Financial Accounting Analysis: D&G Company Transactions and Accounts

VerifiedAdded on 2021/05/20

|33

|6609

|679

Report

AI Summary

This report, prepared for the HCMC University of Technology and Education, analyzes the financial accounting practices of D&G Company. It begins with an introduction to the accounting cycle, detailing its five steps: source documents, journals, ledgers, trial balance, and final accounts. The report applies the double-entry bookkeeping system, demonstrating the recording of business transactions in journal entries and T-accounts. It then proceeds to the preparation of a trial balance and explains its purpose. Furthermore, the report covers the preparation of final accounts, including the profit and loss account and balance sheet, adjusting for accruals, depreciation, and prepayments. The assignment includes examples and calculations based on a provided scenario, illustrating the practical application of accounting principles for sole traders, partnerships, and limited companies. The report concludes with a discussion of the overall financial accounting process and its importance.

RECORDING AND FEEDING BACK ON LEARNER ACHIEVEMENT

Course / Award BTEC HND Business Management

Unit 10 Financial Accounting_A1

Student Name Nguyen Thi Hoai Thuong_MC72152

Assessment criteria that

have been achieved

Assessment Criteria that

are still to be achieved

Assessor’s feedback (specific to assessment criteria)

Passed with M1, M2, D1, D2

Appropriate work provided on each task. Keep it up

Student Name/Signature Rework Due

Date

Assessor Name /

Signature Date

IV Name / Signature Date

Assessor’s feedback on the rework:

Student Name/Signature Date

Assessor Name /

Signature Date

IV Name / Signature Date

HCMC UNIVERSITY OF TECHNOLOGY

AND EDUCATION

Course / Award BTEC HND Business Management

Unit 10 Financial Accounting_A1

Student Name Nguyen Thi Hoai Thuong_MC72152

Assessment criteria that

have been achieved

Assessment Criteria that

are still to be achieved

Assessor’s feedback (specific to assessment criteria)

Passed with M1, M2, D1, D2

Appropriate work provided on each task. Keep it up

Student Name/Signature Rework Due

Date

Assessor Name /

Signature Date

IV Name / Signature Date

Assessor’s feedback on the rework:

Student Name/Signature Date

Assessor Name /

Signature Date

IV Name / Signature Date

HCMC UNIVERSITY OF TECHNOLOGY

AND EDUCATION

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTERNATIONAL EXCHANGE EDUCATION CENTER

HO CHI MINH UNIVERSITY OF TECHNOLOGY AND EDUCATION

ASSIGNMENT 1:

½ RECORD BUSINESS TRANSACTIONS AND

PREPARE FINAL ACCOUNT FOR D&G

LECTURER: MR. SUMIT

STUDENT: NGUYEN THI HOAI THUONG

CLASS: FINANCIAL ACCOUNTING

HO CHI MINH UNIVERSITY OF TECHNOLOGY AND EDUCATION

ASSIGNMENT 1:

½ RECORD BUSINESS TRANSACTIONS AND

PREPARE FINAL ACCOUNT FOR D&G

LECTURER: MR. SUMIT

STUDENT: NGUYEN THI HOAI THUONG

CLASS: FINANCIAL ACCOUNTING

Table of Contents

Introduction.........................................................................................................4

LO1: Record business transactions using Double entry book-keeping, and be

able to extract a Trial Balance............................................................................5

Task 1: Apply the double entry book-keeping system of debits and credits. Record

sales and purchases transactions in a general ledger........................................................5

I. The Accounting Cycle..................................................................................................................5

II. Prepare Journal Entries using Assignment scenario..............................................................10

III. Prepare T-account using assignment scenario....................................................................12

Task 2: Produce a trial balance applying the use of the balance off rule to complete

the ledger.............................................................................................................................18

1. Why do the company need to prepare the Trial Balance?.....................................................18

2. Preparing the Trial balance using assignment scenario.........................................................18

LO2: Prepare final accounts for sole-traders, partnerships and limited

companies in accordance with appropriate principles, conventions and

standards............................................................................................................20

Task 3: Prepare final accounts from given trial balance figures adjusting for accruals,

depreciation and prepayments..........................................................................................20

I. What are Accrual, Prepayment, and Depreciation?...............................................................20

II. The calculation of Accruals, Prepayment, and Depreciation using assignment scenario. .21

Task 4: Produce final accounts for a range of examples that include sole-traders,

partnerships or limited companies...................................................................................23

I. What is Final accounts with Adjustments?.............................................................................23

II. Preparing the Final Accounts with adjustment using assignment scenario.........................24

Conclusion.........................................................................................................29

Bibliography......................................................................................................30

3

Introduction.........................................................................................................4

LO1: Record business transactions using Double entry book-keeping, and be

able to extract a Trial Balance............................................................................5

Task 1: Apply the double entry book-keeping system of debits and credits. Record

sales and purchases transactions in a general ledger........................................................5

I. The Accounting Cycle..................................................................................................................5

II. Prepare Journal Entries using Assignment scenario..............................................................10

III. Prepare T-account using assignment scenario....................................................................12

Task 2: Produce a trial balance applying the use of the balance off rule to complete

the ledger.............................................................................................................................18

1. Why do the company need to prepare the Trial Balance?.....................................................18

2. Preparing the Trial balance using assignment scenario.........................................................18

LO2: Prepare final accounts for sole-traders, partnerships and limited

companies in accordance with appropriate principles, conventions and

standards............................................................................................................20

Task 3: Prepare final accounts from given trial balance figures adjusting for accruals,

depreciation and prepayments..........................................................................................20

I. What are Accrual, Prepayment, and Depreciation?...............................................................20

II. The calculation of Accruals, Prepayment, and Depreciation using assignment scenario. .21

Task 4: Produce final accounts for a range of examples that include sole-traders,

partnerships or limited companies...................................................................................23

I. What is Final accounts with Adjustments?.............................................................................23

II. Preparing the Final Accounts with adjustment using assignment scenario.........................24

Conclusion.........................................................................................................29

Bibliography......................................................................................................30

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Introduction

Besides Management Accounting for internal users in the organization to manage and operate

the company, there is Financial Accounting for external users who are not related to the

company. It helps external users understand the financial position of the company through

financial statements such as income statements, balance sheets. To help readers understand what

Financial Accounting is, the author who is the assistant accountant of D&G company is going to

talk about the processes in financial accounting, known as Accounting Cycle. Moreover, in order

for the reader to visualize the process, the author will have examples such as preparing Journal

Entries, Ledger, Trial Balance, Adjustment, and Financial Statements in this report.

4

Besides Management Accounting for internal users in the organization to manage and operate

the company, there is Financial Accounting for external users who are not related to the

company. It helps external users understand the financial position of the company through

financial statements such as income statements, balance sheets. To help readers understand what

Financial Accounting is, the author who is the assistant accountant of D&G company is going to

talk about the processes in financial accounting, known as Accounting Cycle. Moreover, in order

for the reader to visualize the process, the author will have examples such as preparing Journal

Entries, Ledger, Trial Balance, Adjustment, and Financial Statements in this report.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

LO1: Record business transactions using Double entry book-

keeping, and be able to extract a Trial Balance.

Task 1: Apply the double entry book-keeping system of debits and credits.

Record sales and purchases transactions in a general ledger.

I. The Accounting Cycle

1. Definition

The accounting cycle is a series of actions including identifying, analyzing, and recording the

financial transactions of a company. The steps of the cycle begins when accounting events

happen. Then, it finishes by planning the financial statements. Additional accounting records that

are used in the accounting cycle include the General ledger and Trial Balance. (Kenton, 2019)

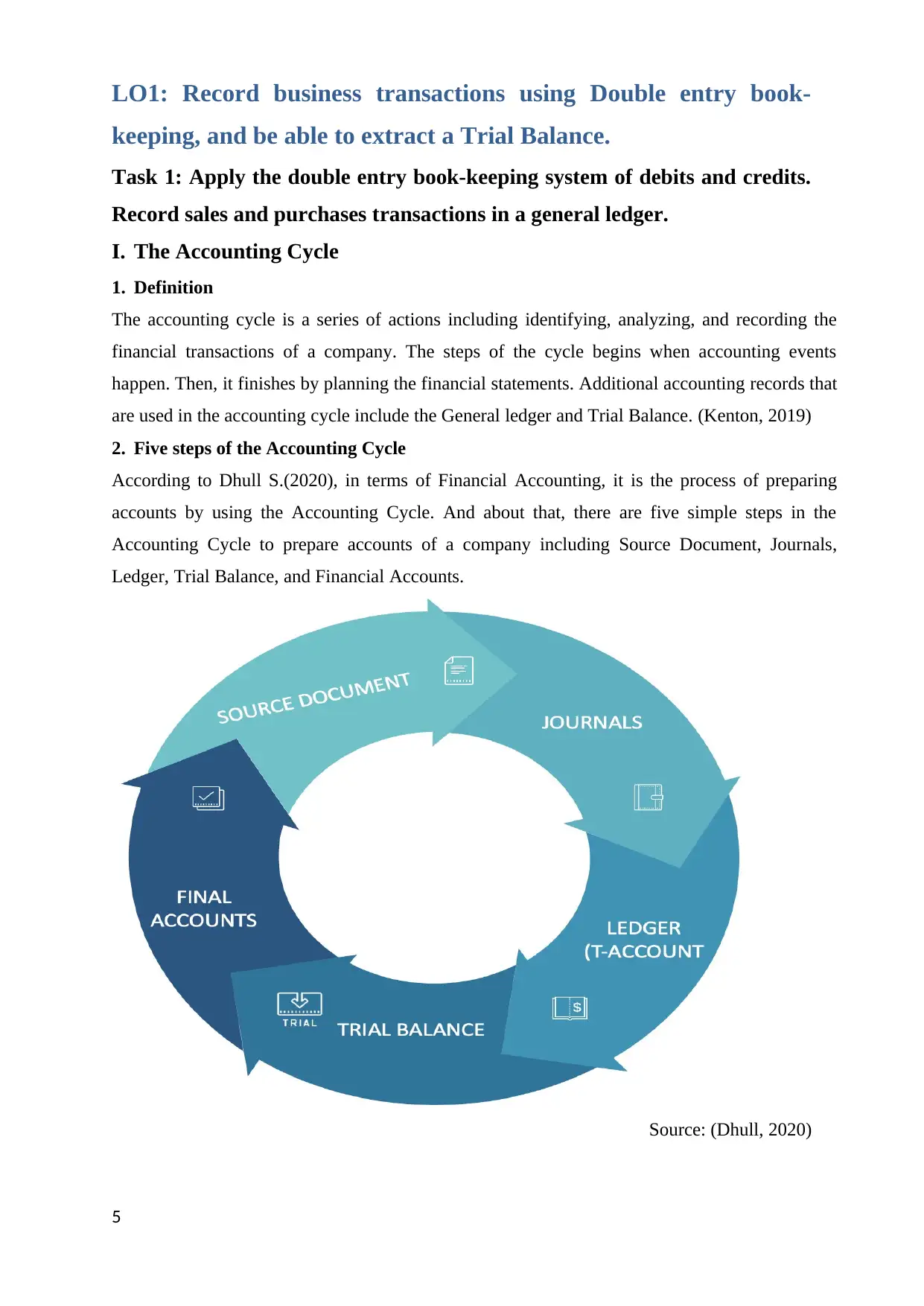

2. Five steps of the Accounting Cycle

According to Dhull S.(2020), in terms of Financial Accounting, it is the process of preparing

accounts by using the Accounting Cycle. And about that, there are five simple steps in the

Accounting Cycle to prepare accounts of a company including Source Document, Journals,

Ledger, Trial Balance, and Financial Accounts.

Source: (Dhull, 2020)

5

keeping, and be able to extract a Trial Balance.

Task 1: Apply the double entry book-keeping system of debits and credits.

Record sales and purchases transactions in a general ledger.

I. The Accounting Cycle

1. Definition

The accounting cycle is a series of actions including identifying, analyzing, and recording the

financial transactions of a company. The steps of the cycle begins when accounting events

happen. Then, it finishes by planning the financial statements. Additional accounting records that

are used in the accounting cycle include the General ledger and Trial Balance. (Kenton, 2019)

2. Five steps of the Accounting Cycle

According to Dhull S.(2020), in terms of Financial Accounting, it is the process of preparing

accounts by using the Accounting Cycle. And about that, there are five simple steps in the

Accounting Cycle to prepare accounts of a company including Source Document, Journals,

Ledger, Trial Balance, and Financial Accounts.

Source: (Dhull, 2020)

5

2.1 Source Document

As Dhull S. (2020) said, Source Document is any kinds of information, or transactions.

Moreover, book-keepers and accountants have to record and keep source documents for each

transaction. And every transaction need to contain the date, the description, and the value of this

transaction (Anon., 2020).

2.2 Journals

Journals, also known as Book of Prime Entry, are the first step to entry information in company

account using Debit and Credit. And, to complete the Journal, there are four steps (Dhull, 2020).

Step 1: Find Accounts

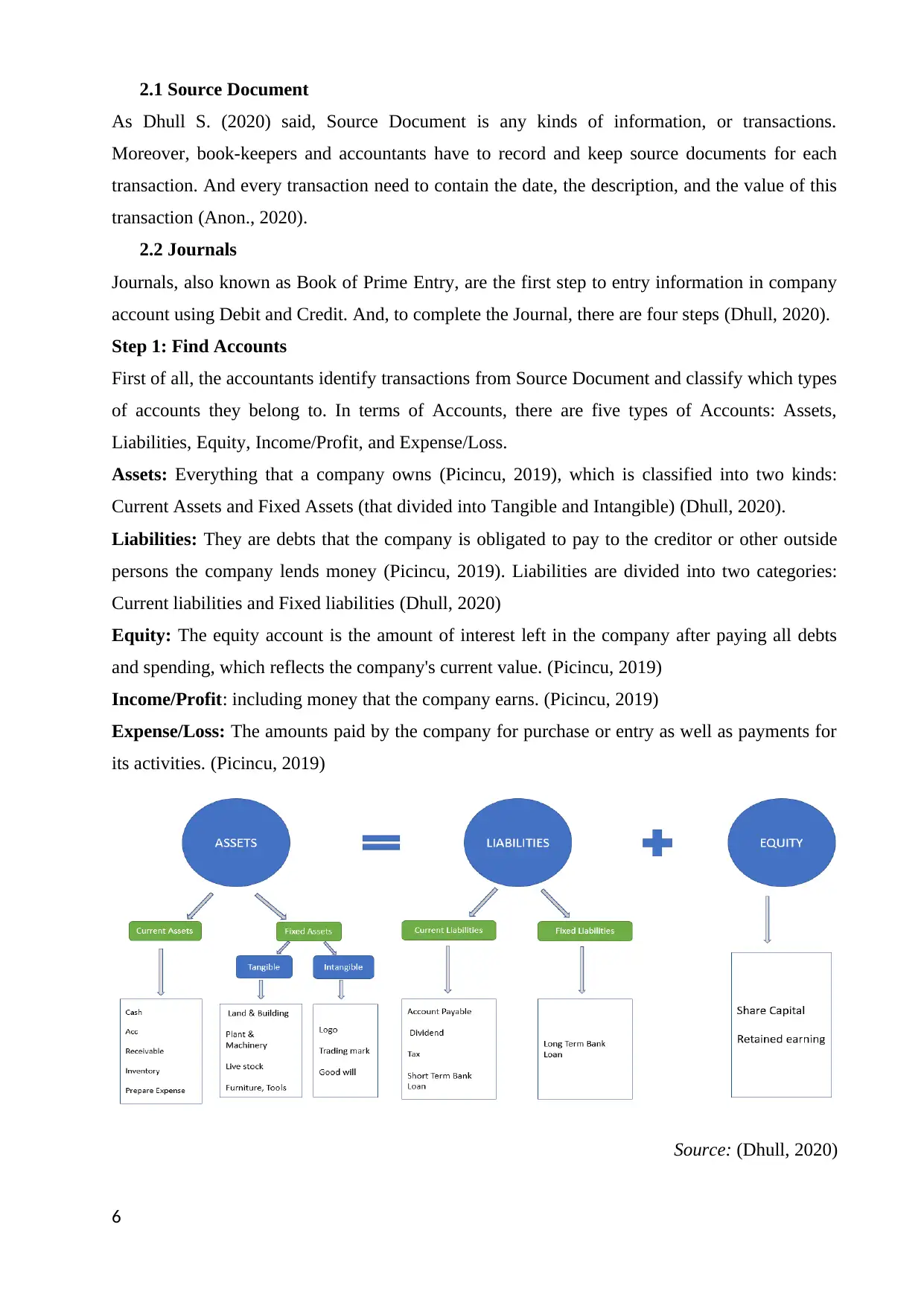

First of all, the accountants identify transactions from Source Document and classify which types

of accounts they belong to. In terms of Accounts, there are five types of Accounts: Assets,

Liabilities, Equity, Income/Profit, and Expense/Loss.

Assets: Everything that a company owns (Picincu, 2019), which is classified into two kinds:

Current Assets and Fixed Assets (that divided into Tangible and Intangible) (Dhull, 2020).

Liabilities: They are debts that the company is obligated to pay to the creditor or other outside

persons the company lends money (Picincu, 2019). Liabilities are divided into two categories:

Current liabilities and Fixed liabilities (Dhull, 2020)

Equity: The equity account is the amount of interest left in the company after paying all debts

and spending, which reflects the company's current value. (Picincu, 2019)

Income/Profit: including money that the company earns. (Picincu, 2019)

Expense/Loss: The amounts paid by the company for purchase or entry as well as payments for

its activities. (Picincu, 2019)

Source: (Dhull, 2020)

6

As Dhull S. (2020) said, Source Document is any kinds of information, or transactions.

Moreover, book-keepers and accountants have to record and keep source documents for each

transaction. And every transaction need to contain the date, the description, and the value of this

transaction (Anon., 2020).

2.2 Journals

Journals, also known as Book of Prime Entry, are the first step to entry information in company

account using Debit and Credit. And, to complete the Journal, there are four steps (Dhull, 2020).

Step 1: Find Accounts

First of all, the accountants identify transactions from Source Document and classify which types

of accounts they belong to. In terms of Accounts, there are five types of Accounts: Assets,

Liabilities, Equity, Income/Profit, and Expense/Loss.

Assets: Everything that a company owns (Picincu, 2019), which is classified into two kinds:

Current Assets and Fixed Assets (that divided into Tangible and Intangible) (Dhull, 2020).

Liabilities: They are debts that the company is obligated to pay to the creditor or other outside

persons the company lends money (Picincu, 2019). Liabilities are divided into two categories:

Current liabilities and Fixed liabilities (Dhull, 2020)

Equity: The equity account is the amount of interest left in the company after paying all debts

and spending, which reflects the company's current value. (Picincu, 2019)

Income/Profit: including money that the company earns. (Picincu, 2019)

Expense/Loss: The amounts paid by the company for purchase or entry as well as payments for

its activities. (Picincu, 2019)

Source: (Dhull, 2020)

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

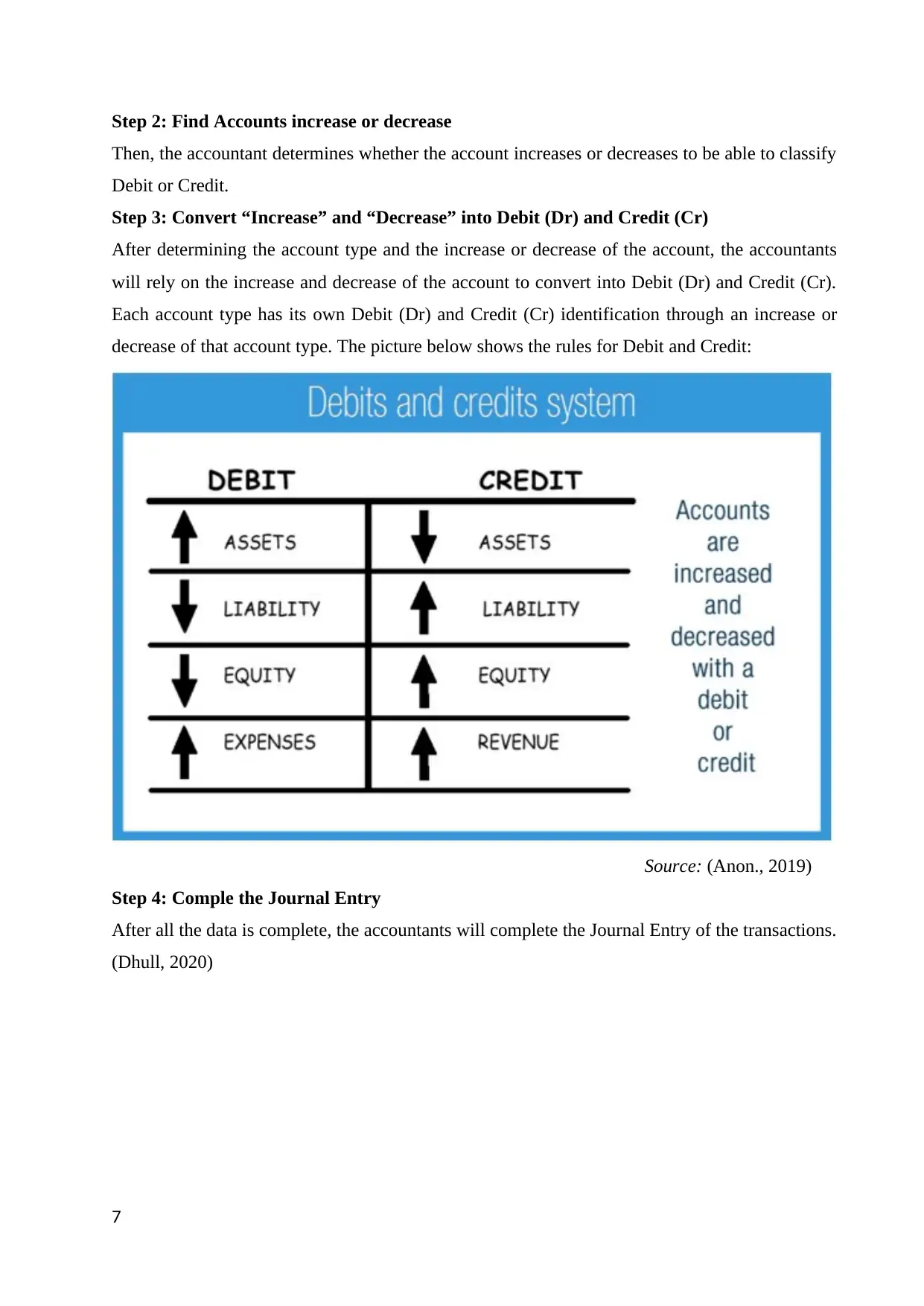

Step 2: Find Accounts increase or decrease

Then, the accountant determines whether the account increases or decreases to be able to classify

Debit or Credit.

Step 3: Convert “Increase” and “Decrease” into Debit (Dr) and Credit (Cr)

After determining the account type and the increase or decrease of the account, the accountants

will rely on the increase and decrease of the account to convert into Debit (Dr) and Credit (Cr).

Each account type has its own Debit (Dr) and Credit (Cr) identification through an increase or

decrease of that account type. The picture below shows the rules for Debit and Credit:

Source: (Anon., 2019)

Step 4: Comple the Journal Entry

After all the data is complete, the accountants will complete the Journal Entry of the transactions.

(Dhull, 2020)

7

Then, the accountant determines whether the account increases or decreases to be able to classify

Debit or Credit.

Step 3: Convert “Increase” and “Decrease” into Debit (Dr) and Credit (Cr)

After determining the account type and the increase or decrease of the account, the accountants

will rely on the increase and decrease of the account to convert into Debit (Dr) and Credit (Cr).

Each account type has its own Debit (Dr) and Credit (Cr) identification through an increase or

decrease of that account type. The picture below shows the rules for Debit and Credit:

Source: (Anon., 2019)

Step 4: Comple the Journal Entry

After all the data is complete, the accountants will complete the Journal Entry of the transactions.

(Dhull, 2020)

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

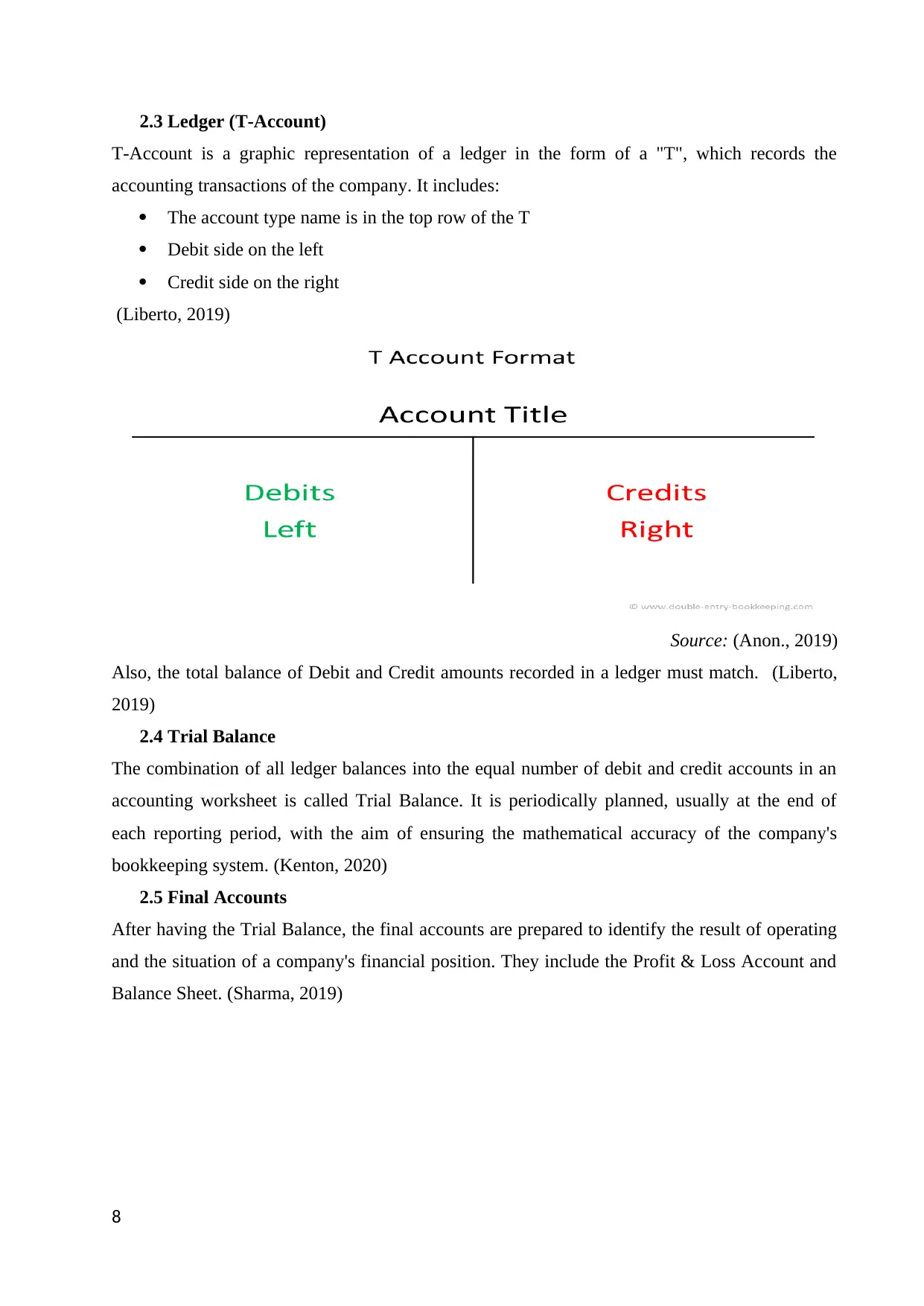

2.3 Ledger (T-Account)

T-Account is a graphic representation of a ledger in the form of a "T", which records the

accounting transactions of the company. It includes:

The account type name is in the top row of the T

Debit side on the left

Credit side on the right

(Liberto, 2019)

Source: (Anon., 2019)

Also, the total balance of Debit and Credit amounts recorded in a ledger must match. (Liberto,

2019)

2.4 Trial Balance

The combination of all ledger balances into the equal number of debit and credit accounts in an

accounting worksheet is called Trial Balance. It is periodically planned, usually at the end of

each reporting period, with the aim of ensuring the mathematical accuracy of the company's

bookkeeping system. (Kenton, 2020)

2.5 Final Accounts

After having the Trial Balance, the final accounts are prepared to identify the result of operating

and the situation of a company's financial position. They include the Profit & Loss Account and

Balance Sheet. (Sharma, 2019)

8

T-Account is a graphic representation of a ledger in the form of a "T", which records the

accounting transactions of the company. It includes:

The account type name is in the top row of the T

Debit side on the left

Credit side on the right

(Liberto, 2019)

Source: (Anon., 2019)

Also, the total balance of Debit and Credit amounts recorded in a ledger must match. (Liberto,

2019)

2.4 Trial Balance

The combination of all ledger balances into the equal number of debit and credit accounts in an

accounting worksheet is called Trial Balance. It is periodically planned, usually at the end of

each reporting period, with the aim of ensuring the mathematical accuracy of the company's

bookkeeping system. (Kenton, 2020)

2.5 Final Accounts

After having the Trial Balance, the final accounts are prepared to identify the result of operating

and the situation of a company's financial position. They include the Profit & Loss Account and

Balance Sheet. (Sharma, 2019)

8

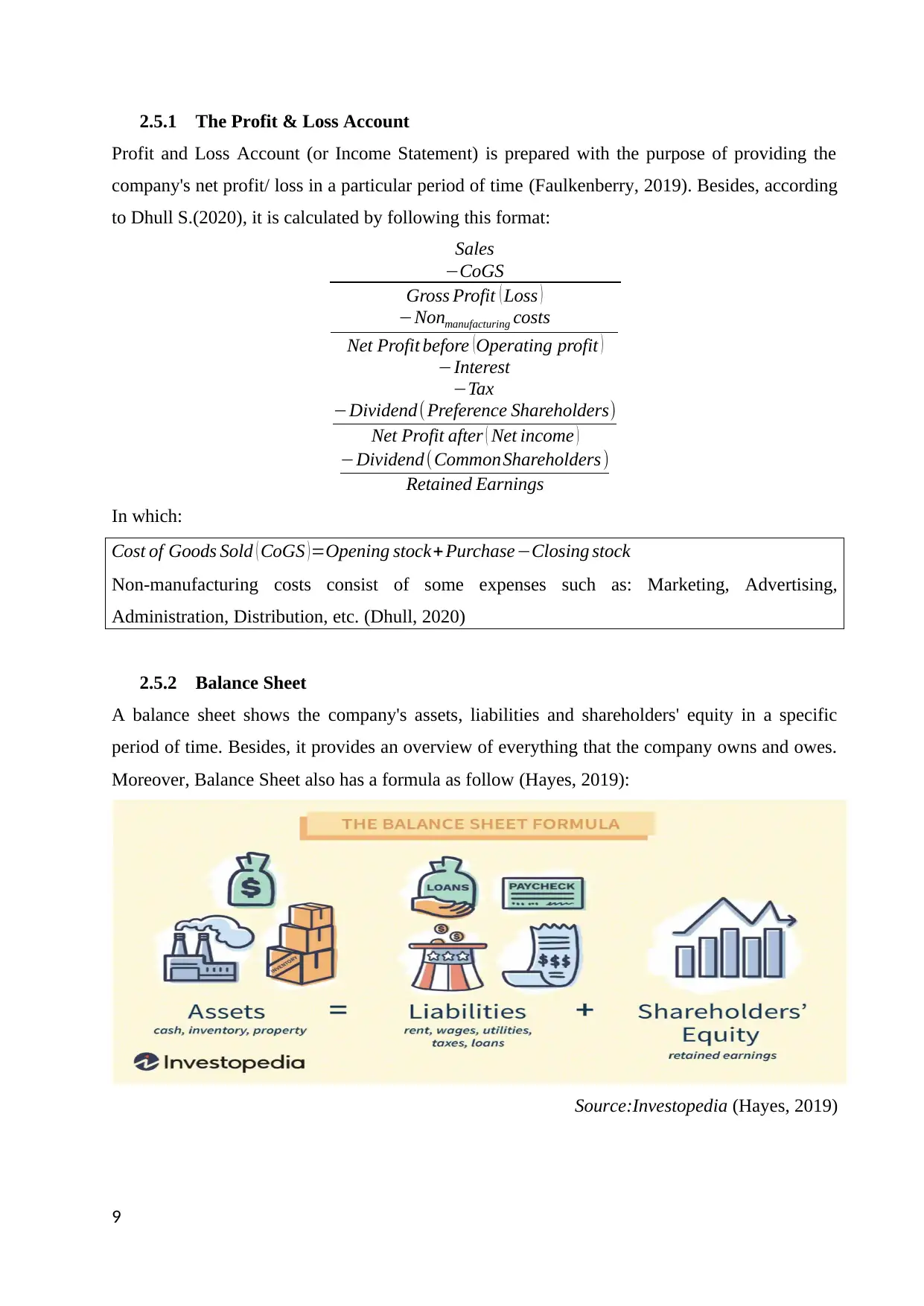

2.5.1 The Profit & Loss Account

Profit and Loss Account (or Income Statement) is prepared with the purpose of providing the

company's net profit/ loss in a particular period of time (Faulkenberry, 2019). Besides, according

to Dhull S.(2020), it is calculated by following this format:

Sales

−CoGS

Gross Profit ( Loss )

−Nonmanufacturing costs

Net Profit before (Operating profit )

−Interest

−Tax

−Dividend(Preference Shareholders)

Net Profit after ( Net income )

−Dividend(CommonShareholders)

Retained Earnings

In which:

Cost of Goods Sold ( CoGS ) =Opening stock+Purchase−Closing stock

Non-manufacturing costs consist of some expenses such as: Marketing, Advertising,

Administration, Distribution, etc. (Dhull, 2020)

2.5.2 Balance Sheet

A balance sheet shows the company's assets, liabilities and shareholders' equity in a specific

period of time. Besides, it provides an overview of everything that the company owns and owes.

Moreover, Balance Sheet also has a formula as follow (Hayes, 2019):

Source:Investopedia (Hayes, 2019)

9

Profit and Loss Account (or Income Statement) is prepared with the purpose of providing the

company's net profit/ loss in a particular period of time (Faulkenberry, 2019). Besides, according

to Dhull S.(2020), it is calculated by following this format:

Sales

−CoGS

Gross Profit ( Loss )

−Nonmanufacturing costs

Net Profit before (Operating profit )

−Interest

−Tax

−Dividend(Preference Shareholders)

Net Profit after ( Net income )

−Dividend(CommonShareholders)

Retained Earnings

In which:

Cost of Goods Sold ( CoGS ) =Opening stock+Purchase−Closing stock

Non-manufacturing costs consist of some expenses such as: Marketing, Advertising,

Administration, Distribution, etc. (Dhull, 2020)

2.5.2 Balance Sheet

A balance sheet shows the company's assets, liabilities and shareholders' equity in a specific

period of time. Besides, it provides an overview of everything that the company owns and owes.

Moreover, Balance Sheet also has a formula as follow (Hayes, 2019):

Source:Investopedia (Hayes, 2019)

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

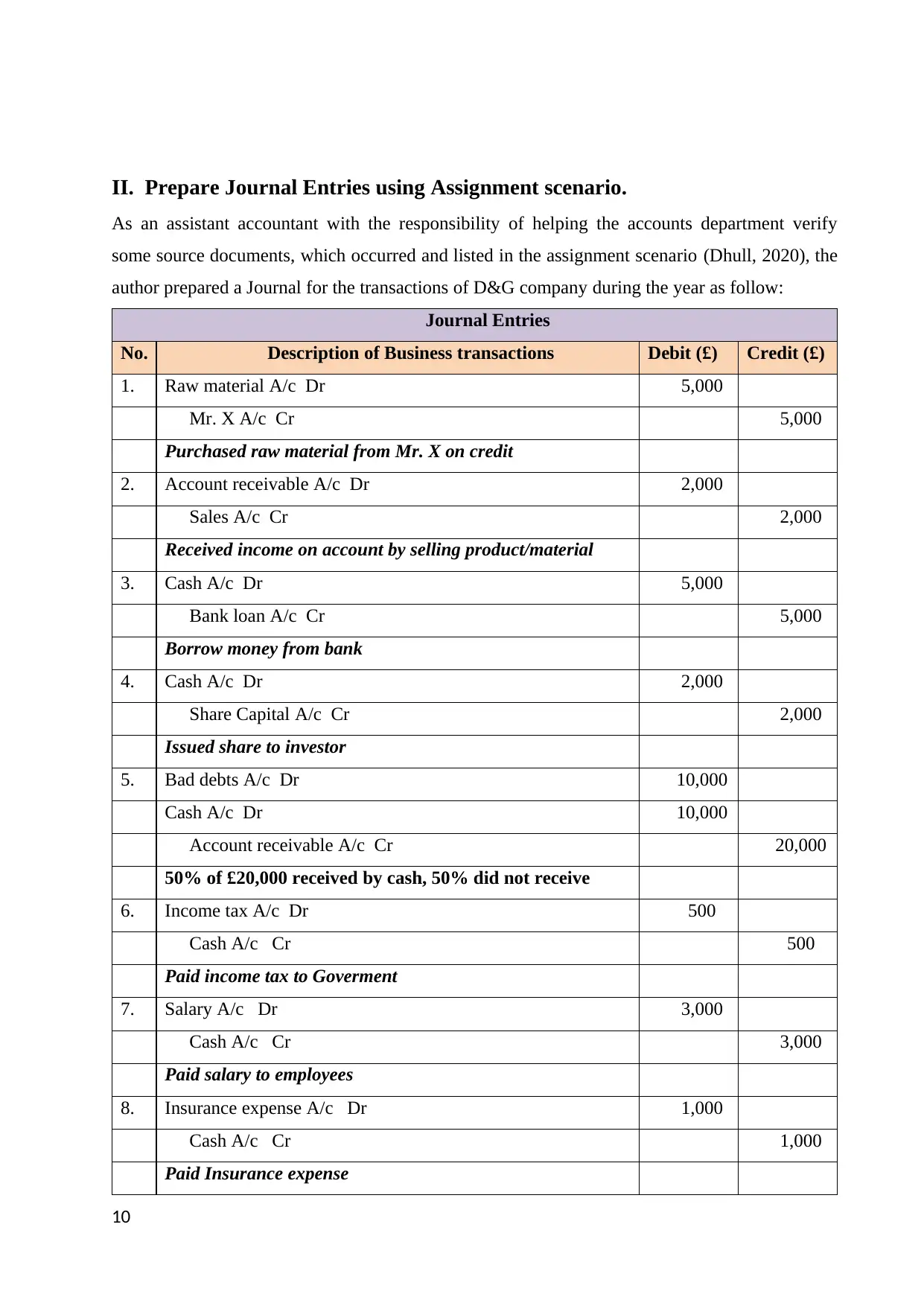

II. Prepare Journal Entries using Assignment scenario.

As an assistant accountant with the responsibility of helping the accounts department verify

some source documents, which occurred and listed in the assignment scenario (Dhull, 2020), the

author prepared a Journal for the transactions of D&G company during the year as follow:

Journal Entries

No. Description of Business transactions Debit (£) Credit (£)

1. Raw material A/c Dr 5,000

Mr. X A/c Cr 5,000

Purchased raw material from Mr. X on credit

2. Account receivable A/c Dr 2,000

Sales A/c Cr 2,000

Received income on account by selling product/material

3. Cash A/c Dr 5,000

Bank loan A/c Cr 5,000

Borrow money from bank

4. Cash A/c Dr 2,000

Share Capital A/c Cr 2,000

Issued share to investor

5. Bad debts A/c Dr 10,000

Cash A/c Dr 10,000

Account receivable A/c Cr 20,000

50% of £20,000 received by cash, 50% did not receive

6. Income tax A/c Dr 500

Cash A/c Cr 500

Paid income tax to Goverment

7. Salary A/c Dr 3,000

Cash A/c Cr 3,000

Paid salary to employees

8. Insurance expense A/c Dr 1,000

Cash A/c Cr 1,000

Paid Insurance expense

10

As an assistant accountant with the responsibility of helping the accounts department verify

some source documents, which occurred and listed in the assignment scenario (Dhull, 2020), the

author prepared a Journal for the transactions of D&G company during the year as follow:

Journal Entries

No. Description of Business transactions Debit (£) Credit (£)

1. Raw material A/c Dr 5,000

Mr. X A/c Cr 5,000

Purchased raw material from Mr. X on credit

2. Account receivable A/c Dr 2,000

Sales A/c Cr 2,000

Received income on account by selling product/material

3. Cash A/c Dr 5,000

Bank loan A/c Cr 5,000

Borrow money from bank

4. Cash A/c Dr 2,000

Share Capital A/c Cr 2,000

Issued share to investor

5. Bad debts A/c Dr 10,000

Cash A/c Dr 10,000

Account receivable A/c Cr 20,000

50% of £20,000 received by cash, 50% did not receive

6. Income tax A/c Dr 500

Cash A/c Cr 500

Paid income tax to Goverment

7. Salary A/c Dr 3,000

Cash A/c Cr 3,000

Paid salary to employees

8. Insurance expense A/c Dr 1,000

Cash A/c Cr 1,000

Paid Insurance expense

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

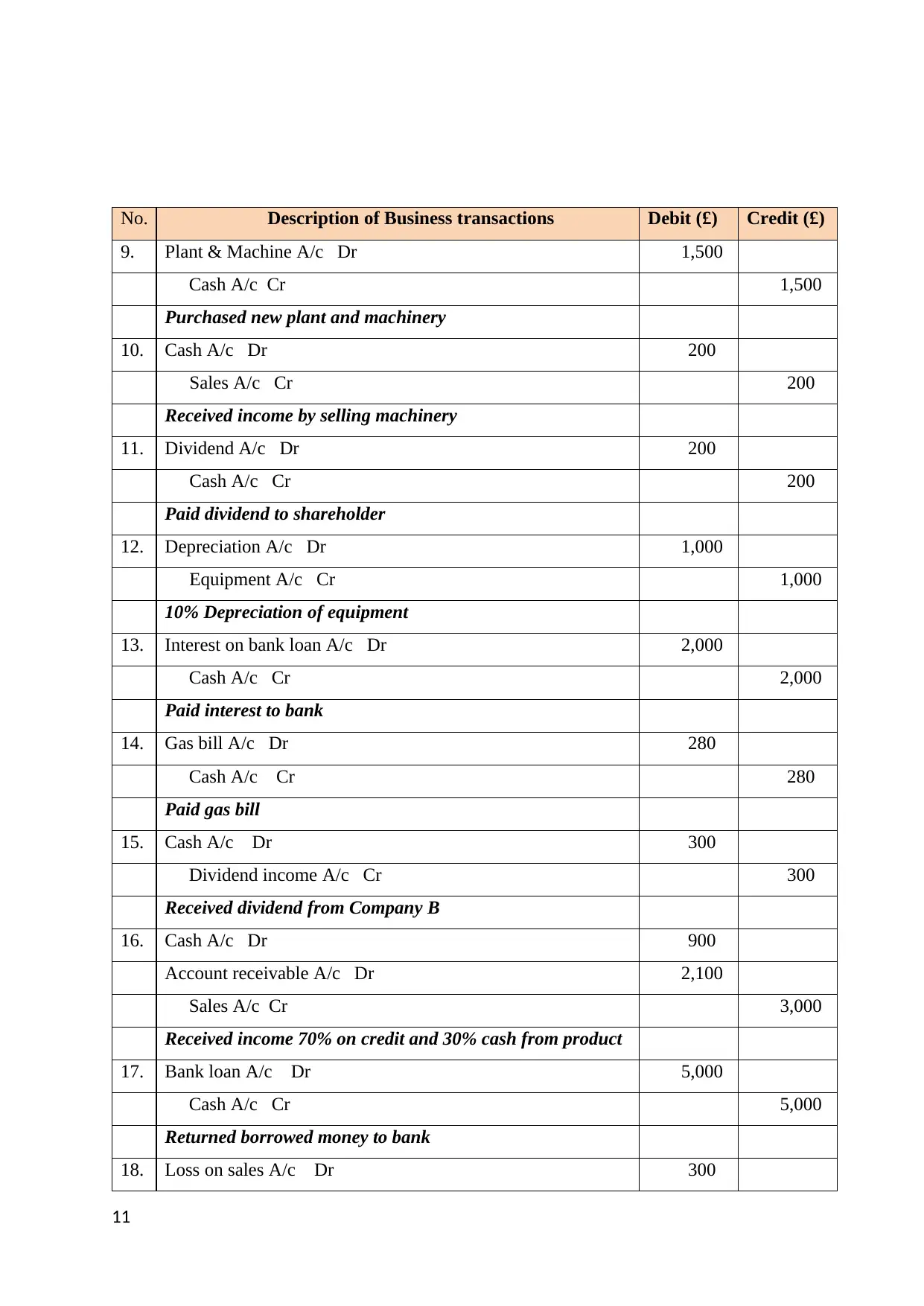

No. Description of Business transactions Debit (£) Credit (£)

9. Plant & Machine A/c Dr 1,500

Cash A/c Cr 1,500

Purchased new plant and machinery

10. Cash A/c Dr 200

Sales A/c Cr 200

Received income by selling machinery

11. Dividend A/c Dr 200

Cash A/c Cr 200

Paid dividend to shareholder

12. Depreciation A/c Dr 1,000

Equipment A/c Cr 1,000

10% Depreciation of equipment

13. Interest on bank loan A/c Dr 2,000

Cash A/c Cr 2,000

Paid interest to bank

14. Gas bill A/c Dr 280

Cash A/c Cr 280

Paid gas bill

15. Cash A/c Dr 300

Dividend income A/c Cr 300

Received dividend from Company B

16. Cash A/c Dr 900

Account receivable A/c Dr 2,100

Sales A/c Cr 3,000

Received income 70% on credit and 30% cash from product

17. Bank loan A/c Dr 5,000

Cash A/c Cr 5,000

Returned borrowed money to bank

18. Loss on sales A/c Dr 300

11

9. Plant & Machine A/c Dr 1,500

Cash A/c Cr 1,500

Purchased new plant and machinery

10. Cash A/c Dr 200

Sales A/c Cr 200

Received income by selling machinery

11. Dividend A/c Dr 200

Cash A/c Cr 200

Paid dividend to shareholder

12. Depreciation A/c Dr 1,000

Equipment A/c Cr 1,000

10% Depreciation of equipment

13. Interest on bank loan A/c Dr 2,000

Cash A/c Cr 2,000

Paid interest to bank

14. Gas bill A/c Dr 280

Cash A/c Cr 280

Paid gas bill

15. Cash A/c Dr 300

Dividend income A/c Cr 300

Received dividend from Company B

16. Cash A/c Dr 900

Account receivable A/c Dr 2,100

Sales A/c Cr 3,000

Received income 70% on credit and 30% cash from product

17. Bank loan A/c Dr 5,000

Cash A/c Cr 5,000

Returned borrowed money to bank

18. Loss on sales A/c Dr 300

11

Machine A/c Cr 300

Sold machine and got loss

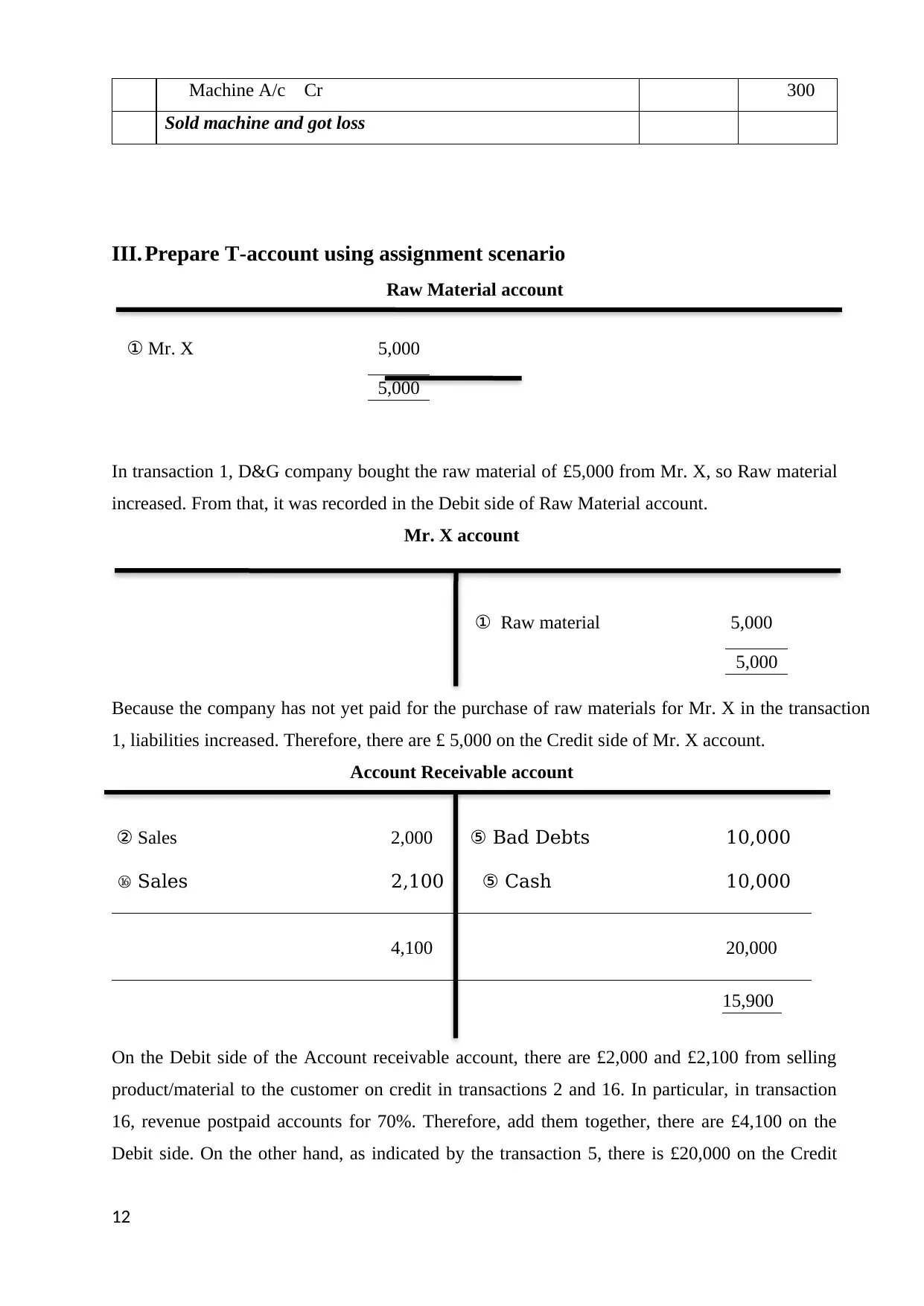

III. Prepare T-account using assignment scenario

Raw Material account

In transaction 1, D&G company bought the raw material of £5,000 from Mr. X, so Raw material

increased. From that, it was recorded in the Debit side of Raw Material account.

Mr. X account

① Raw material 5,000

Because the company has not yet paid for the purchase of raw materials for Mr. X in the transaction

1, liabilities increased. Therefore, there are £ 5,000 on the Credit side of Mr. X account.

Account Receivable account

② Sales 2,000 ⑤ Bad Debts 10,000

Sales⑯ 2,100 ⑤ Cash 10,000

4,100 20,000

On the Debit side of the Account receivable account, there are £2,000 and £2,100 from selling

product/material to the customer on credit in transactions 2 and 16. In particular, in transaction

16, revenue postpaid accounts for 70%. Therefore, add them together, there are £4,100 on the

Debit side. On the other hand, as indicated by the transaction 5, there is £20,000 on the Credit

12

① Mr. X 5,000

5,000

5,000

15,900

Sold machine and got loss

III. Prepare T-account using assignment scenario

Raw Material account

In transaction 1, D&G company bought the raw material of £5,000 from Mr. X, so Raw material

increased. From that, it was recorded in the Debit side of Raw Material account.

Mr. X account

① Raw material 5,000

Because the company has not yet paid for the purchase of raw materials for Mr. X in the transaction

1, liabilities increased. Therefore, there are £ 5,000 on the Credit side of Mr. X account.

Account Receivable account

② Sales 2,000 ⑤ Bad Debts 10,000

Sales⑯ 2,100 ⑤ Cash 10,000

4,100 20,000

On the Debit side of the Account receivable account, there are £2,000 and £2,100 from selling

product/material to the customer on credit in transactions 2 and 16. In particular, in transaction

16, revenue postpaid accounts for 70%. Therefore, add them together, there are £4,100 on the

Debit side. On the other hand, as indicated by the transaction 5, there is £20,000 on the Credit

12

① Mr. X 5,000

5,000

5,000

15,900

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 33

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.