Fair Value Measurement of Financial Instruments

VerifiedAdded on 2019/09/19

|24

|8151

|468

Report

AI Summary

The assignment content is about the financial statements of a Foundation that invests in short-term instruments and provides healthcare services. The Foundation has a contract with Siemens and affiliated companies, which exceeded purchase commitments totaling $137,400,000. Additionally, the Foundation sold approximately $10 million in MGMTMatrix commercial paper before maturity, but later learned that the bankruptcy counsel filed to nullify redemption of certain MGMTMatrix commercial papers, resulting in a settlement payment of $3,900,000. The financial statements also include information about fair value measurements for assets and liabilities, which are based on observable inputs such as quoted prices and market rates, and unobservable inputs such as model-based techniques using significant assumptions not observable in the market.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Harris Memorial Hospital and Harris Community Foundation

Years Ended December 31, 20X7 and 20X6

Contents

Report of Independent Auditors 225

Combined Financial Statements

Combined Balance Sheets 226

Combined Statements of Operations 227

Combined Statements of Changes in Net Assets 228

Combined Statements of Cash Flows 229

Notes to Combined Financial Statements 231

Report of Independent Auditors—Pennypacker & Vandelay, LLC

The Board of Trustees

Harris Memorial Hospital and Harris Community Foundation

We have audited the accompanying combined balance sheets of Harris

Memorial Hospital and Harris Community Foundation and subsidiaries (the

Foundation) as of December 31, 20X7 and 20X6, and the related combined

statements of operations, changes in net assets, and cash flows for the years

then ended.

Management is responsible for the preparation and fair presentation of the

consolidated financial statements in accordance with accounting principles

generally accepted in the United States of America; this includes the design,

implementation, and maintenance of internal control relevant to the

preparation and fair presentation of consolidated financial statements that

are free from material misstatement, whether due to fraud or error.

Years Ended December 31, 20X7 and 20X6

Contents

Report of Independent Auditors 225

Combined Financial Statements

Combined Balance Sheets 226

Combined Statements of Operations 227

Combined Statements of Changes in Net Assets 228

Combined Statements of Cash Flows 229

Notes to Combined Financial Statements 231

Report of Independent Auditors—Pennypacker & Vandelay, LLC

The Board of Trustees

Harris Memorial Hospital and Harris Community Foundation

We have audited the accompanying combined balance sheets of Harris

Memorial Hospital and Harris Community Foundation and subsidiaries (the

Foundation) as of December 31, 20X7 and 20X6, and the related combined

statements of operations, changes in net assets, and cash flows for the years

then ended.

Management is responsible for the preparation and fair presentation of the

consolidated financial statements in accordance with accounting principles

generally accepted in the United States of America; this includes the design,

implementation, and maintenance of internal control relevant to the

preparation and fair presentation of consolidated financial statements that

are free from material misstatement, whether due to fraud or error.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Our responsibility is to express an opinion on these financial statements

based on our audits. We conducted our audits in accordance with auditing

standards generally accepted in the United States. Those standards require

that we plan and perform the audit to obtain reasonable assurance about

whether the financial statements are free of material misstatement.

An audit involves performing procedures to obtain audit evidence about the

amounts and disclosures in the consolidated financial statements. The

procedures selected depend on our judgment, including the assessment of

the risks of material misstatement of the consolidated financial statements,

whether due to fraud or error. In making this risk assessment, we consider

internal control relevant to the Foundation’s preparation and fair

presentation of the consolidated financial statements in order to design audit

procedures that are appropriate in the circumstances, but not for the

purpose of expressing an opinion on the effectiveness of the Foundation’s

internal control. Accordingly, we express no such opinion. An audit also

includes evaluating the appropriateness of accounting policies used and the

reasonableness of significant accounting estimates made by management,

as well as evaluating the overall presentation of the consolidated financial

statements. We believe that the audit evidence we have obtained is

sufficient and appropriate to provide a basis for our audit opinion.

In our opinion, the financial statements referred to above present fairly, in all

material respects, the combined financial position of Harris Memorial

Hospital and Harris Community Foundation and subsidiaries at December 31,

20X7 and 20X6, and the combined changes in their net assets and their cash

flows for the years then ended in conformity with U.S. generally accepted

accounting principles.

TABLE 9A-1 Harris Memorial Hospital and Harris Community

Foundation Combined Balance Sheets (in Thousands)

December 31,

20X7

December 31,

20X6

Assets

Current assets

based on our audits. We conducted our audits in accordance with auditing

standards generally accepted in the United States. Those standards require

that we plan and perform the audit to obtain reasonable assurance about

whether the financial statements are free of material misstatement.

An audit involves performing procedures to obtain audit evidence about the

amounts and disclosures in the consolidated financial statements. The

procedures selected depend on our judgment, including the assessment of

the risks of material misstatement of the consolidated financial statements,

whether due to fraud or error. In making this risk assessment, we consider

internal control relevant to the Foundation’s preparation and fair

presentation of the consolidated financial statements in order to design audit

procedures that are appropriate in the circumstances, but not for the

purpose of expressing an opinion on the effectiveness of the Foundation’s

internal control. Accordingly, we express no such opinion. An audit also

includes evaluating the appropriateness of accounting policies used and the

reasonableness of significant accounting estimates made by management,

as well as evaluating the overall presentation of the consolidated financial

statements. We believe that the audit evidence we have obtained is

sufficient and appropriate to provide a basis for our audit opinion.

In our opinion, the financial statements referred to above present fairly, in all

material respects, the combined financial position of Harris Memorial

Hospital and Harris Community Foundation and subsidiaries at December 31,

20X7 and 20X6, and the combined changes in their net assets and their cash

flows for the years then ended in conformity with U.S. generally accepted

accounting principles.

TABLE 9A-1 Harris Memorial Hospital and Harris Community

Foundation Combined Balance Sheets (in Thousands)

December 31,

20X7

December 31,

20X6

Assets

Current assets

TABLE 9A-1 Harris Memorial Hospital and Harris Community

Foundation Combined Balance Sheets (in Thousands)

December 31,

20X7

December 31,

20X6

Cash and cash equivalents $82,815 $59,696

Assets limited as to use, current portion 5,327 5,088

Accounts receivable

Patients, less allowance for doubtful accounts

($25,302 in 20X7 and $23,014 in 20X6)

70,025 59,939

Other 28,990 24,995

Supplies 7,078 6,663

Total current assets 194,235 156,381

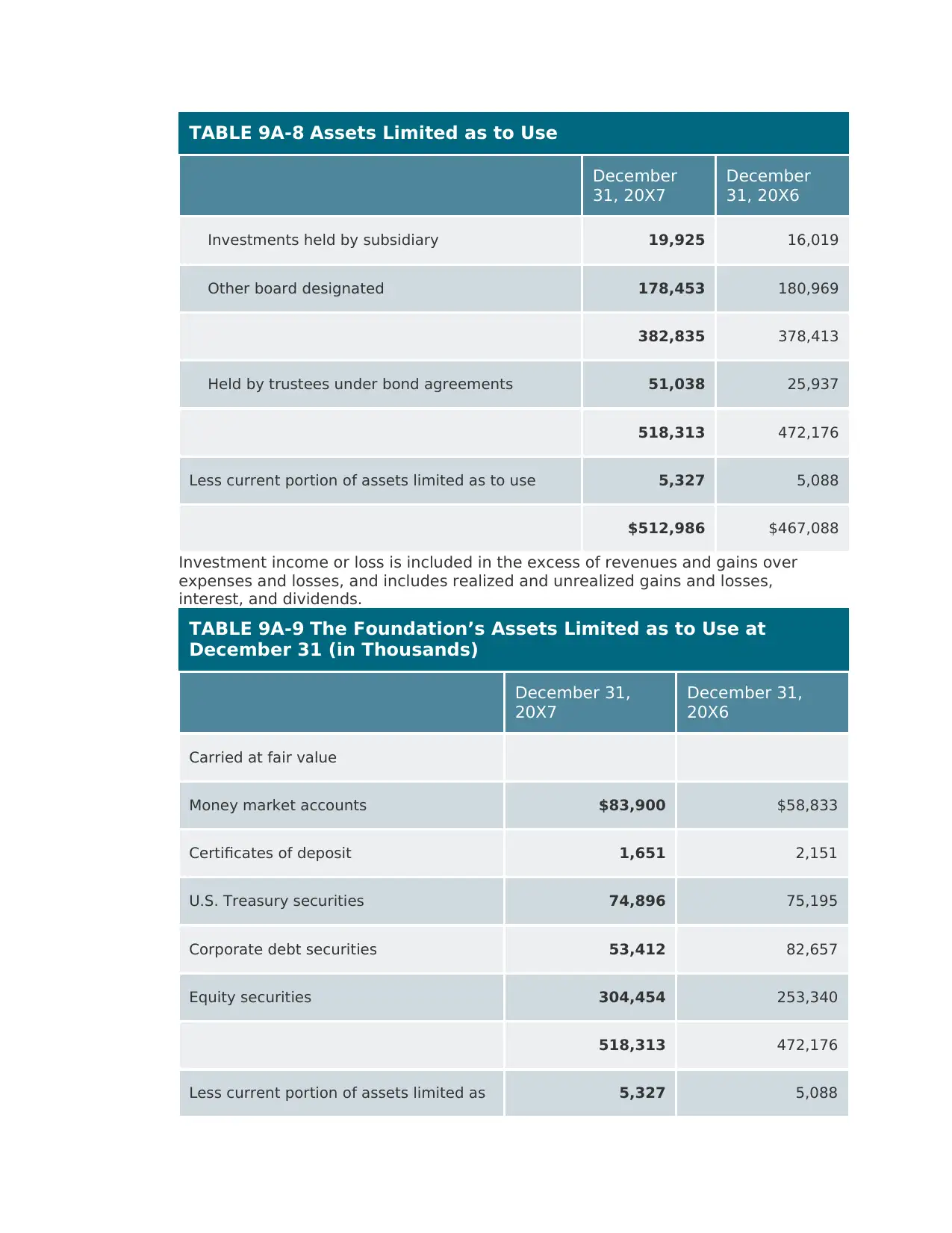

Assets limited as to use

For donor-restricted purposes 84,440 67,826

Board designated for specific purposes 382,835 378,413

Held by trustees under bond agreements 51,038 25,937

518,313 472,176

Less current portion 5,327 5,088

512,986 467,088

Property and equipment, net 563,349 458,829

Other assets 34,476 34,302

Total assets $1,305,046 $1,116,600

Liabilities and net assets

Foundation Combined Balance Sheets (in Thousands)

December 31,

20X7

December 31,

20X6

Cash and cash equivalents $82,815 $59,696

Assets limited as to use, current portion 5,327 5,088

Accounts receivable

Patients, less allowance for doubtful accounts

($25,302 in 20X7 and $23,014 in 20X6)

70,025 59,939

Other 28,990 24,995

Supplies 7,078 6,663

Total current assets 194,235 156,381

Assets limited as to use

For donor-restricted purposes 84,440 67,826

Board designated for specific purposes 382,835 378,413

Held by trustees under bond agreements 51,038 25,937

518,313 472,176

Less current portion 5,327 5,088

512,986 467,088

Property and equipment, net 563,349 458,829

Other assets 34,476 34,302

Total assets $1,305,046 $1,116,600

Liabilities and net assets

TABLE 9A-1 Harris Memorial Hospital and Harris Community

Foundation Combined Balance Sheets (in Thousands)

December 31,

20X7

December 31,

20X6

Current liabilities

Accounts payable $32,572 $24,631

Accrued expenses and other liabilities 58,878 53,725

Due to third-party payers 7,380 12,633

Current maturities of long-term debt 4,692 5,908

Total current liabilities 103,522 96,897

Long-term debt, less current maturities 439,597 332,354

Contingent professional liabilities 33,260 48,487

Due to broker 15,128 19,608

Other liabilities 20,713 5,298

Postretirement benefit obligation, other than pensions 8,207 7,694

Total liabilities 620,427 510,338

Net assets

Unrestricted 600,179 538,436

Temporarily restricted 55,213 40,393

Permanently restricted 29,227 27,433

Total net assets 684,619 606,262

Total liabilities and net assets $1,305,046 $1,116,600

Foundation Combined Balance Sheets (in Thousands)

December 31,

20X7

December 31,

20X6

Current liabilities

Accounts payable $32,572 $24,631

Accrued expenses and other liabilities 58,878 53,725

Due to third-party payers 7,380 12,633

Current maturities of long-term debt 4,692 5,908

Total current liabilities 103,522 96,897

Long-term debt, less current maturities 439,597 332,354

Contingent professional liabilities 33,260 48,487

Due to broker 15,128 19,608

Other liabilities 20,713 5,298

Postretirement benefit obligation, other than pensions 8,207 7,694

Total liabilities 620,427 510,338

Net assets

Unrestricted 600,179 538,436

Temporarily restricted 55,213 40,393

Permanently restricted 29,227 27,433

Total net assets 684,619 606,262

Total liabilities and net assets $1,305,046 $1,116,600

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE 9A-2 Harris Memorial Hospital and Harris Community

Foundation Combined Statements of Operations (in Thousands)

December 31,

20X7

December 31,

20X6

Operating revenues and other support

Net patient service revenue $829,005 $774,662

Provision for doubtful accounts (55,851) (57,975)

Net patient service revenue less provision for

doubtful accounts

773,154 716,687

Other operating revenue 27,055 29,334

Total operating revenue 800,209 746,021

Operating expenses

Salaries and wages $371,449 $329,668

Employee benefits 81,532 77,231

Supplies and purchased services 228,244 225,497

Advertising 3,072 2,376

Staff enrichment 10,767 8,591

Occupancy cost 14,346 13,442

Depreciation 44,392 41,627

Interest 10,974 6,145

Operating expenses 764,776 704,577

Excess of revenue over expenses 35,433 41,444

Nonoperating gains (losses)

Foundation Combined Statements of Operations (in Thousands)

December 31,

20X7

December 31,

20X6

Operating revenues and other support

Net patient service revenue $829,005 $774,662

Provision for doubtful accounts (55,851) (57,975)

Net patient service revenue less provision for

doubtful accounts

773,154 716,687

Other operating revenue 27,055 29,334

Total operating revenue 800,209 746,021

Operating expenses

Salaries and wages $371,449 $329,668

Employee benefits 81,532 77,231

Supplies and purchased services 228,244 225,497

Advertising 3,072 2,376

Staff enrichment 10,767 8,591

Occupancy cost 14,346 13,442

Depreciation 44,392 41,627

Interest 10,974 6,145

Operating expenses 764,776 704,577

Excess of revenue over expenses 35,433 41,444

Nonoperating gains (losses)

TABLE 9A-2 Harris Memorial Hospital and Harris Community

Foundation Combined Statements of Operations (in Thousands)

December 31,

20X7

December 31,

20X6

Contributions, gifts, and bequests 3,189 1,318

Net assets released from restrictions for

research expenditures

14,070 14,474

Research, education, and other nonoperating

expenses

(22,980) (24,773)

Change in interest rate swap value and put

agreements

1,578 9,397

Investment income 30,453 18,402

26,310 18,818

Excess of revenues and gains over expenses and

losses

$61,743 $60,262

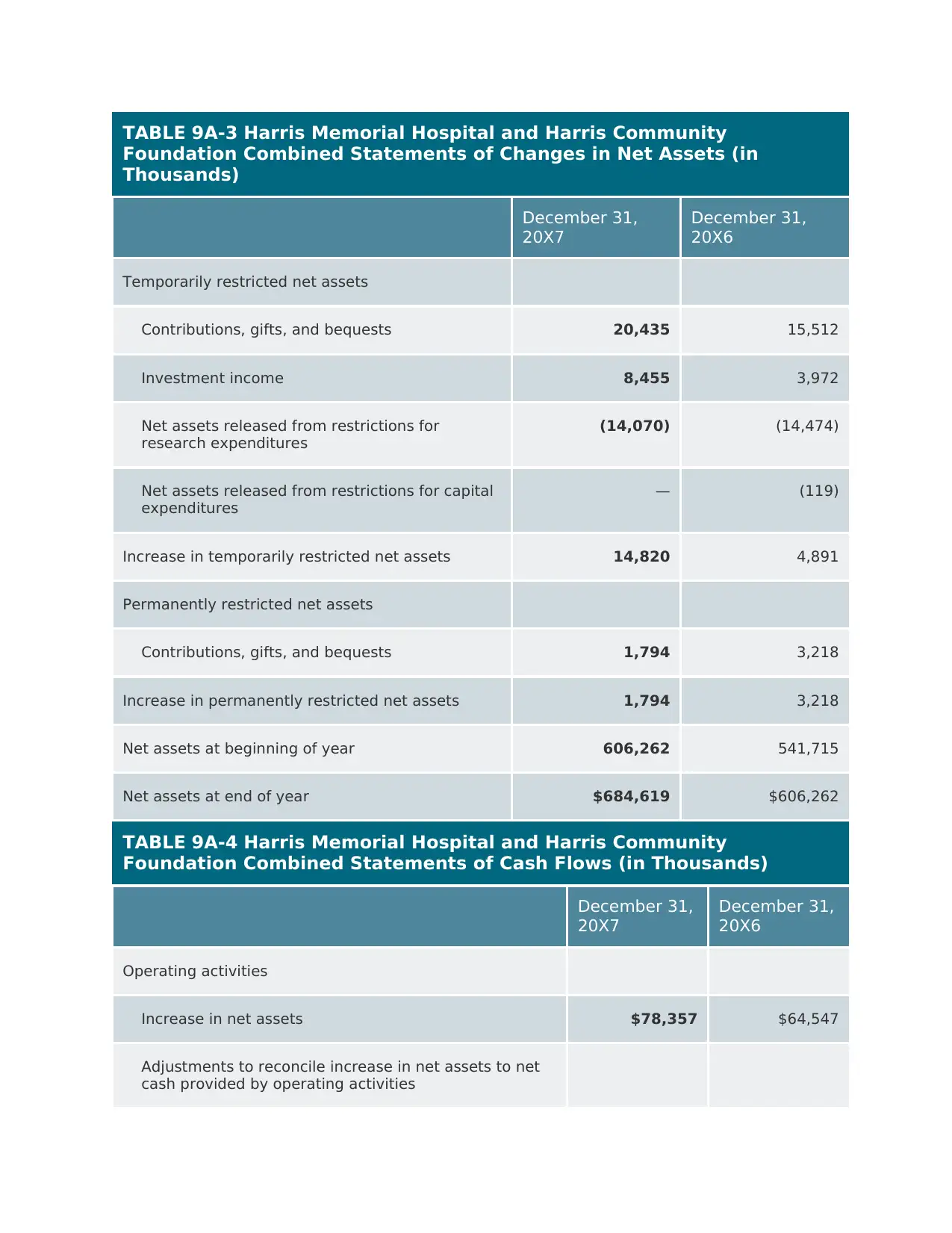

TABLE 9A-3 Harris Memorial Hospital and Harris Community

Foundation Combined Statements of Changes in Net Assets (in

Thousands)

December 31,

20X7

December 31,

20X6

Unrestricted net assets

Excess of revenues and gains over expenses

and losses

$61,743 $60,262

Net assets released from restrictions for capital

expenditures

— 119

Cumulative effect of change in accounting

principle

— (3,943)

Increase in unrestricted net assets 61,743 56,438

Foundation Combined Statements of Operations (in Thousands)

December 31,

20X7

December 31,

20X6

Contributions, gifts, and bequests 3,189 1,318

Net assets released from restrictions for

research expenditures

14,070 14,474

Research, education, and other nonoperating

expenses

(22,980) (24,773)

Change in interest rate swap value and put

agreements

1,578 9,397

Investment income 30,453 18,402

26,310 18,818

Excess of revenues and gains over expenses and

losses

$61,743 $60,262

TABLE 9A-3 Harris Memorial Hospital and Harris Community

Foundation Combined Statements of Changes in Net Assets (in

Thousands)

December 31,

20X7

December 31,

20X6

Unrestricted net assets

Excess of revenues and gains over expenses

and losses

$61,743 $60,262

Net assets released from restrictions for capital

expenditures

— 119

Cumulative effect of change in accounting

principle

— (3,943)

Increase in unrestricted net assets 61,743 56,438

TABLE 9A-3 Harris Memorial Hospital and Harris Community

Foundation Combined Statements of Changes in Net Assets (in

Thousands)

December 31,

20X7

December 31,

20X6

Temporarily restricted net assets

Contributions, gifts, and bequests 20,435 15,512

Investment income 8,455 3,972

Net assets released from restrictions for

research expenditures

(14,070) (14,474)

Net assets released from restrictions for capital

expenditures

— (119)

Increase in temporarily restricted net assets 14,820 4,891

Permanently restricted net assets

Contributions, gifts, and bequests 1,794 3,218

Increase in permanently restricted net assets 1,794 3,218

Net assets at beginning of year 606,262 541,715

Net assets at end of year $684,619 $606,262

TABLE 9A-4 Harris Memorial Hospital and Harris Community

Foundation Combined Statements of Cash Flows (in Thousands)

December 31,

20X7

December 31,

20X6

Operating activities

Increase in net assets $78,357 $64,547

Adjustments to reconcile increase in net assets to net

cash provided by operating activities

Foundation Combined Statements of Changes in Net Assets (in

Thousands)

December 31,

20X7

December 31,

20X6

Temporarily restricted net assets

Contributions, gifts, and bequests 20,435 15,512

Investment income 8,455 3,972

Net assets released from restrictions for

research expenditures

(14,070) (14,474)

Net assets released from restrictions for capital

expenditures

— (119)

Increase in temporarily restricted net assets 14,820 4,891

Permanently restricted net assets

Contributions, gifts, and bequests 1,794 3,218

Increase in permanently restricted net assets 1,794 3,218

Net assets at beginning of year 606,262 541,715

Net assets at end of year $684,619 $606,262

TABLE 9A-4 Harris Memorial Hospital and Harris Community

Foundation Combined Statements of Cash Flows (in Thousands)

December 31,

20X7

December 31,

20X6

Operating activities

Increase in net assets $78,357 $64,547

Adjustments to reconcile increase in net assets to net

cash provided by operating activities

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

TABLE 9A-4 Harris Memorial Hospital and Harris Community

Foundation Combined Statements of Cash Flows (in Thousands)

December 31,

20X7

December 31,

20X6

Change in net unrealized gains and losses on

investment securities

(26,358) 11,432

Cumulative effect of change in accounting principle — (3,943)

Depreciation 44,392 41,627

Gain on sale or disposal of assets, net (6,119) —

Provision for bad debts 55,851 57,975

Change in interest rate swap value and put

agreements

(1,578) (9,397)

Changes in operating assets and liabilities

Assets limited as to use (19,779) (14,274)

Accounts receivable (65,937) (51,251)

Other assets (7,071) (43)

Supplies (415) 840

Accounts payable 7,941 10,613

Accrued expenses and other liabilities 20,568 8,430

Due to third-party payers (5,253) (4,877)

Contingent professional liabilities (15,227) 3,743

Postretirement benefit obligation, other than

pensions

513 456

Net cash provided by operating activities 59,885 115,878

Foundation Combined Statements of Cash Flows (in Thousands)

December 31,

20X7

December 31,

20X6

Change in net unrealized gains and losses on

investment securities

(26,358) 11,432

Cumulative effect of change in accounting principle — (3,943)

Depreciation 44,392 41,627

Gain on sale or disposal of assets, net (6,119) —

Provision for bad debts 55,851 57,975

Change in interest rate swap value and put

agreements

(1,578) (9,397)

Changes in operating assets and liabilities

Assets limited as to use (19,779) (14,274)

Accounts receivable (65,937) (51,251)

Other assets (7,071) (43)

Supplies (415) 840

Accounts payable 7,941 10,613

Accrued expenses and other liabilities 20,568 8,430

Due to third-party payers (5,253) (4,877)

Contingent professional liabilities (15,227) 3,743

Postretirement benefit obligation, other than

pensions

513 456

Net cash provided by operating activities 59,885 115,878

TABLE 9A-4 Harris Memorial Hospital and Harris Community

Foundation Combined Statements of Cash Flows (in Thousands)

December 31,

20X7

December 31,

20X6

Investing activities

Property and equipment acquired (142,793) (159,943)

Cash used in investing activities (142,793) (159,943)

Financing activities

Repayment of long-term debt (177,294) (5,545)

Proceeds from borrowing 283,321 57,614

Net cash provided by financing activities 106,027 52,069

Net increase in cash and cash equivalents 23,119 8,004

Cash and cash equivalents at beginning of year 59,696 51,692

Cash and cash equivalents at end of year $82,815 $59,696

Harris Memorial Hospital and Harris Community Foundation

Notes to Combined Financial Statements

December 31, 20X7

1. Organization and Significant Accounting Policies

Organization and Basis of Combination

Harris Memorial Hospital (the Hospital) and Harris Community Foundation (the

Foundation) are a hospital and charitable foundation located in Jersey, Ohio. The

Hospital and Foundation are exempt from federal income taxes under Section

501(c)(3) of the Internal Revenue Code (IRC). The Hospital and Foundation are

collectively referred to herein as the Foundation.

The Foundation owns and operates the Renee Center, which has 27 skilled nursing

beds; Harris Assurance, Ltd. (Assurance), a for-profit, wholly owned insurance

subsidiary; and Harris Properties (Condit Inn), a for-profit, wholly owned subsidiary.

During 20X6, the Foundation formed the Harris Community Hospital Corporation

(dba Harris Hospital) located in Oldstone, Ohio and the Harris Long Term Acute Care

Hospital Corporation (dba Harris Continuing Care Hospital) located in Jersey, Ohio.

Foundation Combined Statements of Cash Flows (in Thousands)

December 31,

20X7

December 31,

20X6

Investing activities

Property and equipment acquired (142,793) (159,943)

Cash used in investing activities (142,793) (159,943)

Financing activities

Repayment of long-term debt (177,294) (5,545)

Proceeds from borrowing 283,321 57,614

Net cash provided by financing activities 106,027 52,069

Net increase in cash and cash equivalents 23,119 8,004

Cash and cash equivalents at beginning of year 59,696 51,692

Cash and cash equivalents at end of year $82,815 $59,696

Harris Memorial Hospital and Harris Community Foundation

Notes to Combined Financial Statements

December 31, 20X7

1. Organization and Significant Accounting Policies

Organization and Basis of Combination

Harris Memorial Hospital (the Hospital) and Harris Community Foundation (the

Foundation) are a hospital and charitable foundation located in Jersey, Ohio. The

Hospital and Foundation are exempt from federal income taxes under Section

501(c)(3) of the Internal Revenue Code (IRC). The Hospital and Foundation are

collectively referred to herein as the Foundation.

The Foundation owns and operates the Renee Center, which has 27 skilled nursing

beds; Harris Assurance, Ltd. (Assurance), a for-profit, wholly owned insurance

subsidiary; and Harris Properties (Condit Inn), a for-profit, wholly owned subsidiary.

During 20X6, the Foundation formed the Harris Community Hospital Corporation

(dba Harris Hospital) located in Oldstone, Ohio and the Harris Long Term Acute Care

Hospital Corporation (dba Harris Continuing Care Hospital) located in Jersey, Ohio.

The 60-bed Harris Continuing Care Hospital opened in May 20X7. Harris Hospital,

with 92 beds, opened in late July 20X7. At December 31, 20X7, the Foundation has

remaining commitments totaling approximately $7,360,000 under construction

contracts for these and other capital projects.

The Foundation is affiliated with the Harris Health Plan (the Health Plan). The Health

Plan’s financial statements are not included in these combined financial statements.

The Foundation provides healthcare services in the central Ohio region. All

appropriate intercompany accounts have been eliminated in combination.

Cash Equivalents

The Foundation considers all undesignated highly liquid investments with maturities

of 3 months or less when purchased to be cash equivalents.

Supplies

Supplies are stated at cost (first-in, first-out method), which is not in excess of

market value.

Patient Accounts Receivable

Patient accounts receivable are stated at estimated net realizable value. Significant

concentrations of patient accounts receivable were 20% and 19% at December 31,

20X7 and 20X6, respectively, from government-related programs. Patient accounts

receivable from the Health Plan were 25% and 29% at December 31, 20X7 and

20X6, respectively.

The Foundation maintains allowances for uncollectable accounts for estimated

losses resulting from a payer’s inability to make payments on accounts. The

Foundation uses a balance sheet approach to value the allowance account based on

historical write-offs, payer type, and the aging of the accounts. Accounts are written

off when collection efforts have been exhausted. Management continually monitors

and adjusts, as necessary, allowances associated with its receivables. The majority

of uncollectable accounts are from uninsured and the patient portion of accounts

receivable.

Assets Limited as to Use

Assets limited as to use at December 31, 20X7, include 76% and 9% held under

master trust agreements with Liberty Eagle Trust and Highbanks, respectively, and

15% held in government-insured time deposits and other financial instruments.

Assets limited as to use at December 31, 20X6, include 78% and 5% held under

master trust agreements with Liberty Eagle Trust and Highbanks, respectively, and

17% held in government-insured time deposits and other financial instruments. The

investments held under the master trust agreements are diversified among equity,

debt, and money market instruments and are reported at estimated fair value. The

fair value of these investments is generally based on quoted market prices on

national exchanges.

Property and Equipment

Property and equipment are recorded at cost at the date of acquisition or estimated

fair value at the date of donation. Depreciation is computed on the straight-line

method using the estimated economic lives of the depreciable assets, generally

ranging from 3 to 40 years. Expenditures that materially increase values, change

capacities, or extend useful lives are capitalized. Routine maintenance and repair

items are charged to operating expenses.

The Foundation evaluates whether events and circumstances have occurred that

indicate the remaining estimated useful life of long-lived assets may warrant

revision or that the remaining balance of an asset may not be recoverable. The

assessment of possible impairment is based on whether the carrying amount of the

asset exceeds the expected total undiscounted value of cash flows expected to

result from the use of the assets and their eventual disposition. No amounts were

recognized in 20X6.

with 92 beds, opened in late July 20X7. At December 31, 20X7, the Foundation has

remaining commitments totaling approximately $7,360,000 under construction

contracts for these and other capital projects.

The Foundation is affiliated with the Harris Health Plan (the Health Plan). The Health

Plan’s financial statements are not included in these combined financial statements.

The Foundation provides healthcare services in the central Ohio region. All

appropriate intercompany accounts have been eliminated in combination.

Cash Equivalents

The Foundation considers all undesignated highly liquid investments with maturities

of 3 months or less when purchased to be cash equivalents.

Supplies

Supplies are stated at cost (first-in, first-out method), which is not in excess of

market value.

Patient Accounts Receivable

Patient accounts receivable are stated at estimated net realizable value. Significant

concentrations of patient accounts receivable were 20% and 19% at December 31,

20X7 and 20X6, respectively, from government-related programs. Patient accounts

receivable from the Health Plan were 25% and 29% at December 31, 20X7 and

20X6, respectively.

The Foundation maintains allowances for uncollectable accounts for estimated

losses resulting from a payer’s inability to make payments on accounts. The

Foundation uses a balance sheet approach to value the allowance account based on

historical write-offs, payer type, and the aging of the accounts. Accounts are written

off when collection efforts have been exhausted. Management continually monitors

and adjusts, as necessary, allowances associated with its receivables. The majority

of uncollectable accounts are from uninsured and the patient portion of accounts

receivable.

Assets Limited as to Use

Assets limited as to use at December 31, 20X7, include 76% and 9% held under

master trust agreements with Liberty Eagle Trust and Highbanks, respectively, and

15% held in government-insured time deposits and other financial instruments.

Assets limited as to use at December 31, 20X6, include 78% and 5% held under

master trust agreements with Liberty Eagle Trust and Highbanks, respectively, and

17% held in government-insured time deposits and other financial instruments. The

investments held under the master trust agreements are diversified among equity,

debt, and money market instruments and are reported at estimated fair value. The

fair value of these investments is generally based on quoted market prices on

national exchanges.

Property and Equipment

Property and equipment are recorded at cost at the date of acquisition or estimated

fair value at the date of donation. Depreciation is computed on the straight-line

method using the estimated economic lives of the depreciable assets, generally

ranging from 3 to 40 years. Expenditures that materially increase values, change

capacities, or extend useful lives are capitalized. Routine maintenance and repair

items are charged to operating expenses.

The Foundation evaluates whether events and circumstances have occurred that

indicate the remaining estimated useful life of long-lived assets may warrant

revision or that the remaining balance of an asset may not be recoverable. The

assessment of possible impairment is based on whether the carrying amount of the

asset exceeds the expected total undiscounted value of cash flows expected to

result from the use of the assets and their eventual disposition. No amounts were

recognized in 20X6.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

In 20X7, the Foundation recorded a charge of $4,000,000, net of reimbursement, for

unrecoverable costs incurred in connection with repair and maintenance costs of

the Condit Inn.

Derivative Financial Instruments

The Foundation accounts for its derivatives under Statement of Financial Accounting

Standards No. 133, Accounting for Derivative Instruments and Hedging Activities, or

SFAS No. 133. SFAS No. 133 requires that all derivative financial instruments that

qualify for hedge accounting be recognized in the financial statements and

measured at fair value regardless of the purpose or intent for holding them.

Changes in the fair value of derivative financial instruments are recognized

periodically either in operations or in changes in unrestricted net assets. The

Foundation’s policy is to not hold or issue derivatives for trading purposes and to

avoid derivatives with leverage features.

Restricted Support

The Foundation records unconditional promises of cash or other assets at estimated

fair value on the date the promises are received. The Foundation reports gifts of

cash and other assets as restricted support if they are received with donor

stipulations that limit the use of the donated assets. When a donor restriction

expires, that is, when a stipulated time restriction ends or a purpose of restriction is

accomplished, temporarily restricted net assets are reclassified to unrestricted net

assets and reported in the combined statements of operations or combined

statements of changes in net assets (based on nature of restriction) as net assets

released from restrictions.

The Foundation reports gifts of land, buildings, and equipment as unrestricted

support unless explicit donor stipulations specify how the donated assets must be

used. Gifts of long-lived assets with explicit restrictions that specify how the assets

are to be used and gifts of cash or other assets that must be used to acquire long-

lived assets are reported as restricted support. The Foundation reports expirations

of donor restrictions when the donated or acquired long-lived assets are placed in

service.

Permanently restricted net assets have been restricted by donors to be maintained

by the Foundation in perpetuity. The income from permanently restricted net assets

is recorded as unrestricted unless explicitly restricted by donors. Donor-restricted

income on permanently restricted net assets is generally available to support

research and education and is reported as temporarily restricted.

The Foundation’s temporarily restricted net assets are restricted primarily for

research, education, capital projects, and medical care programs and its

permanently restricted net assets are primarily restricted for endowment purposes.

Net Patient Service Revenue

Net patient service revenue is reported at estimated net realizable amounts from

patients, third-party payers, and others for services rendered and includes

estimated retroactive revenue adjustments due to future audits, reviews, and

investigations. Retroactive adjustments are considered in the recognition of

revenue on an estimated basis in the period the related services are rendered, and

such amounts are adjusted in future periods as adjustments become known or as

years are no longer subject to such audits, reviews, and investigations.

Charity Care

The Foundation provides care without charge or at amounts less than its

established rates to patients who meet certain criteria under its charity policy.

Because the Foundation does not pursue collection of amounts determined to

qualify as charity care, they are not reported as revenue. Hospital charges foregone

for charity care, based on established rates, were approximately $35,200,000 in

20X7, prior to application of disproportionate share funds of approximately

$4,800,000 received from the State of Ohio, and $35,300,000 in 20X6, prior to

application of disproportionate share funds of approximately $5,800,000 received

unrecoverable costs incurred in connection with repair and maintenance costs of

the Condit Inn.

Derivative Financial Instruments

The Foundation accounts for its derivatives under Statement of Financial Accounting

Standards No. 133, Accounting for Derivative Instruments and Hedging Activities, or

SFAS No. 133. SFAS No. 133 requires that all derivative financial instruments that

qualify for hedge accounting be recognized in the financial statements and

measured at fair value regardless of the purpose or intent for holding them.

Changes in the fair value of derivative financial instruments are recognized

periodically either in operations or in changes in unrestricted net assets. The

Foundation’s policy is to not hold or issue derivatives for trading purposes and to

avoid derivatives with leverage features.

Restricted Support

The Foundation records unconditional promises of cash or other assets at estimated

fair value on the date the promises are received. The Foundation reports gifts of

cash and other assets as restricted support if they are received with donor

stipulations that limit the use of the donated assets. When a donor restriction

expires, that is, when a stipulated time restriction ends or a purpose of restriction is

accomplished, temporarily restricted net assets are reclassified to unrestricted net

assets and reported in the combined statements of operations or combined

statements of changes in net assets (based on nature of restriction) as net assets

released from restrictions.

The Foundation reports gifts of land, buildings, and equipment as unrestricted

support unless explicit donor stipulations specify how the donated assets must be

used. Gifts of long-lived assets with explicit restrictions that specify how the assets

are to be used and gifts of cash or other assets that must be used to acquire long-

lived assets are reported as restricted support. The Foundation reports expirations

of donor restrictions when the donated or acquired long-lived assets are placed in

service.

Permanently restricted net assets have been restricted by donors to be maintained

by the Foundation in perpetuity. The income from permanently restricted net assets

is recorded as unrestricted unless explicitly restricted by donors. Donor-restricted

income on permanently restricted net assets is generally available to support

research and education and is reported as temporarily restricted.

The Foundation’s temporarily restricted net assets are restricted primarily for

research, education, capital projects, and medical care programs and its

permanently restricted net assets are primarily restricted for endowment purposes.

Net Patient Service Revenue

Net patient service revenue is reported at estimated net realizable amounts from

patients, third-party payers, and others for services rendered and includes

estimated retroactive revenue adjustments due to future audits, reviews, and

investigations. Retroactive adjustments are considered in the recognition of

revenue on an estimated basis in the period the related services are rendered, and

such amounts are adjusted in future periods as adjustments become known or as

years are no longer subject to such audits, reviews, and investigations.

Charity Care

The Foundation provides care without charge or at amounts less than its

established rates to patients who meet certain criteria under its charity policy.

Because the Foundation does not pursue collection of amounts determined to

qualify as charity care, they are not reported as revenue. Hospital charges foregone

for charity care, based on established rates, were approximately $35,200,000 in

20X7, prior to application of disproportionate share funds of approximately

$4,800,000 received from the State of Ohio, and $35,300,000 in 20X6, prior to

application of disproportionate share funds of approximately $5,800,000 received

from the State of Ohio. Clinic charges forgone for charity care, based on established

rates, were $12,525,000 and $10,216,000 in 20X7 and 20X6, respectively.

Health Insurance Program Reimbursement

Revenue from the Medicare and Medicaid programs accounted for approximately

45% and 8%, respectively, of the Foundation’s net patient service revenue for the

year ended December 31, 20X7, and 51% and 11%, respectively, for the year ended

December 31, 20X6. Laws and regulations governing the Medicare and Medicaid

programs are extremely complex and are subject to interpretation. Federal

regulations require the submission of annual cost reports covering medical costs

and expenses associated with services provided to program beneficiaries. Medicare

and Medicaid cost report settlements are estimated in the period services are

provided to beneficiaries. As a result, there is at least a reasonable possibility that

recorded estimates will change by a material amount in the near term. The 20X7

and 20X6 net patient service revenue increased (decreased) approximately

$10,340,000 and $(1,332,000), respectively, due to changes in allowances

previously estimated as a result of the final settlements for years that are no longer

subject to audits, reviews, and investigations. The Foundation believes that it is in

compliance with all applicable laws and regulations and is not aware of any pending

or threatened investigations involving allegations of potential wrongdoing.

Medicare cost reports filed by the Hospital for all years before 20X4 have been

audited and settled as of December 31, 20X7. Medicare cost reports filed by the

Clinic for all years before 20X0 have been audited and settled as of December 31,

20X7. Amounts due to the Medicare and Medicaid programs totaled approximately

$7,380,000 and $12,633,000 at December 31, 20X7 and 20X6, respectively, and

are included in due to third-party payers in the accompanying combined balance

sheets.

Nonoperating Gains and Losses

Nonoperating gains and losses include unrestricted contributions, gifts and

bequests, interest earnings on investments, net assets released from restrictions for

research and education expenditures (net of contributions for such expenditures),

change in interest rate swap value and put agreements, and other gains and losses

unrelated to the Foundation’s primary operations.

Excess of Revenues and Gains over Expenses and Losses

Included in excess of revenues and gains over expenses and losses in the

accompanying combined statements of operations are all changes in unrestricted

net assets other than net assets released from restrictions for capital expenditures,

unrealized gains and losses on investments other than trading investment

securities, and investment returns restricted by donors.

Use of Estimates

The preparation of financial statements in conformity with accounting principles

generally accepted in the United States requires management to make estimates

and assumptions that affect the amounts reported in the combined financial

statements and accompanying notes. Actual results could differ from those

estimates.

Other

Certain reclassifications of donor trust liabilities, previously included in assets

limited as to use, were made to the 20X6 combined financial statements to conform

to the 20X7 presentation.

Additionally, in previous years, the Foundation’s investment portfolio (see Note 7)

was classified as other than trading. As such, unrealized gains and losses that were

considered temporary were excluded from excess of revenues and gains over

expenses and losses. During fiscal year 20X7, the Foundation determined that

substantially all of its investment portfolio was more accurately classified as trading

with unrealized gains and losses included in excess of revenues and gains over

expenses and losses. Therefore, a reclassification was made in the accompanying

rates, were $12,525,000 and $10,216,000 in 20X7 and 20X6, respectively.

Health Insurance Program Reimbursement

Revenue from the Medicare and Medicaid programs accounted for approximately

45% and 8%, respectively, of the Foundation’s net patient service revenue for the

year ended December 31, 20X7, and 51% and 11%, respectively, for the year ended

December 31, 20X6. Laws and regulations governing the Medicare and Medicaid

programs are extremely complex and are subject to interpretation. Federal

regulations require the submission of annual cost reports covering medical costs

and expenses associated with services provided to program beneficiaries. Medicare

and Medicaid cost report settlements are estimated in the period services are

provided to beneficiaries. As a result, there is at least a reasonable possibility that

recorded estimates will change by a material amount in the near term. The 20X7

and 20X6 net patient service revenue increased (decreased) approximately

$10,340,000 and $(1,332,000), respectively, due to changes in allowances

previously estimated as a result of the final settlements for years that are no longer

subject to audits, reviews, and investigations. The Foundation believes that it is in

compliance with all applicable laws and regulations and is not aware of any pending

or threatened investigations involving allegations of potential wrongdoing.

Medicare cost reports filed by the Hospital for all years before 20X4 have been

audited and settled as of December 31, 20X7. Medicare cost reports filed by the

Clinic for all years before 20X0 have been audited and settled as of December 31,

20X7. Amounts due to the Medicare and Medicaid programs totaled approximately

$7,380,000 and $12,633,000 at December 31, 20X7 and 20X6, respectively, and

are included in due to third-party payers in the accompanying combined balance

sheets.

Nonoperating Gains and Losses

Nonoperating gains and losses include unrestricted contributions, gifts and

bequests, interest earnings on investments, net assets released from restrictions for

research and education expenditures (net of contributions for such expenditures),

change in interest rate swap value and put agreements, and other gains and losses

unrelated to the Foundation’s primary operations.

Excess of Revenues and Gains over Expenses and Losses

Included in excess of revenues and gains over expenses and losses in the

accompanying combined statements of operations are all changes in unrestricted

net assets other than net assets released from restrictions for capital expenditures,

unrealized gains and losses on investments other than trading investment

securities, and investment returns restricted by donors.

Use of Estimates

The preparation of financial statements in conformity with accounting principles

generally accepted in the United States requires management to make estimates

and assumptions that affect the amounts reported in the combined financial

statements and accompanying notes. Actual results could differ from those

estimates.

Other

Certain reclassifications of donor trust liabilities, previously included in assets

limited as to use, were made to the 20X6 combined financial statements to conform

to the 20X7 presentation.

Additionally, in previous years, the Foundation’s investment portfolio (see Note 7)

was classified as other than trading. As such, unrealized gains and losses that were

considered temporary were excluded from excess of revenues and gains over

expenses and losses. During fiscal year 20X7, the Foundation determined that

substantially all of its investment portfolio was more accurately classified as trading

with unrealized gains and losses included in excess of revenues and gains over

expenses and losses. Therefore, a reclassification was made in the accompanying

20X6 combined financial statements to reflect this change in classification. A net

unrealized loss of approximately $9,183,000 was reclassified from change in net

unrealized gains and losses on investment securities to investment income.

2. Contingent Professional Liabilities

The Foundation self-insures substantially all of its professional liability risk through

its wholly owned insurance subsidiary. A commercial insurance policy is maintained

to insure claims exceeding $7,000,000 individually or $35,000,000 in the aggregate

in 20X7 on a claims-made basis. Contingent professional liabilities are recorded for

incurred but not reported claims and reported claims based on estimates by

independent actuaries. Management established a fund for the purpose of setting

aside assets based on estimates made by independent actuaries, and these funds

are reported in the combined balance sheets as assets limited as to use.

3. Property and Equipment

TABLE 9A-5 Property and Equipment and Related Accumulated

Depreciation (in Thousands)

December 31,

20X7

December 31,

20X6

Land and improvements $26,945 $26,610

Buildings and improvements

expenditures

447,897 265,965

Fixed and movable equipment 469,441 427,882

Construction-in-progress 112,880 189,807

1,057,163 910,264

Less accumulated depreciation 493,814 451,435

$563,349 $458,829

4. Long-Term Debt

In July 20X7, the Foundation issued the Series 20X7 LTACH Revenue Bonds totaling

$15,700,000. The Series 20X7 LTACH Revenue Bonds are due July 20X2 with

principal and interest payments due monthly. Interest accrues at 65% of LIBOR plus

100 basis points. Effective with the issuance of the bonds, the Foundation entered

into a fixed rate swap agreement for the amount of the bonds by which the

Foundation pays a fixed rate of interest of 4.55%. The change in fair value for the

period ended December 31, 20X7 was not significant to the increase in net assets.

In November 20X6, the Foundation issued Series 20X6 Revenue Bonds with a par

amount of $233,350,000. Proceeds were used to advance refund $31,280,000 of

the Series 20X0A Revenue Bonds, current refund $58,410,000 of the Series 20X1

Revenue Bonds, and finance and/or refinance expansion projects. The Series 20X6

Bonds were issued as Auction Rate Securities and generally bear interest for

successive 7-day auction periods at interest rates determined through Dutch

auctions on the business day preceding the auction period. Any series or subseries

of the Series 20X6 Revenue Bonds may be converted at the option of the

unrealized loss of approximately $9,183,000 was reclassified from change in net

unrealized gains and losses on investment securities to investment income.

2. Contingent Professional Liabilities

The Foundation self-insures substantially all of its professional liability risk through

its wholly owned insurance subsidiary. A commercial insurance policy is maintained

to insure claims exceeding $7,000,000 individually or $35,000,000 in the aggregate

in 20X7 on a claims-made basis. Contingent professional liabilities are recorded for

incurred but not reported claims and reported claims based on estimates by

independent actuaries. Management established a fund for the purpose of setting

aside assets based on estimates made by independent actuaries, and these funds

are reported in the combined balance sheets as assets limited as to use.

3. Property and Equipment

TABLE 9A-5 Property and Equipment and Related Accumulated

Depreciation (in Thousands)

December 31,

20X7

December 31,

20X6

Land and improvements $26,945 $26,610

Buildings and improvements

expenditures

447,897 265,965

Fixed and movable equipment 469,441 427,882

Construction-in-progress 112,880 189,807

1,057,163 910,264

Less accumulated depreciation 493,814 451,435

$563,349 $458,829

4. Long-Term Debt

In July 20X7, the Foundation issued the Series 20X7 LTACH Revenue Bonds totaling

$15,700,000. The Series 20X7 LTACH Revenue Bonds are due July 20X2 with

principal and interest payments due monthly. Interest accrues at 65% of LIBOR plus

100 basis points. Effective with the issuance of the bonds, the Foundation entered

into a fixed rate swap agreement for the amount of the bonds by which the

Foundation pays a fixed rate of interest of 4.55%. The change in fair value for the

period ended December 31, 20X7 was not significant to the increase in net assets.

In November 20X6, the Foundation issued Series 20X6 Revenue Bonds with a par

amount of $233,350,000. Proceeds were used to advance refund $31,280,000 of

the Series 20X0A Revenue Bonds, current refund $58,410,000 of the Series 20X1

Revenue Bonds, and finance and/or refinance expansion projects. The Series 20X6

Bonds were issued as Auction Rate Securities and generally bear interest for

successive 7-day auction periods at interest rates determined through Dutch

auctions on the business day preceding the auction period. Any series or subseries

of the Series 20X6 Revenue Bonds may be converted at the option of the

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Foundation, subject to certain restrictions, to bonds that bear interest in different

rate periods, including daily, weekly, flexible, term, or fixed rate periods. The Series

20X6 Revenue Bonds contain certain restrictive covenants, including minimum

levels of debt service coverage. Management believes the Foundation is in

compliance with all covenants.

TABLE 9A-6 Long-Term Debt (in Thousands)

December

31, 20X7

December

31, 20X6

Revenue bonds, LTACH Series 20X7; interest at 65% of

LIBOR plus100 basis points (4.647% at December 31,

20X7); principal and interest payable monthly through July

20X2

$15,679 $—

Revenue bonds, Series 20X6A-1; interest accrues for

successive7-day auction periods at interest rates

determined through Dutch auctions (3.800% at December

31, 20X7)

42,375 —

Revenue bonds, Series 20X6A-2; interest accrues for

successive7-day auction periods at interest rates

determined through Dutch auctions (3.800% at December

31, 20X7)

42,400 —

Revenue bonds, Series 20X6B; interest accrues for

successive 7-day auction periods at interest rates

determined through Dutch auctions (3.850% at December

31, 20X7)

56,550 —

Revenue bonds, Series 20X6C; interest accrues for

successive 7-day auction periods at interest rates

determined through Dutch auctions (3.850% at December

31, 20X7)

55,275 —

Revenue bonds, Series 20X6D; interest accrues for

successive 7-day auction periods at interest rates

determined through Dutch auctions (3.900% at December

31, 20X7)

36,750 —

Revenue bonds, Series 20X1; interest accrues at a daily

rate determined by the remarketing agent (3.960% at

December 31, 20X7); interest and principal payable

annually through 20X1 (principal payments began in

20X6)

90,360 151,800

Revenue bonds, Series 20X0A; interest at 5.375%;

interest and principal payable annually through 20X9

2,700 35,230

rate periods, including daily, weekly, flexible, term, or fixed rate periods. The Series

20X6 Revenue Bonds contain certain restrictive covenants, including minimum

levels of debt service coverage. Management believes the Foundation is in

compliance with all covenants.

TABLE 9A-6 Long-Term Debt (in Thousands)

December

31, 20X7

December

31, 20X6

Revenue bonds, LTACH Series 20X7; interest at 65% of

LIBOR plus100 basis points (4.647% at December 31,

20X7); principal and interest payable monthly through July

20X2

$15,679 $—

Revenue bonds, Series 20X6A-1; interest accrues for

successive7-day auction periods at interest rates

determined through Dutch auctions (3.800% at December

31, 20X7)

42,375 —

Revenue bonds, Series 20X6A-2; interest accrues for

successive7-day auction periods at interest rates

determined through Dutch auctions (3.800% at December

31, 20X7)

42,400 —

Revenue bonds, Series 20X6B; interest accrues for

successive 7-day auction periods at interest rates

determined through Dutch auctions (3.850% at December

31, 20X7)

56,550 —

Revenue bonds, Series 20X6C; interest accrues for

successive 7-day auction periods at interest rates

determined through Dutch auctions (3.850% at December

31, 20X7)

55,275 —

Revenue bonds, Series 20X6D; interest accrues for

successive 7-day auction periods at interest rates

determined through Dutch auctions (3.900% at December

31, 20X7)

36,750 —

Revenue bonds, Series 20X1; interest accrues at a daily

rate determined by the remarketing agent (3.960% at

December 31, 20X7); interest and principal payable

annually through 20X1 (principal payments began in

20X6)

90,360 151,800

Revenue bonds, Series 20X0A; interest at 5.375%;

interest and principal payable annually through 20X9

2,700 35,230

TABLE 9A-6 Long-Term Debt (in Thousands)

December

31, 20X7

December

31, 20X6

Revenue bonds, Series 20X0B; interest accrues at a daily

rate determined by the remarketing agent (3.960% at

December 31, 20X7); interest and principal payable

annually through 20X9

83,200 84,500

Line of credit 19,000 46,686

Interim construction loan — 7,000

Other — 13,046

444,289 338,262

Less current maturities 4,692 5,908

$439,597 $332,354

In January 20X6, the Foundation entered into a revolving line of credit with Bank of

Central Ohio to fund interim construction costs and provide for liquidity and other

short-term needs. In accordance with terms of the loan agreement, the total

available for borrowing was decreased from $70,000,000 to $30,000,000 30 days

following the issuance of the Series 20X6 Revenue Bonds. The total amount drawn

as of December 31, 20X7 was $19,000,000. Interest is payable quarterly at a rate

equal to the lesser of the maximum lawful rate or LIBOR plus 15 basis points (5.71%

at December 31, 20X7). Amounts drawn are due in full June 25, 20X9.

The Foundation issued Series 20X1 Revenue Bonds with a par amount of

$158,000,000 that were partially refunded in November 20X6. The net proceeds

were used to fund expansion projects.

The Foundation issued Series 20X0A Revenue Bonds with a par amount of

$42,025,000 that were partially refunded in November 20X6 and Series 20X0B

Revenue Bonds with a par amount of $91,200,000. The majority of the proceeds

from the Series 20X0A and Series 20X0B Revenue Bonds were used to refund the

current Series 19X8 Revenue Bonds with an outstanding balance of $19,147,000

and a note payable with an outstanding par amount of $88,000,000.

The Series 20X0A and Series 20X0B Revenue Bonds and the Series 20X1 Revenue

Bonds contain certain restrictive covenants, including minimum levels of debt

service coverage. Management believes the Foundation is in compliance with all

covenants.

1. The Series 20X0B Revenue Bonds and the Series 20X1 Revenue Bonds are variable

rate bonds in a daily mode and can be tendered by holders upon demand. A

remarketing agent selected by the Foundation determines the interest rates and

remarkets both series of bonds. The Series 20X0B Revenue Bonds and the Series

20X1 Revenue Bonds are supported by Standby Bond Purchase Agreements (the

Agreements) with liquidity providers pursuant to which the providers will purchase

any bonds the remarketing agent is unable to market. The termination date of the

December

31, 20X7

December

31, 20X6

Revenue bonds, Series 20X0B; interest accrues at a daily

rate determined by the remarketing agent (3.960% at

December 31, 20X7); interest and principal payable

annually through 20X9

83,200 84,500

Line of credit 19,000 46,686

Interim construction loan — 7,000

Other — 13,046

444,289 338,262

Less current maturities 4,692 5,908

$439,597 $332,354

In January 20X6, the Foundation entered into a revolving line of credit with Bank of

Central Ohio to fund interim construction costs and provide for liquidity and other

short-term needs. In accordance with terms of the loan agreement, the total

available for borrowing was decreased from $70,000,000 to $30,000,000 30 days

following the issuance of the Series 20X6 Revenue Bonds. The total amount drawn

as of December 31, 20X7 was $19,000,000. Interest is payable quarterly at a rate

equal to the lesser of the maximum lawful rate or LIBOR plus 15 basis points (5.71%

at December 31, 20X7). Amounts drawn are due in full June 25, 20X9.

The Foundation issued Series 20X1 Revenue Bonds with a par amount of

$158,000,000 that were partially refunded in November 20X6. The net proceeds

were used to fund expansion projects.

The Foundation issued Series 20X0A Revenue Bonds with a par amount of

$42,025,000 that were partially refunded in November 20X6 and Series 20X0B

Revenue Bonds with a par amount of $91,200,000. The majority of the proceeds

from the Series 20X0A and Series 20X0B Revenue Bonds were used to refund the

current Series 19X8 Revenue Bonds with an outstanding balance of $19,147,000

and a note payable with an outstanding par amount of $88,000,000.

The Series 20X0A and Series 20X0B Revenue Bonds and the Series 20X1 Revenue

Bonds contain certain restrictive covenants, including minimum levels of debt

service coverage. Management believes the Foundation is in compliance with all

covenants.

1. The Series 20X0B Revenue Bonds and the Series 20X1 Revenue Bonds are variable

rate bonds in a daily mode and can be tendered by holders upon demand. A

remarketing agent selected by the Foundation determines the interest rates and

remarkets both series of bonds. The Series 20X0B Revenue Bonds and the Series

20X1 Revenue Bonds are supported by Standby Bond Purchase Agreements (the

Agreements) with liquidity providers pursuant to which the providers will purchase

any bonds the remarketing agent is unable to market. The termination date of the

two Agreements related to the Series 20X0B Revenue Bonds was December 6,

20X7. On October 18, 20X7, these Agreements were extended to December 4,

20X8. There are also two Agreements associated with the Series 20X1 Revenue

Bonds. The termination date of the first Agreement related to the Series 20X1

Revenue Bonds was December 6, 20X7, and on October 18, 20X7, was extended to

December 4, 20X8. The termination date of the second Agreement related to the

Series 20X1 Revenue Bonds is December 15, 20X5, as extended in November 20X4.

All Agreements include covenants that are customary in credit agreements of this

nature. Repayment of bonds purchased under the Agreements is subject to a 5-year

payout beginning July 20X6, if other liquidity facilities, as defined in the bond

agreements, are not executed. The maturities of long-term debt, net of unamortized

premium, as of December 31, 20X7, are shown below (in thousands):

20X8 $4,692

20X9 23,902

20X0 5,136

20X1 5,353

20X2 19,896

Thereafter 385,310

$444,289

2. Total interest costs incurred during fiscal 20X7 and 20X6 were $16,779,140 and

$9,339,000 respectively, including $5,805,140 and $3,194,000 of capitalized

interest costs in 20X7 and 20X6, respectively. Interest paid during fiscal 20X7 and

20X6 was $16,937,249 and $9,084,500, respectively, net of amounts capitalized.

3. Concentrations of Credit Risk

Harris Memorial grants credit without collateral to its patients, most of whom are

local residents and are insured under third-party payer agreements. The mix of

receivables from patients and third-party payers was as follows:

TABLE 9A-7 Mix of Receivables

December 31, 20X7 December 31, 20X6

Medicare 21% 19%

Medicaid 2 2

Major payer 1 15 15

Major payer 2 11 11

20X7. On October 18, 20X7, these Agreements were extended to December 4,

20X8. There are also two Agreements associated with the Series 20X1 Revenue

Bonds. The termination date of the first Agreement related to the Series 20X1

Revenue Bonds was December 6, 20X7, and on October 18, 20X7, was extended to

December 4, 20X8. The termination date of the second Agreement related to the

Series 20X1 Revenue Bonds is December 15, 20X5, as extended in November 20X4.

All Agreements include covenants that are customary in credit agreements of this

nature. Repayment of bonds purchased under the Agreements is subject to a 5-year

payout beginning July 20X6, if other liquidity facilities, as defined in the bond

agreements, are not executed. The maturities of long-term debt, net of unamortized

premium, as of December 31, 20X7, are shown below (in thousands):

20X8 $4,692

20X9 23,902

20X0 5,136

20X1 5,353

20X2 19,896

Thereafter 385,310

$444,289

2. Total interest costs incurred during fiscal 20X7 and 20X6 were $16,779,140 and

$9,339,000 respectively, including $5,805,140 and $3,194,000 of capitalized

interest costs in 20X7 and 20X6, respectively. Interest paid during fiscal 20X7 and

20X6 was $16,937,249 and $9,084,500, respectively, net of amounts capitalized.

3. Concentrations of Credit Risk

Harris Memorial grants credit without collateral to its patients, most of whom are

local residents and are insured under third-party payer agreements. The mix of

receivables from patients and third-party payers was as follows:

TABLE 9A-7 Mix of Receivables

December 31, 20X7 December 31, 20X6

Medicare 21% 19%

Medicaid 2 2

Major payer 1 15 15

Major payer 2 11 11

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE 9A-7 Mix of Receivables

December 31, 20X7 December 31, 20X6

Major payer 3 11 13

Other third-party payers 28 28

Private pay 12 12

Total 100% 100%

4. Interest Rate Swap Agreements

Effective December 20X1, the Foundation entered into an interest rate swap

agreement with an initial notional amount of $150,000,000. The interest rate swap

agreement converts a notional amount of $150,000,000 of floating rate borrowings

to fixed rate borrowings. The Foundation pays a fixed rate of interest (5.17%) and

receives, from the counterparty, a variable rate of interest based on the SIFMA

Municipal Swap Index (SIFMA Index) on the outstanding principal balance of the

Series 20X1 Revenue Bonds until 2031. The Foundation has elected not to apply

hedge accounting; therefore, the change in fair value is included in nonoperating

(gains) losses. The fair value of the interest rate swap at December 31, 20X7 and

20X6, is a liability of approximately $9,498,000 and $16,530,000, respectively, and

is included in due to broker in the accompanying combined balance sheets. The

change in the fair value of the interest rate swap is included in nonoperating gains

(losses) and totaled approximately $(7,032,000) and $(6,885,000) for the years

ended December 31, 20X7 and 20X6, respectively. The change in fair value for the

year ended December 31, 20X7 includes the amendment fee paid to the

counterparty of $7,037,000, realized as a part of the Series 20X1 Revenue Bond

refunding.

Simultaneous with entering into the interest rate swap agreement, the Foundation

also entered into a put agreement with the counterparty. The counterparty may

exercise this put agreement if the daily weighted average of the SIFMA Index is

greater than 7.00% for the 180-day period ending on the day the counterparty

exercises the put option. Under this agreement, the Foundation pays a variable rate

of interest, based on the SIFMA Index, on the outstanding principal balance of the

proposed bonds until 2031. For this put agreement, the counterparty pays the

Foundation an annual premium of 77.30 basis points on an initial notional amount of

$150,000,000 over the term of the put agreement, for a net effective combined

annual payment by the Foundation to the counterparty for the swap agreement and

the put agreement of approximately 4.39%. The premium payment, however, will

cease upon exercise of the put agreement. This put agreement, if exercised, will

offset the cash flows of the interest rate swap agreement noted above. The fair

value of the put agreement at December 31, 20X7 and 20X6, is an asset of

$4,200,000 and $7,016,000, respectively, and has been included in other assets.

The change in the fair value of $(2,816,000) and $(552,000) for the years ended

December 31, 20X7 and 20X6, respectively, has been included in nonoperating

gains (losses) since the put agreement is not a hedge and must be adjusted to fair

value through the performance indicator. A portion of the change in fair value for

the year ended December 31, 20X7 includes the amount related to the partial

refunding of the Series 20X1 Revenue Bonds. The amendment fee received from

the counterparty was $2,005,000.

December 31, 20X7 December 31, 20X6

Major payer 3 11 13

Other third-party payers 28 28

Private pay 12 12

Total 100% 100%

4. Interest Rate Swap Agreements

Effective December 20X1, the Foundation entered into an interest rate swap

agreement with an initial notional amount of $150,000,000. The interest rate swap

agreement converts a notional amount of $150,000,000 of floating rate borrowings

to fixed rate borrowings. The Foundation pays a fixed rate of interest (5.17%) and

receives, from the counterparty, a variable rate of interest based on the SIFMA

Municipal Swap Index (SIFMA Index) on the outstanding principal balance of the

Series 20X1 Revenue Bonds until 2031. The Foundation has elected not to apply

hedge accounting; therefore, the change in fair value is included in nonoperating

(gains) losses. The fair value of the interest rate swap at December 31, 20X7 and

20X6, is a liability of approximately $9,498,000 and $16,530,000, respectively, and

is included in due to broker in the accompanying combined balance sheets. The

change in the fair value of the interest rate swap is included in nonoperating gains

(losses) and totaled approximately $(7,032,000) and $(6,885,000) for the years

ended December 31, 20X7 and 20X6, respectively. The change in fair value for the

year ended December 31, 20X7 includes the amendment fee paid to the

counterparty of $7,037,000, realized as a part of the Series 20X1 Revenue Bond

refunding.

Simultaneous with entering into the interest rate swap agreement, the Foundation

also entered into a put agreement with the counterparty. The counterparty may

exercise this put agreement if the daily weighted average of the SIFMA Index is

greater than 7.00% for the 180-day period ending on the day the counterparty

exercises the put option. Under this agreement, the Foundation pays a variable rate

of interest, based on the SIFMA Index, on the outstanding principal balance of the

proposed bonds until 2031. For this put agreement, the counterparty pays the

Foundation an annual premium of 77.30 basis points on an initial notional amount of

$150,000,000 over the term of the put agreement, for a net effective combined

annual payment by the Foundation to the counterparty for the swap agreement and

the put agreement of approximately 4.39%. The premium payment, however, will

cease upon exercise of the put agreement. This put agreement, if exercised, will

offset the cash flows of the interest rate swap agreement noted above. The fair

value of the put agreement at December 31, 20X7 and 20X6, is an asset of

$4,200,000 and $7,016,000, respectively, and has been included in other assets.

The change in the fair value of $(2,816,000) and $(552,000) for the years ended

December 31, 20X7 and 20X6, respectively, has been included in nonoperating

gains (losses) since the put agreement is not a hedge and must be adjusted to fair

value through the performance indicator. A portion of the change in fair value for

the year ended December 31, 20X7 includes the amount related to the partial

refunding of the Series 20X1 Revenue Bonds. The amendment fee received from

the counterparty was $2,005,000.

On October 30, 20X2, the Foundation entered into an interest rate swap agreement

with an initial notional amount of $96,400,000 ($88,400,000 Series 20X0A and

Series 20X0B and $8,000,000 Series 20X1). The interest rate swap agreement

converts a notional amount of $96,400,000 of floating rate borrowings to fixed rate

borrowings. The Foundation pays a fixed rate of interest (4.34)% and receives, from

the counterparty, a variable rate of interest based on the SIFMA Index on the

outstanding principal balance of the Revenue Bonds until 2031. The Foundation has

elected not to apply hedge accounting; therefore, the change in fair value is

included in nonoperating (gains) losses. The fair value of the interest rate swap at

December 31, 20X7 and 20X6, is a liability of approximately $3,020,000 and

$3,078,000, respectively, and is included in due to broker in the accompanying

combined balance sheets. The change in the fair value of the interest rate swap is

included in nonoperating gains (losses) and totaled approximately $(58,000) and

$(3,639,000) for the years ended December 31, 20X7 and 20X6, respectively. The

change in fair value includes the amendment fee of $176,000 paid to the

counterparty to terminate the portion of the interest rate swap agreement

associated with the Series 20X1 Revenue Bonds. Simultaneous with entering into

the interest rate swap agreement, the Foundation also entered into a put

agreement with the counterparty. The counterparty may exercise this put

agreement if the daily weighted-average of the SIFMA Index is greater than 6.00%

for the 180-day period ending on the day the counterparty exercises the put option.

Under this agreement, the Foundation pays a variable rate of interest, based on the

SIFMA Index, on the outstanding principal balance of the related bonds until 2031.

For this put agreement, the counterparty pays the Foundation an annual premium

of 110.10 basis points on an initial notional amount $96,400,000 over the term of

the put agreement, for a net effective combined annual payment by the Foundation

to the counterparty for the swap agreement and the put agreement of

approximately 3.24%. The premium payment, however, will cease upon exercise of

the put agreement. This put agreement, if exercised, will offset the cash flows of the

interest rate swap agreement noted above. The fair value of the put agreement at

December 31, 20X7 and 20X6, is an asset of approximately $4,970,000 and

$5,056,000, respectively, and has been included in other assets. This change in fair

value of $(86,000) and $(575,000) for the years ended December 31, 20X7 and

20X6, respectively, has been included in nonoperating gains (losses) since the put

agreement is not a hedge and must be adjusted to fair value through the

performance indicator. The change in fair value includes the amendment fee of

$198,000 received from the counterparty to terminate the portion of the put

agreement associated with the Series 20X1 Revenue Bonds.

In anticipation of the issuance of the Series 20X6 Bonds, the Foundation entered

into five interest rate swap transactions in October 20X6 with an initial notional

amount totaling $233,350,000.

The swap transactions serve to substantially fix the expected net interest expense

associated with the Series 20X6 Bonds by converting floating rate borrowings with a

notional amount of $233,350,000 to fixed rate borrowings. For the swaps related to

the Series 20X6A and 20X6B Bonds, the Foundation pays a fixed rate of 3.502% per

annum, and the counterparty pays a variable rate of interest at a rate equal to

57.4% of the 1-month LIBOR rate plus a spread of 0.33%. For the swaps related to

the Series 20X6C Bonds and 20X6D Bonds, the Foundation pays a fixed rate of

3.496% per annum, and the counterparty pays a variable rate of interest at a rate

equal to 57.4% of the 1-month LIBOR rate plus a spread of 0.33%.

The Foundation has elected not to apply hedge accounting; therefore, the change in

fair value is included in nonoperating (gains) losses. The fair value of the interest