Health Services Resource Management.

VerifiedAdded on 2022/11/23

|13

|1815

|54

AI Summary

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running Head: Health Services Resource Management

Health Services Resource Management

Assignment 1

Student Name

Health Services Resource Management

Assignment 1

Student Name

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Health Services Resource Management

Question 1:

(a)

Balance-sheet

2,015 2,014

Assets

Current-Assets

Short term receivables 11,80,862 13,10,776

Cash and Cash Equivalents 45,36,985 31,27,657

Inventories of drugs 40,139 34,333

Other Current Assets 20,428 1,08,328

Total Current-Assets 57,78,414 45,81,094

Non-Current Assets

Long term receivables 87,767 36,478

Motor vehicles 2,000 2,000

Property, Plant & Equipment 82,93,627 89,59,514

Total Non- Current Assets 83,83,394 89,97,992

Total Assets 1,41,61,808 1,35,79,086

Liabilities

Current-Liabilities

Short-term payables 3,26,708 6,98,129

Short term staff benefits 10,99,853 9,09,310

Other current liabilities 38,69,052 27,53,096

Total Current-liabilities 52,95,613 43,60,535

Non-Current Liabilities

Long term loans 2,40,877 1,74,900

Total Current-liabilities 2,40,877 1,74,900

Total Liabilities 55,36,490 45,35,435

1

Question 1:

(a)

Balance-sheet

2,015 2,014

Assets

Current-Assets

Short term receivables 11,80,862 13,10,776

Cash and Cash Equivalents 45,36,985 31,27,657

Inventories of drugs 40,139 34,333

Other Current Assets 20,428 1,08,328

Total Current-Assets 57,78,414 45,81,094

Non-Current Assets

Long term receivables 87,767 36,478

Motor vehicles 2,000 2,000

Property, Plant & Equipment 82,93,627 89,59,514

Total Non- Current Assets 83,83,394 89,97,992

Total Assets 1,41,61,808 1,35,79,086

Liabilities

Current-Liabilities

Short-term payables 3,26,708 6,98,129

Short term staff benefits 10,99,853 9,09,310

Other current liabilities 38,69,052 27,53,096

Total Current-liabilities 52,95,613 43,60,535

Non-Current Liabilities

Long term loans 2,40,877 1,74,900

Total Current-liabilities 2,40,877 1,74,900

Total Liabilities 55,36,490 45,35,435

1

Health Services Resource Management

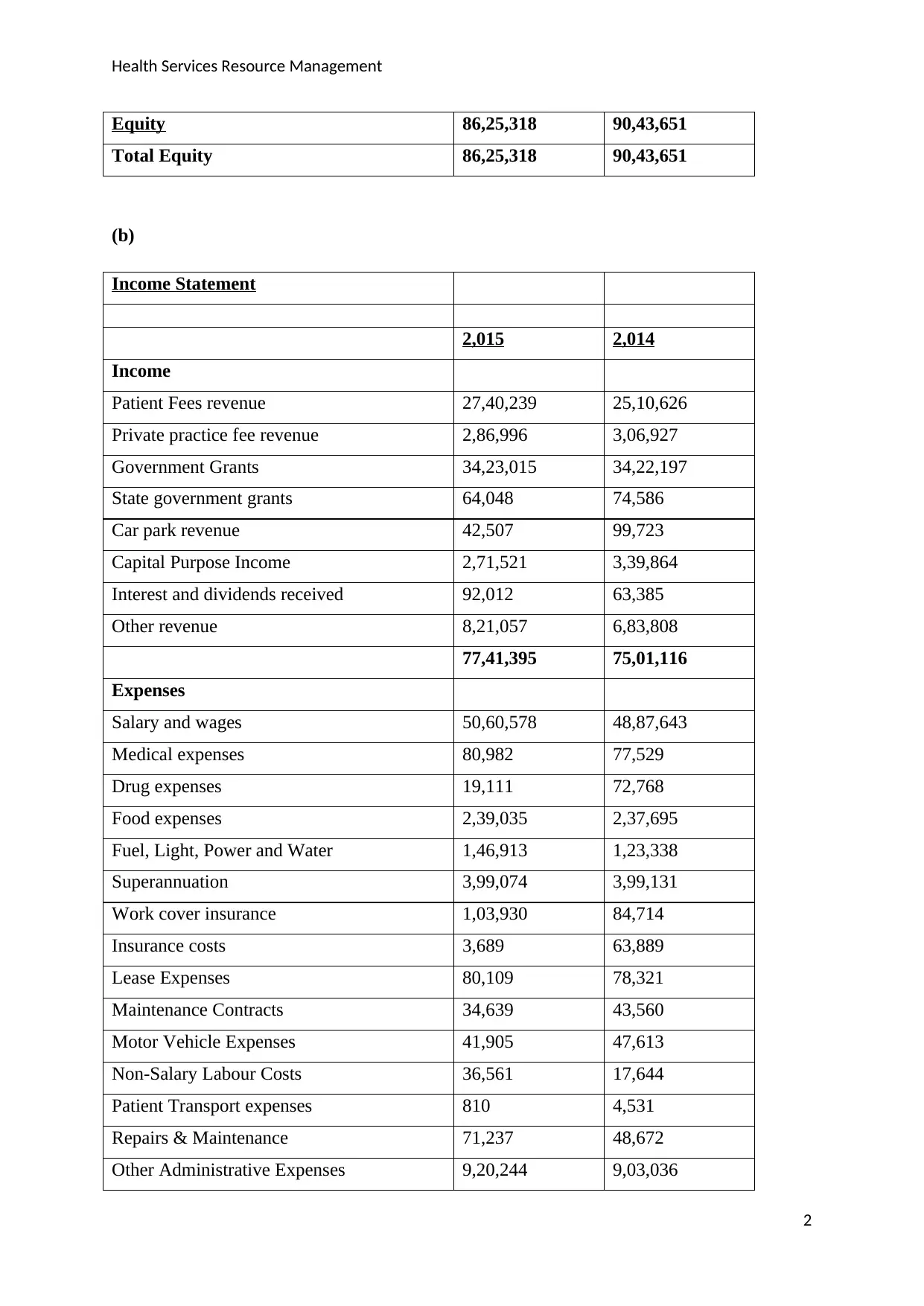

Equity 86,25,318 90,43,651

Total Equity 86,25,318 90,43,651

(b)

Income Statement

2,015 2,014

Income

Patient Fees revenue 27,40,239 25,10,626

Private practice fee revenue 2,86,996 3,06,927

Government Grants 34,23,015 34,22,197

State government grants 64,048 74,586

Car park revenue 42,507 99,723

Capital Purpose Income 2,71,521 3,39,864

Interest and dividends received 92,012 63,385

Other revenue 8,21,057 6,83,808

77,41,395 75,01,116

Expenses

Salary and wages 50,60,578 48,87,643

Medical expenses 80,982 77,529

Drug expenses 19,111 72,768

Food expenses 2,39,035 2,37,695

Fuel, Light, Power and Water 1,46,913 1,23,338

Superannuation 3,99,074 3,99,131

Work cover insurance 1,03,930 84,714

Insurance costs 3,689 63,889

Lease Expenses 80,109 78,321

Maintenance Contracts 34,639 43,560

Motor Vehicle Expenses 41,905 47,613

Non-Salary Labour Costs 36,561 17,644

Patient Transport expenses 810 4,531

Repairs & Maintenance 71,237 48,672

Other Administrative Expenses 9,20,244 9,03,036

2

Equity 86,25,318 90,43,651

Total Equity 86,25,318 90,43,651

(b)

Income Statement

2,015 2,014

Income

Patient Fees revenue 27,40,239 25,10,626

Private practice fee revenue 2,86,996 3,06,927

Government Grants 34,23,015 34,22,197

State government grants 64,048 74,586

Car park revenue 42,507 99,723

Capital Purpose Income 2,71,521 3,39,864

Interest and dividends received 92,012 63,385

Other revenue 8,21,057 6,83,808

77,41,395 75,01,116

Expenses

Salary and wages 50,60,578 48,87,643

Medical expenses 80,982 77,529

Drug expenses 19,111 72,768

Food expenses 2,39,035 2,37,695

Fuel, Light, Power and Water 1,46,913 1,23,338

Superannuation 3,99,074 3,99,131

Work cover insurance 1,03,930 84,714

Insurance costs 3,689 63,889

Lease Expenses 80,109 78,321

Maintenance Contracts 34,639 43,560

Motor Vehicle Expenses 41,905 47,613

Non-Salary Labour Costs 36,561 17,644

Patient Transport expenses 810 4,531

Repairs & Maintenance 71,237 48,672

Other Administrative Expenses 9,20,244 9,03,036

2

Health Services Resource Management

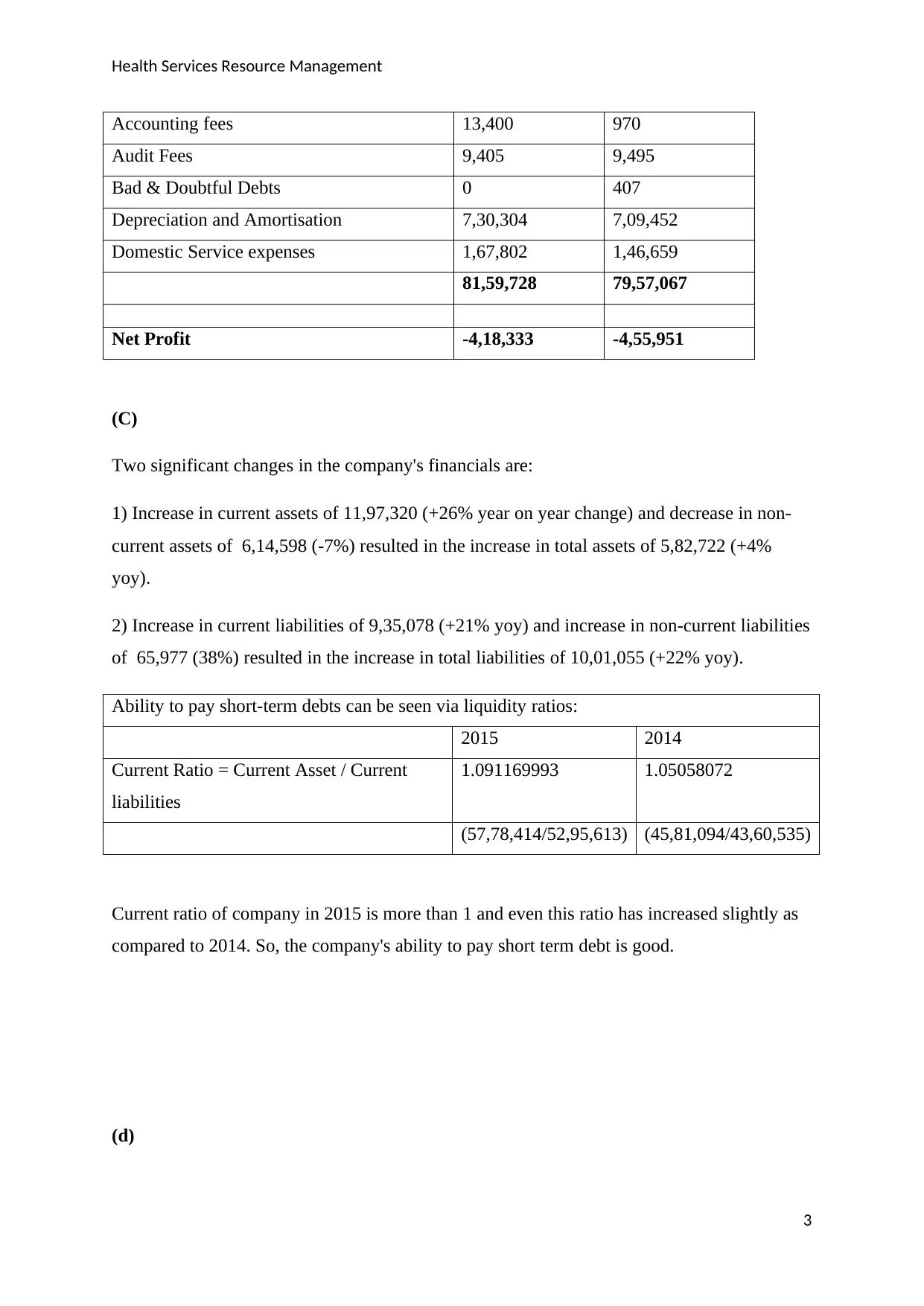

Accounting fees 13,400 970

Audit Fees 9,405 9,495

Bad & Doubtful Debts 0 407

Depreciation and Amortisation 7,30,304 7,09,452

Domestic Service expenses 1,67,802 1,46,659

81,59,728 79,57,067

Net Profit -4,18,333 -4,55,951

(C)

Two significant changes in the company's financials are:

1) Increase in current assets of 11,97,320 (+26% year on year change) and decrease in non-

current assets of 6,14,598 (-7%) resulted in the increase in total assets of 5,82,722 (+4%

yoy).

2) Increase in current liabilities of 9,35,078 (+21% yoy) and increase in non-current liabilities

of 65,977 (38%) resulted in the increase in total liabilities of 10,01,055 (+22% yoy).

Ability to pay short-term debts can be seen via liquidity ratios:

2015 2014

Current Ratio = Current Asset / Current

liabilities

1.091169993 1.05058072

(57,78,414/52,95,613) (45,81,094/43,60,535)

Current ratio of company in 2015 is more than 1 and even this ratio has increased slightly as

compared to 2014. So, the company's ability to pay short term debt is good.

(d)

3

Accounting fees 13,400 970

Audit Fees 9,405 9,495

Bad & Doubtful Debts 0 407

Depreciation and Amortisation 7,30,304 7,09,452

Domestic Service expenses 1,67,802 1,46,659

81,59,728 79,57,067

Net Profit -4,18,333 -4,55,951

(C)

Two significant changes in the company's financials are:

1) Increase in current assets of 11,97,320 (+26% year on year change) and decrease in non-

current assets of 6,14,598 (-7%) resulted in the increase in total assets of 5,82,722 (+4%

yoy).

2) Increase in current liabilities of 9,35,078 (+21% yoy) and increase in non-current liabilities

of 65,977 (38%) resulted in the increase in total liabilities of 10,01,055 (+22% yoy).

Ability to pay short-term debts can be seen via liquidity ratios:

2015 2014

Current Ratio = Current Asset / Current

liabilities

1.091169993 1.05058072

(57,78,414/52,95,613) (45,81,094/43,60,535)

Current ratio of company in 2015 is more than 1 and even this ratio has increased slightly as

compared to 2014. So, the company's ability to pay short term debt is good.

(d)

3

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Health Services Resource Management

Cash-flow statement

4

Cash-flow statement

4

Health Services Resource Management

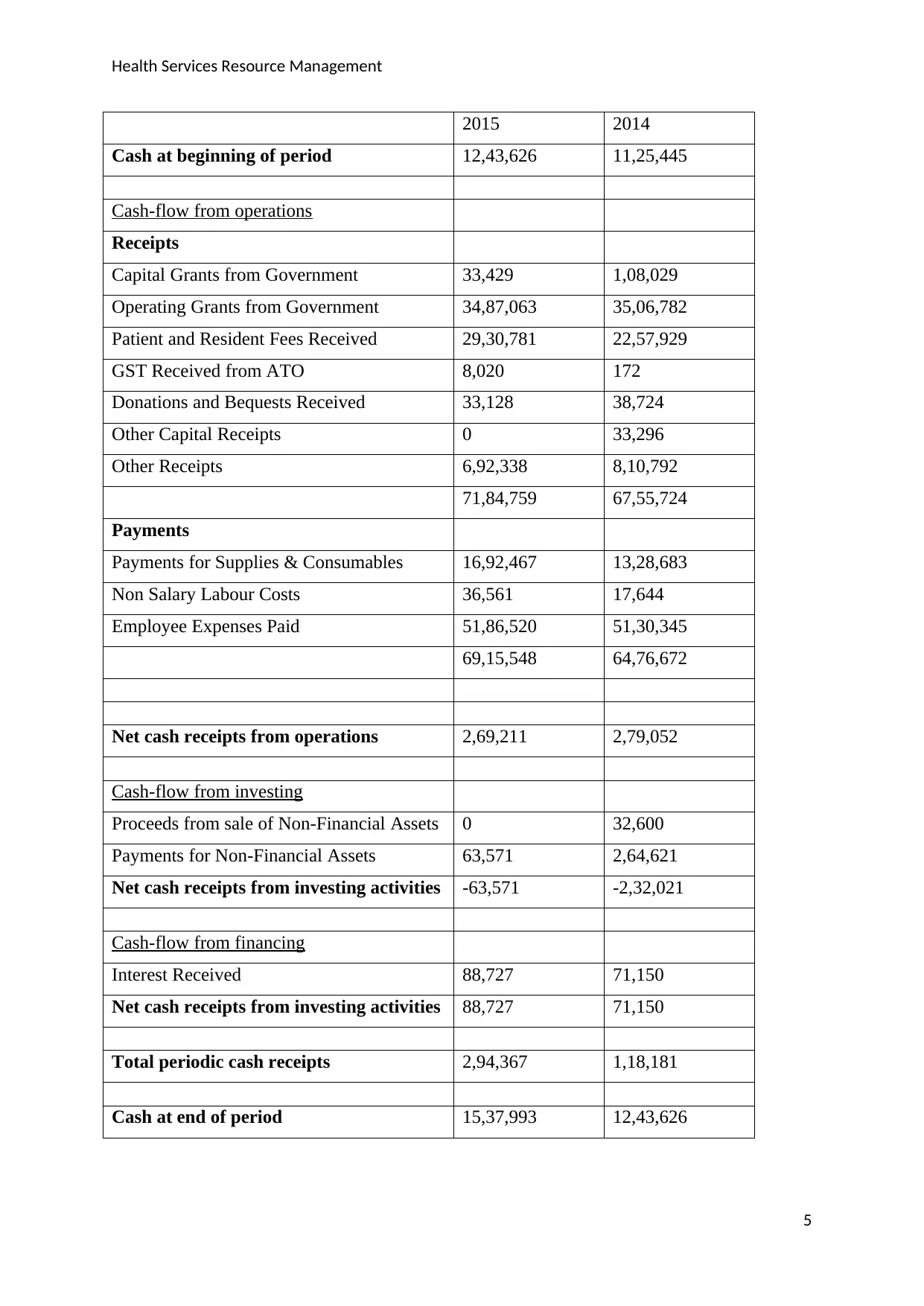

2015 2014

Cash at beginning of period 12,43,626 11,25,445

Cash-flow from operations

Receipts

Capital Grants from Government 33,429 1,08,029

Operating Grants from Government 34,87,063 35,06,782

Patient and Resident Fees Received 29,30,781 22,57,929

GST Received from ATO 8,020 172

Donations and Bequests Received 33,128 38,724

Other Capital Receipts 0 33,296

Other Receipts 6,92,338 8,10,792

71,84,759 67,55,724

Payments

Payments for Supplies & Consumables 16,92,467 13,28,683

Non Salary Labour Costs 36,561 17,644

Employee Expenses Paid 51,86,520 51,30,345

69,15,548 64,76,672

Net cash receipts from operations 2,69,211 2,79,052

Cash-flow from investing

Proceeds from sale of Non-Financial Assets 0 32,600

Payments for Non-Financial Assets 63,571 2,64,621

Net cash receipts from investing activities -63,571 -2,32,021

Cash-flow from financing

Interest Received 88,727 71,150

Net cash receipts from investing activities 88,727 71,150

Total periodic cash receipts 2,94,367 1,18,181

Cash at end of period 15,37,993 12,43,626

5

2015 2014

Cash at beginning of period 12,43,626 11,25,445

Cash-flow from operations

Receipts

Capital Grants from Government 33,429 1,08,029

Operating Grants from Government 34,87,063 35,06,782

Patient and Resident Fees Received 29,30,781 22,57,929

GST Received from ATO 8,020 172

Donations and Bequests Received 33,128 38,724

Other Capital Receipts 0 33,296

Other Receipts 6,92,338 8,10,792

71,84,759 67,55,724

Payments

Payments for Supplies & Consumables 16,92,467 13,28,683

Non Salary Labour Costs 36,561 17,644

Employee Expenses Paid 51,86,520 51,30,345

69,15,548 64,76,672

Net cash receipts from operations 2,69,211 2,79,052

Cash-flow from investing

Proceeds from sale of Non-Financial Assets 0 32,600

Payments for Non-Financial Assets 63,571 2,64,621

Net cash receipts from investing activities -63,571 -2,32,021

Cash-flow from financing

Interest Received 88,727 71,150

Net cash receipts from investing activities 88,727 71,150

Total periodic cash receipts 2,94,367 1,18,181

Cash at end of period 15,37,993 12,43,626

5

Health Services Resource Management

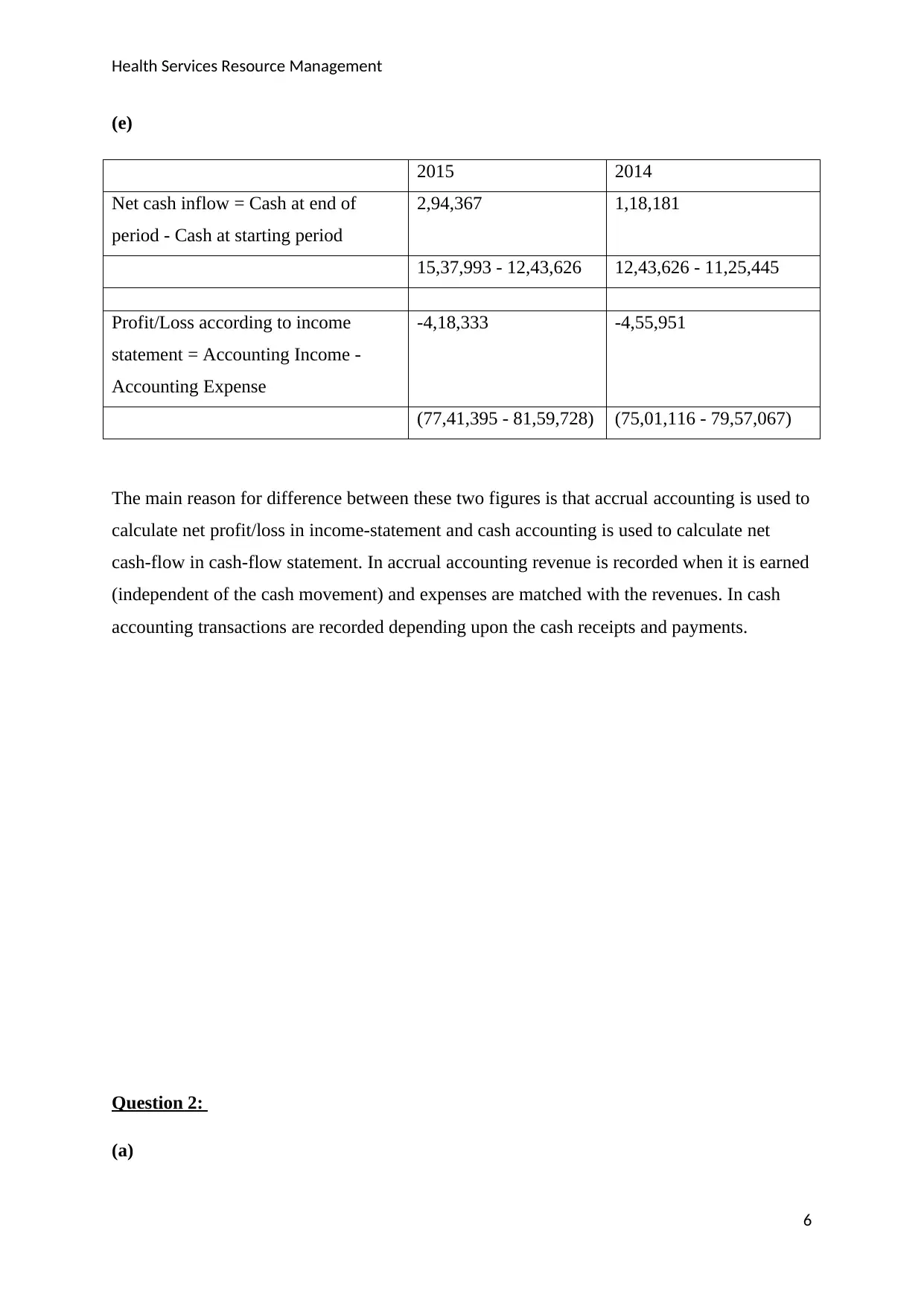

(e)

2015 2014

Net cash inflow = Cash at end of

period - Cash at starting period

2,94,367 1,18,181

15,37,993 - 12,43,626 12,43,626 - 11,25,445

Profit/Loss according to income

statement = Accounting Income -

Accounting Expense

-4,18,333 -4,55,951

(77,41,395 - 81,59,728) (75,01,116 - 79,57,067)

The main reason for difference between these two figures is that accrual accounting is used to

calculate net profit/loss in income-statement and cash accounting is used to calculate net

cash-flow in cash-flow statement. In accrual accounting revenue is recorded when it is earned

(independent of the cash movement) and expenses are matched with the revenues. In cash

accounting transactions are recorded depending upon the cash receipts and payments.

Question 2:

(a)

6

(e)

2015 2014

Net cash inflow = Cash at end of

period - Cash at starting period

2,94,367 1,18,181

15,37,993 - 12,43,626 12,43,626 - 11,25,445

Profit/Loss according to income

statement = Accounting Income -

Accounting Expense

-4,18,333 -4,55,951

(77,41,395 - 81,59,728) (75,01,116 - 79,57,067)

The main reason for difference between these two figures is that accrual accounting is used to

calculate net profit/loss in income-statement and cash accounting is used to calculate net

cash-flow in cash-flow statement. In accrual accounting revenue is recorded when it is earned

(independent of the cash movement) and expenses are matched with the revenues. In cash

accounting transactions are recorded depending upon the cash receipts and payments.

Question 2:

(a)

6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Health Services Resource Management

March

7

March

7

Health Services Resource Management

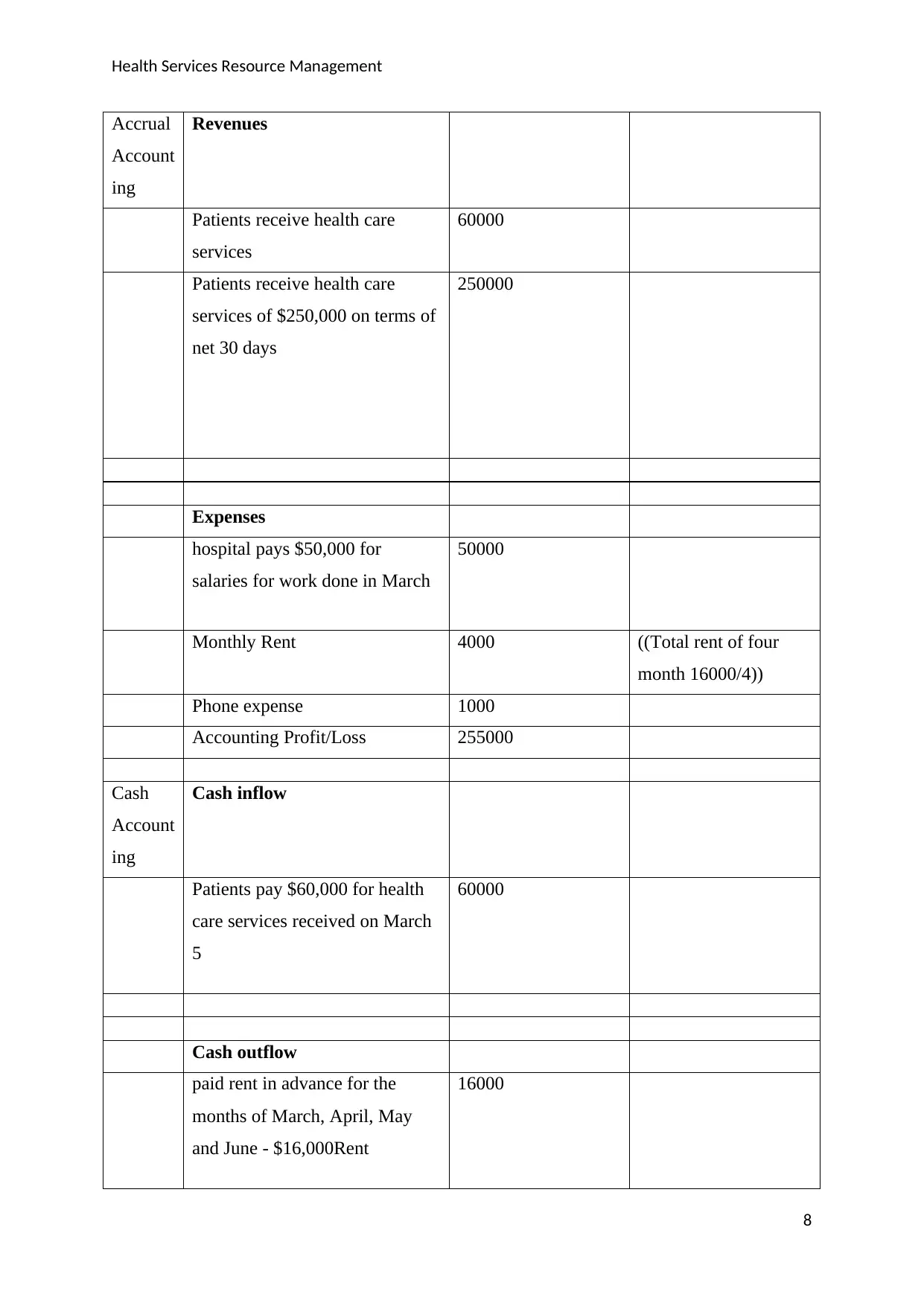

Accrual

Account

ing

Revenues

Patients receive health care

services

60000

Patients receive health care

services of $250,000 on terms of

net 30 days

250000

Expenses

hospital pays $50,000 for

salaries for work done in March

50000

Monthly Rent 4000 ((Total rent of four

month 16000/4))

Phone expense 1000

Accounting Profit/Loss 255000

Cash

Account

ing

Cash inflow

Patients pay $60,000 for health

care services received on March

5

60000

Cash outflow

paid rent in advance for the

months of March, April, May

and June - $16,000Rent

16000

8

Accrual

Account

ing

Revenues

Patients receive health care

services

60000

Patients receive health care

services of $250,000 on terms of

net 30 days

250000

Expenses

hospital pays $50,000 for

salaries for work done in March

50000

Monthly Rent 4000 ((Total rent of four

month 16000/4))

Phone expense 1000

Accounting Profit/Loss 255000

Cash

Account

ing

Cash inflow

Patients pay $60,000 for health

care services received on March

5

60000

Cash outflow

paid rent in advance for the

months of March, April, May

and June - $16,000Rent

16000

8

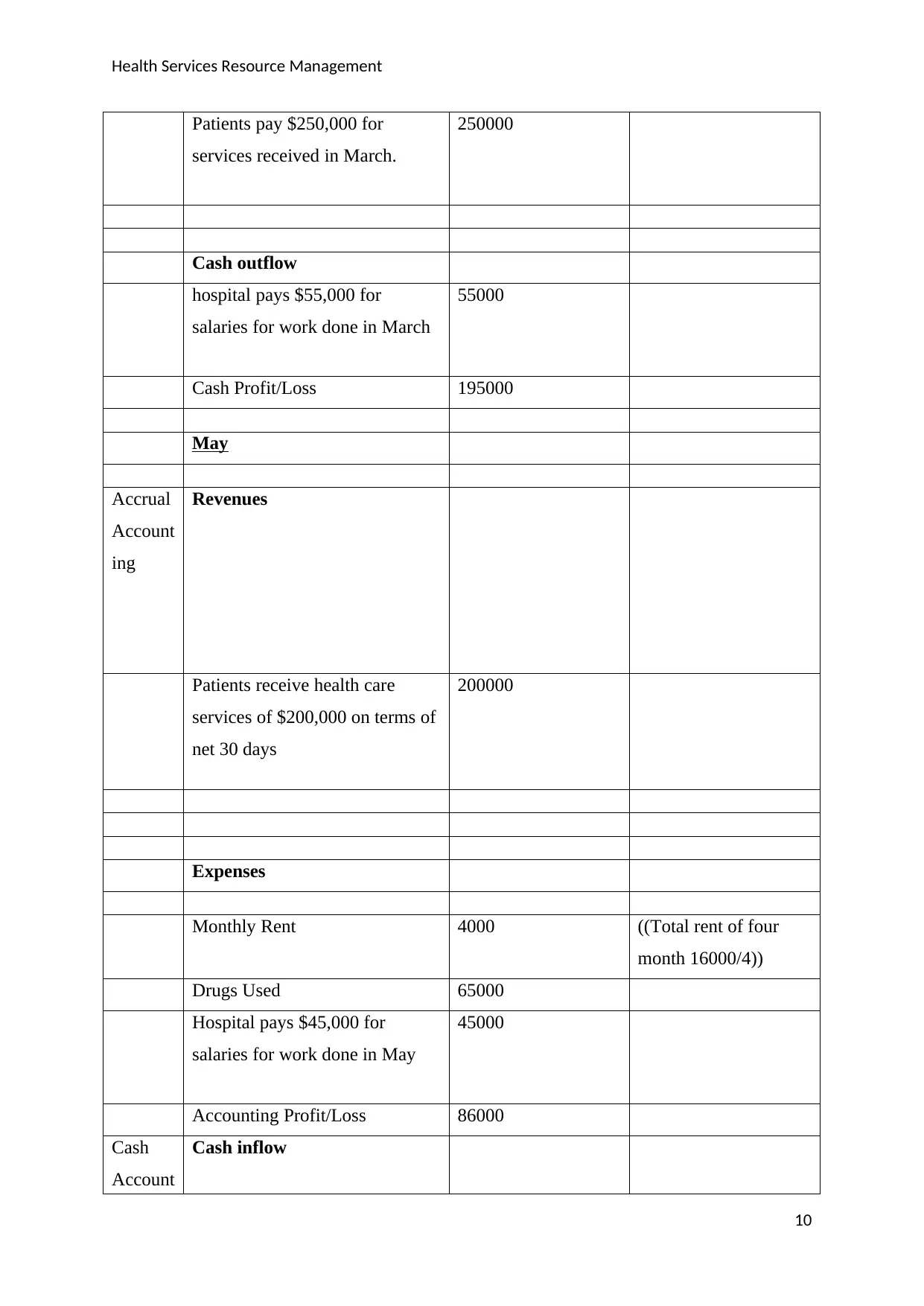

Health Services Resource Management

hospital pays $50,000 for

salaries for work done in March

50000

Cash Profit/Loss -6000

April

Accrual

Account

ing

Revenues

Patients receive health care

services of $250,000 on terms of

net 30 days

250000

Expenses

Monthly Rent 4000 ((Total rent of four

month 16000/4))

Drugs Used 35000

hospital pays $55,000 for

salaries for work done in March

55000

Accounting Profit/Loss 156000

Cash

Account

ing

Cash inflow

9

hospital pays $50,000 for

salaries for work done in March

50000

Cash Profit/Loss -6000

April

Accrual

Account

ing

Revenues

Patients receive health care

services of $250,000 on terms of

net 30 days

250000

Expenses

Monthly Rent 4000 ((Total rent of four

month 16000/4))

Drugs Used 35000

hospital pays $55,000 for

salaries for work done in March

55000

Accounting Profit/Loss 156000

Cash

Account

ing

Cash inflow

9

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Health Services Resource Management

Patients pay $250,000 for

services received in March.

250000

Cash outflow

hospital pays $55,000 for

salaries for work done in March

55000

Cash Profit/Loss 195000

May

Accrual

Account

ing

Revenues

Patients receive health care

services of $200,000 on terms of

net 30 days

200000

Expenses

Monthly Rent 4000 ((Total rent of four

month 16000/4))

Drugs Used 65000

Hospital pays $45,000 for

salaries for work done in May

45000

Accounting Profit/Loss 86000

Cash

Account

Cash inflow

10

Patients pay $250,000 for

services received in March.

250000

Cash outflow

hospital pays $55,000 for

salaries for work done in March

55000

Cash Profit/Loss 195000

May

Accrual

Account

ing

Revenues

Patients receive health care

services of $200,000 on terms of

net 30 days

200000

Expenses

Monthly Rent 4000 ((Total rent of four

month 16000/4))

Drugs Used 65000

Hospital pays $45,000 for

salaries for work done in May

45000

Accounting Profit/Loss 86000

Cash

Account

Cash inflow

10

Health Services Resource Management

ing

Patients pay $250,000 for

services received in April.

250000

Cash outflow

Hospital pays phone bill for

$1,000 received on April 7.

1000

The hospital pays $160,000 for

drugs received in April.

160000

Hospital pays $45,000 for

salaries for work done in May

45000

Cash Profit/Loss 44000

June

Accrual

Account

ing

Revenues

Patients receive $55,000 in

services and pay for them on the

same day

55000

Expenses

Monthly Rent 4000 ((Total rent of four

month 16000/4))

Drugs Used 60000

Pays $50,000 cash for drugs 50000

11

ing

Patients pay $250,000 for

services received in April.

250000

Cash outflow

Hospital pays phone bill for

$1,000 received on April 7.

1000

The hospital pays $160,000 for

drugs received in April.

160000

Hospital pays $45,000 for

salaries for work done in May

45000

Cash Profit/Loss 44000

June

Accrual

Account

ing

Revenues

Patients receive $55,000 in

services and pay for them on the

same day

55000

Expenses

Monthly Rent 4000 ((Total rent of four

month 16000/4))

Drugs Used 60000

Pays $50,000 cash for drugs 50000

11

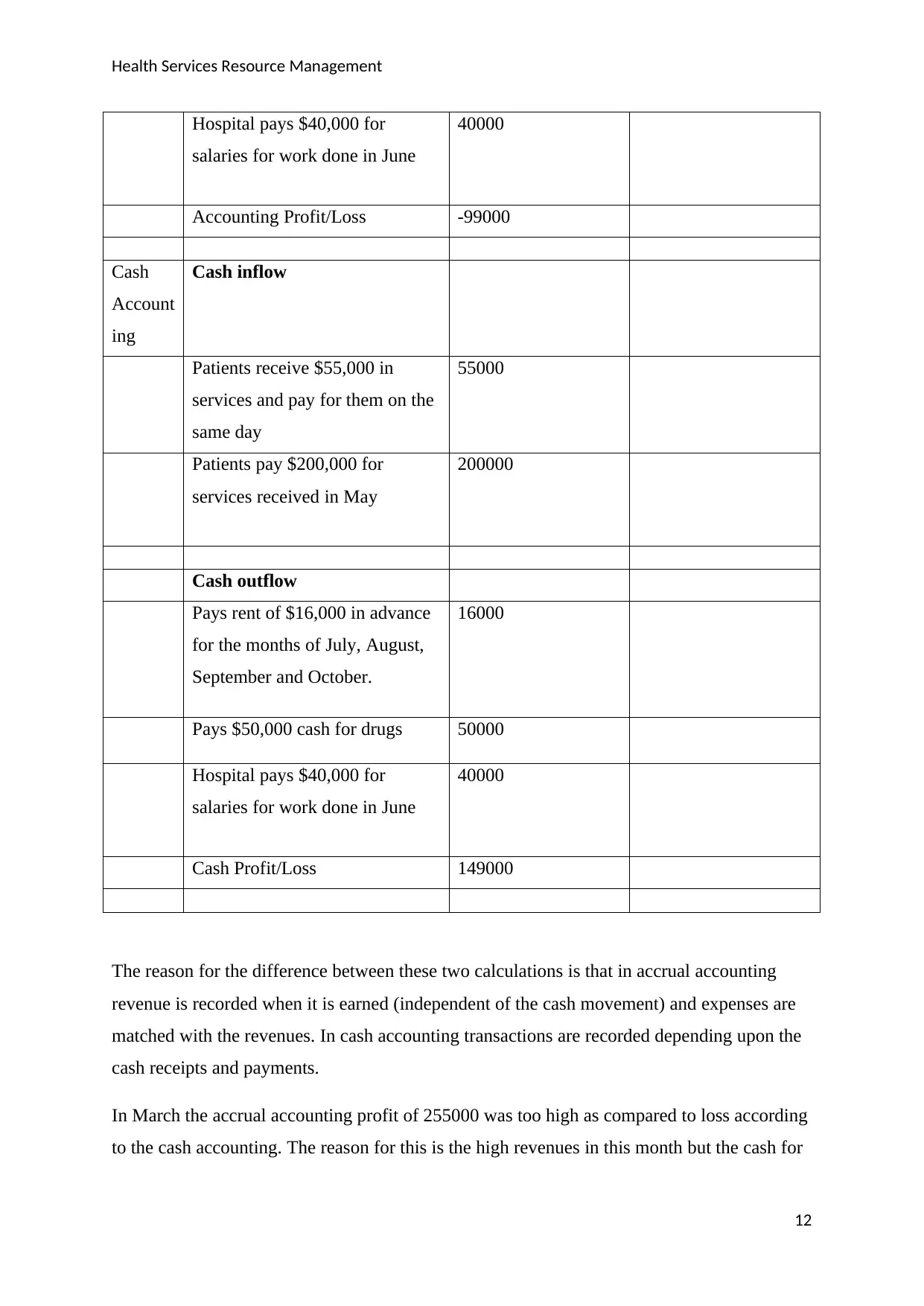

Health Services Resource Management

Hospital pays $40,000 for

salaries for work done in June

40000

Accounting Profit/Loss -99000

Cash

Account

ing

Cash inflow

Patients receive $55,000 in

services and pay for them on the

same day

55000

Patients pay $200,000 for

services received in May

200000

Cash outflow

Pays rent of $16,000 in advance

for the months of July, August,

September and October.

16000

Pays $50,000 cash for drugs 50000

Hospital pays $40,000 for

salaries for work done in June

40000

Cash Profit/Loss 149000

The reason for the difference between these two calculations is that in accrual accounting

revenue is recorded when it is earned (independent of the cash movement) and expenses are

matched with the revenues. In cash accounting transactions are recorded depending upon the

cash receipts and payments.

In March the accrual accounting profit of 255000 was too high as compared to loss according

to the cash accounting. The reason for this is the high revenues in this month but the cash for

12

Hospital pays $40,000 for

salaries for work done in June

40000

Accounting Profit/Loss -99000

Cash

Account

ing

Cash inflow

Patients receive $55,000 in

services and pay for them on the

same day

55000

Patients pay $200,000 for

services received in May

200000

Cash outflow

Pays rent of $16,000 in advance

for the months of July, August,

September and October.

16000

Pays $50,000 cash for drugs 50000

Hospital pays $40,000 for

salaries for work done in June

40000

Cash Profit/Loss 149000

The reason for the difference between these two calculations is that in accrual accounting

revenue is recorded when it is earned (independent of the cash movement) and expenses are

matched with the revenues. In cash accounting transactions are recorded depending upon the

cash receipts and payments.

In March the accrual accounting profit of 255000 was too high as compared to loss according

to the cash accounting. The reason for this is the high revenues in this month but the cash for

12

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.