Private Equity Investments and Value Creation

VerifiedAdded on 2020/01/28

|48

|8524

|36

Case Study

AI Summary

This assignment examines the validity of private equity as a valuable source for income generation and company growth. It requires students to discuss the various ways private equity investments can create value, considering factors like acquisition selection, pricing negotiations, management incentives, and operational improvements. Additionally, the assignment delves into the inherent risks associated with private equity and how investors mitigate them.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Case study

1

1

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

TABLE OF CONTENTS

Module Aims ..................................................................................................................................3

SECTION A.....................................................................................................................................5

SECTION B...................................................................................................................................25

SECTION C...................................................................................................................................33

2

Module Aims ..................................................................................................................................3

SECTION A.....................................................................................................................................5

SECTION B...................................................................................................................................25

SECTION C...................................................................................................................................33

2

MODULE AIMS

Question: 1. Provide an analytical framework for evaluating the strategic and financial impact of private equity and venture

capital in the modern economy?

Answer:

PE and VC plays a major role in the modern economic conditions. With reference to Harvard Management Company

(HMC), its financial impact is it is gaining higher return on their private equity investment as during fiscal year 2015, its

PE return exceeded the benchmark of 10.8% by generating 11.8% return.

On the other hand, investor can generate a better value on their VC by investing funds in companies in their early stage

of growing.

Along with this, it PE and VC pathway also impact the business strategy as it assists investors to redesign their

governance structure and reduce friction among management, shareholders, controlling as well as non-controlling

shareholders. Through this, companies can align their managerial decisions by taking into consideration their

stakeholders interests and satisfy them.

In PE, investors can add value by bringing operational and governance changes and exploit capital market inefficiencies

through buying undervalued assets and disposing off the over-valued assets.

Thus, from this analysis, it becomes clear that PE and VC pathway emphasize strategic, financial and operational

decisions and adds value for the growth equity investors.

Question: 2. Present a critical examination and analysis of the practical management and exit issues related to PE?

Answer:

IPO, trade sale and secondary buyout etc. are the several exit strategies which HMC can use to exit from the private

equity but all the strategies has several issues.

3

Question: 1. Provide an analytical framework for evaluating the strategic and financial impact of private equity and venture

capital in the modern economy?

Answer:

PE and VC plays a major role in the modern economic conditions. With reference to Harvard Management Company

(HMC), its financial impact is it is gaining higher return on their private equity investment as during fiscal year 2015, its

PE return exceeded the benchmark of 10.8% by generating 11.8% return.

On the other hand, investor can generate a better value on their VC by investing funds in companies in their early stage

of growing.

Along with this, it PE and VC pathway also impact the business strategy as it assists investors to redesign their

governance structure and reduce friction among management, shareholders, controlling as well as non-controlling

shareholders. Through this, companies can align their managerial decisions by taking into consideration their

stakeholders interests and satisfy them.

In PE, investors can add value by bringing operational and governance changes and exploit capital market inefficiencies

through buying undervalued assets and disposing off the over-valued assets.

Thus, from this analysis, it becomes clear that PE and VC pathway emphasize strategic, financial and operational

decisions and adds value for the growth equity investors.

Question: 2. Present a critical examination and analysis of the practical management and exit issues related to PE?

Answer:

IPO, trade sale and secondary buyout etc. are the several exit strategies which HMC can use to exit from the private

equity but all the strategies has several issues.

3

More importantly, in an secondary sale, tax issue can be arise. In this, buyers will try to get protect themselves from the

future tax demands of the taxation authorities by demanding certification, tax indemnities from the seller and preparing

an insurance policy as well.

However, after the amendments in the finance act, it becomes very complex and tough for the buyer to obtain this

certificates.

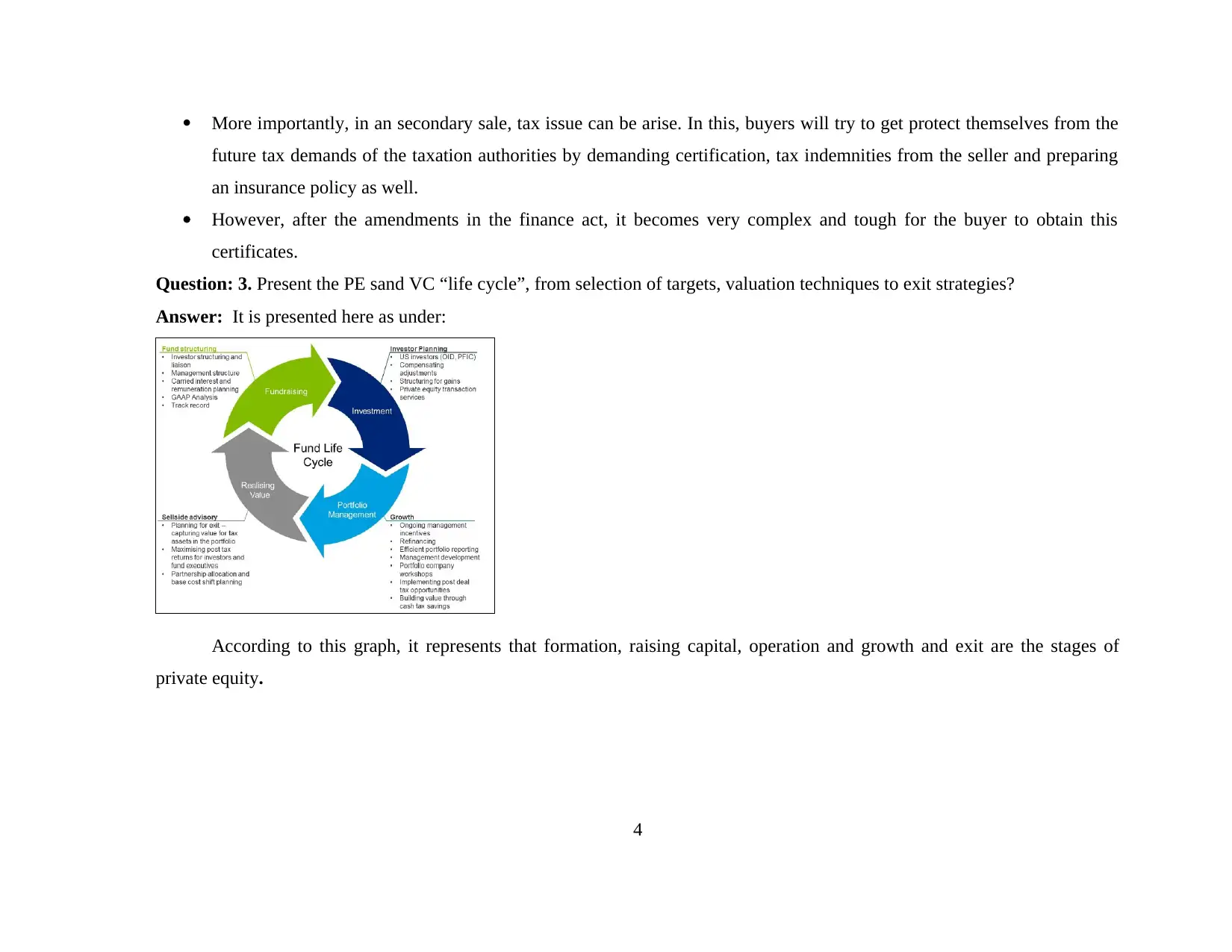

Question: 3. Present the PE sand VC “life cycle”, from selection of targets, valuation techniques to exit strategies?

Answer: It is presented here as under:

According to this graph, it represents that formation, raising capital, operation and growth and exit are the stages of

private equity.

4

future tax demands of the taxation authorities by demanding certification, tax indemnities from the seller and preparing

an insurance policy as well.

However, after the amendments in the finance act, it becomes very complex and tough for the buyer to obtain this

certificates.

Question: 3. Present the PE sand VC “life cycle”, from selection of targets, valuation techniques to exit strategies?

Answer: It is presented here as under:

According to this graph, it represents that formation, raising capital, operation and growth and exit are the stages of

private equity.

4

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

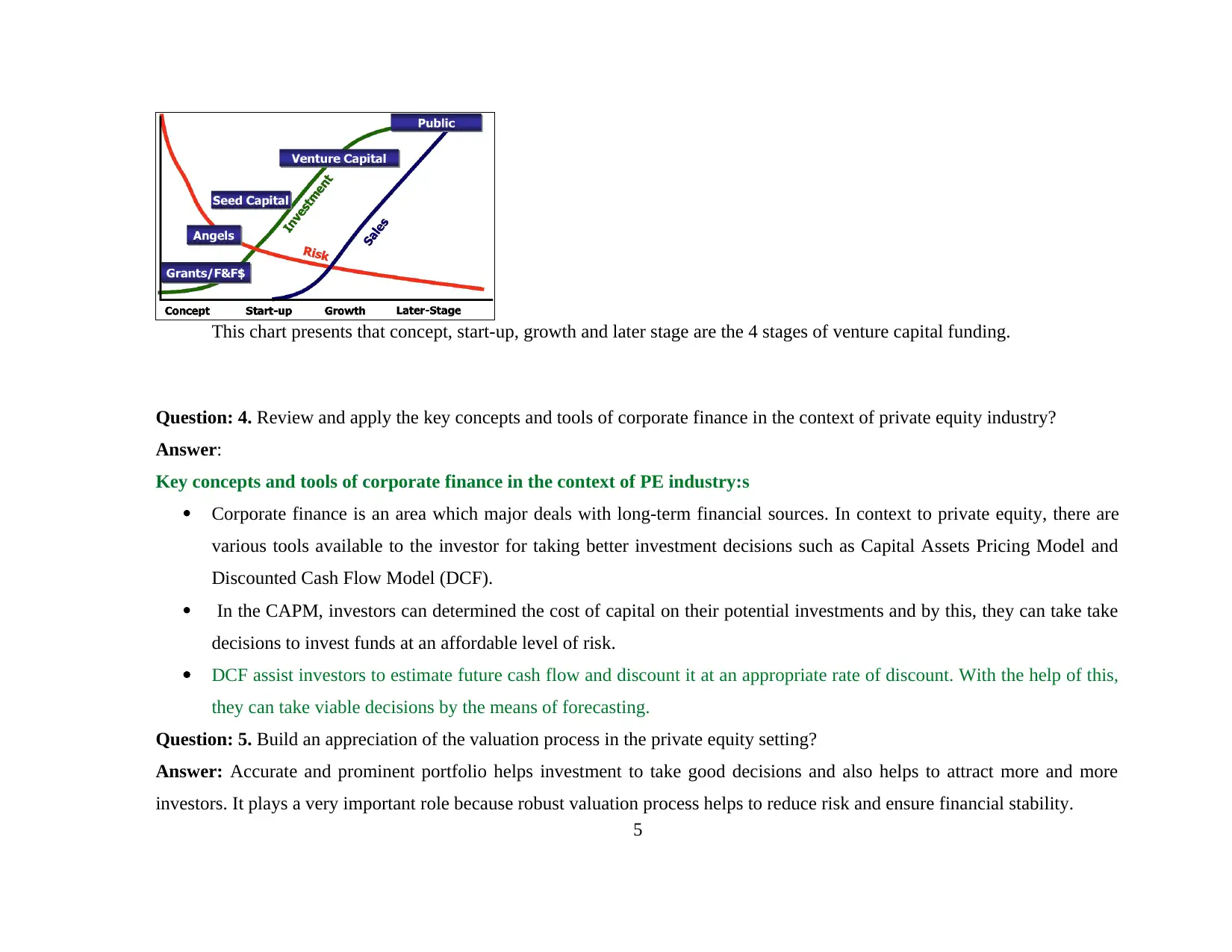

This chart presents that concept, start-up, growth and later stage are the 4 stages of venture capital funding.

Question: 4. Review and apply the key concepts and tools of corporate finance in the context of private equity industry?

Answer:

Key concepts and tools of corporate finance in the context of PE industry:s

Corporate finance is an area which major deals with long-term financial sources. In context to private equity, there are

various tools available to the investor for taking better investment decisions such as Capital Assets Pricing Model and

Discounted Cash Flow Model (DCF).

In the CAPM, investors can determined the cost of capital on their potential investments and by this, they can take take

decisions to invest funds at an affordable level of risk.

DCF assist investors to estimate future cash flow and discount it at an appropriate rate of discount. With the help of this,

they can take viable decisions by the means of forecasting.

Question: 5. Build an appreciation of the valuation process in the private equity setting?

Answer: Accurate and prominent portfolio helps investment to take good decisions and also helps to attract more and more

investors. It plays a very important role because robust valuation process helps to reduce risk and ensure financial stability.

5

Question: 4. Review and apply the key concepts and tools of corporate finance in the context of private equity industry?

Answer:

Key concepts and tools of corporate finance in the context of PE industry:s

Corporate finance is an area which major deals with long-term financial sources. In context to private equity, there are

various tools available to the investor for taking better investment decisions such as Capital Assets Pricing Model and

Discounted Cash Flow Model (DCF).

In the CAPM, investors can determined the cost of capital on their potential investments and by this, they can take take

decisions to invest funds at an affordable level of risk.

DCF assist investors to estimate future cash flow and discount it at an appropriate rate of discount. With the help of this,

they can take viable decisions by the means of forecasting.

Question: 5. Build an appreciation of the valuation process in the private equity setting?

Answer: Accurate and prominent portfolio helps investment to take good decisions and also helps to attract more and more

investors. It plays a very important role because robust valuation process helps to reduce risk and ensure financial stability.

5

Question: 6. Assess the new phenomenon: Sovereign Wealth Funds and their role in the world economy?

Answer: Sovereign wealth funds is regarded as state owned money pool which is invested in different types of financial assets,

also known as budgetary surplus. It plays an important role in the foreign direct investment, government bonds and equity

investment as well.

SECTION A

Question: 1. Describe the main categories of Private Investing and comment on the extent to which these are used by Harvard?

Answer:

Introduction to private equity

Private equity is regarded as a finance source through which organizations can acquire funds by selling business equity to

the individual and institutions. In the corporate world, large number of companies meet their financial need by providing

ownership rights to the investors. In other words, it transfer the controlling power to the shareholders through which they can

take part in controlling regular business operations and decisions. It is an assets class which comprises both debt and equity

funds invested in privately held companies or organizations which are engaging in buyout of another companies. With regards to

HMC, it invest private equity by providing capital to invest in new technology, acquisition, expansion of working capital and

boost the balance sheet as well.

Types of Private equity funds or investment

There are different categories of private investing such as leveraged buyout, growth equity, venture capital, real estate

investment etc which are discussed here as under:

6

Answer: Sovereign wealth funds is regarded as state owned money pool which is invested in different types of financial assets,

also known as budgetary surplus. It plays an important role in the foreign direct investment, government bonds and equity

investment as well.

SECTION A

Question: 1. Describe the main categories of Private Investing and comment on the extent to which these are used by Harvard?

Answer:

Introduction to private equity

Private equity is regarded as a finance source through which organizations can acquire funds by selling business equity to

the individual and institutions. In the corporate world, large number of companies meet their financial need by providing

ownership rights to the investors. In other words, it transfer the controlling power to the shareholders through which they can

take part in controlling regular business operations and decisions. It is an assets class which comprises both debt and equity

funds invested in privately held companies or organizations which are engaging in buyout of another companies. With regards to

HMC, it invest private equity by providing capital to invest in new technology, acquisition, expansion of working capital and

boost the balance sheet as well.

Types of Private equity funds or investment

There are different categories of private investing such as leveraged buyout, growth equity, venture capital, real estate

investment etc which are discussed here as under:

6

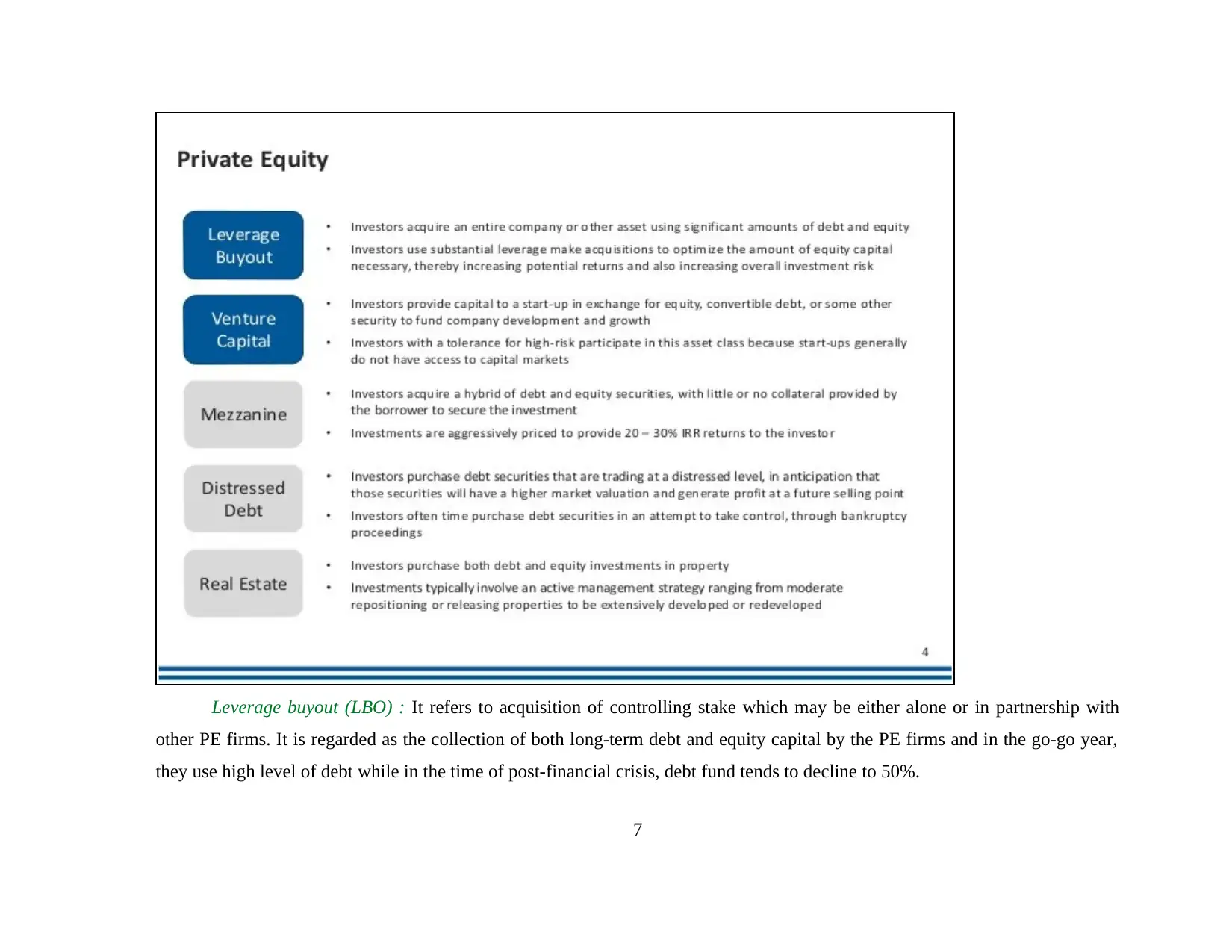

Leverage buyout (LBO) : It refers to acquisition of controlling stake which may be either alone or in partnership with

other PE firms. It is regarded as the collection of both long-term debt and equity capital by the PE firms and in the go-go year,

they use high level of debt while in the time of post-financial crisis, debt fund tends to decline to 50%.

7

other PE firms. It is regarded as the collection of both long-term debt and equity capital by the PE firms and in the go-go year,

they use high level of debt while in the time of post-financial crisis, debt fund tends to decline to 50%.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

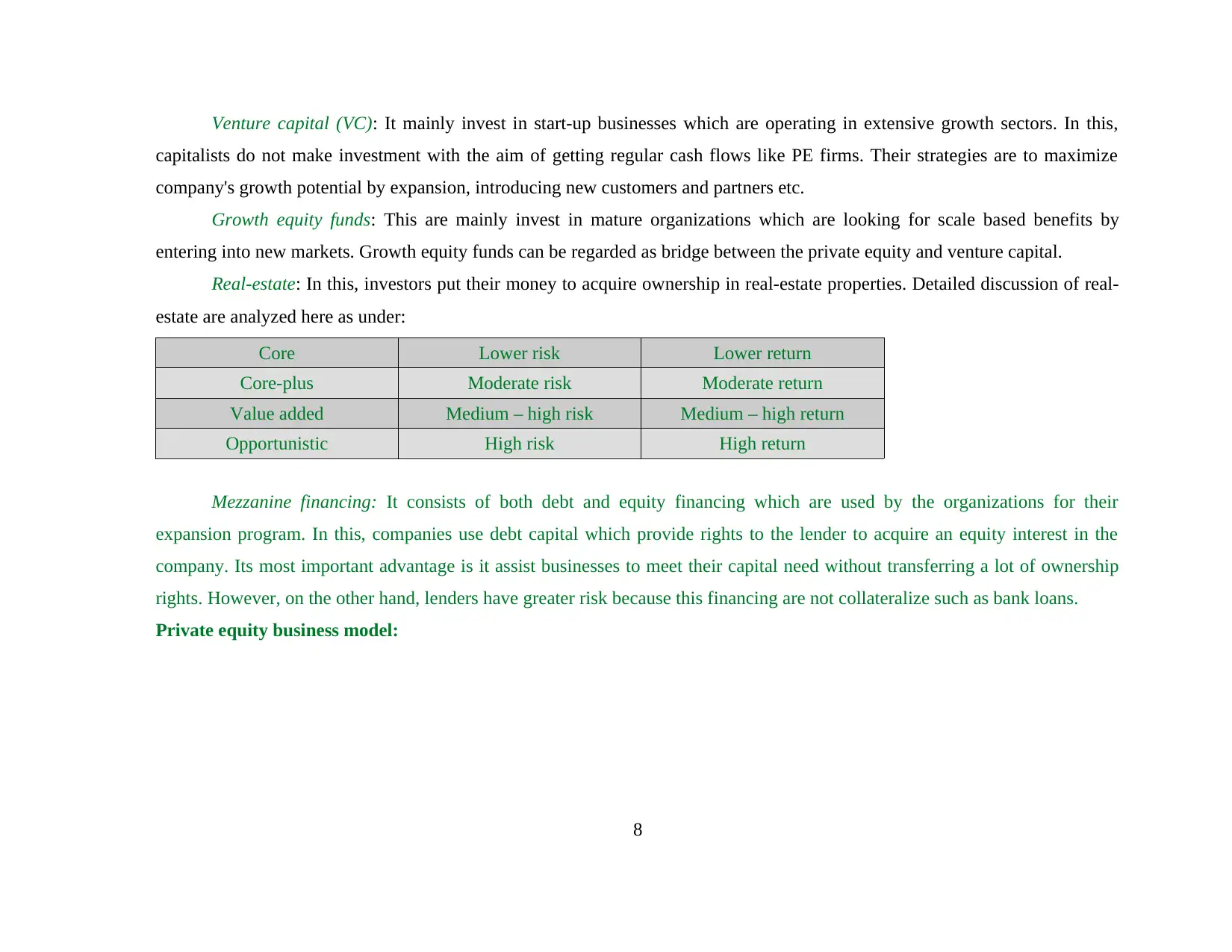

Venture capital (VC): It mainly invest in start-up businesses which are operating in extensive growth sectors. In this,

capitalists do not make investment with the aim of getting regular cash flows like PE firms. Their strategies are to maximize

company's growth potential by expansion, introducing new customers and partners etc.

Growth equity funds: This are mainly invest in mature organizations which are looking for scale based benefits by

entering into new markets. Growth equity funds can be regarded as bridge between the private equity and venture capital.

Real-estate: In this, investors put their money to acquire ownership in real-estate properties. Detailed discussion of real-

estate are analyzed here as under:

Core Lower risk Lower return

Core-plus Moderate risk Moderate return

Value added Medium – high risk Medium – high return

Opportunistic High risk High return

Mezzanine financing: It consists of both debt and equity financing which are used by the organizations for their

expansion program. In this, companies use debt capital which provide rights to the lender to acquire an equity interest in the

company. Its most important advantage is it assist businesses to meet their capital need without transferring a lot of ownership

rights. However, on the other hand, lenders have greater risk because this financing are not collateralize such as bank loans.

Private equity business model:

8

capitalists do not make investment with the aim of getting regular cash flows like PE firms. Their strategies are to maximize

company's growth potential by expansion, introducing new customers and partners etc.

Growth equity funds: This are mainly invest in mature organizations which are looking for scale based benefits by

entering into new markets. Growth equity funds can be regarded as bridge between the private equity and venture capital.

Real-estate: In this, investors put their money to acquire ownership in real-estate properties. Detailed discussion of real-

estate are analyzed here as under:

Core Lower risk Lower return

Core-plus Moderate risk Moderate return

Value added Medium – high risk Medium – high return

Opportunistic High risk High return

Mezzanine financing: It consists of both debt and equity financing which are used by the organizations for their

expansion program. In this, companies use debt capital which provide rights to the lender to acquire an equity interest in the

company. Its most important advantage is it assist businesses to meet their capital need without transferring a lot of ownership

rights. However, on the other hand, lenders have greater risk because this financing are not collateralize such as bank loans.

Private equity business model:

8

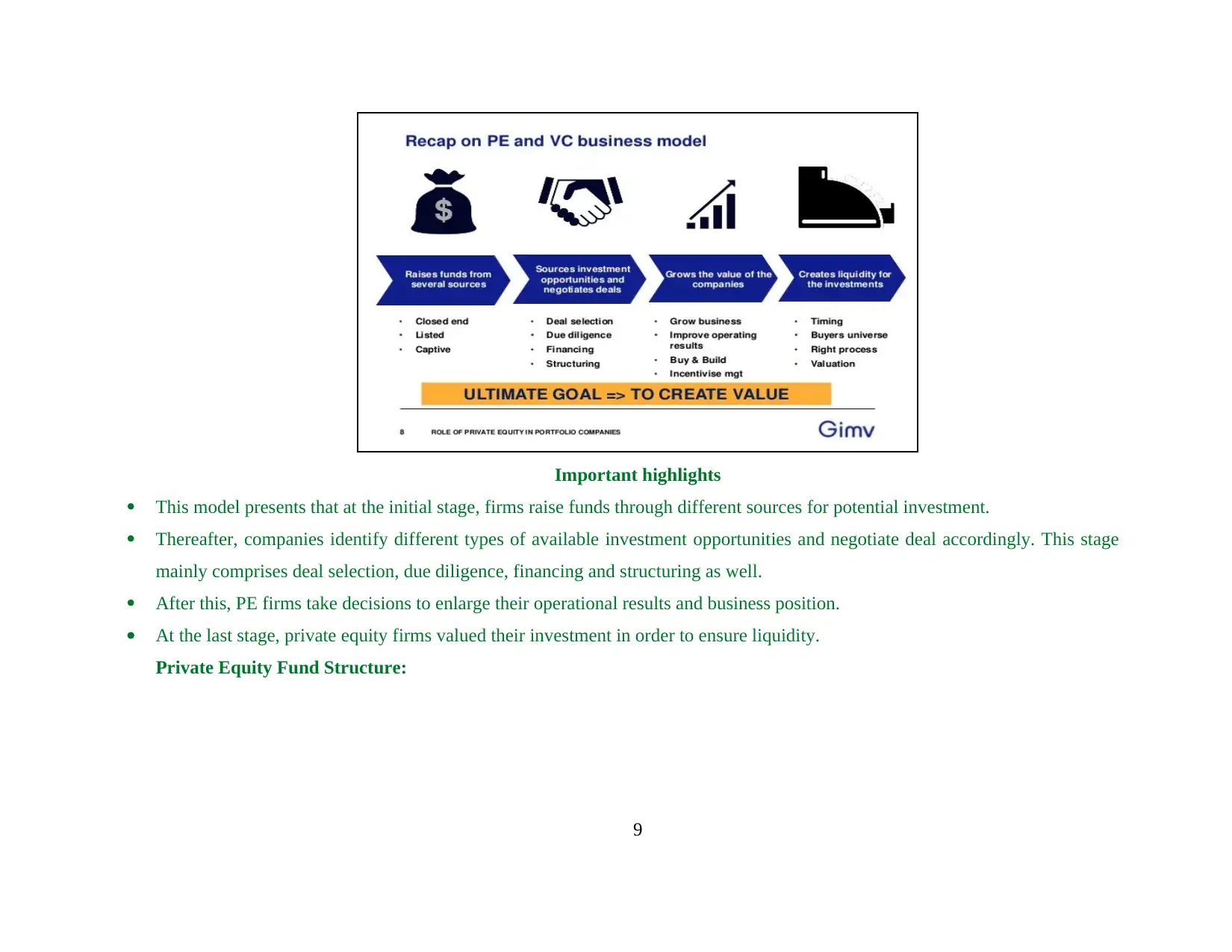

Important highlights

This model presents that at the initial stage, firms raise funds through different sources for potential investment.

Thereafter, companies identify different types of available investment opportunities and negotiate deal accordingly. This stage

mainly comprises deal selection, due diligence, financing and structuring as well.

After this, PE firms take decisions to enlarge their operational results and business position.

At the last stage, private equity firms valued their investment in order to ensure liquidity.

Private Equity Fund Structure:

9

This model presents that at the initial stage, firms raise funds through different sources for potential investment.

Thereafter, companies identify different types of available investment opportunities and negotiate deal accordingly. This stage

mainly comprises deal selection, due diligence, financing and structuring as well.

After this, PE firms take decisions to enlarge their operational results and business position.

At the last stage, private equity firms valued their investment in order to ensure liquidity.

Private Equity Fund Structure:

9

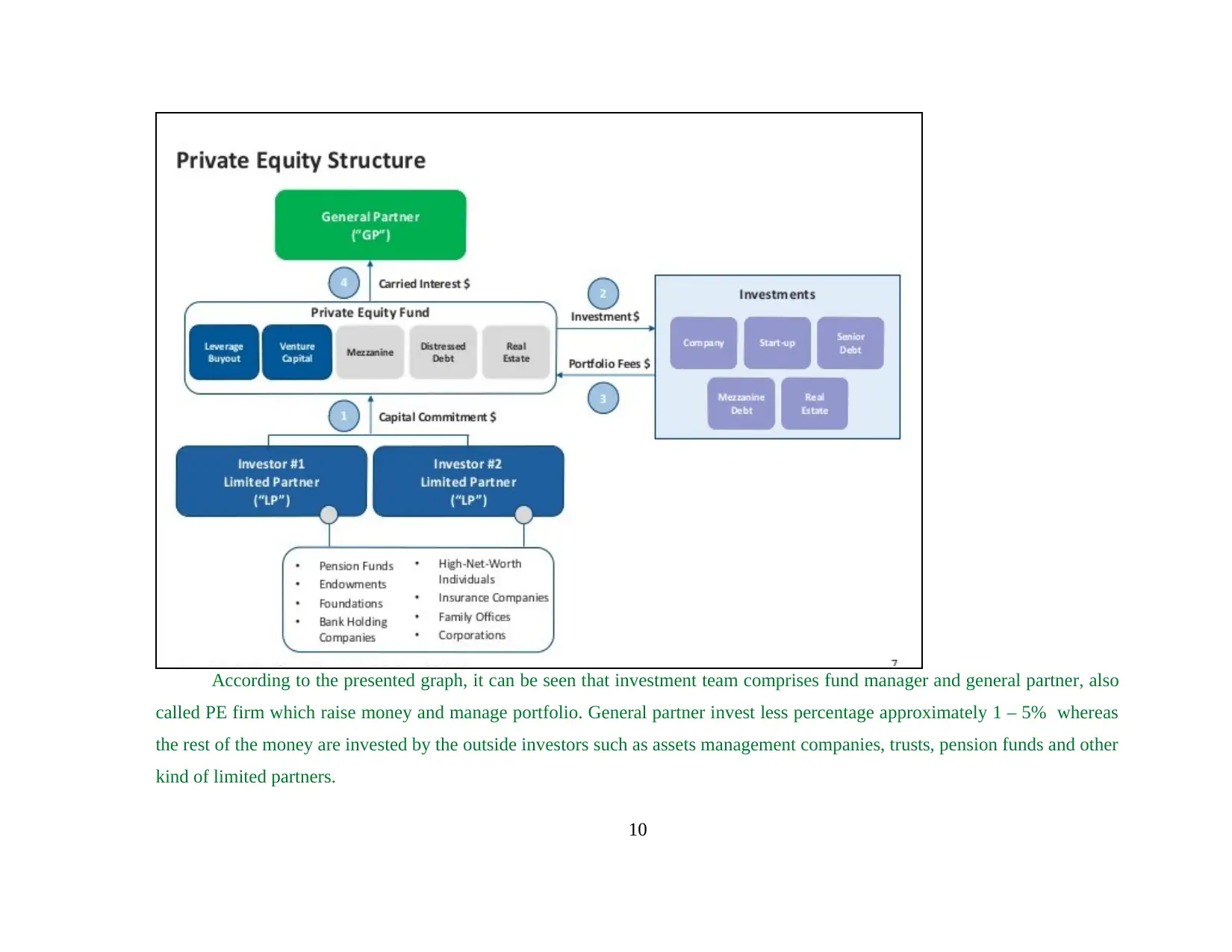

According to the presented graph, it can be seen that investment team comprises fund manager and general partner, also

called PE firm which raise money and manage portfolio. General partner invest less percentage approximately 1 – 5% whereas

the rest of the money are invested by the outside investors such as assets management companies, trusts, pension funds and other

kind of limited partners.

10

called PE firm which raise money and manage portfolio. General partner invest less percentage approximately 1 – 5% whereas

the rest of the money are invested by the outside investors such as assets management companies, trusts, pension funds and other

kind of limited partners.

10

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

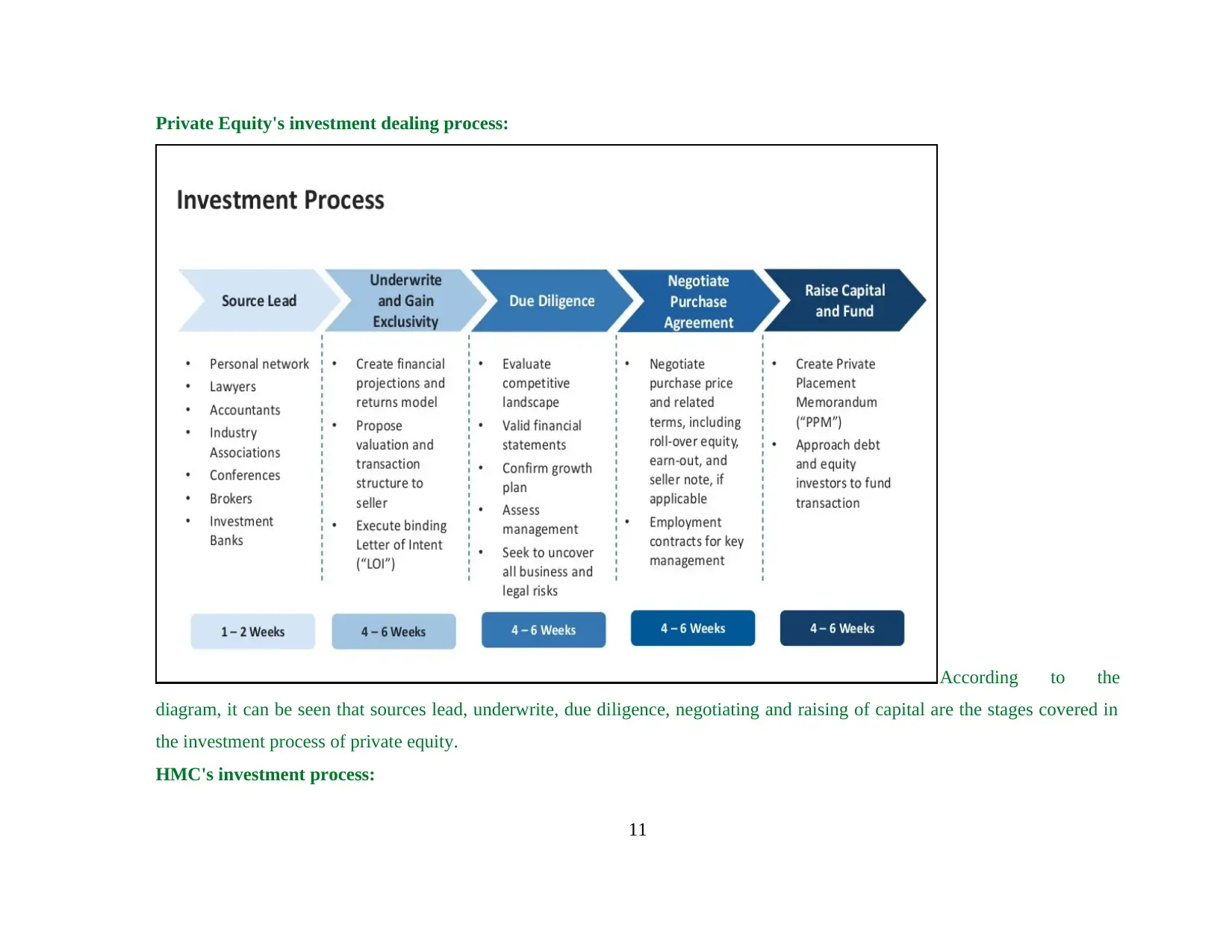

Private Equity's investment dealing process:

According to the

diagram, it can be seen that sources lead, underwrite, due diligence, negotiating and raising of capital are the stages covered in

the investment process of private equity.

HMC's investment process:

11

According to the

diagram, it can be seen that sources lead, underwrite, due diligence, negotiating and raising of capital are the stages covered in

the investment process of private equity.

HMC's investment process:

11

With regards to HMC, at the first stage, its investment team are engaging in more cross assets class discussion and

collaboration. Its board are highly committing to develop a strong investment portfolio by the comparison of various

investment opportunity available to the company.

Secondly, Its CEO is encouraging their portfolio managers to be creative in identifying new investment platform which

will deliver maximum benefit to the company. It keep in mind the flexibility and reduction in management fees while

taking investment decisions.

Harvard University owes $37.6 billion endowment assets. Therefore, deep market experience, analytical study,

determining alternative investment opportunities etc. is also of great importance for portfolio creation. University has

very risky portfolio with a greater beta value but still, it is managed effectively by analysis of the market environment.

12

collaboration. Its board are highly committing to develop a strong investment portfolio by the comparison of various

investment opportunity available to the company.

Secondly, Its CEO is encouraging their portfolio managers to be creative in identifying new investment platform which

will deliver maximum benefit to the company. It keep in mind the flexibility and reduction in management fees while

taking investment decisions.

Harvard University owes $37.6 billion endowment assets. Therefore, deep market experience, analytical study,

determining alternative investment opportunities etc. is also of great importance for portfolio creation. University has

very risky portfolio with a greater beta value but still, it is managed effectively by analysis of the market environment.

12

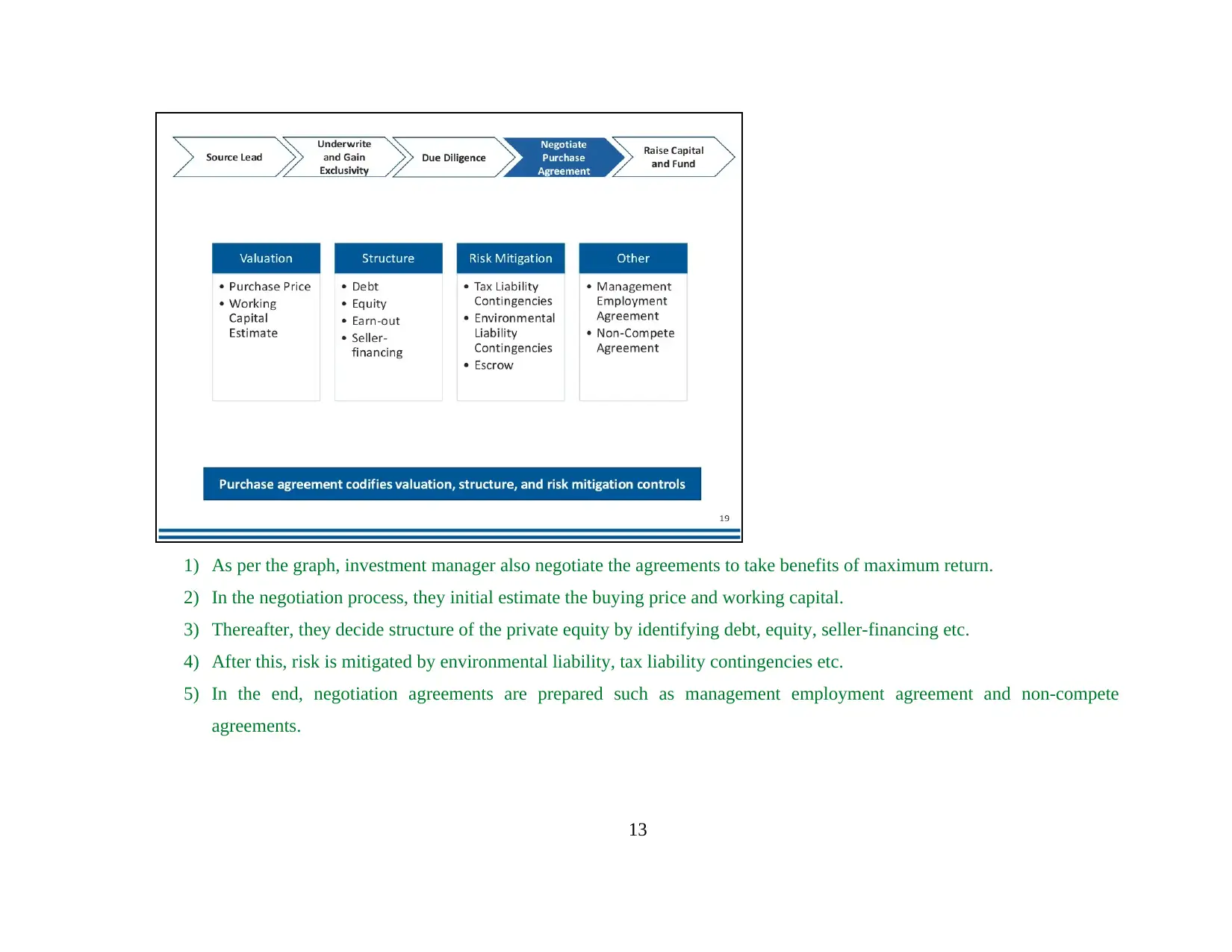

1) As per the graph, investment manager also negotiate the agreements to take benefits of maximum return.

2) In the negotiation process, they initial estimate the buying price and working capital.

3) Thereafter, they decide structure of the private equity by identifying debt, equity, seller-financing etc.

4) After this, risk is mitigated by environmental liability, tax liability contingencies etc.

5) In the end, negotiation agreements are prepared such as management employment agreement and non-compete

agreements.

13

2) In the negotiation process, they initial estimate the buying price and working capital.

3) Thereafter, they decide structure of the private equity by identifying debt, equity, seller-financing etc.

4) After this, risk is mitigated by environmental liability, tax liability contingencies etc.

5) In the end, negotiation agreements are prepared such as management employment agreement and non-compete

agreements.

13

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

In the end, it is operating with both the investment partners and peer institutional investors across the globe. It also meet

with internal as well as external managers of several investment institutions to obtain their advice for the better portfolio

decisions.

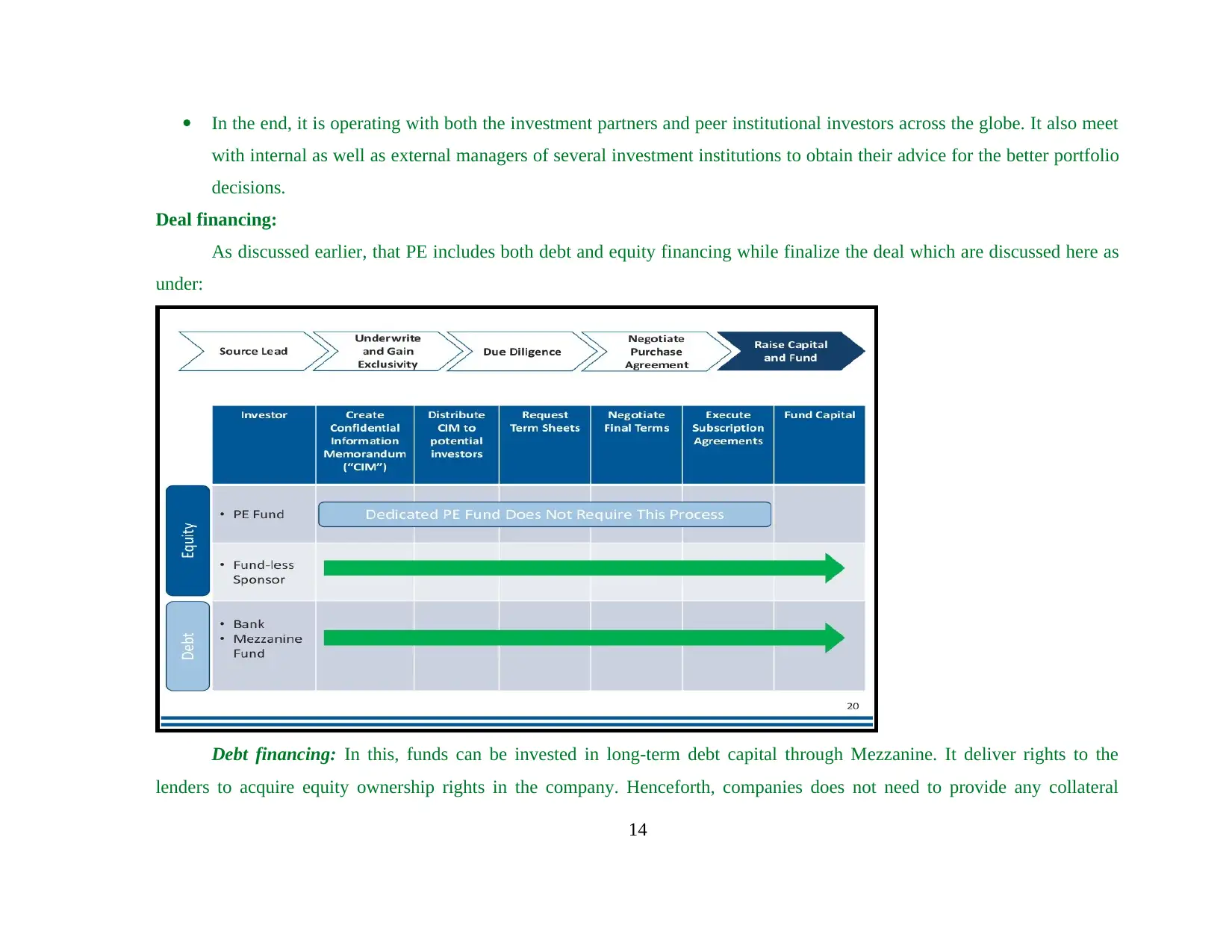

Deal financing:

As discussed earlier, that PE includes both debt and equity financing while finalize the deal which are discussed here as

under:

Debt financing: In this, funds can be invested in long-term debt capital through Mezzanine. It deliver rights to the

lenders to acquire equity ownership rights in the company. Henceforth, companies does not need to provide any collateral

14

with internal as well as external managers of several investment institutions to obtain their advice for the better portfolio

decisions.

Deal financing:

As discussed earlier, that PE includes both debt and equity financing while finalize the deal which are discussed here as

under:

Debt financing: In this, funds can be invested in long-term debt capital through Mezzanine. It deliver rights to the

lenders to acquire equity ownership rights in the company. Henceforth, companies does not need to provide any collateral

14

securities to them which is an advantage of it.

Equity financing: PE fund and fund-less sponsor are the types of equity financing. It is a process through which investor

can raise money through sale of shares. In other words, if funds are acquired by the sale of ownership rights than it is known as

equity financing.

Hybrid investment model of HMC

Harvard University is a private research university which was established in the year 1636. Harvard management

company (HMC)'s CEO Stephen Blyth follows hybrid investment model in which both the internal and external

management teams are focuses on specific area of investment.

The main goal of this is to encourage an integrated investment approach in order to generate sufficient income to meet

University's operational budget need.

Blyth's investment policy is not highly committed to invest huge money in illiquid assets.

According to its endowment report for the fiscal year 2015, its total return and value reported to 5.8% and $37.6 billion

while the performance of each assets class are outlined below:

Important highlights

15

Equity financing: PE fund and fund-less sponsor are the types of equity financing. It is a process through which investor

can raise money through sale of shares. In other words, if funds are acquired by the sale of ownership rights than it is known as

equity financing.

Hybrid investment model of HMC

Harvard University is a private research university which was established in the year 1636. Harvard management

company (HMC)'s CEO Stephen Blyth follows hybrid investment model in which both the internal and external

management teams are focuses on specific area of investment.

The main goal of this is to encourage an integrated investment approach in order to generate sufficient income to meet

University's operational budget need.

Blyth's investment policy is not highly committed to invest huge money in illiquid assets.

According to its endowment report for the fiscal year 2015, its total return and value reported to 5.8% and $37.6 billion

while the performance of each assets class are outlined below:

Important highlights

15

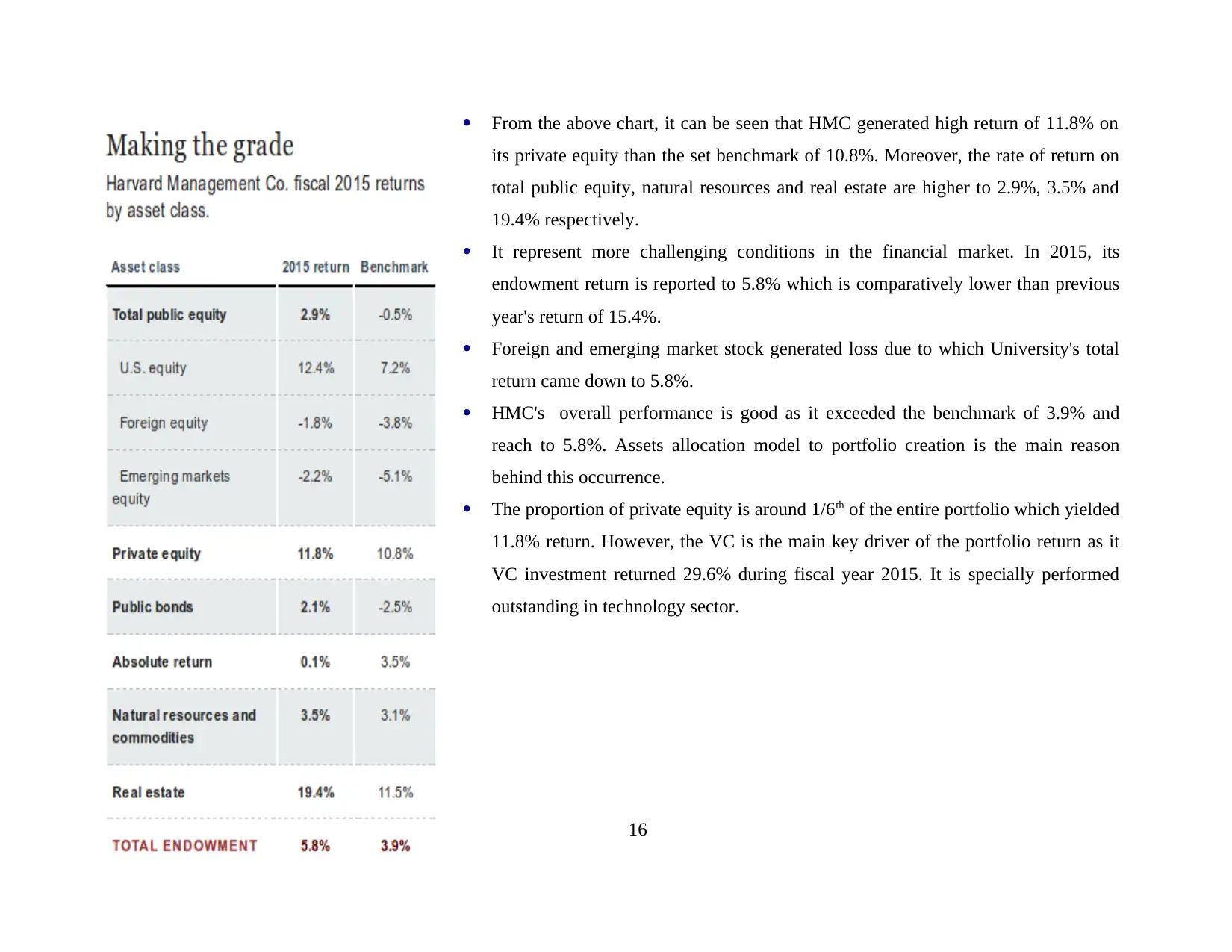

From the above chart, it can be seen that HMC generated high return of 11.8% on

its private equity than the set benchmark of 10.8%. Moreover, the rate of return on

total public equity, natural resources and real estate are higher to 2.9%, 3.5% and

19.4% respectively.

It represent more challenging conditions in the financial market. In 2015, its

endowment return is reported to 5.8% which is comparatively lower than previous

year's return of 15.4%.

Foreign and emerging market stock generated loss due to which University's total

return came down to 5.8%.

HMC's overall performance is good as it exceeded the benchmark of 3.9% and

reach to 5.8%. Assets allocation model to portfolio creation is the main reason

behind this occurrence.

The proportion of private equity is around 1/6th of the entire portfolio which yielded

11.8% return. However, the VC is the main key driver of the portfolio return as it

VC investment returned 29.6% during fiscal year 2015. It is specially performed

outstanding in technology sector.

16

its private equity than the set benchmark of 10.8%. Moreover, the rate of return on

total public equity, natural resources and real estate are higher to 2.9%, 3.5% and

19.4% respectively.

It represent more challenging conditions in the financial market. In 2015, its

endowment return is reported to 5.8% which is comparatively lower than previous

year's return of 15.4%.

Foreign and emerging market stock generated loss due to which University's total

return came down to 5.8%.

HMC's overall performance is good as it exceeded the benchmark of 3.9% and

reach to 5.8%. Assets allocation model to portfolio creation is the main reason

behind this occurrence.

The proportion of private equity is around 1/6th of the entire portfolio which yielded

11.8% return. However, the VC is the main key driver of the portfolio return as it

VC investment returned 29.6% during fiscal year 2015. It is specially performed

outstanding in technology sector.

16

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

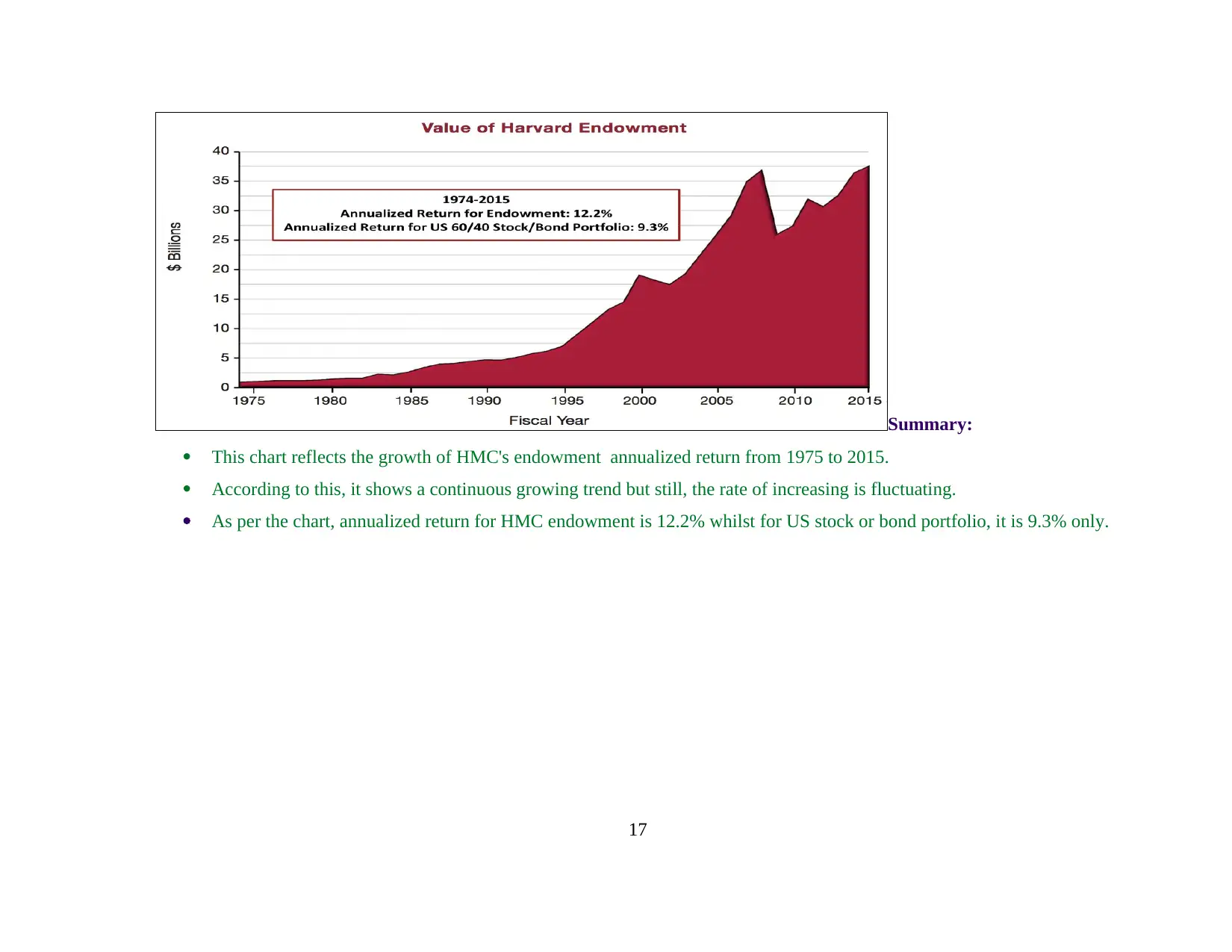

Summary:

This chart reflects the growth of HMC's endowment annualized return from 1975 to 2015.

According to this, it shows a continuous growing trend but still, the rate of increasing is fluctuating.

As per the chart, annualized return for HMC endowment is 12.2% whilst for US stock or bond portfolio, it is 9.3% only.

17

This chart reflects the growth of HMC's endowment annualized return from 1975 to 2015.

According to this, it shows a continuous growing trend but still, the rate of increasing is fluctuating.

As per the chart, annualized return for HMC endowment is 12.2% whilst for US stock or bond portfolio, it is 9.3% only.

17

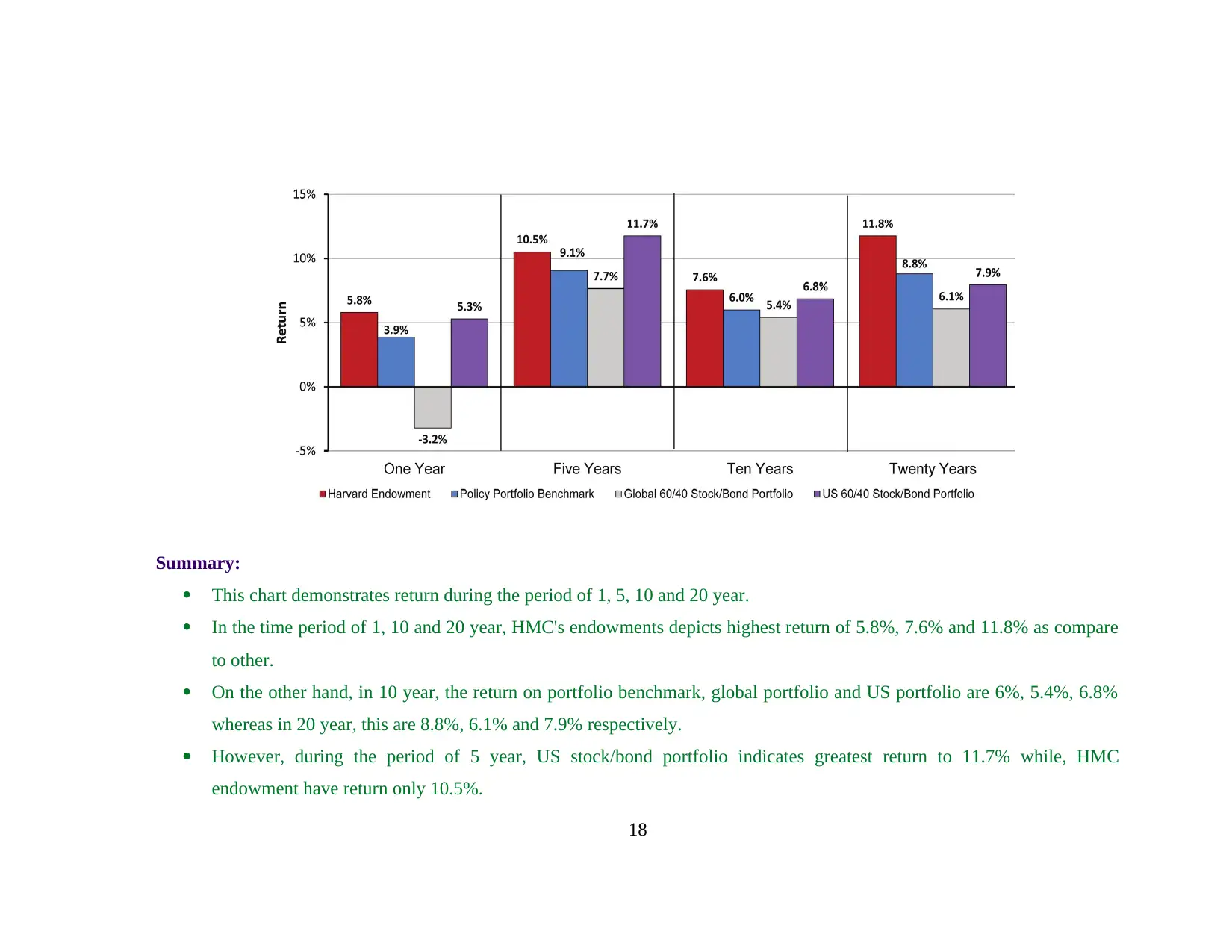

Summary:

This chart demonstrates return during the period of 1, 5, 10 and 20 year.

In the time period of 1, 10 and 20 year, HMC's endowments depicts highest return of 5.8%, 7.6% and 11.8% as compare

to other.

On the other hand, in 10 year, the return on portfolio benchmark, global portfolio and US portfolio are 6%, 5.4%, 6.8%

whereas in 20 year, this are 8.8%, 6.1% and 7.9% respectively.

However, during the period of 5 year, US stock/bond portfolio indicates greatest return to 11.7% while, HMC

endowment have return only 10.5%.

18

This chart demonstrates return during the period of 1, 5, 10 and 20 year.

In the time period of 1, 10 and 20 year, HMC's endowments depicts highest return of 5.8%, 7.6% and 11.8% as compare

to other.

On the other hand, in 10 year, the return on portfolio benchmark, global portfolio and US portfolio are 6%, 5.4%, 6.8%

whereas in 20 year, this are 8.8%, 6.1% and 7.9% respectively.

However, during the period of 5 year, US stock/bond portfolio indicates greatest return to 11.7% while, HMC

endowment have return only 10.5%.

18

Question: 2. What is the role of Limited Liability Partnerships (LLPs) in the organization and structure of the Private Equity

Market? Describe How LLPs facilitate the process of intermediation in the Private Equity market? How are the challenges of

information asymmetry that is characteristic of private equity investing addressed. Comment on the role of the General partners.

Answer:

Meaning of LLP

When two or more people own a general partnership they share open liability for the debt and financial obligation of the

business is known as LLP.

In general partnership, all the partners owes unlimited liability whereas the common structure of LLP is that partners

liability is limited for their financial obligations.

Role of LLP in the private equity:

LLP plays an important role in the structure of private equity, it is because, PE funds follows a framework which take

into account the partners fund, investment horizon, managerial fees and other factors mentioned in the limited

partnership agreement (LPA).

LLP can also be seen as a different opportunity for the investors from the private equity, in which, fund can be provided

in the form of LBO, Mezzanine, distressed debt, loans etc.

Role of general partners:

By registering with state agency general partner, firm can create a limited liability partnership. They contribute capital to

the firm but not participate in regular management of business. General partner can be litigate for any amount of money the

business build on and can end up using own personal assets to pay debt.

Question 3: How has the HMC endowment fund approached asset allocation? What are their main objectives and constraints to

investing in private equity?

Answer:

19

Market? Describe How LLPs facilitate the process of intermediation in the Private Equity market? How are the challenges of

information asymmetry that is characteristic of private equity investing addressed. Comment on the role of the General partners.

Answer:

Meaning of LLP

When two or more people own a general partnership they share open liability for the debt and financial obligation of the

business is known as LLP.

In general partnership, all the partners owes unlimited liability whereas the common structure of LLP is that partners

liability is limited for their financial obligations.

Role of LLP in the private equity:

LLP plays an important role in the structure of private equity, it is because, PE funds follows a framework which take

into account the partners fund, investment horizon, managerial fees and other factors mentioned in the limited

partnership agreement (LPA).

LLP can also be seen as a different opportunity for the investors from the private equity, in which, fund can be provided

in the form of LBO, Mezzanine, distressed debt, loans etc.

Role of general partners:

By registering with state agency general partner, firm can create a limited liability partnership. They contribute capital to

the firm but not participate in regular management of business. General partner can be litigate for any amount of money the

business build on and can end up using own personal assets to pay debt.

Question 3: How has the HMC endowment fund approached asset allocation? What are their main objectives and constraints to

investing in private equity?

Answer:

19

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Approach of HMC's assets allocation and its objective

Asset allocation is the most fundamental strategy for investment decision it is also like challenging task for firm. The

goal of Harvard University endowment is to take strategic investment decision as an institutional investor. In this approach

assets class return, risk and correlation exception serve as the basis for optimization, and has high certainty in its input. For

assets allocation, investor like to follow a tried and true formula for minimizing the risk.

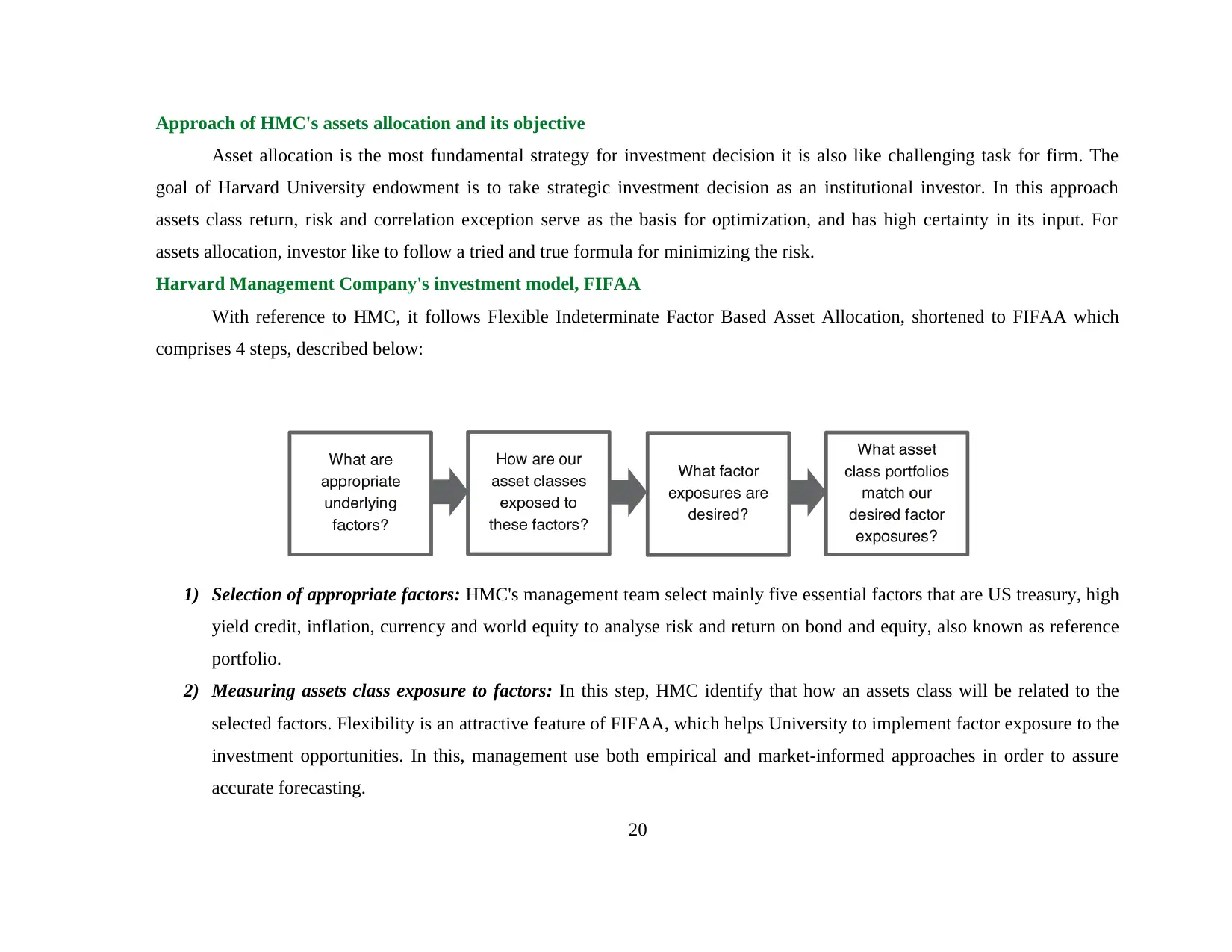

Harvard Management Company's investment model, FIFAA

With reference to HMC, it follows Flexible Indeterminate Factor Based Asset Allocation, shortened to FIFAA which

comprises 4 steps, described below:

1) Selection of appropriate factors: HMC's management team select mainly five essential factors that are US treasury, high

yield credit, inflation, currency and world equity to analyse risk and return on bond and equity, also known as reference

portfolio.

2) Measuring assets class exposure to factors: In this step, HMC identify that how an assets class will be related to the

selected factors. Flexibility is an attractive feature of FIFAA, which helps University to implement factor exposure to the

investment opportunities. In this, management use both empirical and market-informed approaches in order to assure

accurate forecasting.

20

Asset allocation is the most fundamental strategy for investment decision it is also like challenging task for firm. The

goal of Harvard University endowment is to take strategic investment decision as an institutional investor. In this approach

assets class return, risk and correlation exception serve as the basis for optimization, and has high certainty in its input. For

assets allocation, investor like to follow a tried and true formula for minimizing the risk.

Harvard Management Company's investment model, FIFAA

With reference to HMC, it follows Flexible Indeterminate Factor Based Asset Allocation, shortened to FIFAA which

comprises 4 steps, described below:

1) Selection of appropriate factors: HMC's management team select mainly five essential factors that are US treasury, high

yield credit, inflation, currency and world equity to analyse risk and return on bond and equity, also known as reference

portfolio.

2) Measuring assets class exposure to factors: In this step, HMC identify that how an assets class will be related to the

selected factors. Flexibility is an attractive feature of FIFAA, which helps University to implement factor exposure to the

investment opportunities. In this, management use both empirical and market-informed approaches in order to assure

accurate forecasting.

20

3) Choosing factor exposure: This step is about selection of appropriate factor exposure which is based on both risk -return

portfolio. Management team chose factor by taking into consideration decrease in equity exposure, minimizing inflation

exposure, enhance dollar value and increase bond and high yield exposure. It is the main basis of HMC's strategic assets

allocation to fulfill the long term objectives.

4) Creating an assets class portfolio: This step involves creation of portfolio by deciding ranges for twelve or more assets

class. The most important point regarding portfolio creation is that it needs to satisfy or optimize all the five previously

discussed factors. The goal of the HMC's assets allocation process is to brings continuous improvements in multi-assets

class and mean-variance approach. HMC's 2016 assets allocation are analyzed here as under:

21

portfolio. Management team chose factor by taking into consideration decrease in equity exposure, minimizing inflation

exposure, enhance dollar value and increase bond and high yield exposure. It is the main basis of HMC's strategic assets

allocation to fulfill the long term objectives.

4) Creating an assets class portfolio: This step involves creation of portfolio by deciding ranges for twelve or more assets

class. The most important point regarding portfolio creation is that it needs to satisfy or optimize all the five previously

discussed factors. The goal of the HMC's assets allocation process is to brings continuous improvements in multi-assets

class and mean-variance approach. HMC's 2016 assets allocation are analyzed here as under:

21

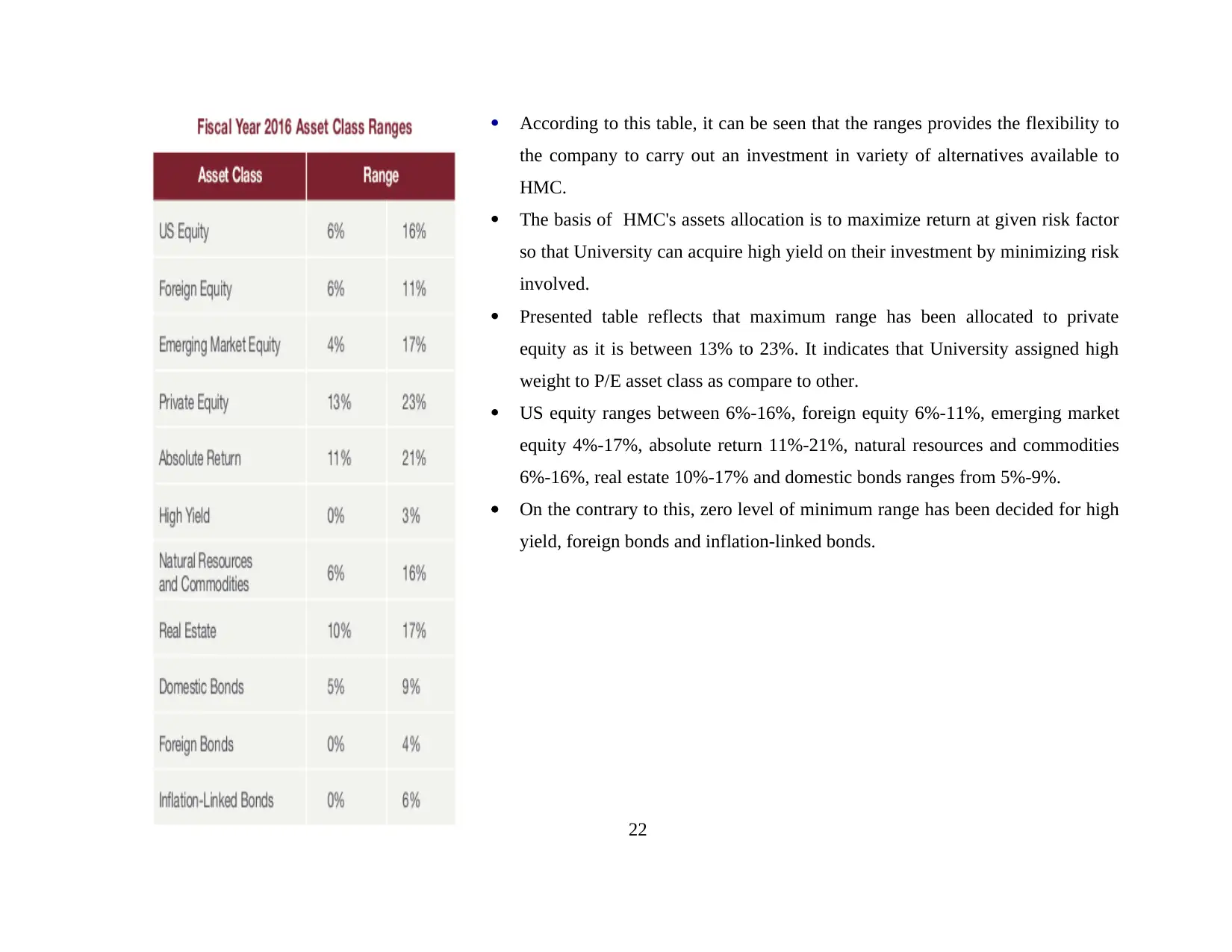

According to this table, it can be seen that the ranges provides the flexibility to

the company to carry out an investment in variety of alternatives available to

HMC.

The basis of HMC's assets allocation is to maximize return at given risk factor

so that University can acquire high yield on their investment by minimizing risk

involved.

Presented table reflects that maximum range has been allocated to private

equity as it is between 13% to 23%. It indicates that University assigned high

weight to P/E asset class as compare to other.

US equity ranges between 6%-16%, foreign equity 6%-11%, emerging market

equity 4%-17%, absolute return 11%-21%, natural resources and commodities

6%-16%, real estate 10%-17% and domestic bonds ranges from 5%-9%.

On the contrary to this, zero level of minimum range has been decided for high

yield, foreign bonds and inflation-linked bonds.

22

the company to carry out an investment in variety of alternatives available to

HMC.

The basis of HMC's assets allocation is to maximize return at given risk factor

so that University can acquire high yield on their investment by minimizing risk

involved.

Presented table reflects that maximum range has been allocated to private

equity as it is between 13% to 23%. It indicates that University assigned high

weight to P/E asset class as compare to other.

US equity ranges between 6%-16%, foreign equity 6%-11%, emerging market

equity 4%-17%, absolute return 11%-21%, natural resources and commodities

6%-16%, real estate 10%-17% and domestic bonds ranges from 5%-9%.

On the contrary to this, zero level of minimum range has been decided for high

yield, foreign bonds and inflation-linked bonds.

22

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Question: 4. Drawing evidence from the 2013 Harvard Endowment report, discuss the role of Private Equity investments in

institutional portfolios. Explain the main risks that could be faced by Private Equity investors and comment on how these can be

managed?

Answer:

Role of private equity in institutional portfolio:

The role of private equity in the institutional portfolio is increasing day by day. Henceforth, it is important for an

investor to actively manage their asset allocation and deliver better return in future.

Looking at the present volatile market era, many of the financial institutions are struggling because of weakened balance

sheet and high exposure to equity funding.

Moreover, bailout and stimulus packages in the nations did not boosted the market to provide adequate funds to the

institutions. As a result, there is only one real source available to them which is debt or equity to meet their financial

need.

Private Equity's risk and its management by HMC:

There are different type of risk involved in private equity. One of the most important risk is it is very difficult for the

investor to gain access to top-tier manager. Moreover, information asymmetry is a risk for the investor which can lead to

take harmful decisions.

Furthermore, dispersion risk is also a challenge which indicates that there is a huge difference in the median return and

top-quartile return for the PE firms. Besides this, they cannot compare the actual performance until the entire portfolio

companies are sold.

Apart from this, they also bear basic investment risk which is regarding identifying, selecting and investing in the

company. Thus, it becomes clear that private equity involved funding, liquidity, market and capital risk for the investors.

23

institutional portfolios. Explain the main risks that could be faced by Private Equity investors and comment on how these can be

managed?

Answer:

Role of private equity in institutional portfolio:

The role of private equity in the institutional portfolio is increasing day by day. Henceforth, it is important for an

investor to actively manage their asset allocation and deliver better return in future.

Looking at the present volatile market era, many of the financial institutions are struggling because of weakened balance

sheet and high exposure to equity funding.

Moreover, bailout and stimulus packages in the nations did not boosted the market to provide adequate funds to the

institutions. As a result, there is only one real source available to them which is debt or equity to meet their financial

need.

Private Equity's risk and its management by HMC:

There are different type of risk involved in private equity. One of the most important risk is it is very difficult for the

investor to gain access to top-tier manager. Moreover, information asymmetry is a risk for the investor which can lead to

take harmful decisions.

Furthermore, dispersion risk is also a challenge which indicates that there is a huge difference in the median return and

top-quartile return for the PE firms. Besides this, they cannot compare the actual performance until the entire portfolio

companies are sold.

Apart from this, they also bear basic investment risk which is regarding identifying, selecting and investing in the

company. Thus, it becomes clear that private equity involved funding, liquidity, market and capital risk for the investors.

23

Therefore, HMC use different methods to manage their risk and reach targets. Value at risk, liquidity adjusted value at

risk, cash flow at risk and sensitivity analysis etc. are the several types which are used by them in their risk management

framework.

Furthermore, diversification, monitoring etc. are also used by the HMC's investment team to minimize their risk and

maximize return.

Harvard Management Company's 2013 Endowment report

Important highlights:

24

risk, cash flow at risk and sensitivity analysis etc. are the several types which are used by them in their risk management

framework.

Furthermore, diversification, monitoring etc. are also used by the HMC's investment team to minimize their risk and

maximize return.

Harvard Management Company's 2013 Endowment report

Important highlights:

24

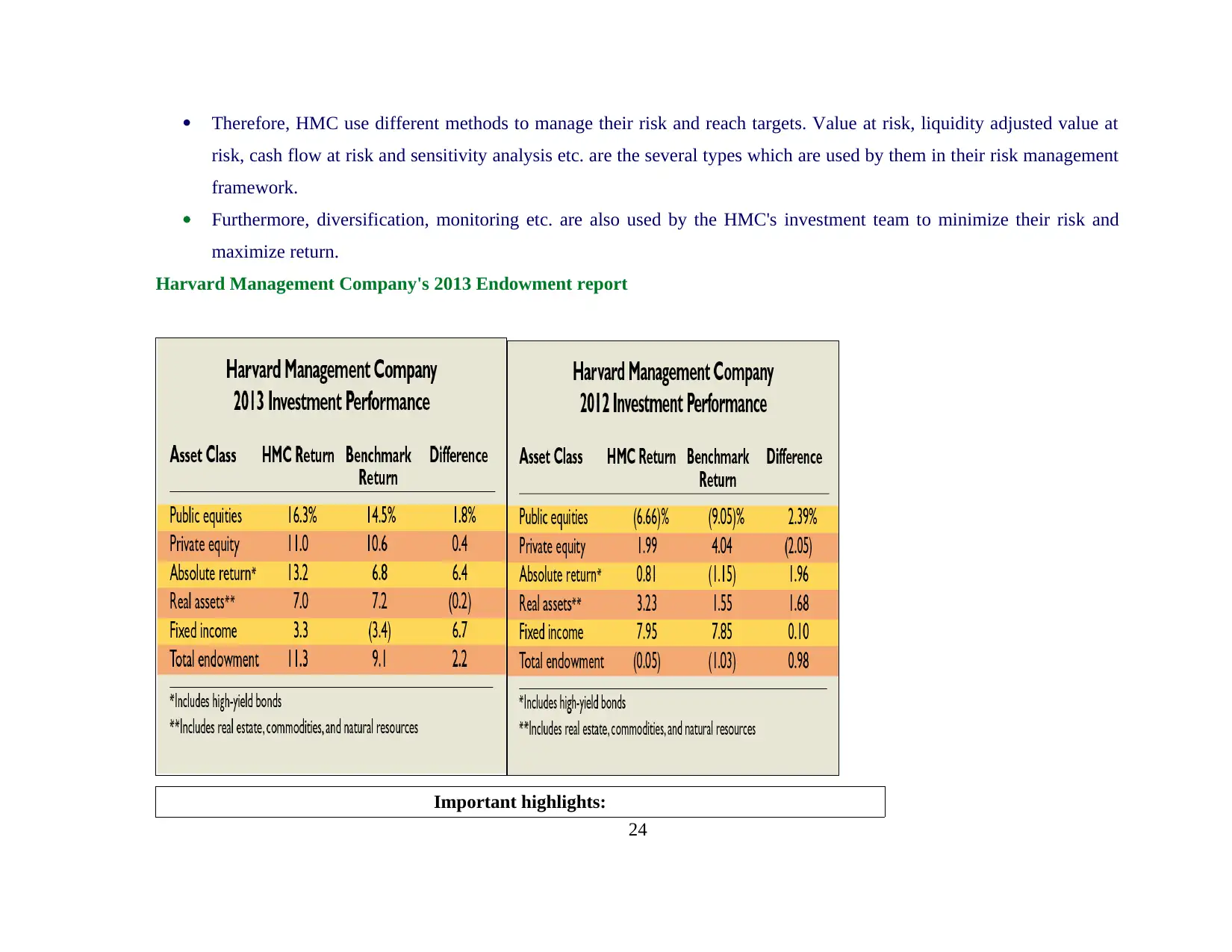

According to the table, it can be seen that on 30th June, 2013, HMC's endowment valued

at $32.7 billion which was increased by $2 billion or by 6.5% from the endowment

value of $30.7 billion in 2012.

During fiscal year 2013, HMC's endowment assets returned 11.3% while in the

historical year, it showed negative return. Henceforth, it can be stated that it was a better

improvement as it shows growth in return.

Public equity assets delivered favorable return of 16.3% which is higher than benchmark

of 14.5%. On the other hand, fixed income and real-estate returned 3.3% and 7.0%

respectively.

HMC's overall endowment was 11.3% which exceeded the benchmark by 2.2% as it was

9.1%.

While, on the basis of internal comparative study, it has been noticed that HMC return

for 2012 was negative to 0.05% which rose up to 11.3% in 2015 which is an evidence

of good improvements.

Question: 5. Describe the main risks inherent in Private Equity Investments and comment on how these are managed by

Harvard Endowment?

Answer:

Inherent risk and its management by Harvard

Risk management plays an inevitable role in designing a successful portfolio. With reference to HMC, its Chief

Investment Officer (CIO) manage its endowment investment portfolio by integrating risk management strategy with its

portfolio creation or investment strategy.

25

at $32.7 billion which was increased by $2 billion or by 6.5% from the endowment

value of $30.7 billion in 2012.

During fiscal year 2013, HMC's endowment assets returned 11.3% while in the

historical year, it showed negative return. Henceforth, it can be stated that it was a better

improvement as it shows growth in return.

Public equity assets delivered favorable return of 16.3% which is higher than benchmark

of 14.5%. On the other hand, fixed income and real-estate returned 3.3% and 7.0%

respectively.

HMC's overall endowment was 11.3% which exceeded the benchmark by 2.2% as it was

9.1%.

While, on the basis of internal comparative study, it has been noticed that HMC return

for 2012 was negative to 0.05% which rose up to 11.3% in 2015 which is an evidence

of good improvements.

Question: 5. Describe the main risks inherent in Private Equity Investments and comment on how these are managed by

Harvard Endowment?

Answer:

Inherent risk and its management by Harvard

Risk management plays an inevitable role in designing a successful portfolio. With reference to HMC, its Chief

Investment Officer (CIO) manage its endowment investment portfolio by integrating risk management strategy with its

portfolio creation or investment strategy.

25

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

It identify risk in the PE and manage it by taking appropriate actions on a timely basis. CIO adjust the inflation rate to

fulfill the current and potential requirement of the university in an effective manner.

Moreover, risk adjusted assets allocation and long-term partnership with the managers assure its operational success.

Further, in order to eliminate risk, its portfolio is created by making mean-variance analysis.

HMC's investment committee and board member are minimizing multiple form of risk such as market, leverage,

illiquidity and counter party risk by continuous monitoring and controlling.

HMC's management board pay focus on measuring its investment risk so as to establish effective control over it.

Moreover, its risk tolerance factor is also a main factor in the portfolio designing.

HMC works with the University to identify and measure different risk parameters and thereby generate adequate return

at an acceptable level of risk. It enable company to meet the return expectation of the University on its universally

diversified investment. portfolio.

ESG Integration, Active ownership and Collaboration are also the main factors which are taken into account by its

portfolio strategy's Managing Director. In this, ESG integration comprises monitoring, evaluation, due diligence and

assets management whereas collaboration depicts that HMC works with universal investors in order to assure sustainable

investment strategies.

Question: 6. Discuss the role of due diligence in private equity investing and comment on how this may be implemented by the

Harvard University Endowment fund?

Answer:

Role of due diligence in private equity

Role of due diligence in private equity firm is understood as a second or third derivative between existing management

and the new owners. Quality of information also refines between shareholder and company by using this approach.

26

fulfill the current and potential requirement of the university in an effective manner.

Moreover, risk adjusted assets allocation and long-term partnership with the managers assure its operational success.

Further, in order to eliminate risk, its portfolio is created by making mean-variance analysis.

HMC's investment committee and board member are minimizing multiple form of risk such as market, leverage,

illiquidity and counter party risk by continuous monitoring and controlling.

HMC's management board pay focus on measuring its investment risk so as to establish effective control over it.

Moreover, its risk tolerance factor is also a main factor in the portfolio designing.

HMC works with the University to identify and measure different risk parameters and thereby generate adequate return

at an acceptable level of risk. It enable company to meet the return expectation of the University on its universally

diversified investment. portfolio.

ESG Integration, Active ownership and Collaboration are also the main factors which are taken into account by its

portfolio strategy's Managing Director. In this, ESG integration comprises monitoring, evaluation, due diligence and

assets management whereas collaboration depicts that HMC works with universal investors in order to assure sustainable

investment strategies.

Question: 6. Discuss the role of due diligence in private equity investing and comment on how this may be implemented by the

Harvard University Endowment fund?

Answer:

Role of due diligence in private equity

Role of due diligence in private equity firm is understood as a second or third derivative between existing management

and the new owners. Quality of information also refines between shareholder and company by using this approach.

26

However, appropriate time is allocated for selection of right kind of private equity through which rate of return can be

increased.

Furthermore, due diligence also teach among experienced management team within boundaries of operation with focus

upon leveraged balance sheet. They reallocate the company constrained operation to a larger facility to give the

opportunity to grow.

It internally shows that employees are responsible for overseeing operational due diligence also had other responsibility.

It also helps to disclosure in a privately owned enterprises it may be of poor quality, influenced by tax and other.

Private Equity Investment due diligence

Due diligence is regarded as a process of minimizing risk comprising in the portfolio. It is important for HMC to

perform significant due diligence while deciding their investment portfolio, particularly private equity investment, analyzed

below:

27

increased.

Furthermore, due diligence also teach among experienced management team within boundaries of operation with focus

upon leveraged balance sheet. They reallocate the company constrained operation to a larger facility to give the

opportunity to grow.

It internally shows that employees are responsible for overseeing operational due diligence also had other responsibility.

It also helps to disclosure in a privately owned enterprises it may be of poor quality, influenced by tax and other.

Private Equity Investment due diligence

Due diligence is regarded as a process of minimizing risk comprising in the portfolio. It is important for HMC to

perform significant due diligence while deciding their investment portfolio, particularly private equity investment, analyzed

below:

27

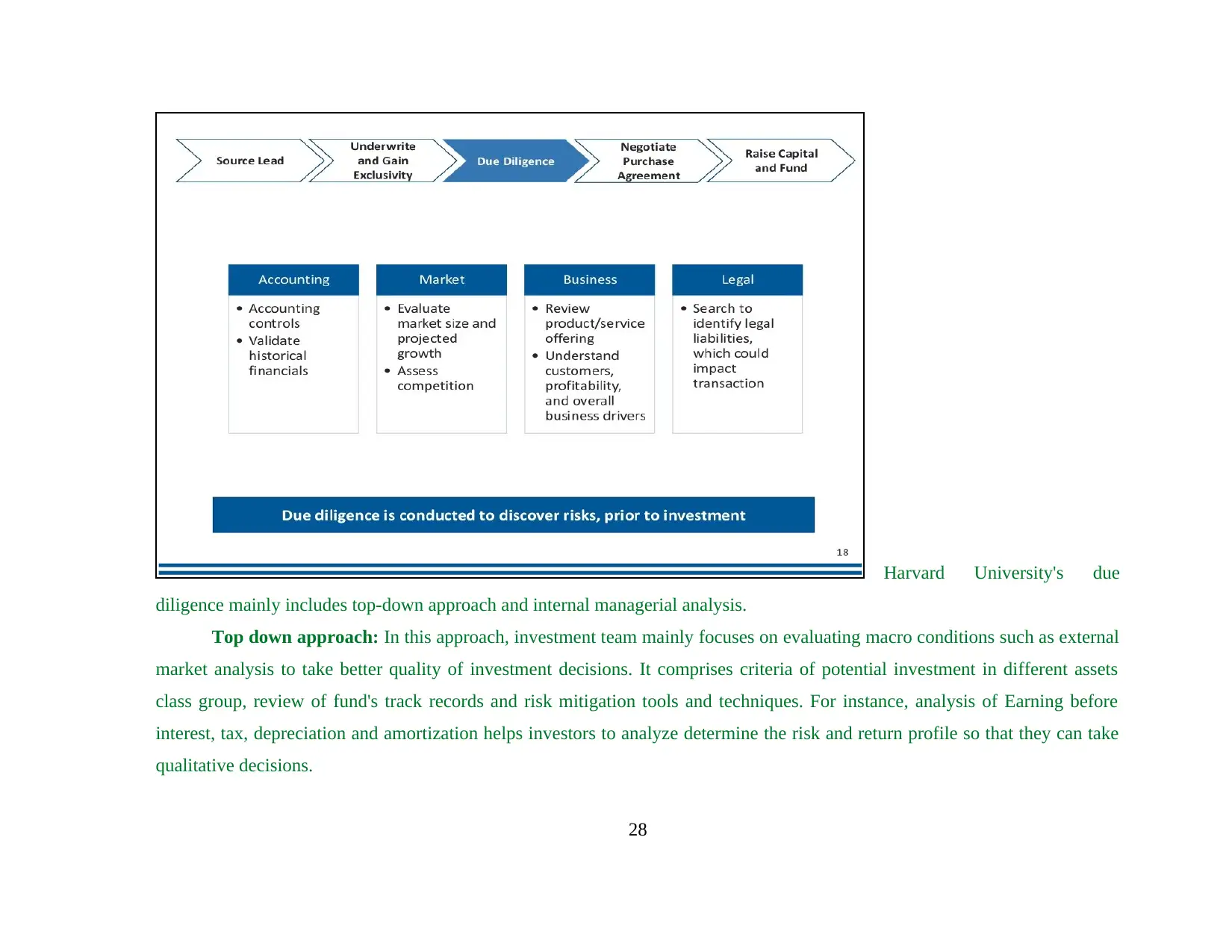

Harvard University's due

diligence mainly includes top-down approach and internal managerial analysis.

Top down approach: In this approach, investment team mainly focuses on evaluating macro conditions such as external

market analysis to take better quality of investment decisions. It comprises criteria of potential investment in different assets

class group, review of fund's track records and risk mitigation tools and techniques. For instance, analysis of Earning before

interest, tax, depreciation and amortization helps investors to analyze determine the risk and return profile so that they can take

qualitative decisions.

28

diligence mainly includes top-down approach and internal managerial analysis.

Top down approach: In this approach, investment team mainly focuses on evaluating macro conditions such as external

market analysis to take better quality of investment decisions. It comprises criteria of potential investment in different assets

class group, review of fund's track records and risk mitigation tools and techniques. For instance, analysis of Earning before

interest, tax, depreciation and amortization helps investors to analyze determine the risk and return profile so that they can take

qualitative decisions.

28

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Manager specific analysis: In this approach, managers examine historical financial records and allocate resources to

gain maximum return. In this, fund analysts consider different segments and industrial sectors to analyze risk/return and make

better portfolio decisions.

HMC's PE due diligence process

HMC's initial due diligence starts with screening process, in which, investment management team analyze historical

financial track records, their business strategy and analysis of management team as well.

After this, at the qualification phase, Harvard University review internal financial statements, operational structure and

projections also.

Thereafter, it will be passed to the next stage, in which, investment board review assets allocation for the portfolio

creation. Qualified investment opportunity will be approved through a formal mechanism.

Managers regularly monitor the investment progress so as to create an optimum portfolio by maximizing return at an

acceptable level of risk.

Challenge in due diligence

One of the most important challenge is that it is very complex for the investors to obtain precise and prominent

information about the market. It is because, in the present era, market is highly volatile. Therefore, it becomes very tough

for an investors to estimate authentic information hence, incorrect information may lead to harmful decisions and

decline return as well.

Volatile external market conditions makes it difficult for the investors to forecast future trend and identify an accurate

amount of future cash flows on potential investment. Thus, wrongful projection may lead to take worst quality of

investment decisions and may lead to failure.

The projection is also dependent upon the expertise and top quality professionals who have great experience in the PE

investment. Therefore, lack of experienced investment team is also a challenge for HMC.

29

gain maximum return. In this, fund analysts consider different segments and industrial sectors to analyze risk/return and make

better portfolio decisions.

HMC's PE due diligence process

HMC's initial due diligence starts with screening process, in which, investment management team analyze historical

financial track records, their business strategy and analysis of management team as well.

After this, at the qualification phase, Harvard University review internal financial statements, operational structure and

projections also.

Thereafter, it will be passed to the next stage, in which, investment board review assets allocation for the portfolio

creation. Qualified investment opportunity will be approved through a formal mechanism.

Managers regularly monitor the investment progress so as to create an optimum portfolio by maximizing return at an

acceptable level of risk.

Challenge in due diligence

One of the most important challenge is that it is very complex for the investors to obtain precise and prominent

information about the market. It is because, in the present era, market is highly volatile. Therefore, it becomes very tough

for an investors to estimate authentic information hence, incorrect information may lead to harmful decisions and

decline return as well.

Volatile external market conditions makes it difficult for the investors to forecast future trend and identify an accurate

amount of future cash flows on potential investment. Thus, wrongful projection may lead to take worst quality of

investment decisions and may lead to failure.

The projection is also dependent upon the expertise and top quality professionals who have great experience in the PE

investment. Therefore, lack of experienced investment team is also a challenge for HMC.

29

SECTION B

Question: 1. Barcelona’s Venture Fund is evaluating a $5 million investment in Cayman Industries. The fund manager has

calculated a cost of equity of 17% and estimates that if Cayman survives for four years, the payoff from selling the stake in

Cayman will be $30 million. The fund manager has estimated the following failure probabilities for Cayman Industries:

Year 1 2 3 4

Probability of Failure 30% 20% 15% 10%

What is the net present value of the potential investment in Cayman Industries?

Answer: According to the scenario, Barcelona’s venture fund is desire to make investment of $5m dollar in Cayman Industries.

The fund manager determined that cost of equity is 17% and also forecast that if the company survives for 4 years, then payoff

from selling the stake in the Cayman will be around $30m. The finance manager predicted that the possibility of project failure

are 30%, 20%, 15% and 10% respectively. Now, Barcelona is intended to assess the viability of this proposal which can be done

through identifying the net present value of the project. NPV indicates the net return which Barcelona can generate by investing

money into Cayman Industries. It is considered as the best technique as it take into account the time value of money and provide

more realistic results about the project return. In the corporate budgeting, NPV method use cost of equity as a discounting rate to

find out the future value of estimated return. Thereafter, total of future value is subtracted from the initial investment to find out

the net project return, called NPV. According to the selection criteria of this rule, if the project indicates favorable or positive

return than investor can accept it. However, in the case of two alternative, potential capitalists has to select such proposal which

yield greater return in the future period. As per the scenario, net present value is calculated here as under:

Probability of project's success

Year Failure probability Success probability (1-failure probability)

1 0.30 0.7

30

Question: 1. Barcelona’s Venture Fund is evaluating a $5 million investment in Cayman Industries. The fund manager has

calculated a cost of equity of 17% and estimates that if Cayman survives for four years, the payoff from selling the stake in

Cayman will be $30 million. The fund manager has estimated the following failure probabilities for Cayman Industries:

Year 1 2 3 4

Probability of Failure 30% 20% 15% 10%

What is the net present value of the potential investment in Cayman Industries?

Answer: According to the scenario, Barcelona’s venture fund is desire to make investment of $5m dollar in Cayman Industries.

The fund manager determined that cost of equity is 17% and also forecast that if the company survives for 4 years, then payoff

from selling the stake in the Cayman will be around $30m. The finance manager predicted that the possibility of project failure

are 30%, 20%, 15% and 10% respectively. Now, Barcelona is intended to assess the viability of this proposal which can be done

through identifying the net present value of the project. NPV indicates the net return which Barcelona can generate by investing

money into Cayman Industries. It is considered as the best technique as it take into account the time value of money and provide

more realistic results about the project return. In the corporate budgeting, NPV method use cost of equity as a discounting rate to

find out the future value of estimated return. Thereafter, total of future value is subtracted from the initial investment to find out

the net project return, called NPV. According to the selection criteria of this rule, if the project indicates favorable or positive

return than investor can accept it. However, in the case of two alternative, potential capitalists has to select such proposal which

yield greater return in the future period. As per the scenario, net present value is calculated here as under:

Probability of project's success

Year Failure probability Success probability (1-failure probability)

1 0.30 0.7

30

2 0.20 0.8

3 0.15 0.85

4 0.10 0.9

Total probability of project's success = 0.70*0.80*0.85*0.90 = 42.84%

Total probability of project's success = 1- 42.84% = 57.16%

According to this, if Cayman survives for a time period of 4 year, than expected NPV will be computed as under:

Money obtain at the end of 4th year by selling the stake in Cayman = $30,000,000

Cost of equity (ke) = (1+17%) ^4 = 1.874

= $30,000,000/1.874

= $16,009,501

Expected NPV of venture capital = ∑ (Period cash flow/ (1+r) ^t) - Initial investment

(0.4284*$16,009,501)+ (0.5716*$5,000,000)

= ($6,858,470 - $2,858,000)

= $4,000,470

Taking into account the results, it can be seen that if the Cayman operates successfully during the projected period of 4

years, than Barcelona can generate positive NPV worth $4,000,470 on his potential investment of $5m. Henceforth, it can be

said that he should accept the project and invest money into the Cayman Industries.

Question: 2. A venture capital Fund Manager is considering investing $2,500,000 in a new project. The projected cash flow

from the project is $12,000,000 at the end of five years if the project is successful at the end of the 5-year period. The cost of

equity for the investor is 15%, and following extensive due diligence on the project the manager has established that there is a

possibility that the project may not survive the 5-year period. The due diligence process has also revealed that there is a

31

3 0.15 0.85

4 0.10 0.9

Total probability of project's success = 0.70*0.80*0.85*0.90 = 42.84%

Total probability of project's success = 1- 42.84% = 57.16%

According to this, if Cayman survives for a time period of 4 year, than expected NPV will be computed as under:

Money obtain at the end of 4th year by selling the stake in Cayman = $30,000,000

Cost of equity (ke) = (1+17%) ^4 = 1.874

= $30,000,000/1.874

= $16,009,501

Expected NPV of venture capital = ∑ (Period cash flow/ (1+r) ^t) - Initial investment

(0.4284*$16,009,501)+ (0.5716*$5,000,000)

= ($6,858,470 - $2,858,000)

= $4,000,470

Taking into account the results, it can be seen that if the Cayman operates successfully during the projected period of 4

years, than Barcelona can generate positive NPV worth $4,000,470 on his potential investment of $5m. Henceforth, it can be

said that he should accept the project and invest money into the Cayman Industries.

Question: 2. A venture capital Fund Manager is considering investing $2,500,000 in a new project. The projected cash flow

from the project is $12,000,000 at the end of five years if the project is successful at the end of the 5-year period. The cost of

equity for the investor is 15%, and following extensive due diligence on the project the manager has established that there is a

possibility that the project may not survive the 5-year period. The due diligence process has also revealed that there is a

31

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

possibility that the project can fail in any given year over the five years. The estimated probability of failure in any given year is

presented in the table below;

Estimated Probability of Failure

Year 1 2 3 4 5

Probability of Failure 0.20 0.20 0.17 0.15 0.15

Further research by an analyst at the Fund Management firm has revealed that there is an investment bank that is familiar with

the venture and is willing to insure against failure for a fee of $1,000,000. The Fund Management firm has approached you to

express an opinion on the following;

1. Proceed without the insurance contract

2. Proceed with the insurance contract

If you become aware that the investment bank has priced risk on the insurance contract correctly, comment on any additional

due diligence information you would recommend the Fund Manager to seek before engaging on the investment.

Answer:

32

presented in the table below;

Estimated Probability of Failure

Year 1 2 3 4 5

Probability of Failure 0.20 0.20 0.17 0.15 0.15

Further research by an analyst at the Fund Management firm has revealed that there is an investment bank that is familiar with

the venture and is willing to insure against failure for a fee of $1,000,000. The Fund Management firm has approached you to

express an opinion on the following;

1. Proceed without the insurance contract

2. Proceed with the insurance contract

If you become aware that the investment bank has priced risk on the insurance contract correctly, comment on any additional

due diligence information you would recommend the Fund Manager to seek before engaging on the investment.

Answer:

32

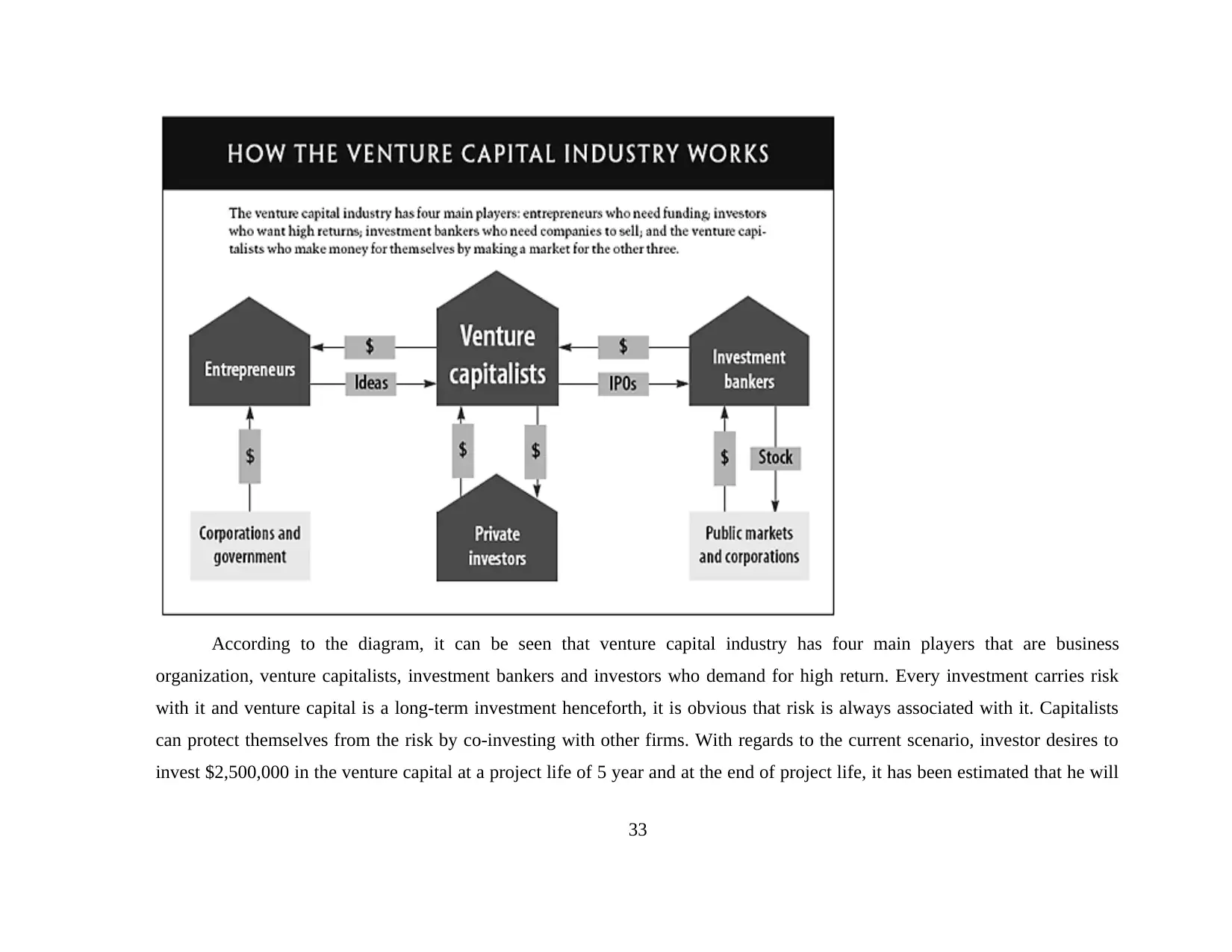

According to the diagram, it can be seen that venture capital industry has four main players that are business

organization, venture capitalists, investment bankers and investors who demand for high return. Every investment carries risk

with it and venture capital is a long-term investment henceforth, it is obvious that risk is always associated with it. Capitalists

can protect themselves from the risk by co-investing with other firms. With regards to the current scenario, investor desires to

invest $2,500,000 in the venture capital at a project life of 5 year and at the end of project life, it has been estimated that he will

33

organization, venture capitalists, investment bankers and investors who demand for high return. Every investment carries risk

with it and venture capital is a long-term investment henceforth, it is obvious that risk is always associated with it. Capitalists

can protect themselves from the risk by co-investing with other firms. With regards to the current scenario, investor desires to

invest $2,500,000 in the venture capital at a project life of 5 year and at the end of project life, it has been estimated that he will

33

obtain $12,000,000. The cost of equity or discounting rate is 15% and the due diligence process revealed that there is also a

probability of project failure hence, the NPV calculations is done below:

1. Proceed without the insurance contract

Year Failure probability

Success probability (1-failure

probability)

1 0.2 0.8

2 0.2 0.8

3 0.17 0.83

4 0.15 0.85

5 0.15 0.85

Total probability of project's success = 0.80*0.80*0.83*0.85*0.85= 38.38%

Total probability of project's success = 1- 38.38% = 61.62%

Money obtain at the end of 5h year by selling the stake = $12,000,000

Cost of equity (ke) = (1+15%) ^5 = 2.011

= $12,000,000/2.011

= $5,966,121

Expected NPV of venture capital = ∑ (Period cash flow/ (1+r) ^t) - Initial investment

(0.3838*$5,966,121+ (0.6162*$2,500,000)

= ($2,289,749 - $1,540,520)

= $749,229

2. Proceed with an insurance contract

Current scenario stated that an investor is willing to insure against project failure at a fee of $1m. By this, capitalists can

assure smooth running of the project and remove the risk of its failure. Here, the expected project's NPV will be as under:

34

probability of project failure hence, the NPV calculations is done below:

1. Proceed without the insurance contract

Year Failure probability

Success probability (1-failure

probability)

1 0.2 0.8

2 0.2 0.8

3 0.17 0.83

4 0.15 0.85

5 0.15 0.85

Total probability of project's success = 0.80*0.80*0.83*0.85*0.85= 38.38%

Total probability of project's success = 1- 38.38% = 61.62%

Money obtain at the end of 5h year by selling the stake = $12,000,000

Cost of equity (ke) = (1+15%) ^5 = 2.011

= $12,000,000/2.011

= $5,966,121

Expected NPV of venture capital = ∑ (Period cash flow/ (1+r) ^t) - Initial investment

(0.3838*$5,966,121+ (0.6162*$2,500,000)

= ($2,289,749 - $1,540,520)

= $749,229

2. Proceed with an insurance contract

Current scenario stated that an investor is willing to insure against project failure at a fee of $1m. By this, capitalists can

assure smooth running of the project and remove the risk of its failure. Here, the expected project's NPV will be as under:

34

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Expected NPV = ($12,000,000/2.011) – (2,500,000+ 1,000,000)

= $5,966,121 – ($3,500,000)

= $2,466,121

3. Comment on additional due diligence to recommend the fund manager to seek before engaging on the investment

Apart from the insurance, there are different types of due diligence available to the fund manager while making any

investment. It includes screening, business and legal due diligence as well.

Screening due diligence: In this process, capitalists can review and evaluate various investment opportunities over its

project life with a predetermined criteria. It helps investor to to minimize risk and take better investment decisions.

Business due diligence: After identifying the opportunity, deal can be assigned to the junior and senior management

team to determine the project viability. It is a specific process, in which, managers review the investment project, market

potential and the business model as well to take better decisions.

Legal due diligence: Venture capitalists can recruit lawyers, advisers etc. to make right selection among all the

alternatives available to him.

Question: 3. Explain the stages in venture capital investing, venture capital investment characteristics, and challenges to venture

capital valuation and performance measurement?

Answer:

Process

Venture capitalists invest their money in the businesses and fulfill the financial requirement of the corporations. Its

process is discussed below:

Seed-stage: In the inaugural stage, capitalists provide money to the entrepreneurs of their product development, build an

efficient management team, business plan and conducting an extensive market research as well. Further, they also provide funds

to an entity to bear the cost of expansion such as sales and distribution, recruiting people and marketing as well.

35

= $5,966,121 – ($3,500,000)

= $2,466,121

3. Comment on additional due diligence to recommend the fund manager to seek before engaging on the investment

Apart from the insurance, there are different types of due diligence available to the fund manager while making any

investment. It includes screening, business and legal due diligence as well.

Screening due diligence: In this process, capitalists can review and evaluate various investment opportunities over its

project life with a predetermined criteria. It helps investor to to minimize risk and take better investment decisions.

Business due diligence: After identifying the opportunity, deal can be assigned to the junior and senior management

team to determine the project viability. It is a specific process, in which, managers review the investment project, market

potential and the business model as well to take better decisions.

Legal due diligence: Venture capitalists can recruit lawyers, advisers etc. to make right selection among all the

alternatives available to him.

Question: 3. Explain the stages in venture capital investing, venture capital investment characteristics, and challenges to venture

capital valuation and performance measurement?

Answer:

Process

Venture capitalists invest their money in the businesses and fulfill the financial requirement of the corporations. Its

process is discussed below:

Seed-stage: In the inaugural stage, capitalists provide money to the entrepreneurs of their product development, build an

efficient management team, business plan and conducting an extensive market research as well. Further, they also provide funds

to an entity to bear the cost of expansion such as sales and distribution, recruiting people and marketing as well.

35

Early stage: Companies which are ready to start their operations in the market, but still, they are not ready for

commercial manufacturing prevail in this stage. It involves both start-up and first stage, in which start-up investing support

product development and initial marketing whereas first stage is regarded as providing capital for the commercial production

and carrying out sales operations.

Formative stage: It is the combination of both the seed and early stage in which investor provide money for different

objectives which are discussed previously.

Later stage: In this, money is provided after starting the manufacturing process but still, before the IPO. This stage helps

to meet the financial need for plant expansion, bringing improvements in products, expanding the operations and Mezzanine

(bridge between IPO and expansion) as well.

Balanced stage: It is the last stage which includes collection of funds from seeds to Mezzanine. In this, money can be

used for varied purpose like mergers and acquisition, reduction in price to enhance competitive strength, taking a step towards

IPO etc.

Characteristic of venture capital funding:

Illiquidity is one of the basic feature of VC funding which indicates that it is not easy for an investor to convert

investment to the cash.

It is a type of long-term investment which ranges between 3 to 5 years but still, the possibility of return is very large.

It is very difficult for identify the market value of VC because of the reason, that such kind of assets are not traded at an

active marketplace.

It contains less historical risk because of unavailability of an active market.

Lack of information is also a characteristic of venture capital. The reason behind this is sometimes, an entrepreneur may

be new hence, in such case, little information will be available to the investor.

36

commercial manufacturing prevail in this stage. It involves both start-up and first stage, in which start-up investing support

product development and initial marketing whereas first stage is regarded as providing capital for the commercial production

and carrying out sales operations.

Formative stage: It is the combination of both the seed and early stage in which investor provide money for different

objectives which are discussed previously.

Later stage: In this, money is provided after starting the manufacturing process but still, before the IPO. This stage helps

to meet the financial need for plant expansion, bringing improvements in products, expanding the operations and Mezzanine

(bridge between IPO and expansion) as well.

Balanced stage: It is the last stage which includes collection of funds from seeds to Mezzanine. In this, money can be

used for varied purpose like mergers and acquisition, reduction in price to enhance competitive strength, taking a step towards

IPO etc.

Characteristic of venture capital funding:

Illiquidity is one of the basic feature of VC funding which indicates that it is not easy for an investor to convert

investment to the cash.

It is a type of long-term investment which ranges between 3 to 5 years but still, the possibility of return is very large.

It is very difficult for identify the market value of VC because of the reason, that such kind of assets are not traded at an

active marketplace.

It contains less historical risk because of unavailability of an active market.

Lack of information is also a characteristic of venture capital. The reason behind this is sometimes, an entrepreneur may

be new hence, in such case, little information will be available to the investor.

36

Vintage cycle indicates that start-up business volume is greatly dependent upon economic environment which provide

both opportunities and risk as well.

Challenges to valuation and performance measurement:

Requirement of a skilled, experienced and talented management team is a major challenge in the venture capital funding.

High payback period of the invested capital is also a challenge for the capitalists.