HSA525 Week 4: CVP Analysis for CAM Alternatives at Benson Medical

VerifiedAdded on 2022/08/16

MANAGEMENT

Paraphrase This Document

• Benson Regional Medical center has been finding the opportunities

for incorporating more alternative and complementary medicines.

• This goal become possible after federal grant has been awarded

from Nation Center for the Integrative and Complementary Health.

• Despite of the western trained skepticism providers of the non-

traditional therapies or medicines forms, there has been increasing

body of the evidence for supporting combinations of the

conventional and complementary medical therapeutic interventions.

• Hence, for the consumers, complementary medicine is

considered to be less expensive compared to conventional

treatment, as it is attractive for the patients who have tried

more approaches of traditional treatment with no or limited

success and it is having easy accessibility.

• The analysis of cost volume profit has been done for

determining breakeven points of sales and volume for three

alternatives of CAM, which are yoga therapy, biofeedback and

acupuncture.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

• Acupuncture is the first alternative. It is ancient process that is rooted in

the Eastern medicine, in which solid and thin needles are inserted in

body strategically and it is manipulated carefully by practitioner.

• Biofeedback is the second alternative. In this, power of mind is

harnessed by patients and become aware of the things going inside their

body for gaining more control over health.

• Yoga therapy is last alternative. It encourages integration of spirit, body

and mind for improving physical and mental health (Finkler, Smith &

Calabrese, 2018).

Paraphrase This Document

• These alternatives are having objectives for helping the

patients for finding relief from the chronic lower discomfort of

back, when interventions of more conventional medical

treatment falls short of the expectations.

• Each approach of CAM has been effective in the management

of chronic lower pain of back for the clients. It is considered

to be safe, when it is performed by licensed or certified

practitioners (Jones et al. 2018).

• Intangible benefits are associated with each of the therapy.

• There are various patients who have reported for being pain

free after years of the intolerable discomfort.

• The others have reported that they are being able for

resuming work and leisure related activities, which were not

possible because of back pain before receiving alternative

and complementary medical interventions (Jones et al. 2018).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

• For the decision regarding recommendation for the finding,

identification of the relevant cost linked with each

alternatives on annual and per client basis and development

of financial assumptions are required.

• For the purpose of CVP, semi-fixed costs are considered to be

FC.

• For CVP and CEA, VC consists of patient consumable supplies

and education materials used in provision of the care

(Cleverley & Cleverley, 2017).

Paraphrase This Document

• There is assumption that integrative and complementary health service line will

incorporate chosen CAM into the existing services. It will be having 160 clients for

first year of operation.

• It is assumed that provider will be contracted with Center and expected for

dedicating total of 10 hours per week at Centre providing care to clients.

• There is the assumption that provider will be available for only 50 weeks per year.

• There will be allocation of 2 hours per week of the one clerical worker for assisting in

scheduling, ensuring the availability of patient education materials, coordination of

required resources for meeting needs of clients and placing follow-up with the

clients (Kaplan et al. 2014).

• For the alternative of spinal manipulation, there would be

requirement of retaining services of outside Radiologist for

reading radiographs, which was estimated for taking 1 hour

per week.

• There would be requirement of X-ray Technicians for taking

radiographs and sending it to the radiographs.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

• Center will employ the technicians and this particular would

not be consuming more than an hour per week.

• There is the assumption that each of the alternatives will be

providing significant patient education materials on routine

basis for the clients and its cost would vary based on market

value of these particular collaterals (Neumann et al. 2016).

Paraphrase This Document

• The clients would be receiving 5 significant broches at the amount

of $.61 apiece.

• The clients would be receiving single trifold brochure for the

therapy of biofeedback.

• The service of acupuncture would be providing 3 separate

brochures at the unit price of amount $7 apiece for First visit and

Q&A brochure and amount of $6.50 for steps of the care brochure

(Cleverley & Cleverley, 2017).

• For completing analysis of CVP for each alternatives of CAM, there are requirements

of price per unit, VC per UOS, total variable cost, annual FC, total fixed cost per

year, unit contribution margin and contribution ratio.

• For the calculation of FC, hourly rate of the compensation is multiplied by number of

the hours dedicated to clients per week.

• For determining TFC per year, annual compensation for each alternatives are added

for each alternatives.

• For calculating VC for each alternatives, brochures unit cost and consumable

supplies are multiplied by anticipated total number of the clients in given year (Bem

et al. 2014).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

• For calculating TC, VC are added for consumable supplies and the brochures for each of the

alternatives.

• For determining VC per patients, TVC is divided by total number of the patients in given

period of time.

• The estimation of price per patient is by taking national average for each of the considered

alternatives.

• Unit CM is calculated by subtracting VC per UOS from price per UOS.

• For the calculation of CM ratio, unit CM is divided by price per UOS.

• The calculation of CVP breakeven point in sales, TFC is divided by CM ratio.

• The calculation of CVP breakeven point in UOS, TFC is divided by Unit CM.

Paraphrase This Document

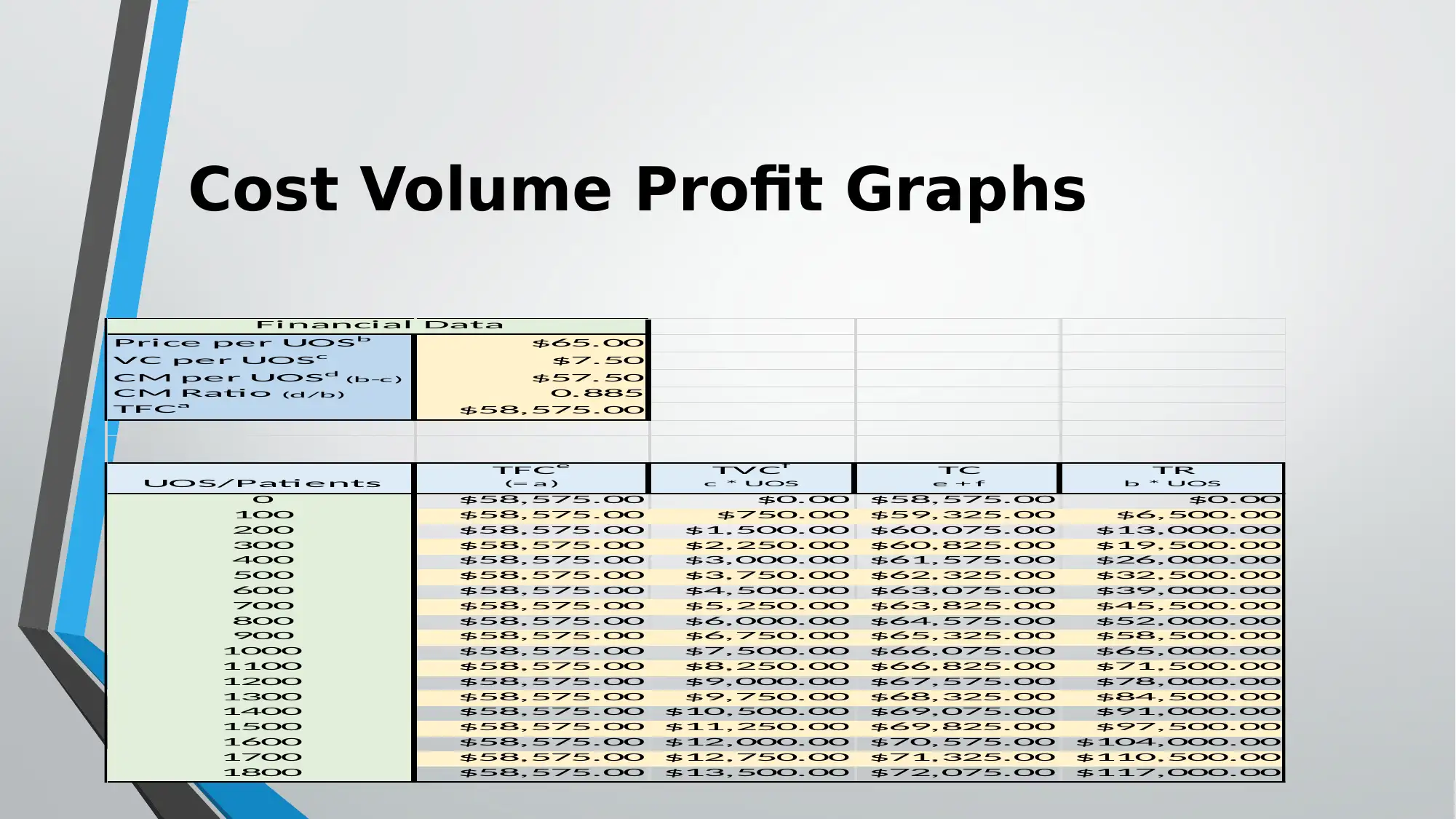

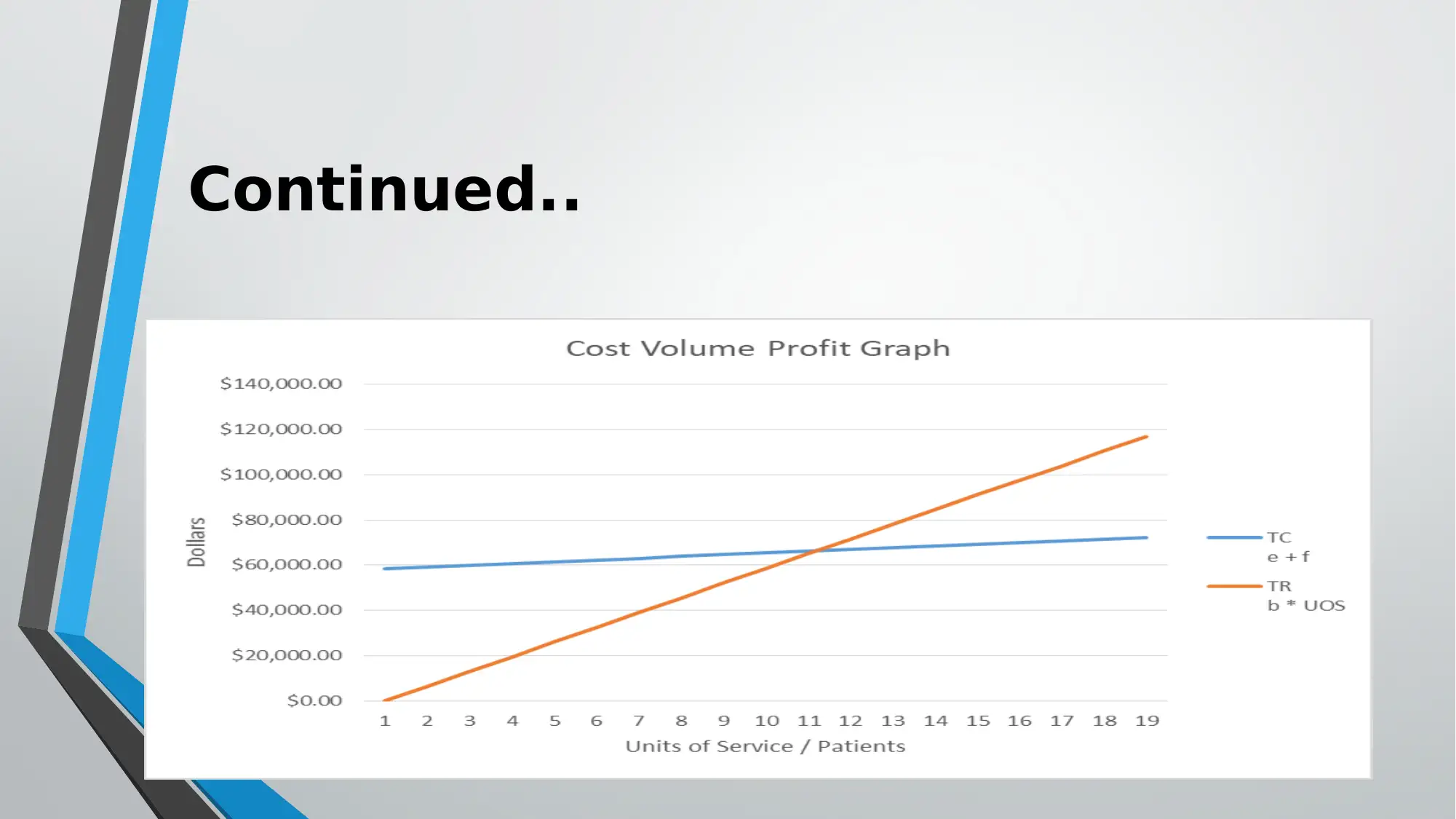

Price per UOS b $65.00

VC per UOS c $7.50

CM per UOS d (b-c) $57.50

CM Ratio (d/b) 0.885

TFC a $58,575.00

UOS/Patients

TFC e

(= a)

TVC f

c * UOS

TC

e + f

TR

b * UOS

0 $58,575.00 $0.00 $58,575.00 $0.00

100 $58,575.00 $750.00 $59,325.00 $6,500.00

200 $58,575.00 $1,500.00 $60,075.00 $13,000.00

300 $58,575.00 $2,250.00 $60,825.00 $19,500.00

400 $58,575.00 $3,000.00 $61,575.00 $26,000.00

500 $58,575.00 $3,750.00 $62,325.00 $32,500.00

600 $58,575.00 $4,500.00 $63,075.00 $39,000.00

700 $58,575.00 $5,250.00 $63,825.00 $45,500.00

800 $58,575.00 $6,000.00 $64,575.00 $52,000.00

900 $58,575.00 $6,750.00 $65,325.00 $58,500.00

1000 $58,575.00 $7,500.00 $66,075.00 $65,000.00

1100 $58,575.00 $8,250.00 $66,825.00 $71,500.00

1200 $58,575.00 $9,000.00 $67,575.00 $78,000.00

1300 $58,575.00 $9,750.00 $68,325.00 $84,500.00

1400 $58,575.00 $10,500.00 $69,075.00 $91,000.00

1500 $58,575.00 $11,250.00 $69,825.00 $97,500.00

1600 $58,575.00 $12,000.00 $70,575.00 $104,000.00

1700 $58,575.00 $12,750.00 $71,325.00 $110,500.00

1800 $58,575.00 $13,500.00 $72,075.00 $117,000.00

Financial Data

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

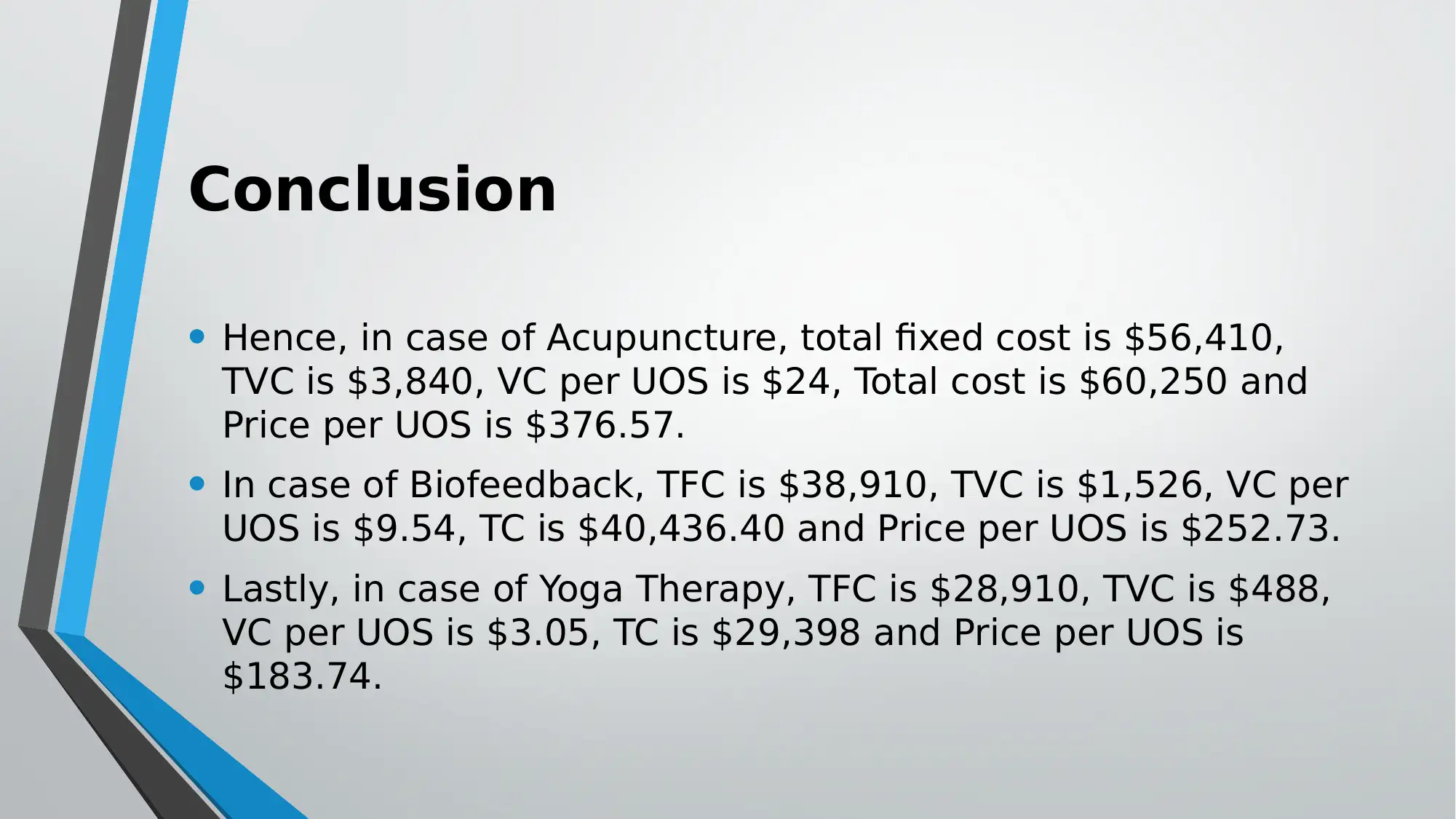

• Hence, in case of Acupuncture, total fixed cost is $56,410,

TVC is $3,840, VC per UOS is $24, Total cost is $60,250 and

Price per UOS is $376.57.

• In case of Biofeedback, TFC is $38,910, TVC is $1,526, VC per

UOS is $9.54, TC is $40,436.40 and Price per UOS is $252.73.

• Lastly, in case of Yoga Therapy, TFC is $28,910, TVC is $488,

VC per UOS is $3.05, TC is $29,398 and Price per UOS is

$183.74.

Paraphrase This Document

• Bem, A., Prędkiewicz, K., Prędkiewicz, P., & Ucieklak-Jeż, P. (2014). Determinants of Hospital's Financial

Liquidity. Procedia Economics and Finance, 12, 27-36.

• Cleverley, W. O., & Cleverley, J. O. (2017). Essentials of health care finance. Jones & Bartlett Learning.

• Finkler, S. A., Smith, D. L., & Calabrese, T. D. (2018). Financial management for public, health, and not-for-

profit organizations. CQ Press.

• Jones, C., Finkler, S. A., Kovner, C. T., & Mose, J. (2018). Financial Management for Nurse Managers and

Executives-E-Book. Elsevier Health Sciences.

• Kaplan, R. S., Witkowski, M., Abbott, M., Guzman, A. B., Higgins, L. D., Meara, J. G., ... & Wertheimer, S.

(2014). Using time-driven activity-based costing to identify value improvement opportunities in

healthcare. Journal of Healthcare Management, 59(6), 399-412.

• Neumann, P. J., Sanders, G. D., Russell, L. B., Siegel, J. E., & Ganiats, T. G. (Eds.). (2016). Cost-

effectiveness in health and medicine. Oxford University Press.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

© 2024 | Zucol Services PVT LTD | All rights reserved.