Audit Report Analysis of Harvey Norman Holdings Limited

VerifiedAdded on 2023/06/08

|13

|3261

|366

AI Summary

This report reflects the key information given in the audit report and responsibilities of the auditors. The audit report analysis, structure and responsibilities of the auditors have been analyzed in this report. The company selected for the case study purpose is Harvey Norman Holdings Limited and auditor’s independence and their responsibilities have been analysed to determine the key information about the company.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

HI6026 Audit, Assurance and Compliance

Trimester 2 2018

1

Trimester 2 2018

1

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

EXECUTIVE SUMMARY

This report reflects the key information given in the audit report and responsibilities

of the auditors. This report has been prepared on the selected company named Harvey

Normal Company. The audit report analysis, structure and responsibilities of the auditors

have been analyzed in this report. Harvey Norman Holding Limited is the company chosen in

the current research study. The group has the auditors named Ernst & Young who have issued

a clean report regarding the financials of the entity and the related controls. The report has

significantly laid the independence declaration that the auditors have made and the nature of

the non-audit services in form of tax compliance and others is also specified. The company

has paid overall remuneration to the auditors that has shown a certain rise when audit services

are concerned. The rest of the matters are briefly explained in the report presented herein.

2

This report reflects the key information given in the audit report and responsibilities

of the auditors. This report has been prepared on the selected company named Harvey

Normal Company. The audit report analysis, structure and responsibilities of the auditors

have been analyzed in this report. Harvey Norman Holding Limited is the company chosen in

the current research study. The group has the auditors named Ernst & Young who have issued

a clean report regarding the financials of the entity and the related controls. The report has

significantly laid the independence declaration that the auditors have made and the nature of

the non-audit services in form of tax compliance and others is also specified. The company

has paid overall remuneration to the auditors that has shown a certain rise when audit services

are concerned. The rest of the matters are briefly explained in the report presented herein.

2

Table of Contents

EXECUTIVE SUMMARY........................................................................................................2

INTRODUCTION......................................................................................................................3

AUDITOR’S INDEPENDENCE...............................................................................................3

PROVISION OF NON-AUDIT SERVICES.............................................................................3

AUDITER REMUNERATION.................................................................................................4

KEY AUDIT MATTERS..........................................................................................................4

AUDIT COMMITTEE & AUDIT CHARTER.........................................................................6

STRUCTURE............................................................................................................................6

FUNCTIONS.............................................................................................................................6

RESPONSIBILITIES.................................................................................................................6

AUDIT OPINION......................................................................................................................7

DIFFERENCE BETWEEN THE RESPONSIBILITIES OF MANAGEMENT AND

AUDITOR..................................................................................................................................7

MATERIAL SUBSEQUENT EVENTS....................................................................................7

CONCLUSION..........................................................................................................................8

REFERENCES...........................................................................................................................8

3

EXECUTIVE SUMMARY........................................................................................................2

INTRODUCTION......................................................................................................................3

AUDITOR’S INDEPENDENCE...............................................................................................3

PROVISION OF NON-AUDIT SERVICES.............................................................................3

AUDITER REMUNERATION.................................................................................................4

KEY AUDIT MATTERS..........................................................................................................4

AUDIT COMMITTEE & AUDIT CHARTER.........................................................................6

STRUCTURE............................................................................................................................6

FUNCTIONS.............................................................................................................................6

RESPONSIBILITIES.................................................................................................................6

AUDIT OPINION......................................................................................................................7

DIFFERENCE BETWEEN THE RESPONSIBILITIES OF MANAGEMENT AND

AUDITOR..................................................................................................................................7

MATERIAL SUBSEQUENT EVENTS....................................................................................7

CONCLUSION..........................................................................................................................8

REFERENCES...........................................................................................................................8

3

INTRODUCTION

The background of the current report lies on the reporting requirements related to the

auditor that are initiated by the International Auditing and Assurance Board (IAASB).

Following the line of these new requirements the current report analyses the company’s

annual report. The areas analysed include the declaration for auditor’s independence, report

of independent auditor, the performance of non-audit services by the auditor, remuneration of

auditor, the composition of the audit committee, and its role and functions, and key

consideration to the audit report issued by the auditor with special emphasis on the key audit

matters. The limelight question is if the company has followed with all the reporting

requirements in its annual report. All the assurance services as related to the auditor are also

reviewed. The company selected for the case study purpose is Harvey Norman Holdings

Limited and auditor’s independence and their responsibilities have been analysed to

determine the key information about the company.

AUDITOR’S INDEPENDENCE

The auditors of the Harvey Norman Holdings Limited are named Ernst & Young. It is

well evidenced by the directors that the regulations laid by the Corporations Act 2001 are

well complied. These regulations do relate to the independence of the auditor. Further, the

mention of audit committee is also made. It is specified that the audit committee is also

convinced and have recommended that the auditors have been independent in their operation.

The auditors have also given a declaration to the directors of the Harvey Norman Holdings

Limited regarding their independence (Harvey Norman Holdings Limited., 2016).The

declaration clearly states that the auditors have not made any contraventions as far as the

applicable codes of the professional conduct and the corporations act 2001, in relation to the

audit conducted are concerned (Tepalagul, and Lin, 2015). This auditor’s independence

report has shown how well auditors have performed and their independence with the Harvey

Norman Holdings Limited. It is analyzed that auditors should keep their independence with

the company when they are auditing the financial statements (Louwers, et al. 2015). In the

audit report, it is considered that auditor has complied with Independence requirements of the

auditing and assurance.

4

The background of the current report lies on the reporting requirements related to the

auditor that are initiated by the International Auditing and Assurance Board (IAASB).

Following the line of these new requirements the current report analyses the company’s

annual report. The areas analysed include the declaration for auditor’s independence, report

of independent auditor, the performance of non-audit services by the auditor, remuneration of

auditor, the composition of the audit committee, and its role and functions, and key

consideration to the audit report issued by the auditor with special emphasis on the key audit

matters. The limelight question is if the company has followed with all the reporting

requirements in its annual report. All the assurance services as related to the auditor are also

reviewed. The company selected for the case study purpose is Harvey Norman Holdings

Limited and auditor’s independence and their responsibilities have been analysed to

determine the key information about the company.

AUDITOR’S INDEPENDENCE

The auditors of the Harvey Norman Holdings Limited are named Ernst & Young. It is

well evidenced by the directors that the regulations laid by the Corporations Act 2001 are

well complied. These regulations do relate to the independence of the auditor. Further, the

mention of audit committee is also made. It is specified that the audit committee is also

convinced and have recommended that the auditors have been independent in their operation.

The auditors have also given a declaration to the directors of the Harvey Norman Holdings

Limited regarding their independence (Harvey Norman Holdings Limited., 2016).The

declaration clearly states that the auditors have not made any contraventions as far as the

applicable codes of the professional conduct and the corporations act 2001, in relation to the

audit conducted are concerned (Tepalagul, and Lin, 2015). This auditor’s independence

report has shown how well auditors have performed and their independence with the Harvey

Norman Holdings Limited. It is analyzed that auditors should keep their independence with

the company when they are auditing the financial statements (Louwers, et al. 2015). In the

audit report, it is considered that auditor has complied with Independence requirements of the

auditing and assurance.

4

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

PROVISION OF NON-AUDIT SERVICES

It is well mentioned in the report that the auditors are engaged in the provision of non-

audit services to the client along with the appraisal work. This thing is mentioned with a

specific headline in the annual report. Further, the directors have taken the recommendations

of the audit committee too regarding this provision of the services by the auditor. The non-

audit services extended by the auditor also comply with the requirements of the corporation’s

act 2001. It is completely analysed by the management that in no case the provision of these

non-audit services has harmed the independence that the auditors need to comply with. For

the financial year ending on June 30, 2017 the auditors have provided tax compliance

services worth $205,803 and other services worth $71,756 as non-audit services to the client

(Bell, Causholli, and Knechel, 2015). There are several other non-audit services which is

offered by auditors to Harvey Norman Holdings Limited such as advising the management

about the legal compliance and preparing the financial statement as per the applicable

accounting standards and harmonization with the international and domestic accounting

standards (Harvey Norman Holdings Limited., 2016).

AUDITER REMUNERATION

The remuneration of the auditors includes the payment that is either made or has to be

made to the auditors for the services they have provided to the client. The services include

both the audit and non-audit services (Choong, and Leung, 2015). In the case of Harvey

Norman Holdings Limited, there is an audit committee too. The remuneration in this case is

bound to be finalised by the audit committee after it gets decided either in the general

meeting or gets fixed by the board of directors. The following table represents the

remuneration that is paid to the auditors for the financial years 2016 and financial year 2017.

The changes that have taken place in the remuneration are also shown in percentage form

(Harvey Norman Holdings Limited., 2016).

AMOUNTS RECEIVED OR

DUE AND RECEIVABLE BY

ERNST & YOUNG FOR:

JUNE 2017

($)

JUNE 2016

($) % change

1. the audit and review function 1955946 1709834 14.39%

5

It is well mentioned in the report that the auditors are engaged in the provision of non-

audit services to the client along with the appraisal work. This thing is mentioned with a

specific headline in the annual report. Further, the directors have taken the recommendations

of the audit committee too regarding this provision of the services by the auditor. The non-

audit services extended by the auditor also comply with the requirements of the corporation’s

act 2001. It is completely analysed by the management that in no case the provision of these

non-audit services has harmed the independence that the auditors need to comply with. For

the financial year ending on June 30, 2017 the auditors have provided tax compliance

services worth $205,803 and other services worth $71,756 as non-audit services to the client

(Bell, Causholli, and Knechel, 2015). There are several other non-audit services which is

offered by auditors to Harvey Norman Holdings Limited such as advising the management

about the legal compliance and preparing the financial statement as per the applicable

accounting standards and harmonization with the international and domestic accounting

standards (Harvey Norman Holdings Limited., 2016).

AUDITER REMUNERATION

The remuneration of the auditors includes the payment that is either made or has to be

made to the auditors for the services they have provided to the client. The services include

both the audit and non-audit services (Choong, and Leung, 2015). In the case of Harvey

Norman Holdings Limited, there is an audit committee too. The remuneration in this case is

bound to be finalised by the audit committee after it gets decided either in the general

meeting or gets fixed by the board of directors. The following table represents the

remuneration that is paid to the auditors for the financial years 2016 and financial year 2017.

The changes that have taken place in the remuneration are also shown in percentage form

(Harvey Norman Holdings Limited., 2016).

AMOUNTS RECEIVED OR

DUE AND RECEIVABLE BY

ERNST & YOUNG FOR:

JUNE 2017

($)

JUNE 2016

($) % change

1. the audit and review function 1955946 1709834 14.39%

5

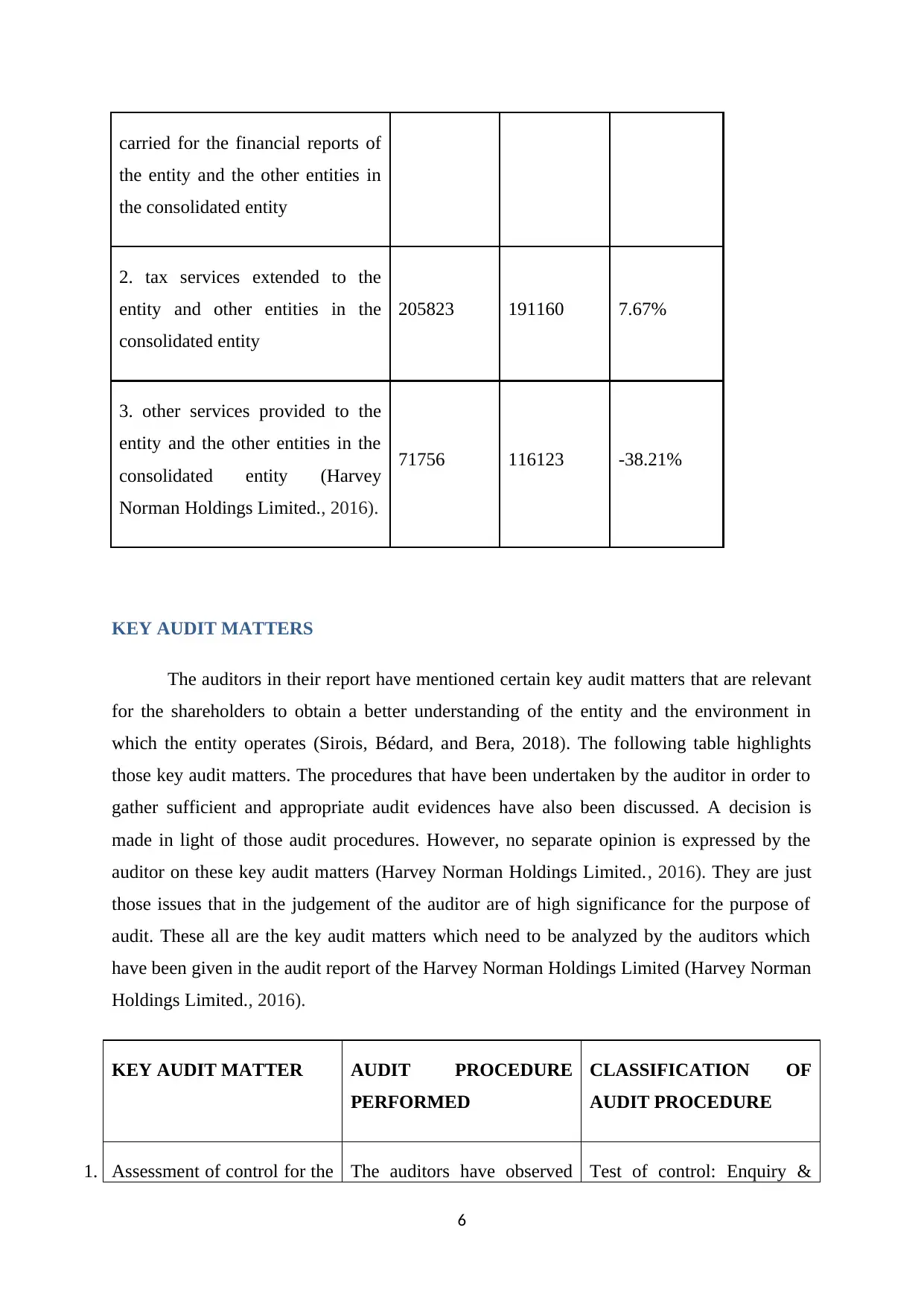

carried for the financial reports of

the entity and the other entities in

the consolidated entity

2. tax services extended to the

entity and other entities in the

consolidated entity

205823 191160 7.67%

3. other services provided to the

entity and the other entities in the

consolidated entity (Harvey

Norman Holdings Limited., 2016).

71756 116123 -38.21%

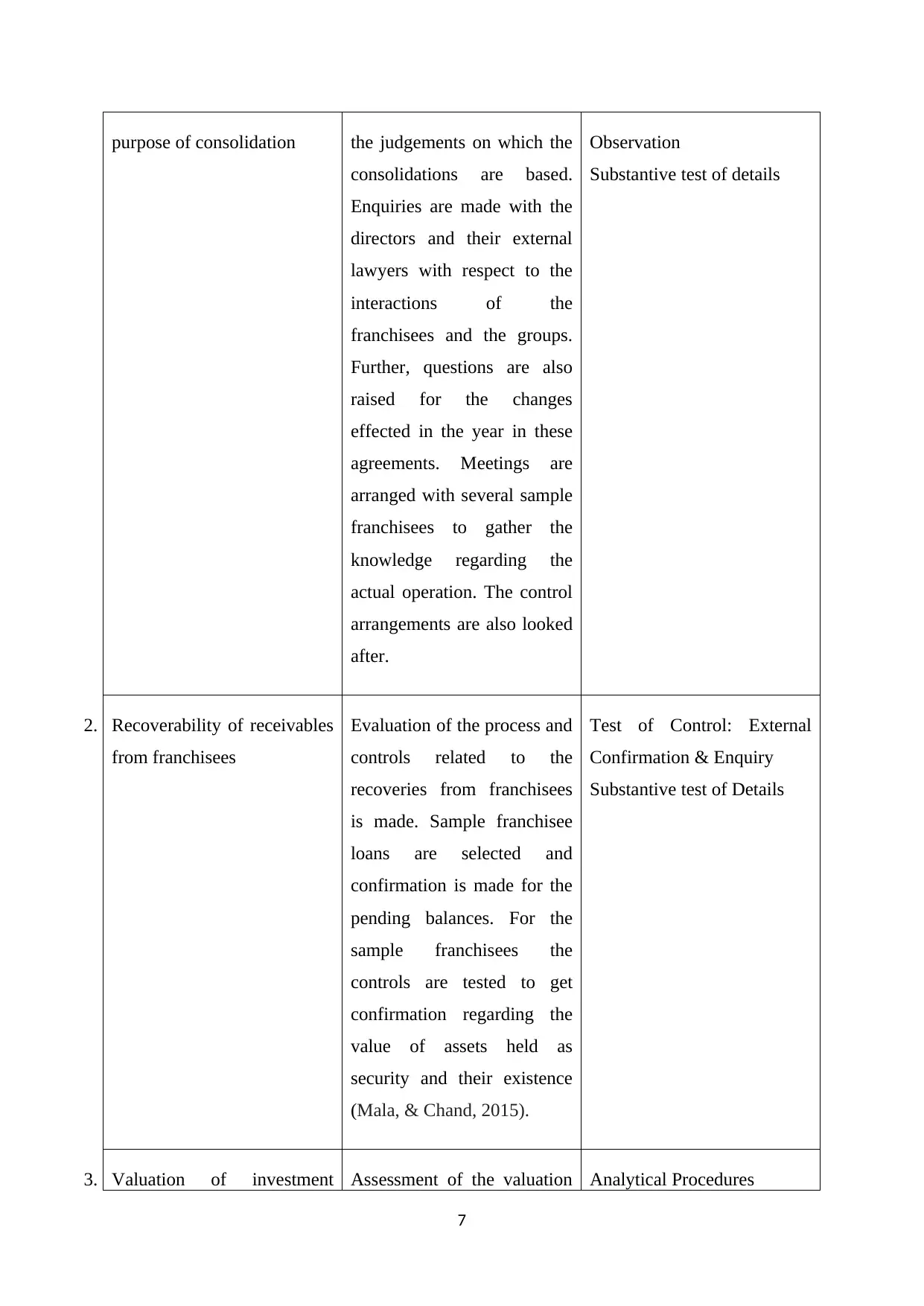

KEY AUDIT MATTERS

The auditors in their report have mentioned certain key audit matters that are relevant

for the shareholders to obtain a better understanding of the entity and the environment in

which the entity operates (Sirois, Bédard, and Bera, 2018). The following table highlights

those key audit matters. The procedures that have been undertaken by the auditor in order to

gather sufficient and appropriate audit evidences have also been discussed. A decision is

made in light of those audit procedures. However, no separate opinion is expressed by the

auditor on these key audit matters (Harvey Norman Holdings Limited., 2016). They are just

those issues that in the judgement of the auditor are of high significance for the purpose of

audit. These all are the key audit matters which need to be analyzed by the auditors which

have been given in the audit report of the Harvey Norman Holdings Limited (Harvey Norman

Holdings Limited., 2016).

KEY AUDIT MATTER AUDIT PROCEDURE

PERFORMED

CLASSIFICATION OF

AUDIT PROCEDURE

1. Assessment of control for the The auditors have observed Test of control: Enquiry &

6

the entity and the other entities in

the consolidated entity

2. tax services extended to the

entity and other entities in the

consolidated entity

205823 191160 7.67%

3. other services provided to the

entity and the other entities in the

consolidated entity (Harvey

Norman Holdings Limited., 2016).

71756 116123 -38.21%

KEY AUDIT MATTERS

The auditors in their report have mentioned certain key audit matters that are relevant

for the shareholders to obtain a better understanding of the entity and the environment in

which the entity operates (Sirois, Bédard, and Bera, 2018). The following table highlights

those key audit matters. The procedures that have been undertaken by the auditor in order to

gather sufficient and appropriate audit evidences have also been discussed. A decision is

made in light of those audit procedures. However, no separate opinion is expressed by the

auditor on these key audit matters (Harvey Norman Holdings Limited., 2016). They are just

those issues that in the judgement of the auditor are of high significance for the purpose of

audit. These all are the key audit matters which need to be analyzed by the auditors which

have been given in the audit report of the Harvey Norman Holdings Limited (Harvey Norman

Holdings Limited., 2016).

KEY AUDIT MATTER AUDIT PROCEDURE

PERFORMED

CLASSIFICATION OF

AUDIT PROCEDURE

1. Assessment of control for the The auditors have observed Test of control: Enquiry &

6

purpose of consolidation the judgements on which the

consolidations are based.

Enquiries are made with the

directors and their external

lawyers with respect to the

interactions of the

franchisees and the groups.

Further, questions are also

raised for the changes

effected in the year in these

agreements. Meetings are

arranged with several sample

franchisees to gather the

knowledge regarding the

actual operation. The control

arrangements are also looked

after.

Observation

Substantive test of details

2. Recoverability of receivables

from franchisees

Evaluation of the process and

controls related to the

recoveries from franchisees

is made. Sample franchisee

loans are selected and

confirmation is made for the

pending balances. For the

sample franchisees the

controls are tested to get

confirmation regarding the

value of assets held as

security and their existence

(Mala, & Chand, 2015).

Test of Control: External

Confirmation & Enquiry

Substantive test of Details

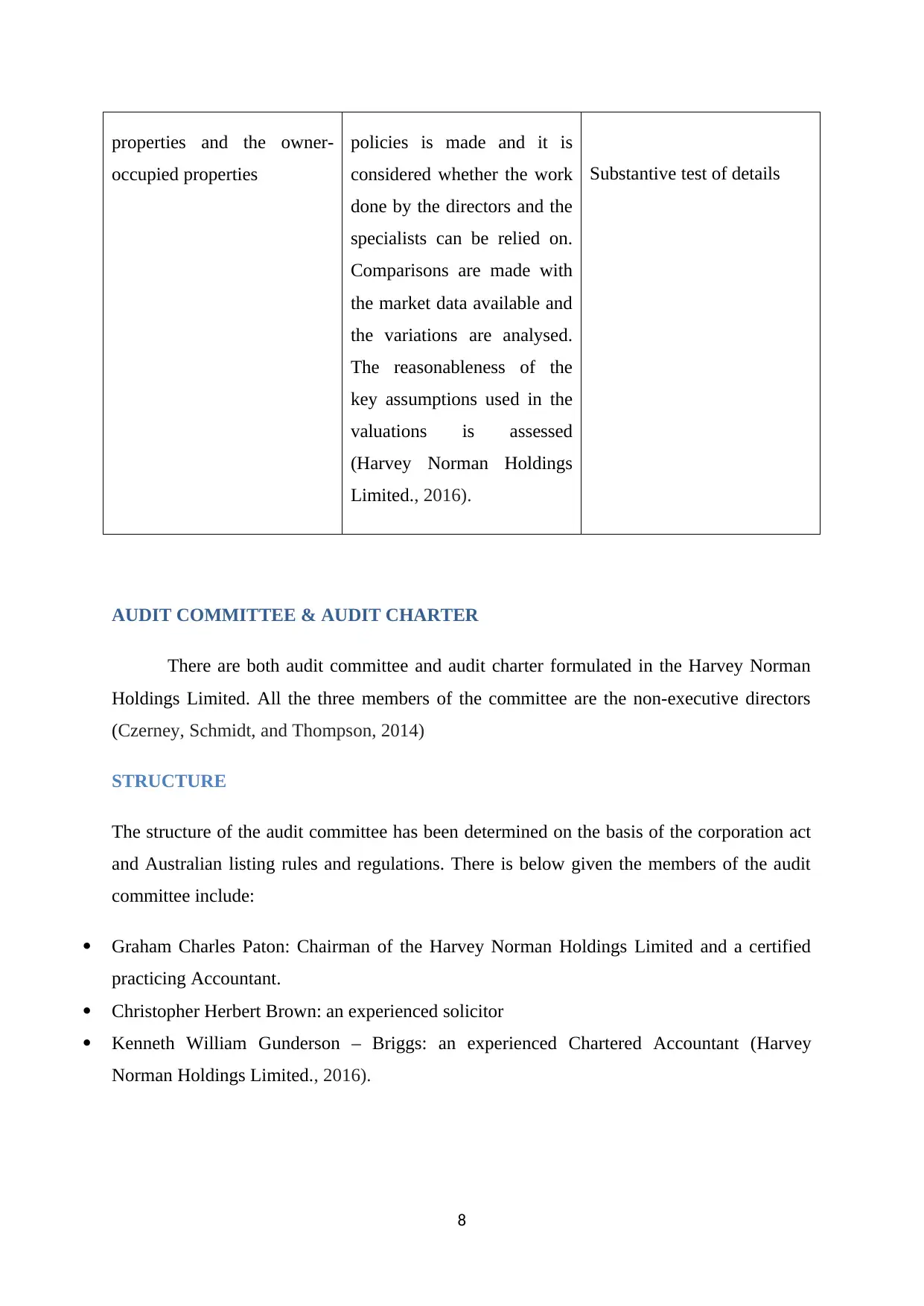

3. Valuation of investment Assessment of the valuation Analytical Procedures

7

consolidations are based.

Enquiries are made with the

directors and their external

lawyers with respect to the

interactions of the

franchisees and the groups.

Further, questions are also

raised for the changes

effected in the year in these

agreements. Meetings are

arranged with several sample

franchisees to gather the

knowledge regarding the

actual operation. The control

arrangements are also looked

after.

Observation

Substantive test of details

2. Recoverability of receivables

from franchisees

Evaluation of the process and

controls related to the

recoveries from franchisees

is made. Sample franchisee

loans are selected and

confirmation is made for the

pending balances. For the

sample franchisees the

controls are tested to get

confirmation regarding the

value of assets held as

security and their existence

(Mala, & Chand, 2015).

Test of Control: External

Confirmation & Enquiry

Substantive test of Details

3. Valuation of investment Assessment of the valuation Analytical Procedures

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

properties and the owner-

occupied properties

policies is made and it is

considered whether the work

done by the directors and the

specialists can be relied on.

Comparisons are made with

the market data available and

the variations are analysed.

The reasonableness of the

key assumptions used in the

valuations is assessed

(Harvey Norman Holdings

Limited., 2016).

Substantive test of details

AUDIT COMMITTEE & AUDIT CHARTER

There are both audit committee and audit charter formulated in the Harvey Norman

Holdings Limited. All the three members of the committee are the non-executive directors

(Czerney, Schmidt, and Thompson, 2014)

STRUCTURE

The structure of the audit committee has been determined on the basis of the corporation act

and Australian listing rules and regulations. There is below given the members of the audit

committee include:

Graham Charles Paton: Chairman of the Harvey Norman Holdings Limited and a certified

practicing Accountant.

Christopher Herbert Brown: an experienced solicitor

Kenneth William Gunderson – Briggs: an experienced Chartered Accountant (Harvey

Norman Holdings Limited., 2016).

8

occupied properties

policies is made and it is

considered whether the work

done by the directors and the

specialists can be relied on.

Comparisons are made with

the market data available and

the variations are analysed.

The reasonableness of the

key assumptions used in the

valuations is assessed

(Harvey Norman Holdings

Limited., 2016).

Substantive test of details

AUDIT COMMITTEE & AUDIT CHARTER

There are both audit committee and audit charter formulated in the Harvey Norman

Holdings Limited. All the three members of the committee are the non-executive directors

(Czerney, Schmidt, and Thompson, 2014)

STRUCTURE

The structure of the audit committee has been determined on the basis of the corporation act

and Australian listing rules and regulations. There is below given the members of the audit

committee include:

Graham Charles Paton: Chairman of the Harvey Norman Holdings Limited and a certified

practicing Accountant.

Christopher Herbert Brown: an experienced solicitor

Kenneth William Gunderson – Briggs: an experienced Chartered Accountant (Harvey

Norman Holdings Limited., 2016).

8

FUNCTIONS

Audit committee is bestowed with the function of oversight. This includes overseeing the

function relating to the appointment and review of the external auditor.

The other parties needed to be overseen include internal auditor and the management

(Badolato, Donelson, and Ege, 2014).

RESPONSIBILITIES

As far as the external auditors are concerned, the audit committee is bound to make decisions

regarding the selection, evaluation and replacement of the external auditor. It is the duty of

the committee to review the audit engagement letter and the audit plan. Determining the

nature of non-audit services and considering the communications that take place between the

management and the auditor also comes in the purview of this. Reviewing the independence

of the external auditor and his effectiveness (Beck, and Mauldin, 2014).

When the internal audit is concerned, it is the duty of the audit committee to make decisions

regarding the person who shall be considered as the head of the internal audit function. The

committee is expected to help the board in reviewing and approving the annual budget and

annual internal audit plan. The committee is responsible for assessing the effectiveness of the

function of internal audit and helping the board to assess the performance of the internal audit

head (Khelil, Hussainey, and Noubbigh, 2016).

Other responsibilities as relating to the review of risk assessment and management policies,

handling of accounting and related complaints, and those related to financial reporting

(Harvey Norman Holdings Limited., 2016).

AUDIT OPINION

The auditors have issued a clean and unmodified opinion on the financials of the

Harvey Norman Holdings Limited. In their opinion the financials of the Harvey Norman

Holdings Limited are prepared fairly and comply with the requirements of the Corporations

Act 2001, Australian Accounting Standards and, the Corporations Regulations 2001.

However, the audit report, auditors have given no disclaimer and passed non-qualified audit

report. It has stated that company has complied with the all the applicable rules and

regulations and maintained proper corporate governance program. This audit opinion is very

much required for the business sustainability and increased business outcomes in long run

(Jans, Alles, and Vasarhelyi, 2014).

9

Audit committee is bestowed with the function of oversight. This includes overseeing the

function relating to the appointment and review of the external auditor.

The other parties needed to be overseen include internal auditor and the management

(Badolato, Donelson, and Ege, 2014).

RESPONSIBILITIES

As far as the external auditors are concerned, the audit committee is bound to make decisions

regarding the selection, evaluation and replacement of the external auditor. It is the duty of

the committee to review the audit engagement letter and the audit plan. Determining the

nature of non-audit services and considering the communications that take place between the

management and the auditor also comes in the purview of this. Reviewing the independence

of the external auditor and his effectiveness (Beck, and Mauldin, 2014).

When the internal audit is concerned, it is the duty of the audit committee to make decisions

regarding the person who shall be considered as the head of the internal audit function. The

committee is expected to help the board in reviewing and approving the annual budget and

annual internal audit plan. The committee is responsible for assessing the effectiveness of the

function of internal audit and helping the board to assess the performance of the internal audit

head (Khelil, Hussainey, and Noubbigh, 2016).

Other responsibilities as relating to the review of risk assessment and management policies,

handling of accounting and related complaints, and those related to financial reporting

(Harvey Norman Holdings Limited., 2016).

AUDIT OPINION

The auditors have issued a clean and unmodified opinion on the financials of the

Harvey Norman Holdings Limited. In their opinion the financials of the Harvey Norman

Holdings Limited are prepared fairly and comply with the requirements of the Corporations

Act 2001, Australian Accounting Standards and, the Corporations Regulations 2001.

However, the audit report, auditors have given no disclaimer and passed non-qualified audit

report. It has stated that company has complied with the all the applicable rules and

regulations and maintained proper corporate governance program. This audit opinion is very

much required for the business sustainability and increased business outcomes in long run

(Jans, Alles, and Vasarhelyi, 2014).

9

DIFFERENCE BETWEEN THE RESPONSIBILITIES OF MANAGEMENT AND

AUDITOR

As far as the financial reporting is concerned, it is the duty of the management to

prepare the financial reports that comply with the requirements of the applicable accounting

standards, and corporation act 2001. It is the duty of the management to assess whether the

entity is able to continue operations as a going concern or not. Management is expected to

ensure that enough controls exist in the entity that provides for preparation of the financial

information free from any sort of misstatements (Hammer, 2015). The differences between

the auditor and management is very much needed to keep the business more transparent and

effective in long run (Eilifsen, Hamilton and Messier., 2017).

However, the auditors are responsible to behave professionally and provide a reasonable

assurance regarding the presentation of the financial information by the management. The

auditor is required to state whether the regulations are complied with or not. Further, the

auditors are required to assess the viability of the going concern assumption laid by the

management (Murphy, and Hogan, 2016). If auditors perform their responsibilities

effectively then it will not only strengthen their overall outcomes but also result to increased

business outcomes in determined approach. This helps in strengthen the overall outcomes and

business efficiency (Harvey Norman Holdings Limited., 2016).

MATERIAL SUBSEQUENT EVENTS

As per the declaration given by the directors in the annual report, there has been no

observation of any material subsequent events. In the opinion of the directors, there are no

transactions or events happening after the balance sheet date that can have or had a

significant effect on the Harvey Norman Holdings Limited’s operations, or the results of

company’s operations, or the state of affairs relating to the entity or the consolidated entity in

the future financial years. These are the subsequent events and material sections which

reflects how well company has been performing its business. Harvey Normal needs to

increase the transparency of its business by complying with the international and domestic

reporting compliance program (Harvey Norman Holdings Limited., 2016).

10

AUDITOR

As far as the financial reporting is concerned, it is the duty of the management to

prepare the financial reports that comply with the requirements of the applicable accounting

standards, and corporation act 2001. It is the duty of the management to assess whether the

entity is able to continue operations as a going concern or not. Management is expected to

ensure that enough controls exist in the entity that provides for preparation of the financial

information free from any sort of misstatements (Hammer, 2015). The differences between

the auditor and management is very much needed to keep the business more transparent and

effective in long run (Eilifsen, Hamilton and Messier., 2017).

However, the auditors are responsible to behave professionally and provide a reasonable

assurance regarding the presentation of the financial information by the management. The

auditor is required to state whether the regulations are complied with or not. Further, the

auditors are required to assess the viability of the going concern assumption laid by the

management (Murphy, and Hogan, 2016). If auditors perform their responsibilities

effectively then it will not only strengthen their overall outcomes but also result to increased

business outcomes in determined approach. This helps in strengthen the overall outcomes and

business efficiency (Harvey Norman Holdings Limited., 2016).

MATERIAL SUBSEQUENT EVENTS

As per the declaration given by the directors in the annual report, there has been no

observation of any material subsequent events. In the opinion of the directors, there are no

transactions or events happening after the balance sheet date that can have or had a

significant effect on the Harvey Norman Holdings Limited’s operations, or the results of

company’s operations, or the state of affairs relating to the entity or the consolidated entity in

the future financial years. These are the subsequent events and material sections which

reflects how well company has been performing its business. Harvey Normal needs to

increase the transparency of its business by complying with the international and domestic

reporting compliance program (Harvey Norman Holdings Limited., 2016).

10

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

CONCLUSION

When the assessment of the audit report issued by the external auditor is made from

the view of a third party stakeholder, the material information reported by the auditor seems

perfectly fine. The auditors have clearly mentions the key areas which as per their judgement

are of the highest significance for the stakeholders. These areas are explained as well as the

audit procedures followed to reduce the risk persistent in them is mentioned in the report. The

presentation seems highly effective. From the reading and understanding of the report, it can

be easily concluded that there is no material information that has been missed by the auditor.

The report is presented in a manner that is able to fully explain and disclose the required

information to the users. There seems no doubt regarding the professionalism with which the

reports are prepared and hence the need to ask any follow up questions is also ruled out. The

main crux of this report is that auditors are the key person who performs the fiduciary

position in the best interest of the stakeholders. The transparency and true and fair view of the

assets and liabilities of company depends upon the audit program and activities undertaken

by the auditors.

11

When the assessment of the audit report issued by the external auditor is made from

the view of a third party stakeholder, the material information reported by the auditor seems

perfectly fine. The auditors have clearly mentions the key areas which as per their judgement

are of the highest significance for the stakeholders. These areas are explained as well as the

audit procedures followed to reduce the risk persistent in them is mentioned in the report. The

presentation seems highly effective. From the reading and understanding of the report, it can

be easily concluded that there is no material information that has been missed by the auditor.

The report is presented in a manner that is able to fully explain and disclose the required

information to the users. There seems no doubt regarding the professionalism with which the

reports are prepared and hence the need to ask any follow up questions is also ruled out. The

main crux of this report is that auditors are the key person who performs the fiduciary

position in the best interest of the stakeholders. The transparency and true and fair view of the

assets and liabilities of company depends upon the audit program and activities undertaken

by the auditors.

11

REFERENCES

Badolato, P.G., Donelson, D.C. and Ege, M., (2014). Audit committee financial expertise and

earnings management: The role of status. Journal of Accounting and Economics, 58(2-3),

pp.208-230.

Beck, M.J. and Mauldin, E.G., (2014). Who's really in charge? Audit committee versus CFO

power and audit fees. The Accounting Review, 89(6), pp.2057-2085.

Bell, T.B., Causholli, M. and Knechel, W.R., (2015). Audit firm tenure, non‐audit services,

and internal assessments of audit quality. Journal of Accounting Research, 53(3), pp.461-509.

Choong, K.K. and Leung, W.Y., (2015). Auditor remuneration, corporate governance and

auditor independence, 2nd ed, Hong Kong, Pearson.

Czerney, K., Schmidt, J. J., and Thompson, A. M. (2014). Does auditor explanatory language

in unqualified audit reports indicate increased financial misstatement risk?. The Accounting

Review, 89(6), 2115-2149.

Eilifsen, A., Hamilton, E. L., and Messier Jr, W. F. (2017). The Importance of Quantifying

Uncertainty: Examining the Effect of Audit Materiality and Sensitivity Analysis Disclosures

on Investors’ Judgments and Decisions. 8(6), 215-219

Hammer, M., (2015). What is business process management?. In Handbook on business

process managemen, 3rd ed, Springer,Berlin : Heidelberg.

Harvey Norman Holdings Limited., (2016). Annual report. Available at

http www harveynormanholdings com au reports announcements:// . . . / - -1/., Accessed on 12th June

2018

Jans, M., Alles, M. G., and Vasarhelyi, M. A. (2014). A field study on the use of process

mining of event logs as an analytical procedure in auditing. The Accounting Review, 89(5),

1751-1773.

Khelil, I., Hussainey, K. and Noubbigh, H., (2016). Audit committee–internal audit

interaction and moral courage. Managerial Auditing Journal, 31(4/5), pp.403-433.

12

Badolato, P.G., Donelson, D.C. and Ege, M., (2014). Audit committee financial expertise and

earnings management: The role of status. Journal of Accounting and Economics, 58(2-3),

pp.208-230.

Beck, M.J. and Mauldin, E.G., (2014). Who's really in charge? Audit committee versus CFO

power and audit fees. The Accounting Review, 89(6), pp.2057-2085.

Bell, T.B., Causholli, M. and Knechel, W.R., (2015). Audit firm tenure, non‐audit services,

and internal assessments of audit quality. Journal of Accounting Research, 53(3), pp.461-509.

Choong, K.K. and Leung, W.Y., (2015). Auditor remuneration, corporate governance and

auditor independence, 2nd ed, Hong Kong, Pearson.

Czerney, K., Schmidt, J. J., and Thompson, A. M. (2014). Does auditor explanatory language

in unqualified audit reports indicate increased financial misstatement risk?. The Accounting

Review, 89(6), 2115-2149.

Eilifsen, A., Hamilton, E. L., and Messier Jr, W. F. (2017). The Importance of Quantifying

Uncertainty: Examining the Effect of Audit Materiality and Sensitivity Analysis Disclosures

on Investors’ Judgments and Decisions. 8(6), 215-219

Hammer, M., (2015). What is business process management?. In Handbook on business

process managemen, 3rd ed, Springer,Berlin : Heidelberg.

Harvey Norman Holdings Limited., (2016). Annual report. Available at

http www harveynormanholdings com au reports announcements:// . . . / - -1/., Accessed on 12th June

2018

Jans, M., Alles, M. G., and Vasarhelyi, M. A. (2014). A field study on the use of process

mining of event logs as an analytical procedure in auditing. The Accounting Review, 89(5),

1751-1773.

Khelil, I., Hussainey, K. and Noubbigh, H., (2016). Audit committee–internal audit

interaction and moral courage. Managerial Auditing Journal, 31(4/5), pp.403-433.

12

Louwers, T. J., Ramsay, R. J., Sinason, D. H., Strawser, J. R., and Thibodeau, J. C.

(2015). Auditing & assurance services. 3rd ed, USA: McGraw-Hill Education.

Mala, R., & Chand, P. (2015). Judgment and Decision‐Making Research in Auditing and

Accounting: Future Research Implications of Person, Task, and Environment

Perspective. Accounting Perspectives, 14(1), 1-50.

Murphy, L. and Hogan, R., (2016). Financial Reporting of Nonfinancial Information: The

Role of the Auditor. Journal of Corporate Accounting & Finance, 28(1), pp.42-49.

Sirois, L.P., Bédard, J. and Bera, P., (2018). The informational value of key audit matters in

the auditor's report: evidence from an Eye-tracking study. 2nd ed, Austdralia: Accounting

Horizons.

Tepalagul, N. and Lin, L., (2015). Auditor independence and audit quality: A literature

review. Journal of Accounting, Auditing & Finance, 30(1), pp.101-121.

13

(2015). Auditing & assurance services. 3rd ed, USA: McGraw-Hill Education.

Mala, R., & Chand, P. (2015). Judgment and Decision‐Making Research in Auditing and

Accounting: Future Research Implications of Person, Task, and Environment

Perspective. Accounting Perspectives, 14(1), 1-50.

Murphy, L. and Hogan, R., (2016). Financial Reporting of Nonfinancial Information: The

Role of the Auditor. Journal of Corporate Accounting & Finance, 28(1), pp.42-49.

Sirois, L.P., Bédard, J. and Bera, P., (2018). The informational value of key audit matters in

the auditor's report: evidence from an Eye-tracking study. 2nd ed, Austdralia: Accounting

Horizons.

Tepalagul, N. and Lin, L., (2015). Auditor independence and audit quality: A literature

review. Journal of Accounting, Auditing & Finance, 30(1), pp.101-121.

13

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.