifiedAdded on 2020/05/28

|14

|3324

|129

Report

AI Summary

This report examines the success of accounting harmonisation, focusing on Singapore as a case study. It explores the rationale for harmonisation, including compliance with IASC and Asian standards, and the impact of globalization. The report identifies key issues in harmonisation, such as cultural obstacles, integration problems, negative impacts on small businesses, and licensing and enforcement challenges. A country-level analysis highlights Singapore's adoption of IFRS and efforts to harmonise SAS with FRS. A case study on Singapore Press Holdings illustrates the implementation process, comparing financial statements before and after harmonisation. The report concludes with recommendations based on the findings, providing valuable insights into the complexities and benefits of accounting harmonisation in a globalized environment. This study assesses the financial position after the harmonization process.

Running head: SUCCESS OF ACCOUNTING HARMONISATION

Success of accounting Harmonisation

Name of the Student

Name of the University

Author’s Note

Success of accounting Harmonisation

Name of the Student

Name of the University

Author’s Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1SUCCESS OF ACCOUNTING HARMONISATION

Table of Contents

1.0 Executive Summary..............................................................................................................2

2.0 Introduction................................................................................................................................2

3.0 Rationale of harmonisation........................................................................................................2

3.1 Compliance with the Standard of IASC................................................................................3

3.2 Compliance with the Asia.....................................................................................................3

3.3 Globalisation.........................................................................................................................3

4.0 Issue in harmonisation...............................................................................................................3

4.1 Cultural Obstacles.................................................................................................................4

4.2 Integration Problems.............................................................................................................4

4.3 Negative impacts on the small business................................................................................4

4.4 Licensing and Enforcement...................................................................................................5

4.5 Political Grouping.................................................................................................................5

4.6 International Sovereignty Issues...........................................................................................5

5.0 Country Level Analysis.............................................................................................................5

5.1 Rationale for Majority of IFRS in Singapore........................................................................5

5.2 Efforts to Harmonise SAS with FRS.....................................................................................6

6.0 Case study on Singapore and “Singapore Press Holdings”.......................................................6

6.1 Background of the Company.................................................................................................6

6.2 Implementation process of FRS from Local SRS.................................................................6

6.3 Before and after harmonisation of impact on the financial statement...................................6

Conclusion and recommendation..................................................................................................11

References......................................................................................................................................12

Table of Contents

1.0 Executive Summary..............................................................................................................2

2.0 Introduction................................................................................................................................2

3.0 Rationale of harmonisation........................................................................................................2

3.1 Compliance with the Standard of IASC................................................................................3

3.2 Compliance with the Asia.....................................................................................................3

3.3 Globalisation.........................................................................................................................3

4.0 Issue in harmonisation...............................................................................................................3

4.1 Cultural Obstacles.................................................................................................................4

4.2 Integration Problems.............................................................................................................4

4.3 Negative impacts on the small business................................................................................4

4.4 Licensing and Enforcement...................................................................................................5

4.5 Political Grouping.................................................................................................................5

4.6 International Sovereignty Issues...........................................................................................5

5.0 Country Level Analysis.............................................................................................................5

5.1 Rationale for Majority of IFRS in Singapore........................................................................5

5.2 Efforts to Harmonise SAS with FRS.....................................................................................6

6.0 Case study on Singapore and “Singapore Press Holdings”.......................................................6

6.1 Background of the Company.................................................................................................6

6.2 Implementation process of FRS from Local SRS.................................................................6

6.3 Before and after harmonisation of impact on the financial statement...................................6

Conclusion and recommendation..................................................................................................11

References......................................................................................................................................12

2SUCCESS OF ACCOUNTING HARMONISATION

1.0 Executive Summary

Harmonisation is considered as the main process for collaborating with various systems

in a particular method. This particular report has been able to show the rationale of the overall

harmonization process which are seen to be in compliance with the Standard of IASC and Asian

standards. The study has been able to infer the different types of the recognised issues in the

harmonization in Singapore Press Holdings.

As per the findings of the report the main form of the barriers in the

harmonization process has been seen to be depicted with the varied information which are based

on the “Cultural Obstacles, Integration Problems, Negative impacts on the small business,

Licensing and Enforcement”. The pre-and the post implementation of the harmonization has

been further able to discuss on PPE less the cost accumulated with the impairment and

depreciation. In case of SAS the fixed assets are considered with fixed assets less accumulated

depreciation (Legenzova, 2016).

2.0 Introduction

The important concept of the harmonisation is considered with the collaboration of

different systems in a certain method. The procedure of accounting policy is maintained as per

the increasing compatibility setting constraints and accounting practices and depicting the way

they change. The basic reason for the study is to assess the financial position after the

harmonisation process (Adrian-Cosmin, 2015).

3.0 Rationale of harmonisation

In general harmonisation in account is based on the similarity with the accounting

standards and financial reporting. Harmonization not only puts emphasis on the elimination of

the contradiction rules but also overcome the reduction in the global differences to achieve the

reduction in the contradiction rules. The process of harmonisation in accounting has been able to

overcome the global differences for achieving an improved international comparability for the

financial statements. The present reporting standard has been able to highlight the subsequent

transition to “Financial Reporting Standards” “(FRS) and INT FRS”. As per the changes with

the significant difference in the balance sheet and income statement for “Singapore Press

Holdings”. As per the opinion by SmithKline Beecham and Daimler-Benz the difference and the

segregation has been able to change the main purpose for the result of accounting requirement

1.0 Executive Summary

Harmonisation is considered as the main process for collaborating with various systems

in a particular method. This particular report has been able to show the rationale of the overall

harmonization process which are seen to be in compliance with the Standard of IASC and Asian

standards. The study has been able to infer the different types of the recognised issues in the

harmonization in Singapore Press Holdings.

As per the findings of the report the main form of the barriers in the

harmonization process has been seen to be depicted with the varied information which are based

on the “Cultural Obstacles, Integration Problems, Negative impacts on the small business,

Licensing and Enforcement”. The pre-and the post implementation of the harmonization has

been further able to discuss on PPE less the cost accumulated with the impairment and

depreciation. In case of SAS the fixed assets are considered with fixed assets less accumulated

depreciation (Legenzova, 2016).

2.0 Introduction

The important concept of the harmonisation is considered with the collaboration of

different systems in a certain method. The procedure of accounting policy is maintained as per

the increasing compatibility setting constraints and accounting practices and depicting the way

they change. The basic reason for the study is to assess the financial position after the

harmonisation process (Adrian-Cosmin, 2015).

3.0 Rationale of harmonisation

In general harmonisation in account is based on the similarity with the accounting

standards and financial reporting. Harmonization not only puts emphasis on the elimination of

the contradiction rules but also overcome the reduction in the global differences to achieve the

reduction in the contradiction rules. The process of harmonisation in accounting has been able to

overcome the global differences for achieving an improved international comparability for the

financial statements. The present reporting standard has been able to highlight the subsequent

transition to “Financial Reporting Standards” “(FRS) and INT FRS”. As per the changes with

the significant difference in the balance sheet and income statement for “Singapore Press

Holdings”. As per the opinion by SmithKline Beecham and Daimler-Benz the difference and the

segregation has been able to change the main purpose for the result of accounting requirement

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3SUCCESS OF ACCOUNTING HARMONISATION

implementation process. The main aim for the harmonisation is seen with the financial

statements which are comparable with the other countries and same countries. The main form of

the conceptualisation of the harmonisation is important for the organizations operating with other

business situations (Frezatti, B. Carter, & F.G. Barroso, 2014).

3.1 Compliance with the Standard of IASC

The IASC is seen to maintain the accounting standard with the published financial

statements. The important form of the compliance is further taken into account with the

standards helpful for harmonisation of the standards which are used by national accounting

requirements (Auvinen et al., 2014).

3.2 Compliance with the Asia

In Singapore the “The Accounting Standards Council” was seen to be

conceptualized in 2007. The financial analysts are able to consider that the

consolidated financial condition of the FBOs are seen with the relevant key

accounting differences and the various types of the supervisory impacts to perform

“Strength of Support Assessment (SOSA)”. The IFRS implementation has been

depicted with "a single set of high quality, uniform, globally-applied, and enforced

accounting standards which is conducive for both domestic and cross-border

investment and financing decisions”. The adaptation of IFRS is taken into account

with greater reliance on the financial statement reporting aspects, which is

presented with by FBOs and other genres of enterprises (Sauer, 2015).

3.3 Globalisation

The accounting standards which are followed in Asia is based on the compliance of both

IAS and GAAP. The increase in the accounting standard compliance has been further

able to comply accounting standard which is taken into account with the

globalization criteria. The main effect on the globalization is considered with

numerous enterprises franchised and setup other than Asian countries. Due to this,

harmonization of accounting standard is seen to be related with the overall

presentation and understanding of the financial presentations of the report in

various countries in which it is seen to be operational. The adoption process of

accounting harmonization is seen to be conducive with undertaking the

responsibilities of the investors in a better way. This has been further able to assess

the concerns with the financial data presented in the annual report. This particular

consideration is further seen to be based on various factors of harmonization

process (Visvikis, 2014).

implementation process. The main aim for the harmonisation is seen with the financial

statements which are comparable with the other countries and same countries. The main form of

the conceptualisation of the harmonisation is important for the organizations operating with other

business situations (Frezatti, B. Carter, & F.G. Barroso, 2014).

3.1 Compliance with the Standard of IASC

The IASC is seen to maintain the accounting standard with the published financial

statements. The important form of the compliance is further taken into account with the

standards helpful for harmonisation of the standards which are used by national accounting

requirements (Auvinen et al., 2014).

3.2 Compliance with the Asia

In Singapore the “The Accounting Standards Council” was seen to be

conceptualized in 2007. The financial analysts are able to consider that the

consolidated financial condition of the FBOs are seen with the relevant key

accounting differences and the various types of the supervisory impacts to perform

“Strength of Support Assessment (SOSA)”. The IFRS implementation has been

depicted with "a single set of high quality, uniform, globally-applied, and enforced

accounting standards which is conducive for both domestic and cross-border

investment and financing decisions”. The adaptation of IFRS is taken into account

with greater reliance on the financial statement reporting aspects, which is

presented with by FBOs and other genres of enterprises (Sauer, 2015).

3.3 Globalisation

The accounting standards which are followed in Asia is based on the compliance of both

IAS and GAAP. The increase in the accounting standard compliance has been further

able to comply accounting standard which is taken into account with the

globalization criteria. The main effect on the globalization is considered with

numerous enterprises franchised and setup other than Asian countries. Due to this,

harmonization of accounting standard is seen to be related with the overall

presentation and understanding of the financial presentations of the report in

various countries in which it is seen to be operational. The adoption process of

accounting harmonization is seen to be conducive with undertaking the

responsibilities of the investors in a better way. This has been further able to assess

the concerns with the financial data presented in the annual report. This particular

consideration is further seen to be based on various factors of harmonization

process (Visvikis, 2014).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4SUCCESS OF ACCOUNTING HARMONISATION

4.0 Issue in harmonisation

The main issue in harmonization is seen with compliance of single accounting standard

which are stated below as follows:

4.1 Cultural Obstacles

This is considered with attitudes, religion and various problems of language barrier. The

research considered with Hofstede and Trompenaar has depicted the difference among the

cultural barrier. The auditors of Singapore have seen to eclipse the personal and the close

reaction and rejection of any form of gifts in the business. The differentiated behaviour and

values of the individuals has its implication on the international standards (Oulasvirta & Bailey,

2016).

4.2 Integration Problems

The main problem in the new accounting standard implemented in Singapore is evident

with the FRSs which is implemented in the “beginning on or after January 1, 2003, apart from FRS 39”.

FRS has been further able to show the disclosure valuation for the independent values and

annual valuation process. The other disparity is seen with business combinations, leases,

borrowing cost and different types of the related party transactions (Calmel, 2014).

The recognition criteria for the integration process has been further seen to be evident with the

combinations of both standards. These are seen with of “FRS/SAS 7, FRS 16/SAS 14, FRS

17/SAS 15, FRS 22/SAS 22, FRS 23/SAS 19, FRS 28/SAS 27 and FRS 39/ SAS 33”. In various

cases the disparity in the recognition for the new standard is seen with the exemption like

“Accounting for Investments in Associates”. The implementation of the new method is further

considered with specific exemptions per applying new method for equity in the accounting

method. The FRS recognition criteria has included the goodwill evaluation which is taken into

consideration after the reserves of 1994. This has been further seen to be based on the several

types of the depictions as per the FRS recognition. It is also discerned that FRS does not need to

depict this but in case of SAS the restatement needs to be done accordingly (Ahmed & Ali,

2015).

4.3 Negative impacts on the small business

The integration problem of SAS and FRS is seen as the main problem for the “Small and

medium size entities (SME)” in Singapore. The changing nature of the global demand is seen

with the different types of the implications for FRS to become more complex for the smaller

4.0 Issue in harmonisation

The main issue in harmonization is seen with compliance of single accounting standard

which are stated below as follows:

4.1 Cultural Obstacles

This is considered with attitudes, religion and various problems of language barrier. The

research considered with Hofstede and Trompenaar has depicted the difference among the

cultural barrier. The auditors of Singapore have seen to eclipse the personal and the close

reaction and rejection of any form of gifts in the business. The differentiated behaviour and

values of the individuals has its implication on the international standards (Oulasvirta & Bailey,

2016).

4.2 Integration Problems

The main problem in the new accounting standard implemented in Singapore is evident

with the FRSs which is implemented in the “beginning on or after January 1, 2003, apart from FRS 39”.

FRS has been further able to show the disclosure valuation for the independent values and

annual valuation process. The other disparity is seen with business combinations, leases,

borrowing cost and different types of the related party transactions (Calmel, 2014).

The recognition criteria for the integration process has been further seen to be evident with the

combinations of both standards. These are seen with of “FRS/SAS 7, FRS 16/SAS 14, FRS

17/SAS 15, FRS 22/SAS 22, FRS 23/SAS 19, FRS 28/SAS 27 and FRS 39/ SAS 33”. In various

cases the disparity in the recognition for the new standard is seen with the exemption like

“Accounting for Investments in Associates”. The implementation of the new method is further

considered with specific exemptions per applying new method for equity in the accounting

method. The FRS recognition criteria has included the goodwill evaluation which is taken into

consideration after the reserves of 1994. This has been further seen to be based on the several

types of the depictions as per the FRS recognition. It is also discerned that FRS does not need to

depict this but in case of SAS the restatement needs to be done accordingly (Ahmed & Ali,

2015).

4.3 Negative impacts on the small business

The integration problem of SAS and FRS is seen as the main problem for the “Small and

medium size entities (SME)” in Singapore. The changing nature of the global demand is seen

with the different types of the implications for FRS to become more complex for the smaller

5SUCCESS OF ACCOUNTING HARMONISATION

companies. The SMEs need to take into account the various type of the considerations for the

companies based in Singapore. The integration of the “Singapore Financial Reporting Standards

(SFRS)” for SE is not considered to accountable publicly and the consideration for the gross

assets is restricted with more than S$10 million (Warren, Moffitt, & Byrnes, 2015).

Moreover, the designated problems of the smaller multinationals have been seen to be

based on the compliance cost percentage of the total revenues in compare to the organizations

which are larger in size. The burgeoning costs in some cases are restricted with the different

types of the aspects to grow and make the significant nature of progress especially for the larger

organizations. The integration process of the different types the accounting standard has seen to

be taken into consideration with the increasing cost of the small business operating in Singapore

(Aarsand & Sandberg, 2014).

4.4 Licensing and Enforcement

The accountants as individuals are able to adhere with the different types of the licensing

process which has been seen to be taken into consideration with the appropriate law-making

body. As per the international council for the accounting the lack of the different aspects has

been seen to be evident with the prosecution actions (Kamla & Haque, 2017).

4.5 Political Grouping

The main issue for the political grouping is seen to be short termed. It is also discerned

that that the political grouping is seen to be appropriate in the emerging countries.

4.6 International Sovereignty Issues

The particular form of the associated concerns has been seen to be based on the differ

types of the depictions which are associated with the CPA licensing laws. In several occasions

the contradicting tax laws, financial regulation and securities laws has been evident with

dictating the appropriate principles of accounting (Bahri, 2014).

5.0 Country Level Analysis

5.1 Rationale for Majority of IFRS in Singapore

The main form of the driving force of the accounting standard in Singapore is

seen with the application of the different types of the standards which are seen to be based on the

significant nature of the depictions as per IASB. IASB is considered to be important with the

companies. The SMEs need to take into account the various type of the considerations for the

companies based in Singapore. The integration of the “Singapore Financial Reporting Standards

(SFRS)” for SE is not considered to accountable publicly and the consideration for the gross

assets is restricted with more than S$10 million (Warren, Moffitt, & Byrnes, 2015).

Moreover, the designated problems of the smaller multinationals have been seen to be

based on the compliance cost percentage of the total revenues in compare to the organizations

which are larger in size. The burgeoning costs in some cases are restricted with the different

types of the aspects to grow and make the significant nature of progress especially for the larger

organizations. The integration process of the different types the accounting standard has seen to

be taken into consideration with the increasing cost of the small business operating in Singapore

(Aarsand & Sandberg, 2014).

4.4 Licensing and Enforcement

The accountants as individuals are able to adhere with the different types of the licensing

process which has been seen to be taken into consideration with the appropriate law-making

body. As per the international council for the accounting the lack of the different aspects has

been seen to be evident with the prosecution actions (Kamla & Haque, 2017).

4.5 Political Grouping

The main issue for the political grouping is seen to be short termed. It is also discerned

that that the political grouping is seen to be appropriate in the emerging countries.

4.6 International Sovereignty Issues

The particular form of the associated concerns has been seen to be based on the differ

types of the depictions which are associated with the CPA licensing laws. In several occasions

the contradicting tax laws, financial regulation and securities laws has been evident with

dictating the appropriate principles of accounting (Bahri, 2014).

5.0 Country Level Analysis

5.1 Rationale for Majority of IFRS in Singapore

The main form of the driving force of the accounting standard in Singapore is

seen with the application of the different types of the standards which are seen to be based on the

significant nature of the depictions as per IASB. IASB is considered to be important with the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6SUCCESS OF ACCOUNTING HARMONISATION

“independent, standard-setting” body of the IFRS. The important objective for IASB is

identified with the harmonization process which are seen to be based on the different types of the

adoption of the worldwide recognition process. IFRS is recognised to issue the majority of the

accounting standards which are based on the significant nature of the depiction taken into

account with the majority of the accounting standard followed in Singapore. In Singapore the

main form of the accounting standard is seen to be depicted with the “Singapore Financial

Reporting Standards (SFRS)” which are in compliance with IFRS. Henceforth, al the companies

need to adhere to the various types of the significant standards which are adhered with the

standards reported on or after 1 January 2003 (Barrett, Mayson, & Bahn, 2014).

5.2 Efforts to Harmonise SAS with FRS

The important form of the initiative for the harmonisation has been taken into account

with “Council on Corporate Disclosure and Governance (“CCDG”)”. The min establishment for

this is further seen to be made in 16 August 2002. The important form of the motive for the

recommendation of the corporate governance models has been closely modelled with the

Financial Reporting Standards (“FRSs”). The essential form of the dissolution is depicted with

the “Accounting Standards Council (ASC)” which are responsible with the “Singapore Financial

Reporting Standards (SFRS)”. The important initiative for ASC is seen with the convergence of

SAS and IFRS for ensuring the global comparability and transparency of the information

(Hellman et al., 2015).

6.0 Case study on Singapore and “Singapore Press Holdings”

6.1 Background of the Company

“Singapore Press Holdings Ltd.” is considered to be a multichannel facility for the overall

advertising system which is based on media organization in Singapore. The business operations

in are further identified with the consideration of the “print, Internet and news media”.

6.2 Implementation process of FRS from Local SRS

Before the implementation of “Financial Reporting Standards (IFRS)”and “SFRS in

2003”, it has been depicted that the important form of the reporting aspects is considered with

the disclosures which is taken into account with the ICPAS and FRS. The advisory committee is

initiated “Ministry of Finance (MOF)” with the “Accountant-General's Department (AGD)”.

“independent, standard-setting” body of the IFRS. The important objective for IASB is

identified with the harmonization process which are seen to be based on the different types of the

adoption of the worldwide recognition process. IFRS is recognised to issue the majority of the

accounting standards which are based on the significant nature of the depiction taken into

account with the majority of the accounting standard followed in Singapore. In Singapore the

main form of the accounting standard is seen to be depicted with the “Singapore Financial

Reporting Standards (SFRS)” which are in compliance with IFRS. Henceforth, al the companies

need to adhere to the various types of the significant standards which are adhered with the

standards reported on or after 1 January 2003 (Barrett, Mayson, & Bahn, 2014).

5.2 Efforts to Harmonise SAS with FRS

The important form of the initiative for the harmonisation has been taken into account

with “Council on Corporate Disclosure and Governance (“CCDG”)”. The min establishment for

this is further seen to be made in 16 August 2002. The important form of the motive for the

recommendation of the corporate governance models has been closely modelled with the

Financial Reporting Standards (“FRSs”). The essential form of the dissolution is depicted with

the “Accounting Standards Council (ASC)” which are responsible with the “Singapore Financial

Reporting Standards (SFRS)”. The important initiative for ASC is seen with the convergence of

SAS and IFRS for ensuring the global comparability and transparency of the information

(Hellman et al., 2015).

6.0 Case study on Singapore and “Singapore Press Holdings”

6.1 Background of the Company

“Singapore Press Holdings Ltd.” is considered to be a multichannel facility for the overall

advertising system which is based on media organization in Singapore. The business operations

in are further identified with the consideration of the “print, Internet and news media”.

6.2 Implementation process of FRS from Local SRS

Before the implementation of “Financial Reporting Standards (IFRS)”and “SFRS in

2003”, it has been depicted that the important form of the reporting aspects is considered with

the disclosures which is taken into account with the ICPAS and FRS. The advisory committee is

initiated “Ministry of Finance (MOF)” with the “Accountant-General's Department (AGD)”.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7SUCCESS OF ACCOUNTING HARMONISATION

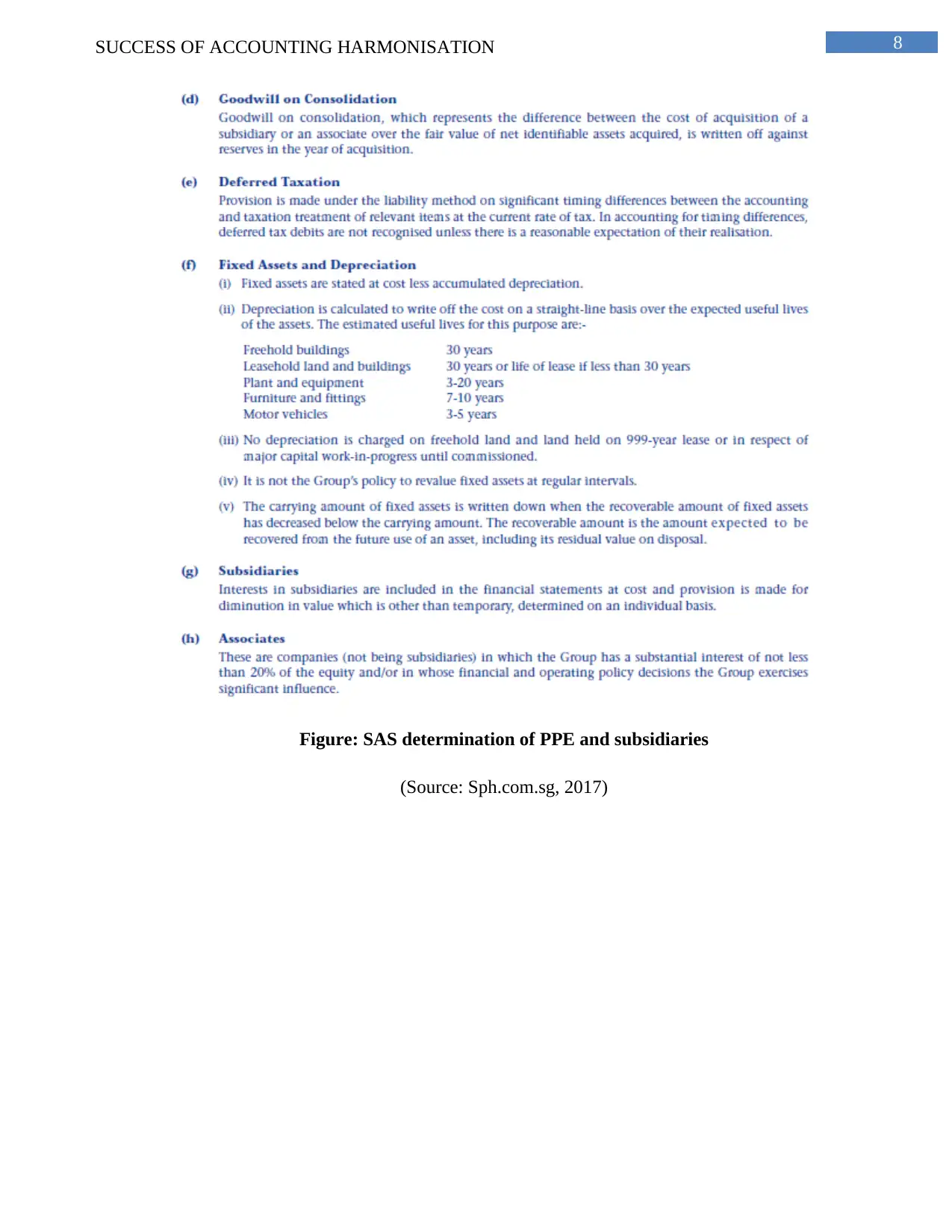

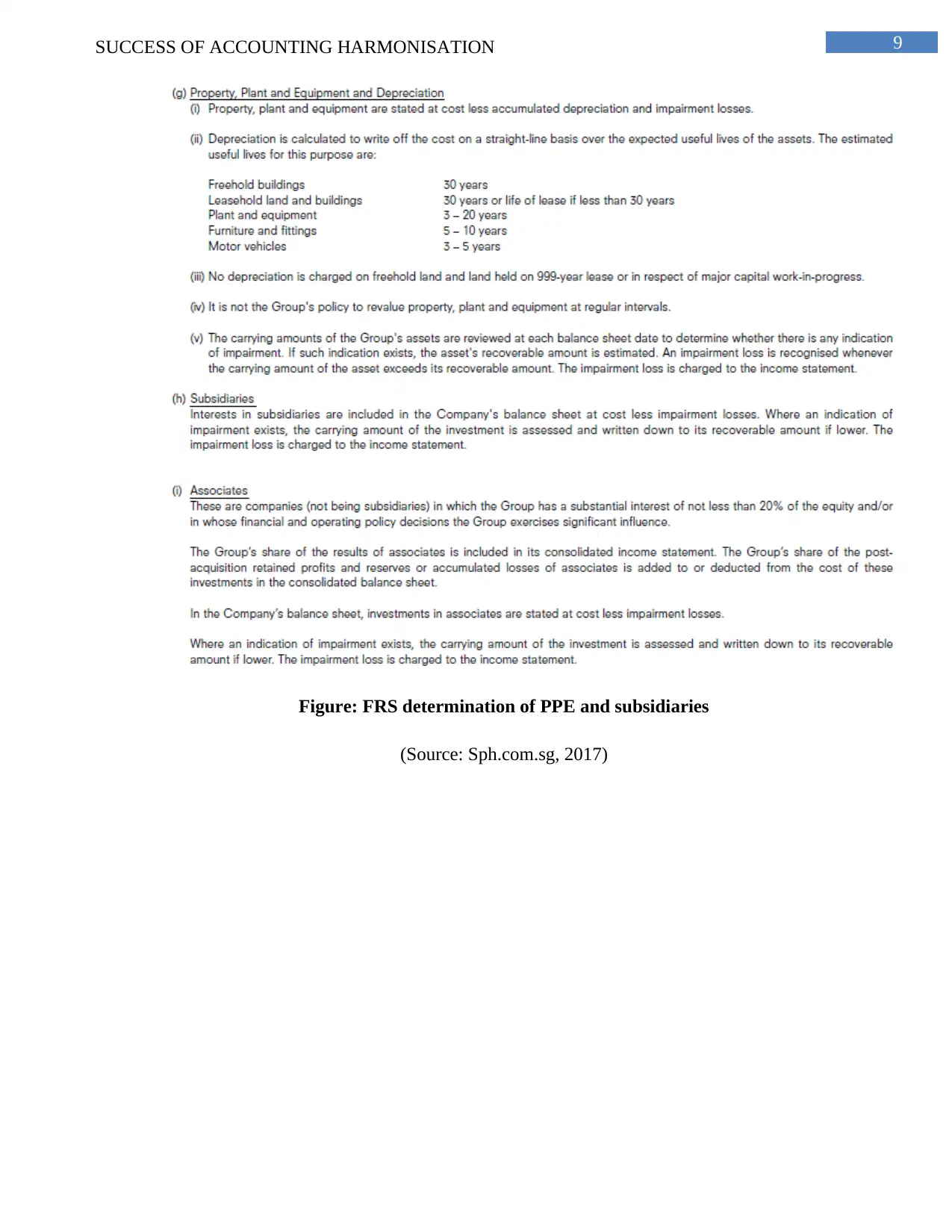

6.3 Before and after harmonisation of impact on the financial statement

The “Singapore Reporting Standard (FRS) 102” has been able to depict that the different

types of the significant considerations for the share based payment which is inclusive of the

expenses which are related to the transactions and grants given to the employees. The post

implementation process of new FRS (on or after January 1, 2003) has been stated with the cost

less accumulated depreciation and impairment losses. The change in the PPE is taken into

consideration as per the estimated useful lives for the furniture and fittings for the next 7-10

years as per the SAS. The revised FRS consideration is based on the estimated useful lives of the

furniture and fittings for the next 5-10 years.

The SAS subsidiaries are included with the financial statements considered with

the cost and provision for the diminution of the value other than the determination of the

individual values. As per the new standards of FRS considerations the interest in the subsidiaries

are based on the balance sheet of the company at a cost less the impairment losses. The various

types of the indication for the impairment has been taken into assessment with the written down

value of the recoverable amount. In this case, the lower is the amount of the impairment losses,

the same has been depicted in the income statement.

The FRS integration for the Goodwill arising for the acquisition has been recorded in the

balance sheet ad put forward to test the impairment as per “FRS 103 – Business combinations” in

FY 2005. This factor has been further seen to be applicable as per reserves considered after 1994.

In this case, the treatment of SAS and SHP is seen to be having the relevant authority for the

external borrowings and the internal resources associated to the finance requirements for the

final purchase or acquisition of the ordinary shares.

6.3 Before and after harmonisation of impact on the financial statement

The “Singapore Reporting Standard (FRS) 102” has been able to depict that the different

types of the significant considerations for the share based payment which is inclusive of the

expenses which are related to the transactions and grants given to the employees. The post

implementation process of new FRS (on or after January 1, 2003) has been stated with the cost

less accumulated depreciation and impairment losses. The change in the PPE is taken into

consideration as per the estimated useful lives for the furniture and fittings for the next 7-10

years as per the SAS. The revised FRS consideration is based on the estimated useful lives of the

furniture and fittings for the next 5-10 years.

The SAS subsidiaries are included with the financial statements considered with

the cost and provision for the diminution of the value other than the determination of the

individual values. As per the new standards of FRS considerations the interest in the subsidiaries

are based on the balance sheet of the company at a cost less the impairment losses. The various

types of the indication for the impairment has been taken into assessment with the written down

value of the recoverable amount. In this case, the lower is the amount of the impairment losses,

the same has been depicted in the income statement.

The FRS integration for the Goodwill arising for the acquisition has been recorded in the

balance sheet ad put forward to test the impairment as per “FRS 103 – Business combinations” in

FY 2005. This factor has been further seen to be applicable as per reserves considered after 1994.

In this case, the treatment of SAS and SHP is seen to be having the relevant authority for the

external borrowings and the internal resources associated to the finance requirements for the

final purchase or acquisition of the ordinary shares.

8SUCCESS OF ACCOUNTING HARMONISATION

Figure: SAS determination of PPE and subsidiaries

(Source: Sph.com.sg, 2017)

Figure: SAS determination of PPE and subsidiaries

(Source: Sph.com.sg, 2017)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9SUCCESS OF ACCOUNTING HARMONISATION

Figure: FRS determination of PPE and subsidiaries

(Source: Sph.com.sg, 2017)

Figure: FRS determination of PPE and subsidiaries

(Source: Sph.com.sg, 2017)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10SUCCESS OF ACCOUNTING HARMONISATION

Figure: SAS treatment combinations

(Source: Sph.com.sg, 2017)

Figure: Business Combinations for FRS

Figure: SAS treatment combinations

(Source: Sph.com.sg, 2017)

Figure: Business Combinations for FRS

11SUCCESS OF ACCOUNTING HARMONISATION

(Source: Sph.com.sg, 2017)

Conclusion and recommendation

The main from of the consideration of the harmonisation in accounting has been

considered with the concept of comparing the financial information with other countries. The

main process for the harmonization are further seen to be vital for the companies those are

willing to operate in the various business environment and multiple regions on a global basis.

The significant issues concerning the harmonisation is regarded with “Cultural Obstacles,

Integration Problems, Negative impacts on the small business, Licensing and Enforcement”.

(Source: Sph.com.sg, 2017)

Conclusion and recommendation

The main from of the consideration of the harmonisation in accounting has been

considered with the concept of comparing the financial information with other countries. The

main process for the harmonization are further seen to be vital for the companies those are

willing to operate in the various business environment and multiple regions on a global basis.

The significant issues concerning the harmonisation is regarded with “Cultural Obstacles,

Integration Problems, Negative impacts on the small business, Licensing and Enforcement”.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.