FBL5030 - Value Creation in Business: A Case Study of Harvey Norman

VerifiedAdded on 2023/06/13

|28

|7785

|167

Report

AI Summary

This report presents a comprehensive financial analysis of Harvey Norman (HVN), focusing on value creation over five fiscal years. It examines the company's income statement, balance sheet, and cash flow statement, utilizing financial ratios to assess performance. The income statement analysis reveals trends in operating expenses and retained earnings, highlighting periods of growth and decline. The balance sheet analysis focuses on changes in property, plant, and equipment, as well as long-term liabilities, to evaluate asset accumulation and debt management. The cash flow statement analysis assesses the company's cash position and its ability to meet short-term obligations. Overall, the report aims to provide insights into Harvey Norman's financial health and its strategies for creating value. Desklib provides access to similar reports and study tools for students.

Running head: FUNDAMENTALS OF VALUE CREATION IN BUSINESSES

Fundamentals of Value Creation in Businesses

Name of the Student:

Name of the University:

Authors Note:

Fundamentals of Value Creation in Businesses

Name of the Student:

Name of the University:

Authors Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FUNDAMENTALS OF VALUE CREATION IN BUSINESSES

1

Table of Contents

3. Presenting the Analysis of the Company:..............................................................................2

3.3 Introduction:.........................................................................................................................2

3.4 Income statement analysis:..................................................................................................2

3.5 Balance sheet analysis:.........................................................................................................5

3.6 Cash flow statement analysis:..............................................................................................8

3.7 Profitability analysis:.........................................................................................................11

3.8 Liquidity analysis:..............................................................................................................14

3.9 Solvency analysis:..............................................................................................................17

3.10 Conclusion:......................................................................................................................20

Reference and Bibliography:....................................................................................................22

Appendices:..............................................................................................................................26

1

Table of Contents

3. Presenting the Analysis of the Company:..............................................................................2

3.3 Introduction:.........................................................................................................................2

3.4 Income statement analysis:..................................................................................................2

3.5 Balance sheet analysis:.........................................................................................................5

3.6 Cash flow statement analysis:..............................................................................................8

3.7 Profitability analysis:.........................................................................................................11

3.8 Liquidity analysis:..............................................................................................................14

3.9 Solvency analysis:..............................................................................................................17

3.10 Conclusion:......................................................................................................................20

Reference and Bibliography:....................................................................................................22

Appendices:..............................................................................................................................26

FUNDAMENTALS OF VALUE CREATION IN BUSINESSES

2

3. Presenting the Analysis of the Company:

3.3 Introduction:

The overall assessment is mainly conducted on Harvey Norman (HVN) organisation,

where its financial performance is evaluated by analysing different financial ratios, income

statement, balance sheet statement and cash flow statement. In addition, the financial

performance is mainly conducted to understand the progress and financial trend of Harvey

Norman for previous five financial year. The company mainly falls under Consumer

discretionary sector, where its financial performance could help in understanding its current

financial condition. Moreover, the income statement analysis is conducted to understand the

changes in retained earnings and operating expenses of the company. The evaluation of

balance sheet mainly helps in depicting the Growth of property, plant, and equipment, while

detecting the growth of long term liabilities. The cash flow statement analysis also helps in

understanding the Cash at the year end, and Net financing cash flows of the company over

the period.

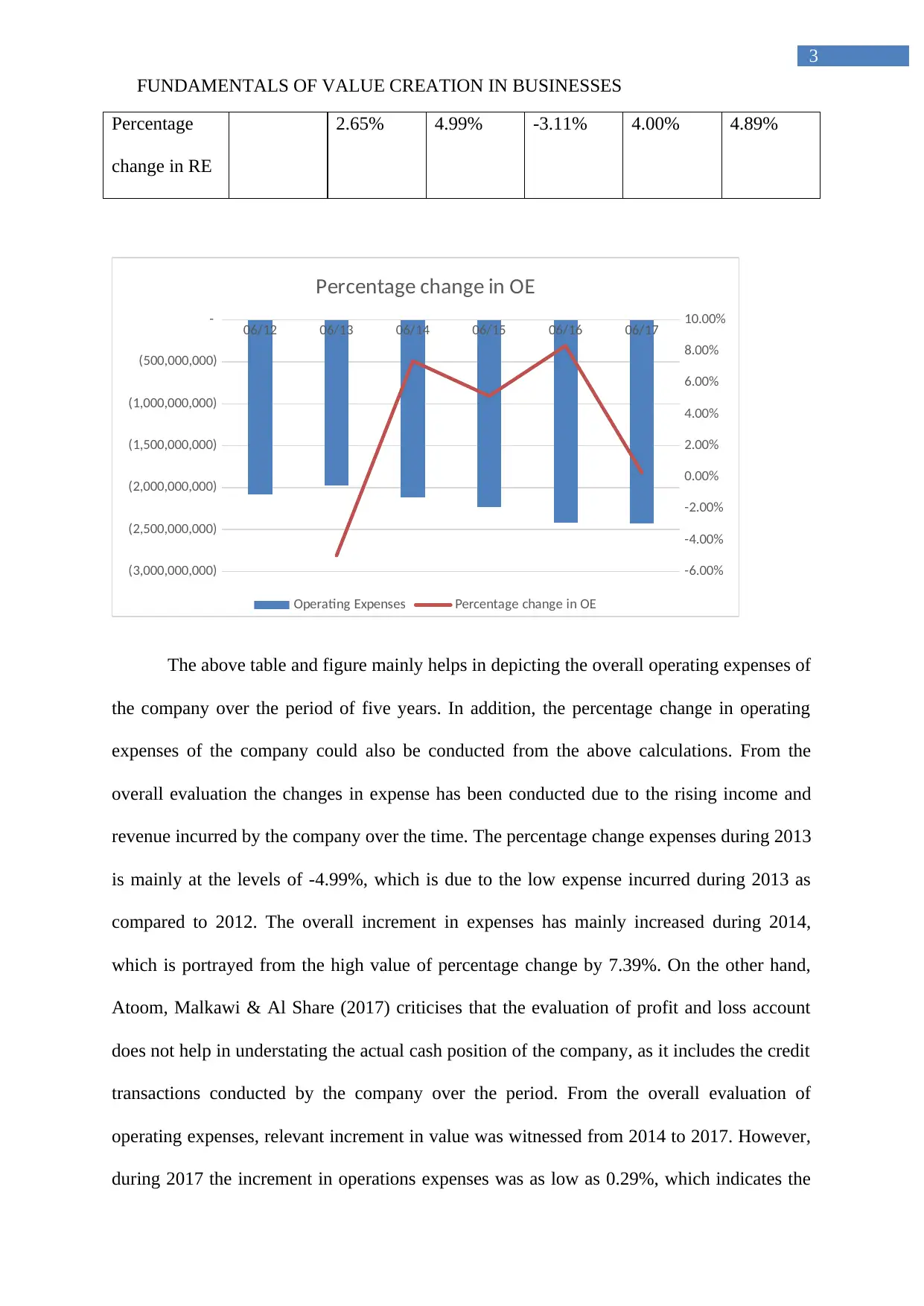

3.4 Income statement analysis:

Particulars 06/12 06/13 06/14 06/15 06/16 06/17

Operating

Expenses

(2,078,166

,000)

(1,974,394

,000)

(2,120,288

,000)

(2,229,745

,000)

(2,416,109

,000)

(2,423,093

,000)

Percentage

change in OE

-4.99% 7.39% 5.16% 8.36% 0.29%

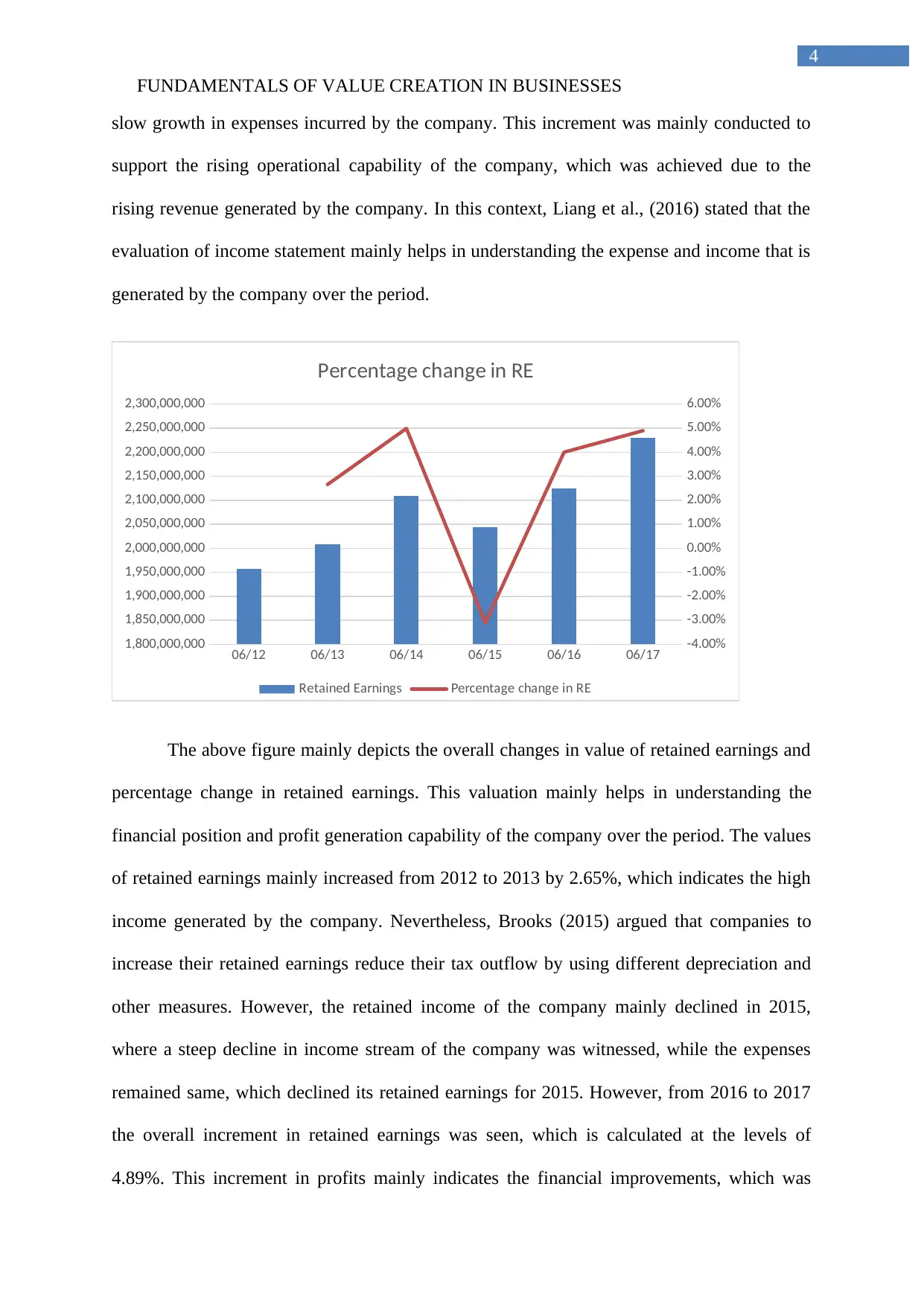

Retained

Earnings

1,956,966,

000

2,008,880,

000

2,109,032,

000

2,043,463,

000

2,125,186,

000

2,229,200,

000

2

3. Presenting the Analysis of the Company:

3.3 Introduction:

The overall assessment is mainly conducted on Harvey Norman (HVN) organisation,

where its financial performance is evaluated by analysing different financial ratios, income

statement, balance sheet statement and cash flow statement. In addition, the financial

performance is mainly conducted to understand the progress and financial trend of Harvey

Norman for previous five financial year. The company mainly falls under Consumer

discretionary sector, where its financial performance could help in understanding its current

financial condition. Moreover, the income statement analysis is conducted to understand the

changes in retained earnings and operating expenses of the company. The evaluation of

balance sheet mainly helps in depicting the Growth of property, plant, and equipment, while

detecting the growth of long term liabilities. The cash flow statement analysis also helps in

understanding the Cash at the year end, and Net financing cash flows of the company over

the period.

3.4 Income statement analysis:

Particulars 06/12 06/13 06/14 06/15 06/16 06/17

Operating

Expenses

(2,078,166

,000)

(1,974,394

,000)

(2,120,288

,000)

(2,229,745

,000)

(2,416,109

,000)

(2,423,093

,000)

Percentage

change in OE

-4.99% 7.39% 5.16% 8.36% 0.29%

Retained

Earnings

1,956,966,

000

2,008,880,

000

2,109,032,

000

2,043,463,

000

2,125,186,

000

2,229,200,

000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

FUNDAMENTALS OF VALUE CREATION IN BUSINESSES

3

Percentage

change in RE

2.65% 4.99% -3.11% 4.00% 4.89%

06/12 06/13 06/14 06/15 06/16 06/17

(3,000,000,000)

(2,500,000,000)

(2,000,000,000)

(1,500,000,000)

(1,000,000,000)

(500,000,000)

-

-6.00%

-4.00%

-2.00%

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

Percentage change in OE

Operating Expenses Percentage change in OE

The above table and figure mainly helps in depicting the overall operating expenses of

the company over the period of five years. In addition, the percentage change in operating

expenses of the company could also be conducted from the above calculations. From the

overall evaluation the changes in expense has been conducted due to the rising income and

revenue incurred by the company over the time. The percentage change expenses during 2013

is mainly at the levels of -4.99%, which is due to the low expense incurred during 2013 as

compared to 2012. The overall increment in expenses has mainly increased during 2014,

which is portrayed from the high value of percentage change by 7.39%. On the other hand,

Atoom, Malkawi & Al Share (2017) criticises that the evaluation of profit and loss account

does not help in understating the actual cash position of the company, as it includes the credit

transactions conducted by the company over the period. From the overall evaluation of

operating expenses, relevant increment in value was witnessed from 2014 to 2017. However,

during 2017 the increment in operations expenses was as low as 0.29%, which indicates the

3

Percentage

change in RE

2.65% 4.99% -3.11% 4.00% 4.89%

06/12 06/13 06/14 06/15 06/16 06/17

(3,000,000,000)

(2,500,000,000)

(2,000,000,000)

(1,500,000,000)

(1,000,000,000)

(500,000,000)

-

-6.00%

-4.00%

-2.00%

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

Percentage change in OE

Operating Expenses Percentage change in OE

The above table and figure mainly helps in depicting the overall operating expenses of

the company over the period of five years. In addition, the percentage change in operating

expenses of the company could also be conducted from the above calculations. From the

overall evaluation the changes in expense has been conducted due to the rising income and

revenue incurred by the company over the time. The percentage change expenses during 2013

is mainly at the levels of -4.99%, which is due to the low expense incurred during 2013 as

compared to 2012. The overall increment in expenses has mainly increased during 2014,

which is portrayed from the high value of percentage change by 7.39%. On the other hand,

Atoom, Malkawi & Al Share (2017) criticises that the evaluation of profit and loss account

does not help in understating the actual cash position of the company, as it includes the credit

transactions conducted by the company over the period. From the overall evaluation of

operating expenses, relevant increment in value was witnessed from 2014 to 2017. However,

during 2017 the increment in operations expenses was as low as 0.29%, which indicates the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FUNDAMENTALS OF VALUE CREATION IN BUSINESSES

4

slow growth in expenses incurred by the company. This increment was mainly conducted to

support the rising operational capability of the company, which was achieved due to the

rising revenue generated by the company. In this context, Liang et al., (2016) stated that the

evaluation of income statement mainly helps in understanding the expense and income that is

generated by the company over the period.

06/12 06/13 06/14 06/15 06/16 06/17

1,800,000,000

1,850,000,000

1,900,000,000

1,950,000,000

2,000,000,000

2,050,000,000

2,100,000,000

2,150,000,000

2,200,000,000

2,250,000,000

2,300,000,000

-4.00%

-3.00%

-2.00%

-1.00%

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

Percentage change in RE

Retained Earnings Percentage change in RE

The above figure mainly depicts the overall changes in value of retained earnings and

percentage change in retained earnings. This valuation mainly helps in understanding the

financial position and profit generation capability of the company over the period. The values

of retained earnings mainly increased from 2012 to 2013 by 2.65%, which indicates the high

income generated by the company. Nevertheless, Brooks (2015) argued that companies to

increase their retained earnings reduce their tax outflow by using different depreciation and

other measures. However, the retained income of the company mainly declined in 2015,

where a steep decline in income stream of the company was witnessed, while the expenses

remained same, which declined its retained earnings for 2015. However, from 2016 to 2017

the overall increment in retained earnings was seen, which is calculated at the levels of

4.89%. This increment in profits mainly indicates the financial improvements, which was

4

slow growth in expenses incurred by the company. This increment was mainly conducted to

support the rising operational capability of the company, which was achieved due to the

rising revenue generated by the company. In this context, Liang et al., (2016) stated that the

evaluation of income statement mainly helps in understanding the expense and income that is

generated by the company over the period.

06/12 06/13 06/14 06/15 06/16 06/17

1,800,000,000

1,850,000,000

1,900,000,000

1,950,000,000

2,000,000,000

2,050,000,000

2,100,000,000

2,150,000,000

2,200,000,000

2,250,000,000

2,300,000,000

-4.00%

-3.00%

-2.00%

-1.00%

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

Percentage change in RE

Retained Earnings Percentage change in RE

The above figure mainly depicts the overall changes in value of retained earnings and

percentage change in retained earnings. This valuation mainly helps in understanding the

financial position and profit generation capability of the company over the period. The values

of retained earnings mainly increased from 2012 to 2013 by 2.65%, which indicates the high

income generated by the company. Nevertheless, Brooks (2015) argued that companies to

increase their retained earnings reduce their tax outflow by using different depreciation and

other measures. However, the retained income of the company mainly declined in 2015,

where a steep decline in income stream of the company was witnessed, while the expenses

remained same, which declined its retained earnings for 2015. However, from 2016 to 2017

the overall increment in retained earnings was seen, which is calculated at the levels of

4.89%. This increment in profits mainly indicates the financial improvements, which was

FUNDAMENTALS OF VALUE CREATION IN BUSINESSES

5

obtained by Harvey Norman in 2017, as compared to other years. Ronapat (2018) stated that

with the evaluation of retained earnings investors can identify the current financial position of

the company, which could be used in the expansion process of the organisation.

The analysis of retained earnings and operational expenses of Harvey Norman mainly

helps in identifying and improving financial position of the company over time. Moreover,

revenue of the organisation has relevantly increased exponentially against the rising operating

expenses, while raising the level of retained earnings of the company. Therefore, it could be

understood that income status of the organisation has relevantly increased over time, due to

the accumulation of high revenues and low expenses incurred from operations. According to

Kanapickiene & Grundiene (2015), the analysis of income statement mainly helps investors

in gauging into the expenses and income that is been conducted by the company over the

fiscal year.

3.5 Balance sheet analysis:

Particulars 06/12 06/13 06/14 06/15 06/16 06/17

NCA - PP&E 536,277,

000

548,903,

000

569,057,

000

552,603,

000

580,805,

000

625,112,

000

Percentage change in

PP&E

2.35% 3.67% -2.89% 5.10% 7.63%

Total NCL 767,164,

000

867,119,

000

471,998,

000

518,605,

000

464,114,

000

633,412,

000

Percentage change in

Long term liabilities

13.03% -45.57% 9.87% -10.51% 36.48%

5

obtained by Harvey Norman in 2017, as compared to other years. Ronapat (2018) stated that

with the evaluation of retained earnings investors can identify the current financial position of

the company, which could be used in the expansion process of the organisation.

The analysis of retained earnings and operational expenses of Harvey Norman mainly

helps in identifying and improving financial position of the company over time. Moreover,

revenue of the organisation has relevantly increased exponentially against the rising operating

expenses, while raising the level of retained earnings of the company. Therefore, it could be

understood that income status of the organisation has relevantly increased over time, due to

the accumulation of high revenues and low expenses incurred from operations. According to

Kanapickiene & Grundiene (2015), the analysis of income statement mainly helps investors

in gauging into the expenses and income that is been conducted by the company over the

fiscal year.

3.5 Balance sheet analysis:

Particulars 06/12 06/13 06/14 06/15 06/16 06/17

NCA - PP&E 536,277,

000

548,903,

000

569,057,

000

552,603,

000

580,805,

000

625,112,

000

Percentage change in

PP&E

2.35% 3.67% -2.89% 5.10% 7.63%

Total NCL 767,164,

000

867,119,

000

471,998,

000

518,605,

000

464,114,

000

633,412,

000

Percentage change in

Long term liabilities

13.03% -45.57% 9.87% -10.51% 36.48%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

FUNDAMENTALS OF VALUE CREATION IN BUSINESSES

6

06/12 06/13 06/14 06/15 06/16 06/17

480,000,000

500,000,000

520,000,000

540,000,000

560,000,000

580,000,000

600,000,000

620,000,000

640,000,000

-4.00%

-2.00%

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

Percentage change in PP&E

NCA - PP&E Percentage change in PP&E

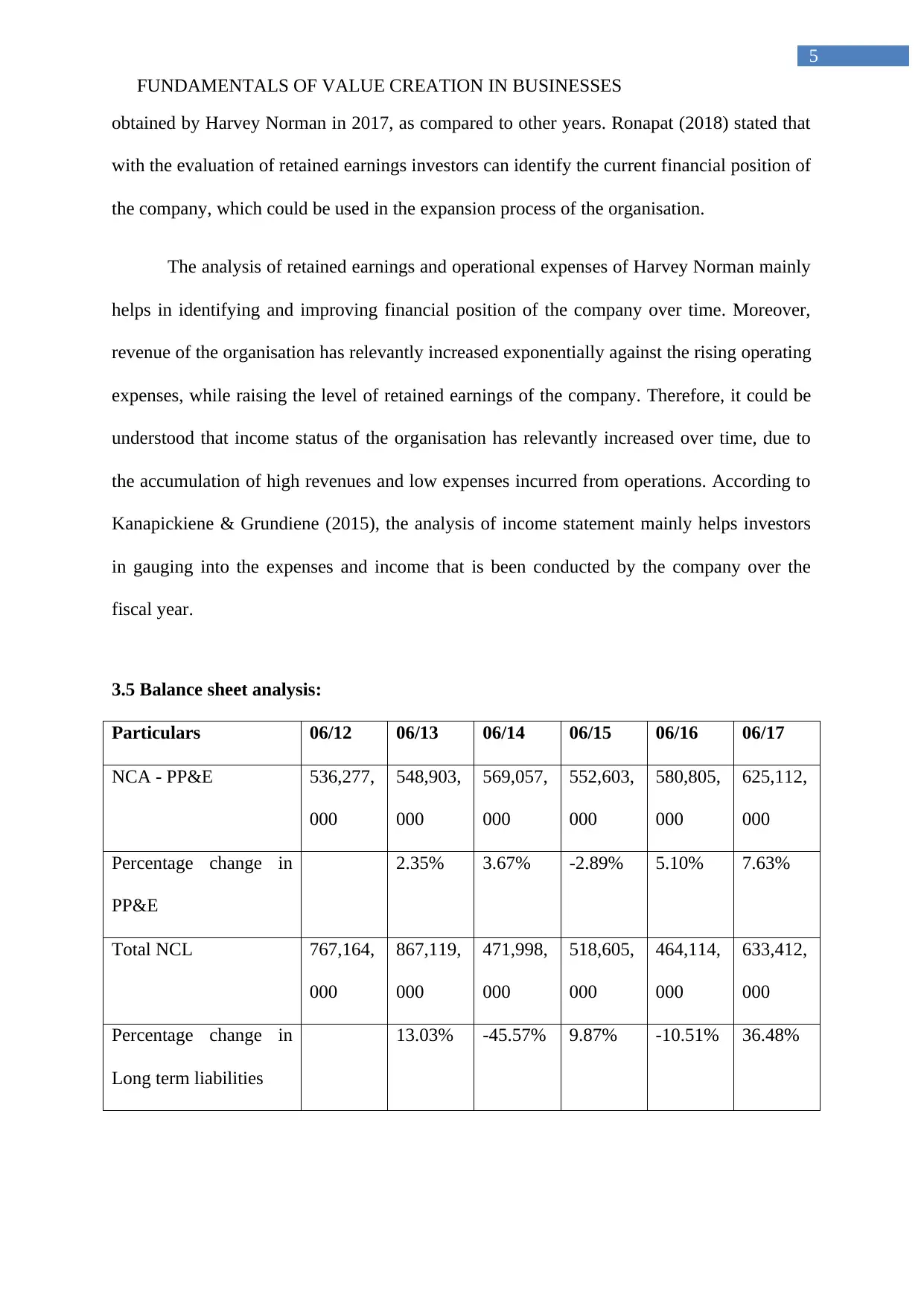

The change in Growth of property, plant and equipment is mainly evaluated with the

help of above figure and tables. The increment in overall valuation of property, plant and

equipment mainly helps in depicting the financial position of the company over time. In

addition, the changes in percentage of property, plant, and equipment from 2012 to 2017 is

relevantly positive, which indicates the accumulation of adequate assets conducted by Harvey

Norman. Furthermore, the financial position, and expenses incurred by the company on

property, plant and equipment can be seen from the above calculations. The values of net

increment in property, plant, and equipment can be seen from the above figure, which has

relevantly increased from 2012 to 2014, while decline in its value can be seen during 2015.

This decline is mainly conducted, due to the reduction in dur to the low accumulation of

revenue and cash conducted during 2015 to support the purchase of assets. Moreover, the

percentage change in property, plant, and equipment during 2015 was mainly at the levels of

-2.89%, which eventually depicts the low expenses incurred in asset accumulation. Buchman,

Harris & Liu (2016) mentioned that with the use of fixed assets analysis the investors

evaluate the operational capability of the company.

6

06/12 06/13 06/14 06/15 06/16 06/17

480,000,000

500,000,000

520,000,000

540,000,000

560,000,000

580,000,000

600,000,000

620,000,000

640,000,000

-4.00%

-2.00%

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

Percentage change in PP&E

NCA - PP&E Percentage change in PP&E

The change in Growth of property, plant and equipment is mainly evaluated with the

help of above figure and tables. The increment in overall valuation of property, plant and

equipment mainly helps in depicting the financial position of the company over time. In

addition, the changes in percentage of property, plant, and equipment from 2012 to 2017 is

relevantly positive, which indicates the accumulation of adequate assets conducted by Harvey

Norman. Furthermore, the financial position, and expenses incurred by the company on

property, plant and equipment can be seen from the above calculations. The values of net

increment in property, plant, and equipment can be seen from the above figure, which has

relevantly increased from 2012 to 2014, while decline in its value can be seen during 2015.

This decline is mainly conducted, due to the reduction in dur to the low accumulation of

revenue and cash conducted during 2015 to support the purchase of assets. Moreover, the

percentage change in property, plant, and equipment during 2015 was mainly at the levels of

-2.89%, which eventually depicts the low expenses incurred in asset accumulation. Buchman,

Harris & Liu (2016) mentioned that with the use of fixed assets analysis the investors

evaluate the operational capability of the company.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FUNDAMENTALS OF VALUE CREATION IN BUSINESSES

7

Moreover, increment in property, plant, and equipment accumulation during 2016 was

at the levels of 5.10%, while during 2017 the value increased to 7.63%. This relevantly

indicates the accumulation of high end fixed assets, which was used in improving the level of

operations of the company. This increment in in property, plant and equipment mainly

supported the overall financial capability and revenue generation capacity of the organisation.

On the contrary, Paul & Mitra (2017) criticises that the increment in fixed asset accumulation

might reduce the cash availability and working capital capability of the company to continue

its operations smoothly.

06/12 06/13 06/14 06/15 06/16 06/17

0

100,000,000

200,000,000

300,000,000

400,000,000

500,000,000

600,000,000

700,000,000

800,000,000

900,000,000

1,000,000,000

-50.00%

-40.00%

-30.00%

-20.00%

-10.00%

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

Percentage change in Long term liabilities

Total NCL Percentage change in Long term liabilities

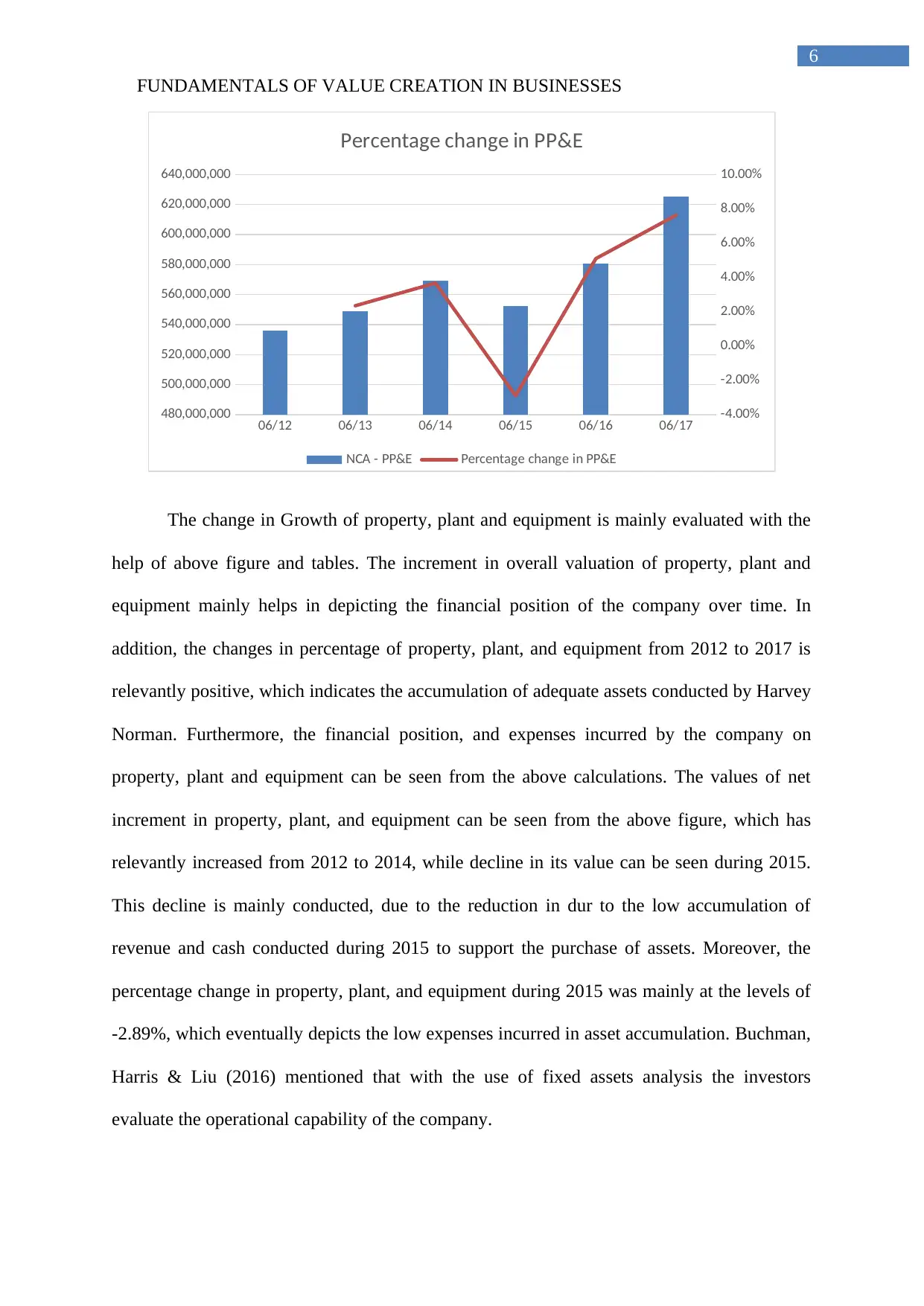

The overall figure helps in understanding the change in long term liabilities of the

company over the period of 5 years, which has changed exponentially over time. In addition,

the changes in percentage of long term liabilities is mainly identified from the non-current

liabilities of Harvey Norman. Moreover, the long-term liabilities accumulated by the

company can be identified from the above figure, which has declined from 2012 to 2017.

Moreover, the financial performance of company mainly improved due to the low

accumulation of debt conducted for supporting its operations. The long-term liabilities mainly

declined in 2014, where the change in long term debt was at the levels of -45.57%. Carlino et

7

Moreover, increment in property, plant, and equipment accumulation during 2016 was

at the levels of 5.10%, while during 2017 the value increased to 7.63%. This relevantly

indicates the accumulation of high end fixed assets, which was used in improving the level of

operations of the company. This increment in in property, plant and equipment mainly

supported the overall financial capability and revenue generation capacity of the organisation.

On the contrary, Paul & Mitra (2017) criticises that the increment in fixed asset accumulation

might reduce the cash availability and working capital capability of the company to continue

its operations smoothly.

06/12 06/13 06/14 06/15 06/16 06/17

0

100,000,000

200,000,000

300,000,000

400,000,000

500,000,000

600,000,000

700,000,000

800,000,000

900,000,000

1,000,000,000

-50.00%

-40.00%

-30.00%

-20.00%

-10.00%

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

Percentage change in Long term liabilities

Total NCL Percentage change in Long term liabilities

The overall figure helps in understanding the change in long term liabilities of the

company over the period of 5 years, which has changed exponentially over time. In addition,

the changes in percentage of long term liabilities is mainly identified from the non-current

liabilities of Harvey Norman. Moreover, the long-term liabilities accumulated by the

company can be identified from the above figure, which has declined from 2012 to 2017.

Moreover, the financial performance of company mainly improved due to the low

accumulation of debt conducted for supporting its operations. The long-term liabilities mainly

declined in 2014, where the change in long term debt was at the levels of -45.57%. Carlino et

FUNDAMENTALS OF VALUE CREATION IN BUSINESSES

8

al., (2017) mentioned that with the evaluation of non-current liabilities the current debt

position of the company can be identified, which could help in understanding solvency

condition of the company. This relevantly indicates that the company disposed maximum of

the liabilities during the financial year, which declined the net income and cash position. The

increment in long term liabilities of the company increased in 2015, where a sudden decline

was seen in 2016, as the long-term debt declined by -10.51%. This decline in overall long-

term debt mainly helps in understanding the financial improvements, which is achieved by

the company during the five financial years. On the other hand, during 2017 the increment in

long term liabilities can be seen at the levels of 36.548%, which was conducted to support the

operational needs of the organisation. On the other hand, Lakshmi, Martin & Venkatesan

(2016) argued that accumulation of high end non-current liabilities by the organisation could

increase the level of interest payments, which might hamper the level of profits that is

generated from operations.

3.6 Cash flow statement analysis:

Particulars 06/12 06/13 06/14 06/15 06/16 06/17

Cash at End of Period 140,093,

000

124,567,

000

115,172,

000

153,220,

000

103,631,

000

42,882,0

00

Percentage change in

Cash at end of period

-11.08% -7.54% 33.04% -32.36% -58.62%

Net Financing

Cashflows

-

8,509,00

0

-

46,562,0

00

-

235,213,

000

-

220,597,

000

-

307,427,

000

-

287,124,

000

Percentage change in

net financing cash

447.21% 405.16% -6.21% 39.36% -6.60%

8

al., (2017) mentioned that with the evaluation of non-current liabilities the current debt

position of the company can be identified, which could help in understanding solvency

condition of the company. This relevantly indicates that the company disposed maximum of

the liabilities during the financial year, which declined the net income and cash position. The

increment in long term liabilities of the company increased in 2015, where a sudden decline

was seen in 2016, as the long-term debt declined by -10.51%. This decline in overall long-

term debt mainly helps in understanding the financial improvements, which is achieved by

the company during the five financial years. On the other hand, during 2017 the increment in

long term liabilities can be seen at the levels of 36.548%, which was conducted to support the

operational needs of the organisation. On the other hand, Lakshmi, Martin & Venkatesan

(2016) argued that accumulation of high end non-current liabilities by the organisation could

increase the level of interest payments, which might hamper the level of profits that is

generated from operations.

3.6 Cash flow statement analysis:

Particulars 06/12 06/13 06/14 06/15 06/16 06/17

Cash at End of Period 140,093,

000

124,567,

000

115,172,

000

153,220,

000

103,631,

000

42,882,0

00

Percentage change in

Cash at end of period

-11.08% -7.54% 33.04% -32.36% -58.62%

Net Financing

Cashflows

-

8,509,00

0

-

46,562,0

00

-

235,213,

000

-

220,597,

000

-

307,427,

000

-

287,124,

000

Percentage change in

net financing cash

447.21% 405.16% -6.21% 39.36% -6.60%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

FUNDAMENTALS OF VALUE CREATION IN BUSINESSES

9

flows

06/12 06/13 06/14 06/15 06/16 06/17

0

20,000,000

40,000,000

60,000,000

80,000,000

100,000,000

120,000,000

140,000,000

160,000,000

180,000,000

-80.00%

-60.00%

-40.00%

-20.00%

0.00%

20.00%

40.00%

Percentage change in Cash at end of period

Cash at End of Period Percentage change in Cash at end of period

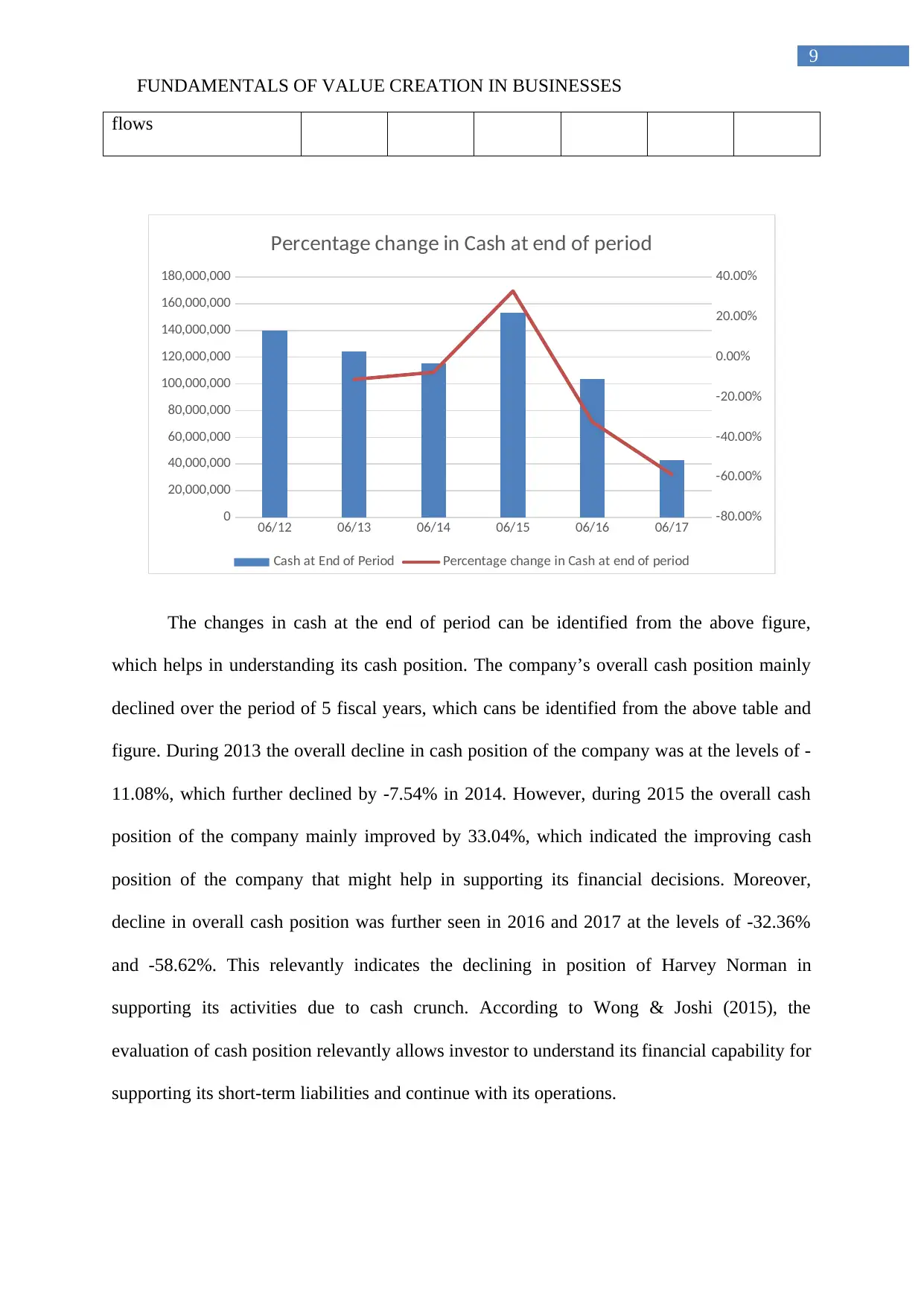

The changes in cash at the end of period can be identified from the above figure,

which helps in understanding its cash position. The company’s overall cash position mainly

declined over the period of 5 fiscal years, which cans be identified from the above table and

figure. During 2013 the overall decline in cash position of the company was at the levels of -

11.08%, which further declined by -7.54% in 2014. However, during 2015 the overall cash

position of the company mainly improved by 33.04%, which indicated the improving cash

position of the company that might help in supporting its financial decisions. Moreover,

decline in overall cash position was further seen in 2016 and 2017 at the levels of -32.36%

and -58.62%. This relevantly indicates the declining in position of Harvey Norman in

supporting its activities due to cash crunch. According to Wong & Joshi (2015), the

evaluation of cash position relevantly allows investor to understand its financial capability for

supporting its short-term liabilities and continue with its operations.

9

flows

06/12 06/13 06/14 06/15 06/16 06/17

0

20,000,000

40,000,000

60,000,000

80,000,000

100,000,000

120,000,000

140,000,000

160,000,000

180,000,000

-80.00%

-60.00%

-40.00%

-20.00%

0.00%

20.00%

40.00%

Percentage change in Cash at end of period

Cash at End of Period Percentage change in Cash at end of period

The changes in cash at the end of period can be identified from the above figure,

which helps in understanding its cash position. The company’s overall cash position mainly

declined over the period of 5 fiscal years, which cans be identified from the above table and

figure. During 2013 the overall decline in cash position of the company was at the levels of -

11.08%, which further declined by -7.54% in 2014. However, during 2015 the overall cash

position of the company mainly improved by 33.04%, which indicated the improving cash

position of the company that might help in supporting its financial decisions. Moreover,

decline in overall cash position was further seen in 2016 and 2017 at the levels of -32.36%

and -58.62%. This relevantly indicates the declining in position of Harvey Norman in

supporting its activities due to cash crunch. According to Wong & Joshi (2015), the

evaluation of cash position relevantly allows investor to understand its financial capability for

supporting its short-term liabilities and continue with its operations.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FUNDAMENTALS OF VALUE CREATION IN BUSINESSES

10

Therefore, it could be understood that cash position of the Harvey Norman mainly

declined over the period of 5 years, which relevantly reduces its ability to conduct smooth

operations. This continuous decline in cash position during 2013, 2014, 2016 and 2017 is

mainly complemented with the rising in net assets. This relevantly indicates that Harvey

Norman has used its spare cash to purchase relevant assets for complementing the increment

in assets such as property, plant, and equipment. Hence, it could be understood that decline in

cash position of Harvey Norman is supported by the increment in total assets, which is used

to improve its operational capability. On the other hand, Wijesundera et al., (2015) argued

that the evaluation of cash position does not allow investors to gauge into the financial

growth and progress, which could be obtained by the company in near future.

06/12 06/13 06/14 06/15 06/16 06/17

-350,000,000

-300,000,000

-250,000,000

-200,000,000

-150,000,000

-100,000,000

-50,000,000

0

-100.00%

0.00%

100.00%

200.00%

300.00%

400.00%

500.00%

Percentage change in net financing cash flows

Net Financing Cashflows Percentage change in net financing cash flows

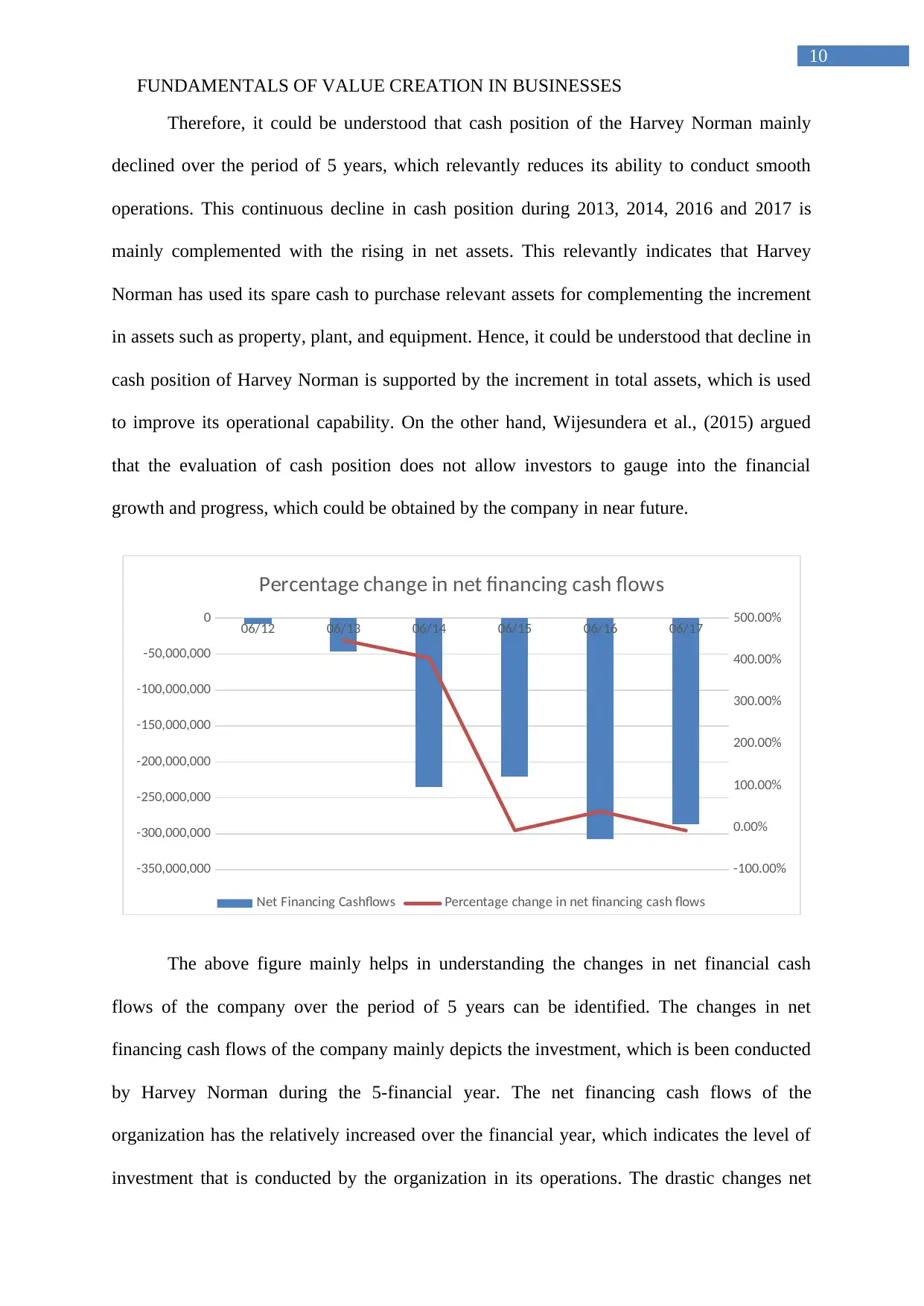

The above figure mainly helps in understanding the changes in net financial cash

flows of the company over the period of 5 years can be identified. The changes in net

financing cash flows of the company mainly depicts the investment, which is been conducted

by Harvey Norman during the 5-financial year. The net financing cash flows of the

organization has the relatively increased over the financial year, which indicates the level of

investment that is conducted by the organization in its operations. The drastic changes net

10

Therefore, it could be understood that cash position of the Harvey Norman mainly

declined over the period of 5 years, which relevantly reduces its ability to conduct smooth

operations. This continuous decline in cash position during 2013, 2014, 2016 and 2017 is

mainly complemented with the rising in net assets. This relevantly indicates that Harvey

Norman has used its spare cash to purchase relevant assets for complementing the increment

in assets such as property, plant, and equipment. Hence, it could be understood that decline in

cash position of Harvey Norman is supported by the increment in total assets, which is used

to improve its operational capability. On the other hand, Wijesundera et al., (2015) argued

that the evaluation of cash position does not allow investors to gauge into the financial

growth and progress, which could be obtained by the company in near future.

06/12 06/13 06/14 06/15 06/16 06/17

-350,000,000

-300,000,000

-250,000,000

-200,000,000

-150,000,000

-100,000,000

-50,000,000

0

-100.00%

0.00%

100.00%

200.00%

300.00%

400.00%

500.00%

Percentage change in net financing cash flows

Net Financing Cashflows Percentage change in net financing cash flows

The above figure mainly helps in understanding the changes in net financial cash

flows of the company over the period of 5 years can be identified. The changes in net

financing cash flows of the company mainly depicts the investment, which is been conducted

by Harvey Norman during the 5-financial year. The net financing cash flows of the

organization has the relatively increased over the financial year, which indicates the level of

investment that is conducted by the organization in its operations. The drastic changes net

FUNDAMENTALS OF VALUE CREATION IN BUSINESSES

11

financing cash flows was seen you during 2013, where the percentage change in client to

447.21%. Moreover, the continuous increment in investment is seen in 2014 with a total

percentage change in investments of 405.16%. However, during 2015 the overall investment

growth mainly declined to -6.21%, which indicated it slow growth and investment capability

of the company to support its operations. Moreover, the net financing cash flows conducted

by Harvey Norman continue to during 2016, which was again halted in 2017, as the change in

percentage of Financing cash flow became -6.60%. In this context, Choi, Kim & Oh (2017)

stated that with the evaluation of cash flow statement the overall financial capability of the

organization can be identified, which is essential for investors while making relevant

investment decisions.

3.7 Profitability analysis:

Particulars 06/12 06/13 06/14 06/15 06/16 06/17

Net Profit after Tax

Before Abnormal

176,315,

000

144,477,

000

212,238,

000

268,914,

000

351,340,

000

452,966,

000

Total Revenue 2,352,97

8,000

2,239,71

6,000

2,435,33

6,000

2,580,96

1,000

2,825,97

8,000

2,904,74

2,000

Net Profit Margin (%) 7.49% 6.45% 8.71% 10.42% 12.43% 15.59%

11

financing cash flows was seen you during 2013, where the percentage change in client to

447.21%. Moreover, the continuous increment in investment is seen in 2014 with a total

percentage change in investments of 405.16%. However, during 2015 the overall investment

growth mainly declined to -6.21%, which indicated it slow growth and investment capability

of the company to support its operations. Moreover, the net financing cash flows conducted

by Harvey Norman continue to during 2016, which was again halted in 2017, as the change in

percentage of Financing cash flow became -6.60%. In this context, Choi, Kim & Oh (2017)

stated that with the evaluation of cash flow statement the overall financial capability of the

organization can be identified, which is essential for investors while making relevant

investment decisions.

3.7 Profitability analysis:

Particulars 06/12 06/13 06/14 06/15 06/16 06/17

Net Profit after Tax

Before Abnormal

176,315,

000

144,477,

000

212,238,

000

268,914,

000

351,340,

000

452,966,

000

Total Revenue 2,352,97

8,000

2,239,71

6,000

2,435,33

6,000

2,580,96

1,000

2,825,97

8,000

2,904,74

2,000

Net Profit Margin (%) 7.49% 6.45% 8.71% 10.42% 12.43% 15.59%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 28

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.