FIN 5545 Project: Currency Futures to Hedge Exchange Rate Risk

VerifiedAdded on 2023/05/30

|9

|1314

|89

Project

AI Summary

This project analyzes the application of currency futures to hedge exchange rate risk. The student takes a short position in Euro FX futures to mitigate the risk of fluctuating EUR/USD exchange rates. The project includes calculations of contract size, a three-column spreadsheet of EUR/USD and future prices, daily and cumulative returns, margin requirements, and unhedged/hedged values. It plots the hedged and unhedged values, calculates standard deviations, and evaluates the effectiveness of the hedging strategy. The student also discusses the use of Eurodollar futures as a currency derivative and explores other derivative options for investment, concluding that buying a put option on the Euro/US Dollar Futures would minimize risk. The solution demonstrates the process of managing currency risk for a company receiving Euros and converting them to USD.

Running head: FINANCE

Finance

Name of the Student:

Name of the University:

Authors Note:

Finance

Name of the Student:

Name of the University:

Authors Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCE

1

Table of Contents

1. Explaining the position that needs to be taken for hedging the exchange risk:.....................2

2. Indicating the contract size and number of contracts will be used for hedging the payment:

....................................................................................................................................................2

3. Providing three column spread sheet:....................................................................................2

4. Calculating daily and cumulative returns of future position:.................................................3

5. Providing calculation of margin:............................................................................................3

6. Calculating Unhedged and hedged value of the future contract:...........................................4

7. Plotting hedged and unhedged value, while calculating their standard deviation:................5

8. Indicating whether the strategy hold grounds and lowed the exchange rate risk:.................5

9. Indicating whether Eurodollar can be used as currency derivative, while stating when

companies would use Eurodollar:..............................................................................................6

10. Indicating the derivative options that can be used for investment:......................................6

Reference and Bibliography:......................................................................................................7

1

Table of Contents

1. Explaining the position that needs to be taken for hedging the exchange risk:.....................2

2. Indicating the contract size and number of contracts will be used for hedging the payment:

....................................................................................................................................................2

3. Providing three column spread sheet:....................................................................................2

4. Calculating daily and cumulative returns of future position:.................................................3

5. Providing calculation of margin:............................................................................................3

6. Calculating Unhedged and hedged value of the future contract:...........................................4

7. Plotting hedged and unhedged value, while calculating their standard deviation:................5

8. Indicating whether the strategy hold grounds and lowed the exchange rate risk:.................5

9. Indicating whether Eurodollar can be used as currency derivative, while stating when

companies would use Eurodollar:..............................................................................................6

10. Indicating the derivative options that can be used for investment:......................................6

Reference and Bibliography:......................................................................................................7

FINANCE

2

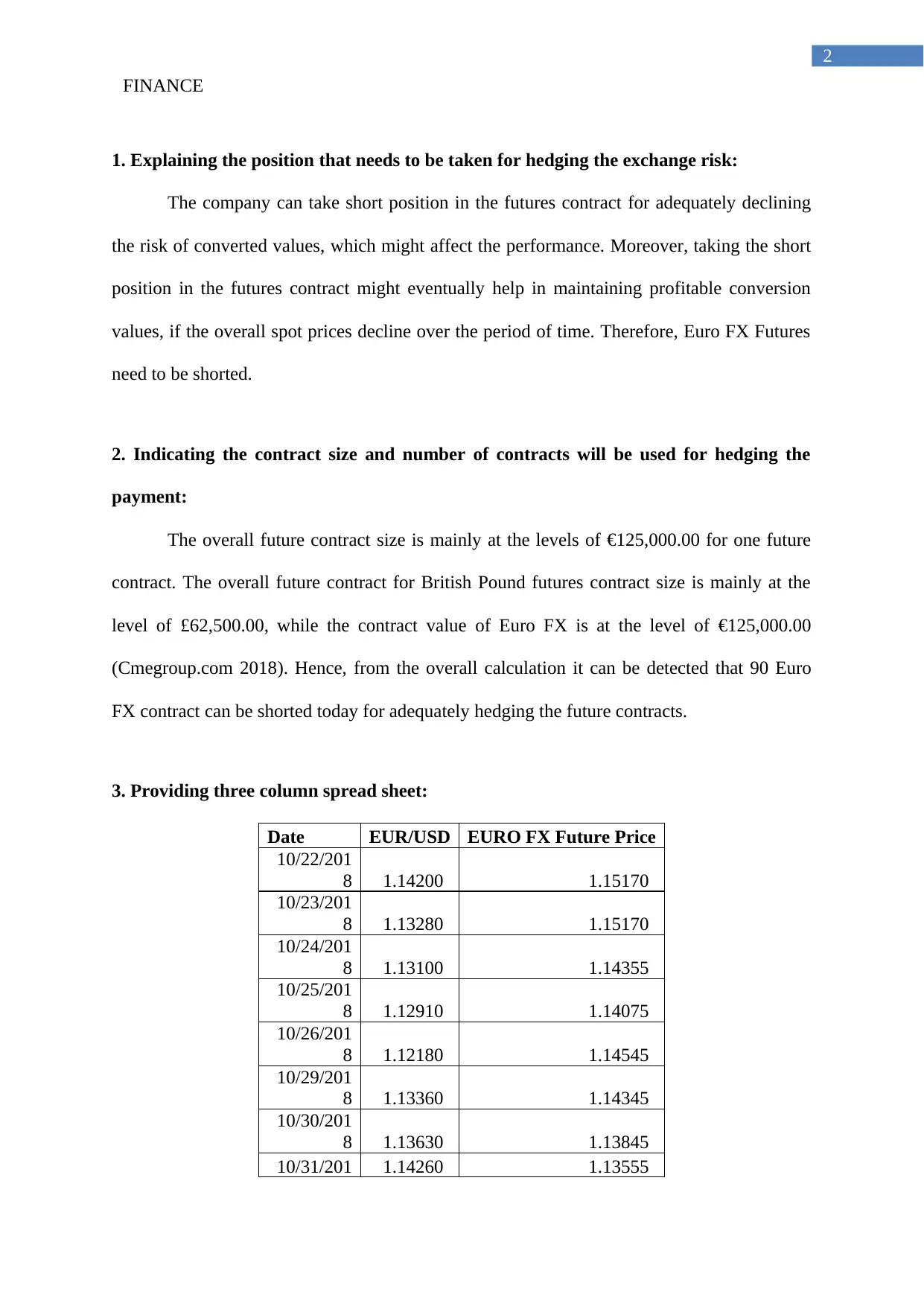

1. Explaining the position that needs to be taken for hedging the exchange risk:

The company can take short position in the futures contract for adequately declining

the risk of converted values, which might affect the performance. Moreover, taking the short

position in the futures contract might eventually help in maintaining profitable conversion

values, if the overall spot prices decline over the period of time. Therefore, Euro FX Futures

need to be shorted.

2. Indicating the contract size and number of contracts will be used for hedging the

payment:

The overall future contract size is mainly at the levels of €125,000.00 for one future

contract. The overall future contract for British Pound futures contract size is mainly at the

level of £62,500.00, while the contract value of Euro FX is at the level of €125,000.00

(Cmegroup.com 2018). Hence, from the overall calculation it can be detected that 90 Euro

FX contract can be shorted today for adequately hedging the future contracts.

3. Providing three column spread sheet:

Date EUR/USD EURO FX Future Price

10/22/201

8 1.14200 1.15170

10/23/201

8 1.13280 1.15170

10/24/201

8 1.13100 1.14355

10/25/201

8 1.12910 1.14075

10/26/201

8 1.12180 1.14545

10/29/201

8 1.13360 1.14345

10/30/201

8 1.13630 1.13845

10/31/201 1.14260 1.13555

2

1. Explaining the position that needs to be taken for hedging the exchange risk:

The company can take short position in the futures contract for adequately declining

the risk of converted values, which might affect the performance. Moreover, taking the short

position in the futures contract might eventually help in maintaining profitable conversion

values, if the overall spot prices decline over the period of time. Therefore, Euro FX Futures

need to be shorted.

2. Indicating the contract size and number of contracts will be used for hedging the

payment:

The overall future contract size is mainly at the levels of €125,000.00 for one future

contract. The overall future contract for British Pound futures contract size is mainly at the

level of £62,500.00, while the contract value of Euro FX is at the level of €125,000.00

(Cmegroup.com 2018). Hence, from the overall calculation it can be detected that 90 Euro

FX contract can be shorted today for adequately hedging the future contracts.

3. Providing three column spread sheet:

Date EUR/USD EURO FX Future Price

10/22/201

8 1.14200 1.15170

10/23/201

8 1.13280 1.15170

10/24/201

8 1.13100 1.14355

10/25/201

8 1.12910 1.14075

10/26/201

8 1.12180 1.14545

10/29/201

8 1.13360 1.14345

10/30/201

8 1.13630 1.13845

10/31/201 1.14260 1.13555

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

FINANCE

3

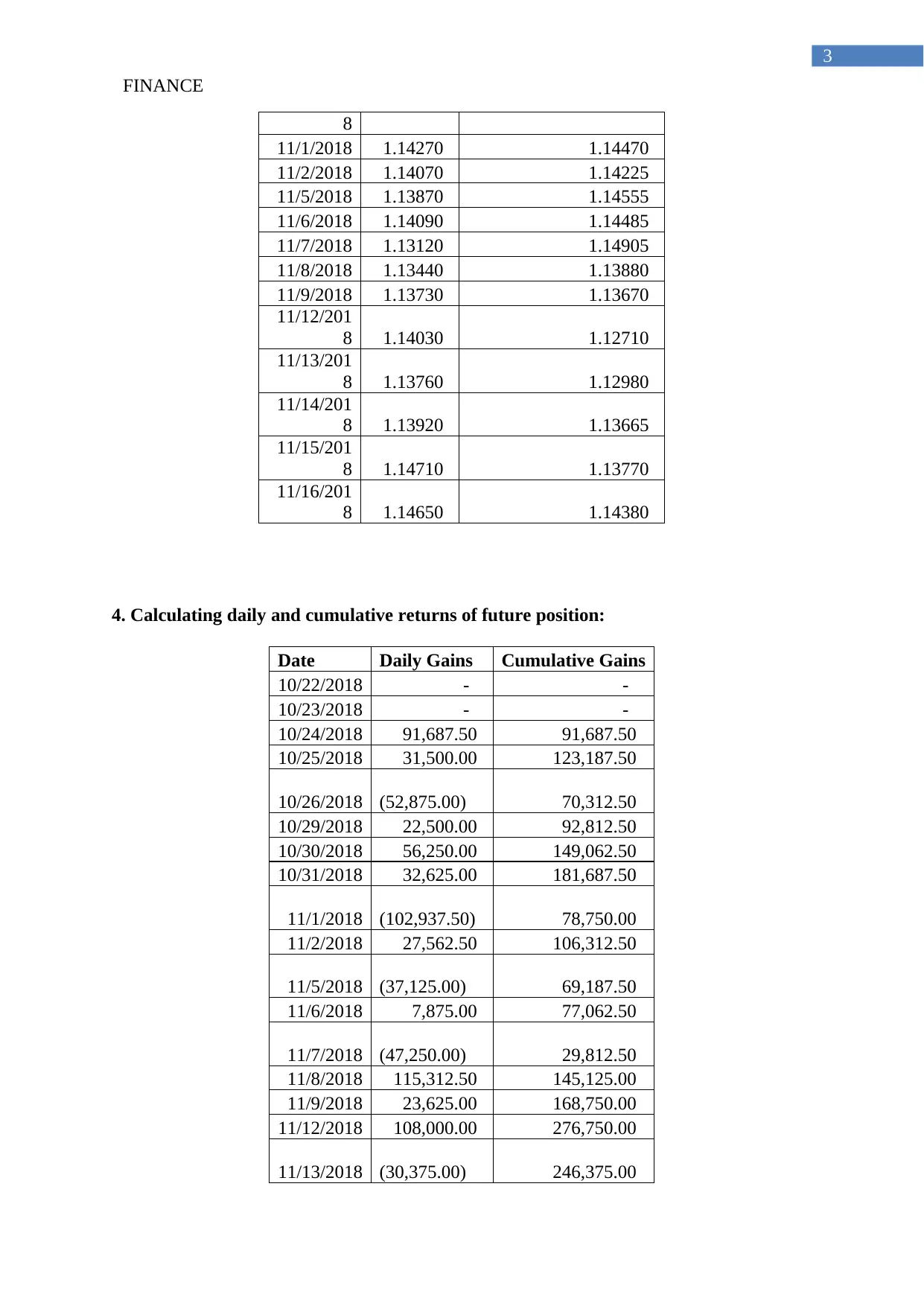

8

11/1/2018 1.14270 1.14470

11/2/2018 1.14070 1.14225

11/5/2018 1.13870 1.14555

11/6/2018 1.14090 1.14485

11/7/2018 1.13120 1.14905

11/8/2018 1.13440 1.13880

11/9/2018 1.13730 1.13670

11/12/201

8 1.14030 1.12710

11/13/201

8 1.13760 1.12980

11/14/201

8 1.13920 1.13665

11/15/201

8 1.14710 1.13770

11/16/201

8 1.14650 1.14380

4. Calculating daily and cumulative returns of future position:

Date Daily Gains Cumulative Gains

10/22/2018 - -

10/23/2018 - -

10/24/2018 91,687.50 91,687.50

10/25/2018 31,500.00 123,187.50

10/26/2018 (52,875.00) 70,312.50

10/29/2018 22,500.00 92,812.50

10/30/2018 56,250.00 149,062.50

10/31/2018 32,625.00 181,687.50

11/1/2018 (102,937.50) 78,750.00

11/2/2018 27,562.50 106,312.50

11/5/2018 (37,125.00) 69,187.50

11/6/2018 7,875.00 77,062.50

11/7/2018 (47,250.00) 29,812.50

11/8/2018 115,312.50 145,125.00

11/9/2018 23,625.00 168,750.00

11/12/2018 108,000.00 276,750.00

11/13/2018 (30,375.00) 246,375.00

3

8

11/1/2018 1.14270 1.14470

11/2/2018 1.14070 1.14225

11/5/2018 1.13870 1.14555

11/6/2018 1.14090 1.14485

11/7/2018 1.13120 1.14905

11/8/2018 1.13440 1.13880

11/9/2018 1.13730 1.13670

11/12/201

8 1.14030 1.12710

11/13/201

8 1.13760 1.12980

11/14/201

8 1.13920 1.13665

11/15/201

8 1.14710 1.13770

11/16/201

8 1.14650 1.14380

4. Calculating daily and cumulative returns of future position:

Date Daily Gains Cumulative Gains

10/22/2018 - -

10/23/2018 - -

10/24/2018 91,687.50 91,687.50

10/25/2018 31,500.00 123,187.50

10/26/2018 (52,875.00) 70,312.50

10/29/2018 22,500.00 92,812.50

10/30/2018 56,250.00 149,062.50

10/31/2018 32,625.00 181,687.50

11/1/2018 (102,937.50) 78,750.00

11/2/2018 27,562.50 106,312.50

11/5/2018 (37,125.00) 69,187.50

11/6/2018 7,875.00 77,062.50

11/7/2018 (47,250.00) 29,812.50

11/8/2018 115,312.50 145,125.00

11/9/2018 23,625.00 168,750.00

11/12/2018 108,000.00 276,750.00

11/13/2018 (30,375.00) 246,375.00

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCE

4

11/14/2018 (77,062.50) 169,312.50

11/15/2018 (11,812.50) 157,500.00

11/16/2018 (68,625.00) 88,875.00

5. Providing calculation of margin:

Date Margin Account Balance

10/22/201

8 720,000.00

10/23/201

8 720,000.00

10/24/201

8 811,687.50

10/25/201

8 843,187.50

10/26/201

8 790,312.50

10/29/201

8 812,812.50

10/30/201

8 869,062.50

10/31/201

8 901,687.50

11/1/2018 798,750.00

11/2/2018 826,312.50

11/5/2018 789,187.50

11/6/2018 797,062.50

11/7/2018 749,812.50

11/8/2018 865,125.00

11/9/2018 888,750.00

11/12/201

8 996,750.00

11/13/201

8 966,375.00

11/14/201

8 889,312.50

11/15/201

8 877,500.00

11/16/201

8 808,875.00

4

11/14/2018 (77,062.50) 169,312.50

11/15/2018 (11,812.50) 157,500.00

11/16/2018 (68,625.00) 88,875.00

5. Providing calculation of margin:

Date Margin Account Balance

10/22/201

8 720,000.00

10/23/201

8 720,000.00

10/24/201

8 811,687.50

10/25/201

8 843,187.50

10/26/201

8 790,312.50

10/29/201

8 812,812.50

10/30/201

8 869,062.50

10/31/201

8 901,687.50

11/1/2018 798,750.00

11/2/2018 826,312.50

11/5/2018 789,187.50

11/6/2018 797,062.50

11/7/2018 749,812.50

11/8/2018 865,125.00

11/9/2018 888,750.00

11/12/201

8 996,750.00

11/13/201

8 966,375.00

11/14/201

8 889,312.50

11/15/201

8 877,500.00

11/16/201

8 808,875.00

FINANCE

5

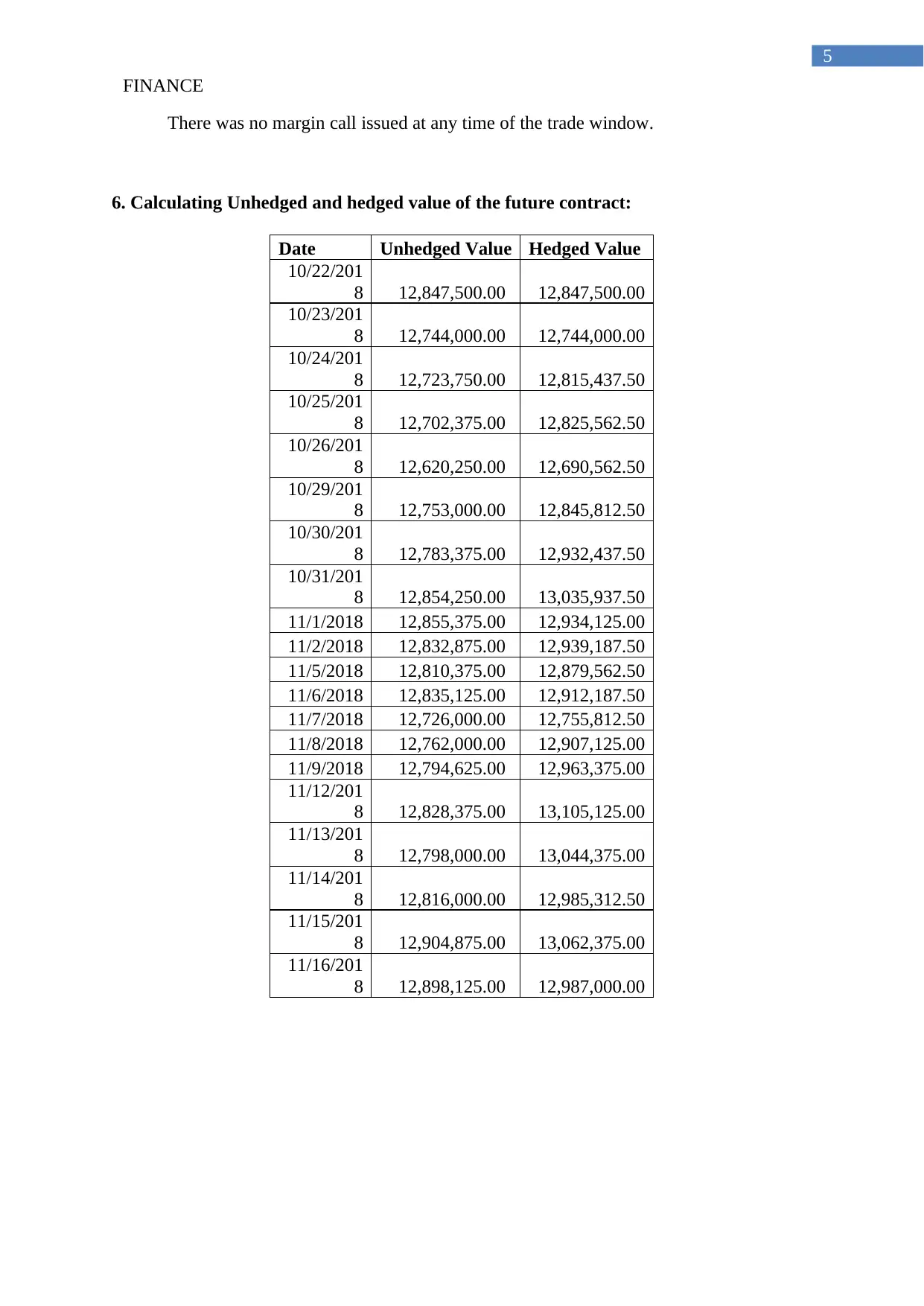

There was no margin call issued at any time of the trade window.

6. Calculating Unhedged and hedged value of the future contract:

Date Unhedged Value Hedged Value

10/22/201

8 12,847,500.00 12,847,500.00

10/23/201

8 12,744,000.00 12,744,000.00

10/24/201

8 12,723,750.00 12,815,437.50

10/25/201

8 12,702,375.00 12,825,562.50

10/26/201

8 12,620,250.00 12,690,562.50

10/29/201

8 12,753,000.00 12,845,812.50

10/30/201

8 12,783,375.00 12,932,437.50

10/31/201

8 12,854,250.00 13,035,937.50

11/1/2018 12,855,375.00 12,934,125.00

11/2/2018 12,832,875.00 12,939,187.50

11/5/2018 12,810,375.00 12,879,562.50

11/6/2018 12,835,125.00 12,912,187.50

11/7/2018 12,726,000.00 12,755,812.50

11/8/2018 12,762,000.00 12,907,125.00

11/9/2018 12,794,625.00 12,963,375.00

11/12/201

8 12,828,375.00 13,105,125.00

11/13/201

8 12,798,000.00 13,044,375.00

11/14/201

8 12,816,000.00 12,985,312.50

11/15/201

8 12,904,875.00 13,062,375.00

11/16/201

8 12,898,125.00 12,987,000.00

5

There was no margin call issued at any time of the trade window.

6. Calculating Unhedged and hedged value of the future contract:

Date Unhedged Value Hedged Value

10/22/201

8 12,847,500.00 12,847,500.00

10/23/201

8 12,744,000.00 12,744,000.00

10/24/201

8 12,723,750.00 12,815,437.50

10/25/201

8 12,702,375.00 12,825,562.50

10/26/201

8 12,620,250.00 12,690,562.50

10/29/201

8 12,753,000.00 12,845,812.50

10/30/201

8 12,783,375.00 12,932,437.50

10/31/201

8 12,854,250.00 13,035,937.50

11/1/2018 12,855,375.00 12,934,125.00

11/2/2018 12,832,875.00 12,939,187.50

11/5/2018 12,810,375.00 12,879,562.50

11/6/2018 12,835,125.00 12,912,187.50

11/7/2018 12,726,000.00 12,755,812.50

11/8/2018 12,762,000.00 12,907,125.00

11/9/2018 12,794,625.00 12,963,375.00

11/12/201

8 12,828,375.00 13,105,125.00

11/13/201

8 12,798,000.00 13,044,375.00

11/14/201

8 12,816,000.00 12,985,312.50

11/15/201

8 12,904,875.00 13,062,375.00

11/16/201

8 12,898,125.00 12,987,000.00

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

FINANCE

6

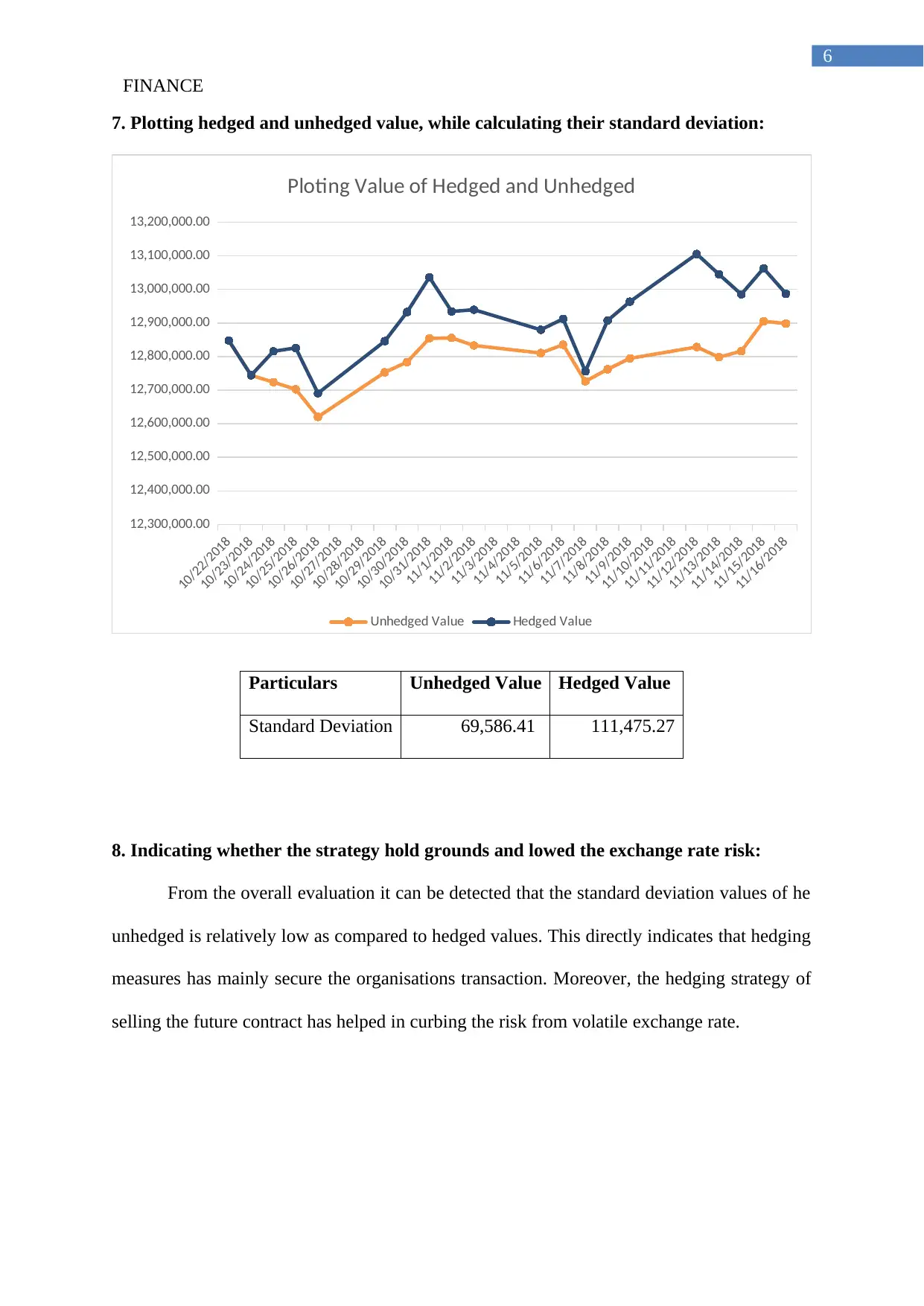

7. Plotting hedged and unhedged value, while calculating their standard deviation:

10/22/2018

10/23/2018

10/24/2018

10/25/2018

10/26/2018

10/27/2018

10/28/2018

10/29/2018

10/30/2018

10/31/2018

11/1/2018

11/2/2018

11/3/2018

11/4/2018

11/5/2018

11/6/2018

11/7/2018

11/8/2018

11/9/2018

11/10/2018

11/11/2018

11/12/2018

11/13/2018

11/14/2018

11/15/2018

11/16/2018

12,300,000.00

12,400,000.00

12,500,000.00

12,600,000.00

12,700,000.00

12,800,000.00

12,900,000.00

13,000,000.00

13,100,000.00

13,200,000.00

Ploting Value of Hedged and Unhedged

Unhedged Value Hedged Value

Particulars Unhedged Value Hedged Value

Standard Deviation 69,586.41 111,475.27

8. Indicating whether the strategy hold grounds and lowed the exchange rate risk:

From the overall evaluation it can be detected that the standard deviation values of he

unhedged is relatively low as compared to hedged values. This directly indicates that hedging

measures has mainly secure the organisations transaction. Moreover, the hedging strategy of

selling the future contract has helped in curbing the risk from volatile exchange rate.

6

7. Plotting hedged and unhedged value, while calculating their standard deviation:

10/22/2018

10/23/2018

10/24/2018

10/25/2018

10/26/2018

10/27/2018

10/28/2018

10/29/2018

10/30/2018

10/31/2018

11/1/2018

11/2/2018

11/3/2018

11/4/2018

11/5/2018

11/6/2018

11/7/2018

11/8/2018

11/9/2018

11/10/2018

11/11/2018

11/12/2018

11/13/2018

11/14/2018

11/15/2018

11/16/2018

12,300,000.00

12,400,000.00

12,500,000.00

12,600,000.00

12,700,000.00

12,800,000.00

12,900,000.00

13,000,000.00

13,100,000.00

13,200,000.00

Ploting Value of Hedged and Unhedged

Unhedged Value Hedged Value

Particulars Unhedged Value Hedged Value

Standard Deviation 69,586.41 111,475.27

8. Indicating whether the strategy hold grounds and lowed the exchange rate risk:

From the overall evaluation it can be detected that the standard deviation values of he

unhedged is relatively low as compared to hedged values. This directly indicates that hedging

measures has mainly secure the organisations transaction. Moreover, the hedging strategy of

selling the future contract has helped in curbing the risk from volatile exchange rate.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCE

7

9. Indicating whether Eurodollar can be used as currency derivative, while stating when

companies would use Eurodollar:

Yes, Euro Dollar Futures is also a currency derivates, which are used by companies to

curbing the losses during the currency conversion. For example, if a US company selling

goods to Europe gets payments in EUR, which will have exchange rate risk. Hence,

Eurodollar can be used for curing the losses incurred from currency transaction and minimise

the conversion value.

10. Indicating the derivative options that can be used for investment:

The use of Options on Euro/US Dollar Futures can be conducted, which might

eventually help minimise the risk from declining values and maximise the profit levels. The

option contract relatively allows the organisation to exercise the contract on their will, which

is not possible in futures contract. Hence, buying put option will eventually allow the

organisation to minimise the risk when the values of the EUR/USD declines. However, when

the values of the EUR /USD increase then the company can opt out of the option contract by

paying only the premiums and generating high returns from the rising values (Mensi,

Hammoudeh and Yoon 2015).

7

9. Indicating whether Eurodollar can be used as currency derivative, while stating when

companies would use Eurodollar:

Yes, Euro Dollar Futures is also a currency derivates, which are used by companies to

curbing the losses during the currency conversion. For example, if a US company selling

goods to Europe gets payments in EUR, which will have exchange rate risk. Hence,

Eurodollar can be used for curing the losses incurred from currency transaction and minimise

the conversion value.

10. Indicating the derivative options that can be used for investment:

The use of Options on Euro/US Dollar Futures can be conducted, which might

eventually help minimise the risk from declining values and maximise the profit levels. The

option contract relatively allows the organisation to exercise the contract on their will, which

is not possible in futures contract. Hence, buying put option will eventually allow the

organisation to minimise the risk when the values of the EUR/USD declines. However, when

the values of the EUR /USD increase then the company can opt out of the option contract by

paying only the premiums and generating high returns from the rising values (Mensi,

Hammoudeh and Yoon 2015).

FINANCE

8

Reference and Bibliography:

Cmegroup.com. 2018. British Pound Futures GBP/USD Quotes - CME Group. [online]

Available at: https://www.cmegroup.com/trading/fx/g10/british-pound.html [Accessed 2 Dec.

2018].

Cmegroup.com. 2018. Euro FX Futures EUR/USD Quotes - CME Group. [online] Available

at: https://www.cmegroup.com/trading/fx/g10/euro-fx_quotes_globex.html [Accessed 2 Dec.

2018].

Finance.yahoo.com. 2018. Yahoo is now part of Oath. [online] Available at:

https://finance.yahoo.com/quote/EURUSD=X/ [Accessed 2 Dec. 2018].

Mensi, W., Hammoudeh, S. and Yoon, S.M., 2015. Structural breaks, dynamic correlations,

asymmetric volatility transmission, and hedging strategies for petroleum prices and USD

exchange rate. Energy Economics, 48, pp.46-60.

8

Reference and Bibliography:

Cmegroup.com. 2018. British Pound Futures GBP/USD Quotes - CME Group. [online]

Available at: https://www.cmegroup.com/trading/fx/g10/british-pound.html [Accessed 2 Dec.

2018].

Cmegroup.com. 2018. Euro FX Futures EUR/USD Quotes - CME Group. [online] Available

at: https://www.cmegroup.com/trading/fx/g10/euro-fx_quotes_globex.html [Accessed 2 Dec.

2018].

Finance.yahoo.com. 2018. Yahoo is now part of Oath. [online] Available at:

https://finance.yahoo.com/quote/EURUSD=X/ [Accessed 2 Dec. 2018].

Mensi, W., Hammoudeh, S. and Yoon, S.M., 2015. Structural breaks, dynamic correlations,

asymmetric volatility transmission, and hedging strategies for petroleum prices and USD

exchange rate. Energy Economics, 48, pp.46-60.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.