Advanced Accounting: Consolidation and Investment Analysis Homework

VerifiedAdded on 2020/04/21

|14

|1918

|298

Homework Assignment

AI Summary

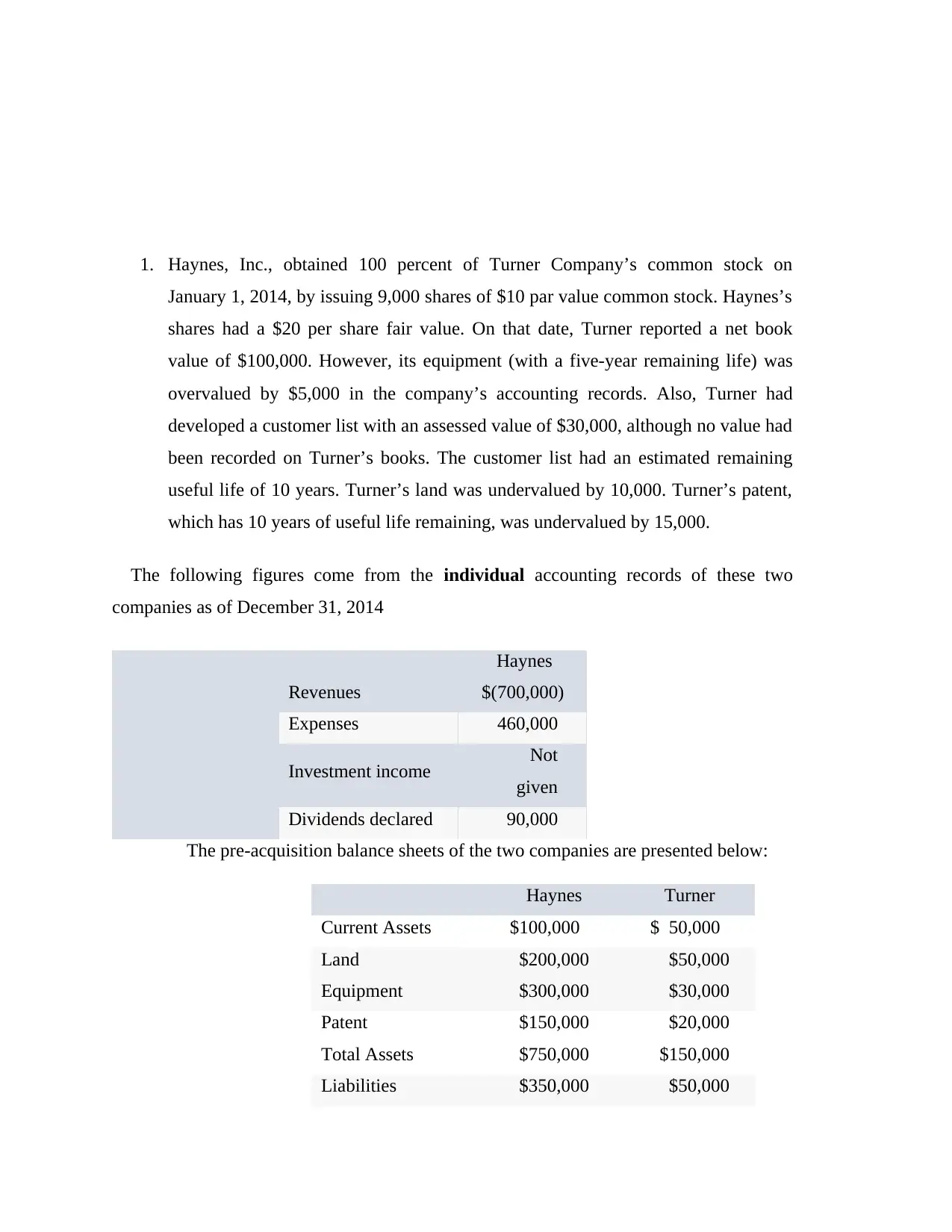

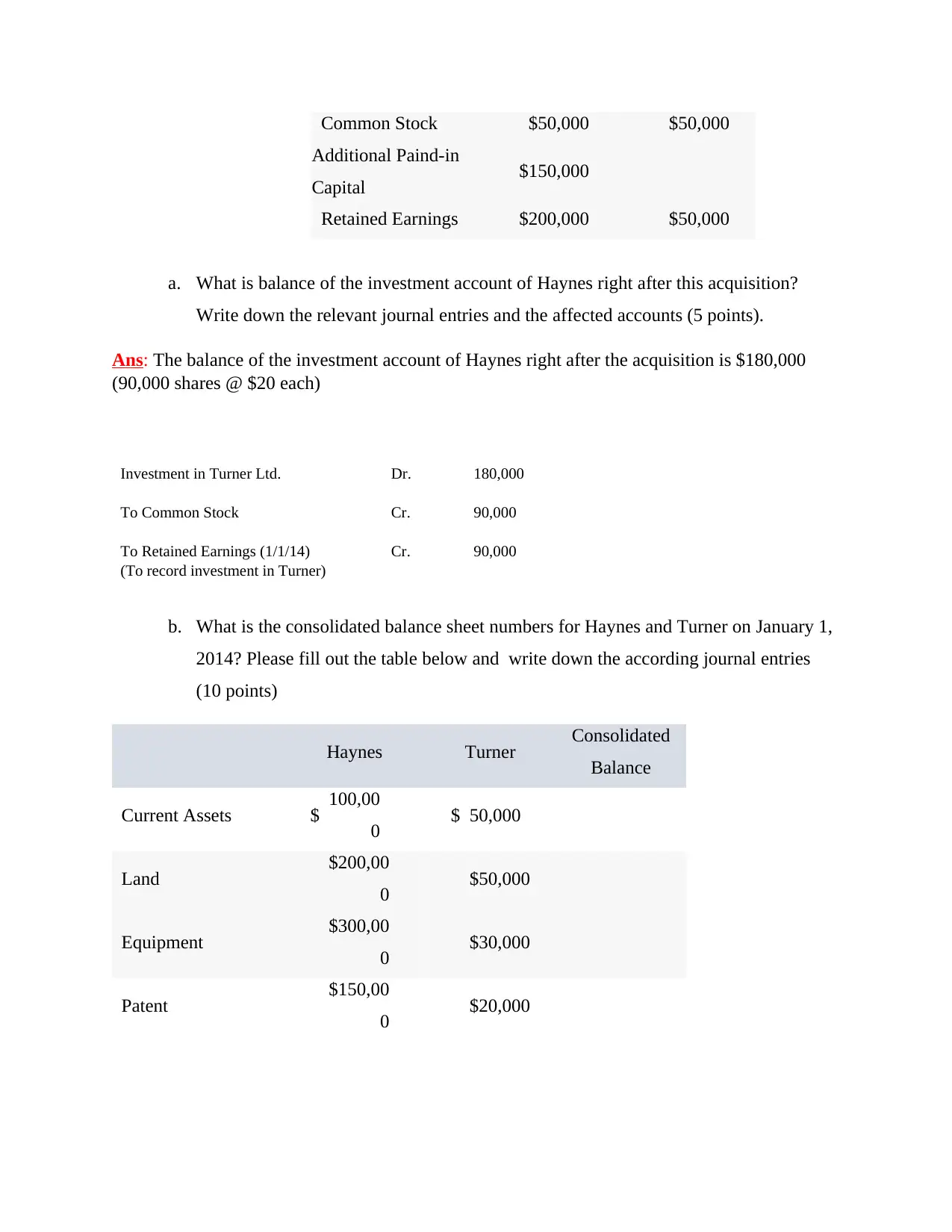

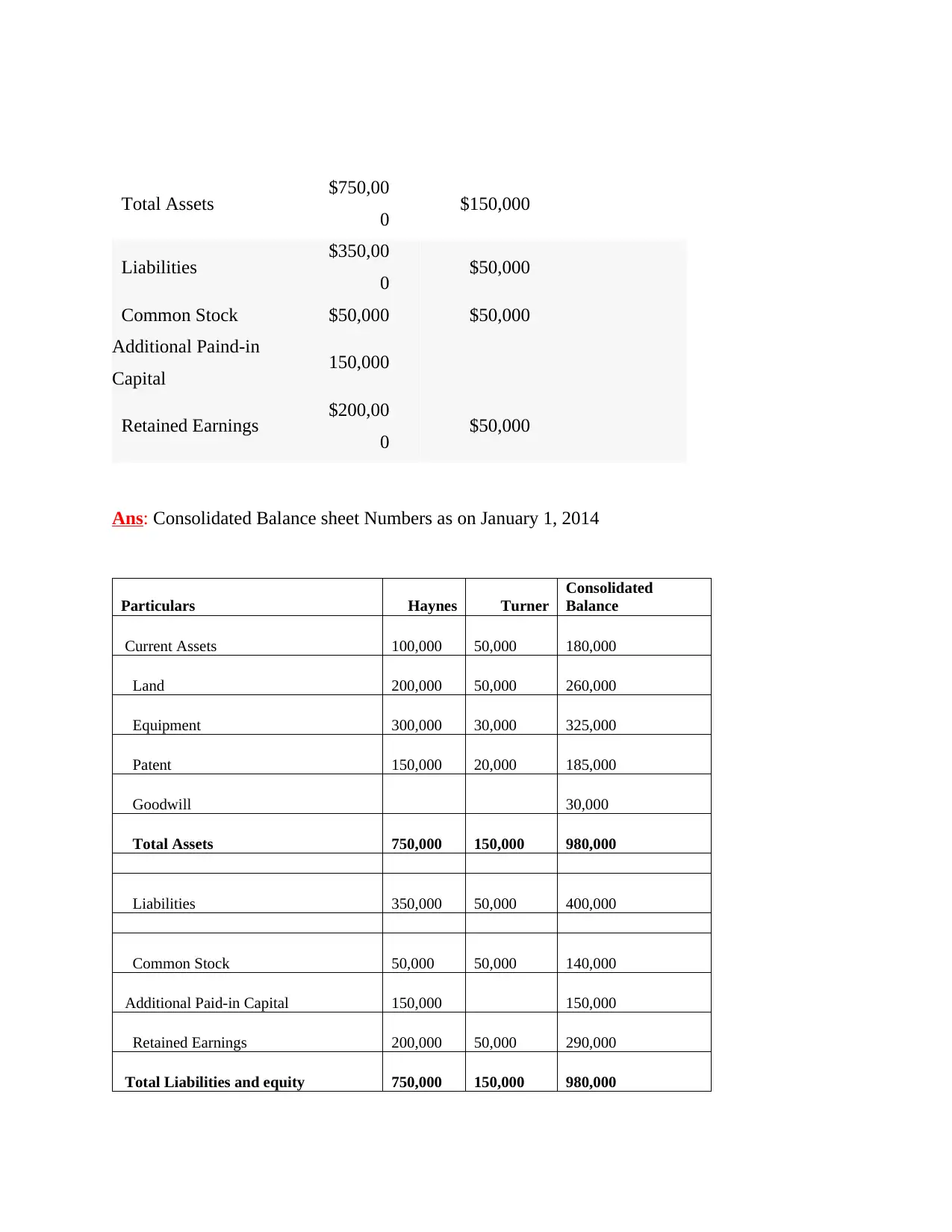

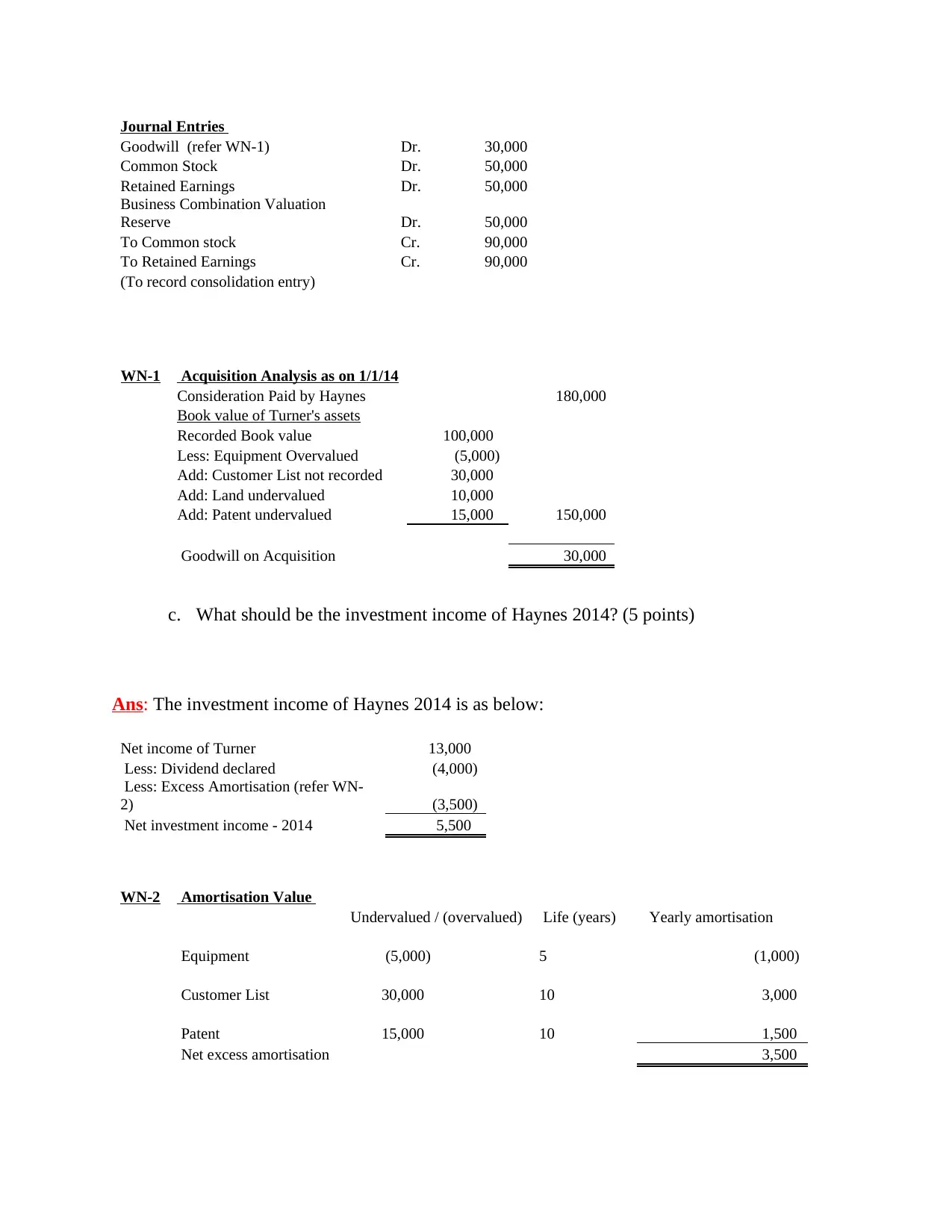

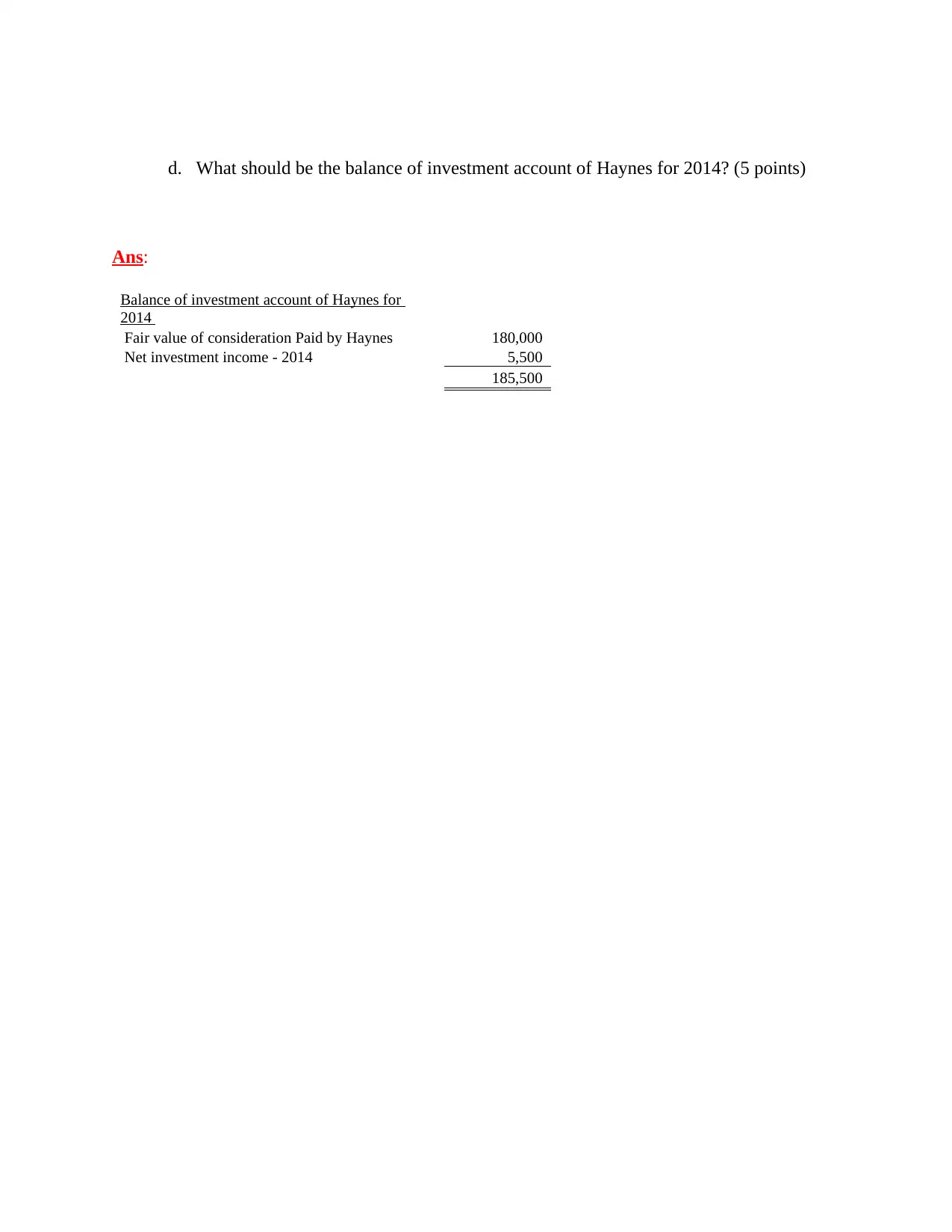

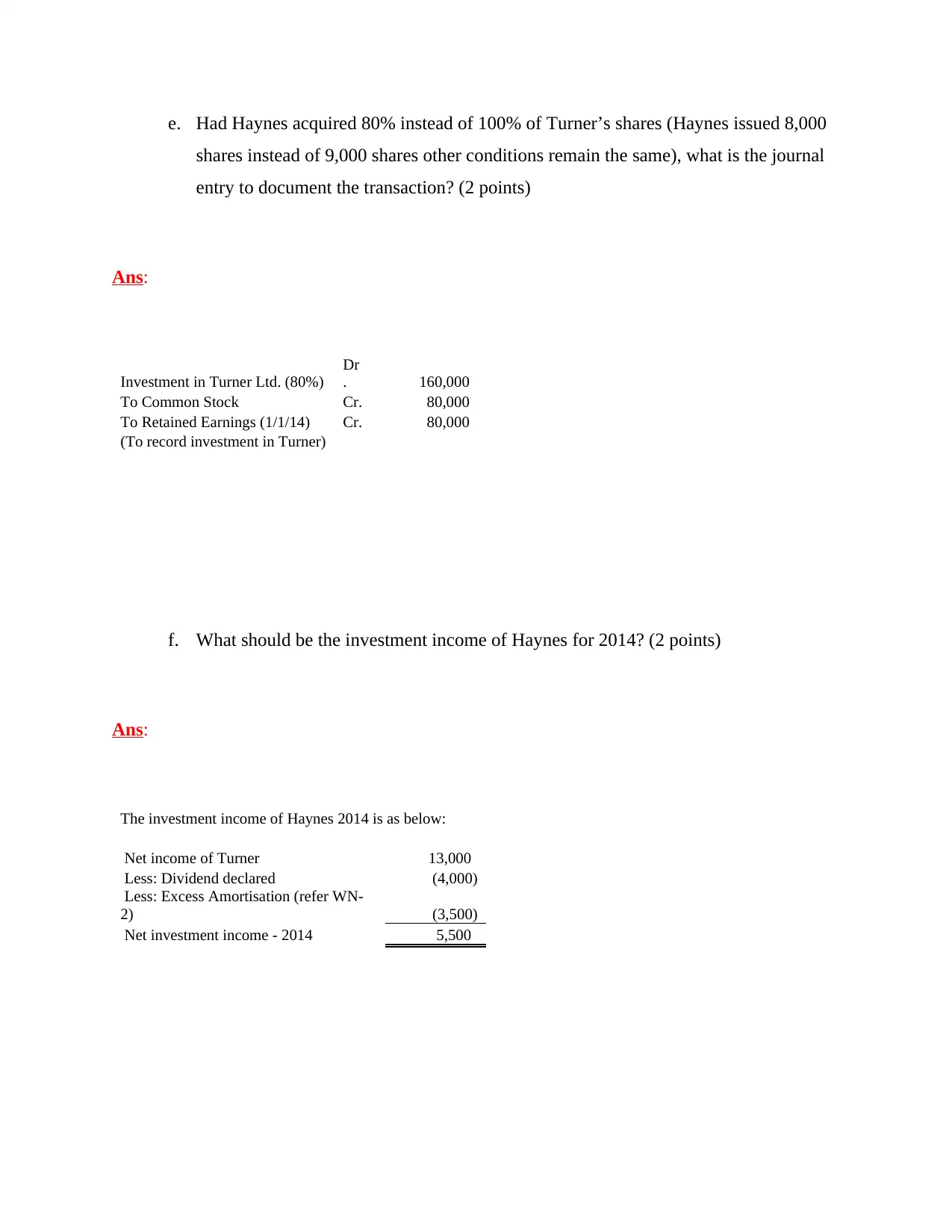

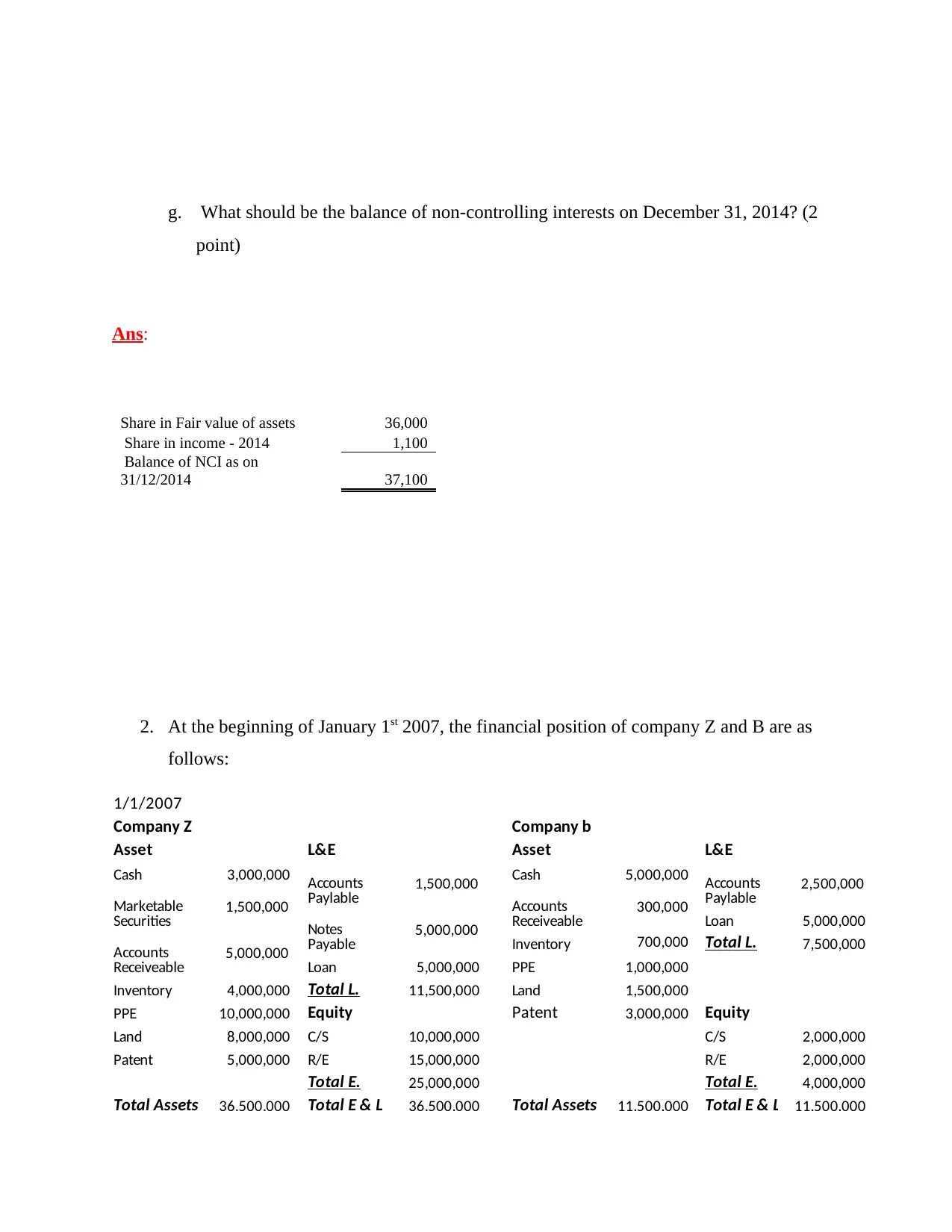

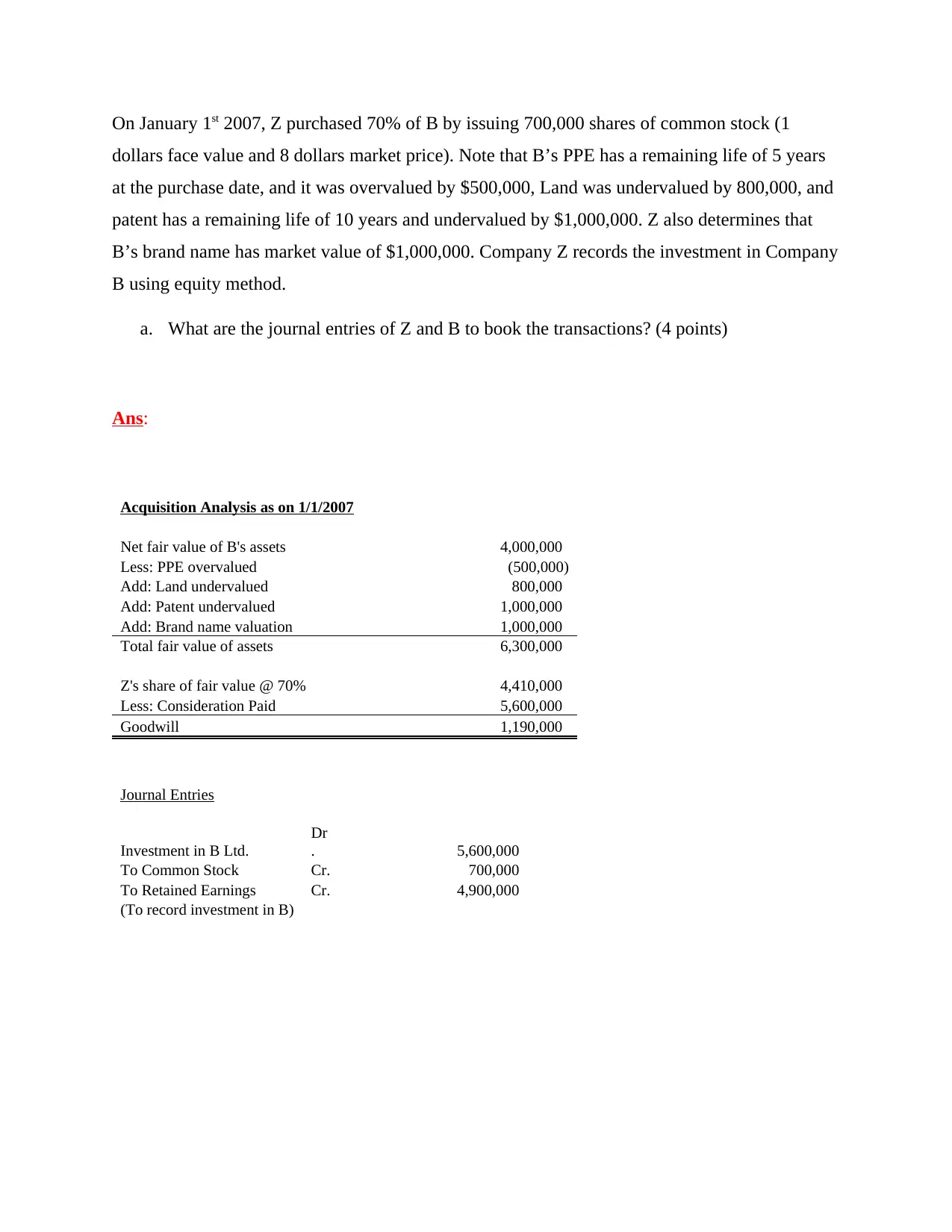

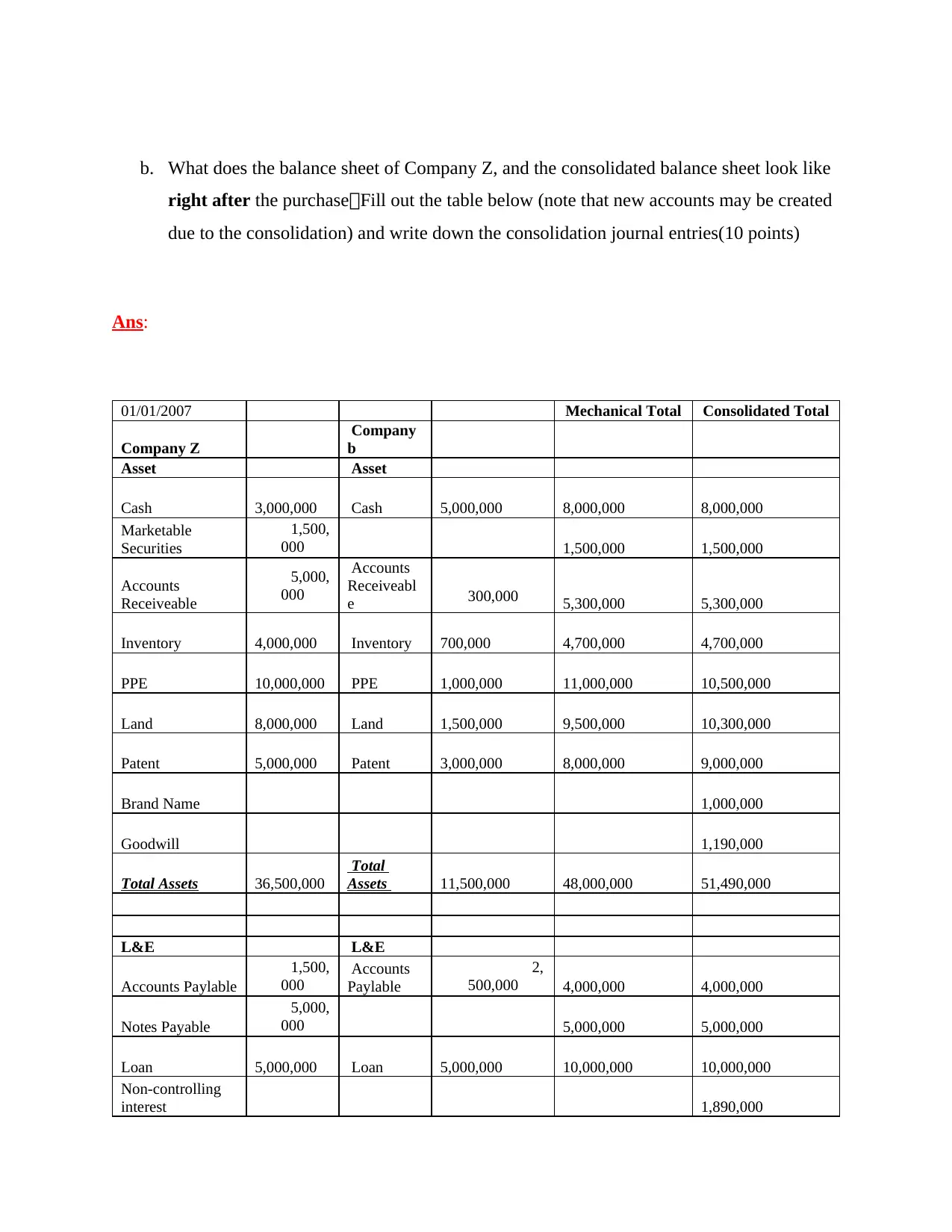

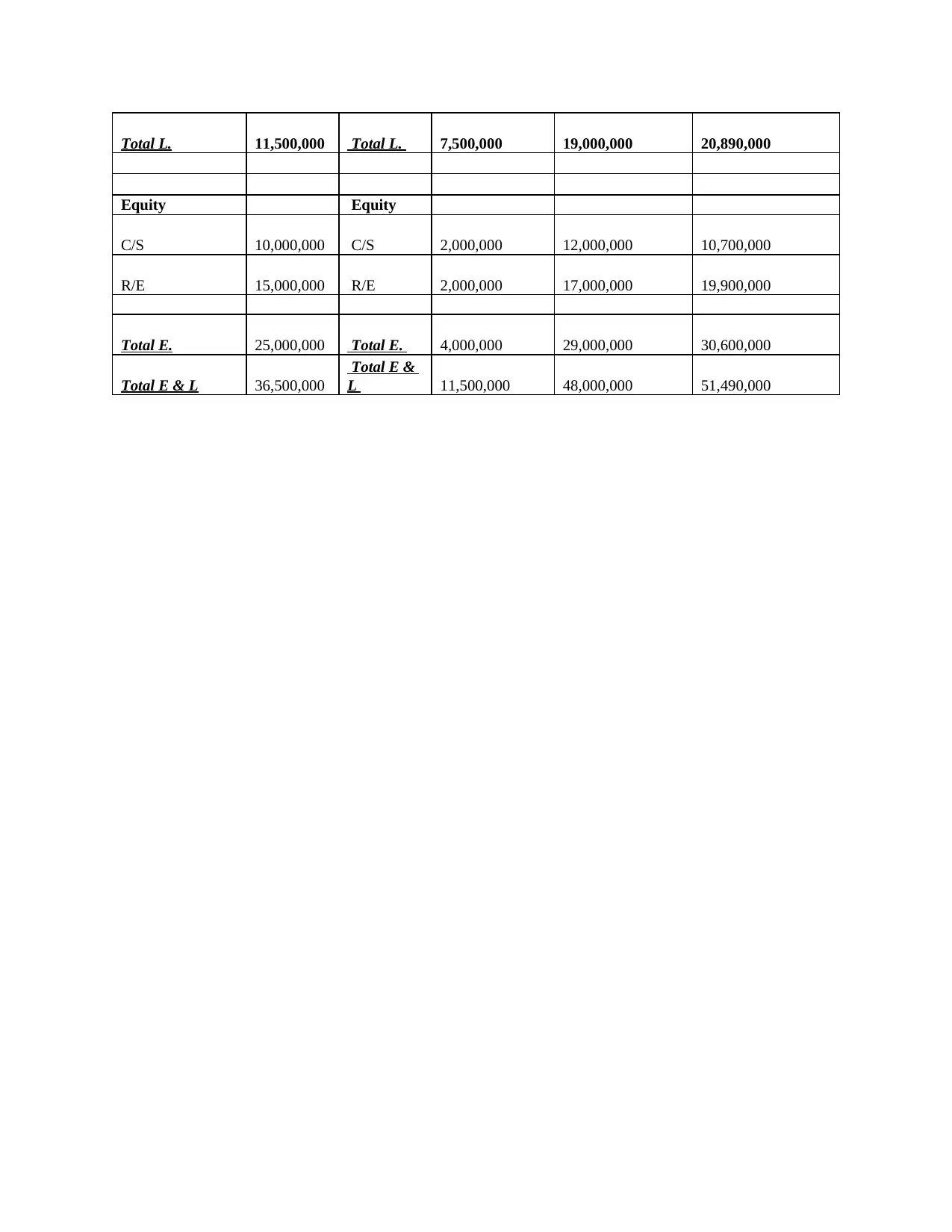

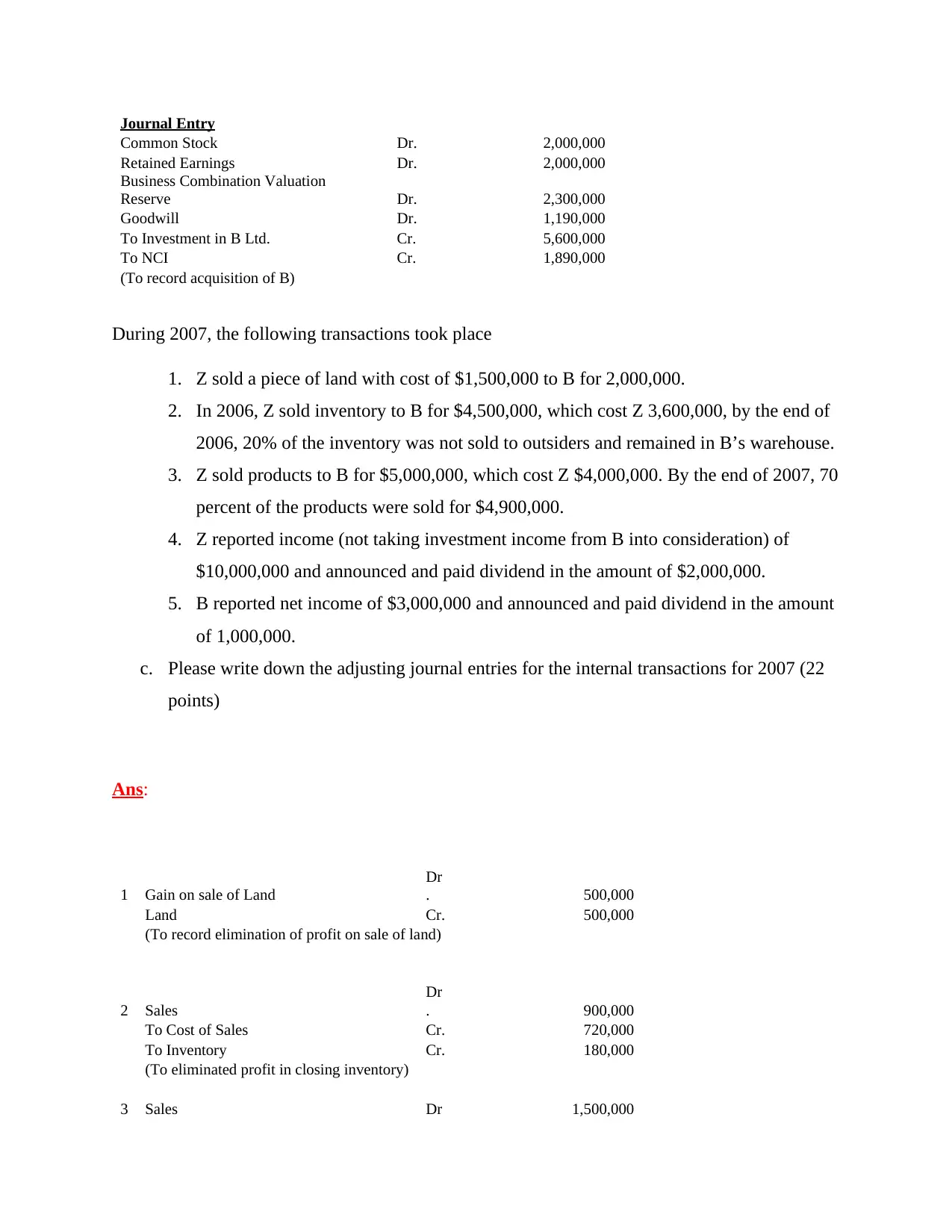

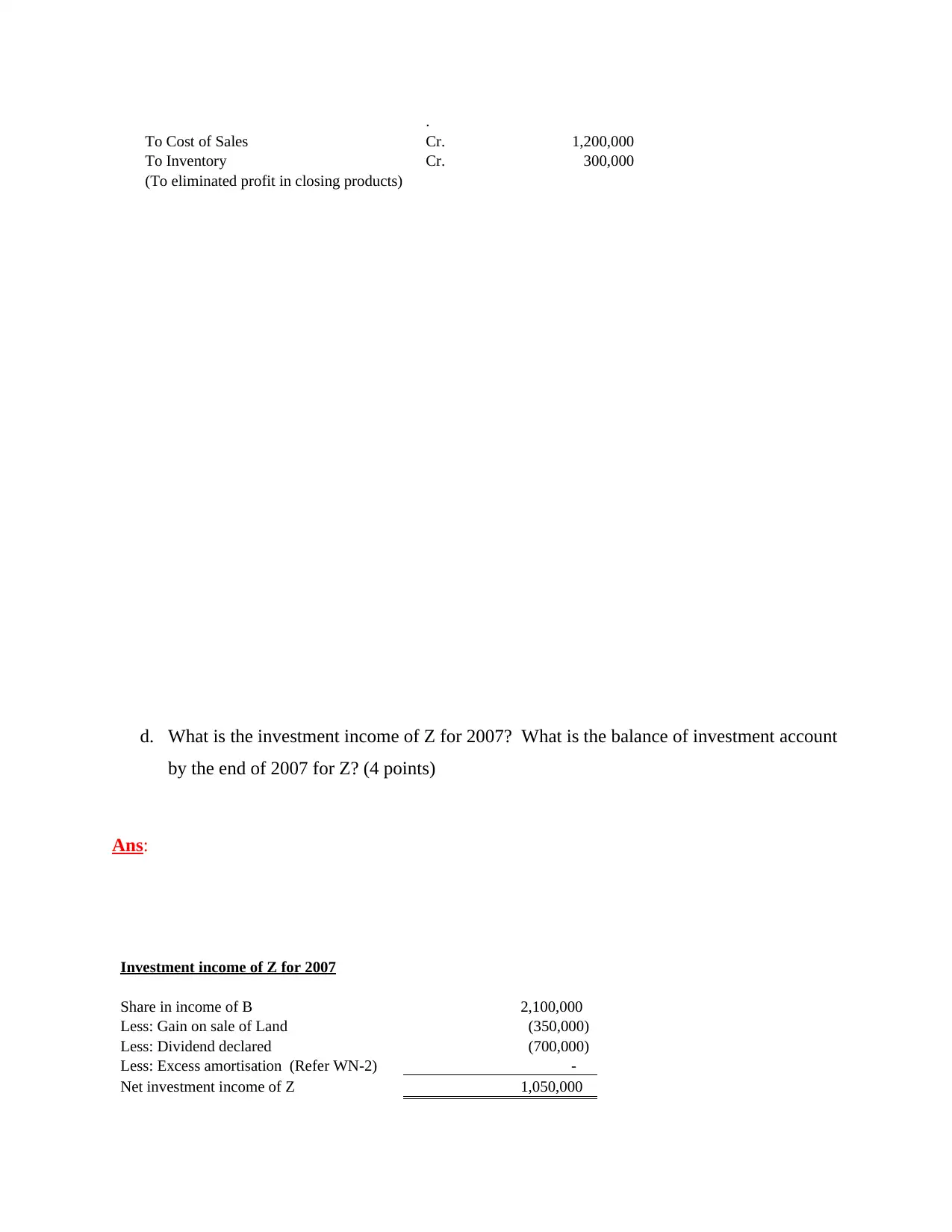

This assignment provides a detailed analysis of consolidation accounting principles, focusing on business combinations and the preparation of consolidated financial statements. The solution addresses various scenarios, including the acquisition of a subsidiary, calculation of goodwill, and the equity method of accounting. The assignment covers the preparation of journal entries for acquisition, consolidation entries, and the calculation of investment income, non-controlling interests, and the impact of intercompany transactions. It also explores the effects of undervalued or overvalued assets, and the allocation of purchase price differences. The assignment includes examples of pre-acquisition balance sheets, consolidated balance sheets, and the calculation of investment income. The solution also analyzes the impact of different ownership percentages and intercompany transactions, such as the sale of land and inventory, and the elimination of unrealized profits. The assignment provides step-by-step solutions, including journal entries, calculations, and explanations, making it a valuable resource for students studying advanced accounting and financial statement consolidation.

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.